Audit Expectation Gap and Threats to Audit Independence in Australia

VerifiedAdded on 2022/10/12

|10

|1815

|99

AI Summary

This article discusses the audit expectation gap and threats to audit independence in Australia, with a focus on the audit engagement of Bletchington Limited. It covers the definition of audit expectation gap, unrealistic expectations of financial statement users, and the responsibilities of auditors. It also discusses the potential threats to audit independence and the safeguards to overcome them.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Running head: AUDITING AND ASSURANCE IN AUSTRALIA

Auditing and Assurance in Australia

Name of the Student

Name of the University

Author’s Note

Auditing and Assurance in Australia

Name of the Student

Name of the University

Author’s Note

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

1AUDITING AND ASSURANCE IN AUSTRALIA

MEMO

To: William Albanese

From: The Audit Manager

Date: 31th August, 2019

Subject: Audit Expectation Gap and Threats to Audit Independence

The main objective behind writing this memo is to provide the required information on two

crucial aspects of audit engagement for the audit of Bletchington Limited (Bletchington).

Audit Expectation Gap – Audit Expectation Gap is considered as a crucial aspect in the audit

engagement process and it can be defined as the difference between what the users of the

financial reports and public consider auditors are responsible for and what the auditors

themselves believe their responsibility (Ruhnke & Schmidt, 2014). It can be seen from the case

of Bletchington that it is one of the largest clients of SBF. It is a large manufacturing company

that involves in business with the countries having demographically elected government. All

these factors indicates towards the fact that Bletchington has certain special users of their

financial reports; they are governments of the trading countries, owners and investors, suppliers,

lenders, employees and management (Litjens, van Buuren & Vergoossen, 2015). Now, it is

mentioned earlier that the occurrence of audit expectation gap can be seen when there is a

difference between the expectations of the users of the financial statement and the assurance

providers that are the auditors. The presence of audit expectation gap will indicate that there is

any alignment between the financial statement users’ belief and the performance of the auditors

(Okafor & Otalor, 2013). The same aspect can take place in the audit engagement of

Bletchington because of the fact that the users of the financial statements of the company may

MEMO

To: William Albanese

From: The Audit Manager

Date: 31th August, 2019

Subject: Audit Expectation Gap and Threats to Audit Independence

The main objective behind writing this memo is to provide the required information on two

crucial aspects of audit engagement for the audit of Bletchington Limited (Bletchington).

Audit Expectation Gap – Audit Expectation Gap is considered as a crucial aspect in the audit

engagement process and it can be defined as the difference between what the users of the

financial reports and public consider auditors are responsible for and what the auditors

themselves believe their responsibility (Ruhnke & Schmidt, 2014). It can be seen from the case

of Bletchington that it is one of the largest clients of SBF. It is a large manufacturing company

that involves in business with the countries having demographically elected government. All

these factors indicates towards the fact that Bletchington has certain special users of their

financial reports; they are governments of the trading countries, owners and investors, suppliers,

lenders, employees and management (Litjens, van Buuren & Vergoossen, 2015). Now, it is

mentioned earlier that the occurrence of audit expectation gap can be seen when there is a

difference between the expectations of the users of the financial statement and the assurance

providers that are the auditors. The presence of audit expectation gap will indicate that there is

any alignment between the financial statement users’ belief and the performance of the auditors

(Okafor & Otalor, 2013). The same aspect can take place in the audit engagement of

Bletchington because of the fact that the users of the financial statements of the company may

2AUDITING AND ASSURANCE IN AUSTRALIA

want more that what the auditor provide. The users of the financial statements of Bletchington

can be impractical in their views and thus, the audit engagement partner may have to face

unrealistic expectations. Some of them are mentioned below:

The auditors of Bletchington provide complete assurance.

The auditors guarantee the future feasibility of Bletchington.

The auditors will provide the unqualified audit opinion which implies that all the

accounts of Bletchington are completely correct.

The auditors will definitely find the frauds and errors in case there is any in

Bletchington’s financial statements.

Every transaction of Bletchington has been checked by the auditors (Litjens, van Buuren

& Vergoossen, 2015).

However, in reality, the auditors do not fulfill the above-mentioned expectations of the users of

the financial statements because the auditors are responsible for the following:

The auditors are responsible for providing reasonable assurance only.

The auditors do not provide the guarantee for the future viability of the entities.

The auditors only provide an unqualified audit opinion when they believe that there are

not any material misstatements in the entity’s financial statements.

The auditors do not guarantee on the fact that there is not existence of any fraud, but it’s

their responsibility to undertake reasonable steps to expose any fraud.

It is the responsibility of the auditors to test only a sample of the financial transactions of

the entities (Kamau, 2013).

want more that what the auditor provide. The users of the financial statements of Bletchington

can be impractical in their views and thus, the audit engagement partner may have to face

unrealistic expectations. Some of them are mentioned below:

The auditors of Bletchington provide complete assurance.

The auditors guarantee the future feasibility of Bletchington.

The auditors will provide the unqualified audit opinion which implies that all the

accounts of Bletchington are completely correct.

The auditors will definitely find the frauds and errors in case there is any in

Bletchington’s financial statements.

Every transaction of Bletchington has been checked by the auditors (Litjens, van Buuren

& Vergoossen, 2015).

However, in reality, the auditors do not fulfill the above-mentioned expectations of the users of

the financial statements because the auditors are responsible for the following:

The auditors are responsible for providing reasonable assurance only.

The auditors do not provide the guarantee for the future viability of the entities.

The auditors only provide an unqualified audit opinion when they believe that there are

not any material misstatements in the entity’s financial statements.

The auditors do not guarantee on the fact that there is not existence of any fraud, but it’s

their responsibility to undertake reasonable steps to expose any fraud.

It is the responsibility of the auditors to test only a sample of the financial transactions of

the entities (Kamau, 2013).

3AUDITING AND ASSURANCE IN AUSTRALIA

Threat to Independence and Safeguards – It can be seen from the provided information of

Bletchington that there are certain situations that can lead to the development of audit

independence threat. These are discussed below with the potential safeguards:

Issue Explanation Safeguard Measures

Self-Interest Threat According to APES 110, Paragraph

100.12 (a), the occurrence of self-

interest threat can be seen when any

financial or other interest creates

inappropriate influence on the

judgment or behavior of the auditors

(apesb.org.au, 2019). As per APES

110, Paragraph 200.4, there can be

the occurrence of self-interest threat

when the audit firm has undue

dependence on the total fees of the

client. In case of SBF, Bletchington

is one of its largest clients by fee

revenue and it indicates towards the

undue dependency of SBF on

Bletchington in terms of total fees.

This can lead to self-interest threat.

In addition, the same paragraph also

states that there can be the

The main safeguard to overcome

this issue is external review by a

legally authorized third party of

the audit reports, returns,

information or communication

produced by the auditor so that

he/she can identify compromise of

audit objectivity or the presence of

bias in these reports (Dart &

Chandler, 2013).

Threat to Independence and Safeguards – It can be seen from the provided information of

Bletchington that there are certain situations that can lead to the development of audit

independence threat. These are discussed below with the potential safeguards:

Issue Explanation Safeguard Measures

Self-Interest Threat According to APES 110, Paragraph

100.12 (a), the occurrence of self-

interest threat can be seen when any

financial or other interest creates

inappropriate influence on the

judgment or behavior of the auditors

(apesb.org.au, 2019). As per APES

110, Paragraph 200.4, there can be

the occurrence of self-interest threat

when the audit firm has undue

dependence on the total fees of the

client. In case of SBF, Bletchington

is one of its largest clients by fee

revenue and it indicates towards the

undue dependency of SBF on

Bletchington in terms of total fees.

This can lead to self-interest threat.

In addition, the same paragraph also

states that there can be the

The main safeguard to overcome

this issue is external review by a

legally authorized third party of

the audit reports, returns,

information or communication

produced by the auditor so that

he/she can identify compromise of

audit objectivity or the presence of

bias in these reports (Dart &

Chandler, 2013).

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

4AUDITING AND ASSURANCE IN AUSTRALIA

occurrence of self-interest threat of

audit independence when an audit

firm is largely concerned regarding

the possibility to lose a significant

client. The potential of the presence

of this aspect can be seen in case of

SBF since Bletchington is one of the

largest clients of them in terms of

fees revenue and it is not unusual for

them to be concerned about the

possibility of losing them. This can

compromise the audit objectivity of

SBF.

Self-Review Threat As per APES 110, Paragraph 100.12

(b), there can be occurrence of self-

review threat of audit independence

when an auditor will not correctly

evaluate previous judgment’s results

made by a member or which the

auditor will rely at the time to form

the audit opinion as a part to provide

the auditing services. According to

APES 110, Paragraph 200.5, an

As a safeguard, it is needed to

ensure the fact that the internal

audit team does not have any

involvement in the

implementation, selection and

training of any of the accounting

system because of the fact that the

internal audit team is responsible

for providing report on the

effectiveness of the implemented

occurrence of self-interest threat of

audit independence when an audit

firm is largely concerned regarding

the possibility to lose a significant

client. The potential of the presence

of this aspect can be seen in case of

SBF since Bletchington is one of the

largest clients of them in terms of

fees revenue and it is not unusual for

them to be concerned about the

possibility of losing them. This can

compromise the audit objectivity of

SBF.

Self-Review Threat As per APES 110, Paragraph 100.12

(b), there can be occurrence of self-

review threat of audit independence

when an auditor will not correctly

evaluate previous judgment’s results

made by a member or which the

auditor will rely at the time to form

the audit opinion as a part to provide

the auditing services. According to

APES 110, Paragraph 200.5, an

As a safeguard, it is needed to

ensure the fact that the internal

audit team does not have any

involvement in the

implementation, selection and

training of any of the accounting

system because of the fact that the

internal audit team is responsible

for providing report on the

effectiveness of the implemented

5AUDITING AND ASSURANCE IN AUSTRALIA

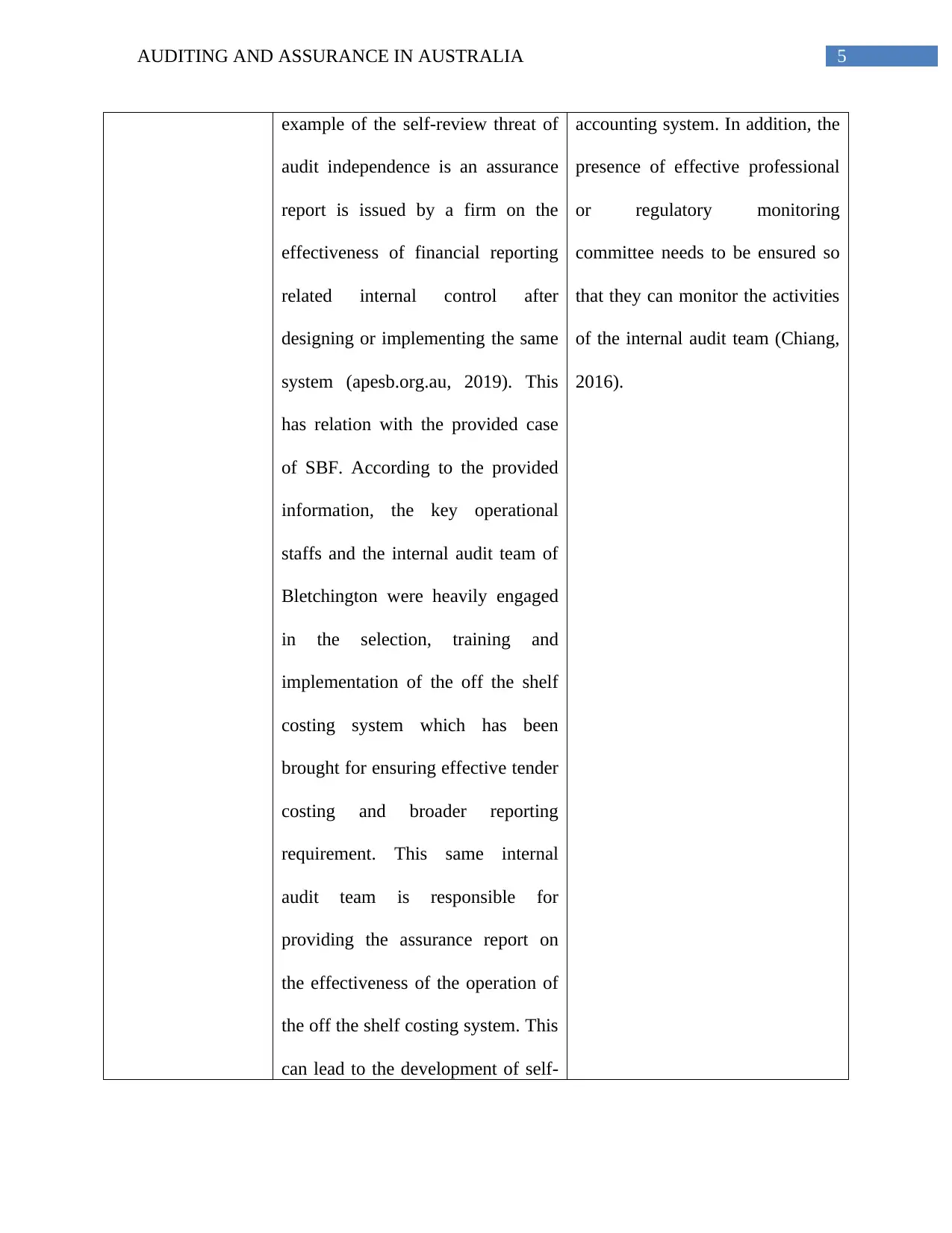

example of the self-review threat of

audit independence is an assurance

report is issued by a firm on the

effectiveness of financial reporting

related internal control after

designing or implementing the same

system (apesb.org.au, 2019). This

has relation with the provided case

of SBF. According to the provided

information, the key operational

staffs and the internal audit team of

Bletchington were heavily engaged

in the selection, training and

implementation of the off the shelf

costing system which has been

brought for ensuring effective tender

costing and broader reporting

requirement. This same internal

audit team is responsible for

providing the assurance report on

the effectiveness of the operation of

the off the shelf costing system. This

can lead to the development of self-

accounting system. In addition, the

presence of effective professional

or regulatory monitoring

committee needs to be ensured so

that they can monitor the activities

of the internal audit team (Chiang,

2016).

example of the self-review threat of

audit independence is an assurance

report is issued by a firm on the

effectiveness of financial reporting

related internal control after

designing or implementing the same

system (apesb.org.au, 2019). This

has relation with the provided case

of SBF. According to the provided

information, the key operational

staffs and the internal audit team of

Bletchington were heavily engaged

in the selection, training and

implementation of the off the shelf

costing system which has been

brought for ensuring effective tender

costing and broader reporting

requirement. This same internal

audit team is responsible for

providing the assurance report on

the effectiveness of the operation of

the off the shelf costing system. This

can lead to the development of self-

accounting system. In addition, the

presence of effective professional

or regulatory monitoring

committee needs to be ensured so

that they can monitor the activities

of the internal audit team (Chiang,

2016).

6AUDITING AND ASSURANCE IN AUSTRALIA

review threat of audit independence

(Abdul Wahab, Zain & Abdul

Rahman, 2015).

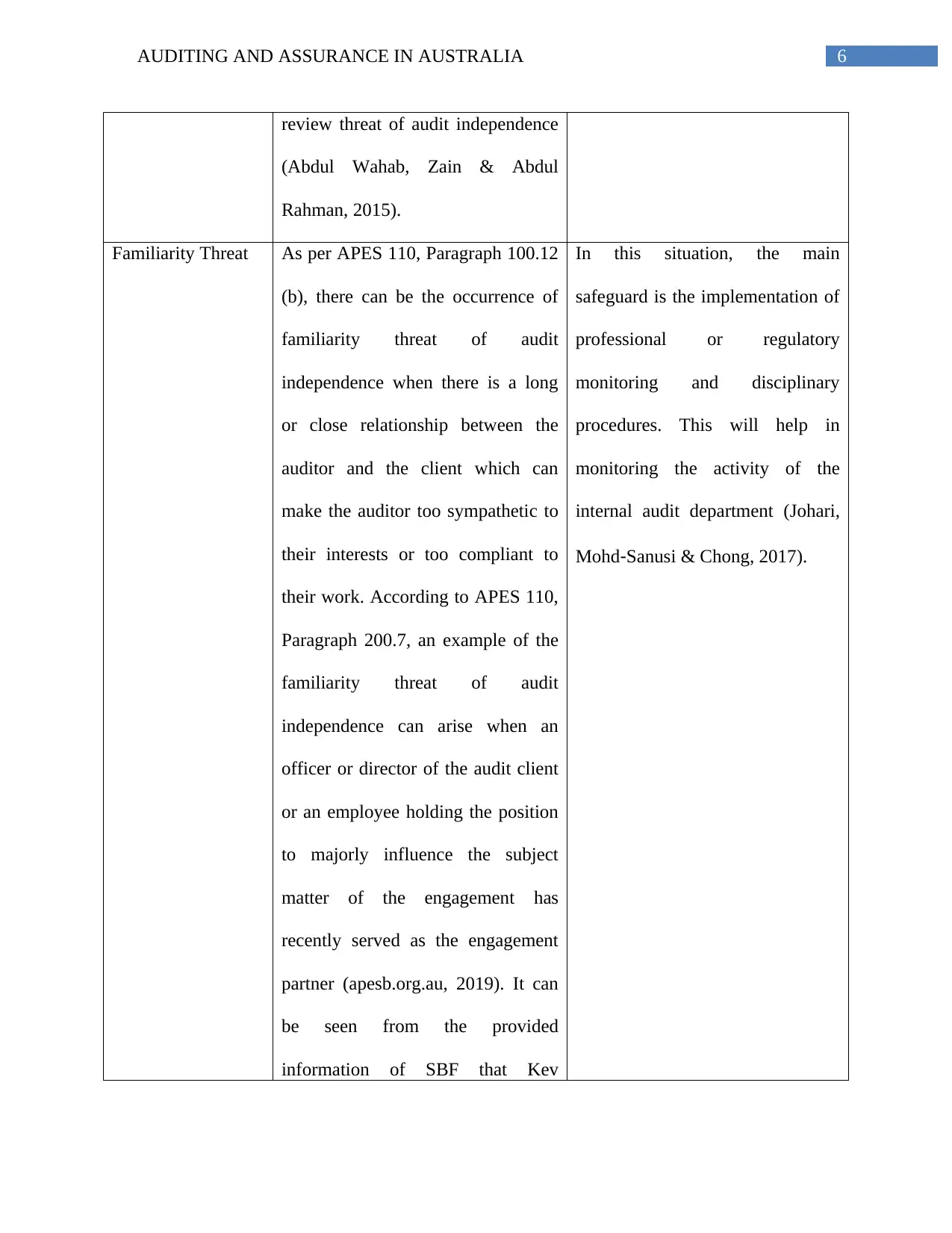

Familiarity Threat As per APES 110, Paragraph 100.12

(b), there can be the occurrence of

familiarity threat of audit

independence when there is a long

or close relationship between the

auditor and the client which can

make the auditor too sympathetic to

their interests or too compliant to

their work. According to APES 110,

Paragraph 200.7, an example of the

familiarity threat of audit

independence can arise when an

officer or director of the audit client

or an employee holding the position

to majorly influence the subject

matter of the engagement has

recently served as the engagement

partner (apesb.org.au, 2019). It can

be seen from the provided

information of SBF that Kev

In this situation, the main

safeguard is the implementation of

professional or regulatory

monitoring and disciplinary

procedures. This will help in

monitoring the activity of the

internal audit department (Johari,

Mohd‐Sanusi & Chong, 2017).

review threat of audit independence

(Abdul Wahab, Zain & Abdul

Rahman, 2015).

Familiarity Threat As per APES 110, Paragraph 100.12

(b), there can be the occurrence of

familiarity threat of audit

independence when there is a long

or close relationship between the

auditor and the client which can

make the auditor too sympathetic to

their interests or too compliant to

their work. According to APES 110,

Paragraph 200.7, an example of the

familiarity threat of audit

independence can arise when an

officer or director of the audit client

or an employee holding the position

to majorly influence the subject

matter of the engagement has

recently served as the engagement

partner (apesb.org.au, 2019). It can

be seen from the provided

information of SBF that Kev

In this situation, the main

safeguard is the implementation of

professional or regulatory

monitoring and disciplinary

procedures. This will help in

monitoring the activity of the

internal audit department (Johari,

Mohd‐Sanusi & Chong, 2017).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7AUDITING AND ASSURANCE IN AUSTRALIA

Kevanna is the head of the internal

audit department of Bletchington

and he was the ex-audit partner of

SBF. This particular aspect can lead

to familiarity threat of audit

independence Kev Kevanna can

provide significant information to

SBF which can influence the audit

engagement (Tepalagul & Lin,

2015).

Kevanna is the head of the internal

audit department of Bletchington

and he was the ex-audit partner of

SBF. This particular aspect can lead

to familiarity threat of audit

independence Kev Kevanna can

provide significant information to

SBF which can influence the audit

engagement (Tepalagul & Lin,

2015).

8AUDITING AND ASSURANCE IN AUSTRALIA

References

Abdul Wahab, E. A., Mat Zain, M., & Abdul Rahman, R. (2015). Political connections: a threat

to auditor independence?. Journal of Accounting in Emerging Economies, 5(2), 222-246.

Apesb.org.au. (2019). APES 110 Code of Ethics for Professional Accountants. Retrieved 31 July

2019, from https://www.apesb.org.au/uploads/standards/apesb_standards/standardc1.pdf

Chiang, C. (2016). Conceptualising the linkage between professional scepticism and auditor

independence. Pacific Accounting Review, 28(2), 180-200.

Dart, E., & Chandler, R. (2013). Client employment of previous auditors: shareholders’ views on

auditor independence. Accounting and Business Research, 43(3), 205-224.

Johari, R. J., Mohd‐Sanusi, Z., & Chong, V. K. (2017). Effects of Auditors' Ethical Orientation

and Self‐Interest Independence Threat on the Mediating Role of Moral Intensity and

Ethical Decision‐Making Process. International Journal of Auditing, 21(1), 38-58.

Kamau, C. G. (2013). Determinants of audit expectation gap: Evidence from limited companies

in Kenya. International Journal of Science and Research (IJSR,) Volume, 2(1).

Litjens, R., van Buuren, J., & Vergoossen, R. (2015). Addressing Information Needs to Reduce

the Audit Expectation Gap: Evidence from D utch Bankers, Audited Companies and

Auditors. International Journal of Auditing, 19(3), 267-281.

Okafor, C. A., & Otalor, J. I. (2013). Narrowing the expectation gap in auditing: the role of the

auditing profession. Research Journal of Finance and Accounting, 4(2), 43-52.

References

Abdul Wahab, E. A., Mat Zain, M., & Abdul Rahman, R. (2015). Political connections: a threat

to auditor independence?. Journal of Accounting in Emerging Economies, 5(2), 222-246.

Apesb.org.au. (2019). APES 110 Code of Ethics for Professional Accountants. Retrieved 31 July

2019, from https://www.apesb.org.au/uploads/standards/apesb_standards/standardc1.pdf

Chiang, C. (2016). Conceptualising the linkage between professional scepticism and auditor

independence. Pacific Accounting Review, 28(2), 180-200.

Dart, E., & Chandler, R. (2013). Client employment of previous auditors: shareholders’ views on

auditor independence. Accounting and Business Research, 43(3), 205-224.

Johari, R. J., Mohd‐Sanusi, Z., & Chong, V. K. (2017). Effects of Auditors' Ethical Orientation

and Self‐Interest Independence Threat on the Mediating Role of Moral Intensity and

Ethical Decision‐Making Process. International Journal of Auditing, 21(1), 38-58.

Kamau, C. G. (2013). Determinants of audit expectation gap: Evidence from limited companies

in Kenya. International Journal of Science and Research (IJSR,) Volume, 2(1).

Litjens, R., van Buuren, J., & Vergoossen, R. (2015). Addressing Information Needs to Reduce

the Audit Expectation Gap: Evidence from D utch Bankers, Audited Companies and

Auditors. International Journal of Auditing, 19(3), 267-281.

Okafor, C. A., & Otalor, J. I. (2013). Narrowing the expectation gap in auditing: the role of the

auditing profession. Research Journal of Finance and Accounting, 4(2), 43-52.

9AUDITING AND ASSURANCE IN AUSTRALIA

Ruhnke, K., & Schmidt, M. (2014). The audit expectation gap: existence, causes, and the impact

of changes. Accounting and Business research, 44(5), 572-601.

Tepalagul, N., & Lin, L. (2015). Auditor independence and audit quality: A literature

review. Journal of Accounting, Auditing & Finance, 30(1), 101-121.

Ruhnke, K., & Schmidt, M. (2014). The audit expectation gap: existence, causes, and the impact

of changes. Accounting and Business research, 44(5), 572-601.

Tepalagul, N., & Lin, L. (2015). Auditor independence and audit quality: A literature

review. Journal of Accounting, Auditing & Finance, 30(1), 101-121.

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.