Audit Case Study: Materiality, Risk, and Executive Pay at Cloud 9

VerifiedAdded on 2023/04/25

|11

|2193

|200

Case Study

AI Summary

This case study provides an analysis of the audit procedures applied to Cloud 9 Pty Ltd, an athletic shoe supplier. It includes a discussion of materiality, focusing on the appropriateness of using total assets as a base due to a significant disposal proceed impacting profit before tax. Analytical procedures, including ratio analysis (profitability, liquidity, efficiency, and leverage), are applied to assess business risks. Specific areas of emphasis for the audit, such as cash, revenues, trade receivables, and inventories, are identified. The report also examines executive remuneration practices in three ASX-listed mining companies (Rio Tinto, Altura Mining, and BHP Billiton), comparing compensation levels and linking remuneration policies with company performance. The analysis concludes that Rio Tinto's executive payments are most closely tied to profit and performance compared to the other two entities. Desklib offers similar solved assignments and past papers for students.

Running head: AUDITING AND ASSURANCE

Auditing and assurance

Name of the student

Name of the university

Student ID

Author note

Auditing and assurance

Name of the student

Name of the university

Student ID

Author note

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1AUDITING AND ASSURANCE

Table of Contents

Case study – Cloud 9 Pty Ltd.....................................................................................................2

Part 1 – Materiality.................................................................................................................2

Part 2 – Analytical procedure.................................................................................................2

(a) Analysing business risks..........................................................................................2

(b) Specific areas to be specially emphasised...............................................................4

Research question.......................................................................................................................5

Introduction............................................................................................................................5

Discussion..............................................................................................................................5

Conclusion..............................................................................................................................8

Reference....................................................................................................................................9

Table of Contents

Case study – Cloud 9 Pty Ltd.....................................................................................................2

Part 1 – Materiality.................................................................................................................2

Part 2 – Analytical procedure.................................................................................................2

(a) Analysing business risks..........................................................................................2

(b) Specific areas to be specially emphasised...............................................................4

Research question.......................................................................................................................5

Introduction............................................................................................................................5

Discussion..............................................................................................................................5

Conclusion..............................................................................................................................8

Reference....................................................................................................................................9

2AUDITING AND ASSURANCE

Case study – Cloud 9 Pty Ltd

Part 1 – Materiality

Preliminary estimate for the materiality at the level of financial report is generally

called as the planning materiality (PM). It is considered as the maximum amount by which it

is believed by the auditors that the financial report can be misstated through unknown or

known fraud or error. Misstatement involved in the financial report is likely to mislead the

decision of the users taken on the basis of the financial reports. Once the materiality level is

established by the auditor in planning stage, they must set the level for performance

materiality that is the level of tolerable misstatement for the client’s financial reports. PM

shall be larger than the tolerable level of materiality (Amiram et al., 2017).

In give case study of Cloud 9 Pty Ltd it is mentioned that the company basically deals

in supplying athletic shoes to various customers including rebel Sports, Myer, David Jones,

and Foot Locker. For carrying out the audit of the entity, Cloud 9 appointed W&S Partners

accounting firm based in Australia. While planning for the audit the auditors were

considering the financial statement for establishing materiality level.

Materiality level are generally based on 1% of total equity, 0.5% of total assets, 2% of

gross profit, 0.5% of total turnover or 5% of profit before tax. Most acceptable criteria for

materiality is taking profit before tax as base. However, this cannot be considered if the profit

is impacted significantly by the amount of any particular transaction or if the company

reported loss for the particular period (Audsabumrungrat, Pornupatham & Tan, 2015). In case

of Cloud 9, it can be identified from its financial report that during the year 2017 it received

significant amount that is 15,76,859 as disposal proceeds that have likely impact on net profit

for the year. Hence, net profit before tax cannot be considered for establishing the materiality

base. In this case, total asset will be better criteria for establishing the materiality level. Total

asset of the company is 32,864,958 and 0.5% of total asset will be 164,324.79. Hence, it will

be considered as the level for materiality (Lakis, & Masiulevičius, 2017).

Part 2 – Analytical procedure

(a) Analysing business risks

Analytical procedures are used for financial audit for assisting the auditors to gain an

insight for the business operations and identifying the potential risk areas those require

Case study – Cloud 9 Pty Ltd

Part 1 – Materiality

Preliminary estimate for the materiality at the level of financial report is generally

called as the planning materiality (PM). It is considered as the maximum amount by which it

is believed by the auditors that the financial report can be misstated through unknown or

known fraud or error. Misstatement involved in the financial report is likely to mislead the

decision of the users taken on the basis of the financial reports. Once the materiality level is

established by the auditor in planning stage, they must set the level for performance

materiality that is the level of tolerable misstatement for the client’s financial reports. PM

shall be larger than the tolerable level of materiality (Amiram et al., 2017).

In give case study of Cloud 9 Pty Ltd it is mentioned that the company basically deals

in supplying athletic shoes to various customers including rebel Sports, Myer, David Jones,

and Foot Locker. For carrying out the audit of the entity, Cloud 9 appointed W&S Partners

accounting firm based in Australia. While planning for the audit the auditors were

considering the financial statement for establishing materiality level.

Materiality level are generally based on 1% of total equity, 0.5% of total assets, 2% of

gross profit, 0.5% of total turnover or 5% of profit before tax. Most acceptable criteria for

materiality is taking profit before tax as base. However, this cannot be considered if the profit

is impacted significantly by the amount of any particular transaction or if the company

reported loss for the particular period (Audsabumrungrat, Pornupatham & Tan, 2015). In case

of Cloud 9, it can be identified from its financial report that during the year 2017 it received

significant amount that is 15,76,859 as disposal proceeds that have likely impact on net profit

for the year. Hence, net profit before tax cannot be considered for establishing the materiality

base. In this case, total asset will be better criteria for establishing the materiality level. Total

asset of the company is 32,864,958 and 0.5% of total asset will be 164,324.79. Hence, it will

be considered as the level for materiality (Lakis, & Masiulevičius, 2017).

Part 2 – Analytical procedure

(a) Analysing business risks

Analytical procedures are used for financial audit for assisting the auditors to gain an

insight for the business operations and identifying the potential risk areas those require

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3AUDITING AND ASSURANCE

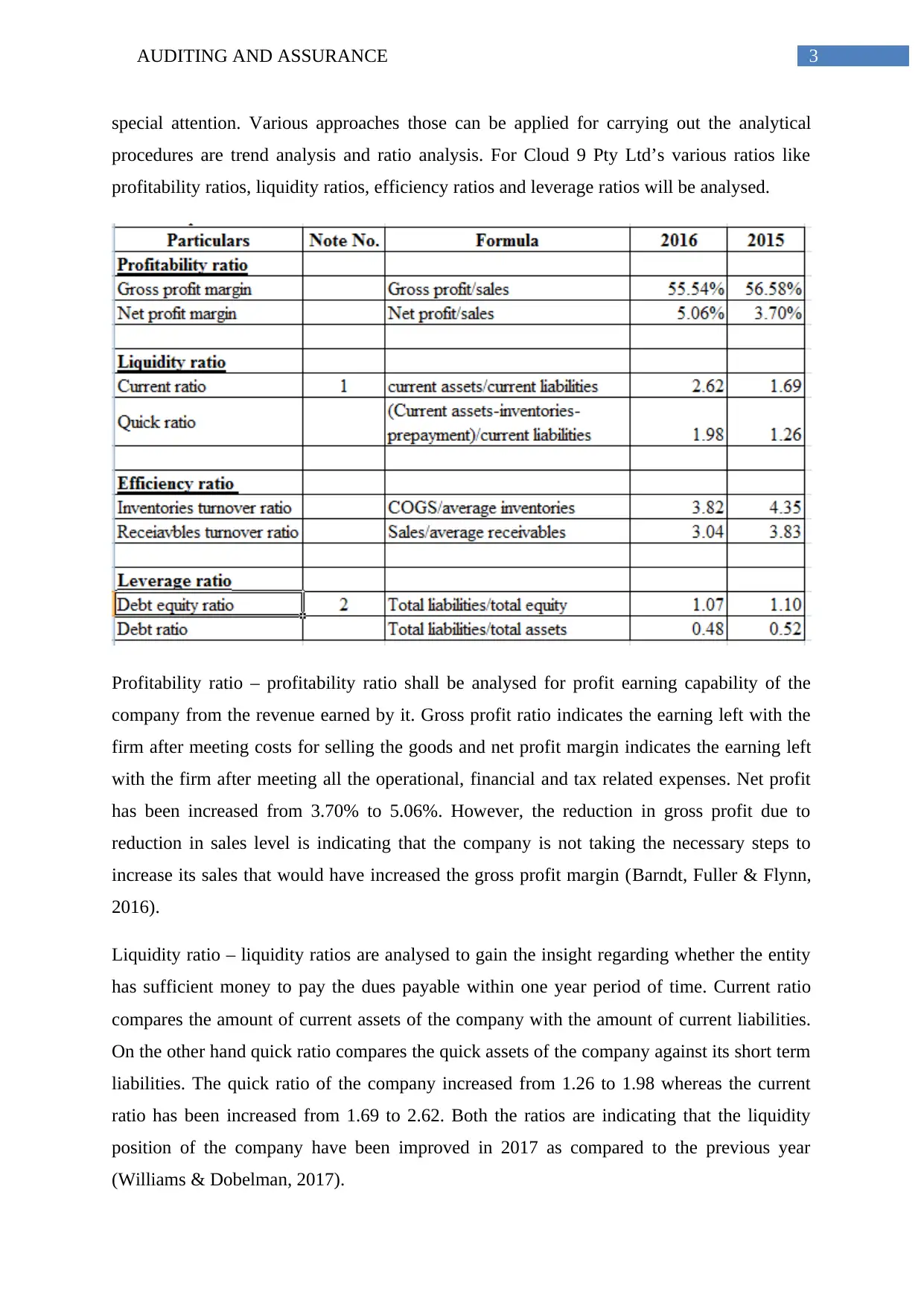

special attention. Various approaches those can be applied for carrying out the analytical

procedures are trend analysis and ratio analysis. For Cloud 9 Pty Ltd’s various ratios like

profitability ratios, liquidity ratios, efficiency ratios and leverage ratios will be analysed.

Profitability ratio – profitability ratio shall be analysed for profit earning capability of the

company from the revenue earned by it. Gross profit ratio indicates the earning left with the

firm after meeting costs for selling the goods and net profit margin indicates the earning left

with the firm after meeting all the operational, financial and tax related expenses. Net profit

has been increased from 3.70% to 5.06%. However, the reduction in gross profit due to

reduction in sales level is indicating that the company is not taking the necessary steps to

increase its sales that would have increased the gross profit margin (Barndt, Fuller & Flynn,

2016).

Liquidity ratio – liquidity ratios are analysed to gain the insight regarding whether the entity

has sufficient money to pay the dues payable within one year period of time. Current ratio

compares the amount of current assets of the company with the amount of current liabilities.

On the other hand quick ratio compares the quick assets of the company against its short term

liabilities. The quick ratio of the company increased from 1.26 to 1.98 whereas the current

ratio has been increased from 1.69 to 2.62. Both the ratios are indicating that the liquidity

position of the company have been improved in 2017 as compared to the previous year

(Williams & Dobelman, 2017).

special attention. Various approaches those can be applied for carrying out the analytical

procedures are trend analysis and ratio analysis. For Cloud 9 Pty Ltd’s various ratios like

profitability ratios, liquidity ratios, efficiency ratios and leverage ratios will be analysed.

Profitability ratio – profitability ratio shall be analysed for profit earning capability of the

company from the revenue earned by it. Gross profit ratio indicates the earning left with the

firm after meeting costs for selling the goods and net profit margin indicates the earning left

with the firm after meeting all the operational, financial and tax related expenses. Net profit

has been increased from 3.70% to 5.06%. However, the reduction in gross profit due to

reduction in sales level is indicating that the company is not taking the necessary steps to

increase its sales that would have increased the gross profit margin (Barndt, Fuller & Flynn,

2016).

Liquidity ratio – liquidity ratios are analysed to gain the insight regarding whether the entity

has sufficient money to pay the dues payable within one year period of time. Current ratio

compares the amount of current assets of the company with the amount of current liabilities.

On the other hand quick ratio compares the quick assets of the company against its short term

liabilities. The quick ratio of the company increased from 1.26 to 1.98 whereas the current

ratio has been increased from 1.69 to 2.62. Both the ratios are indicating that the liquidity

position of the company have been improved in 2017 as compared to the previous year

(Williams & Dobelman, 2017).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4AUDITING AND ASSURANCE

Efficiency ratio – efficiency ratios are analysed to measure the efficiency level of the entity

with which it is replacing its inventories or collecting the dues from debtors. Inventory

turnover ratio that indicates the times the company replaces or sells its inventories within the

specific period under concern. On the other hand, receivables turnover ratio indicates the

times it collects the dues from its debtors. As both ratios have reduced in 2017 as compared

to 2016 it can be stated that the efficiency of the company is reduced (Uechi et al., 2015)

Leverage ratio – it indicates the solvency position of the company though focusing on the

debt component and equity component of the capital structure. Debt to equity ratio of the

company reduced from 1.10 to 1.07 over the years from 2016 to 2017. On the other hand,

debt ratio that indicates the assets of the company financed though debt is reduced from 0.52

to 0.47 over the years from 2016 to 2017. Both the ratios are indicating that the solvency

position of the company has been improved in 2017 (Greco, Figueira & Ehrgott 2016).

(b) Specific areas to be specially emphasised

Looking into the financial report of Cloud 9 Pty Ltd and materiality level projection it

can be stated that the auditor shall pay special attention for revenues, trade receivable,

inventories and cash. Cash shall be paid special attention as being the most liquid asset it is

always susceptible to fraud, error or misstatement. Further, looking into the ratio analysis it

can be stated that the problematic areas are revenues, trade receivables and inventories and

hence these items shall be paid special attention.

Efficiency ratio – efficiency ratios are analysed to measure the efficiency level of the entity

with which it is replacing its inventories or collecting the dues from debtors. Inventory

turnover ratio that indicates the times the company replaces or sells its inventories within the

specific period under concern. On the other hand, receivables turnover ratio indicates the

times it collects the dues from its debtors. As both ratios have reduced in 2017 as compared

to 2016 it can be stated that the efficiency of the company is reduced (Uechi et al., 2015)

Leverage ratio – it indicates the solvency position of the company though focusing on the

debt component and equity component of the capital structure. Debt to equity ratio of the

company reduced from 1.10 to 1.07 over the years from 2016 to 2017. On the other hand,

debt ratio that indicates the assets of the company financed though debt is reduced from 0.52

to 0.47 over the years from 2016 to 2017. Both the ratios are indicating that the solvency

position of the company has been improved in 2017 (Greco, Figueira & Ehrgott 2016).

(b) Specific areas to be specially emphasised

Looking into the financial report of Cloud 9 Pty Ltd and materiality level projection it

can be stated that the auditor shall pay special attention for revenues, trade receivable,

inventories and cash. Cash shall be paid special attention as being the most liquid asset it is

always susceptible to fraud, error or misstatement. Further, looking into the ratio analysis it

can be stated that the problematic areas are revenues, trade receivables and inventories and

hence these items shall be paid special attention.

5AUDITING AND ASSURANCE

Research question

Introduction

The aim of the report is to extract information associated with executive remuneration

for 3 ASX listed companies. The companies those will be analysed are Rio Tinto Plc, Altura

Mining and BHP Billiton. The selected companies belong to Australian mining industry and

are among the leading mining companies of Australia.

Discussion

Payment to the executives –

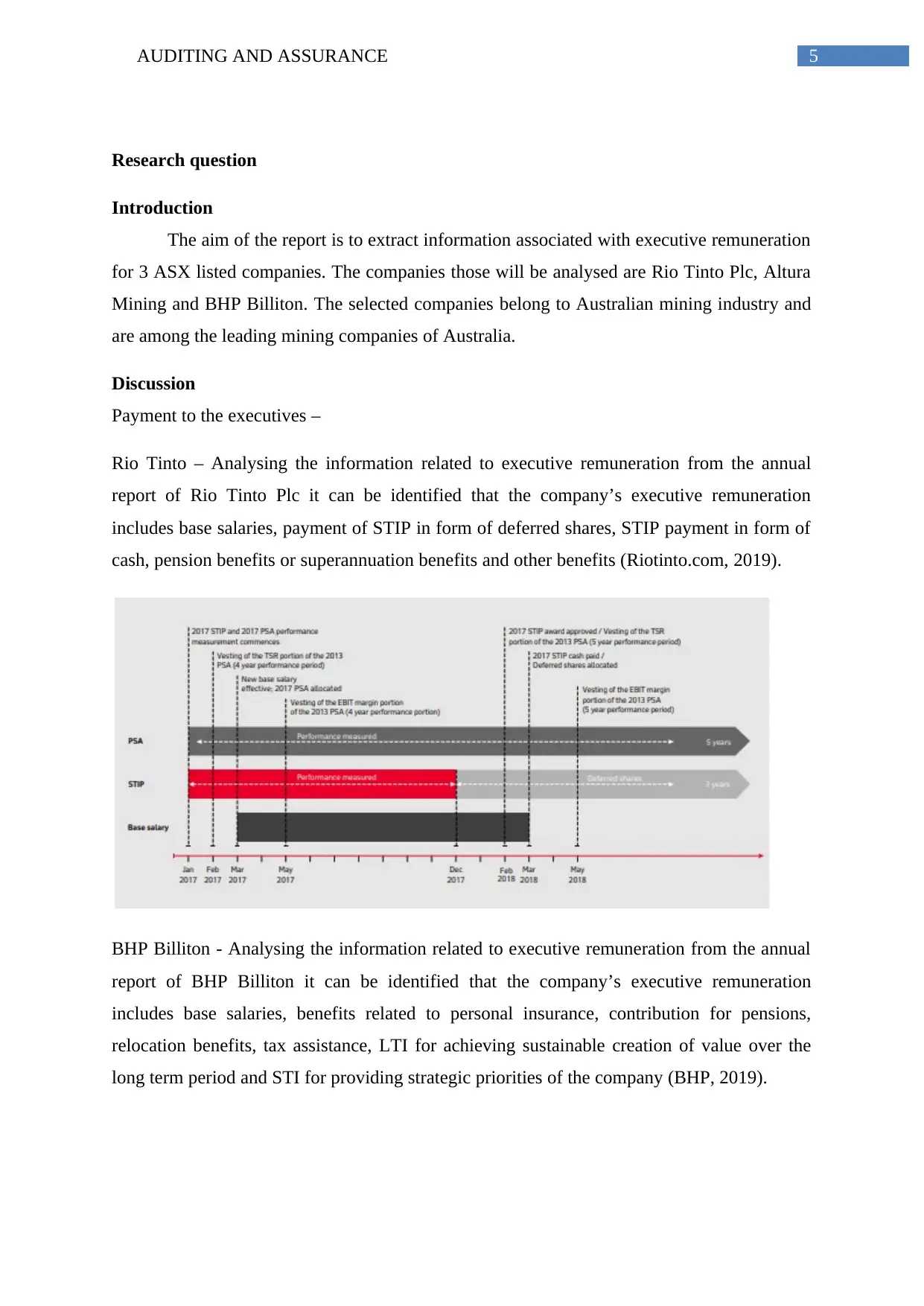

Rio Tinto – Analysing the information related to executive remuneration from the annual

report of Rio Tinto Plc it can be identified that the company’s executive remuneration

includes base salaries, payment of STIP in form of deferred shares, STIP payment in form of

cash, pension benefits or superannuation benefits and other benefits (Riotinto.com, 2019).

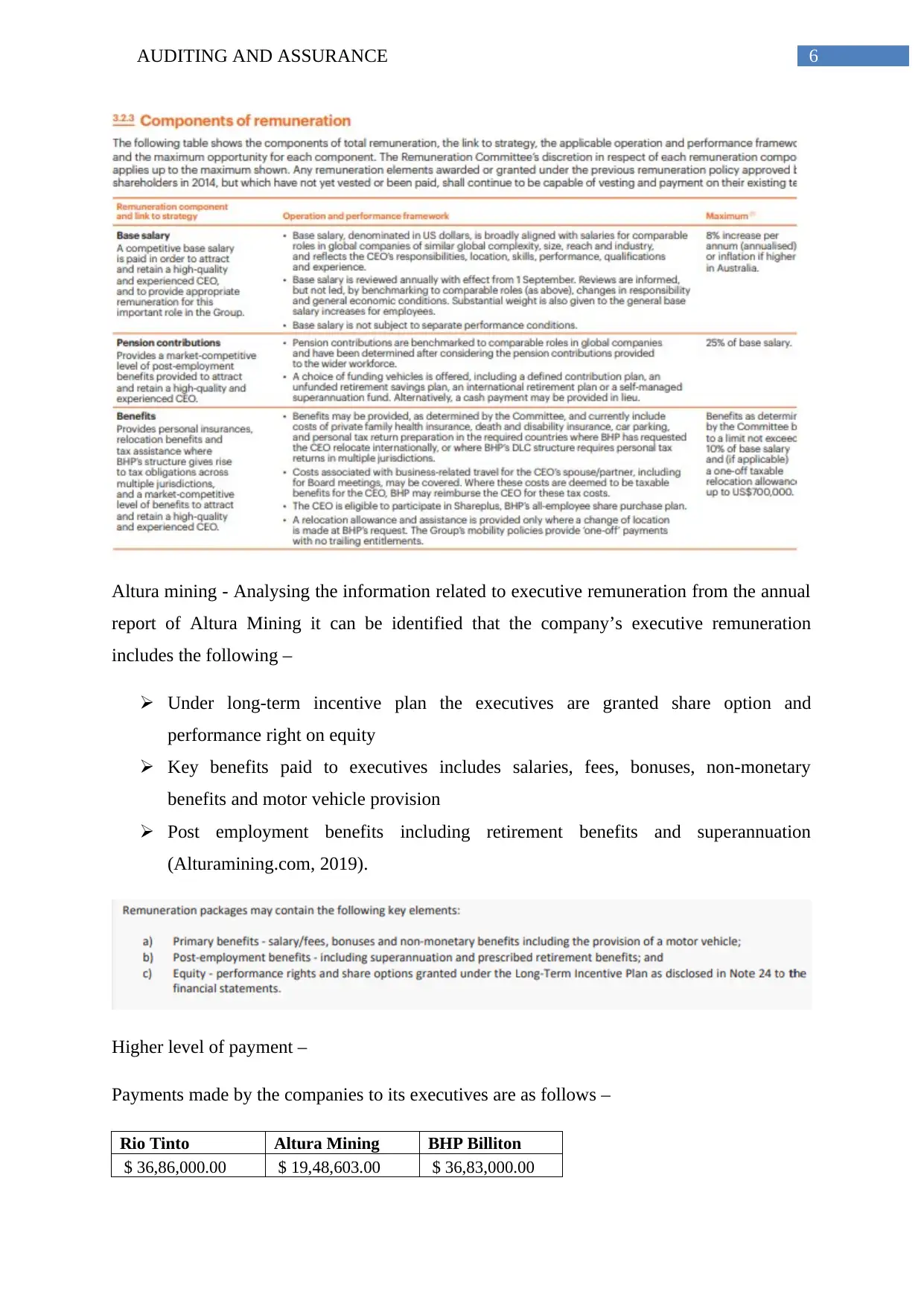

BHP Billiton - Analysing the information related to executive remuneration from the annual

report of BHP Billiton it can be identified that the company’s executive remuneration

includes base salaries, benefits related to personal insurance, contribution for pensions,

relocation benefits, tax assistance, LTI for achieving sustainable creation of value over the

long term period and STI for providing strategic priorities of the company (BHP, 2019).

Research question

Introduction

The aim of the report is to extract information associated with executive remuneration

for 3 ASX listed companies. The companies those will be analysed are Rio Tinto Plc, Altura

Mining and BHP Billiton. The selected companies belong to Australian mining industry and

are among the leading mining companies of Australia.

Discussion

Payment to the executives –

Rio Tinto – Analysing the information related to executive remuneration from the annual

report of Rio Tinto Plc it can be identified that the company’s executive remuneration

includes base salaries, payment of STIP in form of deferred shares, STIP payment in form of

cash, pension benefits or superannuation benefits and other benefits (Riotinto.com, 2019).

BHP Billiton - Analysing the information related to executive remuneration from the annual

report of BHP Billiton it can be identified that the company’s executive remuneration

includes base salaries, benefits related to personal insurance, contribution for pensions,

relocation benefits, tax assistance, LTI for achieving sustainable creation of value over the

long term period and STI for providing strategic priorities of the company (BHP, 2019).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6AUDITING AND ASSURANCE

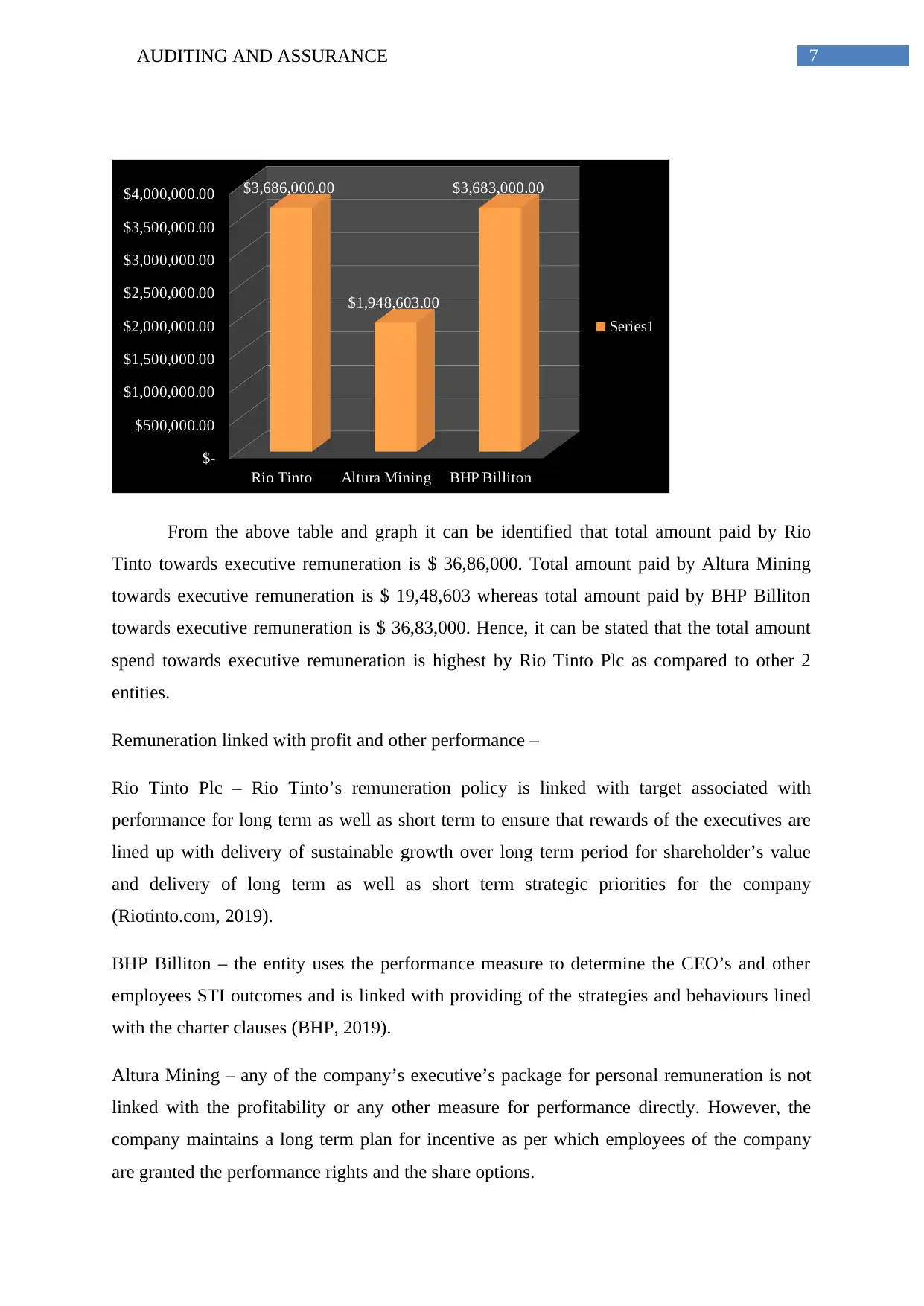

Altura mining - Analysing the information related to executive remuneration from the annual

report of Altura Mining it can be identified that the company’s executive remuneration

includes the following –

Under long-term incentive plan the executives are granted share option and

performance right on equity

Key benefits paid to executives includes salaries, fees, bonuses, non-monetary

benefits and motor vehicle provision

Post employment benefits including retirement benefits and superannuation

(Alturamining.com, 2019).

Higher level of payment –

Payments made by the companies to its executives are as follows –

Rio Tinto Altura Mining BHP Billiton

$ 36,86,000.00 $ 19,48,603.00 $ 36,83,000.00

Altura mining - Analysing the information related to executive remuneration from the annual

report of Altura Mining it can be identified that the company’s executive remuneration

includes the following –

Under long-term incentive plan the executives are granted share option and

performance right on equity

Key benefits paid to executives includes salaries, fees, bonuses, non-monetary

benefits and motor vehicle provision

Post employment benefits including retirement benefits and superannuation

(Alturamining.com, 2019).

Higher level of payment –

Payments made by the companies to its executives are as follows –

Rio Tinto Altura Mining BHP Billiton

$ 36,86,000.00 $ 19,48,603.00 $ 36,83,000.00

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7AUDITING AND ASSURANCE

Rio Tinto Altura Mining BHP Billiton

$-

$500,000.00

$1,000,000.00

$1,500,000.00

$2,000,000.00

$2,500,000.00

$3,000,000.00

$3,500,000.00

$4,000,000.00 $3,686,000.00

$1,948,603.00

$3,683,000.00

Series1

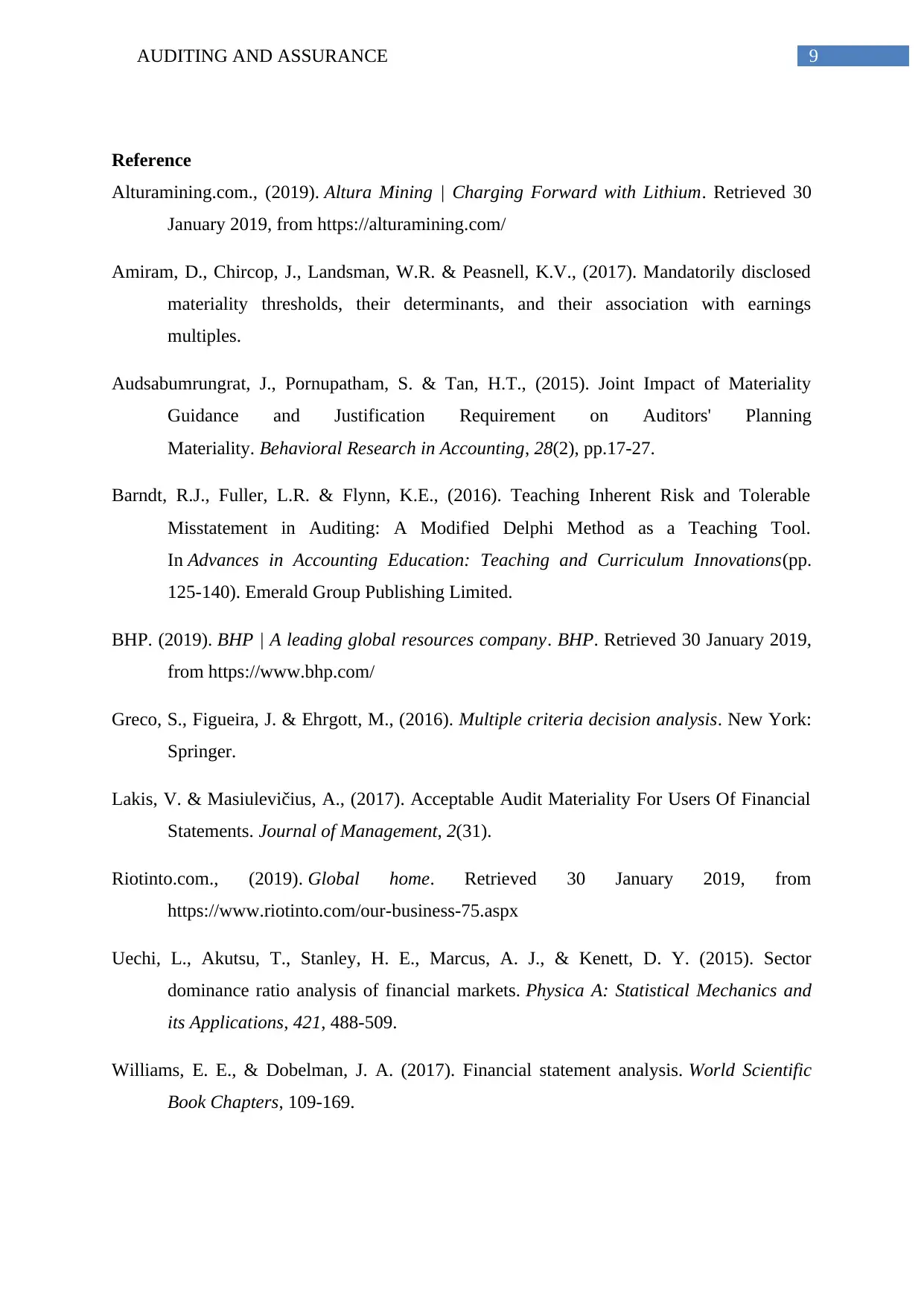

From the above table and graph it can be identified that total amount paid by Rio

Tinto towards executive remuneration is $ 36,86,000. Total amount paid by Altura Mining

towards executive remuneration is $ 19,48,603 whereas total amount paid by BHP Billiton

towards executive remuneration is $ 36,83,000. Hence, it can be stated that the total amount

spend towards executive remuneration is highest by Rio Tinto Plc as compared to other 2

entities.

Remuneration linked with profit and other performance –

Rio Tinto Plc – Rio Tinto’s remuneration policy is linked with target associated with

performance for long term as well as short term to ensure that rewards of the executives are

lined up with delivery of sustainable growth over long term period for shareholder’s value

and delivery of long term as well as short term strategic priorities for the company

(Riotinto.com, 2019).

BHP Billiton – the entity uses the performance measure to determine the CEO’s and other

employees STI outcomes and is linked with providing of the strategies and behaviours lined

with the charter clauses (BHP, 2019).

Altura Mining – any of the company’s executive’s package for personal remuneration is not

linked with the profitability or any other measure for performance directly. However, the

company maintains a long term plan for incentive as per which employees of the company

are granted the performance rights and the share options.

Rio Tinto Altura Mining BHP Billiton

$-

$500,000.00

$1,000,000.00

$1,500,000.00

$2,000,000.00

$2,500,000.00

$3,000,000.00

$3,500,000.00

$4,000,000.00 $3,686,000.00

$1,948,603.00

$3,683,000.00

Series1

From the above table and graph it can be identified that total amount paid by Rio

Tinto towards executive remuneration is $ 36,86,000. Total amount paid by Altura Mining

towards executive remuneration is $ 19,48,603 whereas total amount paid by BHP Billiton

towards executive remuneration is $ 36,83,000. Hence, it can be stated that the total amount

spend towards executive remuneration is highest by Rio Tinto Plc as compared to other 2

entities.

Remuneration linked with profit and other performance –

Rio Tinto Plc – Rio Tinto’s remuneration policy is linked with target associated with

performance for long term as well as short term to ensure that rewards of the executives are

lined up with delivery of sustainable growth over long term period for shareholder’s value

and delivery of long term as well as short term strategic priorities for the company

(Riotinto.com, 2019).

BHP Billiton – the entity uses the performance measure to determine the CEO’s and other

employees STI outcomes and is linked with providing of the strategies and behaviours lined

with the charter clauses (BHP, 2019).

Altura Mining – any of the company’s executive’s package for personal remuneration is not

linked with the profitability or any other measure for performance directly. However, the

company maintains a long term plan for incentive as per which employees of the company

are granted the performance rights and the share options.

8AUDITING AND ASSURANCE

From the above it can be stated that executive payment of Rio Tinto is mostly linked

with profit and other performance as compared to other 2 entities.

Conclusion

Above discussion leads to the conclusion that the executives remuneration paid by the

Australian entities are in form of base salaries, benefits related to personal insurance,

contribution for pensions, relocation benefits, tax assistance, LTI, STI, post employment

benefits and superannuation. However, some of the companies pay the executives based on

the company’s profits and performance measures used for evaluation their performances.

From the above it can be stated that executive payment of Rio Tinto is mostly linked

with profit and other performance as compared to other 2 entities.

Conclusion

Above discussion leads to the conclusion that the executives remuneration paid by the

Australian entities are in form of base salaries, benefits related to personal insurance,

contribution for pensions, relocation benefits, tax assistance, LTI, STI, post employment

benefits and superannuation. However, some of the companies pay the executives based on

the company’s profits and performance measures used for evaluation their performances.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9AUDITING AND ASSURANCE

Reference

Alturamining.com., (2019). Altura Mining | Charging Forward with Lithium. Retrieved 30

January 2019, from https://alturamining.com/

Amiram, D., Chircop, J., Landsman, W.R. & Peasnell, K.V., (2017). Mandatorily disclosed

materiality thresholds, their determinants, and their association with earnings

multiples.

Audsabumrungrat, J., Pornupatham, S. & Tan, H.T., (2015). Joint Impact of Materiality

Guidance and Justification Requirement on Auditors' Planning

Materiality. Behavioral Research in Accounting, 28(2), pp.17-27.

Barndt, R.J., Fuller, L.R. & Flynn, K.E., (2016). Teaching Inherent Risk and Tolerable

Misstatement in Auditing: A Modified Delphi Method as a Teaching Tool.

In Advances in Accounting Education: Teaching and Curriculum Innovations(pp.

125-140). Emerald Group Publishing Limited.

BHP. (2019). BHP | A leading global resources company. BHP. Retrieved 30 January 2019,

from https://www.bhp.com/

Greco, S., Figueira, J. & Ehrgott, M., (2016). Multiple criteria decision analysis. New York:

Springer.

Lakis, V. & Masiulevičius, A., (2017). Acceptable Audit Materiality For Users Of Financial

Statements. Journal of Management, 2(31).

Riotinto.com., (2019). Global home. Retrieved 30 January 2019, from

https://www.riotinto.com/our-business-75.aspx

Uechi, L., Akutsu, T., Stanley, H. E., Marcus, A. J., & Kenett, D. Y. (2015). Sector

dominance ratio analysis of financial markets. Physica A: Statistical Mechanics and

its Applications, 421, 488-509.

Williams, E. E., & Dobelman, J. A. (2017). Financial statement analysis. World Scientific

Book Chapters, 109-169.

Reference

Alturamining.com., (2019). Altura Mining | Charging Forward with Lithium. Retrieved 30

January 2019, from https://alturamining.com/

Amiram, D., Chircop, J., Landsman, W.R. & Peasnell, K.V., (2017). Mandatorily disclosed

materiality thresholds, their determinants, and their association with earnings

multiples.

Audsabumrungrat, J., Pornupatham, S. & Tan, H.T., (2015). Joint Impact of Materiality

Guidance and Justification Requirement on Auditors' Planning

Materiality. Behavioral Research in Accounting, 28(2), pp.17-27.

Barndt, R.J., Fuller, L.R. & Flynn, K.E., (2016). Teaching Inherent Risk and Tolerable

Misstatement in Auditing: A Modified Delphi Method as a Teaching Tool.

In Advances in Accounting Education: Teaching and Curriculum Innovations(pp.

125-140). Emerald Group Publishing Limited.

BHP. (2019). BHP | A leading global resources company. BHP. Retrieved 30 January 2019,

from https://www.bhp.com/

Greco, S., Figueira, J. & Ehrgott, M., (2016). Multiple criteria decision analysis. New York:

Springer.

Lakis, V. & Masiulevičius, A., (2017). Acceptable Audit Materiality For Users Of Financial

Statements. Journal of Management, 2(31).

Riotinto.com., (2019). Global home. Retrieved 30 January 2019, from

https://www.riotinto.com/our-business-75.aspx

Uechi, L., Akutsu, T., Stanley, H. E., Marcus, A. J., & Kenett, D. Y. (2015). Sector

dominance ratio analysis of financial markets. Physica A: Statistical Mechanics and

its Applications, 421, 488-509.

Williams, E. E., & Dobelman, J. A. (2017). Financial statement analysis. World Scientific

Book Chapters, 109-169.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10AUDITING AND ASSURANCE

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.