ACC3AUD - Medibank (MPL) Audit: Business Risks & Operations Analysis

VerifiedAdded on 2023/04/19

|9

|1819

|405

Report

AI Summary

This report provides an analysis of Medibank Private Limited's operations and identifies key business risks that could impact the audit engagement for 2018. It outlines the areas in which Medibank operates, including health insurance and health services, and discusses four primary business risks: mark...

Running head: AUDITING AND ASSURANCE

Auditing and Assurance

Name of the Student:

Name of the University:

Author’s Note:

Course ID:

Auditing and Assurance

Name of the Student:

Name of the University:

Author’s Note:

Course ID:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1AUDITING AND ASSURANCE

Table of Contents

1. Areas in which Medibank conducts its operations:.....................................................................2

4. Four business risks that could have impact on the audit of Medibank:.......................................2

References:......................................................................................................................................7

Table of Contents

1. Areas in which Medibank conducts its operations:.....................................................................2

4. Four business risks that could have impact on the audit of Medibank:.......................................2

References:......................................................................................................................................7

2AUDITING AND ASSURANCE

1. Areas in which Medibank conducts its operations:

Medibank Private Limited is an integrated healthcare organisation involved in providing

health solutions and private health insurance in Australia. The organisation is engaged in

operating in two segments, which mainly include Medibank Health and Health Insurance. It is

the second biggest health insurance provider after Bupa in Australia having 29.1% of market

share and 3.8 million members (Medibank 2018). The segment of Health Insurance provides

private health insurance products constituting of hospital cover providing members with health

cover for hospital treatments. The organisation includes ancillary cover as well that offers its

members with health cover for healthcare services like optical, dental and physiotherapy. The

segment provides health insurance products to the overseas students and overseas patients.

In addition, the segment of Medibank Health provides telehealth and health management

services to the corporate and governmental customers along with distributing life, travel as well

as pet insurance products. The organisation is associated with underwriting its health insurance

products under the brands of AHM and Medibank. The head office of the organisation is situated

at Docklands in Australia and it has been established in 1976. The primary aim of the

organisation is intended to deliver superior health to the customers by providing health services,

advocacy of the health system and overall community work. Thus, Medibank ensures widening

the most effective combination of products, services and advices for its customers.

4. Four business risks that could have impact on the audit of Medibank:

The four business risks, which could affect the audit operations of Medibank, include the

following:

1. Areas in which Medibank conducts its operations:

Medibank Private Limited is an integrated healthcare organisation involved in providing

health solutions and private health insurance in Australia. The organisation is engaged in

operating in two segments, which mainly include Medibank Health and Health Insurance. It is

the second biggest health insurance provider after Bupa in Australia having 29.1% of market

share and 3.8 million members (Medibank 2018). The segment of Health Insurance provides

private health insurance products constituting of hospital cover providing members with health

cover for hospital treatments. The organisation includes ancillary cover as well that offers its

members with health cover for healthcare services like optical, dental and physiotherapy. The

segment provides health insurance products to the overseas students and overseas patients.

In addition, the segment of Medibank Health provides telehealth and health management

services to the corporate and governmental customers along with distributing life, travel as well

as pet insurance products. The organisation is associated with underwriting its health insurance

products under the brands of AHM and Medibank. The head office of the organisation is situated

at Docklands in Australia and it has been established in 1976. The primary aim of the

organisation is intended to deliver superior health to the customers by providing health services,

advocacy of the health system and overall community work. Thus, Medibank ensures widening

the most effective combination of products, services and advices for its customers.

4. Four business risks that could have impact on the audit of Medibank:

The four business risks, which could affect the audit operations of Medibank, include the

following:

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3AUDITING AND ASSURANCE

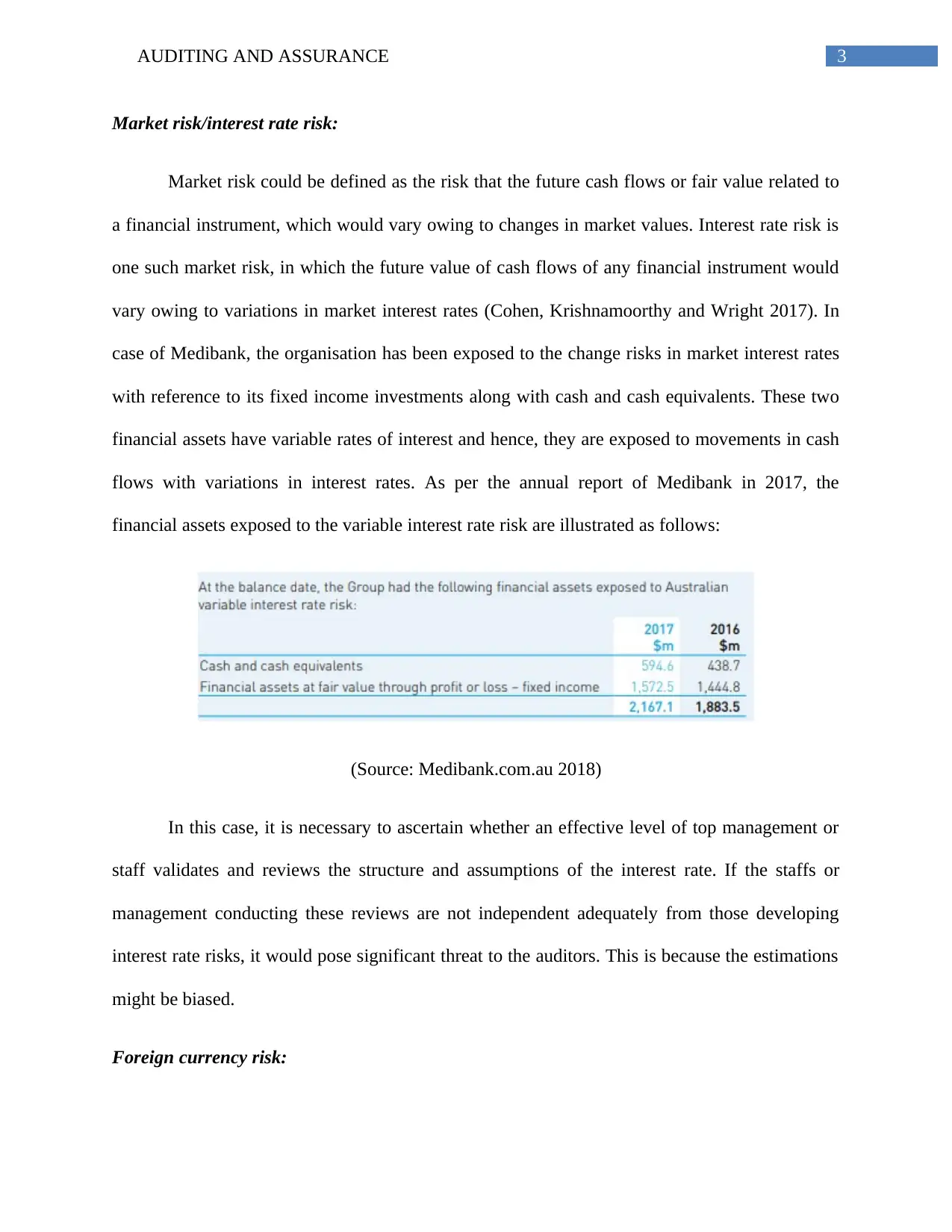

Market risk/interest rate risk:

Market risk could be defined as the risk that the future cash flows or fair value related to

a financial instrument, which would vary owing to changes in market values. Interest rate risk is

one such market risk, in which the future value of cash flows of any financial instrument would

vary owing to variations in market interest rates (Cohen, Krishnamoorthy and Wright 2017). In

case of Medibank, the organisation has been exposed to the change risks in market interest rates

with reference to its fixed income investments along with cash and cash equivalents. These two

financial assets have variable rates of interest and hence, they are exposed to movements in cash

flows with variations in interest rates. As per the annual report of Medibank in 2017, the

financial assets exposed to the variable interest rate risk are illustrated as follows:

(Source: Medibank.com.au 2018)

In this case, it is necessary to ascertain whether an effective level of top management or

staff validates and reviews the structure and assumptions of the interest rate. If the staffs or

management conducting these reviews are not independent adequately from those developing

interest rate risks, it would pose significant threat to the auditors. This is because the estimations

might be biased.

Foreign currency risk:

Market risk/interest rate risk:

Market risk could be defined as the risk that the future cash flows or fair value related to

a financial instrument, which would vary owing to changes in market values. Interest rate risk is

one such market risk, in which the future value of cash flows of any financial instrument would

vary owing to variations in market interest rates (Cohen, Krishnamoorthy and Wright 2017). In

case of Medibank, the organisation has been exposed to the change risks in market interest rates

with reference to its fixed income investments along with cash and cash equivalents. These two

financial assets have variable rates of interest and hence, they are exposed to movements in cash

flows with variations in interest rates. As per the annual report of Medibank in 2017, the

financial assets exposed to the variable interest rate risk are illustrated as follows:

(Source: Medibank.com.au 2018)

In this case, it is necessary to ascertain whether an effective level of top management or

staff validates and reviews the structure and assumptions of the interest rate. If the staffs or

management conducting these reviews are not independent adequately from those developing

interest rate risks, it would pose significant threat to the auditors. This is because the estimations

might be biased.

Foreign currency risk:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4AUDITING AND ASSURANCE

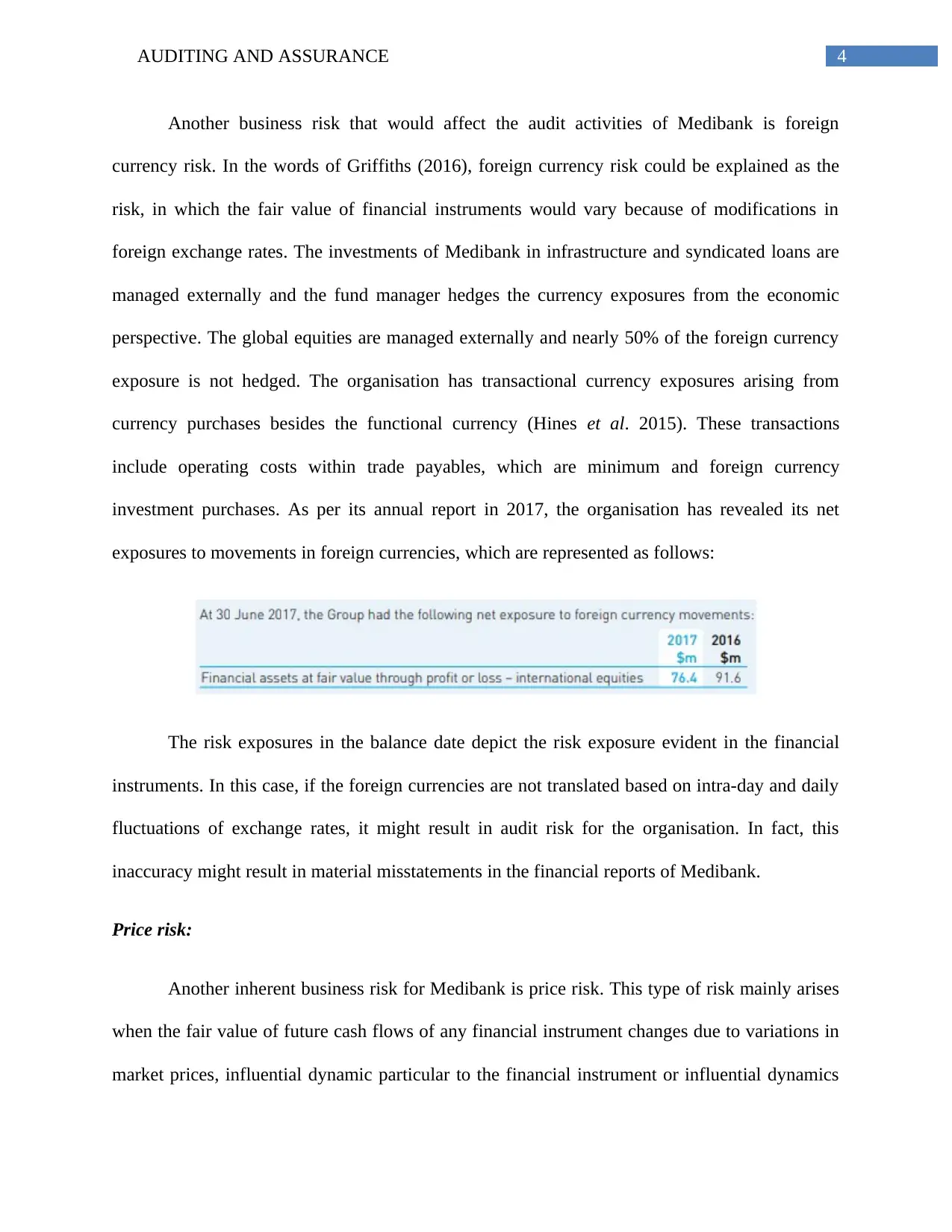

Another business risk that would affect the audit activities of Medibank is foreign

currency risk. In the words of Griffiths (2016), foreign currency risk could be explained as the

risk, in which the fair value of financial instruments would vary because of modifications in

foreign exchange rates. The investments of Medibank in infrastructure and syndicated loans are

managed externally and the fund manager hedges the currency exposures from the economic

perspective. The global equities are managed externally and nearly 50% of the foreign currency

exposure is not hedged. The organisation has transactional currency exposures arising from

currency purchases besides the functional currency (Hines et al. 2015). These transactions

include operating costs within trade payables, which are minimum and foreign currency

investment purchases. As per its annual report in 2017, the organisation has revealed its net

exposures to movements in foreign currencies, which are represented as follows:

The risk exposures in the balance date depict the risk exposure evident in the financial

instruments. In this case, if the foreign currencies are not translated based on intra-day and daily

fluctuations of exchange rates, it might result in audit risk for the organisation. In fact, this

inaccuracy might result in material misstatements in the financial reports of Medibank.

Price risk:

Another inherent business risk for Medibank is price risk. This type of risk mainly arises

when the fair value of future cash flows of any financial instrument changes due to variations in

market prices, influential dynamic particular to the financial instrument or influential dynamics

Another business risk that would affect the audit activities of Medibank is foreign

currency risk. In the words of Griffiths (2016), foreign currency risk could be explained as the

risk, in which the fair value of financial instruments would vary because of modifications in

foreign exchange rates. The investments of Medibank in infrastructure and syndicated loans are

managed externally and the fund manager hedges the currency exposures from the economic

perspective. The global equities are managed externally and nearly 50% of the foreign currency

exposure is not hedged. The organisation has transactional currency exposures arising from

currency purchases besides the functional currency (Hines et al. 2015). These transactions

include operating costs within trade payables, which are minimum and foreign currency

investment purchases. As per its annual report in 2017, the organisation has revealed its net

exposures to movements in foreign currencies, which are represented as follows:

The risk exposures in the balance date depict the risk exposure evident in the financial

instruments. In this case, if the foreign currencies are not translated based on intra-day and daily

fluctuations of exchange rates, it might result in audit risk for the organisation. In fact, this

inaccuracy might result in material misstatements in the financial reports of Medibank.

Price risk:

Another inherent business risk for Medibank is price risk. This type of risk mainly arises

when the fair value of future cash flows of any financial instrument changes due to variations in

market prices, influential dynamic particular to the financial instrument or influential dynamics

5AUDITING AND ASSURANCE

impacting all other similar financial instruments in the market (Iskandar et al. 2018). Medibank

is observed to be exposed to price risk in relation to its fixed income investments owing to

fluctuations in credit spreads. The management of risk is conducted by active credit exposure

management as well as credit spread duration. The equity price risk of the organisation takes

place from investment in infrastructure, property, Australian and global equities. The risk

management department of Medibank manages this risk by developing and monitoring

objectives along with constraints on investments, expansion plans and investment restrictions in

each sector, market and nation. If the estimations are not made accurately, the future return on

investment would be lower and this poses a significant audit risk for the organisation. In

addition, the impact of provisional pricing and future price revisions might not be disclosed

adequately in the financial statements (Leidner and Lenz 2017).

Credit risk:

As commented by Bessis (2015), credit risk is apparent in investment and lending. This

could arise due to brokers, agents, clients and reinsurers. This type of risk is default in decline or

payment in the quality of credit. The investment concentration in counterparty, economic sector,

geographical areas and industry is normally risky. Moreover, this type of risk could occur from

too much exposure to group organisations. Furthermore, perfunctory overview of the potential

risks and complexities in complicated derivative contracts could result in credit risk as well.

In case of Medibank, credit risk takes place from the financial assets of the organisation

constituting of cash and cash equivalents, trade and other receivables along with financial assets

at fair value via profit or loss. The organisation uses reference to exposures by ratings bands,

industry, country and instrument type. The policy of investment management of Medibank

impacting all other similar financial instruments in the market (Iskandar et al. 2018). Medibank

is observed to be exposed to price risk in relation to its fixed income investments owing to

fluctuations in credit spreads. The management of risk is conducted by active credit exposure

management as well as credit spread duration. The equity price risk of the organisation takes

place from investment in infrastructure, property, Australian and global equities. The risk

management department of Medibank manages this risk by developing and monitoring

objectives along with constraints on investments, expansion plans and investment restrictions in

each sector, market and nation. If the estimations are not made accurately, the future return on

investment would be lower and this poses a significant audit risk for the organisation. In

addition, the impact of provisional pricing and future price revisions might not be disclosed

adequately in the financial statements (Leidner and Lenz 2017).

Credit risk:

As commented by Bessis (2015), credit risk is apparent in investment and lending. This

could arise due to brokers, agents, clients and reinsurers. This type of risk is default in decline or

payment in the quality of credit. The investment concentration in counterparty, economic sector,

geographical areas and industry is normally risky. Moreover, this type of risk could occur from

too much exposure to group organisations. Furthermore, perfunctory overview of the potential

risks and complexities in complicated derivative contracts could result in credit risk as well.

In case of Medibank, credit risk takes place from the financial assets of the organisation

constituting of cash and cash equivalents, trade and other receivables along with financial assets

at fair value via profit or loss. The organisation uses reference to exposures by ratings bands,

industry, country and instrument type. The policy of investment management of Medibank

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6AUDITING AND ASSURANCE

restricts maximum of internally handled credit exposure to A- or increased rated categories in

relation to long-term investments and A2 or greater in relation to short-term investments. The

external rating agencies like Standard & Poor’s mainly help in providing credit rating to

Medibank. Any shifts or departures from this policy and recruiting external managers need

approval from the board of the organisation.

Credit risk is computed depending on the repaying ability of the organisation (borrower).

Some organisations have established departments accountable for analysing the credit risks of its

existing and potential customers. In addition, with the help of technology, the business

organisations have the ability to assess data rapidly for analysing the risk profiles of their

customers (Sadgrove 2016). However, in case of Medibank, the organisation does not possess

financial instruments for mitigating credit risk and hence, security is not ensured on investments.

There are certain exceptions, which include asset-backed securities, covered bonds and

mortgage-backed securities. The board of Medibank manages the effect of the counterparty

default with the help of approved limits by rating, counterparty and expansion of counterparties.

This might have significant influence on the financial statements, as the unavailability of

financial instruments to mitigate credit risk might have adverse impact on the investment return

for the investors. As a result, it could be considered as a significant audit risk for the organisation

(Van Buuren et al. 2014).

restricts maximum of internally handled credit exposure to A- or increased rated categories in

relation to long-term investments and A2 or greater in relation to short-term investments. The

external rating agencies like Standard & Poor’s mainly help in providing credit rating to

Medibank. Any shifts or departures from this policy and recruiting external managers need

approval from the board of the organisation.

Credit risk is computed depending on the repaying ability of the organisation (borrower).

Some organisations have established departments accountable for analysing the credit risks of its

existing and potential customers. In addition, with the help of technology, the business

organisations have the ability to assess data rapidly for analysing the risk profiles of their

customers (Sadgrove 2016). However, in case of Medibank, the organisation does not possess

financial instruments for mitigating credit risk and hence, security is not ensured on investments.

There are certain exceptions, which include asset-backed securities, covered bonds and

mortgage-backed securities. The board of Medibank manages the effect of the counterparty

default with the help of approved limits by rating, counterparty and expansion of counterparties.

This might have significant influence on the financial statements, as the unavailability of

financial instruments to mitigate credit risk might have adverse impact on the investment return

for the investors. As a result, it could be considered as a significant audit risk for the organisation

(Van Buuren et al. 2014).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7AUDITING AND ASSURANCE

References:

Bessis, J., 2015. Risk management in banking. John Wiley & Sons.

Cohen, J., Krishnamoorthy, G. and Wright, A., 2017. Enterprise Risk Management and the

Financial Reporting Process: The Experiences of Audit Committee Members, CFO s, and

External Auditors. Contemporary Accounting Research, 34(2), pp.1178-1209.

Griffiths, P., 2016. Risk-based auditing. Routledge.

Hines, C.S., Masli, A., Mauldin, E.G. and Peters, G.F., 2015. Board risk committees and audit

pricing. Auditing: A Journal of Practice & Theory, 34(4), pp.59-84.

Iskandar, T.M., Jamil, A., Yatim, P. and Sanusi, Z.M., 2018. The role of internal audit and audit

committee in the implementation of enterprise risk management. International Journal of

Business and Globalisation, 21(2), pp.239-260.

Leidner, J.J. and Lenz, H., 2017. Client's business risk, public‐interest entities, and audit fees:

The case of German credit institutions. International Journal of Auditing, 21(3), pp.324-338.

Medibank., 2018. Medibank Private Health Insurance | For Better Health | Medibank. [online]

Available at: https://www.medibank.com.au/ [Accessed 20 Dec. 2018].

Medibank.com.au., 2018. [online] Available at:

https://www.medibank.com.au/content/dam/medibank/About-Us/pdfs/MPL_Annual_Report_201

7.pdf [Accessed 20 Dec. 2018].

Sadgrove, K., 2016. The complete guide to business risk management. Routledge.

References:

Bessis, J., 2015. Risk management in banking. John Wiley & Sons.

Cohen, J., Krishnamoorthy, G. and Wright, A., 2017. Enterprise Risk Management and the

Financial Reporting Process: The Experiences of Audit Committee Members, CFO s, and

External Auditors. Contemporary Accounting Research, 34(2), pp.1178-1209.

Griffiths, P., 2016. Risk-based auditing. Routledge.

Hines, C.S., Masli, A., Mauldin, E.G. and Peters, G.F., 2015. Board risk committees and audit

pricing. Auditing: A Journal of Practice & Theory, 34(4), pp.59-84.

Iskandar, T.M., Jamil, A., Yatim, P. and Sanusi, Z.M., 2018. The role of internal audit and audit

committee in the implementation of enterprise risk management. International Journal of

Business and Globalisation, 21(2), pp.239-260.

Leidner, J.J. and Lenz, H., 2017. Client's business risk, public‐interest entities, and audit fees:

The case of German credit institutions. International Journal of Auditing, 21(3), pp.324-338.

Medibank., 2018. Medibank Private Health Insurance | For Better Health | Medibank. [online]

Available at: https://www.medibank.com.au/ [Accessed 20 Dec. 2018].

Medibank.com.au., 2018. [online] Available at:

https://www.medibank.com.au/content/dam/medibank/About-Us/pdfs/MPL_Annual_Report_201

7.pdf [Accessed 20 Dec. 2018].

Sadgrove, K., 2016. The complete guide to business risk management. Routledge.

8AUDITING AND ASSURANCE

Van Buuren, J., Koch, C., Van Nieuw Amerongen, N. and Wright, A.M., 2014. The use of

business risk audit perspectives by non-Big 4 audit firms. Auditing: A Journal of Practice &

Theory, 33(3), pp.105-128.

Van Buuren, J., Koch, C., Van Nieuw Amerongen, N. and Wright, A.M., 2014. The use of

business risk audit perspectives by non-Big 4 audit firms. Auditing: A Journal of Practice &

Theory, 33(3), pp.105-128.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 9

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.