Auditing and Assurance Report: Retail Food Group Performance Review

VerifiedAdded on 2021/06/17

|17

|4545

|62

Report

AI Summary

This report provides a comprehensive analysis of the auditing and assurance practices of the Retail Food Group (RFG), examining its financial performance and internal controls. The analysis includes an evaluation of the 2016 and 2017 audit reports, assessing the type and appropriateness of the auditor's report. The report delves into RFG's internal control environment, identifying weaknesses and proposing solutions to mitigate risks. It also explores the business risks associated with RFG from an auditor's perspective, considering ethical issues and operational deficiencies. The report emphasizes the importance of ethical considerations for auditors and concludes with a summary of key findings and recommendations.

Auditing and Assurance of the Retail Food Group 1

AUDITING AND ASSURANCE OF THE RETAIL FOOD GROUP

Student by (Name)

Professor’s (Name)

College

Course

Date

AUDITING AND ASSURANCE OF THE RETAIL FOOD GROUP

Student by (Name)

Professor’s (Name)

College

Course

Date

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Auditing and Assurance of the Retail Food Group 2

Contents

Introduction......................................................................................................................................2

The evaluation of the 2016 and 2017 audit reports......................................................................3

The kind of report auditor that the auditor issued....................................................................4

The appropriateness of the audit report issued................................................................................5

The internal control environment of RFG.......................................................................................5

The assessment of RFG’s internal control environment..............................................................6

Ways to overcome the identified internal control weakness........................................................8

The business risk associated with the RFG from the auditors’ point of view..........................9

RFG’s operations from an ethical perspective...............................................................................10

The deficiencies in the practice of RFG’s operations................................................................11

Why ethical issues should interest the auditors......................................................................12

Conclusion.....................................................................................................................................12

Contents

Introduction......................................................................................................................................2

The evaluation of the 2016 and 2017 audit reports......................................................................3

The kind of report auditor that the auditor issued....................................................................4

The appropriateness of the audit report issued................................................................................5

The internal control environment of RFG.......................................................................................5

The assessment of RFG’s internal control environment..............................................................6

Ways to overcome the identified internal control weakness........................................................8

The business risk associated with the RFG from the auditors’ point of view..........................9

RFG’s operations from an ethical perspective...............................................................................10

The deficiencies in the practice of RFG’s operations................................................................11

Why ethical issues should interest the auditors......................................................................12

Conclusion.....................................................................................................................................12

Auditing and Assurance of the Retail Food Group 3

Auditing and Assurance of the Retail Food Group

Introduction

The Retail Food Group (RFG) was established in 1989 and in 2003 incorporated to become

the most major holding company of the RFG's units. It brands several types of retail food

franchise. Some of its brands are Donut King, Brumby's Bakery, Pizza Capers, Gloria jeans,

Pizza bar, and Michel's Patisserie. It operates under the following pillars; the franchise, the

International, the Allied beverage and coffee, and the Commercial division. We evaluated the

audit reports for 2016 and 2017. We collected the data from a reliable source and we hereby

declare that all the data and records we are showing here is authentic.

The evaluation of the 2016 and 2017 audit reports

The auditor used the Retail Food Group’s annual reports, financial statements and

accounts to do his auditing. The RFG's annual reports have marked the company's exceptional

decade of growth. It has shown the company's commitment to offering its shareholders

outstanding services and investing a distinct global operating platform (Schaper et al. 2014). In

2016, the year’s annual reports showed that the group’s NPAT (Net Profit After Taxation) profit

amounted to 66.4 dollars, a 20.5% increase over the previous year (Wright and Clarke 2009).

The financial statement revealed that the year’s earnings translated per share translated into

40.5cps (Cents Per Share) and thus contributing the total year's dividends per share into 27.5cps.

This was an 18.5% increase from the previous year. During the year, the final accounting records

proved that the company marked a 24% EBITDA (Earnings before Interest, Taxes, Depreciation,

Auditing and Assurance of the Retail Food Group

Introduction

The Retail Food Group (RFG) was established in 1989 and in 2003 incorporated to become

the most major holding company of the RFG's units. It brands several types of retail food

franchise. Some of its brands are Donut King, Brumby's Bakery, Pizza Capers, Gloria jeans,

Pizza bar, and Michel's Patisserie. It operates under the following pillars; the franchise, the

International, the Allied beverage and coffee, and the Commercial division. We evaluated the

audit reports for 2016 and 2017. We collected the data from a reliable source and we hereby

declare that all the data and records we are showing here is authentic.

The evaluation of the 2016 and 2017 audit reports

The auditor used the Retail Food Group’s annual reports, financial statements and

accounts to do his auditing. The RFG's annual reports have marked the company's exceptional

decade of growth. It has shown the company's commitment to offering its shareholders

outstanding services and investing a distinct global operating platform (Schaper et al. 2014). In

2016, the year’s annual reports showed that the group’s NPAT (Net Profit After Taxation) profit

amounted to 66.4 dollars, a 20.5% increase over the previous year (Wright and Clarke 2009).

The financial statement revealed that the year’s earnings translated per share translated into

40.5cps (Cents Per Share) and thus contributing the total year's dividends per share into 27.5cps.

This was an 18.5% increase from the previous year. During the year, the final accounting records

proved that the company marked a 24% EBITDA (Earnings before Interest, Taxes, Depreciation,

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Auditing and Assurance of the Retail Food Group 4

and Amortization) profit, which amounted to 110.2m dollars. The coffee operations contributed

over 50% to the company’s EBITDA result. This result illustrated the company’s growing

diversity of their revenue across its global businesses. It also emphasized the RFG’s ability to

sustain its multiple platforms and as well as enhancing its performance in the future. The RFG's

account records described that the group’s net sales that year was $16.1 billion, and their gross

profit was $2.0 billion. Their net income was 68.3 million, and their adjusted EBITDA was

$366,6m. It marked a remarkable growth for the Retail Food group (Hoitash et al. 2009).

The 2017’s annual reports indicated that the RFG’s revenue was 349.3m dollars, a 27.0%

increase from the previous year’s revenue. The books of accounting clearly revealed that the

RFG's EBITDA was 123.5m dollars, a difference of 12.1% from 2016's EBITDA income. The

books also demonstrated that the groups' NPAT amounted to $75.7m which marked a 14.0%

increment of 14.0% from 2016. The auditing records exhibited that the RFG's EPS (Earnings Per

Share) was 43.7cps, and its dividends that year was 29.75cps, which marked a rise of 7.9% and

8.2% respectively from the previous year's results. The territories under which RFG operates in

the increase from 69 in 2016 to 81 in 2017 (Dar 2011). This marked a significant growth of

17.4%, which showed the RFG’s capacity to grow and expand their licensed territories further.

The five pillars' contribution to the EBITDA was highly valued. The records of accounts in each

pillar were used to demonstrate the individual contribution of each sector and their ratio of

contribution calculated. The Franchise contributed $53.7m dollars which were 43% of the total

EBITDA in 2017. The Franchise contributed the highest EBITDA amount to the company during

the year. The International pillar and the coffee operations and the beverage allied group

contributed a total of $15.3m and $42.7m respectively EBITDA result. What it marked was a

13% and a 34% individual contribution to the company’s total EBITDA value during the year.

and Amortization) profit, which amounted to 110.2m dollars. The coffee operations contributed

over 50% to the company’s EBITDA result. This result illustrated the company’s growing

diversity of their revenue across its global businesses. It also emphasized the RFG’s ability to

sustain its multiple platforms and as well as enhancing its performance in the future. The RFG's

account records described that the group’s net sales that year was $16.1 billion, and their gross

profit was $2.0 billion. Their net income was 68.3 million, and their adjusted EBITDA was

$366,6m. It marked a remarkable growth for the Retail Food group (Hoitash et al. 2009).

The 2017’s annual reports indicated that the RFG’s revenue was 349.3m dollars, a 27.0%

increase from the previous year’s revenue. The books of accounting clearly revealed that the

RFG's EBITDA was 123.5m dollars, a difference of 12.1% from 2016's EBITDA income. The

books also demonstrated that the groups' NPAT amounted to $75.7m which marked a 14.0%

increment of 14.0% from 2016. The auditing records exhibited that the RFG's EPS (Earnings Per

Share) was 43.7cps, and its dividends that year was 29.75cps, which marked a rise of 7.9% and

8.2% respectively from the previous year's results. The territories under which RFG operates in

the increase from 69 in 2016 to 81 in 2017 (Dar 2011). This marked a significant growth of

17.4%, which showed the RFG’s capacity to grow and expand their licensed territories further.

The five pillars' contribution to the EBITDA was highly valued. The records of accounts in each

pillar were used to demonstrate the individual contribution of each sector and their ratio of

contribution calculated. The Franchise contributed $53.7m dollars which were 43% of the total

EBITDA in 2017. The Franchise contributed the highest EBITDA amount to the company during

the year. The International pillar and the coffee operations and the beverage allied group

contributed a total of $15.3m and $42.7m respectively EBITDA result. What it marked was a

13% and a 34% individual contribution to the company’s total EBITDA value during the year.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Auditing and Assurance of the Retail Food Group 5

The Commercial Division pillar recorded an EBITDA result of $11.8m, which was a 10%

contribution to the total EBITDA amount. The returns from the five pillars of growth enabled the

RFG group to increase their dividends to 29.75cps from the previous year's dividend which was

27.5cps. The RFG’s increased profit and revenue enabled the company to expand its territories

from 69 in 2016 to 81 in 29 in 2017 (Horngren et al. 2012). Their expansion in territories marked

the company’s exceptional growth and its ability to grow further in the future.

The kind of report auditor that the auditor issued

The auditor presented a clean type of audit report. All the accounting and the records

were transparent, and there was no hidden information concerning the company's financial data.

The group had maintained and safeguarded all their accounting books, and they were readily

available to the auditor when he needed them. The auditing was prepared by the GAAP

(Generally Accepted Accounting Principles). The auditor reserved no information concerning the

financial position of the RFA. All the accounting books; the statement of RFA's financial

position, loss and profit statements, cash flows accounts, statements of changes in equity,

additional stock exchange statements, and many more were readily available, and the company

had maintained them properly (Chan et al. 2009). The RFG group had enough policies and

internal controls to ensure the safety of their assets and inventories. The auditor of the Retail

Food Group examines all the company’s financial accounts and statements to help in assessing

the company’s financial position.

The Commercial Division pillar recorded an EBITDA result of $11.8m, which was a 10%

contribution to the total EBITDA amount. The returns from the five pillars of growth enabled the

RFG group to increase their dividends to 29.75cps from the previous year's dividend which was

27.5cps. The RFG’s increased profit and revenue enabled the company to expand its territories

from 69 in 2016 to 81 in 29 in 2017 (Horngren et al. 2012). Their expansion in territories marked

the company’s exceptional growth and its ability to grow further in the future.

The kind of report auditor that the auditor issued

The auditor presented a clean type of audit report. All the accounting and the records

were transparent, and there was no hidden information concerning the company's financial data.

The group had maintained and safeguarded all their accounting books, and they were readily

available to the auditor when he needed them. The auditing was prepared by the GAAP

(Generally Accepted Accounting Principles). The auditor reserved no information concerning the

financial position of the RFA. All the accounting books; the statement of RFA's financial

position, loss and profit statements, cash flows accounts, statements of changes in equity,

additional stock exchange statements, and many more were readily available, and the company

had maintained them properly (Chan et al. 2009). The RFG group had enough policies and

internal controls to ensure the safety of their assets and inventories. The auditor of the Retail

Food Group examines all the company’s financial accounts and statements to help in assessing

the company’s financial position.

Auditing and Assurance of the Retail Food Group 6

The appropriateness of the audit report issued

A clean audit report is a requirement by most financial institutions before they can lend

money to business organizations. If the company is in need of financial assistance, any lending

institution will give the company loans easily because its auditing reports are readily available

(Bing and Jing 2009). The report's availability and transparency offer the prospective investors

an opportunity to access the company's financial position to make them make an informed

decision whether to become a company's shareholder or not. The report's availability will assist

the company to earn more clients. This clean report maintains the company's customers to gain

their confidence in them in delivering to them quality products and services. It will also help

them make more informed decisions on their investment strategies.

The internal control environment of RFG

The internal control environment of the RFG group is the basis upon which its internal

control system is created (HORNGREN et al. 2012). The RFG's control environment strives to

achieve the company's goals and objectives, furnish the proper financial records to both their

internal and the external stakeholders, carry out an effective and efficient business, fulfill all the

legal requirements, and protect its business assets. The critical components of the RFG's internal

control environment are; the environment in charge, the assessment of risks, the activities in

charge, the informative and communicative control elements, and the monitoring activities (Shao

2009). The control environment is the group of policies upon which the internal control within

RFG is based. The risk assessment is the methodology that the RFG uses to identify, assess, and

mitigate risks with the aim of the aim of achieving the company’s goals. The information and

The appropriateness of the audit report issued

A clean audit report is a requirement by most financial institutions before they can lend

money to business organizations. If the company is in need of financial assistance, any lending

institution will give the company loans easily because its auditing reports are readily available

(Bing and Jing 2009). The report's availability and transparency offer the prospective investors

an opportunity to access the company's financial position to make them make an informed

decision whether to become a company's shareholder or not. The report's availability will assist

the company to earn more clients. This clean report maintains the company's customers to gain

their confidence in them in delivering to them quality products and services. It will also help

them make more informed decisions on their investment strategies.

The internal control environment of RFG

The internal control environment of the RFG group is the basis upon which its internal

control system is created (HORNGREN et al. 2012). The RFG's control environment strives to

achieve the company's goals and objectives, furnish the proper financial records to both their

internal and the external stakeholders, carry out an effective and efficient business, fulfill all the

legal requirements, and protect its business assets. The critical components of the RFG's internal

control environment are; the environment in charge, the assessment of risks, the activities in

charge, the informative and communicative control elements, and the monitoring activities (Shao

2009). The control environment is the group of policies upon which the internal control within

RFG is based. The risk assessment is the methodology that the RFG uses to identify, assess, and

mitigate risks with the aim of the aim of achieving the company’s goals. The information and

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Auditing and Assurance of the Retail Food Group 7

communication system of the company will involve distributing all the information required to

perform the risk controls. It will help the internal and the external stakeholders to comprehend

the duties and the responsibilities of the internal control system (Badara et al. 2013). The control

activities are the actions that the management of RFG will take and perform regarding its

policies and standards that will direct them to control the risks to help the company achieve its

goals and objectives. The monitoring activities mean the act of evaluating the implementation of

all the five components of an internal audit. We will assess the RFG’s internal control

environment and come up with ways to overcome the identified control weakness (Liu et al.

2009).

The assessment of RFG’s internal control environment

Regarding the results of the 2016 and 2017 auditing, the auditors came up with the final

results of all the associated risks with each component of internal control (Karagiorgos et al.

2011).

If an internal control component has a high risk, it means if the risk is not mitigated

immediately, it could cause the company to fail meeting some or most of its objectives. Controls

must be taken directly to prevent the adverse effects from happening. Medium risks may affect

the company's performance, but the results are not detrimental. Actions need not be considered

immediately (Klamn et al. 2012). Low threats mean that the possibility of the risk affecting the

performance of the company is manageable but should not be ignored. If the risks of the internal

components of the Retail Food Group are low, the company can still meet its goals and

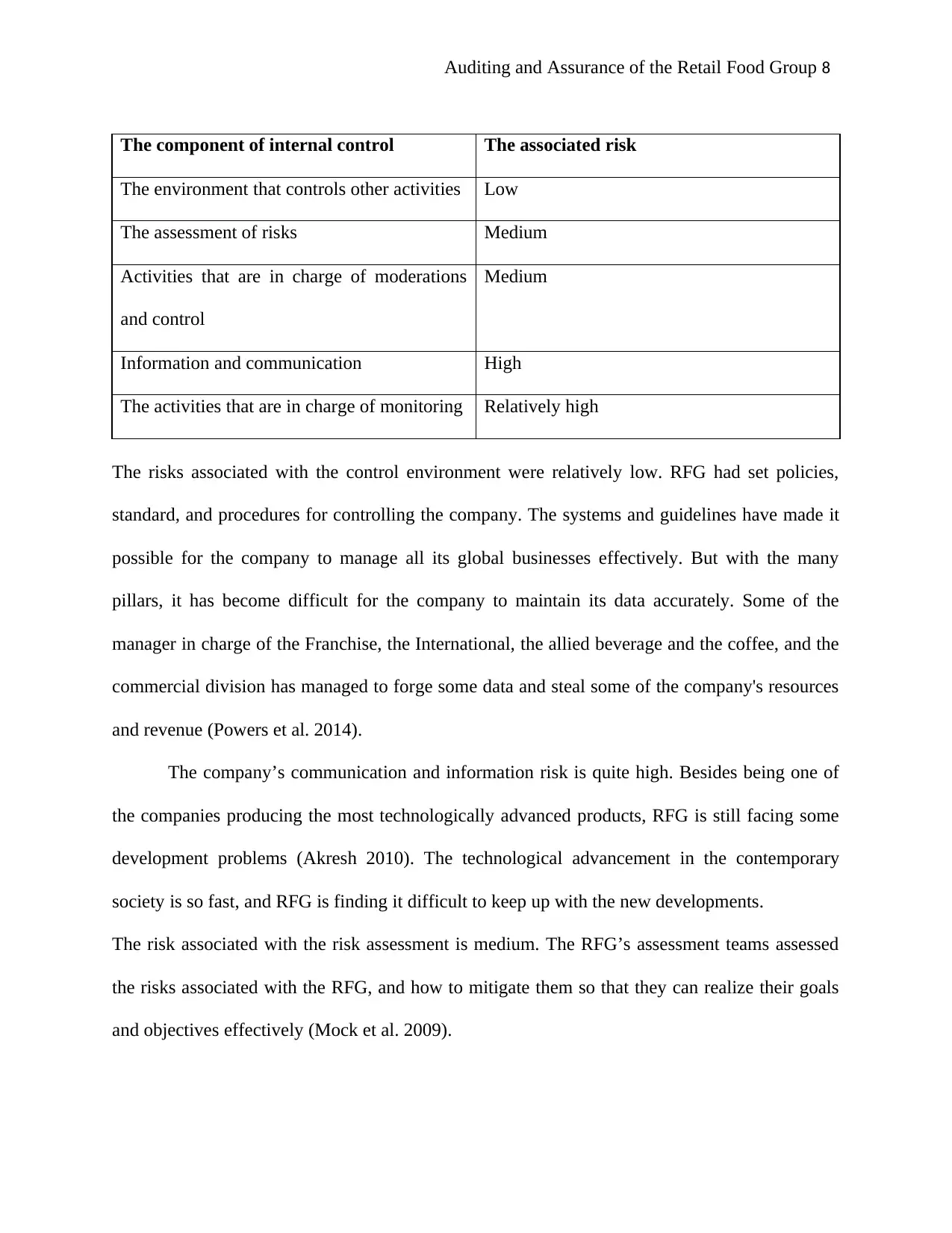

objectives without much trouble. The table below shows all the elements of internal controls

with their associated rate of risk.

communication system of the company will involve distributing all the information required to

perform the risk controls. It will help the internal and the external stakeholders to comprehend

the duties and the responsibilities of the internal control system (Badara et al. 2013). The control

activities are the actions that the management of RFG will take and perform regarding its

policies and standards that will direct them to control the risks to help the company achieve its

goals and objectives. The monitoring activities mean the act of evaluating the implementation of

all the five components of an internal audit. We will assess the RFG’s internal control

environment and come up with ways to overcome the identified control weakness (Liu et al.

2009).

The assessment of RFG’s internal control environment

Regarding the results of the 2016 and 2017 auditing, the auditors came up with the final

results of all the associated risks with each component of internal control (Karagiorgos et al.

2011).

If an internal control component has a high risk, it means if the risk is not mitigated

immediately, it could cause the company to fail meeting some or most of its objectives. Controls

must be taken directly to prevent the adverse effects from happening. Medium risks may affect

the company's performance, but the results are not detrimental. Actions need not be considered

immediately (Klamn et al. 2012). Low threats mean that the possibility of the risk affecting the

performance of the company is manageable but should not be ignored. If the risks of the internal

components of the Retail Food Group are low, the company can still meet its goals and

objectives without much trouble. The table below shows all the elements of internal controls

with their associated rate of risk.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Auditing and Assurance of the Retail Food Group 8

The component of internal control The associated risk

The environment that controls other activities Low

The assessment of risks Medium

Activities that are in charge of moderations

and control

Medium

Information and communication High

The activities that are in charge of monitoring Relatively high

The risks associated with the control environment were relatively low. RFG had set policies,

standard, and procedures for controlling the company. The systems and guidelines have made it

possible for the company to manage all its global businesses effectively. But with the many

pillars, it has become difficult for the company to maintain its data accurately. Some of the

manager in charge of the Franchise, the International, the allied beverage and the coffee, and the

commercial division has managed to forge some data and steal some of the company's resources

and revenue (Powers et al. 2014).

The company’s communication and information risk is quite high. Besides being one of

the companies producing the most technologically advanced products, RFG is still facing some

development problems (Akresh 2010). The technological advancement in the contemporary

society is so fast, and RFG is finding it difficult to keep up with the new developments.

The risk associated with the risk assessment is medium. The RFG’s assessment teams assessed

the risks associated with the RFG, and how to mitigate them so that they can realize their goals

and objectives effectively (Mock et al. 2009).

The component of internal control The associated risk

The environment that controls other activities Low

The assessment of risks Medium

Activities that are in charge of moderations

and control

Medium

Information and communication High

The activities that are in charge of monitoring Relatively high

The risks associated with the control environment were relatively low. RFG had set policies,

standard, and procedures for controlling the company. The systems and guidelines have made it

possible for the company to manage all its global businesses effectively. But with the many

pillars, it has become difficult for the company to maintain its data accurately. Some of the

manager in charge of the Franchise, the International, the allied beverage and the coffee, and the

commercial division has managed to forge some data and steal some of the company's resources

and revenue (Powers et al. 2014).

The company’s communication and information risk is quite high. Besides being one of

the companies producing the most technologically advanced products, RFG is still facing some

development problems (Akresh 2010). The technological advancement in the contemporary

society is so fast, and RFG is finding it difficult to keep up with the new developments.

The risk associated with the risk assessment is medium. The RFG’s assessment teams assessed

the risks associated with the RFG, and how to mitigate them so that they can realize their goals

and objectives effectively (Mock et al. 2009).

Auditing and Assurance of the Retail Food Group 9

The company’s activities for monitoring risks were relatively high (Al Sawalqa et al.

2012). There were many underlying weaknesses under this component of internal control. Some

of them were; inadequate monitoring tools, clear criteria for monitoring the activities within the

company, and lack of transparency on the roles and the responsibility of the monitoring

activities. Some groups did not give accurate data in the required format while some presented

the accounting records incomplete and sometimes late. The data of the audits sometimes was

inconsistent with the data of the Retail Food Group.

Ways to overcome the identified internal control weakness

The Food Retail Group came up with policies to mitigate the risks associated with each

component. It was clear that the monitoring activities had the highest risk. The RFG defined

some methods and criteria for monitoring activities, information, and the performance of the

company (Balsam et al. 2014). The group decided to assess the need for a proper data analysis at

all levels. They chose to allocate enough resources for the meeting of the company's objectives

and keep track of record of all the activities within the company. The company's managers set a

clear means of ensuring a transparent follow-up of all the data regarding the company's assets,

liabilities, income, expenses, and much other related information (Tsay 2010).

The company’s communication and information risks are quite high. To overcome it, the Retail

Food Company has to innovative enough to come up with advancing technology. They have to

keep updating their communication skills and information availability by developing their

technology throughout. This was expensive for them, but they had no choice.

The company’s activities for monitoring risks were relatively high (Al Sawalqa et al.

2012). There were many underlying weaknesses under this component of internal control. Some

of them were; inadequate monitoring tools, clear criteria for monitoring the activities within the

company, and lack of transparency on the roles and the responsibility of the monitoring

activities. Some groups did not give accurate data in the required format while some presented

the accounting records incomplete and sometimes late. The data of the audits sometimes was

inconsistent with the data of the Retail Food Group.

Ways to overcome the identified internal control weakness

The Food Retail Group came up with policies to mitigate the risks associated with each

component. It was clear that the monitoring activities had the highest risk. The RFG defined

some methods and criteria for monitoring activities, information, and the performance of the

company (Balsam et al. 2014). The group decided to assess the need for a proper data analysis at

all levels. They chose to allocate enough resources for the meeting of the company's objectives

and keep track of record of all the activities within the company. The company's managers set a

clear means of ensuring a transparent follow-up of all the data regarding the company's assets,

liabilities, income, expenses, and much other related information (Tsay 2010).

The company’s communication and information risks are quite high. To overcome it, the Retail

Food Company has to innovative enough to come up with advancing technology. They have to

keep updating their communication skills and information availability by developing their

technology throughout. This was expensive for them, but they had no choice.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Auditing and Assurance of the Retail Food Group 10

The business risk associated with the RFG from the auditors’ point of view

The Franchise is the RFG's most significant source of income. The auditor's reports

showed that they contribute over 40% of the company's total EBITDA and sequentially they are

RFG's most significant source of income. The company is over pressuring them thus making the

RTG's revenue unsustainable. Over 10% of the Franchise market is weak, and this is a signal of

problems. The company is increasing the EPS (Earnings Per Share) and the dividends they are

giving to their shareholders. They raised the shareholder's EPS from 40.5cps in 2016 to 43.7cps

in 2017, as per their accounting records. This was a 7.9% rise in the EPS. They also increased

their dividends from 27.5cps to 29.75cps. Expanding the shareholder's cent per share could be an

advantage by earning the company more shareholders, but on the other hand, it could reduce

their revenue over time if they raise them without considering cost factors.

Due to its large size, the company is highly sensitive to its markets shocks. Many investors

would opt to go for smaller companies in the hospitality industry as a result. The cost of

maintaining such a big company is also high, and slight poor management would mean a

deterioration in the company’s revenue and income. It could also mean a failure of the company,

and its operations might cease (Rossier et al. 2015).

The risks the company has regarding protecting its assets are very high. Insurance companies

demand high insurance fees to insure them. The costs of maintaining their business assets, other

than insurance are also very high. Such costs include repair and renewal of these assets, the costs

of securing them, and many other related costs.

The company has high revenues and income from their various operations. These high revenues

attract incredibly high taxation from the government. It is usually a huge challenge for the Retail

The business risk associated with the RFG from the auditors’ point of view

The Franchise is the RFG's most significant source of income. The auditor's reports

showed that they contribute over 40% of the company's total EBITDA and sequentially they are

RFG's most significant source of income. The company is over pressuring them thus making the

RTG's revenue unsustainable. Over 10% of the Franchise market is weak, and this is a signal of

problems. The company is increasing the EPS (Earnings Per Share) and the dividends they are

giving to their shareholders. They raised the shareholder's EPS from 40.5cps in 2016 to 43.7cps

in 2017, as per their accounting records. This was a 7.9% rise in the EPS. They also increased

their dividends from 27.5cps to 29.75cps. Expanding the shareholder's cent per share could be an

advantage by earning the company more shareholders, but on the other hand, it could reduce

their revenue over time if they raise them without considering cost factors.

Due to its large size, the company is highly sensitive to its markets shocks. Many investors

would opt to go for smaller companies in the hospitality industry as a result. The cost of

maintaining such a big company is also high, and slight poor management would mean a

deterioration in the company’s revenue and income. It could also mean a failure of the company,

and its operations might cease (Rossier et al. 2015).

The risks the company has regarding protecting its assets are very high. Insurance companies

demand high insurance fees to insure them. The costs of maintaining their business assets, other

than insurance are also very high. Such costs include repair and renewal of these assets, the costs

of securing them, and many other related costs.

The company has high revenues and income from their various operations. These high revenues

attract incredibly high taxation from the government. It is usually a huge challenge for the Retail

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Auditing and Assurance of the Retail Food Group 11

Food Group since all their efforts and hard work end up being reduced. This can be shown by the

difference between the company's EBITDA (Earnings before interests, taxation, depreciation,

and amortization) and its NPAT (Net profit after taxation). The auditor's reports showed that in

2016, the RFG's EBITDA amount was $110.2m and its NPAT was $66.4m. That was a

considerable drop in profit most of which was contributed by the high taxation. The records of

2017 audits showed a similar analysis. The 2017's EBITDA for the company was $123.5m while

its NPAT was $75.7m. The high taxation from the government reduces the company's net profit,

and this could discourage the company from investing further. Expanding their business also is

attracts further tax as a requirement by the law. This is limiting the RFG from growing their

business as fast as they would have wished.

RFG’s operations from an ethical perspective

It is essential to understand the operations of the Retail food group from an ethical

perspective because it will help us understand the reasons behind buying their products. It helps

us know the company's strategic plans and whether their operations meet the legal requirements.

The RFG is involved in designing, developing, and managing their franchise and their

intellectual property from rebranding and copyright (Wright and Clarke 2009). Six principles

guide RFG's operations from an ethical performance; the duties and obligations, the interest of

the public, wholeness and uprightness, goals and independence, enough support and care, and

logic. The RFG must carry out their duties keeping in mind that they are responsible for their

actions. They should conduct themselves with the utmost care. They should consider the interest

of their customers to produce brands that are required by the public. Some of their operations are

marketing strategies like advertising, brand blending, innovation and many other activities

Food Group since all their efforts and hard work end up being reduced. This can be shown by the

difference between the company's EBITDA (Earnings before interests, taxation, depreciation,

and amortization) and its NPAT (Net profit after taxation). The auditor's reports showed that in

2016, the RFG's EBITDA amount was $110.2m and its NPAT was $66.4m. That was a

considerable drop in profit most of which was contributed by the high taxation. The records of

2017 audits showed a similar analysis. The 2017's EBITDA for the company was $123.5m while

its NPAT was $75.7m. The high taxation from the government reduces the company's net profit,

and this could discourage the company from investing further. Expanding their business also is

attracts further tax as a requirement by the law. This is limiting the RFG from growing their

business as fast as they would have wished.

RFG’s operations from an ethical perspective

It is essential to understand the operations of the Retail food group from an ethical

perspective because it will help us understand the reasons behind buying their products. It helps

us know the company's strategic plans and whether their operations meet the legal requirements.

The RFG is involved in designing, developing, and managing their franchise and their

intellectual property from rebranding and copyright (Wright and Clarke 2009). Six principles

guide RFG's operations from an ethical performance; the duties and obligations, the interest of

the public, wholeness and uprightness, goals and independence, enough support and care, and

logic. The RFG must carry out their duties keeping in mind that they are responsible for their

actions. They should conduct themselves with the utmost care. They should consider the interest

of their customers to produce brands that are required by the public. Some of their operations are

marketing strategies like advertising, brand blending, innovation and many other activities

Auditing and Assurance of the Retail Food Group 12

(Leschewski 2016). The RFG has franchised their products, made various types of brands, and

promoted retailing of their products (Wright and Clarke 2009). All these operations should be

carried out ethically while following six principles.

The deficiencies in the practice of RFG’s operations

The Retail Food Group's product is not very popular compared to that of their competitors.

This is because they have poor marketing strategies which have affected the awareness of their

brands in the market (Hattersley 2013). There is a quite big contrast between the perception of

RFG's brands and that of their competitors' brands. The RFG aims at improving their market

strategies and making their products known to their customers. To be able to accomplish this

new objective, they will develop market franchises to improve their advertising and marketing

strategies (Ashbaugh‐Skaife et al. 2009). An increase in the use of mobile phones will force the

RFG to be more innovative to increase the chances of their products being bought online. If they

don't consider this new development, the demand for their products will remain stagnant, and

thus their competitors will have an advantage over them (Jiang et al. 2010). This innovation will

cause them a lot of money, and then it will take time before they recover all those resources. The

RFG has high debts since its debt to equity ratio is 69.95%. This means that the company is

currently making losses and its current assets might not be able to pay for all its liabilities.

Why ethical issues should interest the auditors

Auditors must promote ethical conduct while doing their professional responsibilities and

duties (Wright and Clarke 2009). It is a legal requirement of the law that all the auditors ethically

conduct themselves by giving the correct audit records. The ethical issues such as the marketing

(Leschewski 2016). The RFG has franchised their products, made various types of brands, and

promoted retailing of their products (Wright and Clarke 2009). All these operations should be

carried out ethically while following six principles.

The deficiencies in the practice of RFG’s operations

The Retail Food Group's product is not very popular compared to that of their competitors.

This is because they have poor marketing strategies which have affected the awareness of their

brands in the market (Hattersley 2013). There is a quite big contrast between the perception of

RFG's brands and that of their competitors' brands. The RFG aims at improving their market

strategies and making their products known to their customers. To be able to accomplish this

new objective, they will develop market franchises to improve their advertising and marketing

strategies (Ashbaugh‐Skaife et al. 2009). An increase in the use of mobile phones will force the

RFG to be more innovative to increase the chances of their products being bought online. If they

don't consider this new development, the demand for their products will remain stagnant, and

thus their competitors will have an advantage over them (Jiang et al. 2010). This innovation will

cause them a lot of money, and then it will take time before they recover all those resources. The

RFG has high debts since its debt to equity ratio is 69.95%. This means that the company is

currently making losses and its current assets might not be able to pay for all its liabilities.

Why ethical issues should interest the auditors

Auditors must promote ethical conduct while doing their professional responsibilities and

duties (Wright and Clarke 2009). It is a legal requirement of the law that all the auditors ethically

conduct themselves by giving the correct audit records. The ethical issues such as the marketing

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 17

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.