Auditing and Assurance Services Name of the University Author's Note

VerifiedAdded on 2023/04/23

|18

|3975

|474

AI Summary

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Running head: AUDITING AND ASSURANCE SERVICES

Auditing and Assurance Services

Name of the Student

Name of the University

Author’s Note

Auditing and Assurance Services

Name of the Student

Name of the University

Author’s Note

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

1AUDITING AND ASSURANCE SERVICES

Table of Contents

Question 1: Advanced Computer Solutions...............................................................................2

Requirement a: Assertions.....................................................................................................2

Requirement b: Substantive Audit Procedures......................................................................3

Requirement c: ASA 701.......................................................................................................4

ASA 701 Communicating Key Audit Matters....................................................................4

Determination Rationales...................................................................................................4

Required Disclosure...........................................................................................................5

Question 2: Green Machine Ltd.................................................................................................6

Requirement a: Assertions.....................................................................................................6

Requirement b: Substantive Audit Procedures......................................................................7

Requirement c: ASA 701.......................................................................................................8

ASA 701 Communicating Key Audit Matters....................................................................8

Determination Rationales...................................................................................................9

Required Disclosure...........................................................................................................9

References................................................................................................................................12

Appendices...............................................................................................................................15

Question 1: Advanced Computer Solutions

Requirement a: Assertions

Table of Contents

Question 1: Advanced Computer Solutions...............................................................................2

Requirement a: Assertions.....................................................................................................2

Requirement b: Substantive Audit Procedures......................................................................3

Requirement c: ASA 701.......................................................................................................4

ASA 701 Communicating Key Audit Matters....................................................................4

Determination Rationales...................................................................................................4

Required Disclosure...........................................................................................................5

Question 2: Green Machine Ltd.................................................................................................6

Requirement a: Assertions.....................................................................................................6

Requirement b: Substantive Audit Procedures......................................................................7

Requirement c: ASA 701.......................................................................................................8

ASA 701 Communicating Key Audit Matters....................................................................8

Determination Rationales...................................................................................................9

Required Disclosure...........................................................................................................9

References................................................................................................................................12

Appendices...............................................................................................................................15

Question 1: Advanced Computer Solutions

Requirement a: Assertions

2AUDITING AND ASSURANCE SERVICES

Accuracy or Valuation: Testing of this assertion helps in showing whether there is any error

in the inventory transactions or not. The auditors is needed to test the correctness of the

values of physical inventory; and they need to test whether the same amount of inventory

comes to the income statements from the balance sheet as cost of goods sold (Smieliauskas,

2013). Moreover, it is needed for the companies to record the inventories in lower of cost and

net realizable value in the financial statements. The companies need to ensure their adherence

to the standards and principles of AASB 16 for the accurate valuation of the inventories. The

inventories of Advanced Computer Solutions have been moved to six regional warehouses in

March 2018. For this reason, there can be the possibility of error in the process to physically

counting the inventory in the new warehouses. In addition, it is likely that the correct amount

of inventory has not come to the income statements from balance sheet as cost of goods sold

and these reasons can decrease the inventory turnover in 2018. Moreover, it is likely that the

management of Advanced Computer Solutions has not recorded the inventory at the lower of

cost and net realizable value which can lead to material misstatements in inventory. It is also

probable that the company has not followed AASB 116. Hence, this assertion is at risk

(Dowling and Leech, 2014).

Cut Off: The examination of this assertion shows whether the inventory transaction have

been recorded in the correct financial period. For this, the auditor must test all the receiving

as well as shipping documents with the aim to verify whether the transactions have been

recorded in the correct period (Tan, 2015). It restricts the companies to record the previous

year’s transaction in the current year. As per the provided information of the company, the

inventory of the current year includes both the sales of the current and previous year. This

particular aspect indicates that there is error in the recording of certain inventory transactions

in the proper financial period. It is likely that the responsible staffs has wrongly included the

Accuracy or Valuation: Testing of this assertion helps in showing whether there is any error

in the inventory transactions or not. The auditors is needed to test the correctness of the

values of physical inventory; and they need to test whether the same amount of inventory

comes to the income statements from the balance sheet as cost of goods sold (Smieliauskas,

2013). Moreover, it is needed for the companies to record the inventories in lower of cost and

net realizable value in the financial statements. The companies need to ensure their adherence

to the standards and principles of AASB 16 for the accurate valuation of the inventories. The

inventories of Advanced Computer Solutions have been moved to six regional warehouses in

March 2018. For this reason, there can be the possibility of error in the process to physically

counting the inventory in the new warehouses. In addition, it is likely that the correct amount

of inventory has not come to the income statements from balance sheet as cost of goods sold

and these reasons can decrease the inventory turnover in 2018. Moreover, it is likely that the

management of Advanced Computer Solutions has not recorded the inventory at the lower of

cost and net realizable value which can lead to material misstatements in inventory. It is also

probable that the company has not followed AASB 116. Hence, this assertion is at risk

(Dowling and Leech, 2014).

Cut Off: The examination of this assertion shows whether the inventory transaction have

been recorded in the correct financial period. For this, the auditor must test all the receiving

as well as shipping documents with the aim to verify whether the transactions have been

recorded in the correct period (Tan, 2015). It restricts the companies to record the previous

year’s transaction in the current year. As per the provided information of the company, the

inventory of the current year includes both the sales of the current and previous year. This

particular aspect indicates that there is error in the recording of certain inventory transactions

in the proper financial period. It is likely that the responsible staffs has wrongly included the

3AUDITING AND ASSURANCE SERVICES

previous year’s sale in the current year’s inventory which create risk. For the presence of

these reasons, this assertion is at risk (Hussain and Al-Mourad, 2014).

Requirement b: Substantive Audit Procedures

First Risk: The requirement for the auditor is to observe and test the procedures include

under the physical inventory counting process. Specifically, the auditor must scrutinize the

physical inventory counting process when they are being progressing and they need to

examine the inventory count tags (Council, 2014). Most importantly, the auditor must involve

in the testing of the inventory in the six regional warehouses and needs to compare the results

with the confirmation from the central warehouse with the aim to find the error. In addition,

the auditor is needed to verify whether the company has followed the principles and standards

of AASB 116 for the accounting of their inventories. Lastly, the auditor must test the costing

process of the company to ensure the correct flow of inventory in the income statements as

cost of goods (Council, 2014).

Second Risk: With the aim to test this audit assertion, the auditor need to ensure the testing

of all the goods received to warehouses and goods delivered to suppliers notes so that the

errors in the cut offs can be identified (Seidel, 2014). The auditor must involve applying the

required analytical procedures for identifying the irrationality in the recording of inventory

transactions as the result of this can shows the problem area to the auditor. Lastly, any halt

request in inventory receiving from the warehouses needs to be tested for the exclusion of

irrelevant inventory items (Seidel, 2014).

Requirement c: ASA 701

ASA 701 Communicating Key Audit Matters

Definition: As per ASA 701, Key Audit Matters are the matters that are largely significant

for the audit of the financial statements of the current year (auasb.gov.au, 2019).

previous year’s sale in the current year’s inventory which create risk. For the presence of

these reasons, this assertion is at risk (Hussain and Al-Mourad, 2014).

Requirement b: Substantive Audit Procedures

First Risk: The requirement for the auditor is to observe and test the procedures include

under the physical inventory counting process. Specifically, the auditor must scrutinize the

physical inventory counting process when they are being progressing and they need to

examine the inventory count tags (Council, 2014). Most importantly, the auditor must involve

in the testing of the inventory in the six regional warehouses and needs to compare the results

with the confirmation from the central warehouse with the aim to find the error. In addition,

the auditor is needed to verify whether the company has followed the principles and standards

of AASB 116 for the accounting of their inventories. Lastly, the auditor must test the costing

process of the company to ensure the correct flow of inventory in the income statements as

cost of goods (Council, 2014).

Second Risk: With the aim to test this audit assertion, the auditor need to ensure the testing

of all the goods received to warehouses and goods delivered to suppliers notes so that the

errors in the cut offs can be identified (Seidel, 2014). The auditor must involve applying the

required analytical procedures for identifying the irrationality in the recording of inventory

transactions as the result of this can shows the problem area to the auditor. Lastly, any halt

request in inventory receiving from the warehouses needs to be tested for the exclusion of

irrelevant inventory items (Seidel, 2014).

Requirement c: ASA 701

ASA 701 Communicating Key Audit Matters

Definition: As per ASA 701, Key Audit Matters are the matters that are largely significant

for the audit of the financial statements of the current year (auasb.gov.au, 2019).

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

4AUDITING AND ASSURANCE SERVICES

Objective: As per ASA 701, the objectives of the auditors are to ascertain the key audit

matters, develop an opinion on the financial statements and communication of these matters

in the auditor’s report (auasb.gov.au, 2019).

Requirement: ASA 701 puts the obligation on the auditors to follow certain requirements in

the key audit matters. First, the auditor must consider the areas with high risk of material

misstatements in the financial statements. Second, the auditors are required to test the

significant judgments and assumptions of the management for analysing the uncertainty.

Third, they need to consider the effects of significant events and transactions on the audit

process (auasb.gov.au, 2019).

Benefits: The major benefit of ASA 701 is that it leads to establish effective communication

of key audit matters with the respective parties. After that, the principles of ASA 701 helps to

set up transparency in the process of financial reporting that eventually leads to the increase

in the quality of financial reporting (auasb.gov.au, 2019).

Determination Rationales

As per the regulation of ASA 701, the identified assertions at risks can be considered

as key audit matters due to the fact that the errors in the inventory valuation along with the

wrong recording of inventory can create material impact on the accounting books of

Advanced Computer Solutions (Wang, Yu and Zhao, 2014). After that, the used judgements

and assumptions by the management of the company are subject to uncertainty. Moreover,

the significant events that can impact the determination of key audit matters are the change in

the warehouse and the issues in accounting software as these aspects can lead to

misstatements in inventory transitions (Lee and Park, 2013).

Objective: As per ASA 701, the objectives of the auditors are to ascertain the key audit

matters, develop an opinion on the financial statements and communication of these matters

in the auditor’s report (auasb.gov.au, 2019).

Requirement: ASA 701 puts the obligation on the auditors to follow certain requirements in

the key audit matters. First, the auditor must consider the areas with high risk of material

misstatements in the financial statements. Second, the auditors are required to test the

significant judgments and assumptions of the management for analysing the uncertainty.

Third, they need to consider the effects of significant events and transactions on the audit

process (auasb.gov.au, 2019).

Benefits: The major benefit of ASA 701 is that it leads to establish effective communication

of key audit matters with the respective parties. After that, the principles of ASA 701 helps to

set up transparency in the process of financial reporting that eventually leads to the increase

in the quality of financial reporting (auasb.gov.au, 2019).

Determination Rationales

As per the regulation of ASA 701, the identified assertions at risks can be considered

as key audit matters due to the fact that the errors in the inventory valuation along with the

wrong recording of inventory can create material impact on the accounting books of

Advanced Computer Solutions (Wang, Yu and Zhao, 2014). After that, the used judgements

and assumptions by the management of the company are subject to uncertainty. Moreover,

the significant events that can impact the determination of key audit matters are the change in

the warehouse and the issues in accounting software as these aspects can lead to

misstatements in inventory transitions (Lee and Park, 2013).

5AUDITING AND ASSURANCE SERVICES

Required Disclosure

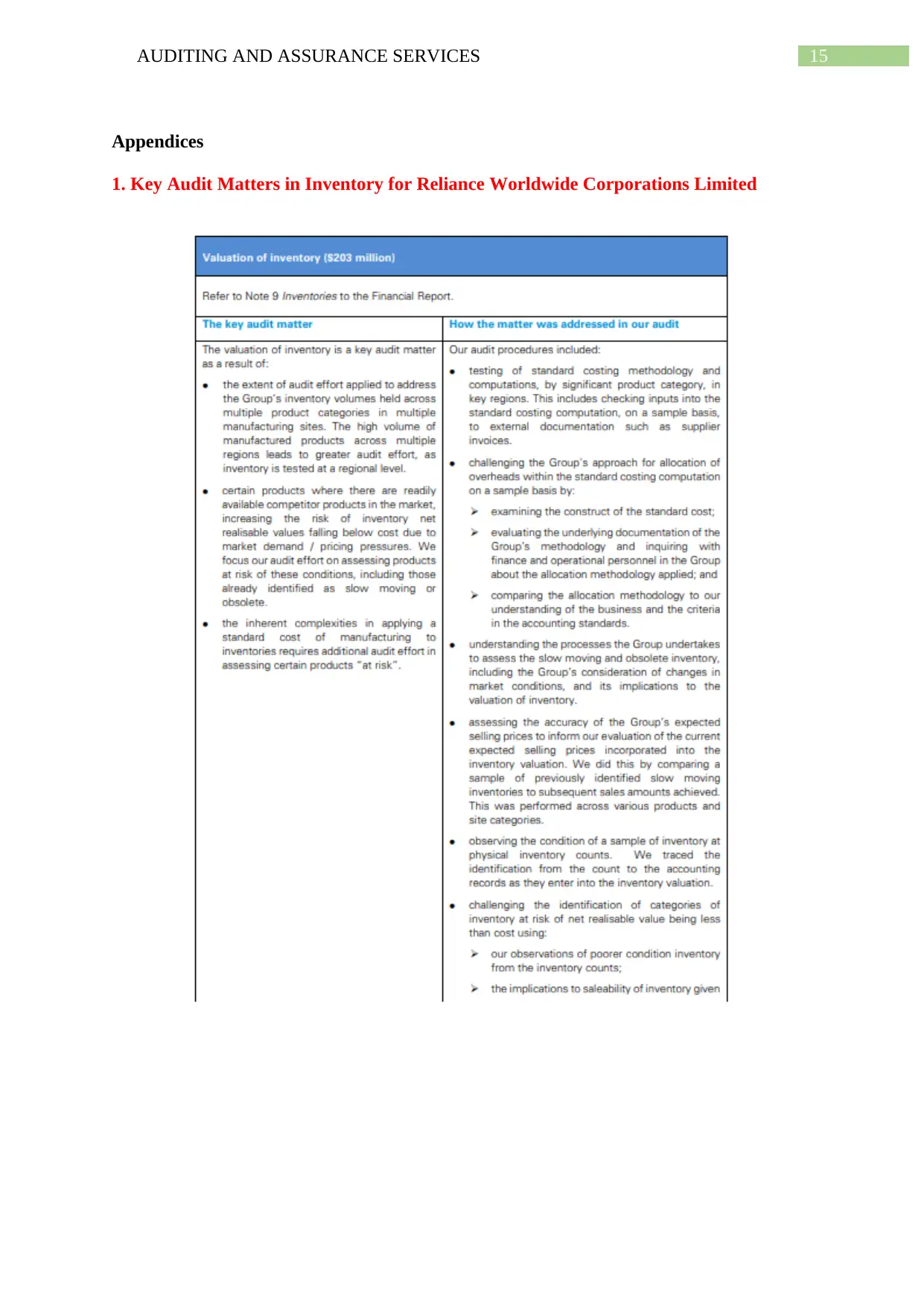

In this context, the example of Reliance Worldwide Corporation Limited can be

presented as the company also has inventories as one of the key audit matters. The auditors of

the company have considered inventory as key audit matter due to high volume of

manufactured products, increased risk of the fall of inventory realizable value below cost and

the presence of inherent complexities. The applied audit procedures are test of standard

costing methodology; understand the company’s process for assessing slow moving of

obsolete inventory, accuracy assessment of the company’s expected selling prices and others

(rwc.com, 2019). Almost same approach needs to be taken for Advanced Computer

Solutions.

Why Significant How Audit Addressed the Key Audit

Mattes

Valuation of Inventory after moving to

new warehouses on March 2018

It can be seen that the inventories of the

company have been transferred to six new

warehouses from a central warehouse that

can lead to the error in physical inventory

count and can create material misstatements

(auasb.gov.au, 2019).

The undertaken audit procedures are:

- Observe and test the procedures include

under the physical inventory counting

process

- Scrutinize the physical inventory counting

process

-Verifying the compliance with the standards

of AASB 116

- Testing of the inventory in the six regional

warehouses and needs to compare the results

with the confirmation from the central

warehouse (auasb.gov.au, 2019)

Inventory of 2018 includes the sales of

2017

It can be seen that sales of 2017 has been

included in the inventory of 2018 of the

company and it can create material effect on

the company as the management has used

The undertaken audit procedures are:

- Testing of all the goods received to

warehouses and goods delivered to suppliers

notes

- Applying the required analytical procedures

for identifying the irrationality in the

Required Disclosure

In this context, the example of Reliance Worldwide Corporation Limited can be

presented as the company also has inventories as one of the key audit matters. The auditors of

the company have considered inventory as key audit matter due to high volume of

manufactured products, increased risk of the fall of inventory realizable value below cost and

the presence of inherent complexities. The applied audit procedures are test of standard

costing methodology; understand the company’s process for assessing slow moving of

obsolete inventory, accuracy assessment of the company’s expected selling prices and others

(rwc.com, 2019). Almost same approach needs to be taken for Advanced Computer

Solutions.

Why Significant How Audit Addressed the Key Audit

Mattes

Valuation of Inventory after moving to

new warehouses on March 2018

It can be seen that the inventories of the

company have been transferred to six new

warehouses from a central warehouse that

can lead to the error in physical inventory

count and can create material misstatements

(auasb.gov.au, 2019).

The undertaken audit procedures are:

- Observe and test the procedures include

under the physical inventory counting

process

- Scrutinize the physical inventory counting

process

-Verifying the compliance with the standards

of AASB 116

- Testing of the inventory in the six regional

warehouses and needs to compare the results

with the confirmation from the central

warehouse (auasb.gov.au, 2019)

Inventory of 2018 includes the sales of

2017

It can be seen that sales of 2017 has been

included in the inventory of 2018 of the

company and it can create material effect on

the company as the management has used

The undertaken audit procedures are:

- Testing of all the goods received to

warehouses and goods delivered to suppliers

notes

- Applying the required analytical procedures

for identifying the irrationality in the

6AUDITING AND ASSURANCE SERVICES

certain assumptions and judgements in here.

For this reason, it is significant for the audit

of the company (auasb.gov.au, 2019).

recording of inventory transactions

- Consider the effects of significant events

and transactions on the audit process

(auasb.gov.au, 2019)

Question 2: Green Machine Ltd

Requirement a: Assertions

Accuracy: Errors in the transactions of property, plant and equipment can be identified with

the help of the assertion (Garcia-Blandon, Argilés‐Bosch and Martinez-Blasco, 2014). It puts

the obligation on the business organizations to ensure correct classification as well as

distinction between the capital and revenue expenditures for property, plant and equipment.

According to the provided information of Green Machine Ltd, certain revenue expenditures

are capitalized and certain capital expenditure are included in the income statements as

revenue expenses; and this transactions shows the improper classification as well as

distinction between the company’s revenue and capital expenditures (Garcia-Blandon,

Argilés‐Bosch and Martinez-Blasco, 2014). These incorrect transactions have effects on the

company’s income statements as it can misstate the company’s net profit (García Blandón

and Argilés Bosch, 2013). Hence, it can be said that this particular assertion is at risk.

Valuation: The auditors can ensure whether the assets, liabilities and equity have been

recorded with the proper value in the financial statements by examining this assertion. As per

this assertion, companies are needed to deduct the correct amount of accumulated

depreciation while reporting the property, plant and equipment at cost value (Lincke, 2015).

It demands the use of appropriate rate of depreciation. As per the information, Green

Machine Ltd has applied too low rate of depreciation which led to the decrease in the

expenditure of depreciation in the income statement. This reduction can lead to the reduction

certain assumptions and judgements in here.

For this reason, it is significant for the audit

of the company (auasb.gov.au, 2019).

recording of inventory transactions

- Consider the effects of significant events

and transactions on the audit process

(auasb.gov.au, 2019)

Question 2: Green Machine Ltd

Requirement a: Assertions

Accuracy: Errors in the transactions of property, plant and equipment can be identified with

the help of the assertion (Garcia-Blandon, Argilés‐Bosch and Martinez-Blasco, 2014). It puts

the obligation on the business organizations to ensure correct classification as well as

distinction between the capital and revenue expenditures for property, plant and equipment.

According to the provided information of Green Machine Ltd, certain revenue expenditures

are capitalized and certain capital expenditure are included in the income statements as

revenue expenses; and this transactions shows the improper classification as well as

distinction between the company’s revenue and capital expenditures (Garcia-Blandon,

Argilés‐Bosch and Martinez-Blasco, 2014). These incorrect transactions have effects on the

company’s income statements as it can misstate the company’s net profit (García Blandón

and Argilés Bosch, 2013). Hence, it can be said that this particular assertion is at risk.

Valuation: The auditors can ensure whether the assets, liabilities and equity have been

recorded with the proper value in the financial statements by examining this assertion. As per

this assertion, companies are needed to deduct the correct amount of accumulated

depreciation while reporting the property, plant and equipment at cost value (Lincke, 2015).

It demands the use of appropriate rate of depreciation. As per the information, Green

Machine Ltd has applied too low rate of depreciation which led to the decrease in the

expenditure of depreciation in the income statement. This reduction can lead to the reduction

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7AUDITING AND ASSURANCE SERVICES

in the operating expenses of the company that can sprightly contribute towards the

misstatements of net profit. At the same time, improper application of depreciation rate

indicates towards the fact that the company has not been able to report the correct value of

their property, plant and equipment in the financial statements (Johnson, Keune and Winchel,

2014). Hence, this assertion is at the risk.

Requirement b: Substantive Audit Procedures

First Risk: Due to the wrong division between the capital and revenue expenditures, there

can be material impacts on the company’s financial statements. Hence, the substantive audit

procedure is the review the property, plant and equipment related expenses in the company.

At the same time, reviewing the policies and procedures of the company for the capitalization

of the expenses related to property, plant and equipment is another crucial audit procedure

that the auditor needs to consider (Meleshenko and Usanova, 2014). After that, the auditor

needs to undertake evaluating the financial ratios and industry results. In case of the repair

and maintenance expenses, the need for the auditor is to review Green Machine Ltd’s policies

to ensure the aspect that whether the company has recorded them as expenses or they have

been capitalized. After that, the auditor needs to discuss about the company’s management

about the policies and procedures related to capital expenditures and revenue expenditures.

All these processes will make the auditor enable in assessing the fact that which revenue

expenses have been capitalized and which capital expenses have been recorded in profit and

loss account.

Second Risk: For this particular assertion risk, it is needed for the auditor of Green Machine

Ltd to conduct an investigation on the valuation procedure of property, plant and equipment

in the company. With the aim to ensure reasonableness in depreciation, the auditor needs t

ensure checking the fact that whether the useful lives of property, plant and equipment

reflects the rates of depreciation. The main responsibility of the auditor will be the

in the operating expenses of the company that can sprightly contribute towards the

misstatements of net profit. At the same time, improper application of depreciation rate

indicates towards the fact that the company has not been able to report the correct value of

their property, plant and equipment in the financial statements (Johnson, Keune and Winchel,

2014). Hence, this assertion is at the risk.

Requirement b: Substantive Audit Procedures

First Risk: Due to the wrong division between the capital and revenue expenditures, there

can be material impacts on the company’s financial statements. Hence, the substantive audit

procedure is the review the property, plant and equipment related expenses in the company.

At the same time, reviewing the policies and procedures of the company for the capitalization

of the expenses related to property, plant and equipment is another crucial audit procedure

that the auditor needs to consider (Meleshenko and Usanova, 2014). After that, the auditor

needs to undertake evaluating the financial ratios and industry results. In case of the repair

and maintenance expenses, the need for the auditor is to review Green Machine Ltd’s policies

to ensure the aspect that whether the company has recorded them as expenses or they have

been capitalized. After that, the auditor needs to discuss about the company’s management

about the policies and procedures related to capital expenditures and revenue expenditures.

All these processes will make the auditor enable in assessing the fact that which revenue

expenses have been capitalized and which capital expenses have been recorded in profit and

loss account.

Second Risk: For this particular assertion risk, it is needed for the auditor of Green Machine

Ltd to conduct an investigation on the valuation procedure of property, plant and equipment

in the company. With the aim to ensure reasonableness in depreciation, the auditor needs t

ensure checking the fact that whether the useful lives of property, plant and equipment

reflects the rates of depreciation. The main responsibility of the auditor will be the

8AUDITING AND ASSURANCE SERVICES

recalculation of the rate of depreciation by considering the residual value of property, plant

and equipment and whether there is any loss or profit due to the sale of these assets. Thus, for

addressing the accuracy, the requirement for the auditor is to ensure recalculating the

schedule of depreciation to make sure that the valuation and disclosures of property, plant

and equipment has been done correctly. After that, comparing the depreciation ratios need to

be done by the auditors in this process. With the aim to ensure consistency, the auditor is

required to check the past trends of depreciation rates and expenses for comparing them to

the current year’s results. After deriving the correct rate of depreciation, the auditor needs to

apply them for gaining the revised amount of depreciation expenses. This will help the

auditor in gaining the difference in the depreciation expenses (Carson, Fargher and Zhang,

2016).

Requirement c: ASA 701

ASA 701 Communicating Key Audit Matters

The principles of ASA 701 states that there are certain issues or matters that the

auditors consider significant for the audit of the financial statements and these are called the

Key Audit Matters. There are certain objectives of the auditors in dealing with the key audit

matters; they are determination of key audit matters, establishment of audit opinion and the

communication of the same (auasb.gov.au, 2019).

In addition, the auditors are needed to follow certain requirements under ASA 701.

The first requirement is to consider the areas with higher risk of material misstatements in the

financial statements as per ASA 315 (auasb.gov.au, 2019). After that, the auditors must

undertake the analysis of any uncertainties in the judgements and assumptions that the

auditors use for the preparation of financial statements. Lastly, it is also needed for the

auditor to evaluate the significant events or transactions for auditing (auasb.gov.au, 2019).

recalculation of the rate of depreciation by considering the residual value of property, plant

and equipment and whether there is any loss or profit due to the sale of these assets. Thus, for

addressing the accuracy, the requirement for the auditor is to ensure recalculating the

schedule of depreciation to make sure that the valuation and disclosures of property, plant

and equipment has been done correctly. After that, comparing the depreciation ratios need to

be done by the auditors in this process. With the aim to ensure consistency, the auditor is

required to check the past trends of depreciation rates and expenses for comparing them to

the current year’s results. After deriving the correct rate of depreciation, the auditor needs to

apply them for gaining the revised amount of depreciation expenses. This will help the

auditor in gaining the difference in the depreciation expenses (Carson, Fargher and Zhang,

2016).

Requirement c: ASA 701

ASA 701 Communicating Key Audit Matters

The principles of ASA 701 states that there are certain issues or matters that the

auditors consider significant for the audit of the financial statements and these are called the

Key Audit Matters. There are certain objectives of the auditors in dealing with the key audit

matters; they are determination of key audit matters, establishment of audit opinion and the

communication of the same (auasb.gov.au, 2019).

In addition, the auditors are needed to follow certain requirements under ASA 701.

The first requirement is to consider the areas with higher risk of material misstatements in the

financial statements as per ASA 315 (auasb.gov.au, 2019). After that, the auditors must

undertake the analysis of any uncertainties in the judgements and assumptions that the

auditors use for the preparation of financial statements. Lastly, it is also needed for the

auditor to evaluate the significant events or transactions for auditing (auasb.gov.au, 2019).

9AUDITING AND ASSURANCE SERVICES

The most important benefit of ASA 701 is that it can establish effective

communication of key audit matters with the key stakeholders. After that, the standard of

ASA 701 assists to set up clearness in the process of financial reporting that ultimately

contributes to the increase in the quality of financial reporting (auasb.gov.au, 2019).

Determination Rationales

It can be said after applying the principles of ASA 701 that the key assertions at risk

are the key audit matters in Green Machine Ltd because of the fact that wrong application of

depreciation rate and wrong distinction between expenses can misstate the net profit of the

company and can lead to material misstatements (Chen, He and Stice, 2016). At the same

time, the involvement of certain judgements and assumptions can be seen in the company that

can be uncertain in certain aspects. Hence, the presence of these reasons makes these risks as

key audit matters (Sun and Liu, 2014).

Required Disclosure

The example of Department of Defence can be presented in here where the auditors

have considered property, plant and equipment as key audit matter because of the

involvement of high level of management judgments in determining the fair value of these

assets along with the presence of subjectivity in the valuation assessment. The key audit

procedures taken by the auditors are the assessment of the appropriateness of fair value

measurement methodology, assessment of the applied useful lives of these assets with the

available information, testing the sample of cost attribution model and others

(defence.gov.au, 2019). Same types of procedures need to be followed in the case of Green

Machine Ltd.

Why Significant How Audit Addressed the Key Audit

The most important benefit of ASA 701 is that it can establish effective

communication of key audit matters with the key stakeholders. After that, the standard of

ASA 701 assists to set up clearness in the process of financial reporting that ultimately

contributes to the increase in the quality of financial reporting (auasb.gov.au, 2019).

Determination Rationales

It can be said after applying the principles of ASA 701 that the key assertions at risk

are the key audit matters in Green Machine Ltd because of the fact that wrong application of

depreciation rate and wrong distinction between expenses can misstate the net profit of the

company and can lead to material misstatements (Chen, He and Stice, 2016). At the same

time, the involvement of certain judgements and assumptions can be seen in the company that

can be uncertain in certain aspects. Hence, the presence of these reasons makes these risks as

key audit matters (Sun and Liu, 2014).

Required Disclosure

The example of Department of Defence can be presented in here where the auditors

have considered property, plant and equipment as key audit matter because of the

involvement of high level of management judgments in determining the fair value of these

assets along with the presence of subjectivity in the valuation assessment. The key audit

procedures taken by the auditors are the assessment of the appropriateness of fair value

measurement methodology, assessment of the applied useful lives of these assets with the

available information, testing the sample of cost attribution model and others

(defence.gov.au, 2019). Same types of procedures need to be followed in the case of Green

Machine Ltd.

Why Significant How Audit Addressed the Key Audit

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

10AUDITING AND ASSURANCE SERVICES

Mattes

Inappropriate division between revenue

and capital expenses

Some items were capitalized when they

should have been expensed and other capital

items were included in repairs and

maintenance in the income statement. It is

subject to the judgements and assumptions of

management and important for the audit of

the company (auasb.gov.au, 2019).

The undertaken audit procedures are:

- Review the property, plant and equipment

related expenses in the company

- Reviewing the policies and procedures of

the company for the capitalization of the

expenses related to property, plant and

equipment (auasb.gov.au, 2019)

-Evaluating the financial ratios and industry

results

-Review Green Machine Ltd’s policies to

ensure the aspect that whether the company

has recorded them as expenses or they have

been capitalized

-Discuss about the company’s management

about the policies and procedures related to

capital expenditures and revenue

expenditures (auasb.gov.au, 2019)

Low rate of depreciation has been charged

on property, plant and equipment

There is a range of depreciation rates within

categories and there has been concern that the

rates applied to some assets have been too

low. This can create material misstatements

in the financial statements and it involves

certain judgements as well as assumptions of

the management. Hence, it is significant for

the audit of the company (auasb.gov.au,

2019).

The undertaken audit procedures are:

-Checking the fact that whether the useful

lives of property, plant and equipment

reflects the rates of depreciation

-Recalculation of the rate of depreciation by

considering the residual value of property,

plant and equipment and whether there is any

loss or profit due to the sale of these assets

(auasb.gov.au, 2019)

-Recalculating the schedule of depreciation

- comparing the depreciation ratios

-Check the past trends of depreciation rates

and expenses for comparing them to the

current year’s results

-Application of the new depreciation rate to

Mattes

Inappropriate division between revenue

and capital expenses

Some items were capitalized when they

should have been expensed and other capital

items were included in repairs and

maintenance in the income statement. It is

subject to the judgements and assumptions of

management and important for the audit of

the company (auasb.gov.au, 2019).

The undertaken audit procedures are:

- Review the property, plant and equipment

related expenses in the company

- Reviewing the policies and procedures of

the company for the capitalization of the

expenses related to property, plant and

equipment (auasb.gov.au, 2019)

-Evaluating the financial ratios and industry

results

-Review Green Machine Ltd’s policies to

ensure the aspect that whether the company

has recorded them as expenses or they have

been capitalized

-Discuss about the company’s management

about the policies and procedures related to

capital expenditures and revenue

expenditures (auasb.gov.au, 2019)

Low rate of depreciation has been charged

on property, plant and equipment

There is a range of depreciation rates within

categories and there has been concern that the

rates applied to some assets have been too

low. This can create material misstatements

in the financial statements and it involves

certain judgements as well as assumptions of

the management. Hence, it is significant for

the audit of the company (auasb.gov.au,

2019).

The undertaken audit procedures are:

-Checking the fact that whether the useful

lives of property, plant and equipment

reflects the rates of depreciation

-Recalculation of the rate of depreciation by

considering the residual value of property,

plant and equipment and whether there is any

loss or profit due to the sale of these assets

(auasb.gov.au, 2019)

-Recalculating the schedule of depreciation

- comparing the depreciation ratios

-Check the past trends of depreciation rates

and expenses for comparing them to the

current year’s results

-Application of the new depreciation rate to

11AUDITING AND ASSURANCE SERVICES

gain the revised depreciation expenses

(auasb.gov.au, 2019)

gain the revised depreciation expenses

(auasb.gov.au, 2019)

12AUDITING AND ASSURANCE SERVICES

References

Auasb.gov.au. 2019. [online] Available at:

https://www.auasb.gov.au/admin/file/content102/c3/ASA_701_2015.pdf [Accessed 18 Jan.

2019].

Carson, E., Fargher, N. and Zhang, Y., 2016. Trends in auditor reporting in Australia: a

synthesis and opportunities for research. Australian Accounting Review, 26(3), pp.226-242.

Chen, P.F., He, S., Ma, Z. and Stice, D., 2016. The information role of audit opinions in debt

contracting. Journal of Accounting and Economics, 61(1), pp.121-144.

Council, F.R., 2014. Audit Quality Inspections Annual Report 2011/12. London: FRC.

Defence.gov.au. 2019. Annual Report 2017-18. [online] Available at:

http://www.defence.gov.au/annualreports/17-18/Downloads/DAR_2017-18_Complete.pdf

[Accessed 23 Jan. 2019].

Dowling, C. and Leech, S.A., 2014. A Big 4 firm's use of information technology to control

the audit process: How an audit support system is changing auditor behavior. Contemporary

Accounting Research, 31(1), pp.230-252.

García Blandón, J. and Argilés Bosch, J.M., 2013. Audit tenure and audit Qualifications in a

low litigation risk setting: An analysis of the Spanish market. Estudios de Economía, 40(2),

pp.133-156.

Garcia-Blandon, J., Argilés‐Bosch, J. and Martinez-Blasco, M., 2014. Audit Firm Tenure and

Audit Qualifications in Spain: A Multinomial Approach.

Hussain, M. and Al-Mourad, M.B., 2014, May. Effective Third Party Auditing in Cloud

Computing. In Advanced Information Networking and Applications Workshops (WAINA),

2014 28th International Conference on (pp. 91-95). IEEE.

References

Auasb.gov.au. 2019. [online] Available at:

https://www.auasb.gov.au/admin/file/content102/c3/ASA_701_2015.pdf [Accessed 18 Jan.

2019].

Carson, E., Fargher, N. and Zhang, Y., 2016. Trends in auditor reporting in Australia: a

synthesis and opportunities for research. Australian Accounting Review, 26(3), pp.226-242.

Chen, P.F., He, S., Ma, Z. and Stice, D., 2016. The information role of audit opinions in debt

contracting. Journal of Accounting and Economics, 61(1), pp.121-144.

Council, F.R., 2014. Audit Quality Inspections Annual Report 2011/12. London: FRC.

Defence.gov.au. 2019. Annual Report 2017-18. [online] Available at:

http://www.defence.gov.au/annualreports/17-18/Downloads/DAR_2017-18_Complete.pdf

[Accessed 23 Jan. 2019].

Dowling, C. and Leech, S.A., 2014. A Big 4 firm's use of information technology to control

the audit process: How an audit support system is changing auditor behavior. Contemporary

Accounting Research, 31(1), pp.230-252.

García Blandón, J. and Argilés Bosch, J.M., 2013. Audit tenure and audit Qualifications in a

low litigation risk setting: An analysis of the Spanish market. Estudios de Economía, 40(2),

pp.133-156.

Garcia-Blandon, J., Argilés‐Bosch, J. and Martinez-Blasco, M., 2014. Audit Firm Tenure and

Audit Qualifications in Spain: A Multinomial Approach.

Hussain, M. and Al-Mourad, M.B., 2014, May. Effective Third Party Auditing in Cloud

Computing. In Advanced Information Networking and Applications Workshops (WAINA),

2014 28th International Conference on (pp. 91-95). IEEE.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

13AUDITING AND ASSURANCE SERVICES

Johnson, L.M., Keune, M.B. and Winchel, J., 2014. Auditor perceptions of the PCAOB

oversight process. Working paper, University of Tennessee, University of Dayton, and

University of Virginia.

Lee, C. and Park, M.S., 2013. Subjectivity in fair-value estimates, audit quality, and

informativeness of other comprehensive income. Advances in accounting, 29(2), pp.218-231.

Lincke, S., 2015. Performing an Audit or Security Test. In Security Planning (pp. 217-234).

Springer, Cham.

Meleshenko, S.S. and Usanova, D.S., 2014. Methodological Approaches to the Assessing of

the Quality of Audit Sampling. Mediterranean Journal of Social Sciences, 5(24), p.176.

Rwc.com. 2019. Results for announcement to the market. [online] Available at:

http://www.rwc.com/wp-content/uploads/2018/08/Appendix-4E-and-Financial-Report-FOR-

RELEASE.pdf [Accessed 23 Jan. 2019].

Seidel, T.A., 2014. The effective use of the audit risk model at the account level.

Smieliauskas, W., 2013. Argument, audit and principles-based accounting,[in:] (pp. 228-

241). Routledge, London.

Sun, J. and Liu, G., 2014. Audit committees’ oversight of bank risk-taking. Journal of

Banking & Finance, 40, pp.376-387.

Tan, B.S., 2015. The value of audit and the economic history of market. International

Journal of Economics and Accounting, 6(4), pp.346-351.

Titera, W.R., 2013. Updating audit standard—Enabling audit data analysis. Journal of Information

Systems, 27(1), pp.325-331.

Johnson, L.M., Keune, M.B. and Winchel, J., 2014. Auditor perceptions of the PCAOB

oversight process. Working paper, University of Tennessee, University of Dayton, and

University of Virginia.

Lee, C. and Park, M.S., 2013. Subjectivity in fair-value estimates, audit quality, and

informativeness of other comprehensive income. Advances in accounting, 29(2), pp.218-231.

Lincke, S., 2015. Performing an Audit or Security Test. In Security Planning (pp. 217-234).

Springer, Cham.

Meleshenko, S.S. and Usanova, D.S., 2014. Methodological Approaches to the Assessing of

the Quality of Audit Sampling. Mediterranean Journal of Social Sciences, 5(24), p.176.

Rwc.com. 2019. Results for announcement to the market. [online] Available at:

http://www.rwc.com/wp-content/uploads/2018/08/Appendix-4E-and-Financial-Report-FOR-

RELEASE.pdf [Accessed 23 Jan. 2019].

Seidel, T.A., 2014. The effective use of the audit risk model at the account level.

Smieliauskas, W., 2013. Argument, audit and principles-based accounting,[in:] (pp. 228-

241). Routledge, London.

Sun, J. and Liu, G., 2014. Audit committees’ oversight of bank risk-taking. Journal of

Banking & Finance, 40, pp.376-387.

Tan, B.S., 2015. The value of audit and the economic history of market. International

Journal of Economics and Accounting, 6(4), pp.346-351.

Titera, W.R., 2013. Updating audit standard—Enabling audit data analysis. Journal of Information

Systems, 27(1), pp.325-331.

14AUDITING AND ASSURANCE SERVICES

Wang, Y., Yu, L. and Zhao, Y., 2014. The association between audit-partner quality and

engagement quality: Evidence from financial report misstatements. Auditing: A Journal of

Practice & Theory, 34(3), pp.81-111.

Wang, Y., Yu, L. and Zhao, Y., 2014. The association between audit-partner quality and

engagement quality: Evidence from financial report misstatements. Auditing: A Journal of

Practice & Theory, 34(3), pp.81-111.

15AUDITING AND ASSURANCE SERVICES

Appendices

1. Key Audit Matters in Inventory for Reliance Worldwide Corporations Limited

Appendices

1. Key Audit Matters in Inventory for Reliance Worldwide Corporations Limited

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

16AUDITING AND ASSURANCE SERVICES

(Source: rwc.com, 2019)

(Source: rwc.com, 2019)

17AUDITING AND ASSURANCE SERVICES

2. Key Audit Matters in Property, Plant and Equipment for Department of Deference

(Source: defence.gov.au, 2019)

2. Key Audit Matters in Property, Plant and Equipment for Department of Deference

(Source: defence.gov.au, 2019)

1 out of 18

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.