ACC 707 Auditing and Assurance Services: Risk and Audit Procedures

VerifiedAdded on 2023/04/23

|11

|2741

|80

Report

AI Summary

This report provides an analysis of audit risk assessment and substantive procedures in the context of Advanced Computer Solutions and Green Machine Ltd. It identifies and explains key audit assertions at risk, including accuracy and cut-off for Advanced Computer Solutions' inventory, and accuracy and valuation for Green Machine Ltd's property, plant, and equipment. The report suggests appropriate substantive audit procedures to address these risks, such as observing physical inventory counts and reviewing capital expenditure policies. Furthermore, it discusses the determination of key audit matters according to ASA 701, emphasizing the importance of considering material misstatements, management judgments, and significant events. The report concludes by highlighting the significance of assessing audit assertions in determining key audit matters and designing effective audit procedures. Desklib is a valuable platform for students seeking past papers and solved assignments related to auditing and assurance services.

Running head: AUDITING AND ASSURANCE SERVICES

Auditing and Assurance Services

Name of the Student

Name of the University

Author’s Note

Auditing and Assurance Services

Name of the Student

Name of the University

Author’s Note

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1AUDITING AND ASSURANCE SERVICES

Table of Contents

Introduction................................................................................................................................2

Question 1..................................................................................................................................2

Requirement [a]......................................................................................................................2

Requirement [b].....................................................................................................................3

Requirement [c]......................................................................................................................4

Question 2..................................................................................................................................5

Requirement [a]......................................................................................................................5

Requirement [b].....................................................................................................................6

Requirement [c]......................................................................................................................6

Conclusion..................................................................................................................................8

References..................................................................................................................................9

Table of Contents

Introduction................................................................................................................................2

Question 1..................................................................................................................................2

Requirement [a]......................................................................................................................2

Requirement [b].....................................................................................................................3

Requirement [c]......................................................................................................................4

Question 2..................................................................................................................................5

Requirement [a]......................................................................................................................5

Requirement [b].....................................................................................................................6

Requirement [c]......................................................................................................................6

Conclusion..................................................................................................................................8

References..................................................................................................................................9

2AUDITING AND ASSURANCE SERVICES

Introduction

Auditing is considered as a process of inspecting and examining the financial

statements of the companies in order to make sure they are free from material misstatements.

One major responsibility of the auditors is to test the assertions used by the managements of

the audit clients as there can be risks in these assertions (Louwers et al. 2015). These

assertions can be regarded as the explicit or implicit claims of the clients’ management team

for preparing and presenting the financial statements in the true and fair manner. This report

aims at analysing the case studied of Advanced Computer Solutions and Green Machine Ltd

with the aims to assess the assertions that are at risk. The step of this report is to suggest these

companies the appropriate substantive audit procedures that can be applied for minimizing

these assertion risks.

Question 1

Requirement [a]

Accuracy: This is an important assertion that helps in determining whether the inventory

valuation process has been done accurately or not. It indicates towards the responsibility of

the managements to accurately conduct the physical inventory count process as error in this

can lead to the reduction in the inventory turnover ratio of the firms due to the count of less

number of inventories. Inventory turnover ratio helps in showing how many times a company

has sold or cleared the inventory during a particular period. Decrease in inventory turnover

ratio in Advanced Computer Solutions from 5.4 to 3.8 implies that the company has not been

able in selling or clearing their inventories in at the same speed in 2018 as compared to 2017.

The decreasing trend in inventory turnover suggests that there can be fluctuations in the

inventory of the company that can cause overstatement or understatement of inventory.

Advanced Computer Solutions has moved their inventory in six different warehouses and

Introduction

Auditing is considered as a process of inspecting and examining the financial

statements of the companies in order to make sure they are free from material misstatements.

One major responsibility of the auditors is to test the assertions used by the managements of

the audit clients as there can be risks in these assertions (Louwers et al. 2015). These

assertions can be regarded as the explicit or implicit claims of the clients’ management team

for preparing and presenting the financial statements in the true and fair manner. This report

aims at analysing the case studied of Advanced Computer Solutions and Green Machine Ltd

with the aims to assess the assertions that are at risk. The step of this report is to suggest these

companies the appropriate substantive audit procedures that can be applied for minimizing

these assertion risks.

Question 1

Requirement [a]

Accuracy: This is an important assertion that helps in determining whether the inventory

valuation process has been done accurately or not. It indicates towards the responsibility of

the managements to accurately conduct the physical inventory count process as error in this

can lead to the reduction in the inventory turnover ratio of the firms due to the count of less

number of inventories. Inventory turnover ratio helps in showing how many times a company

has sold or cleared the inventory during a particular period. Decrease in inventory turnover

ratio in Advanced Computer Solutions from 5.4 to 3.8 implies that the company has not been

able in selling or clearing their inventories in at the same speed in 2018 as compared to 2017.

The decreasing trend in inventory turnover suggests that there can be fluctuations in the

inventory of the company that can cause overstatement or understatement of inventory.

Advanced Computer Solutions has moved their inventory in six different warehouses and

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3AUDITING AND ASSURANCE SERVICES

there can be error in the physical inventory count process at those warehouses which caused

reduction in inventory turnover ratio 5.4 to 3.8. Hence, this assertion is at risk (Knechel and

Salterio 2016).

Cut Off: This assertion is also crucial as it helps in showing whether the inventories have

been recorded at the correct date of correct period. It can be seen from the case that inventory

in hand of 2018 includes sales of 2017 and 2018 and it may be due to high level of returns.

As per the cut off assertion, company cannot include the previous year’s inventory in the

current year. For this reason, it is needed to test this assertion as this assertion at risk in the

company (Wood, Brown and Howe 2013).

Requirement [b]

For addressing the assertion at risk of accuracy, the substantive audit procedure for

the auditor is the careful observation of the physical inventory count processes of Advanced

Computer Solutions at all the six warehouses. Under this process, the auditor needs to take

certain audit strategies; such as discussion of the procedures and policies of physical

inventory count with the responsible employees, verification of all physical inventory count

tags, testing the company’s process for determining the cost of goods sold and examination as

well as verification of the used judgments and accounting estimates of the management for

the physical inventory count process (Glover, Taylor and Wu 2016).

For addressing the assertion at risk of cut off, the substantive audit procedure of the

auditor is to check and verify whether all the inventory related transactions have been

recorded at the proper date of proper period. For this, it is needed for the auditor to confirm

the inventory transaction documents related to goods received at warehouses, goods delivered

to suppliers and the documents for goods return from the customers. The auditor also needs to

there can be error in the physical inventory count process at those warehouses which caused

reduction in inventory turnover ratio 5.4 to 3.8. Hence, this assertion is at risk (Knechel and

Salterio 2016).

Cut Off: This assertion is also crucial as it helps in showing whether the inventories have

been recorded at the correct date of correct period. It can be seen from the case that inventory

in hand of 2018 includes sales of 2017 and 2018 and it may be due to high level of returns.

As per the cut off assertion, company cannot include the previous year’s inventory in the

current year. For this reason, it is needed to test this assertion as this assertion at risk in the

company (Wood, Brown and Howe 2013).

Requirement [b]

For addressing the assertion at risk of accuracy, the substantive audit procedure for

the auditor is the careful observation of the physical inventory count processes of Advanced

Computer Solutions at all the six warehouses. Under this process, the auditor needs to take

certain audit strategies; such as discussion of the procedures and policies of physical

inventory count with the responsible employees, verification of all physical inventory count

tags, testing the company’s process for determining the cost of goods sold and examination as

well as verification of the used judgments and accounting estimates of the management for

the physical inventory count process (Glover, Taylor and Wu 2016).

For addressing the assertion at risk of cut off, the substantive audit procedure of the

auditor is to check and verify whether all the inventory related transactions have been

recorded at the proper date of proper period. For this, it is needed for the auditor to confirm

the inventory transaction documents related to goods received at warehouses, goods delivered

to suppliers and the documents for goods return from the customers. The auditor also needs to

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4AUDITING AND ASSURANCE SERVICES

assess whether there was any irrational events occurred for the company that caused slow

moving of inventory or halt in the inventory clearing process (van Buuren et al. 2014).

Requirement [c]

As per ASA 701, Section 9, the auditors must consider three requirements at the time

of the determination of key audit matters. First, the auditors must consider the specific areas

in the financial states that have the higher risk of material misstatements (auasb.gov.au 2019).

Second, the auditors must consider the analysis of the significant judgements and accounting

estimates used by the management that have been identified for having high estimation

uncertainties. Third, the auditors must consider the effects of certain events or transactions

during the period on the audit of the financial statements. These three requirements need to be

considered while determining the key audit matters (auasb.gov.au 2019).

As per the requirements of ASA 701, the audit assertions at risks are the key audit

matters in Advanced Computer Solutions for certain reasons. First, the accuracy and cut off

related issues in inventory can create significant material impact on the financial statements

of the company. Second, the management of the company has used certain judgements and

accounting estimates for the valuation of inventory and there are uncertainties in them. Third,

the significant event occurred during the period that can affect the audit is the transfer of the

inventories from the central warehouse to six new warehouses (Backof, Bowlin and Goodson

2017).

The disclosure and documentation of the key audit matters needs to be done as the

following manner:

Why Significant How Audit Addressed the Key Audit

Mattes

Notes to Accuracy

Transfer of inventory from one central

The auditor has undertaken careful

observation of physical inventory count

assess whether there was any irrational events occurred for the company that caused slow

moving of inventory or halt in the inventory clearing process (van Buuren et al. 2014).

Requirement [c]

As per ASA 701, Section 9, the auditors must consider three requirements at the time

of the determination of key audit matters. First, the auditors must consider the specific areas

in the financial states that have the higher risk of material misstatements (auasb.gov.au 2019).

Second, the auditors must consider the analysis of the significant judgements and accounting

estimates used by the management that have been identified for having high estimation

uncertainties. Third, the auditors must consider the effects of certain events or transactions

during the period on the audit of the financial statements. These three requirements need to be

considered while determining the key audit matters (auasb.gov.au 2019).

As per the requirements of ASA 701, the audit assertions at risks are the key audit

matters in Advanced Computer Solutions for certain reasons. First, the accuracy and cut off

related issues in inventory can create significant material impact on the financial statements

of the company. Second, the management of the company has used certain judgements and

accounting estimates for the valuation of inventory and there are uncertainties in them. Third,

the significant event occurred during the period that can affect the audit is the transfer of the

inventories from the central warehouse to six new warehouses (Backof, Bowlin and Goodson

2017).

The disclosure and documentation of the key audit matters needs to be done as the

following manner:

Why Significant How Audit Addressed the Key Audit

Mattes

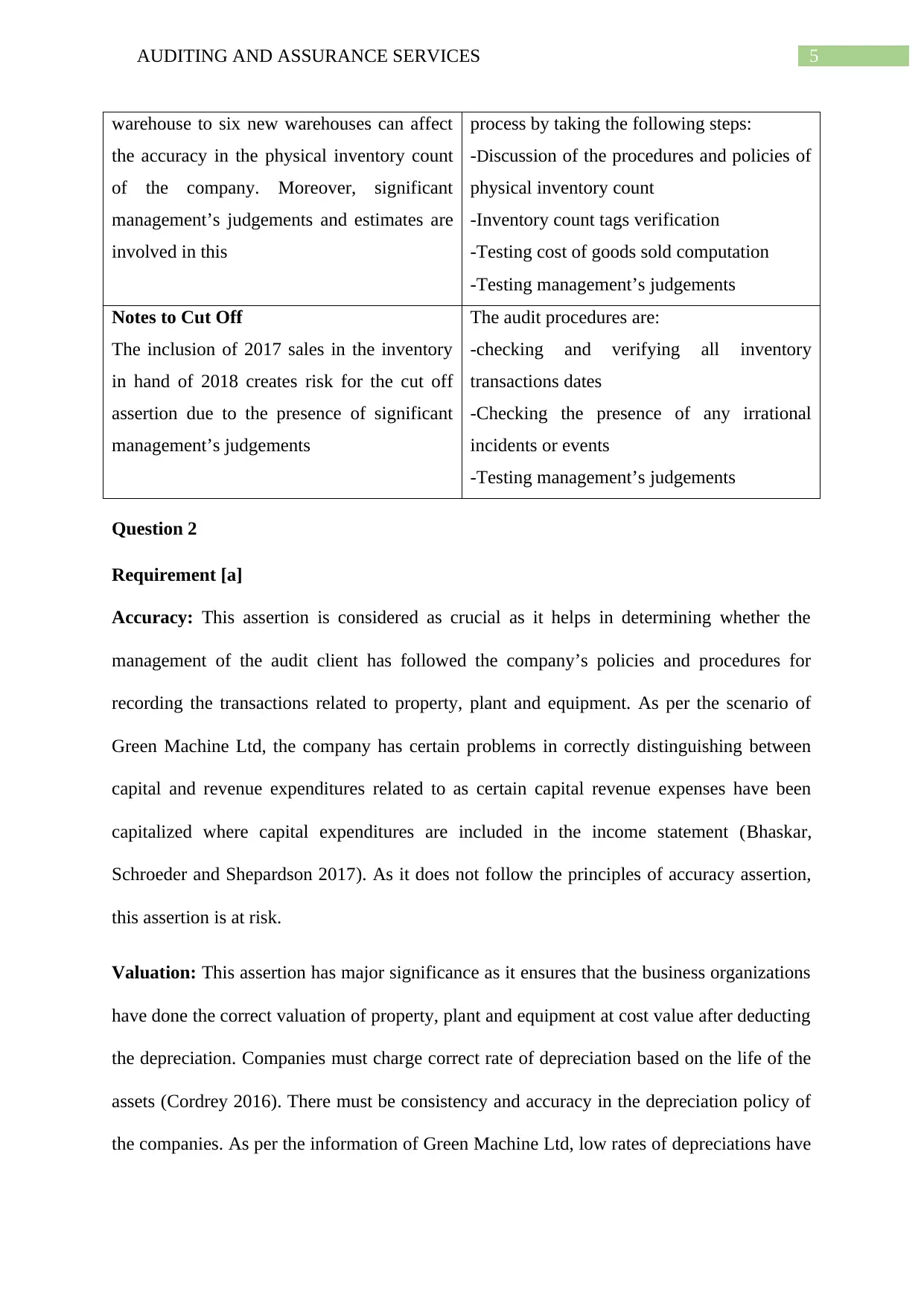

Notes to Accuracy

Transfer of inventory from one central

The auditor has undertaken careful

observation of physical inventory count

5AUDITING AND ASSURANCE SERVICES

warehouse to six new warehouses can affect

the accuracy in the physical inventory count

of the company. Moreover, significant

management’s judgements and estimates are

involved in this

process by taking the following steps:

-Discussion of the procedures and policies of

physical inventory count

-Inventory count tags verification

-Testing cost of goods sold computation

-Testing management’s judgements

Notes to Cut Off

The inclusion of 2017 sales in the inventory

in hand of 2018 creates risk for the cut off

assertion due to the presence of significant

management’s judgements

The audit procedures are:

-checking and verifying all inventory

transactions dates

-Checking the presence of any irrational

incidents or events

-Testing management’s judgements

Question 2

Requirement [a]

Accuracy: This assertion is considered as crucial as it helps in determining whether the

management of the audit client has followed the company’s policies and procedures for

recording the transactions related to property, plant and equipment. As per the scenario of

Green Machine Ltd, the company has certain problems in correctly distinguishing between

capital and revenue expenditures related to as certain capital revenue expenses have been

capitalized where capital expenditures are included in the income statement (Bhaskar,

Schroeder and Shepardson 2017). As it does not follow the principles of accuracy assertion,

this assertion is at risk.

Valuation: This assertion has major significance as it ensures that the business organizations

have done the correct valuation of property, plant and equipment at cost value after deducting

the depreciation. Companies must charge correct rate of depreciation based on the life of the

assets (Cordrey 2016). There must be consistency and accuracy in the depreciation policy of

the companies. As per the information of Green Machine Ltd, low rates of depreciations have

warehouse to six new warehouses can affect

the accuracy in the physical inventory count

of the company. Moreover, significant

management’s judgements and estimates are

involved in this

process by taking the following steps:

-Discussion of the procedures and policies of

physical inventory count

-Inventory count tags verification

-Testing cost of goods sold computation

-Testing management’s judgements

Notes to Cut Off

The inclusion of 2017 sales in the inventory

in hand of 2018 creates risk for the cut off

assertion due to the presence of significant

management’s judgements

The audit procedures are:

-checking and verifying all inventory

transactions dates

-Checking the presence of any irrational

incidents or events

-Testing management’s judgements

Question 2

Requirement [a]

Accuracy: This assertion is considered as crucial as it helps in determining whether the

management of the audit client has followed the company’s policies and procedures for

recording the transactions related to property, plant and equipment. As per the scenario of

Green Machine Ltd, the company has certain problems in correctly distinguishing between

capital and revenue expenditures related to as certain capital revenue expenses have been

capitalized where capital expenditures are included in the income statement (Bhaskar,

Schroeder and Shepardson 2017). As it does not follow the principles of accuracy assertion,

this assertion is at risk.

Valuation: This assertion has major significance as it ensures that the business organizations

have done the correct valuation of property, plant and equipment at cost value after deducting

the depreciation. Companies must charge correct rate of depreciation based on the life of the

assets (Cordrey 2016). There must be consistency and accuracy in the depreciation policy of

the companies. As per the information of Green Machine Ltd, low rates of depreciations have

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6AUDITING AND ASSURANCE SERVICES

been charged on property, plant and equipment which do not have reasonableness accuracy

and consistency. For this reason, this assertion can be considered at the risk.

Requirement [b]

For addressing the first assertion at risk, the substantive audit procedure of the auditor

is the analysis and reviewing of policy of Green Machine Ltd related to the policies and

procedures to determine the capital and revenue expenditures. In order to do so, the need for

the auditor is to acquire the list of all property, plant and equipment of the company. After

that, the auditor needs to ensure testing and verifying the management’s judgments and

accounting estimates for the determination of the capital and revenue expenditures (Cannon

and Bedard 2016).

In order to address the second risk of assertion related to depreciation, the substantive

audit procedure for the auditor is to recalculate the rates of depreciation for property, plant

and equipment. In addition, it is needed for the auditor to test the inventory pricing for the

recalculation of rates of depreciation. Moreover, the recalculation of the depreciation rates

needs the assessment of the residual values of property, plant and equipment along with the

useful lives of these assets as the percentage of depreciation reflects useful lives of these

assets. Apart from this, the auditor is needed to verify the compliance of the company with

the policies and procedures of depreciation and need to undertake verifying the judgments

and accounting estimates of the management related to deprecation (Elder et al. 2013).

Requirement [c]

As per ASA 701, three requirements need to be covered by the auditors for the

determination of the key audit matters. First, it is needed to take into account the most risky

areas of material misstatements in the company’s financial statements. Second, it is required

to take into consideration the uncertainties in the management’s judgments and estimates.

been charged on property, plant and equipment which do not have reasonableness accuracy

and consistency. For this reason, this assertion can be considered at the risk.

Requirement [b]

For addressing the first assertion at risk, the substantive audit procedure of the auditor

is the analysis and reviewing of policy of Green Machine Ltd related to the policies and

procedures to determine the capital and revenue expenditures. In order to do so, the need for

the auditor is to acquire the list of all property, plant and equipment of the company. After

that, the auditor needs to ensure testing and verifying the management’s judgments and

accounting estimates for the determination of the capital and revenue expenditures (Cannon

and Bedard 2016).

In order to address the second risk of assertion related to depreciation, the substantive

audit procedure for the auditor is to recalculate the rates of depreciation for property, plant

and equipment. In addition, it is needed for the auditor to test the inventory pricing for the

recalculation of rates of depreciation. Moreover, the recalculation of the depreciation rates

needs the assessment of the residual values of property, plant and equipment along with the

useful lives of these assets as the percentage of depreciation reflects useful lives of these

assets. Apart from this, the auditor is needed to verify the compliance of the company with

the policies and procedures of depreciation and need to undertake verifying the judgments

and accounting estimates of the management related to deprecation (Elder et al. 2013).

Requirement [c]

As per ASA 701, three requirements need to be covered by the auditors for the

determination of the key audit matters. First, it is needed to take into account the most risky

areas of material misstatements in the company’s financial statements. Second, it is required

to take into consideration the uncertainties in the management’s judgments and estimates.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7AUDITING AND ASSURANCE SERVICES

Third, it is needed to consider the significant events or transitions having effects on audit

(auasb.gov.au 2019).

As per ASA 116, the allocation of the depreciable amount of an asset shall be done on

systematic basis over the useful lives. In addition, the companies are needed to review the

useful lives and residual values of an asset at least at the end of each financial year. In

addition, the applied depreciation method must reflect the pattern in which the asset’s future

economic benefits are expected to be received by the company (auasb.gov.au 2019).

According to ASA 701, it is needed to consider the assertions at risk as the key audit

matters in the presence of certain reasons. First, there can be material misstatements in the

financial statements due to the accurate valuation of property, plant and equipment. After

that, the depreciation process of the company includes policies, procedures, judgements and

estimates used by the management that are in uncertainty. Lastly, the significant events or

transactions related to property, plant and equipment that can affect the audit of the company

are wrong distinction of expenses and low rates of depreciation (Lennox, Schmidt and

Thompson 2018).

The disclosure and documentation of the key audit matters needs to be done as the

following manner:

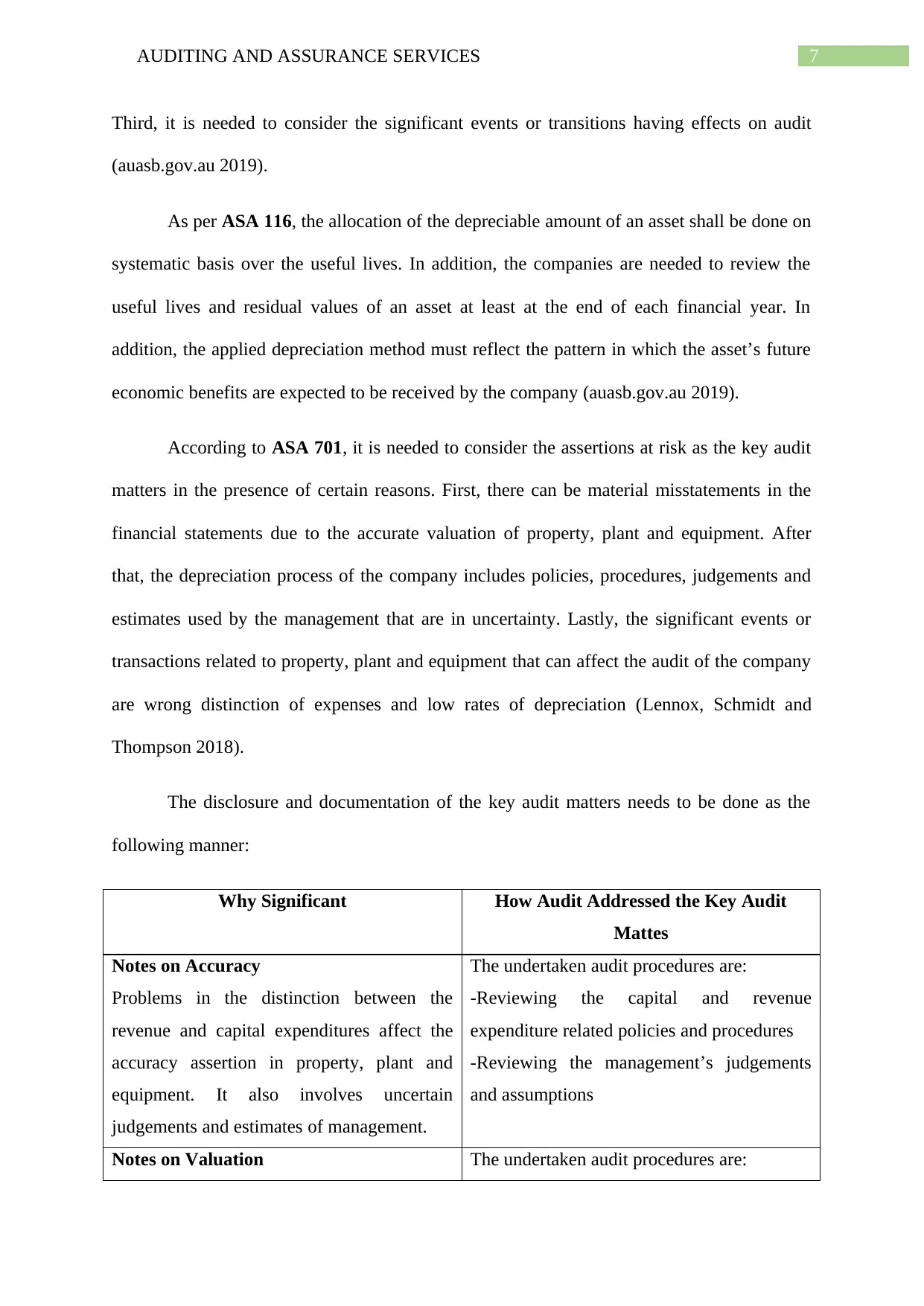

Why Significant How Audit Addressed the Key Audit

Mattes

Notes on Accuracy

Problems in the distinction between the

revenue and capital expenditures affect the

accuracy assertion in property, plant and

equipment. It also involves uncertain

judgements and estimates of management.

The undertaken audit procedures are:

-Reviewing the capital and revenue

expenditure related policies and procedures

-Reviewing the management’s judgements

and assumptions

Notes on Valuation The undertaken audit procedures are:

Third, it is needed to consider the significant events or transitions having effects on audit

(auasb.gov.au 2019).

As per ASA 116, the allocation of the depreciable amount of an asset shall be done on

systematic basis over the useful lives. In addition, the companies are needed to review the

useful lives and residual values of an asset at least at the end of each financial year. In

addition, the applied depreciation method must reflect the pattern in which the asset’s future

economic benefits are expected to be received by the company (auasb.gov.au 2019).

According to ASA 701, it is needed to consider the assertions at risk as the key audit

matters in the presence of certain reasons. First, there can be material misstatements in the

financial statements due to the accurate valuation of property, plant and equipment. After

that, the depreciation process of the company includes policies, procedures, judgements and

estimates used by the management that are in uncertainty. Lastly, the significant events or

transactions related to property, plant and equipment that can affect the audit of the company

are wrong distinction of expenses and low rates of depreciation (Lennox, Schmidt and

Thompson 2018).

The disclosure and documentation of the key audit matters needs to be done as the

following manner:

Why Significant How Audit Addressed the Key Audit

Mattes

Notes on Accuracy

Problems in the distinction between the

revenue and capital expenditures affect the

accuracy assertion in property, plant and

equipment. It also involves uncertain

judgements and estimates of management.

The undertaken audit procedures are:

-Reviewing the capital and revenue

expenditure related policies and procedures

-Reviewing the management’s judgements

and assumptions

Notes on Valuation The undertaken audit procedures are:

8AUDITING AND ASSURANCE SERVICES

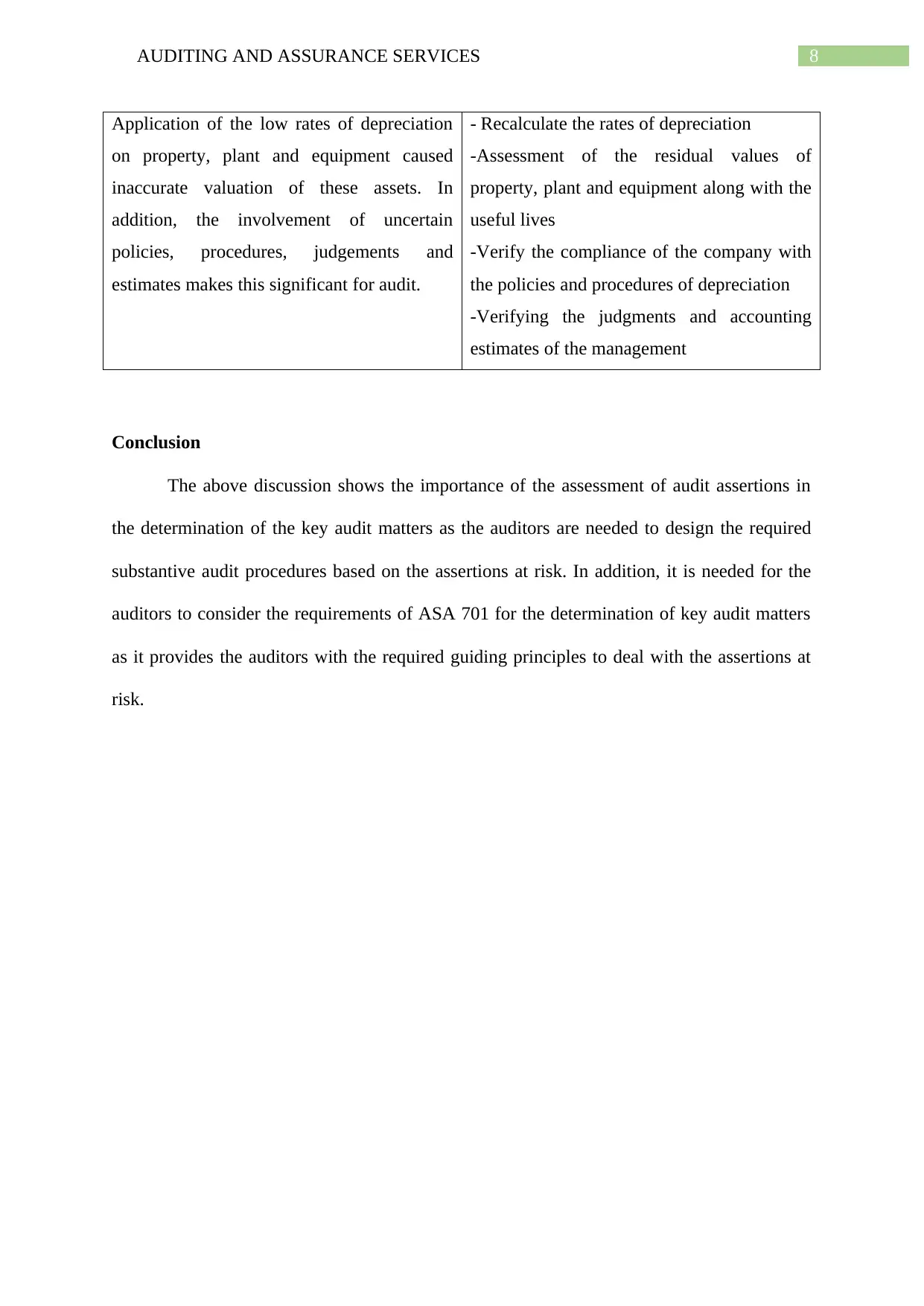

Application of the low rates of depreciation

on property, plant and equipment caused

inaccurate valuation of these assets. In

addition, the involvement of uncertain

policies, procedures, judgements and

estimates makes this significant for audit.

- Recalculate the rates of depreciation

-Assessment of the residual values of

property, plant and equipment along with the

useful lives

-Verify the compliance of the company with

the policies and procedures of depreciation

-Verifying the judgments and accounting

estimates of the management

Conclusion

The above discussion shows the importance of the assessment of audit assertions in

the determination of the key audit matters as the auditors are needed to design the required

substantive audit procedures based on the assertions at risk. In addition, it is needed for the

auditors to consider the requirements of ASA 701 for the determination of key audit matters

as it provides the auditors with the required guiding principles to deal with the assertions at

risk.

Application of the low rates of depreciation

on property, plant and equipment caused

inaccurate valuation of these assets. In

addition, the involvement of uncertain

policies, procedures, judgements and

estimates makes this significant for audit.

- Recalculate the rates of depreciation

-Assessment of the residual values of

property, plant and equipment along with the

useful lives

-Verify the compliance of the company with

the policies and procedures of depreciation

-Verifying the judgments and accounting

estimates of the management

Conclusion

The above discussion shows the importance of the assessment of audit assertions in

the determination of the key audit matters as the auditors are needed to design the required

substantive audit procedures based on the assertions at risk. In addition, it is needed for the

auditors to consider the requirements of ASA 701 for the determination of key audit matters

as it provides the auditors with the required guiding principles to deal with the assertions at

risk.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9AUDITING AND ASSURANCE SERVICES

References

Auasb.gov.au. 2019. Auditing Standard ASA 701 Communicating Key Audit Matters in the

Independent Auditor’s Report. [online] Available at:

https://www.auasb.gov.au/admin/file/content102/c3/ASA_701_2015.pdf [Accessed 21 Jan.

2019].

Auasb.gov.au. 2019. Property, Plant and Equipment. [online] Available at:

https://www.auasb.gov.au/admin/file/content102/c3/ASA_701_2015.pdf [Accessed 21 Jan.

2019].

Backof, A., Bowlin, K. and Goodson, B., 2017. The impact of proposed changes to the

content of the audit report on jurors’ assessments of auditor negligence.

Bhaskar, L.S., Schroeder, J.H. and Shepardson, M.L., 2017. Integration of Internal Control

and Financial Statement Audits: Are Two Audits Better Than One?.

Cannon, N.H. and Bedard, J.C., 2016. Auditing challenging fair value measurements:

Evidence from the field. The Accounting Review, 92(4), pp.81-114.

Cordrey, W.J., 2016. DOD Financial Management: Greater Visibility Needed to Better

Assess Audit Readiness for Property, Plant, and Equipment (No. GAO-16-383).

GOVERNMENT ACCOUNTABILITY OFFICE WASHINGTON DC WASHINGTON DC

United States.

Elder, R.J., Akresh, A.D., Glover, S.M., Higgs, J.L. and Liljegren, J., 2013. Audit sampling

research: A synthesis and implications for future research. Auditing: A Journal of Practice &

Theory, 32(sp1), pp.99-129.

References

Auasb.gov.au. 2019. Auditing Standard ASA 701 Communicating Key Audit Matters in the

Independent Auditor’s Report. [online] Available at:

https://www.auasb.gov.au/admin/file/content102/c3/ASA_701_2015.pdf [Accessed 21 Jan.

2019].

Auasb.gov.au. 2019. Property, Plant and Equipment. [online] Available at:

https://www.auasb.gov.au/admin/file/content102/c3/ASA_701_2015.pdf [Accessed 21 Jan.

2019].

Backof, A., Bowlin, K. and Goodson, B., 2017. The impact of proposed changes to the

content of the audit report on jurors’ assessments of auditor negligence.

Bhaskar, L.S., Schroeder, J.H. and Shepardson, M.L., 2017. Integration of Internal Control

and Financial Statement Audits: Are Two Audits Better Than One?.

Cannon, N.H. and Bedard, J.C., 2016. Auditing challenging fair value measurements:

Evidence from the field. The Accounting Review, 92(4), pp.81-114.

Cordrey, W.J., 2016. DOD Financial Management: Greater Visibility Needed to Better

Assess Audit Readiness for Property, Plant, and Equipment (No. GAO-16-383).

GOVERNMENT ACCOUNTABILITY OFFICE WASHINGTON DC WASHINGTON DC

United States.

Elder, R.J., Akresh, A.D., Glover, S.M., Higgs, J.L. and Liljegren, J., 2013. Audit sampling

research: A synthesis and implications for future research. Auditing: A Journal of Practice &

Theory, 32(sp1), pp.99-129.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10AUDITING AND ASSURANCE SERVICES

Glover, S.M., Taylor, M.H. and Wu, Y.J., 2016. Current practices and challenges in auditing

fair value measurements and complex estimates: Implications for auditing standards and the

academy. Auditing: A Journal of Practice & Theory, 36(1), pp.63-84.

Knechel, W.R. and Salterio, S.E., 2016. Auditing: Assurance and risk. Routledge.

Lennox, C.S., Schmidt, J.J. and Thompson, A., 2018. Is the expanded model of audit

reporting informative to investors? Evidence from the UK.

Louwers, T.J., Ramsay, R.J., Sinason, D.H., Strawser, J.R. and Thibodeau, J.C.,

2015. Auditing & assurance services. McGraw-Hill Education.

van Buuren, J., Koch, C., van Nieuw Amerongen, N. and Wright, A.M., 2014. The use of

business risk audit perspectives by non-Big 4 audit firms. Auditing: A Journal of Practice &

Theory, 33(3), pp.105-128.

Wood, J., Brown, W. and Howe, H., 2013. IT Auditing and Application Controls for Small

and Mid-Sized Enterprises: Revenue, Expenditure, Inventory, Payroll, and More (Vol. 573).

John Wiley & Sons.

Glover, S.M., Taylor, M.H. and Wu, Y.J., 2016. Current practices and challenges in auditing

fair value measurements and complex estimates: Implications for auditing standards and the

academy. Auditing: A Journal of Practice & Theory, 36(1), pp.63-84.

Knechel, W.R. and Salterio, S.E., 2016. Auditing: Assurance and risk. Routledge.

Lennox, C.S., Schmidt, J.J. and Thompson, A., 2018. Is the expanded model of audit

reporting informative to investors? Evidence from the UK.

Louwers, T.J., Ramsay, R.J., Sinason, D.H., Strawser, J.R. and Thibodeau, J.C.,

2015. Auditing & assurance services. McGraw-Hill Education.

van Buuren, J., Koch, C., van Nieuw Amerongen, N. and Wright, A.M., 2014. The use of

business risk audit perspectives by non-Big 4 audit firms. Auditing: A Journal of Practice &

Theory, 33(3), pp.105-128.

Wood, J., Brown, W. and Howe, H., 2013. IT Auditing and Application Controls for Small

and Mid-Sized Enterprises: Revenue, Expenditure, Inventory, Payroll, and More (Vol. 573).

John Wiley & Sons.

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.