Auditing and Ethical Practices Report: Rio Tinto Financial Analysis

VerifiedAdded on 2023/03/23

|15

|3066

|63

Report

AI Summary

This report provides a comprehensive analysis of auditing and ethical practices, focusing on the concept of materiality and its application in financial statement audits. It begins by defining materiality and discussing the factors that influence its determination, such as the reliability of information and the relationship between audit risk and materiality levels. The report then delves into the specific case of Rio Tinto, outlining the bases used for computing materiality, including net profit, revenue, shareholder's equity, and total assets, along with quantitative estimates. Significant items for audit, such as provisions and commitments, are identified, and relevant audit procedures are suggested. The report also includes a preliminary analytical review, key ratio analysis of Rio Tinto's financial performance over four years, and identifies key assertions and audit procedures for revenues and cash. The analysis of profitability, liquidity, and leverage ratios, along with their trends, provides insights into potential areas of risk and the need for further audit scrutiny. Overall, the report serves as a practical guide to auditing financial statements, emphasizing the importance of materiality, analytical procedures, and ethical considerations.

Running head: AUDITING AND ETHICAL PRACTICES

Auditing and ethical practices

Name of the student

Name of the university

Student ID

Author note

Auditing and ethical practices

Name of the student

Name of the university

Student ID

Author note

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1AUDITING AND ETHICAL PRACTICES

Table of Contents

Section 1..........................................................................................................................................2

Level of materiality......................................................................................................................2

Items those can be considered as significant for the purpose of audit.........................................4

Section 2..........................................................................................................................................5

Section 3........................................................................................................................................11

Reviewing statement of cash flows...........................................................................................11

Reviewing audit report..............................................................................................................11

Reference.......................................................................................................................................13

Table of Contents

Section 1..........................................................................................................................................2

Level of materiality......................................................................................................................2

Items those can be considered as significant for the purpose of audit.........................................4

Section 2..........................................................................................................................................5

Section 3........................................................................................................................................11

Reviewing statement of cash flows...........................................................................................11

Reviewing audit report..............................................................................................................11

Reference.......................................................................................................................................13

2AUDITING AND ETHICAL PRACTICES

Section 1

Level of materiality

One of the major concepts of audit is audit materiality that is the misstatement in the

financial statement taken place due to intentional error. Main objective of auditing is to express

opinion on the financial statement of the entity based on the presented financial information. The

auditor express the opinion regarding whether the information presented is not involved with any

material misstatement (Lai, Melloni & Stacchezzini, 2017). AUS 202 stated that the auditor shall

state in the auditor’s report that whether the report is prepared in accordance with the required

framework and all the material aspects have been taken care of (Auasb.gov.au, 2019). However,

various other factors those are taken into consideration while materiality is established are

reliability of the information those are provided by the entity’s management, accountant and

internal auditors, any significant changes taken place as compared to the previous year and other

qualitative and quantitative factors. There is an inverse relationship among the risk and

materiality level. If the level of materiality is high the audit risks level is low whereas the risk

level is high when the materiality level is low (Byrnes et al., 2015).

Planning materiality is the preliminary estimate made by the auditors in the audit

planning stage for financial statement items amounts. Level of planning materiality is the highest

amount by which it is believed by the auditors that the statements are likely to be misstated by

known as well as unknown frauds. In the preliminary stage the materiality impact of the item is

assessed individually and then in aggregate. Some of the bases are there those can be taken into

consideration while computing the materiality (Arens et al., 2016). These include net profit,

Section 1

Level of materiality

One of the major concepts of audit is audit materiality that is the misstatement in the

financial statement taken place due to intentional error. Main objective of auditing is to express

opinion on the financial statement of the entity based on the presented financial information. The

auditor express the opinion regarding whether the information presented is not involved with any

material misstatement (Lai, Melloni & Stacchezzini, 2017). AUS 202 stated that the auditor shall

state in the auditor’s report that whether the report is prepared in accordance with the required

framework and all the material aspects have been taken care of (Auasb.gov.au, 2019). However,

various other factors those are taken into consideration while materiality is established are

reliability of the information those are provided by the entity’s management, accountant and

internal auditors, any significant changes taken place as compared to the previous year and other

qualitative and quantitative factors. There is an inverse relationship among the risk and

materiality level. If the level of materiality is high the audit risks level is low whereas the risk

level is high when the materiality level is low (Byrnes et al., 2015).

Planning materiality is the preliminary estimate made by the auditors in the audit

planning stage for financial statement items amounts. Level of planning materiality is the highest

amount by which it is believed by the auditors that the statements are likely to be misstated by

known as well as unknown frauds. In the preliminary stage the materiality impact of the item is

assessed individually and then in aggregate. Some of the bases are there those can be taken into

consideration while computing the materiality (Arens et al., 2016). These include net profit,

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3AUDITING AND ETHICAL PRACTICES

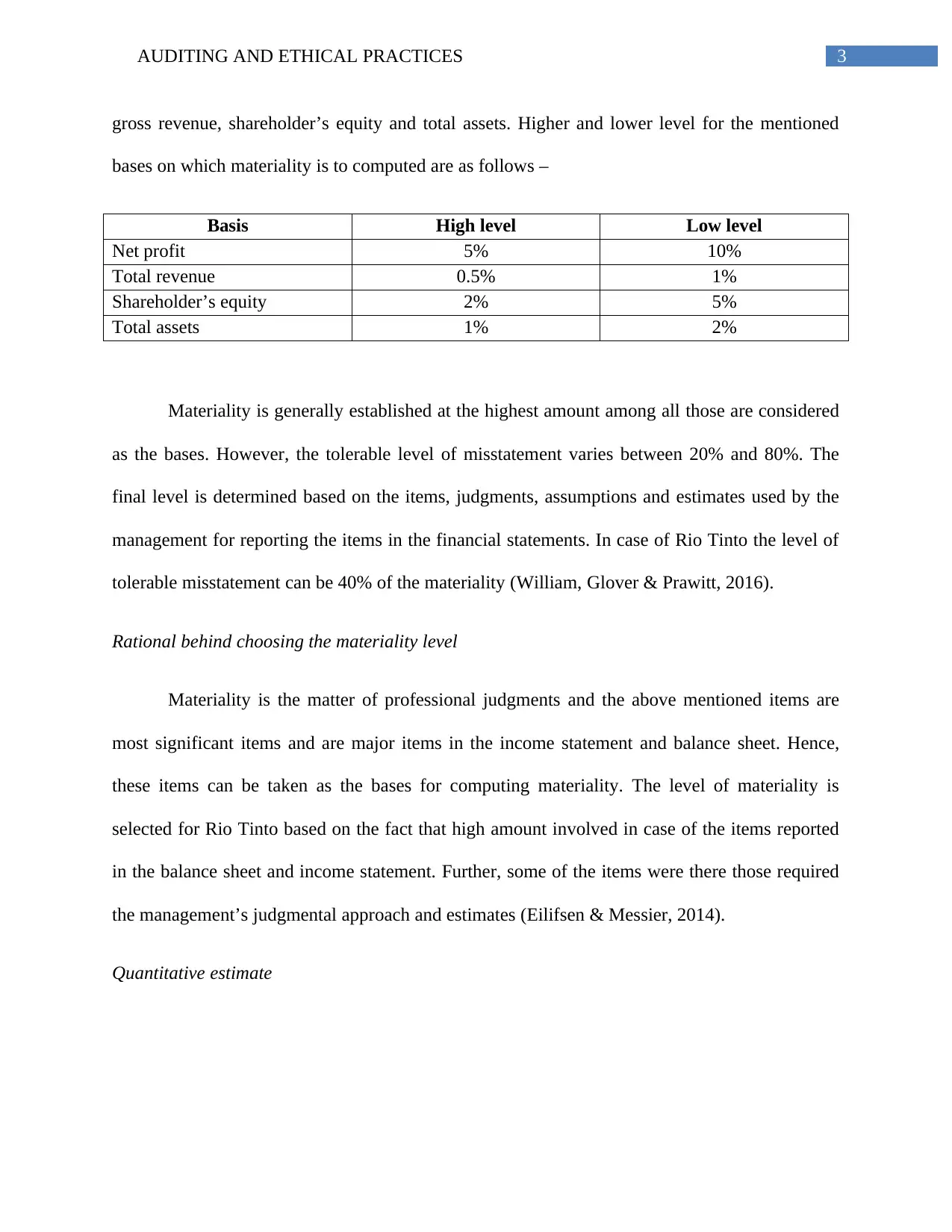

gross revenue, shareholder’s equity and total assets. Higher and lower level for the mentioned

bases on which materiality is to computed are as follows –

Basis High level Low level

Net profit 5% 10%

Total revenue 0.5% 1%

Shareholder’s equity 2% 5%

Total assets 1% 2%

Materiality is generally established at the highest amount among all those are considered

as the bases. However, the tolerable level of misstatement varies between 20% and 80%. The

final level is determined based on the items, judgments, assumptions and estimates used by the

management for reporting the items in the financial statements. In case of Rio Tinto the level of

tolerable misstatement can be 40% of the materiality (William, Glover & Prawitt, 2016).

Rational behind choosing the materiality level

Materiality is the matter of professional judgments and the above mentioned items are

most significant items and are major items in the income statement and balance sheet. Hence,

these items can be taken as the bases for computing materiality. The level of materiality is

selected for Rio Tinto based on the fact that high amount involved in case of the items reported

in the balance sheet and income statement. Further, some of the items were there those required

the management’s judgmental approach and estimates (Eilifsen & Messier, 2014).

Quantitative estimate

gross revenue, shareholder’s equity and total assets. Higher and lower level for the mentioned

bases on which materiality is to computed are as follows –

Basis High level Low level

Net profit 5% 10%

Total revenue 0.5% 1%

Shareholder’s equity 2% 5%

Total assets 1% 2%

Materiality is generally established at the highest amount among all those are considered

as the bases. However, the tolerable level of misstatement varies between 20% and 80%. The

final level is determined based on the items, judgments, assumptions and estimates used by the

management for reporting the items in the financial statements. In case of Rio Tinto the level of

tolerable misstatement can be 40% of the materiality (William, Glover & Prawitt, 2016).

Rational behind choosing the materiality level

Materiality is the matter of professional judgments and the above mentioned items are

most significant items and are major items in the income statement and balance sheet. Hence,

these items can be taken as the bases for computing materiality. The level of materiality is

selected for Rio Tinto based on the fact that high amount involved in case of the items reported

in the balance sheet and income statement. Further, some of the items were there those required

the management’s judgmental approach and estimates (Eilifsen & Messier, 2014).

Quantitative estimate

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4AUDITING AND ETHICAL PRACTICES

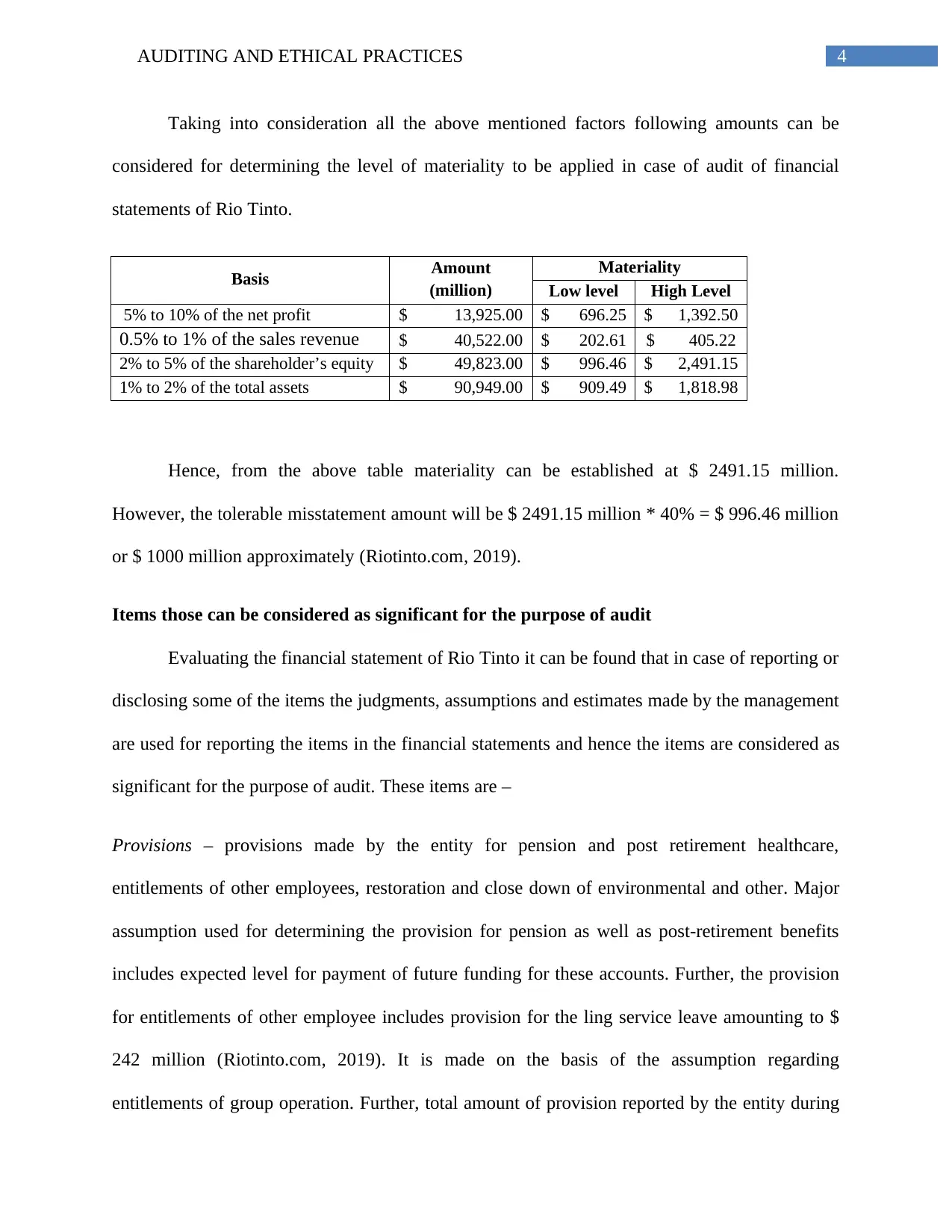

Taking into consideration all the above mentioned factors following amounts can be

considered for determining the level of materiality to be applied in case of audit of financial

statements of Rio Tinto.

Basis Amount

(million)

Materiality

Low level High Level

5% to 10% of the net profit $ 13,925.00 $ 696.25 $ 1,392.50

0.5% to 1% of the sales revenue $ 40,522.00 $ 202.61 $ 405.22

2% to 5% of the shareholder’s equity $ 49,823.00 $ 996.46 $ 2,491.15

1% to 2% of the total assets $ 90,949.00 $ 909.49 $ 1,818.98

Hence, from the above table materiality can be established at $ 2491.15 million.

However, the tolerable misstatement amount will be $ 2491.15 million * 40% = $ 996.46 million

or $ 1000 million approximately (Riotinto.com, 2019).

Items those can be considered as significant for the purpose of audit

Evaluating the financial statement of Rio Tinto it can be found that in case of reporting or

disclosing some of the items the judgments, assumptions and estimates made by the management

are used for reporting the items in the financial statements and hence the items are considered as

significant for the purpose of audit. These items are –

Provisions – provisions made by the entity for pension and post retirement healthcare,

entitlements of other employees, restoration and close down of environmental and other. Major

assumption used for determining the provision for pension as well as post-retirement benefits

includes expected level for payment of future funding for these accounts. Further, the provision

for entitlements of other employee includes provision for the ling service leave amounting to $

242 million (Riotinto.com, 2019). It is made on the basis of the assumption regarding

entitlements of group operation. Further, total amount of provision reported by the entity during

Taking into consideration all the above mentioned factors following amounts can be

considered for determining the level of materiality to be applied in case of audit of financial

statements of Rio Tinto.

Basis Amount

(million)

Materiality

Low level High Level

5% to 10% of the net profit $ 13,925.00 $ 696.25 $ 1,392.50

0.5% to 1% of the sales revenue $ 40,522.00 $ 202.61 $ 405.22

2% to 5% of the shareholder’s equity $ 49,823.00 $ 996.46 $ 2,491.15

1% to 2% of the total assets $ 90,949.00 $ 909.49 $ 1,818.98

Hence, from the above table materiality can be established at $ 2491.15 million.

However, the tolerable misstatement amount will be $ 2491.15 million * 40% = $ 996.46 million

or $ 1000 million approximately (Riotinto.com, 2019).

Items those can be considered as significant for the purpose of audit

Evaluating the financial statement of Rio Tinto it can be found that in case of reporting or

disclosing some of the items the judgments, assumptions and estimates made by the management

are used for reporting the items in the financial statements and hence the items are considered as

significant for the purpose of audit. These items are –

Provisions – provisions made by the entity for pension and post retirement healthcare,

entitlements of other employees, restoration and close down of environmental and other. Major

assumption used for determining the provision for pension as well as post-retirement benefits

includes expected level for payment of future funding for these accounts. Further, the provision

for entitlements of other employee includes provision for the ling service leave amounting to $

242 million (Riotinto.com, 2019). It is made on the basis of the assumption regarding

entitlements of group operation. Further, total amount of provision reported by the entity during

5AUDITING AND ETHICAL PRACTICES

the year closed 2018 amounted to $ 13,608 million. As huge amount and various assumptions are

used for providing provision this is regarded as significant item (Riotinto.com, 2019). For

auditing provisions following audit procedure shall be followed –

Assuring that all the items under contingencies that will take place are considered for

providing amount as provisions

The accounting treatment that is charging the amount of provision against the profit and

loss shall be verified

Auditor shall look into the account and shall assure that amount for all the items of

provisions are properly disclosed with appropriate amount.

Commitments and contingencies – the entity committed to purchase as well as market a part of

output the Sohar Aluminium Company LLC and the entity immediately sells the product

purchased to 3rd parties. In addition to this it is committed for providing emergency funding to

Sohar Aluminium Company LLC, if required (Riotinto.com, 2019). For auditing Commitments

and contingencies following audit procedure shall be followed –

Analysing the likelihood of occurrence – likelihood of the event to determine the impact

on the financial statement 1st its chances of taking place is to be estimated. There are

different levels of occurrence - remote, reasonably probable and probable. Events those

are reasonably probable and probable shall be considered as contingencies and disclosed

accordingly.

Section 2

Preliminary analytical review is carried out by the auditor to gain knowledge of the

client’s business and is carried out at the level of audit planning. It assists the auditors to assess

the year closed 2018 amounted to $ 13,608 million. As huge amount and various assumptions are

used for providing provision this is regarded as significant item (Riotinto.com, 2019). For

auditing provisions following audit procedure shall be followed –

Assuring that all the items under contingencies that will take place are considered for

providing amount as provisions

The accounting treatment that is charging the amount of provision against the profit and

loss shall be verified

Auditor shall look into the account and shall assure that amount for all the items of

provisions are properly disclosed with appropriate amount.

Commitments and contingencies – the entity committed to purchase as well as market a part of

output the Sohar Aluminium Company LLC and the entity immediately sells the product

purchased to 3rd parties. In addition to this it is committed for providing emergency funding to

Sohar Aluminium Company LLC, if required (Riotinto.com, 2019). For auditing Commitments

and contingencies following audit procedure shall be followed –

Analysing the likelihood of occurrence – likelihood of the event to determine the impact

on the financial statement 1st its chances of taking place is to be estimated. There are

different levels of occurrence - remote, reasonably probable and probable. Events those

are reasonably probable and probable shall be considered as contingencies and disclosed

accordingly.

Section 2

Preliminary analytical review is carried out by the auditor to gain knowledge of the

client’s business and is carried out at the level of audit planning. It assists the auditors to assess

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6AUDITING AND ETHICAL PRACTICES

the material risk involved in the financial statements and its operation to set up the extent, time

required and nature of the audit to be planned. It involves both management’s investigation as

well as analytical procedure that is established at the time when planning the audit for the client.

Various methods are there to perform the analytical procedure and one of such method is key

ratio analysis that helps in identifying the risk area and the trends of the ratios to understand the

overview (Coetzee & Lubbe, 2014).

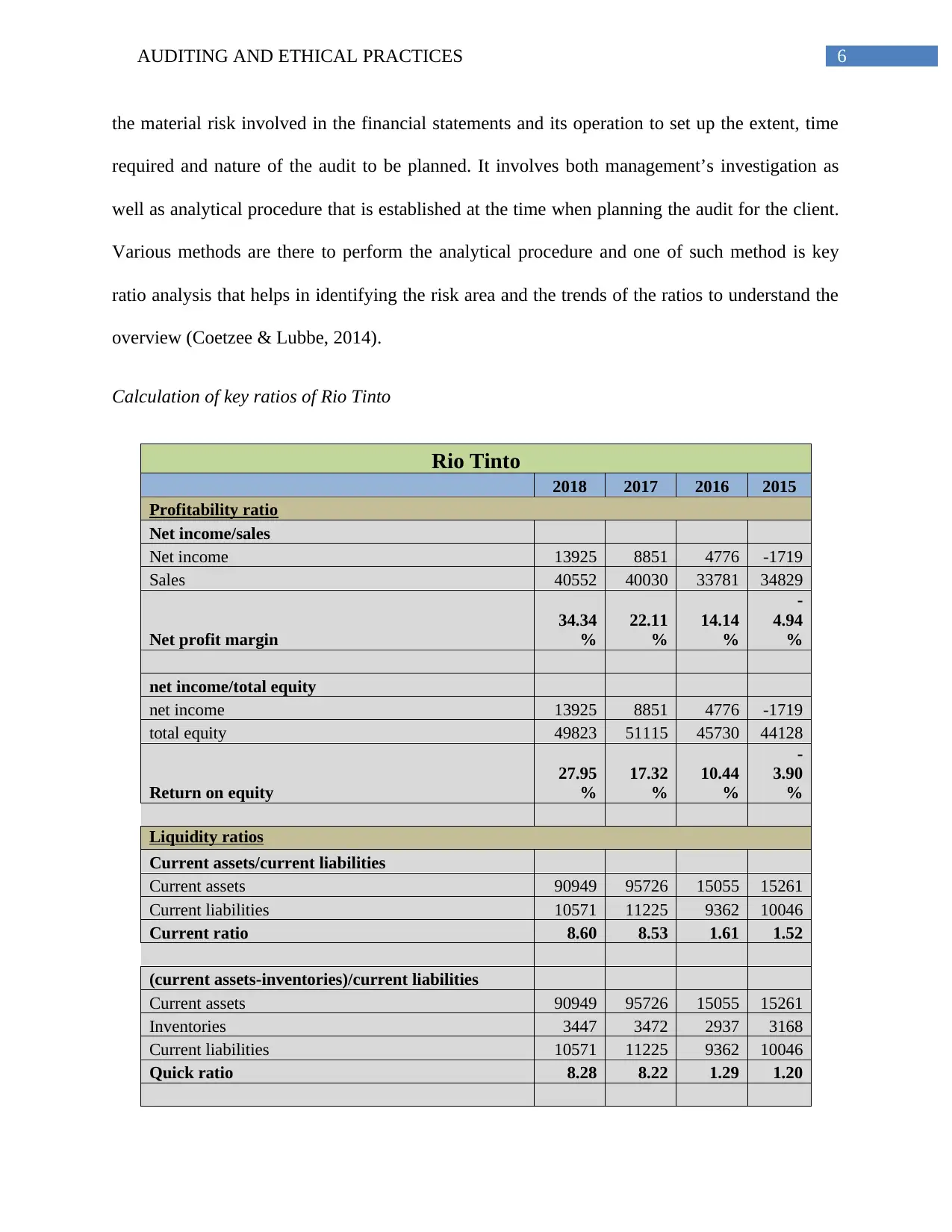

Calculation of key ratios of Rio Tinto

Rio Tinto

2018 2017 2016 2015

Profitability ratio

Net income/sales

Net income 13925 8851 4776 -1719

Sales 40552 40030 33781 34829

Net profit margin

34.34

%

22.11

%

14.14

%

-

4.94

%

net income/total equity

net income 13925 8851 4776 -1719

total equity 49823 51115 45730 44128

Return on equity

27.95

%

17.32

%

10.44

%

-

3.90

%

Liquidity ratios

Current assets/current liabilities

Current assets 90949 95726 15055 15261

Current liabilities 10571 11225 9362 10046

Current ratio 8.60 8.53 1.61 1.52

(current assets-inventories)/current liabilities

Current assets 90949 95726 15055 15261

Inventories 3447 3472 2937 3168

Current liabilities 10571 11225 9362 10046

Quick ratio 8.28 8.22 1.29 1.20

the material risk involved in the financial statements and its operation to set up the extent, time

required and nature of the audit to be planned. It involves both management’s investigation as

well as analytical procedure that is established at the time when planning the audit for the client.

Various methods are there to perform the analytical procedure and one of such method is key

ratio analysis that helps in identifying the risk area and the trends of the ratios to understand the

overview (Coetzee & Lubbe, 2014).

Calculation of key ratios of Rio Tinto

Rio Tinto

2018 2017 2016 2015

Profitability ratio

Net income/sales

Net income 13925 8851 4776 -1719

Sales 40552 40030 33781 34829

Net profit margin

34.34

%

22.11

%

14.14

%

-

4.94

%

net income/total equity

net income 13925 8851 4776 -1719

total equity 49823 51115 45730 44128

Return on equity

27.95

%

17.32

%

10.44

%

-

3.90

%

Liquidity ratios

Current assets/current liabilities

Current assets 90949 95726 15055 15261

Current liabilities 10571 11225 9362 10046

Current ratio 8.60 8.53 1.61 1.52

(current assets-inventories)/current liabilities

Current assets 90949 95726 15055 15261

Inventories 3447 3472 2937 3168

Current liabilities 10571 11225 9362 10046

Quick ratio 8.28 8.22 1.29 1.20

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7AUDITING AND ETHICAL PRACTICES

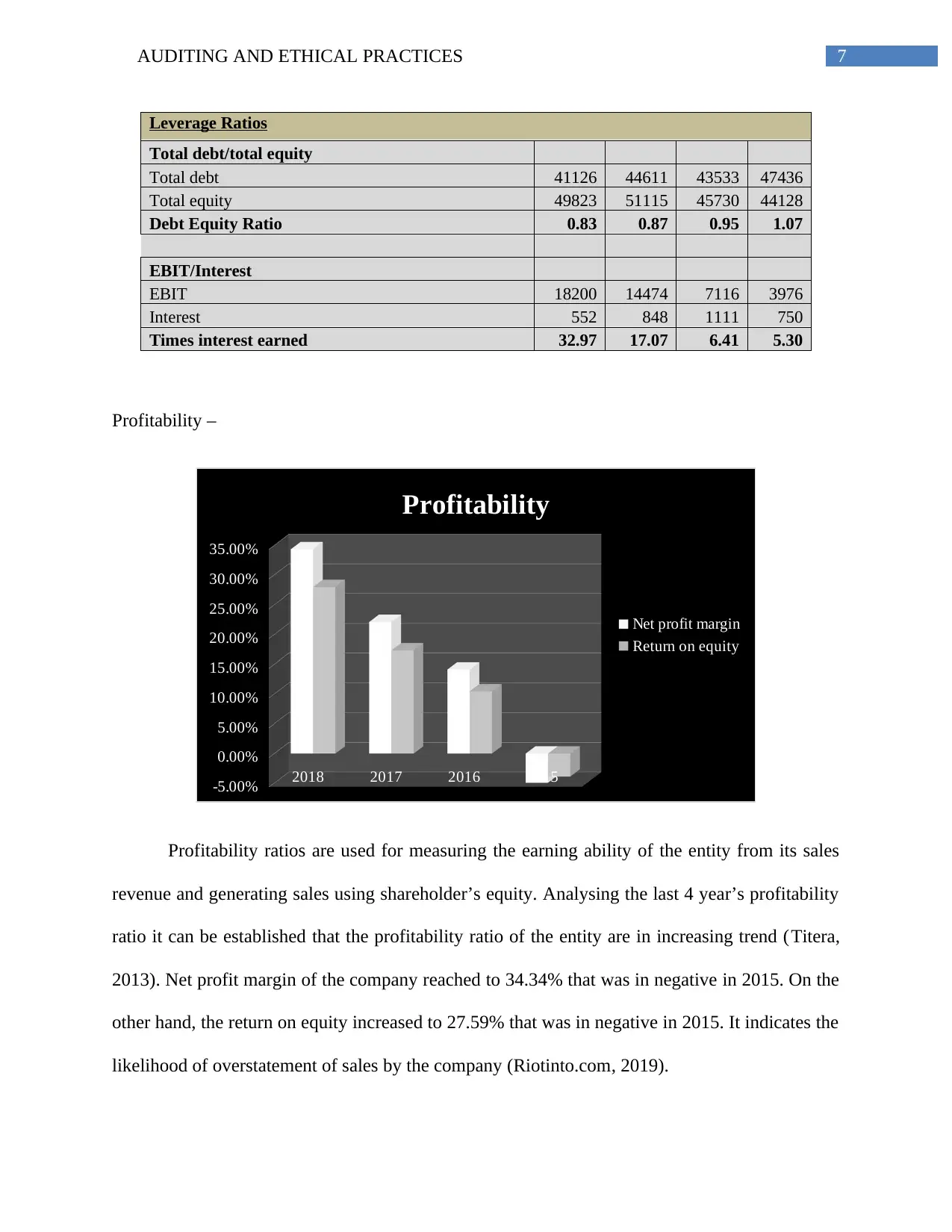

Leverage Ratios

Total debt/total equity

Total debt 41126 44611 43533 47436

Total equity 49823 51115 45730 44128

Debt Equity Ratio 0.83 0.87 0.95 1.07

EBIT/Interest

EBIT 18200 14474 7116 3976

Interest 552 848 1111 750

Times interest earned 32.97 17.07 6.41 5.30

Profitability –

2018 2017 2016 2015

-5.00%

0.00%

5.00%

10.00%

15.00%

20.00%

25.00%

30.00%

35.00%

Profitability

Net profit margin

Return on equity

Profitability ratios are used for measuring the earning ability of the entity from its sales

revenue and generating sales using shareholder’s equity. Analysing the last 4 year’s profitability

ratio it can be established that the profitability ratio of the entity are in increasing trend (Titera,

2013). Net profit margin of the company reached to 34.34% that was in negative in 2015. On the

other hand, the return on equity increased to 27.59% that was in negative in 2015. It indicates the

likelihood of overstatement of sales by the company (Riotinto.com, 2019).

Leverage Ratios

Total debt/total equity

Total debt 41126 44611 43533 47436

Total equity 49823 51115 45730 44128

Debt Equity Ratio 0.83 0.87 0.95 1.07

EBIT/Interest

EBIT 18200 14474 7116 3976

Interest 552 848 1111 750

Times interest earned 32.97 17.07 6.41 5.30

Profitability –

2018 2017 2016 2015

-5.00%

0.00%

5.00%

10.00%

15.00%

20.00%

25.00%

30.00%

35.00%

Profitability

Net profit margin

Return on equity

Profitability ratios are used for measuring the earning ability of the entity from its sales

revenue and generating sales using shareholder’s equity. Analysing the last 4 year’s profitability

ratio it can be established that the profitability ratio of the entity are in increasing trend (Titera,

2013). Net profit margin of the company reached to 34.34% that was in negative in 2015. On the

other hand, the return on equity increased to 27.59% that was in negative in 2015. It indicates the

likelihood of overstatement of sales by the company (Riotinto.com, 2019).

8AUDITING AND ETHICAL PRACTICES

Liquidity –

2018 2017 2016 2015

0.00

1.00

2.00

3.00

4.00

5.00

6.00

7.00

8.00

9.00

Liquidity

Current ratio

Quick ratio

It is used for measuring the short term liquidity position of the company. Analysing the

last 4 year’s liquidity ratio it can be established that the liquidity ratio of the entity are in

increasing trend (Ruhnke, Pronobis & Michel, 2014). Current ratio of the company reached to

8.60% that was only 1.52 in 2015. On the other hand, the quick ratio increased to 8.28 that was

only 1.07 in 2015. It indicates the likelihood of overstatement of current assets like cash by the

company (Riotinto.com, 2019).

Leverage ratio -

Liquidity –

2018 2017 2016 2015

0.00

1.00

2.00

3.00

4.00

5.00

6.00

7.00

8.00

9.00

Liquidity

Current ratio

Quick ratio

It is used for measuring the short term liquidity position of the company. Analysing the

last 4 year’s liquidity ratio it can be established that the liquidity ratio of the entity are in

increasing trend (Ruhnke, Pronobis & Michel, 2014). Current ratio of the company reached to

8.60% that was only 1.52 in 2015. On the other hand, the quick ratio increased to 8.28 that was

only 1.07 in 2015. It indicates the likelihood of overstatement of current assets like cash by the

company (Riotinto.com, 2019).

Leverage ratio -

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9AUDITING AND ETHICAL PRACTICES

2018 2017 2016 2015

0.00

5.00

10.00

15.00

20.00

25.00

30.00

35.00

Leverage

Debt Equity Ratio

Times interest erned

Leverage ratios are used to assess the financial stability and long term sustainability of

the entity as very high level of debt equity ratio and lower time’s interest earned signifies that the

entity is not stable financially (Louwers et al., 2015). Analysing the last 4 year’s leverage ratio it

can be established that the leverage ratio of the entity are in reducing trend. Debt equity of the

company reduced to 0.83 that was as high as 1.07 in 2015. On the other hand, the time’s interest

earned increased to 32.97 times that was 5.30 times in 2015 (Riotinto.com, 2019).

Taking into consideration the findings from the ratio it can be determined that the

following accounts are required to be selected for the purpose of analytical review –

Revenues – revenues of the entity are continuously in increasing trend and reached to $ 40,552

million in 2018 from $ 34,829 million in 2015.

Key assertions –

Cut off – sales revenue considered for the current period does not include any amount

that pertains to other period

2018 2017 2016 2015

0.00

5.00

10.00

15.00

20.00

25.00

30.00

35.00

Leverage

Debt Equity Ratio

Times interest erned

Leverage ratios are used to assess the financial stability and long term sustainability of

the entity as very high level of debt equity ratio and lower time’s interest earned signifies that the

entity is not stable financially (Louwers et al., 2015). Analysing the last 4 year’s leverage ratio it

can be established that the leverage ratio of the entity are in reducing trend. Debt equity of the

company reduced to 0.83 that was as high as 1.07 in 2015. On the other hand, the time’s interest

earned increased to 32.97 times that was 5.30 times in 2015 (Riotinto.com, 2019).

Taking into consideration the findings from the ratio it can be determined that the

following accounts are required to be selected for the purpose of analytical review –

Revenues – revenues of the entity are continuously in increasing trend and reached to $ 40,552

million in 2018 from $ 34,829 million in 2015.

Key assertions –

Cut off – sales revenue considered for the current period does not include any amount

that pertains to other period

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10AUDITING AND ETHICAL PRACTICES

Accuracy – amount of sales transactions reported are error free and reported at the full

amount (Kharisova & Kozlova, 2014).

Audit procedure –

Cut off – sales balances shall be simultaneously verify with the amount of account

receivables and cash

Accuracy – reported balance of sales revenues shall be verified with the amount in sales

register (Knechel & Salterio, 2016).

Cash – though much change are not there in cash balance, however being the most liquid item it

shall be considered for analytical review.

Key assertion –

Completeness – all cash related receipts and payments have been taken into consideration

while prepared the statement

Existence – all cash receipts and payments reported are error free and reported at the full

amount (Coetzee & Lubbe, 2014).

Audit procedure –

Completeness – cash register transactions shall be matched with bank balance and

reported amount of cash in balance sheet

Existence – all the payment invoices and bill receipt shall be matched with reported

balances (Christensen et al., 2016).

Accuracy – amount of sales transactions reported are error free and reported at the full

amount (Kharisova & Kozlova, 2014).

Audit procedure –

Cut off – sales balances shall be simultaneously verify with the amount of account

receivables and cash

Accuracy – reported balance of sales revenues shall be verified with the amount in sales

register (Knechel & Salterio, 2016).

Cash – though much change are not there in cash balance, however being the most liquid item it

shall be considered for analytical review.

Key assertion –

Completeness – all cash related receipts and payments have been taken into consideration

while prepared the statement

Existence – all cash receipts and payments reported are error free and reported at the full

amount (Coetzee & Lubbe, 2014).

Audit procedure –

Completeness – cash register transactions shall be matched with bank balance and

reported amount of cash in balance sheet

Existence – all the payment invoices and bill receipt shall be matched with reported

balances (Christensen et al., 2016).

11AUDITING AND ETHICAL PRACTICES

Section 3

Reviewing statement of cash flows

Cash flows from operating activities provided major cash inflows

Cash used in financing activities were major outflows of cash

Disposal of unincorporated joint operations, subsidiaries, joint ventures and associates

was primary source of cash receipt amounted to $ 7753 million and purchase of plant,

equipment and property and intangible assets was primary cash payment amounted to $

5430 million (Riotinto.com, 2019).

Non-cash investing and financing activities were equity dividend paid to the owners of

the entity

From the cash flow statement of the company it is identified that for all the activities

big differences are not there in cash inflows and outflows. However, cash used in

investing activities for past 2 years has been converted to cash inflow in 2018. Further

the cash balance is increased from $ 10,550 million to $ 10,773 million in last 2 years.

Hence the positive changes are signifying that the going concern assumption of the

entity is in order (Riotinto.com, 2019). However, cash from operation is indicating risk

for which the auditor shall reconcile all the operational payments and receipts with the

respective invoices and bill receipt and with the day’s cash register as well as bank

account.

Reviewing audit report

For the year closed at 30th June 2018, the audit of the company’s financial statement

carried out by PricewaterhouseCoopers. They expressed unmodified opinion stating that the

Section 3

Reviewing statement of cash flows

Cash flows from operating activities provided major cash inflows

Cash used in financing activities were major outflows of cash

Disposal of unincorporated joint operations, subsidiaries, joint ventures and associates

was primary source of cash receipt amounted to $ 7753 million and purchase of plant,

equipment and property and intangible assets was primary cash payment amounted to $

5430 million (Riotinto.com, 2019).

Non-cash investing and financing activities were equity dividend paid to the owners of

the entity

From the cash flow statement of the company it is identified that for all the activities

big differences are not there in cash inflows and outflows. However, cash used in

investing activities for past 2 years has been converted to cash inflow in 2018. Further

the cash balance is increased from $ 10,550 million to $ 10,773 million in last 2 years.

Hence the positive changes are signifying that the going concern assumption of the

entity is in order (Riotinto.com, 2019). However, cash from operation is indicating risk

for which the auditor shall reconcile all the operational payments and receipts with the

respective invoices and bill receipt and with the day’s cash register as well as bank

account.

Reviewing audit report

For the year closed at 30th June 2018, the audit of the company’s financial statement

carried out by PricewaterhouseCoopers. They expressed unmodified opinion stating that the

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 15