Auditing and Ethics

VerifiedAdded on 2022/12/23

|12

|2697

|1

AI Summary

This document discusses the concept of auditing and ethics in the context of TPG Telecom Limited. It covers topics such as materiality, financial ratios, and cash flow analysis. The document also provides insights into the audit procedure and the audit report provided by KPMG.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Running head : AUDITING AND ETHICS

AUDITING AND ETHICS

Name of the Student

Name of the University

Author Note

AUDITING AND ETHICS

Name of the Student

Name of the University

Author Note

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

1

AUDITING AND ETHICS

Table of Contents

Section 1.....................................................................................................................................2

Section 2.....................................................................................................................................2

Section 3.....................................................................................................................................6

References..................................................................................................................................9

AUDITING AND ETHICS

Table of Contents

Section 1.....................................................................................................................................2

Section 2.....................................................................................................................................2

Section 3.....................................................................................................................................6

References..................................................................................................................................9

2

AUDITING AND ETHICS

TPG Telecom Limited is an Australian telecommunication and Information Technology

company that has its specialisation in consumer and business internet services and mobile

telephone services. TPG Telecom Limited as of august 2015 is considered as the second

largest provider of internet services in Australia and is considered as the largest mobile

network operator (2019 Tpg.com.au). The formation of the Information Technology giant

TPG Telecom Limited was on account of a merger between the Total Peripherals Group,

whose establishment was in the year 1986 by David and Vicky Teoh and SP Tele media in

the year 2008/. In the year 2018, TPG and Vodafone Hutch son Australia made an

announcement of their intention to merge the company (2019 Tpg.com.au).

Section 1

The level of materiality of TPG Telecom Limited that is to be used for the audit of the group

accounts for the year ended 2018, is calculated on the basis of the total assets that is 2 percent

of AUD 5416.4 Million, that is AUD 108.328 Million (2019 Tpg.com.au).

Materiality refers to the concept or convention that comes within auditing and accounting

relating to the significance of an amount, transaction or any kind of discrepancy. The main

objective of an audit of the financial statements is to enable the auditor to express an opinion

that the financial statements that are prepared in all material aspects are in conformity with an

identified financial reporting framework such as the Generally Accepted Accounting

Principles (2019 Tpg.com.au).

The financial statements of TPG Telecom Limited has been reviewed. Based on the review of

the various draft notes in the financial statements, the disclosures have been taken into

consideration. The important aspects that may have significance to the audit are as follows:

Particulars Amounts [000]

Salaries and fees to the Executive director 1610

AUDITING AND ETHICS

TPG Telecom Limited is an Australian telecommunication and Information Technology

company that has its specialisation in consumer and business internet services and mobile

telephone services. TPG Telecom Limited as of august 2015 is considered as the second

largest provider of internet services in Australia and is considered as the largest mobile

network operator (2019 Tpg.com.au). The formation of the Information Technology giant

TPG Telecom Limited was on account of a merger between the Total Peripherals Group,

whose establishment was in the year 1986 by David and Vicky Teoh and SP Tele media in

the year 2008/. In the year 2018, TPG and Vodafone Hutch son Australia made an

announcement of their intention to merge the company (2019 Tpg.com.au).

Section 1

The level of materiality of TPG Telecom Limited that is to be used for the audit of the group

accounts for the year ended 2018, is calculated on the basis of the total assets that is 2 percent

of AUD 5416.4 Million, that is AUD 108.328 Million (2019 Tpg.com.au).

Materiality refers to the concept or convention that comes within auditing and accounting

relating to the significance of an amount, transaction or any kind of discrepancy. The main

objective of an audit of the financial statements is to enable the auditor to express an opinion

that the financial statements that are prepared in all material aspects are in conformity with an

identified financial reporting framework such as the Generally Accepted Accounting

Principles (2019 Tpg.com.au).

The financial statements of TPG Telecom Limited has been reviewed. Based on the review of

the various draft notes in the financial statements, the disclosures have been taken into

consideration. The important aspects that may have significance to the audit are as follows:

Particulars Amounts [000]

Salaries and fees to the Executive director 1610

3

AUDITING AND ETHICS

Fees and salaries of the Non -Executive Directors 365

STI cash bonus 1600

Non monetary benefits 145

Total 3355

Superannuation benefits 25

Other long term benefits 27

Total 3407

Section 2

The apparent trends and the changes in the ratios have been studies and the following

conclusions have been drawn (2019 Tpg.com.au). All the figures are mentioned in AUD

millions.

The net profit margins of TPG Telecom Limited for the years 2016, 2017 and 2018 are 36%,

36% and 34% respectively. The net profit margins are not very favourable in the past 3 years.

Above that, it has shown a declining trend in the year 2018 (2019 Tpg.com.au). It is an

indicator that the company does not keep the potential to come up with promising results in

the years to come.

AUDITING AND ETHICS

Fees and salaries of the Non -Executive Directors 365

STI cash bonus 1600

Non monetary benefits 145

Total 3355

Superannuation benefits 25

Other long term benefits 27

Total 3407

Section 2

The apparent trends and the changes in the ratios have been studies and the following

conclusions have been drawn (2019 Tpg.com.au). All the figures are mentioned in AUD

millions.

The net profit margins of TPG Telecom Limited for the years 2016, 2017 and 2018 are 36%,

36% and 34% respectively. The net profit margins are not very favourable in the past 3 years.

Above that, it has shown a declining trend in the year 2018 (2019 Tpg.com.au). It is an

indicator that the company does not keep the potential to come up with promising results in

the years to come.

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

4

AUDITING AND ETHICS

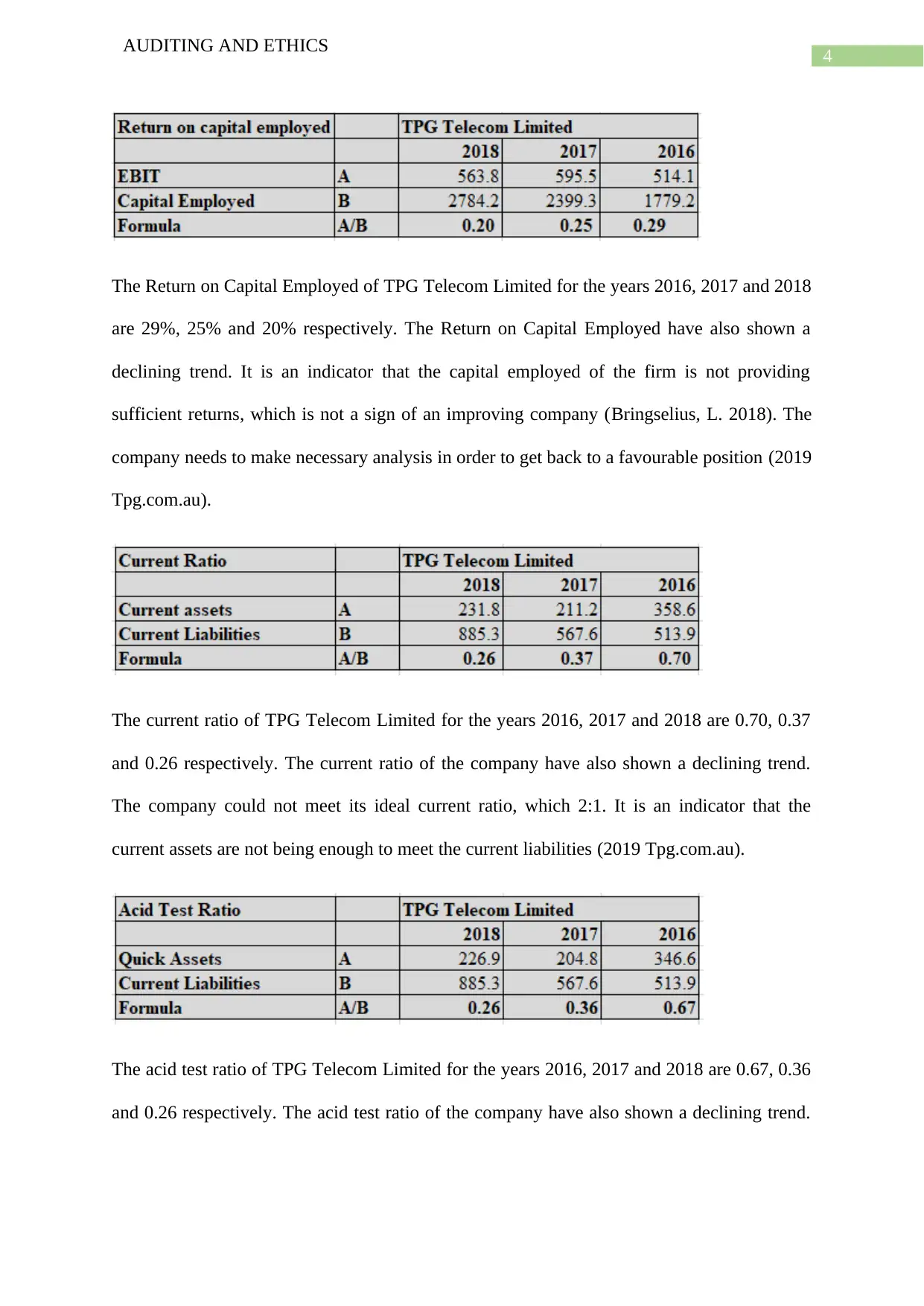

The Return on Capital Employed of TPG Telecom Limited for the years 2016, 2017 and 2018

are 29%, 25% and 20% respectively. The Return on Capital Employed have also shown a

declining trend. It is an indicator that the capital employed of the firm is not providing

sufficient returns, which is not a sign of an improving company (Bringselius, L. 2018). The

company needs to make necessary analysis in order to get back to a favourable position (2019

Tpg.com.au).

The current ratio of TPG Telecom Limited for the years 2016, 2017 and 2018 are 0.70, 0.37

and 0.26 respectively. The current ratio of the company have also shown a declining trend.

The company could not meet its ideal current ratio, which 2:1. It is an indicator that the

current assets are not being enough to meet the current liabilities (2019 Tpg.com.au).

The acid test ratio of TPG Telecom Limited for the years 2016, 2017 and 2018 are 0.67, 0.36

and 0.26 respectively. The acid test ratio of the company have also shown a declining trend.

AUDITING AND ETHICS

The Return on Capital Employed of TPG Telecom Limited for the years 2016, 2017 and 2018

are 29%, 25% and 20% respectively. The Return on Capital Employed have also shown a

declining trend. It is an indicator that the capital employed of the firm is not providing

sufficient returns, which is not a sign of an improving company (Bringselius, L. 2018). The

company needs to make necessary analysis in order to get back to a favourable position (2019

Tpg.com.au).

The current ratio of TPG Telecom Limited for the years 2016, 2017 and 2018 are 0.70, 0.37

and 0.26 respectively. The current ratio of the company have also shown a declining trend.

The company could not meet its ideal current ratio, which 2:1. It is an indicator that the

current assets are not being enough to meet the current liabilities (2019 Tpg.com.au).

The acid test ratio of TPG Telecom Limited for the years 2016, 2017 and 2018 are 0.67, 0.36

and 0.26 respectively. The acid test ratio of the company have also shown a declining trend.

5

AUDITING AND ETHICS

The company could not meet its ideal current ratio, which 1:1. It is an indicator that the quick

assets are also not being enough to meet the current liabilities (2019 Tpg.com.au).

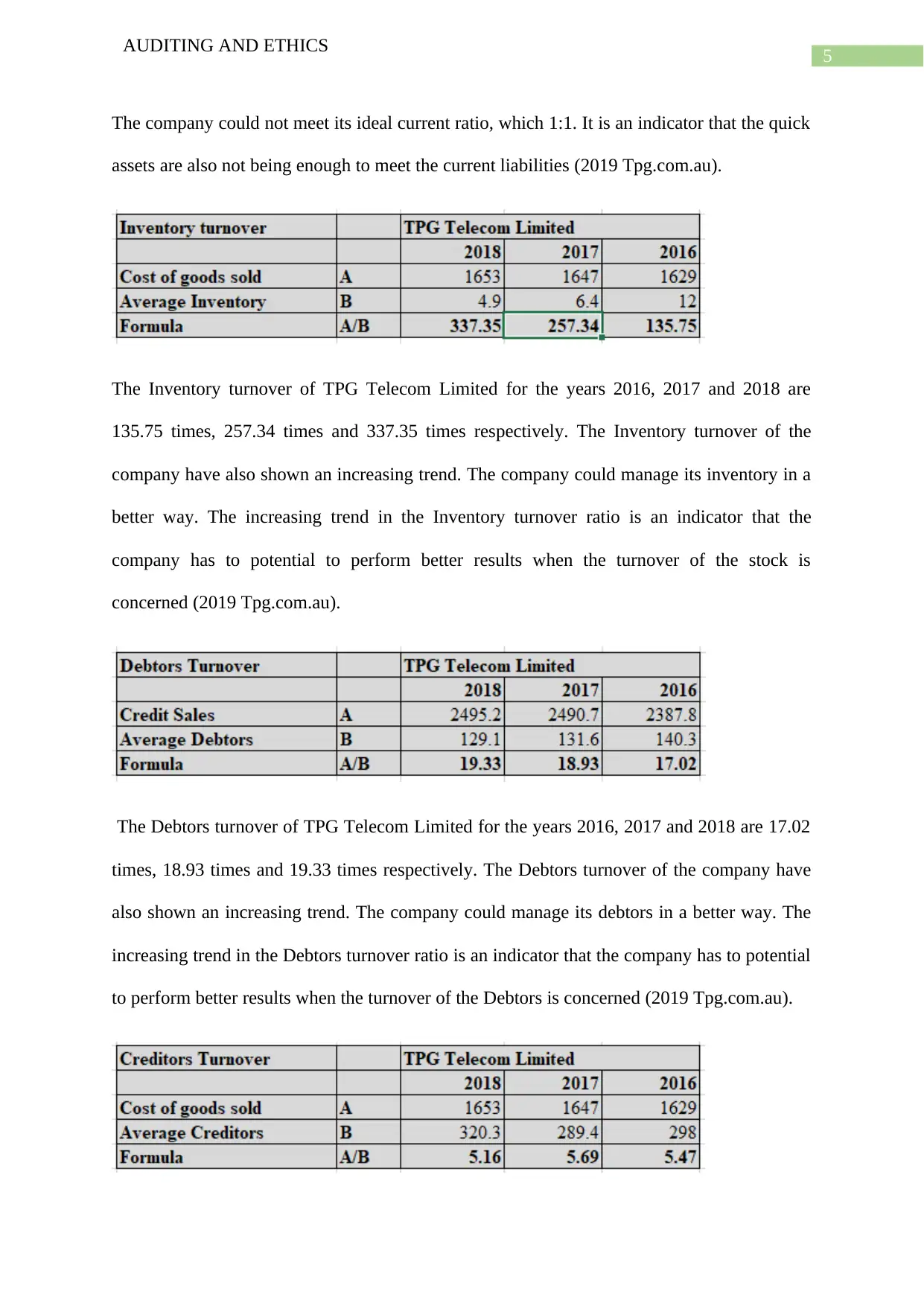

The Inventory turnover of TPG Telecom Limited for the years 2016, 2017 and 2018 are

135.75 times, 257.34 times and 337.35 times respectively. The Inventory turnover of the

company have also shown an increasing trend. The company could manage its inventory in a

better way. The increasing trend in the Inventory turnover ratio is an indicator that the

company has to potential to perform better results when the turnover of the stock is

concerned (2019 Tpg.com.au).

The Debtors turnover of TPG Telecom Limited for the years 2016, 2017 and 2018 are 17.02

times, 18.93 times and 19.33 times respectively. The Debtors turnover of the company have

also shown an increasing trend. The company could manage its debtors in a better way. The

increasing trend in the Debtors turnover ratio is an indicator that the company has to potential

to perform better results when the turnover of the Debtors is concerned (2019 Tpg.com.au).

AUDITING AND ETHICS

The company could not meet its ideal current ratio, which 1:1. It is an indicator that the quick

assets are also not being enough to meet the current liabilities (2019 Tpg.com.au).

The Inventory turnover of TPG Telecom Limited for the years 2016, 2017 and 2018 are

135.75 times, 257.34 times and 337.35 times respectively. The Inventory turnover of the

company have also shown an increasing trend. The company could manage its inventory in a

better way. The increasing trend in the Inventory turnover ratio is an indicator that the

company has to potential to perform better results when the turnover of the stock is

concerned (2019 Tpg.com.au).

The Debtors turnover of TPG Telecom Limited for the years 2016, 2017 and 2018 are 17.02

times, 18.93 times and 19.33 times respectively. The Debtors turnover of the company have

also shown an increasing trend. The company could manage its debtors in a better way. The

increasing trend in the Debtors turnover ratio is an indicator that the company has to potential

to perform better results when the turnover of the Debtors is concerned (2019 Tpg.com.au).

6

AUDITING AND ETHICS

The Creditors turnover of TPG Telecom Limited for the years 2016, 2017 and 2018 are 17.02

times, 5.47 times, 5.69 and 5.16 times respectively (2019 Tpg.com.au). The Creditors

turnover of the company have also shown a fluctuating trend. The company could manage its

creditors in a better way. The fluctuating trend in the Creditors turnover ratio is an indicator

that the company has to potential to perform better results when the turnover of the Creditors

is concerned (2019 Tpg.com.au).

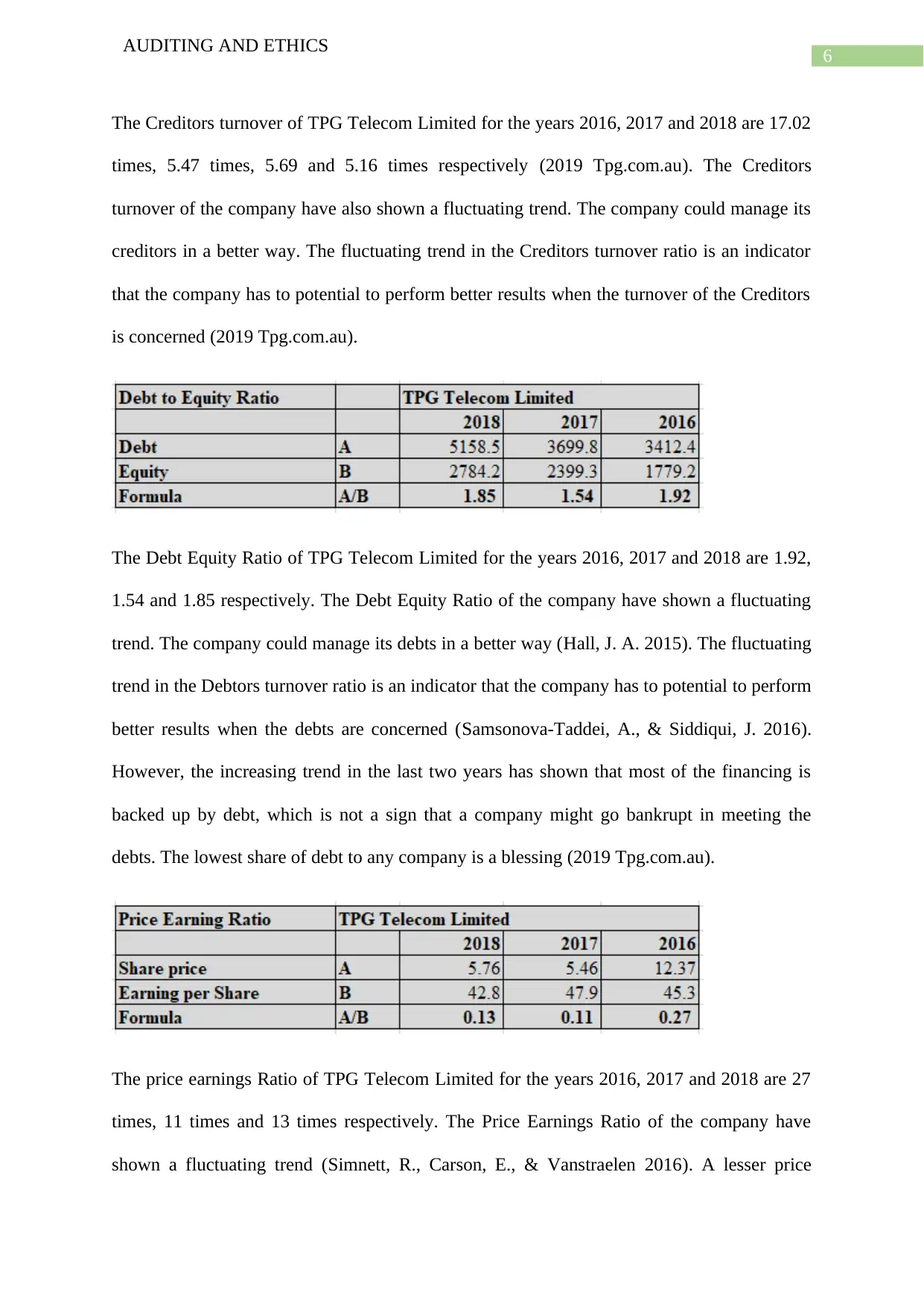

The Debt Equity Ratio of TPG Telecom Limited for the years 2016, 2017 and 2018 are 1.92,

1.54 and 1.85 respectively. The Debt Equity Ratio of the company have shown a fluctuating

trend. The company could manage its debts in a better way (Hall, J. A. 2015). The fluctuating

trend in the Debtors turnover ratio is an indicator that the company has to potential to perform

better results when the debts are concerned (Samsonova-Taddei, A., & Siddiqui, J. 2016).

However, the increasing trend in the last two years has shown that most of the financing is

backed up by debt, which is not a sign that a company might go bankrupt in meeting the

debts. The lowest share of debt to any company is a blessing (2019 Tpg.com.au).

The price earnings Ratio of TPG Telecom Limited for the years 2016, 2017 and 2018 are 27

times, 11 times and 13 times respectively. The Price Earnings Ratio of the company have

shown a fluctuating trend (Simnett, R., Carson, E., & Vanstraelen 2016). A lesser price

AUDITING AND ETHICS

The Creditors turnover of TPG Telecom Limited for the years 2016, 2017 and 2018 are 17.02

times, 5.47 times, 5.69 and 5.16 times respectively (2019 Tpg.com.au). The Creditors

turnover of the company have also shown a fluctuating trend. The company could manage its

creditors in a better way. The fluctuating trend in the Creditors turnover ratio is an indicator

that the company has to potential to perform better results when the turnover of the Creditors

is concerned (2019 Tpg.com.au).

The Debt Equity Ratio of TPG Telecom Limited for the years 2016, 2017 and 2018 are 1.92,

1.54 and 1.85 respectively. The Debt Equity Ratio of the company have shown a fluctuating

trend. The company could manage its debts in a better way (Hall, J. A. 2015). The fluctuating

trend in the Debtors turnover ratio is an indicator that the company has to potential to perform

better results when the debts are concerned (Samsonova-Taddei, A., & Siddiqui, J. 2016).

However, the increasing trend in the last two years has shown that most of the financing is

backed up by debt, which is not a sign that a company might go bankrupt in meeting the

debts. The lowest share of debt to any company is a blessing (2019 Tpg.com.au).

The price earnings Ratio of TPG Telecom Limited for the years 2016, 2017 and 2018 are 27

times, 11 times and 13 times respectively. The Price Earnings Ratio of the company have

shown a fluctuating trend (Simnett, R., Carson, E., & Vanstraelen 2016). A lesser price

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7

AUDITING AND ETHICS

earning shows that the investors of the company have expectations of lower returns, which

reduces their confidence to invest in the company (Taplin, R., Singh, A., Kerr, R., & Lee, A.

2018). The price earnings of TPG Telecom Limited have shown an increasing trend in the

year 2018, which is a sign that the investors have an expectation of higher returns (Kaptein,

M. 2015). However, the price earning of the company for all the three years is very low, in

comparison to the ideal price earnings ratio that is prevailing in the market (2019

Tpg.com.au).

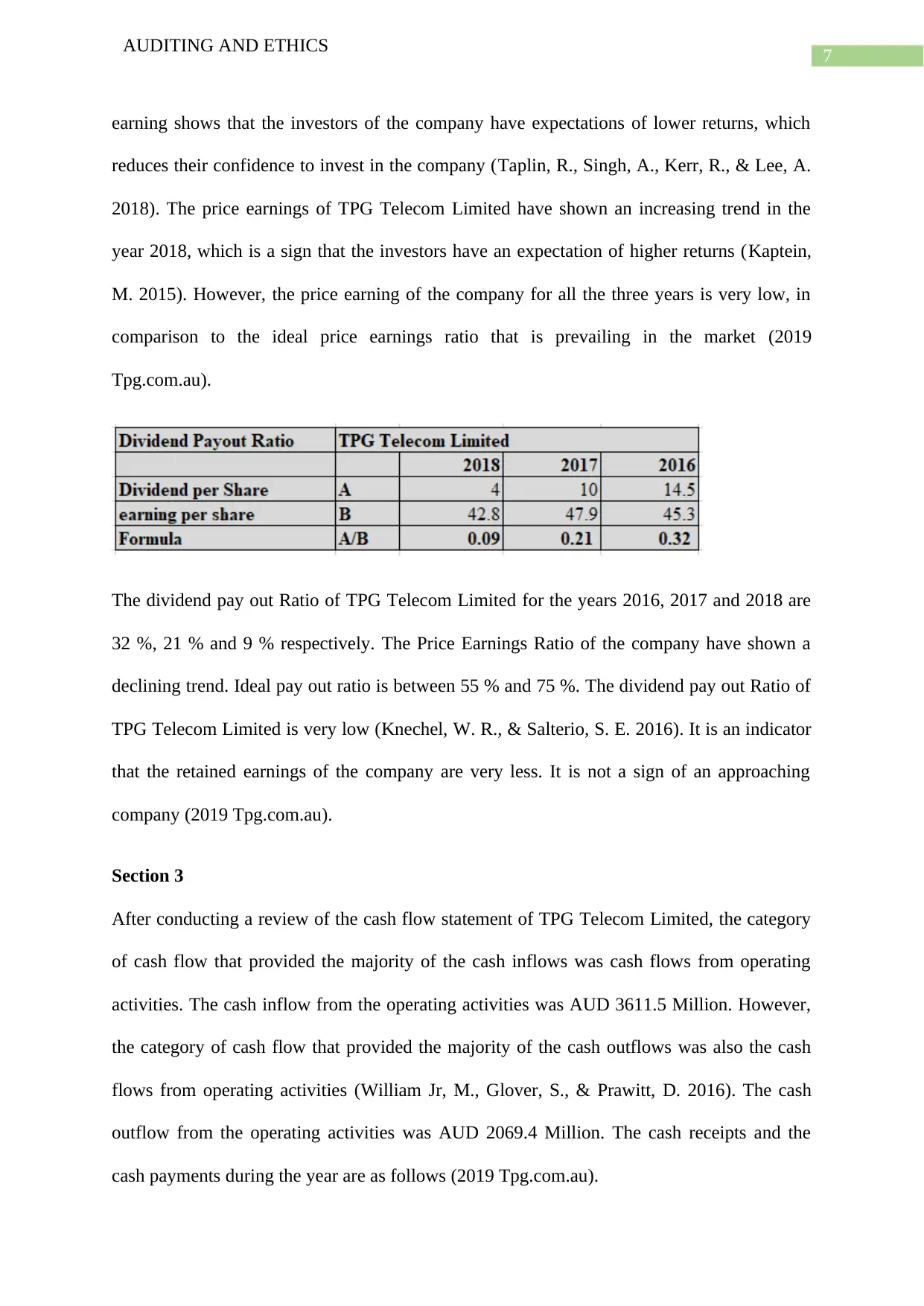

The dividend pay out Ratio of TPG Telecom Limited for the years 2016, 2017 and 2018 are

32 %, 21 % and 9 % respectively. The Price Earnings Ratio of the company have shown a

declining trend. Ideal pay out ratio is between 55 % and 75 %. The dividend pay out Ratio of

TPG Telecom Limited is very low (Knechel, W. R., & Salterio, S. E. 2016). It is an indicator

that the retained earnings of the company are very less. It is not a sign of an approaching

company (2019 Tpg.com.au).

Section 3

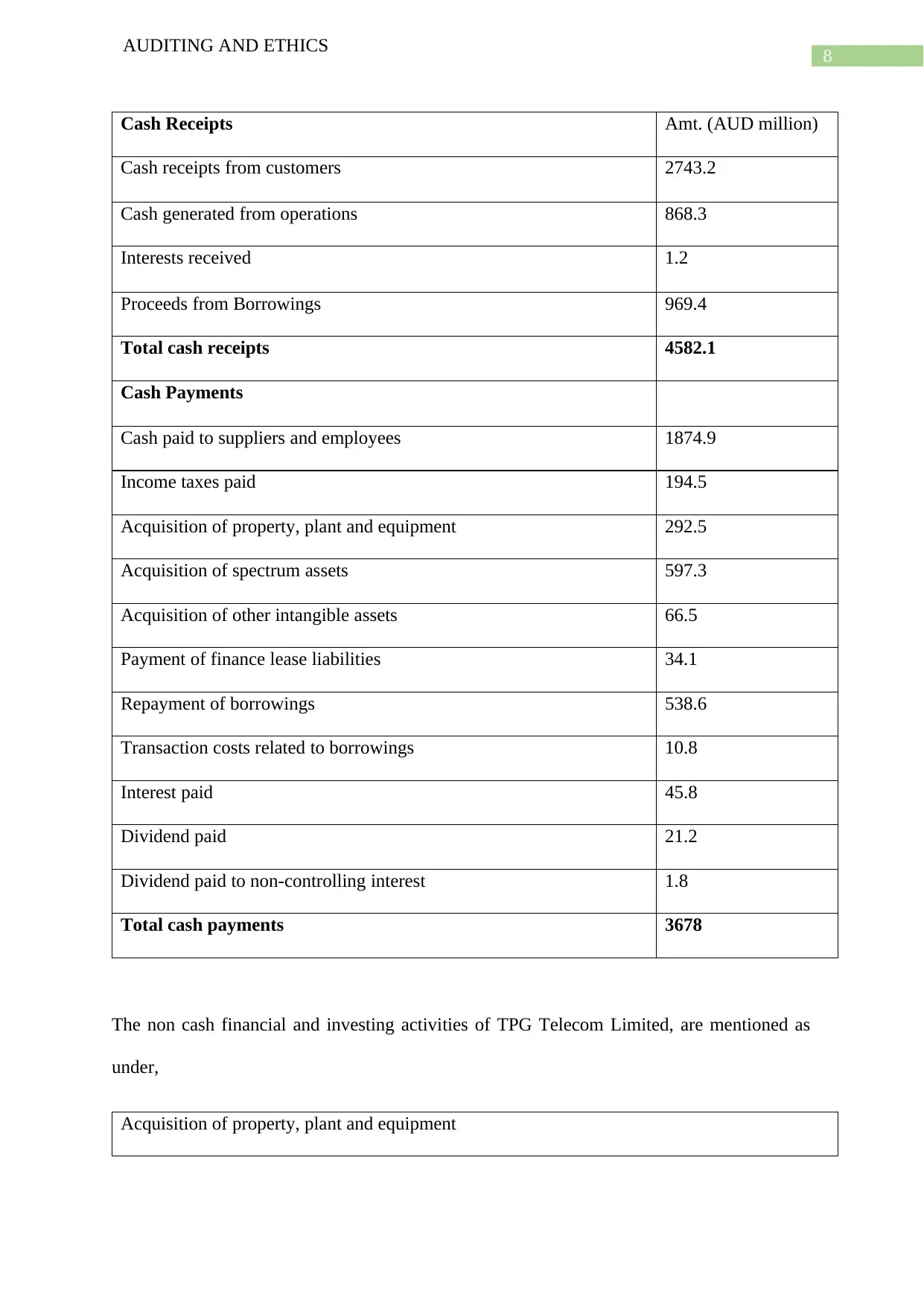

After conducting a review of the cash flow statement of TPG Telecom Limited, the category

of cash flow that provided the majority of the cash inflows was cash flows from operating

activities. The cash inflow from the operating activities was AUD 3611.5 Million. However,

the category of cash flow that provided the majority of the cash outflows was also the cash

flows from operating activities (William Jr, M., Glover, S., & Prawitt, D. 2016). The cash

outflow from the operating activities was AUD 2069.4 Million. The cash receipts and the

cash payments during the year are as follows (2019 Tpg.com.au).

AUDITING AND ETHICS

earning shows that the investors of the company have expectations of lower returns, which

reduces their confidence to invest in the company (Taplin, R., Singh, A., Kerr, R., & Lee, A.

2018). The price earnings of TPG Telecom Limited have shown an increasing trend in the

year 2018, which is a sign that the investors have an expectation of higher returns (Kaptein,

M. 2015). However, the price earning of the company for all the three years is very low, in

comparison to the ideal price earnings ratio that is prevailing in the market (2019

Tpg.com.au).

The dividend pay out Ratio of TPG Telecom Limited for the years 2016, 2017 and 2018 are

32 %, 21 % and 9 % respectively. The Price Earnings Ratio of the company have shown a

declining trend. Ideal pay out ratio is between 55 % and 75 %. The dividend pay out Ratio of

TPG Telecom Limited is very low (Knechel, W. R., & Salterio, S. E. 2016). It is an indicator

that the retained earnings of the company are very less. It is not a sign of an approaching

company (2019 Tpg.com.au).

Section 3

After conducting a review of the cash flow statement of TPG Telecom Limited, the category

of cash flow that provided the majority of the cash inflows was cash flows from operating

activities. The cash inflow from the operating activities was AUD 3611.5 Million. However,

the category of cash flow that provided the majority of the cash outflows was also the cash

flows from operating activities (William Jr, M., Glover, S., & Prawitt, D. 2016). The cash

outflow from the operating activities was AUD 2069.4 Million. The cash receipts and the

cash payments during the year are as follows (2019 Tpg.com.au).

8

AUDITING AND ETHICS

Cash Receipts Amt. (AUD million)

Cash receipts from customers 2743.2

Cash generated from operations 868.3

Interests received 1.2

Proceeds from Borrowings 969.4

Total cash receipts 4582.1

Cash Payments

Cash paid to suppliers and employees 1874.9

Income taxes paid 194.5

Acquisition of property, plant and equipment 292.5

Acquisition of spectrum assets 597.3

Acquisition of other intangible assets 66.5

Payment of finance lease liabilities 34.1

Repayment of borrowings 538.6

Transaction costs related to borrowings 10.8

Interest paid 45.8

Dividend paid 21.2

Dividend paid to non-controlling interest 1.8

Total cash payments 3678

The non cash financial and investing activities of TPG Telecom Limited, are mentioned as

under,

Acquisition of property, plant and equipment

AUDITING AND ETHICS

Cash Receipts Amt. (AUD million)

Cash receipts from customers 2743.2

Cash generated from operations 868.3

Interests received 1.2

Proceeds from Borrowings 969.4

Total cash receipts 4582.1

Cash Payments

Cash paid to suppliers and employees 1874.9

Income taxes paid 194.5

Acquisition of property, plant and equipment 292.5

Acquisition of spectrum assets 597.3

Acquisition of other intangible assets 66.5

Payment of finance lease liabilities 34.1

Repayment of borrowings 538.6

Transaction costs related to borrowings 10.8

Interest paid 45.8

Dividend paid 21.2

Dividend paid to non-controlling interest 1.8

Total cash payments 3678

The non cash financial and investing activities of TPG Telecom Limited, are mentioned as

under,

Acquisition of property, plant and equipment

9

AUDITING AND ETHICS

Acquisition of spectrum assets

Acquisition of other intangible assets

The going concern risk of this company is quite high (Zarefar, A., & Zarefar, A. 2016). The

ratio analysis that is being conducted on the business shows that the operations of the

business are not being carried on at an effective rate (Brennan, N. 2016). The trend in going

concern risk is the negative trend. The costs of the company are increasing, which are not met

by the sales that are taking place (Mela, N. F., & Zarefar, A. 2016).

The audit procedure that could be followed in this case could be the procedure of inspection.

It can be defined as the process of verification and vouching the documents (Ferramosca, S.,

D'Onza, G., & Allegrini, M. 2017). This procedure is of utmost importance, and it forms

around 60 percent of the audit work, including the inspection of the documents (Duska, R. F.,

Duska, B. S., & Kury, K. W. 2018). The turnover of the company is favourable, however the

trends do not show promising results. This is an indicator that the company needs to go

through proper inspection of the documents. The invoices need to be rechecked (Gaynor, G.

B., Janvrin, D. J., Pittman, M. K., Pevzner, M. B., & White, L. F. 2015).

The audit has been performed by the top big 4 accounting firm that is KPMG. The type of the

audit report that has been provided by the KPMG is a qualified report (SURYANTO, 2017).

A qualified report refers to the audit opinion, which is expressed to the financial statements

that are not prepared in all material respect while those misstatements are not pervasive

(Helin, S. and Babri, M., 2015).

AUDITING AND ETHICS

Acquisition of spectrum assets

Acquisition of other intangible assets

The going concern risk of this company is quite high (Zarefar, A., & Zarefar, A. 2016). The

ratio analysis that is being conducted on the business shows that the operations of the

business are not being carried on at an effective rate (Brennan, N. 2016). The trend in going

concern risk is the negative trend. The costs of the company are increasing, which are not met

by the sales that are taking place (Mela, N. F., & Zarefar, A. 2016).

The audit procedure that could be followed in this case could be the procedure of inspection.

It can be defined as the process of verification and vouching the documents (Ferramosca, S.,

D'Onza, G., & Allegrini, M. 2017). This procedure is of utmost importance, and it forms

around 60 percent of the audit work, including the inspection of the documents (Duska, R. F.,

Duska, B. S., & Kury, K. W. 2018). The turnover of the company is favourable, however the

trends do not show promising results. This is an indicator that the company needs to go

through proper inspection of the documents. The invoices need to be rechecked (Gaynor, G.

B., Janvrin, D. J., Pittman, M. K., Pevzner, M. B., & White, L. F. 2015).

The audit has been performed by the top big 4 accounting firm that is KPMG. The type of the

audit report that has been provided by the KPMG is a qualified report (SURYANTO, 2017).

A qualified report refers to the audit opinion, which is expressed to the financial statements

that are not prepared in all material respect while those misstatements are not pervasive

(Helin, S. and Babri, M., 2015).

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

10

AUDITING AND ETHICS

References

(2019). Tpg.com.au. Retrieved 2 September 2019, from

https://www.tpg.com.au/about/pdfs/TPM%20Group%20-%20Statutory

%20Accounts%20-%20FY18v16%20-%20Secure.pdf

Brennan, N. (2016). Are Ethics Relevant to the Practice of Professional

Accounting?. Accountancy Plus, (1), 23-24.

Bringselius, L. (2018). Efficiency, economy and effectiveness—but what about ethics?

Supreme audit institutions at a critical juncture. Public Money & Management,

38(2), 105-110.

Duska, R. F., Duska, B. S., & Kury, K. W. (2018). Accounting ethics. Wiley-Blackwell.

Ferramosca, S., D'Onza, G., & Allegrini, M. (2017). The internal auditing of corporate

governance, risk management and ethics: comparing banks with other

industries. International Journal of Business Governance and Ethics, 12(3), 218-

240.

Gaynor, G. B., Janvrin, D. J., Pittman, M. K., Pevzner, M. B., & White, L. F. (2015).

Comments of the Auditing Standards Committee of the Auditing Section of the

American Accounting Association on IESBA Consultation Paper: Improving the

Structure of the Code of Ethics for Professional Accountants: Participating

Committee Members. Current Issues in Auditing, 9(1), C12-C17.

Hall, J. A. (2015). Information technology auditing. Cengage Learning.

Helin, S. and Babri, M., 2015. Travelling with a code of ethics: a contextual study of a

Swedish MNC auditing a Chinese supplier. Journal of Cleaner Production, 107,

pp.41-53.

AUDITING AND ETHICS

References

(2019). Tpg.com.au. Retrieved 2 September 2019, from

https://www.tpg.com.au/about/pdfs/TPM%20Group%20-%20Statutory

%20Accounts%20-%20FY18v16%20-%20Secure.pdf

Brennan, N. (2016). Are Ethics Relevant to the Practice of Professional

Accounting?. Accountancy Plus, (1), 23-24.

Bringselius, L. (2018). Efficiency, economy and effectiveness—but what about ethics?

Supreme audit institutions at a critical juncture. Public Money & Management,

38(2), 105-110.

Duska, R. F., Duska, B. S., & Kury, K. W. (2018). Accounting ethics. Wiley-Blackwell.

Ferramosca, S., D'Onza, G., & Allegrini, M. (2017). The internal auditing of corporate

governance, risk management and ethics: comparing banks with other

industries. International Journal of Business Governance and Ethics, 12(3), 218-

240.

Gaynor, G. B., Janvrin, D. J., Pittman, M. K., Pevzner, M. B., & White, L. F. (2015).

Comments of the Auditing Standards Committee of the Auditing Section of the

American Accounting Association on IESBA Consultation Paper: Improving the

Structure of the Code of Ethics for Professional Accountants: Participating

Committee Members. Current Issues in Auditing, 9(1), C12-C17.

Hall, J. A. (2015). Information technology auditing. Cengage Learning.

Helin, S. and Babri, M., 2015. Travelling with a code of ethics: a contextual study of a

Swedish MNC auditing a Chinese supplier. Journal of Cleaner Production, 107,

pp.41-53.

11

AUDITING AND ETHICS

Kaptein, M. (2015). The effectiveness of ethics programs: The role of scope, composition,

and sequence. Journal of Business Ethics, 132(2), 415-431.

Knechel, W. R., & Salterio, S. E. (2016). Auditing: Assurance and risk. Routledge.

Mela, N. F., & Zarefar, A. (2016). The Relationship of professional commitment of auditing

student and anticipatory socialization toward whistleblowing

intention. Procedia-Social and Behavioral Sciences, 219, 507-512.

Samsonova-Taddei, A., & Siddiqui, J. (2016). Regulation and the promotion of audit ethics:

Analysis of the content of the EU’s policy. Journal of Business Ethics, 139(1),

183-195.

Simnett, R., Carson, E., & Vanstraelen, A. (2016). International archival auditing and

assurance research: Trends, methodological issues, and opportunities. Auditing:

A Journal of Practice & Theory, 35(3), 1-32.

SURYANTO, T. (2017). Cultural Ethics and Consequences in Whistle-Blowing Among

Professional Accountants: An Empirical Analysis. Journal of Applied Economic

Sciences, 12(6).

Taplin, R., Singh, A., Kerr, R., & Lee, A. (2018). The use of short role-plays for an ethics

intervention in university auditing courses. Accounting Education, 27(4), 383-

402.

William Jr, M., Glover, S., & Prawitt, D. (2016). Auditing and assurance services: A

systematic approach. McGraw-Hill Education.

Zarefar, A., & Zarefar, A. (2016). The Influence of Ethics, experience and competency

toward the quality of auditing with professional auditor scepticism as a

Moderating Variable. Procedia-Social and Behavioral Sciences, 219, 828-832.

AUDITING AND ETHICS

Kaptein, M. (2015). The effectiveness of ethics programs: The role of scope, composition,

and sequence. Journal of Business Ethics, 132(2), 415-431.

Knechel, W. R., & Salterio, S. E. (2016). Auditing: Assurance and risk. Routledge.

Mela, N. F., & Zarefar, A. (2016). The Relationship of professional commitment of auditing

student and anticipatory socialization toward whistleblowing

intention. Procedia-Social and Behavioral Sciences, 219, 507-512.

Samsonova-Taddei, A., & Siddiqui, J. (2016). Regulation and the promotion of audit ethics:

Analysis of the content of the EU’s policy. Journal of Business Ethics, 139(1),

183-195.

Simnett, R., Carson, E., & Vanstraelen, A. (2016). International archival auditing and

assurance research: Trends, methodological issues, and opportunities. Auditing:

A Journal of Practice & Theory, 35(3), 1-32.

SURYANTO, T. (2017). Cultural Ethics and Consequences in Whistle-Blowing Among

Professional Accountants: An Empirical Analysis. Journal of Applied Economic

Sciences, 12(6).

Taplin, R., Singh, A., Kerr, R., & Lee, A. (2018). The use of short role-plays for an ethics

intervention in university auditing courses. Accounting Education, 27(4), 383-

402.

William Jr, M., Glover, S., & Prawitt, D. (2016). Auditing and assurance services: A

systematic approach. McGraw-Hill Education.

Zarefar, A., & Zarefar, A. (2016). The Influence of Ethics, experience and competency

toward the quality of auditing with professional auditor scepticism as a

Moderating Variable. Procedia-Social and Behavioral Sciences, 219, 828-832.

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.