Auditing and Ethics: Materiality and Preliminary Analytical Review

VerifiedAdded on 2023/01/04

|16

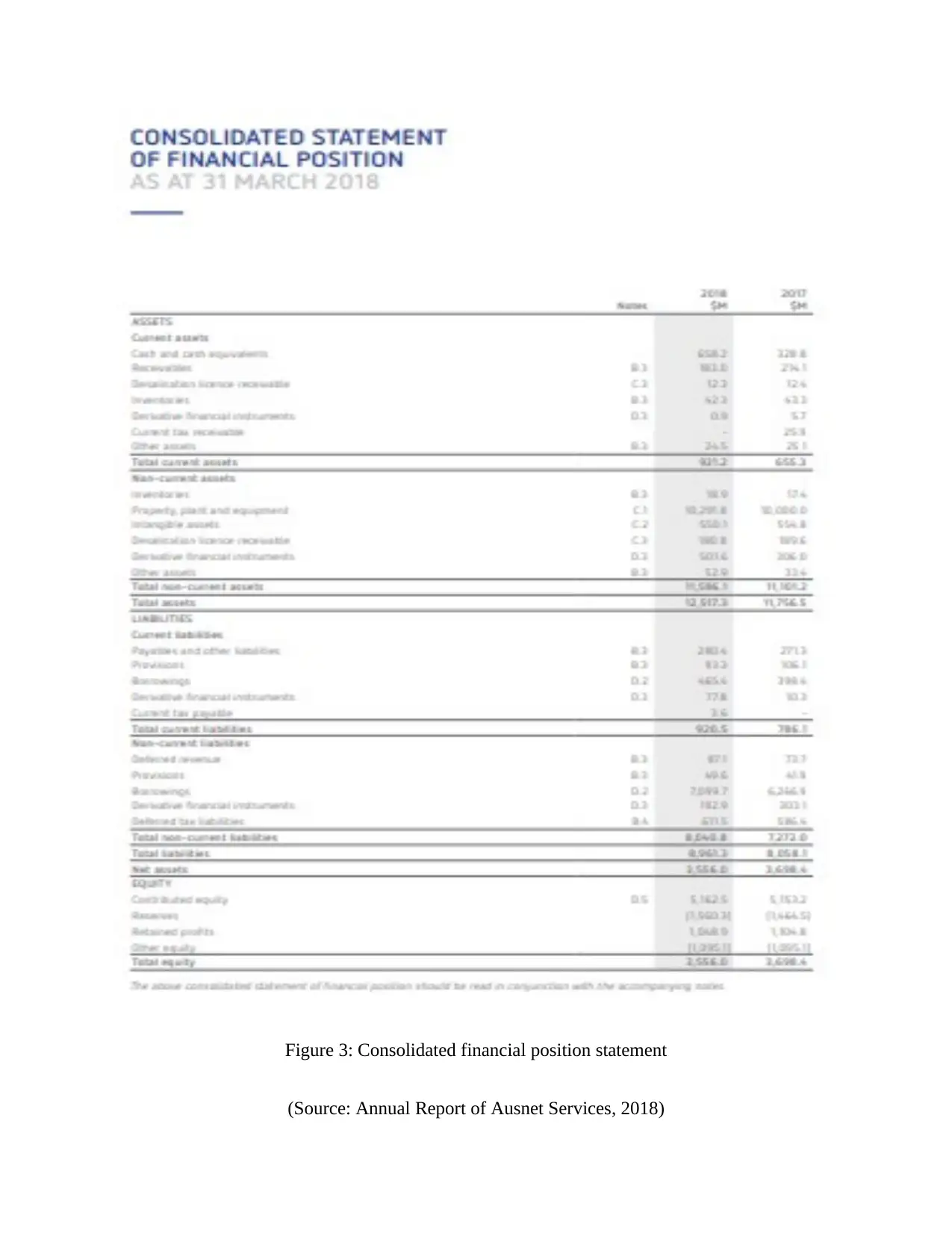

|3091

|82

AI Summary

This document discusses the concepts of materiality and preliminary analytical review in auditing and ethics. It explains how materiality is used by auditors to assess the impact of misstatements on financial statements. It also explores the importance of preliminary analytical review in identifying material misstatement risks. The document includes case studies and examples related to Ausnet Service Limited.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Auditing and ethics

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Table of Contents

Section 1..........................................................................................................................................3

Section 2..........................................................................................................................................4

Section 3..........................................................................................................................................8

References......................................................................................................................................11

Section 1..........................................................................................................................................3

Section 2..........................................................................................................................................4

Section 3..........................................................................................................................................8

References......................................................................................................................................11

SECTION 1

Audit materiality is considered as the most significant concept meant for auditors. Further, the

misstatement inclusive of errors & omissions, are stated to be material, in a situation where, in

aggregate or individual manner, they are likely to impact the user’s decision of users reasonably

based on financial statements (Lakis&Masiulevičius, 2017). Furthermore, the materiality concept

is thus a core element to the audit; it is applicable by the auditors at the stage of planning and

while conducting the audit as well as evaluating the affect of monitored audit misstatements and

invalid misstatements, if present on the financial statements (DeZoort, Holt, & Stanley, 2018).

In auditing, materiality is convention related with the transactional significance, divergence or an

amount. The aim of an audit of the financial statement is to allow the auditor state an opinion if

or if not there is the financial statement preparation, in every material respect, with adherence to

determine financial reporting structure (Christensen et al. 2018). The representation the in the

standard report of auditor in regards with the fair presentation, and in conformity with the

acceptable accounting standards shows the belief of auditor that the financial statements are

considered as awhile with no material misstatement (Graham, Bedard, & Dutta, 2018).

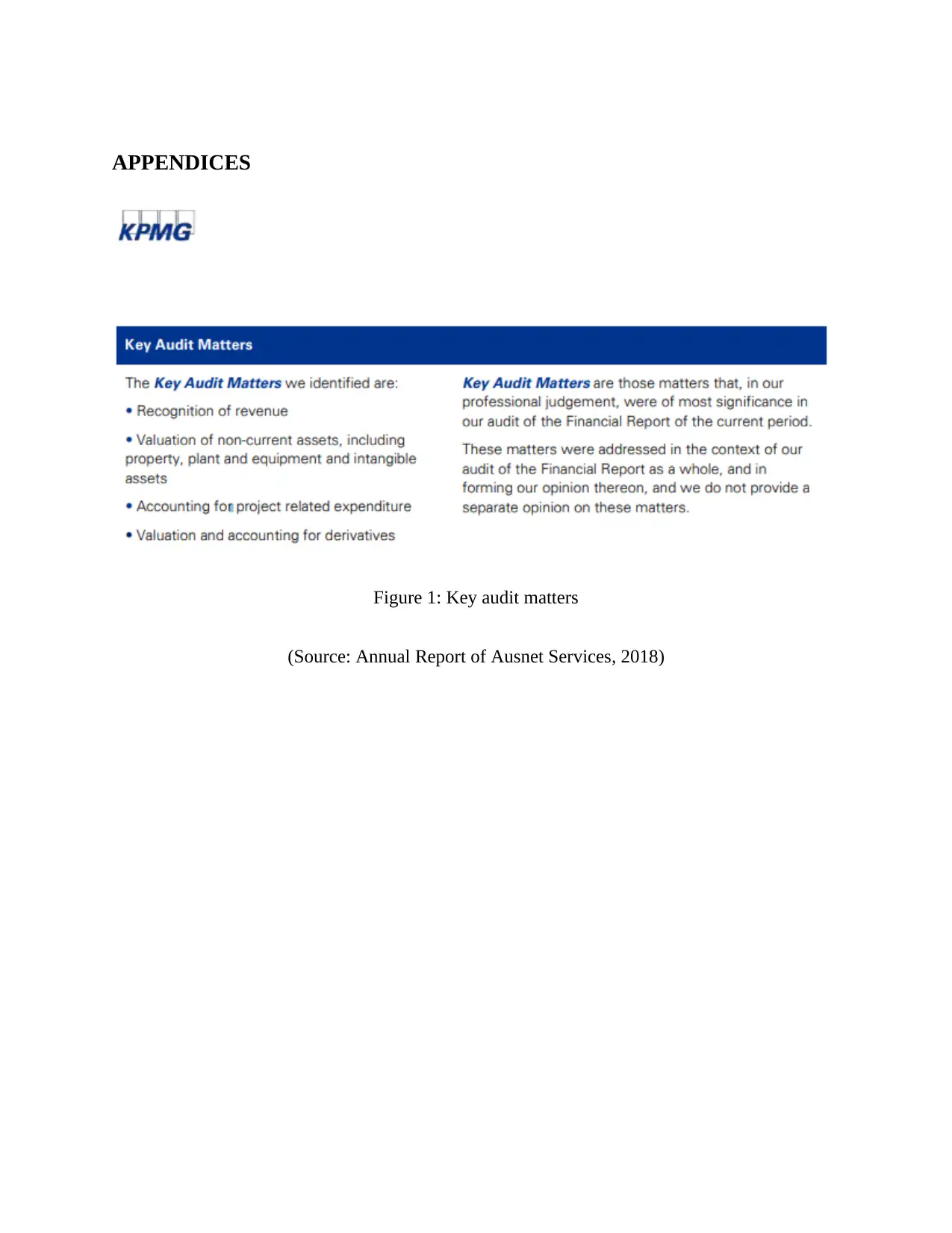

In case of Ausnet Service Limited, the significant audit matter which is identified by the

company and the manner in which auditor address those matters by considering the level of

materiality for the year ending in 2018 , are as follows –

Valuation and accounting for derivatives.

Recognition of Revenue.

Valuation of the Asset such as Property, plant, and equipment.

Audit materiality is considered as the most significant concept meant for auditors. Further, the

misstatement inclusive of errors & omissions, are stated to be material, in a situation where, in

aggregate or individual manner, they are likely to impact the user’s decision of users reasonably

based on financial statements (Lakis&Masiulevičius, 2017). Furthermore, the materiality concept

is thus a core element to the audit; it is applicable by the auditors at the stage of planning and

while conducting the audit as well as evaluating the affect of monitored audit misstatements and

invalid misstatements, if present on the financial statements (DeZoort, Holt, & Stanley, 2018).

In auditing, materiality is convention related with the transactional significance, divergence or an

amount. The aim of an audit of the financial statement is to allow the auditor state an opinion if

or if not there is the financial statement preparation, in every material respect, with adherence to

determine financial reporting structure (Christensen et al. 2018). The representation the in the

standard report of auditor in regards with the fair presentation, and in conformity with the

acceptable accounting standards shows the belief of auditor that the financial statements are

considered as awhile with no material misstatement (Graham, Bedard, & Dutta, 2018).

In case of Ausnet Service Limited, the significant audit matter which is identified by the

company and the manner in which auditor address those matters by considering the level of

materiality for the year ending in 2018 , are as follows –

Valuation and accounting for derivatives.

Recognition of Revenue.

Valuation of the Asset such as Property, plant, and equipment.

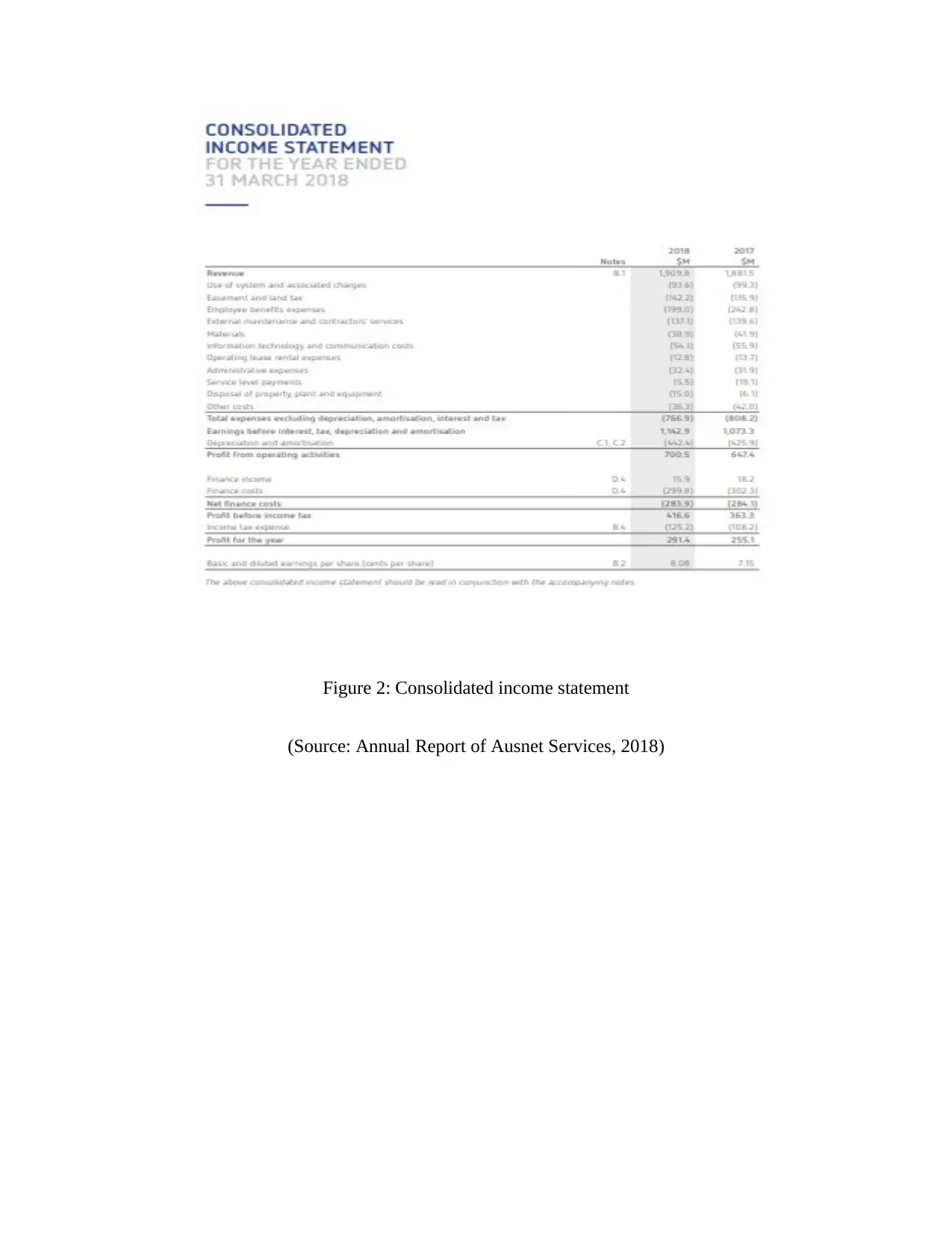

There are significant changes in the derivative financial instruments. The liability for the

derivative instrument has been significantly increased in 2018 in comparison to the previous

year. Since it is considered as the material amount and the obligation of the entity enhanced,

therefore, the auditor has to check whether it is appropriately recognized at their fair value (Lu,

Wu, & Yu, 2017). Further, the revenue of the company is a material part of the company due to

the nature of the regulatory aspect and process of the billing for transmission of electricity,

distribution of gas and electricity (Ishak, & Nor, 2018). There is inherent complexity in the

billing process related to the estimation of energy consumed and the identification of relevant

tariff rates. Moreover, the company has disposed ofa significant amount of property, plant, and

equipment (Chen, Gul, Veeraraghavan, &Zolotoy, 2015). Out of the total amount of $ 10,291.8

M, disposal of $ 15 M is considered as a material amount. The auditor should discuss the same

with the management, and identify whether the company used these proceeds in the payment of

any obligation. It may lead to an impact on going concern capability of the company.

Apart from the above aspects, the company has provided the disclosures regarding the

contingencies, event occurring after balance sheet date, non-adoption of the new accounting

standard and others. Although the board of director of the company reported some contingent

liabilities which are considered material, the auditor should analyze whether any provision is

required on those liabilities. Some disclosures are given in the financial statement related to the

event occurring after balancesheet date such as Dividend, Singapore Stock Exchange delisting,

and some matters. The auditor should evaluate whether it significantly affect the decision of the

users, and accordingly carried out the procedures.

derivative instrument has been significantly increased in 2018 in comparison to the previous

year. Since it is considered as the material amount and the obligation of the entity enhanced,

therefore, the auditor has to check whether it is appropriately recognized at their fair value (Lu,

Wu, & Yu, 2017). Further, the revenue of the company is a material part of the company due to

the nature of the regulatory aspect and process of the billing for transmission of electricity,

distribution of gas and electricity (Ishak, & Nor, 2018). There is inherent complexity in the

billing process related to the estimation of energy consumed and the identification of relevant

tariff rates. Moreover, the company has disposed ofa significant amount of property, plant, and

equipment (Chen, Gul, Veeraraghavan, &Zolotoy, 2015). Out of the total amount of $ 10,291.8

M, disposal of $ 15 M is considered as a material amount. The auditor should discuss the same

with the management, and identify whether the company used these proceeds in the payment of

any obligation. It may lead to an impact on going concern capability of the company.

Apart from the above aspects, the company has provided the disclosures regarding the

contingencies, event occurring after balance sheet date, non-adoption of the new accounting

standard and others. Although the board of director of the company reported some contingent

liabilities which are considered material, the auditor should analyze whether any provision is

required on those liabilities. Some disclosures are given in the financial statement related to the

event occurring after balancesheet date such as Dividend, Singapore Stock Exchange delisting,

and some matters. The auditor should evaluate whether it significantly affect the decision of the

users, and accordingly carried out the procedures.

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

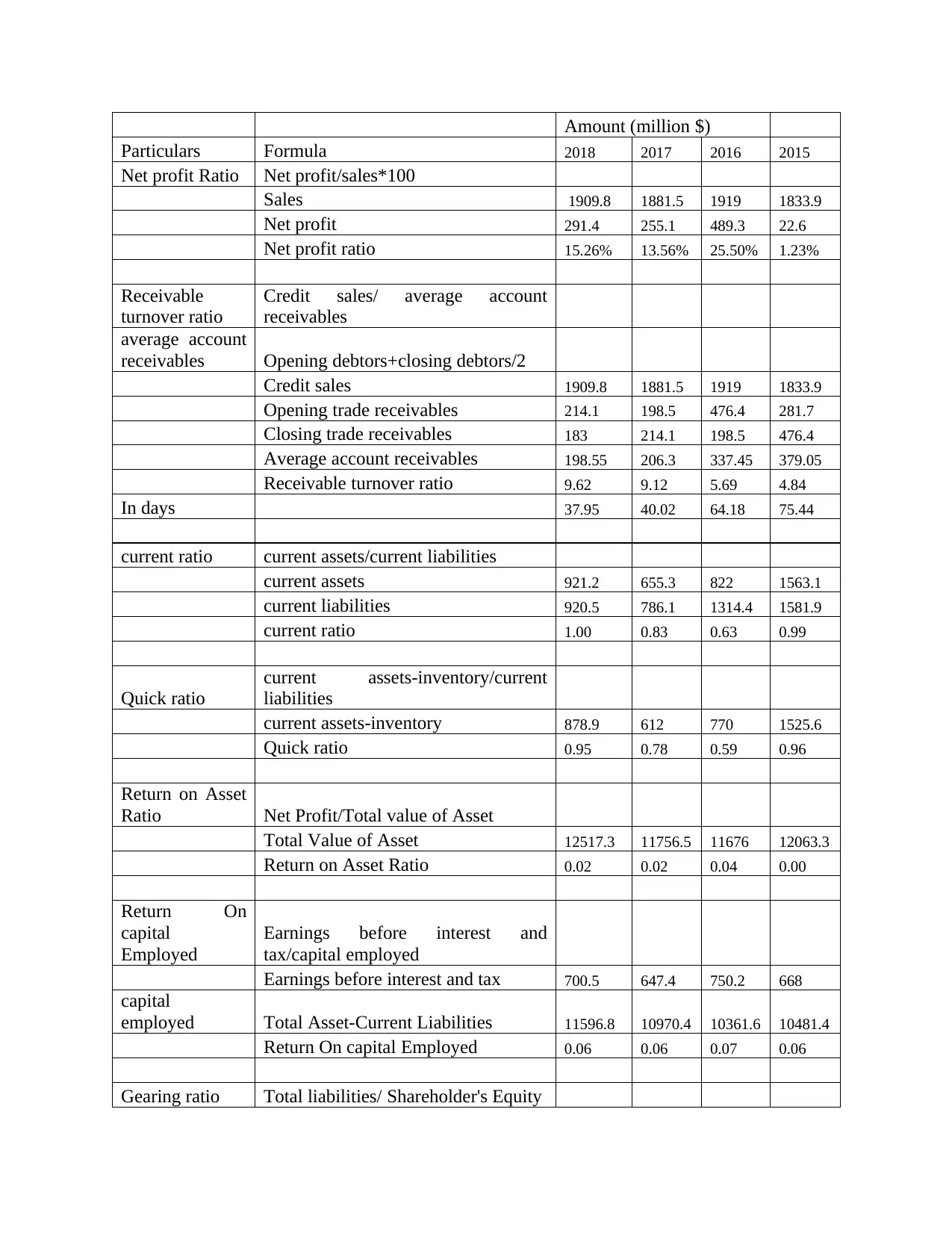

SECTION 2

Preliminary analytical reviews are conducted to hold an interpretation of the business and its

related environments such as financial performance comparative to last years and valid industry

to help in considering the material misstatement risks to identify the scope, timing and nature of

an audit (Hines, Masli, Mauldin, & Peters, 2015). Preliminary analytical review is a risk

assessment as mandatory by ISA 315, has been referred as an analytical process as well as

management inquiry process applicable to the audit’s planning stage (Knechel&Salterio, 2016).

Further, in the risk assessment standards, there is a need for auditors to perform a risk assessment

process that comprises of the analytical process and managerial inquiries. In this way, the risk

assessment process is inclusive of conducting observation and detection generally concentrated

on acquiring a better understanding of the internal control and considerable contracts that are into

account (Trotman, 2015). Therefore, the preliminary analytical review involves a considerable

element of the risk assessment procedures. According to the auditing standards, there should be

the applicability of analytical procedures in the planning phases of the audit. At the time of the

crucial engagement point, auditors make use of analytical procedures to determine possible issue

areas so that resultant audit work can be developed to make a reduction in the risk of

considerable material misstatement (Brasel, Doxey, Grenier, & Reffett, 2016). At a standard

starting point, the analytical process at the time period of plan offers an organized approach, for

becoming familiar with the business of the client. For this aspect, auditors are required to

consider that preliminary analytical procedures are dependent on the unaudited data, so they

must remember the efficiency of control on their reliability while making a decision on how

much weight should place on the outcomes (Hale, Guldenmund, & Goossens, 2017).

Table 1 Ratio analysis of Ausnet Service Limited

Preliminary analytical reviews are conducted to hold an interpretation of the business and its

related environments such as financial performance comparative to last years and valid industry

to help in considering the material misstatement risks to identify the scope, timing and nature of

an audit (Hines, Masli, Mauldin, & Peters, 2015). Preliminary analytical review is a risk

assessment as mandatory by ISA 315, has been referred as an analytical process as well as

management inquiry process applicable to the audit’s planning stage (Knechel&Salterio, 2016).

Further, in the risk assessment standards, there is a need for auditors to perform a risk assessment

process that comprises of the analytical process and managerial inquiries. In this way, the risk

assessment process is inclusive of conducting observation and detection generally concentrated

on acquiring a better understanding of the internal control and considerable contracts that are into

account (Trotman, 2015). Therefore, the preliminary analytical review involves a considerable

element of the risk assessment procedures. According to the auditing standards, there should be

the applicability of analytical procedures in the planning phases of the audit. At the time of the

crucial engagement point, auditors make use of analytical procedures to determine possible issue

areas so that resultant audit work can be developed to make a reduction in the risk of

considerable material misstatement (Brasel, Doxey, Grenier, & Reffett, 2016). At a standard

starting point, the analytical process at the time period of plan offers an organized approach, for

becoming familiar with the business of the client. For this aspect, auditors are required to

consider that preliminary analytical procedures are dependent on the unaudited data, so they

must remember the efficiency of control on their reliability while making a decision on how

much weight should place on the outcomes (Hale, Guldenmund, & Goossens, 2017).

Table 1 Ratio analysis of Ausnet Service Limited

Amount (million $)

Particulars Formula 2018 2017 2016 2015

Net profit Ratio Net profit/sales*100

Sales 1909.8 1881.5 1919 1833.9

Net profit 291.4 255.1 489.3 22.6

Net profit ratio 15.26% 13.56% 25.50% 1.23%

Receivable

turnover ratio

Credit sales/ average account

receivables

average account

receivables Opening debtors+closing debtors/2

Credit sales 1909.8 1881.5 1919 1833.9

Opening trade receivables 214.1 198.5 476.4 281.7

Closing trade receivables 183 214.1 198.5 476.4

Average account receivables 198.55 206.3 337.45 379.05

Receivable turnover ratio 9.62 9.12 5.69 4.84

In days 37.95 40.02 64.18 75.44

current ratio current assets/current liabilities

current assets 921.2 655.3 822 1563.1

current liabilities 920.5 786.1 1314.4 1581.9

current ratio 1.00 0.83 0.63 0.99

Quick ratio

current assets-inventory/current

liabilities

current assets-inventory 878.9 612 770 1525.6

Quick ratio 0.95 0.78 0.59 0.96

Return on Asset

Ratio Net Profit/Total value of Asset

Total Value of Asset 12517.3 11756.5 11676 12063.3

Return on Asset Ratio 0.02 0.02 0.04 0.00

Return On

capital

Employed

Earnings before interest and

tax/capital employed

Earnings before interest and tax 700.5 647.4 750.2 668

capital

employed Total Asset-Current Liabilities 11596.8 10970.4 10361.6 10481.4

Return On capital Employed 0.06 0.06 0.07 0.06

Gearing ratio Total liabilities/ Shareholder's Equity

Particulars Formula 2018 2017 2016 2015

Net profit Ratio Net profit/sales*100

Sales 1909.8 1881.5 1919 1833.9

Net profit 291.4 255.1 489.3 22.6

Net profit ratio 15.26% 13.56% 25.50% 1.23%

Receivable

turnover ratio

Credit sales/ average account

receivables

average account

receivables Opening debtors+closing debtors/2

Credit sales 1909.8 1881.5 1919 1833.9

Opening trade receivables 214.1 198.5 476.4 281.7

Closing trade receivables 183 214.1 198.5 476.4

Average account receivables 198.55 206.3 337.45 379.05

Receivable turnover ratio 9.62 9.12 5.69 4.84

In days 37.95 40.02 64.18 75.44

current ratio current assets/current liabilities

current assets 921.2 655.3 822 1563.1

current liabilities 920.5 786.1 1314.4 1581.9

current ratio 1.00 0.83 0.63 0.99

Quick ratio

current assets-inventory/current

liabilities

current assets-inventory 878.9 612 770 1525.6

Quick ratio 0.95 0.78 0.59 0.96

Return on Asset

Ratio Net Profit/Total value of Asset

Total Value of Asset 12517.3 11756.5 11676 12063.3

Return on Asset Ratio 0.02 0.02 0.04 0.00

Return On

capital

Employed

Earnings before interest and

tax/capital employed

Earnings before interest and tax 700.5 647.4 750.2 668

capital

employed Total Asset-Current Liabilities 11596.8 10970.4 10361.6 10481.4

Return On capital Employed 0.06 0.06 0.07 0.06

Gearing ratio Total liabilities/ Shareholder's Equity

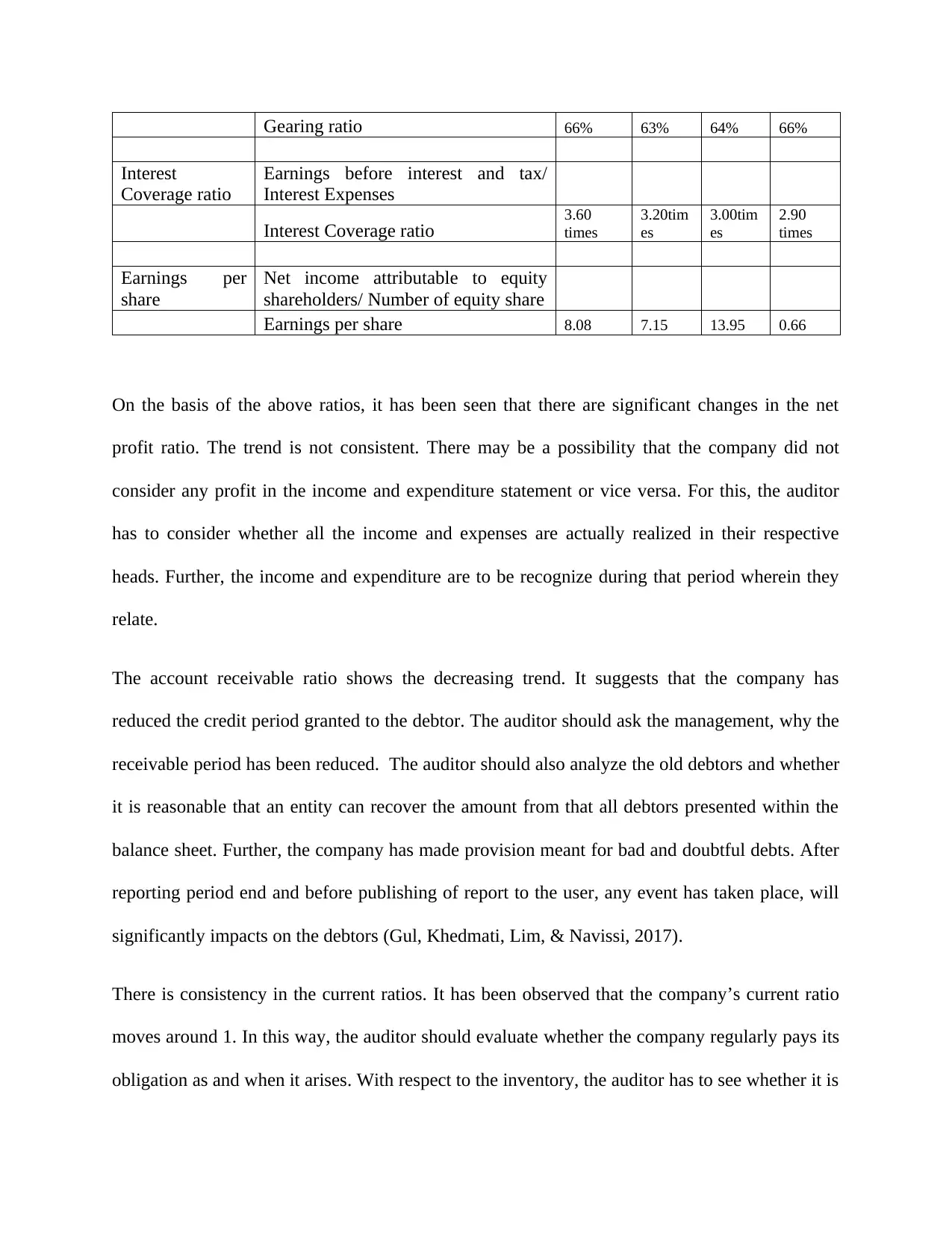

Gearing ratio 66% 63% 64% 66%

Interest

Coverage ratio

Earnings before interest and tax/

Interest Expenses

Interest Coverage ratio 3.60

times

3.20tim

es

3.00tim

es

2.90

times

Earnings per

share

Net income attributable to equity

shareholders/ Number of equity share

Earnings per share 8.08 7.15 13.95 0.66

On the basis of the above ratios, it has been seen that there are significant changes in the net

profit ratio. The trend is not consistent. There may be a possibility that the company did not

consider any profit in the income and expenditure statement or vice versa. For this, the auditor

has to consider whether all the income and expenses are actually realized in their respective

heads. Further, the income and expenditure are to be recognize during that period wherein they

relate.

The account receivable ratio shows the decreasing trend. It suggests that the company has

reduced the credit period granted to the debtor. The auditor should ask the management, why the

receivable period has been reduced. The auditor should also analyze the old debtors and whether

it is reasonable that an entity can recover the amount from that all debtors presented within the

balance sheet. Further, the company has made provision meant for bad and doubtful debts. After

reporting period end and before publishing of report to the user, any event has taken place, will

significantly impacts on the debtors (Gul, Khedmati, Lim, & Navissi, 2017).

There is consistency in the current ratios. It has been observed that the company’s current ratio

moves around 1. In this way, the auditor should evaluate whether the company regularly pays its

obligation as and when it arises. With respect to the inventory, the auditor has to see whether it is

Interest

Coverage ratio

Earnings before interest and tax/

Interest Expenses

Interest Coverage ratio 3.60

times

3.20tim

es

3.00tim

es

2.90

times

Earnings per

share

Net income attributable to equity

shareholders/ Number of equity share

Earnings per share 8.08 7.15 13.95 0.66

On the basis of the above ratios, it has been seen that there are significant changes in the net

profit ratio. The trend is not consistent. There may be a possibility that the company did not

consider any profit in the income and expenditure statement or vice versa. For this, the auditor

has to consider whether all the income and expenses are actually realized in their respective

heads. Further, the income and expenditure are to be recognize during that period wherein they

relate.

The account receivable ratio shows the decreasing trend. It suggests that the company has

reduced the credit period granted to the debtor. The auditor should ask the management, why the

receivable period has been reduced. The auditor should also analyze the old debtors and whether

it is reasonable that an entity can recover the amount from that all debtors presented within the

balance sheet. Further, the company has made provision meant for bad and doubtful debts. After

reporting period end and before publishing of report to the user, any event has taken place, will

significantly impacts on the debtors (Gul, Khedmati, Lim, & Navissi, 2017).

There is consistency in the current ratios. It has been observed that the company’s current ratio

moves around 1. In this way, the auditor should evaluate whether the company regularly pays its

obligation as and when it arises. With respect to the inventory, the auditor has to see whether it is

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

valued as per the applicable accounting standard, whether the entity has control over the

inventory recognized in the financial statement, all old or absolute inventory has not been

recognized as a part of the inventory and many other related aspects (Annual Report of Ausnet

Services Ltd, 2015).

There is the consistency in the, Return on Capital Employed Ratio, Interest Coverage Ratio,

Gearing Ratio and Return on Assets Ratio. The auditor should identify whether all the assets,

liabilities which are presented in the financial statement are existed at the year-end, whether the

company has the right to utilize its assets and responsible for the liabilities.

There is a significant difference in the Earning per share ratio of the company for the period

between 2015 and 2016. The auditor should refer his obligations with respect to the prior period

item and extend the audit procedure, if essential.

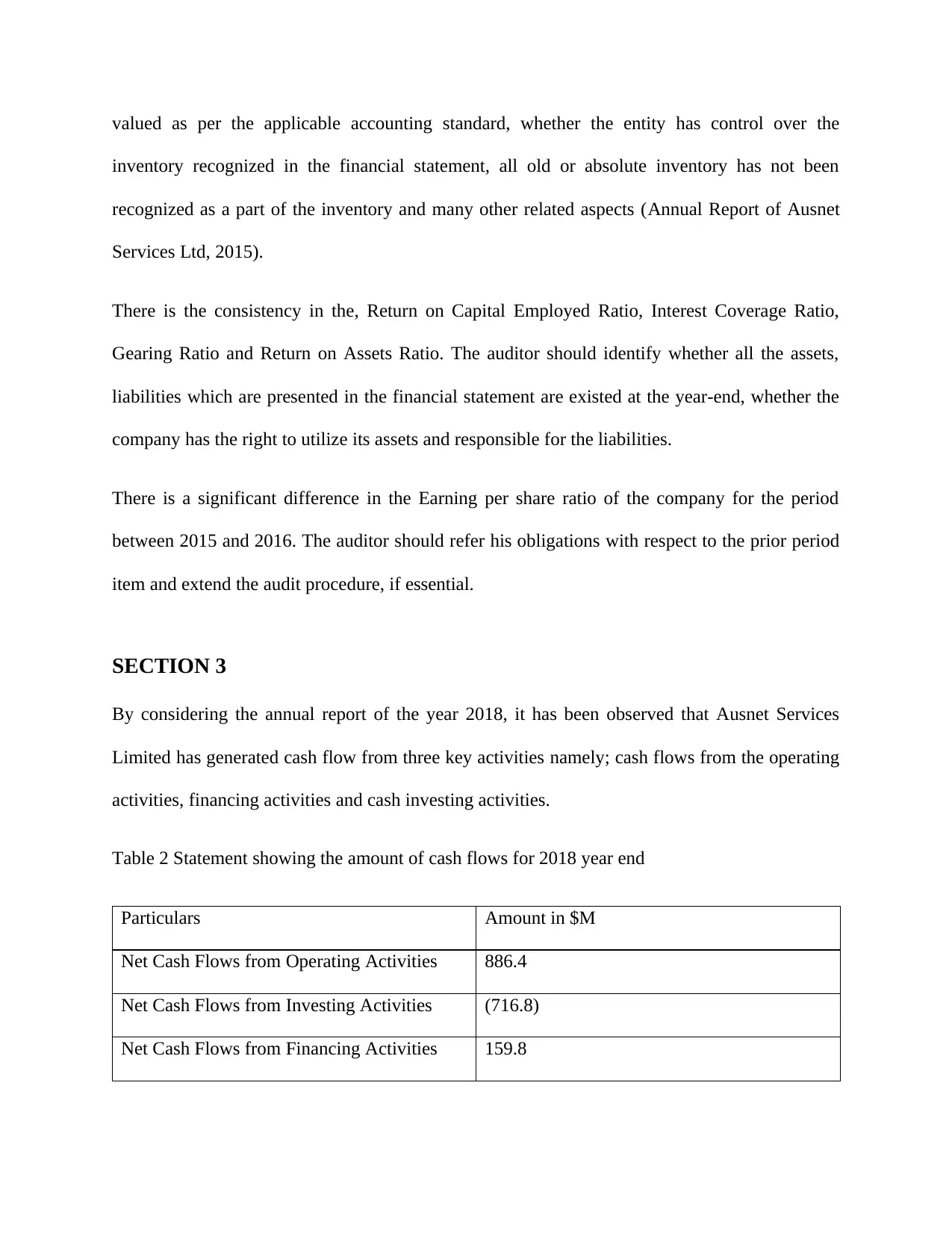

SECTION 3

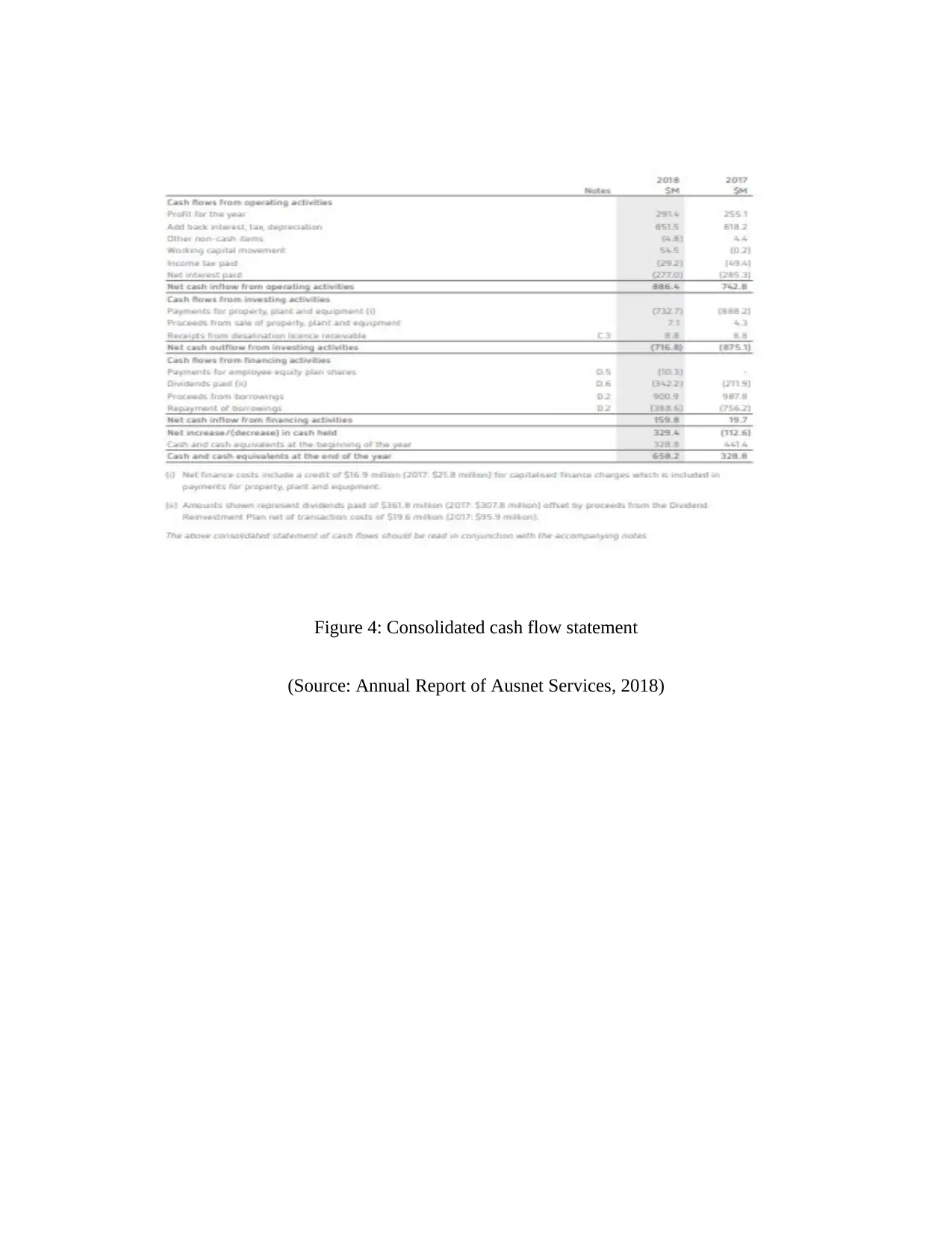

By considering the annual report of the year 2018, it has been observed that Ausnet Services

Limited has generated cash flow from three key activities namely; cash flows from the operating

activities, financing activities and cash investing activities.

Table 2 Statement showing the amount of cash flows for 2018 year end

Particulars Amount in $M

Net Cash Flows from Operating Activities 886.4

Net Cash Flows from Investing Activities (716.8)

Net Cash Flows from Financing Activities 159.8

inventory recognized in the financial statement, all old or absolute inventory has not been

recognized as a part of the inventory and many other related aspects (Annual Report of Ausnet

Services Ltd, 2015).

There is the consistency in the, Return on Capital Employed Ratio, Interest Coverage Ratio,

Gearing Ratio and Return on Assets Ratio. The auditor should identify whether all the assets,

liabilities which are presented in the financial statement are existed at the year-end, whether the

company has the right to utilize its assets and responsible for the liabilities.

There is a significant difference in the Earning per share ratio of the company for the period

between 2015 and 2016. The auditor should refer his obligations with respect to the prior period

item and extend the audit procedure, if essential.

SECTION 3

By considering the annual report of the year 2018, it has been observed that Ausnet Services

Limited has generated cash flow from three key activities namely; cash flows from the operating

activities, financing activities and cash investing activities.

Table 2 Statement showing the amount of cash flows for 2018 year end

Particulars Amount in $M

Net Cash Flows from Operating Activities 886.4

Net Cash Flows from Investing Activities (716.8)

Net Cash Flows from Financing Activities 159.8

It has been analyzed that, Ausnet Services Ltd, was generating the major cash flows from its

operating activities. Moreover, the investing category has the greatest outflow. Operating

activities are been associated with primary operations of the company.By analyzing the operating

activities, it has been seen that there is a significant change in the working capital movement. In

the year 2017, there is the outflow of $0.2 million;on the other hand, in the year 2018, there was

an inflow of $ 54.5 Million(Annual Report of Ausnet Services Ltd, 2018). The cash flows from

the primary activities consist of the amount received from debtors, accrued revenue received, and

reduction in the current inventory, increase in the accrued expenses and increase in the related

party receivables, increase in the non-current provision and deferred revenue and others.

Further, the primary payment includes payment to the creditors, payment to other payables,

interest paid, and others.

Further, the non-cash flow financing activity includes the foreign exchange rate changes. In other

words, the foreign exchange movement leads to non-cash flow financing activity. By considering

the corporate cash flow statement, it can be identified that inflows from the operations of the

company have been improvised as compare with the previous year. There is a significant change

in the working capital movement. Further, the company has disposed of its investment in

Property, Plant, and equipment. Further, the repayment of the borrowing by the company in

2018, as compared with the year 2017 is reduced, although there is no significant reduction in the

borrowing by the company (Annual Report of Ausnet Services Ltd, 2018). Based on above

analysis, it can be stated that even if the company carried its operations in a good manner, but the

auditor has to check the going concern risk. He/she has to evaluate whether the company is

capable of running its operation in the near future. It is recommended that auditor should use the

substantive audit procedure. This type of audit procedure implemented by the auditor to find the

operating activities. Moreover, the investing category has the greatest outflow. Operating

activities are been associated with primary operations of the company.By analyzing the operating

activities, it has been seen that there is a significant change in the working capital movement. In

the year 2017, there is the outflow of $0.2 million;on the other hand, in the year 2018, there was

an inflow of $ 54.5 Million(Annual Report of Ausnet Services Ltd, 2018). The cash flows from

the primary activities consist of the amount received from debtors, accrued revenue received, and

reduction in the current inventory, increase in the accrued expenses and increase in the related

party receivables, increase in the non-current provision and deferred revenue and others.

Further, the primary payment includes payment to the creditors, payment to other payables,

interest paid, and others.

Further, the non-cash flow financing activity includes the foreign exchange rate changes. In other

words, the foreign exchange movement leads to non-cash flow financing activity. By considering

the corporate cash flow statement, it can be identified that inflows from the operations of the

company have been improvised as compare with the previous year. There is a significant change

in the working capital movement. Further, the company has disposed of its investment in

Property, Plant, and equipment. Further, the repayment of the borrowing by the company in

2018, as compared with the year 2017 is reduced, although there is no significant reduction in the

borrowing by the company (Annual Report of Ausnet Services Ltd, 2018). Based on above

analysis, it can be stated that even if the company carried its operations in a good manner, but the

auditor has to check the going concern risk. He/she has to evaluate whether the company is

capable of running its operation in the near future. It is recommended that auditor should use the

substantive audit procedure. This type of audit procedure implemented by the auditor to find the

evidence related with the existence, completeness, valuation of assets and liabilities, proper

disclosures and many other aspects (Leonov, Leonova, Veselova, &Kotelyanets, 2018). The

auditor should inspect the agreement of borrowings and ascertain their repayment period,

whether the company repay the borrowing as and when due. At the year end, the auditor has to

evaluate any significant changes in the asset or liabilities. In addition, the auditor should make

the discussion from the management and identify the reason for the disposal of an asset and

whether the proceeds from the disposal of assets applicable by the company (Oberski, 2016).

In the financial report of Ausnet Service Limited 2018, auditor gives the faithful and fair opinion

of the Group’s financial position as of 31 March 2018, along with the financial performance for

the 2018 year end. Auditor states that financial statements are as per the compliance of

Australian Accounting Standard and the Corporations regulations 2001. In this report, there are

no additional sections and paragraph included which indicates about any audit issue.

disclosures and many other aspects (Leonov, Leonova, Veselova, &Kotelyanets, 2018). The

auditor should inspect the agreement of borrowings and ascertain their repayment period,

whether the company repay the borrowing as and when due. At the year end, the auditor has to

evaluate any significant changes in the asset or liabilities. In addition, the auditor should make

the discussion from the management and identify the reason for the disposal of an asset and

whether the proceeds from the disposal of assets applicable by the company (Oberski, 2016).

In the financial report of Ausnet Service Limited 2018, auditor gives the faithful and fair opinion

of the Group’s financial position as of 31 March 2018, along with the financial performance for

the 2018 year end. Auditor states that financial statements are as per the compliance of

Australian Accounting Standard and the Corporations regulations 2001. In this report, there are

no additional sections and paragraph included which indicates about any audit issue.

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

REFERENCES

Brasel, K., Doxey, M. M., Grenier, J. H., &Reffett, A. (2016). Risk disclosure preceding

negative outcomes: The effects of reporting critical audit matters on judgments of auditor

liability. The Accounting Review, 91(5), 1345-1362.

Cao, M., Chychyla, R., & Stewart, T. (2015). Big Data analytics in financial statement

audits. Accounting Horizons, 29(2), 423-429.

Chen, Y., Gul, F. A., Veeraraghavan, M., &Zolotoy, L. (2015). Executive equity risk-taking

incentives and audit pricing. The Accounting Review, 90(6), 2205-2234.

Christensen, B. E., Eilifsen, A., Glover, S. M., & Messier Jr, W. F. (2018). The Effect of

Materiality Disclosures on Investors’ Decision Making. Available at SSRN 3096564.

DeZoort, F. T., Holt, T., & Stanley, J. D. (2018). A Comparative Analysis of Investor and

Auditor Materiality Judgments. Auditing: A Journal of Practice and Theory.

Graham, L., Bedard, J. C., & Dutta, S. (2018). Managing group audit risk in a multicomponent

audit setting. International Journal of Auditing, 22(1), 40-54.

Gul, F. A., Khedmati, M., Lim, E. K., &Navissi, F. (2017). Managerial ability, financial distress,

and audit fees. Accounting Horizons, 32(1), 29-51.

Hale, A., Guldenmund, F., &Goossens, L. (2017). Auditing resilience in risk control and safety

management systems. In Resilience Engineering (pp. 289-314). CRC Press.

Hines, C. S., Masli, A., Mauldin, E. G., & Peters, G. F. (2015). Board risk committees and audit

pricing. Auditing: A Journal of Practice & Theory, 34(4), 59-84.

Brasel, K., Doxey, M. M., Grenier, J. H., &Reffett, A. (2016). Risk disclosure preceding

negative outcomes: The effects of reporting critical audit matters on judgments of auditor

liability. The Accounting Review, 91(5), 1345-1362.

Cao, M., Chychyla, R., & Stewart, T. (2015). Big Data analytics in financial statement

audits. Accounting Horizons, 29(2), 423-429.

Chen, Y., Gul, F. A., Veeraraghavan, M., &Zolotoy, L. (2015). Executive equity risk-taking

incentives and audit pricing. The Accounting Review, 90(6), 2205-2234.

Christensen, B. E., Eilifsen, A., Glover, S. M., & Messier Jr, W. F. (2018). The Effect of

Materiality Disclosures on Investors’ Decision Making. Available at SSRN 3096564.

DeZoort, F. T., Holt, T., & Stanley, J. D. (2018). A Comparative Analysis of Investor and

Auditor Materiality Judgments. Auditing: A Journal of Practice and Theory.

Graham, L., Bedard, J. C., & Dutta, S. (2018). Managing group audit risk in a multicomponent

audit setting. International Journal of Auditing, 22(1), 40-54.

Gul, F. A., Khedmati, M., Lim, E. K., &Navissi, F. (2017). Managerial ability, financial distress,

and audit fees. Accounting Horizons, 32(1), 29-51.

Hale, A., Guldenmund, F., &Goossens, L. (2017). Auditing resilience in risk control and safety

management systems. In Resilience Engineering (pp. 289-314). CRC Press.

Hines, C. S., Masli, A., Mauldin, E. G., & Peters, G. F. (2015). Board risk committees and audit

pricing. Auditing: A Journal of Practice & Theory, 34(4), 59-84.

Ishak, S., &Nor, M. N. M. (2018). AUDIT FUNCTION, RISK MANAGEMENT AND THE

SIGNIFICANCE OF AUDIT OPINION. International Journal of Accounting, 3(13), 88-93.

Knechel, W. R., &Salterio, S. E. (2016). Auditing: Assurance and risk. Routledge.

Lakis, V., &Masiulevičius, A. (2017). ACCEPTABLE AUDIT MATERIALITY FOR USERS

OF FINANCIAL STATEMENTS. Journal of Management, 2(31).

Leonov, P. Y., Leonova, E. K., Veselova, E. A., &Kotelyanets, O. S. (2018). General Scheme of

Risk–Oriented Audit Stages. KnE Engineering, 3(6), 402-415.

Lu, L. Y., Wu, H., & Yu, Y. (2017). Investment-related pressure and audit risk. Auditing: A

Journal of Practice & Theory, 36(3), 137-157.

Oberski, D. L. (2016). Beyond the number of classes: separating substantive from non-

substantive dependence in latent class analysis. Advances in Data Analysis and

Classification, 10(2), 171-182.

Trotman, K. T. (2015). Audit Evidence. Wiley Encyclopedia of Management, 1-5.

Online

Annual Report of Ausnet Services, 2018. Retrieved

From<https://www.ausnetservices.com.au/-/.../AusNet/.../Reports/2018-Annual-

Report.ashx>

Annual Report of Ausnet Services, 2015. Retrieved From

<https://www.ausnetservices.com.au/-/media/Files/AusNet/.../2015/AnnualReport.ashx>

SIGNIFICANCE OF AUDIT OPINION. International Journal of Accounting, 3(13), 88-93.

Knechel, W. R., &Salterio, S. E. (2016). Auditing: Assurance and risk. Routledge.

Lakis, V., &Masiulevičius, A. (2017). ACCEPTABLE AUDIT MATERIALITY FOR USERS

OF FINANCIAL STATEMENTS. Journal of Management, 2(31).

Leonov, P. Y., Leonova, E. K., Veselova, E. A., &Kotelyanets, O. S. (2018). General Scheme of

Risk–Oriented Audit Stages. KnE Engineering, 3(6), 402-415.

Lu, L. Y., Wu, H., & Yu, Y. (2017). Investment-related pressure and audit risk. Auditing: A

Journal of Practice & Theory, 36(3), 137-157.

Oberski, D. L. (2016). Beyond the number of classes: separating substantive from non-

substantive dependence in latent class analysis. Advances in Data Analysis and

Classification, 10(2), 171-182.

Trotman, K. T. (2015). Audit Evidence. Wiley Encyclopedia of Management, 1-5.

Online

Annual Report of Ausnet Services, 2018. Retrieved

From<https://www.ausnetservices.com.au/-/.../AusNet/.../Reports/2018-Annual-

Report.ashx>

Annual Report of Ausnet Services, 2015. Retrieved From

<https://www.ausnetservices.com.au/-/media/Files/AusNet/.../2015/AnnualReport.ashx>

APPENDICES

Figure 1: Key audit matters

(Source: Annual Report of Ausnet Services, 2018)

Figure 1: Key audit matters

(Source: Annual Report of Ausnet Services, 2018)

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Figure 2: Consolidated income statement

(Source: Annual Report of Ausnet Services, 2018)

(Source: Annual Report of Ausnet Services, 2018)

Figure 3: Consolidated financial position statement

(Source: Annual Report of Ausnet Services, 2018)

(Source: Annual Report of Ausnet Services, 2018)

Figure 4: Consolidated cash flow statement

(Source: Annual Report of Ausnet Services, 2018)

(Source: Annual Report of Ausnet Services, 2018)

1 out of 16

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.