CQUniversity Auditing and Ethics Report: Northern Star Ltd, 2019

VerifiedAdded on 2023/03/21

|13

|2483

|29

Report

AI Summary

This report analyzes an auditing and ethics report based on the annual report of Northern Star Ltd. It begins with an assessment of materiality and the scope of the audit, examining how materiality is determined and its impact on financial statements. The report then reviews draft notes and disclosures, focusing on significant items like dividends and business combinations. Section 2 performs an analytical review of the financial statements, calculating and interpreting profitability, liquidity, and efficiency ratios. Section 3 analyzes the cash flow statement, highlighting cash flows from operating, investing, and financing activities. The report concludes with a review of the auditor's report and the application of the going concern principle. This report is a comprehensive analysis of the audit process and financial statement analysis.

Running head: AUDITING AND ETHICS

AUDITING AND ETHICS

Name of the Student:

Name of the University:

Author’s Note:

AUDITING AND ETHICS

Name of the Student:

Name of the University:

Author’s Note:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1

AUDITING AND ETHICS

Table of Contents

Section 1....................................................................................................................................2

Materiality and Scope of Audit.............................................................................................2

Review of Draft Notes and Disclosures................................................................................4

Section 2....................................................................................................................................6

Analytical Review of the Financial statements.....................................................................6

Section 3....................................................................................................................................9

Analysis of the Cash flow statement.....................................................................................9

Review of the Auditor Report.............................................................................................11

Reference.................................................................................................................................11

AUDITING AND ETHICS

Table of Contents

Section 1....................................................................................................................................2

Materiality and Scope of Audit.............................................................................................2

Review of Draft Notes and Disclosures................................................................................4

Section 2....................................................................................................................................6

Analytical Review of the Financial statements.....................................................................6

Section 3....................................................................................................................................9

Analysis of the Cash flow statement.....................................................................................9

Review of the Auditor Report.............................................................................................11

Reference.................................................................................................................................11

2

AUDITING AND ETHICS

Section 1

Materiality and Scope of Audit

The assessment would be focusing on the materiality aspect of the business and the

different processes which is applied by the management of the company for the purpose of

reviewing the materiality of the business. The concept of materiality states that an item is

considered to be material if the same has important impact on the financial statements of the

business or is of complex nature or is of significant amount (Appelbaum, Kogan & Vasarhelyi,

2017). The auditor of a business decides whether an item of the financial statement is misstated

or not on the basis of the materiality of the items. Therefore, it can be said that the judgement of

the auditor relies on materiality aspect of an item. In this case the company which is considered

is Northern Star ltd which is listed in Australian Stock exchange (Nsrltd.com., 2019). The

company Northern Star ltd is listed in top 25 companies which are gold miners in the region.

The concept of materiality is a fundamental concept with in the scope of audit as the

auditor relies on the planning materiality of a business to determine whether a financial statement

is properly presented in the financial accounts of the business. In order to get an estimate of

materiality, the auditor needs to apply his judgement and consider a percentage on the basis of

which planning materiality of the business is computed. The auditor of the business needs to take

a base on which the percentage would be applied to compute planning materiality of the

business. The planning materiality of the business is computed considering either qualitative

factors or it can also be computed considering quantitative factors. The qualitative factors

include items which are significant for the financial statements while quantitative factors include

items which are of numerically of higher value (Müller-Burmeister & Velte, 2016). The

percentage which is to be charged for determining materiality are up to the judgements of the

AUDITING AND ETHICS

Section 1

Materiality and Scope of Audit

The assessment would be focusing on the materiality aspect of the business and the

different processes which is applied by the management of the company for the purpose of

reviewing the materiality of the business. The concept of materiality states that an item is

considered to be material if the same has important impact on the financial statements of the

business or is of complex nature or is of significant amount (Appelbaum, Kogan & Vasarhelyi,

2017). The auditor of a business decides whether an item of the financial statement is misstated

or not on the basis of the materiality of the items. Therefore, it can be said that the judgement of

the auditor relies on materiality aspect of an item. In this case the company which is considered

is Northern Star ltd which is listed in Australian Stock exchange (Nsrltd.com., 2019). The

company Northern Star ltd is listed in top 25 companies which are gold miners in the region.

The concept of materiality is a fundamental concept with in the scope of audit as the

auditor relies on the planning materiality of a business to determine whether a financial statement

is properly presented in the financial accounts of the business. In order to get an estimate of

materiality, the auditor needs to apply his judgement and consider a percentage on the basis of

which planning materiality of the business is computed. The auditor of the business needs to take

a base on which the percentage would be applied to compute planning materiality of the

business. The planning materiality of the business is computed considering either qualitative

factors or it can also be computed considering quantitative factors. The qualitative factors

include items which are significant for the financial statements while quantitative factors include

items which are of numerically of higher value (Müller-Burmeister & Velte, 2016). The

percentage which is to be charged for determining materiality are up to the judgements of the

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3

AUDITING AND ETHICS

auditor depending on the size of the business and nature of its operations. The planning

materiality is then used for ascertaining the performance materiality of each item.

The annual reports for 2018 is considered for Northern Star Ltd for the purpose of

computing the materiality of the business. As per the annual report of the business, there has

been significant increase in the total asset of the business which is an indication that the business

is moving forward with an objective of maximising the wealth of the business. The figure of total

assets is shown to be $ 12,16,870,000 which is highest and it is even more than the sales which is

achieved by the business. The materiality computation is generally done considering the highest

value which is presented in the annual reports of the business (Pike, Curtis & Chui, 2013). An

estimate for computing planning materiality of the business is considered to be 5% of the base

amount which is the total asset figure of the business. The computation of planning materiality is

shown in the equation below:

Planning Materiality=Total Asset∗5 %

¿ $ 1,216,870,000∗5 %

¿ $ 60,843,500

On the basis of the estimate which is computed above, performance materiality of the business

would be taken into consideration.

Review of Draft Notes and Disclosures

The draft notes and disclosures are appropriately shown in the annual reports of Northern

Star Ltd for the year 2018 which has significance of its own as they relate to complex treatments

AUDITING AND ETHICS

auditor depending on the size of the business and nature of its operations. The planning

materiality is then used for ascertaining the performance materiality of each item.

The annual reports for 2018 is considered for Northern Star Ltd for the purpose of

computing the materiality of the business. As per the annual report of the business, there has

been significant increase in the total asset of the business which is an indication that the business

is moving forward with an objective of maximising the wealth of the business. The figure of total

assets is shown to be $ 12,16,870,000 which is highest and it is even more than the sales which is

achieved by the business. The materiality computation is generally done considering the highest

value which is presented in the annual reports of the business (Pike, Curtis & Chui, 2013). An

estimate for computing planning materiality of the business is considered to be 5% of the base

amount which is the total asset figure of the business. The computation of planning materiality is

shown in the equation below:

Planning Materiality=Total Asset∗5 %

¿ $ 1,216,870,000∗5 %

¿ $ 60,843,500

On the basis of the estimate which is computed above, performance materiality of the business

would be taken into consideration.

Review of Draft Notes and Disclosures

The draft notes and disclosures are appropriately shown in the annual reports of Northern

Star Ltd for the year 2018 which has significance of its own as they relate to complex treatments

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4

AUDITING AND ETHICS

of the business. The significant items which are shown in the notes to account section of the

annual reports are listed below:

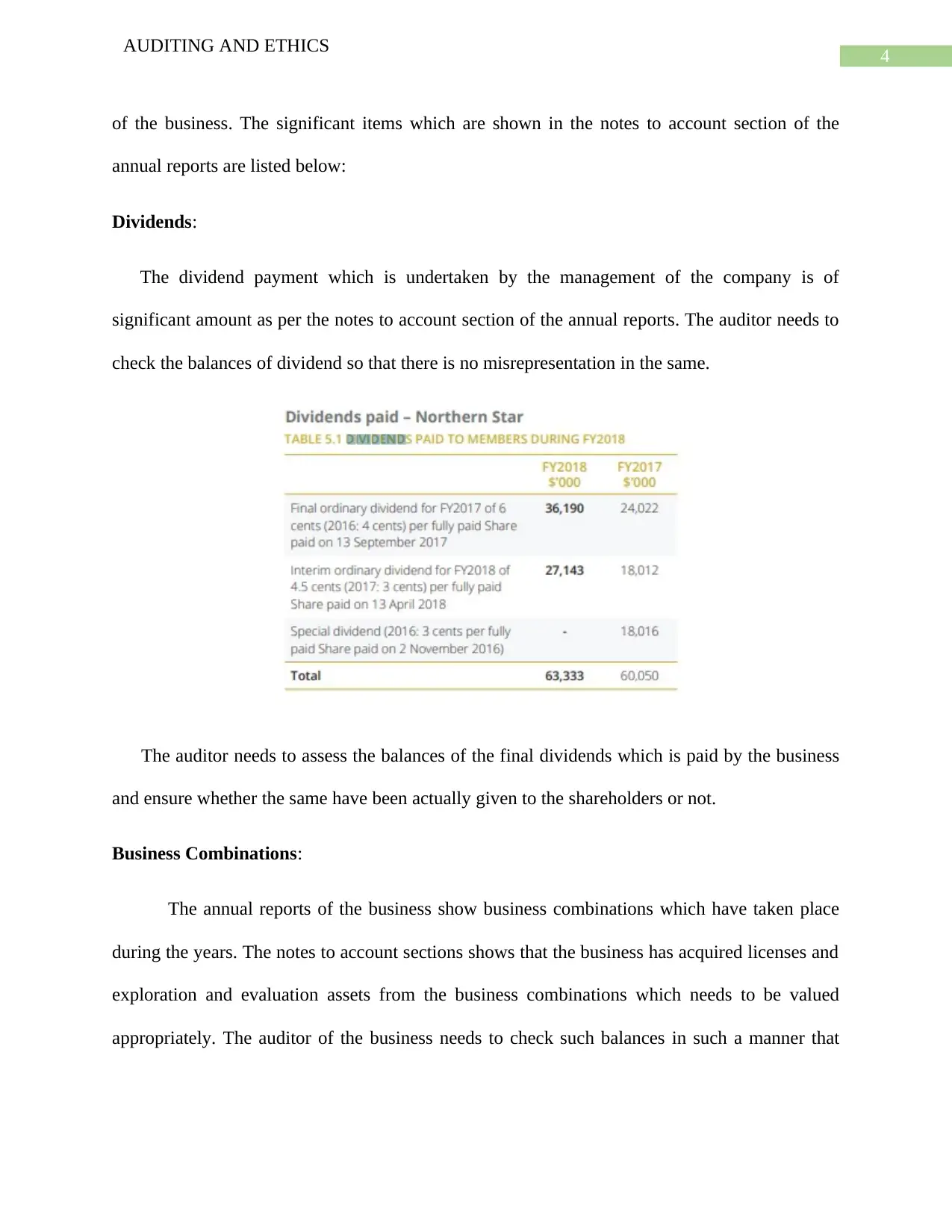

Dividends:

The dividend payment which is undertaken by the management of the company is of

significant amount as per the notes to account section of the annual reports. The auditor needs to

check the balances of dividend so that there is no misrepresentation in the same.

The auditor needs to assess the balances of the final dividends which is paid by the business

and ensure whether the same have been actually given to the shareholders or not.

Business Combinations:

The annual reports of the business show business combinations which have taken place

during the years. The notes to account sections shows that the business has acquired licenses and

exploration and evaluation assets from the business combinations which needs to be valued

appropriately. The auditor of the business needs to check such balances in such a manner that

AUDITING AND ETHICS

of the business. The significant items which are shown in the notes to account section of the

annual reports are listed below:

Dividends:

The dividend payment which is undertaken by the management of the company is of

significant amount as per the notes to account section of the annual reports. The auditor needs to

check the balances of dividend so that there is no misrepresentation in the same.

The auditor needs to assess the balances of the final dividends which is paid by the business

and ensure whether the same have been actually given to the shareholders or not.

Business Combinations:

The annual reports of the business show business combinations which have taken place

during the years. The notes to account sections shows that the business has acquired licenses and

exploration and evaluation assets from the business combinations which needs to be valued

appropriately. The auditor of the business needs to check such balances in such a manner that

5

AUDITING AND ETHICS

there are no discrepancies in the amounts which are represented in the notes to account section of

the annual reports.

Total Assets:

The total assets of the business are disclosed in the balance sheet of the company and the

auditor of the business needs to check the viability of the items which are presented in the

balance sheet of the business. The auditor needs to ensure that the assets of the business are

properly valued considering the values which is shown in the balance sheet of the company.

Section 2

Analytical Review of the Financial statements

Analytical review is one of the techniques which is available to the auditor in which

significant ratios are computed from the financial statements which informs about various

aspects of the business. The ratios which are considered relate to different areas of performance

of the business. Some of the key ratios of the business are discussed below in details:

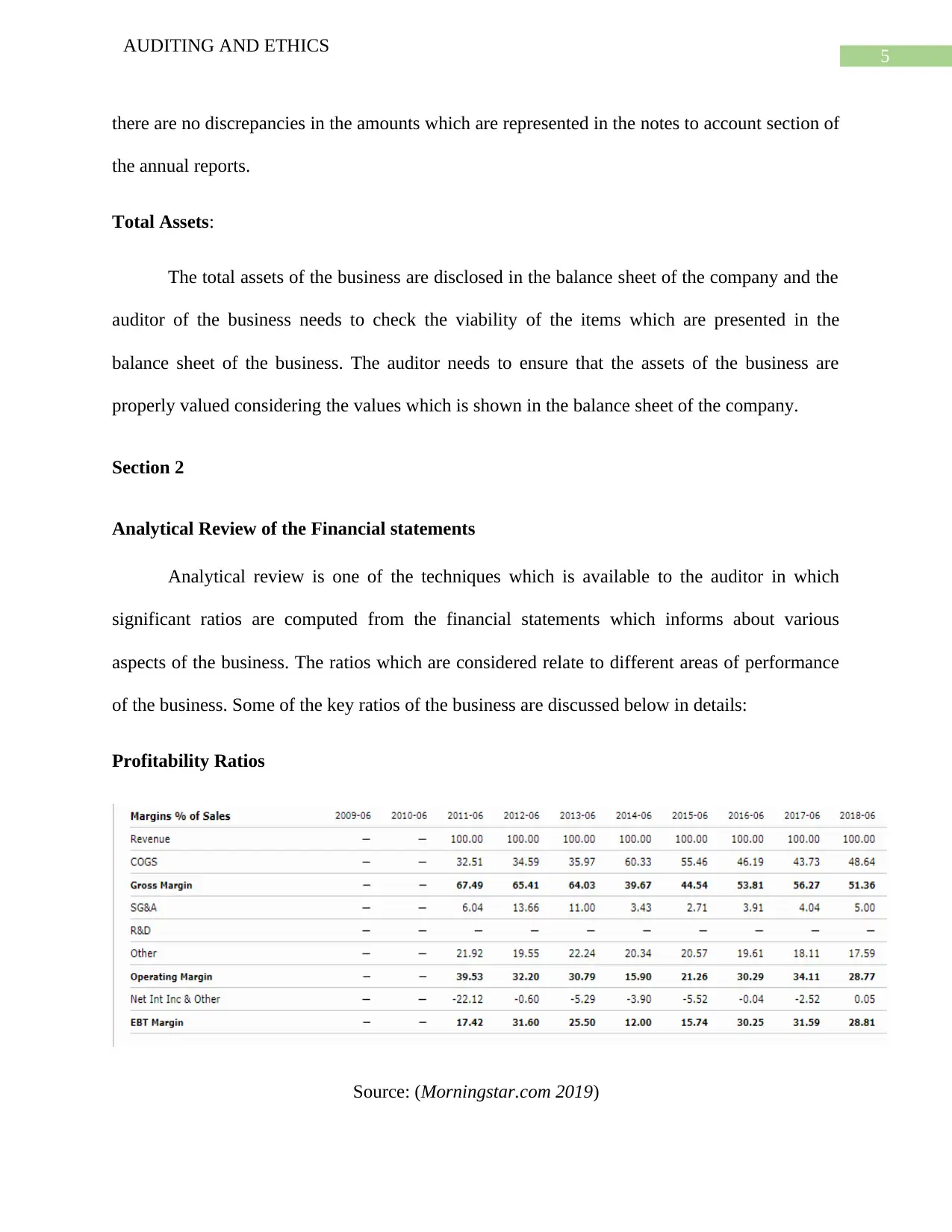

Profitability Ratios

Source: (Morningstar.com 2019)

AUDITING AND ETHICS

there are no discrepancies in the amounts which are represented in the notes to account section of

the annual reports.

Total Assets:

The total assets of the business are disclosed in the balance sheet of the company and the

auditor of the business needs to check the viability of the items which are presented in the

balance sheet of the business. The auditor needs to ensure that the assets of the business are

properly valued considering the values which is shown in the balance sheet of the company.

Section 2

Analytical Review of the Financial statements

Analytical review is one of the techniques which is available to the auditor in which

significant ratios are computed from the financial statements which informs about various

aspects of the business. The ratios which are considered relate to different areas of performance

of the business. Some of the key ratios of the business are discussed below in details:

Profitability Ratios

Source: (Morningstar.com 2019)

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6

AUDITING AND ETHICS

The above figure represents the profitability ratios of the business which includes

important ratios which are gross profit margin, net profit margin and operating margin. There has

been a slight increase in the sales of the business which in turn shows that the profitability of the

business has increased significantly during the period. The increase in the profitability of the

business suggest that the management of the company is trying to improve the profits which is

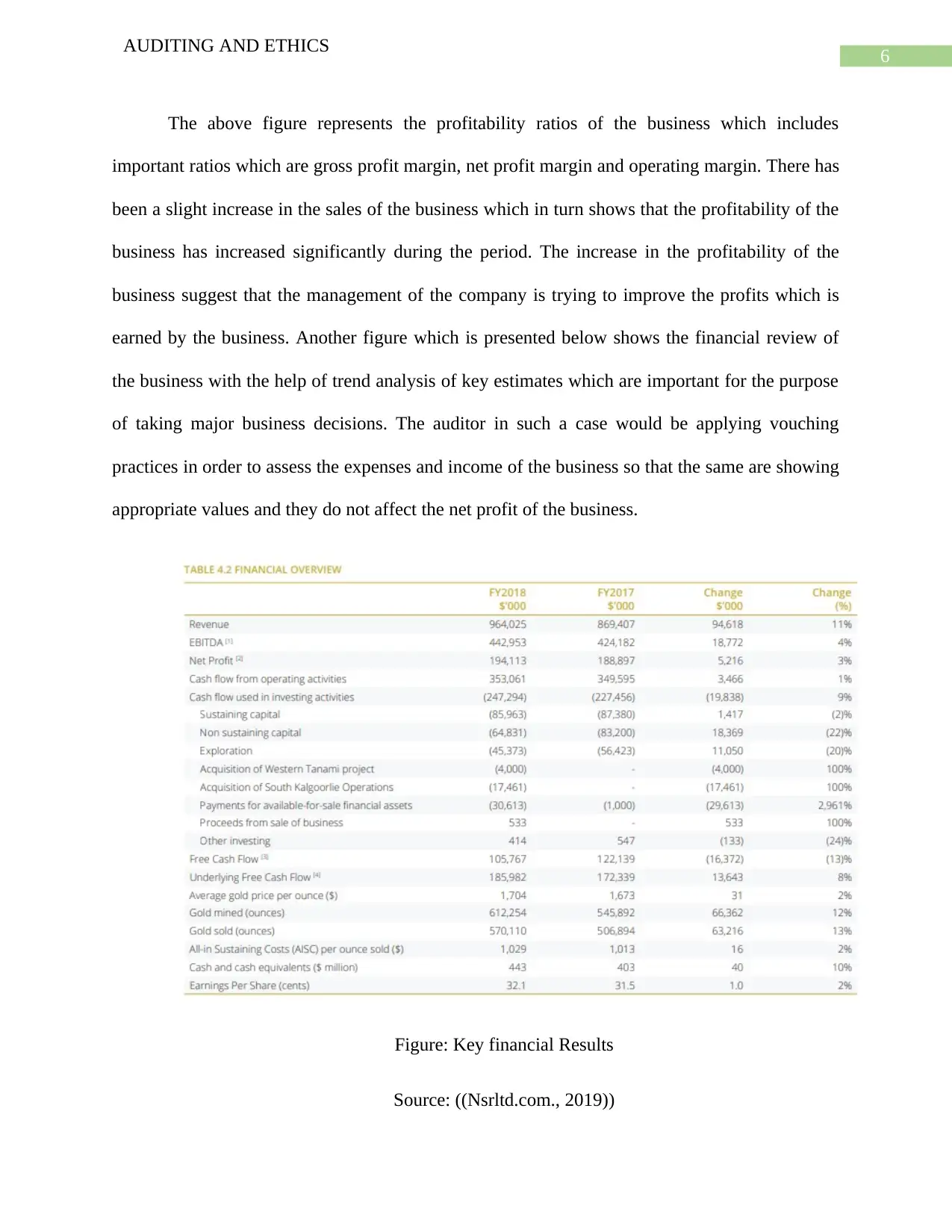

earned by the business. Another figure which is presented below shows the financial review of

the business with the help of trend analysis of key estimates which are important for the purpose

of taking major business decisions. The auditor in such a case would be applying vouching

practices in order to assess the expenses and income of the business so that the same are showing

appropriate values and they do not affect the net profit of the business.

Figure: Key financial Results

Source: ((Nsrltd.com., 2019))

AUDITING AND ETHICS

The above figure represents the profitability ratios of the business which includes

important ratios which are gross profit margin, net profit margin and operating margin. There has

been a slight increase in the sales of the business which in turn shows that the profitability of the

business has increased significantly during the period. The increase in the profitability of the

business suggest that the management of the company is trying to improve the profits which is

earned by the business. Another figure which is presented below shows the financial review of

the business with the help of trend analysis of key estimates which are important for the purpose

of taking major business decisions. The auditor in such a case would be applying vouching

practices in order to assess the expenses and income of the business so that the same are showing

appropriate values and they do not affect the net profit of the business.

Figure: Key financial Results

Source: ((Nsrltd.com., 2019))

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7

AUDITING AND ETHICS

The financial review also shows that the net profit of the business has increased slightly

which shows that the management of the company is taking steps for enhancing the profits which

is generated by the business.

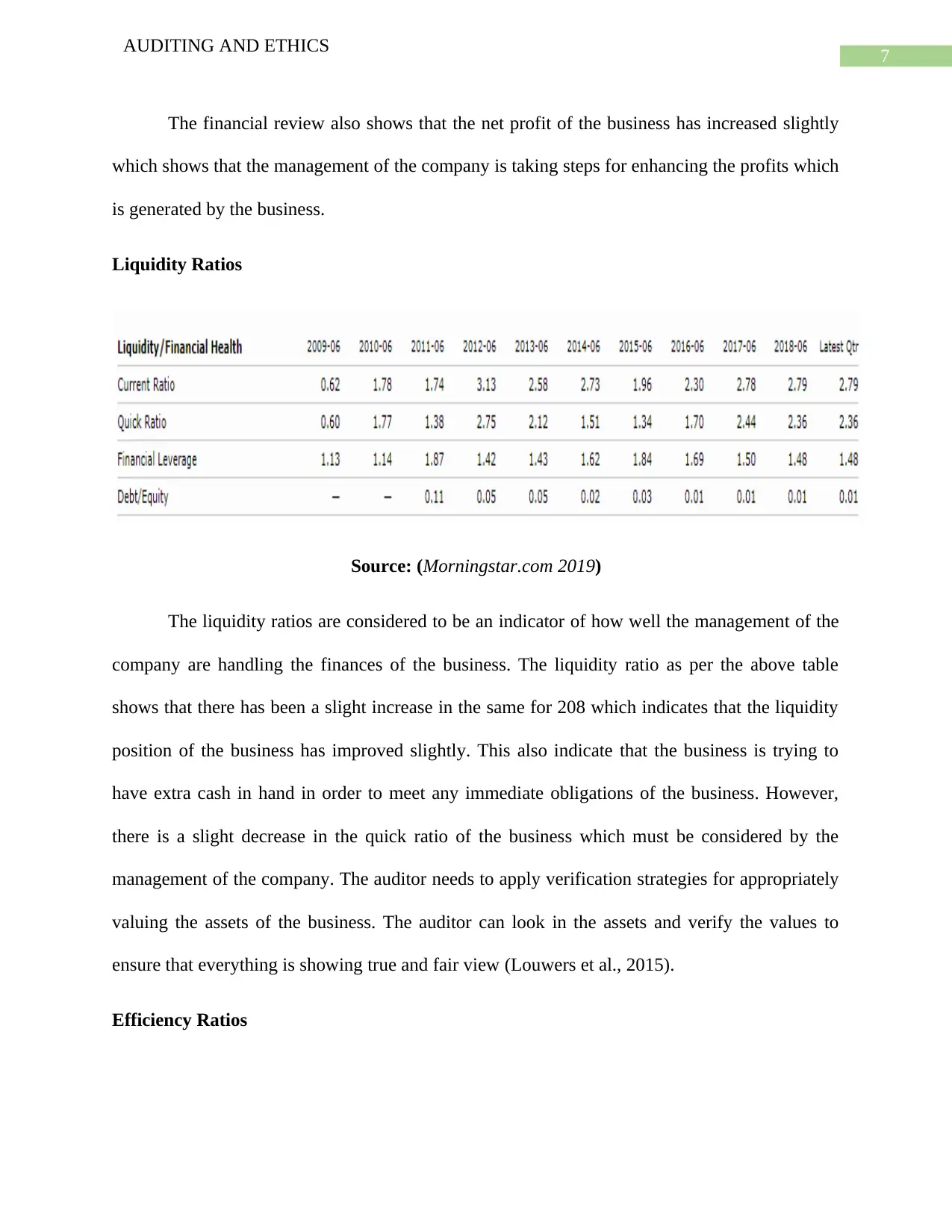

Liquidity Ratios

Source: (Morningstar.com 2019)

The liquidity ratios are considered to be an indicator of how well the management of the

company are handling the finances of the business. The liquidity ratio as per the above table

shows that there has been a slight increase in the same for 208 which indicates that the liquidity

position of the business has improved slightly. This also indicate that the business is trying to

have extra cash in hand in order to meet any immediate obligations of the business. However,

there is a slight decrease in the quick ratio of the business which must be considered by the

management of the company. The auditor needs to apply verification strategies for appropriately

valuing the assets of the business. The auditor can look in the assets and verify the values to

ensure that everything is showing true and fair view (Louwers et al., 2015).

Efficiency Ratios

AUDITING AND ETHICS

The financial review also shows that the net profit of the business has increased slightly

which shows that the management of the company is taking steps for enhancing the profits which

is generated by the business.

Liquidity Ratios

Source: (Morningstar.com 2019)

The liquidity ratios are considered to be an indicator of how well the management of the

company are handling the finances of the business. The liquidity ratio as per the above table

shows that there has been a slight increase in the same for 208 which indicates that the liquidity

position of the business has improved slightly. This also indicate that the business is trying to

have extra cash in hand in order to meet any immediate obligations of the business. However,

there is a slight decrease in the quick ratio of the business which must be considered by the

management of the company. The auditor needs to apply verification strategies for appropriately

valuing the assets of the business. The auditor can look in the assets and verify the values to

ensure that everything is showing true and fair view (Louwers et al., 2015).

Efficiency Ratios

8

AUDITING AND ETHICS

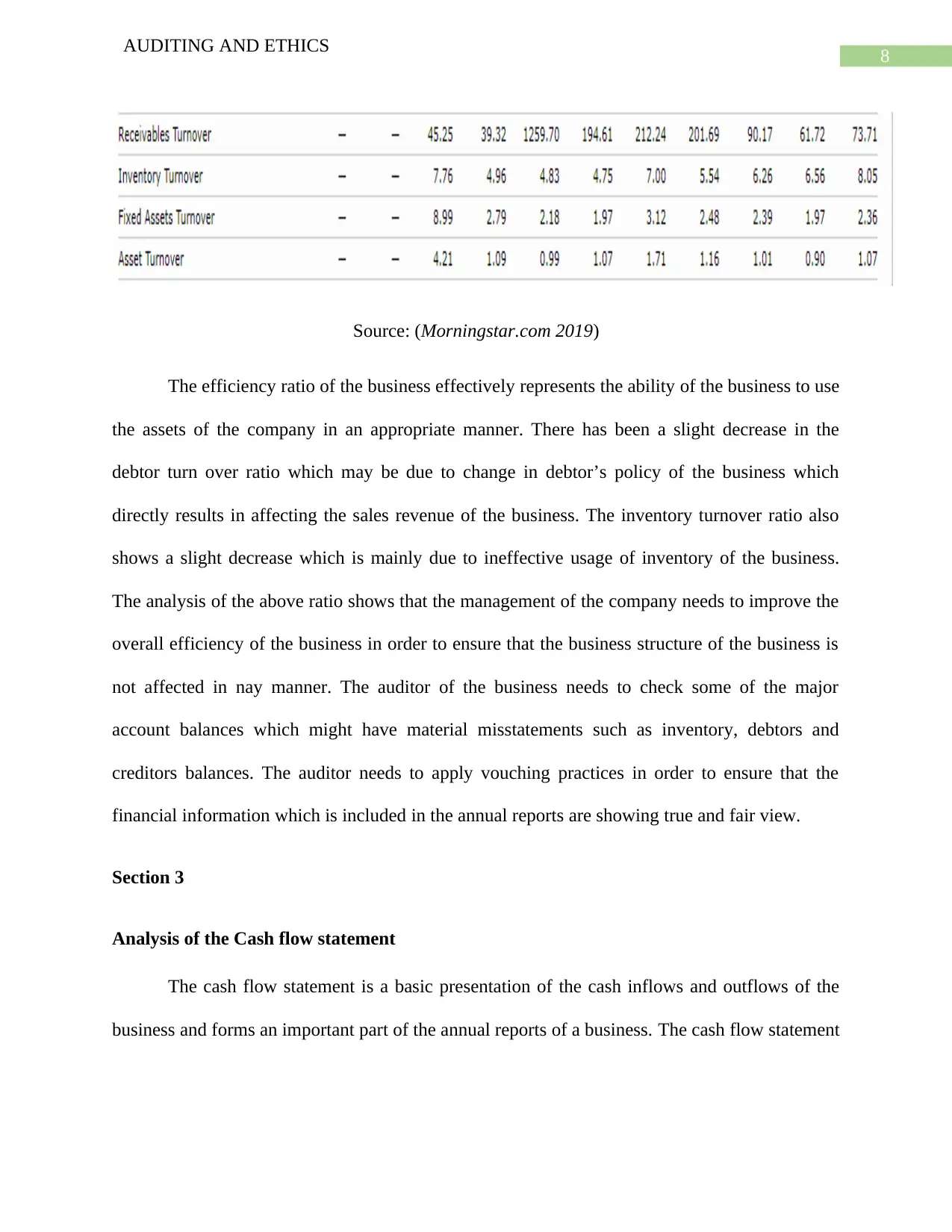

Source: (Morningstar.com 2019)

The efficiency ratio of the business effectively represents the ability of the business to use

the assets of the company in an appropriate manner. There has been a slight decrease in the

debtor turn over ratio which may be due to change in debtor’s policy of the business which

directly results in affecting the sales revenue of the business. The inventory turnover ratio also

shows a slight decrease which is mainly due to ineffective usage of inventory of the business.

The analysis of the above ratio shows that the management of the company needs to improve the

overall efficiency of the business in order to ensure that the business structure of the business is

not affected in nay manner. The auditor of the business needs to check some of the major

account balances which might have material misstatements such as inventory, debtors and

creditors balances. The auditor needs to apply vouching practices in order to ensure that the

financial information which is included in the annual reports are showing true and fair view.

Section 3

Analysis of the Cash flow statement

The cash flow statement is a basic presentation of the cash inflows and outflows of the

business and forms an important part of the annual reports of a business. The cash flow statement

AUDITING AND ETHICS

Source: (Morningstar.com 2019)

The efficiency ratio of the business effectively represents the ability of the business to use

the assets of the company in an appropriate manner. There has been a slight decrease in the

debtor turn over ratio which may be due to change in debtor’s policy of the business which

directly results in affecting the sales revenue of the business. The inventory turnover ratio also

shows a slight decrease which is mainly due to ineffective usage of inventory of the business.

The analysis of the above ratio shows that the management of the company needs to improve the

overall efficiency of the business in order to ensure that the business structure of the business is

not affected in nay manner. The auditor of the business needs to check some of the major

account balances which might have material misstatements such as inventory, debtors and

creditors balances. The auditor needs to apply vouching practices in order to ensure that the

financial information which is included in the annual reports are showing true and fair view.

Section 3

Analysis of the Cash flow statement

The cash flow statement is a basic presentation of the cash inflows and outflows of the

business and forms an important part of the annual reports of a business. The cash flow statement

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9

AUDITING AND ETHICS

for Northern Star ltd for the year 2018 shows cash from operating activities, investing activities

and financing activities.

The cash flow from operating activities of the business includes core business activities

of the business and it is from such activities that the management of the company generates

maximum cash inflows and also incurs maximum cash outflows. The cash flow statement of the

business for the year 2018 shows that the management has genera (Bhandari & Iyer, 2013).ted

maximum cash flow from receipts from customers which is shown to be of $ 966,770,000 which

is of significant amount. The maximum cash outflow is also shown in the operational activities

of the business which is shown to be from cash paid to suppliers which is shown to be $

520,486,000. The cash generated from operations of the business is shown to be much higher in

comparison to previous year which shows that the business is growing.

The cash from financing activities of the business for the year 2018 is shown to be

significant low and it is even negative which is mainly due to the numerous purchases which is

made by the management of the company during the period. The purchases of the assets shows

that the management of the company is trying to expand the scale of operations and thereby

collecting more assets. The management of the company has also sold off some of the previous

assets of the business.

The cash flow from financing activities of the business is shown to be negative as the

business has undertaken dividend payments and lease payments during the period which is of

significant amount.

The principle of going concern is a fundamental principle of accounting and it is also

referred by the auditor of the business while conducting the audit of the business. The

AUDITING AND ETHICS

for Northern Star ltd for the year 2018 shows cash from operating activities, investing activities

and financing activities.

The cash flow from operating activities of the business includes core business activities

of the business and it is from such activities that the management of the company generates

maximum cash inflows and also incurs maximum cash outflows. The cash flow statement of the

business for the year 2018 shows that the management has genera (Bhandari & Iyer, 2013).ted

maximum cash flow from receipts from customers which is shown to be of $ 966,770,000 which

is of significant amount. The maximum cash outflow is also shown in the operational activities

of the business which is shown to be from cash paid to suppliers which is shown to be $

520,486,000. The cash generated from operations of the business is shown to be much higher in

comparison to previous year which shows that the business is growing.

The cash from financing activities of the business for the year 2018 is shown to be

significant low and it is even negative which is mainly due to the numerous purchases which is

made by the management of the company during the period. The purchases of the assets shows

that the management of the company is trying to expand the scale of operations and thereby

collecting more assets. The management of the company has also sold off some of the previous

assets of the business.

The cash flow from financing activities of the business is shown to be negative as the

business has undertaken dividend payments and lease payments during the period which is of

significant amount.

The principle of going concern is a fundamental principle of accounting and it is also

referred by the auditor of the business while conducting the audit of the business. The

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10

AUDITING AND ETHICS

profitability ratio for the company is shown to be favourable and there is rise in the same as well

which suggest growth. The management of the company is purchasing assets with a view of

expanding the operations of the business which signifies that the business is trying to expand in

operations. The liquidity ratio of the business is shown to be appropriate which is also a

favourable sign for the business. The auditor of the company must not consider going concern

principle as there is no sign present which can suggest that the going concern of the business

might be affected.

Review of the Auditor Report

The report of the auditor provides the opinion regarding the accuracy of the financial

statement of the business. As per the opinion of the auditor the financial statements are prepared

following relevant accounting standards and followed provisions of Corporation Act 2001 and

therefore are also showing true and fair view. The key audit matters are there which the auditor

of the business must consider before providing an opinion on the financial statement of the

business.

AUDITING AND ETHICS

profitability ratio for the company is shown to be favourable and there is rise in the same as well

which suggest growth. The management of the company is purchasing assets with a view of

expanding the operations of the business which signifies that the business is trying to expand in

operations. The liquidity ratio of the business is shown to be appropriate which is also a

favourable sign for the business. The auditor of the company must not consider going concern

principle as there is no sign present which can suggest that the going concern of the business

might be affected.

Review of the Auditor Report

The report of the auditor provides the opinion regarding the accuracy of the financial

statement of the business. As per the opinion of the auditor the financial statements are prepared

following relevant accounting standards and followed provisions of Corporation Act 2001 and

therefore are also showing true and fair view. The key audit matters are there which the auditor

of the business must consider before providing an opinion on the financial statement of the

business.

11

AUDITING AND ETHICS

Reference

Appelbaum, D., Kogan, A., & Vasarhelyi, M. A. (2017). Big Data and analytics in the modern

audit engagement: Research needs. Auditing: A Journal of Practice & Theory, 36(4), 1-

27.

Bhandari, S. B., & Iyer, R. (2013). Predicting business failure using cash flow statement based

measures. Managerial Finance, 39(7), 667-676.

Investments, B., Portfolio, Y., FundsETFs, I., Funds, M., Tools, T., & Screener, B. et al.

(2019). NST Northern Star Resources Ltd Stock Analysis, Price & History |

Morningstar. Morningstar.com. Retrieved 13 May 2019, from

https://www.morningstar.com/stocks/XASX/NST/quote.html

Louwers, T. J., Ramsay, R. J., Sinason, D. H., Strawser, J. R., & Thibodeau, J. C.

(2015). Auditing & assurance services. McGraw-Hill Education.

Müller-Burmeister, C., & Velte, P. (2016). Increased materiality judgments in financial

accounting and external audit: a critical comparison between German and international

standard setting. International Journal of Critical Accounting, 8(3-4), 227-245.

Nsrltd.com. (2019). Northern Star – Annual Reports . [online] Available at:

https://www.nsrltd.com/investor-media/reports/annual-reports/?

doing_wp_cron=1557754899.2553660869598388671875 [Accessed 13 May 2019].

AUDITING AND ETHICS

Reference

Appelbaum, D., Kogan, A., & Vasarhelyi, M. A. (2017). Big Data and analytics in the modern

audit engagement: Research needs. Auditing: A Journal of Practice & Theory, 36(4), 1-

27.

Bhandari, S. B., & Iyer, R. (2013). Predicting business failure using cash flow statement based

measures. Managerial Finance, 39(7), 667-676.

Investments, B., Portfolio, Y., FundsETFs, I., Funds, M., Tools, T., & Screener, B. et al.

(2019). NST Northern Star Resources Ltd Stock Analysis, Price & History |

Morningstar. Morningstar.com. Retrieved 13 May 2019, from

https://www.morningstar.com/stocks/XASX/NST/quote.html

Louwers, T. J., Ramsay, R. J., Sinason, D. H., Strawser, J. R., & Thibodeau, J. C.

(2015). Auditing & assurance services. McGraw-Hill Education.

Müller-Burmeister, C., & Velte, P. (2016). Increased materiality judgments in financial

accounting and external audit: a critical comparison between German and international

standard setting. International Journal of Critical Accounting, 8(3-4), 227-245.

Nsrltd.com. (2019). Northern Star – Annual Reports . [online] Available at:

https://www.nsrltd.com/investor-media/reports/annual-reports/?

doing_wp_cron=1557754899.2553660869598388671875 [Accessed 13 May 2019].

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.