Auditing and Ethics: Financial Analysis of Genworth Mortgage Insurance

VerifiedAdded on 2021/04/21

|16

|3106

|44

Report

AI Summary

This report provides a comprehensive analysis of the auditing and ethics considerations for Genworth Mortgage Insurance Australia Limited. It begins by defining audit materiality and its application within the context of Genworth, including quantitative and qualitative aspects. The report examines the level of materiality used in the audit of group accounts, referencing relevant standards and considering key financial figures like Gross Written Premium and total assets. It then delves into the financial position of the company, analyzing key ratios such as financial leverage, return on equity, net profit margin, and the current ratio from 2014 to 2017. The report identifies key risk areas and recommends relevant auditing procedures, including assertions of existence, completeness, rights and obligations, accuracy and valuation, and presentation and disclosure. Furthermore, the analysis extends to the statement of cash flows, detailing cash inflows and outflows from investing and financing activities, as well as the company's exposure to various risks, including liquidity, market, and credit risks. The report concludes with a summary of the key findings and implications for the audit process.

Running head: Auditing and Ethics

Auditing and Ethics

Auditing and Ethics

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Auditing and Ethics 1

Contents

Introduction.................................................................................................................................................2

Section 1......................................................................................................................................................2

Level of materiality used in the audit of group accounts in Genworth Mortgage Insurance Australia

Limited....................................................................................................................................................2

Section 2......................................................................................................................................................5

Analysis of the financial position of the company and relevant auditing procedures for assertions.........5

Section 3....................................................................................................................................................10

Analysis of the statement of cash flows.................................................................................................10

Conclusion.................................................................................................................................................12

References.................................................................................................................................................13

Contents

Introduction.................................................................................................................................................2

Section 1......................................................................................................................................................2

Level of materiality used in the audit of group accounts in Genworth Mortgage Insurance Australia

Limited....................................................................................................................................................2

Section 2......................................................................................................................................................5

Analysis of the financial position of the company and relevant auditing procedures for assertions.........5

Section 3....................................................................................................................................................10

Analysis of the statement of cash flows.................................................................................................10

Conclusion.................................................................................................................................................12

References.................................................................................................................................................13

Auditing and Ethics 2

Introduction

Audit materiality is amongst the most important concepts for auditors. Misstatements are

considered material if they influence the decision making of the users based on the financial

statements. Materiality encompasses qualitative and quantitative aspects of auditing. While

dealing with materiality in the aspects of quantity, the points to be considered are setting up of

the preliminary judgment of materiality which is done at the planning stage of audit (ICAEW,

2017).

In this context, there are certain phrases in relation to materiality such as misstatements including

omissions which can impact the decision making of the users of financial statements. It is also

based on the judgment which is based upon the surrounding circumstances comprising of size

and nature if misstatements (CFI Education Inc, 2015). .So, in this article, the concept of

materiality would be discussed in the context of Genworth Mortgage Insurance Australia

Limited.

The draft annual report and its financial statements would also be analyzed along with the

various ratios over the period of 2014-2017. The key risk areas will be assessed and audit

procedures would be advised to mitigate those risks.

Introduction

Audit materiality is amongst the most important concepts for auditors. Misstatements are

considered material if they influence the decision making of the users based on the financial

statements. Materiality encompasses qualitative and quantitative aspects of auditing. While

dealing with materiality in the aspects of quantity, the points to be considered are setting up of

the preliminary judgment of materiality which is done at the planning stage of audit (ICAEW,

2017).

In this context, there are certain phrases in relation to materiality such as misstatements including

omissions which can impact the decision making of the users of financial statements. It is also

based on the judgment which is based upon the surrounding circumstances comprising of size

and nature if misstatements (CFI Education Inc, 2015). .So, in this article, the concept of

materiality would be discussed in the context of Genworth Mortgage Insurance Australia

Limited.

The draft annual report and its financial statements would also be analyzed along with the

various ratios over the period of 2014-2017. The key risk areas will be assessed and audit

procedures would be advised to mitigate those risks.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Auditing and Ethics 3

Section 1

Level of materiality used in the audit of group accounts in Genworth Mortgage Insurance

Australia Limited

The auditors set the materiality regarding the financial statements at the stage of planning. The

primary purpose is to use it to identify the performance of materiality and clarifying the

thresholds for accumulating misstatements. The concept of materiality pertains to misstatements

and omissions which are considered to be material if they individually or collectively affect the

decision making of the stakeholders on the basis of financial statements. It comprises of

qualitative and quantitative aspects.

As per ASA 320 Materiality in Planning and Performing an Audit, the quantitative

considerations consider the aspects such as setting preliminary judgment for materiality.It is

done at the planning stage of audit and the performance materiality is considered .i.e. materiality

on a line item basis for example inventory and accounts receivable. The materiality should be

estimated in a cycle or a particular account(AASB Standard, 2013).

As per AASB 1031, the qualitative considerations pertain to the non-disclosers made by the

company such as contingent liability and transactions of a related party. There are various

methods which the group auditors use to determine the level of component materiality

comprising of setting up the limit of aggregate of component materiality which is relative to the

group materiality. Their limits would increase proportionately to the increase in the number of

components. Factors influencing the level of component materiality comprise the fact that

component materiality is lower than the group materiality.

Section 1

Level of materiality used in the audit of group accounts in Genworth Mortgage Insurance

Australia Limited

The auditors set the materiality regarding the financial statements at the stage of planning. The

primary purpose is to use it to identify the performance of materiality and clarifying the

thresholds for accumulating misstatements. The concept of materiality pertains to misstatements

and omissions which are considered to be material if they individually or collectively affect the

decision making of the stakeholders on the basis of financial statements. It comprises of

qualitative and quantitative aspects.

As per ASA 320 Materiality in Planning and Performing an Audit, the quantitative

considerations consider the aspects such as setting preliminary judgment for materiality.It is

done at the planning stage of audit and the performance materiality is considered .i.e. materiality

on a line item basis for example inventory and accounts receivable. The materiality should be

estimated in a cycle or a particular account(AASB Standard, 2013).

As per AASB 1031, the qualitative considerations pertain to the non-disclosers made by the

company such as contingent liability and transactions of a related party. There are various

methods which the group auditors use to determine the level of component materiality

comprising of setting up the limit of aggregate of component materiality which is relative to the

group materiality. Their limits would increase proportionately to the increase in the number of

components. Factors influencing the level of component materiality comprise the fact that

component materiality is lower than the group materiality.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Auditing and Ethics 4

In Genworth Mortgage Insurance Australia Limited, the general rule of considering materiality

is 5-10% of normalizing net income and 0.5-2% of the total assets. In this case, the materiality

margin in Gross Written Premium (GWP) should be up to 5-10 %. 10% of GWP A$ 381.91

Million in the year 2016 is A$ 38.191 Million. The maximum GWP in the year 2017 should be

A$ 343.719 Million. In this case, the GWP in the year 2017 is A$368.963 Million.

The total assets in 2016 are A$ 3835.552 Million. The materiality margin, in this case, should be

2% of the total assets which should be A$ 76.711 Million. The total assets should be A$

3758.841 Million. In the given case, the total amount is A$ 3765.885 Million which is greater

than the given amount.

The operating lease commitments of the company were A$10.135 Million in 2016 whereas it

was A$22.317 Million in the year 2017. The group leases the property and equipment as per the

operating leases in which the lessor retains all the benefits and risks arising out of the ownership

of leased items which expire from one to five years.

Upon their renewal, the terms are renewed and the payments of the lease comprise of base

amount along with an incremental contingent rental. The contingent rentals are based upon the

fluctuations in the Consumer Price Index. The auditing procedures to address the contingencies

and risk assessment are:

1. Control the environment

2. Assessment of risk

3. Information system

4. Control the activities

5. Monitoring controls

In Genworth Mortgage Insurance Australia Limited, the general rule of considering materiality

is 5-10% of normalizing net income and 0.5-2% of the total assets. In this case, the materiality

margin in Gross Written Premium (GWP) should be up to 5-10 %. 10% of GWP A$ 381.91

Million in the year 2016 is A$ 38.191 Million. The maximum GWP in the year 2017 should be

A$ 343.719 Million. In this case, the GWP in the year 2017 is A$368.963 Million.

The total assets in 2016 are A$ 3835.552 Million. The materiality margin, in this case, should be

2% of the total assets which should be A$ 76.711 Million. The total assets should be A$

3758.841 Million. In the given case, the total amount is A$ 3765.885 Million which is greater

than the given amount.

The operating lease commitments of the company were A$10.135 Million in 2016 whereas it

was A$22.317 Million in the year 2017. The group leases the property and equipment as per the

operating leases in which the lessor retains all the benefits and risks arising out of the ownership

of leased items which expire from one to five years.

Upon their renewal, the terms are renewed and the payments of the lease comprise of base

amount along with an incremental contingent rental. The contingent rentals are based upon the

fluctuations in the Consumer Price Index. The auditing procedures to address the contingencies

and risk assessment are:

1. Control the environment

2. Assessment of risk

3. Information system

4. Control the activities

5. Monitoring controls

Auditing and Ethics 5

The auditors are required to assess the issues of governance and whether the company has

created and maintained a culture of honesty and ethical behavior. Secondly, auditors are required

to evaluate the risk assessment procedures of the entity by identifying its business risks and

estimating the relevance of those risks.

The next step would be to obtain the understanding of the information systems and accounting

records. The auditors are required to understand how the company communicates its role in

financial reporting with the regulatory authorities. They are also required to obtain the

understanding of the control activities which are relevant to evaluate the risks of material

misstatements and to formulate procedures to mitigate the risks. Lastly, the auditors should

analyze the monitoring activities used to control over the financial reporting ( Budescu, Peecher

& Solomon,2012).

Section 2

Analysis of the financial position of the company and relevant auditing procedures for

assertions

As per Genworth (2017) the company is the leading provider of Lenders Mortgage Insurance

(LMI) in Australia. LMI has been a crucial part of the residential mortgage lending market in

Australia since Housing Loan Insurance Corporation was founded in 1965 by the Australian

Government.

The vision of Genworth is to provide consumer-focused capital and risk management solutions

in the residential mortgage markets. In the year 2017, its Gross Written Premium was

The auditors are required to assess the issues of governance and whether the company has

created and maintained a culture of honesty and ethical behavior. Secondly, auditors are required

to evaluate the risk assessment procedures of the entity by identifying its business risks and

estimating the relevance of those risks.

The next step would be to obtain the understanding of the information systems and accounting

records. The auditors are required to understand how the company communicates its role in

financial reporting with the regulatory authorities. They are also required to obtain the

understanding of the control activities which are relevant to evaluate the risks of material

misstatements and to formulate procedures to mitigate the risks. Lastly, the auditors should

analyze the monitoring activities used to control over the financial reporting ( Budescu, Peecher

& Solomon,2012).

Section 2

Analysis of the financial position of the company and relevant auditing procedures for

assertions

As per Genworth (2017) the company is the leading provider of Lenders Mortgage Insurance

(LMI) in Australia. LMI has been a crucial part of the residential mortgage lending market in

Australia since Housing Loan Insurance Corporation was founded in 1965 by the Australian

Government.

The vision of Genworth is to provide consumer-focused capital and risk management solutions

in the residential mortgage markets. In the year 2017, its Gross Written Premium was

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Auditing and Ethics 6

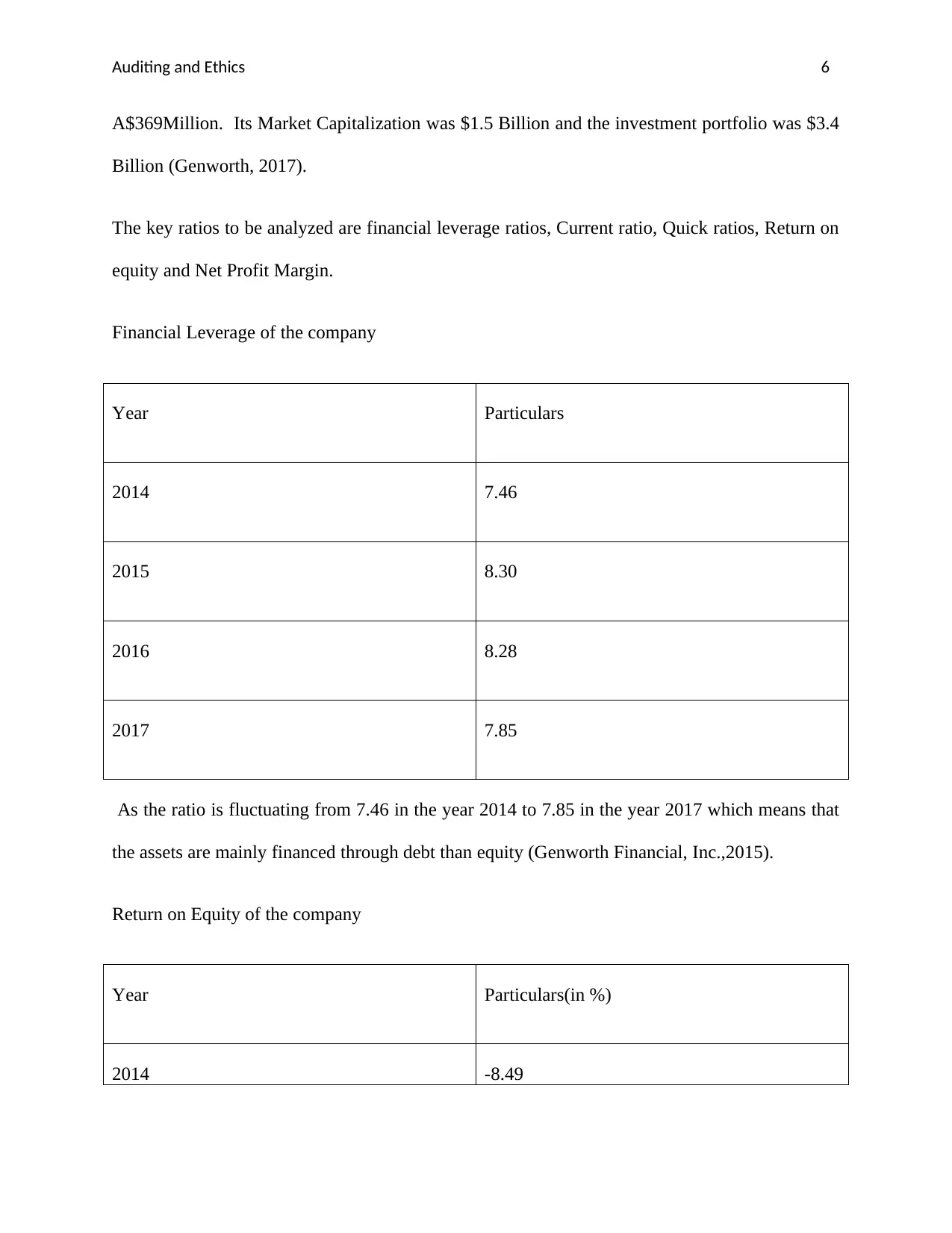

A$369Million. Its Market Capitalization was $1.5 Billion and the investment portfolio was $3.4

Billion (Genworth, 2017).

The key ratios to be analyzed are financial leverage ratios, Current ratio, Quick ratios, Return on

equity and Net Profit Margin.

Financial Leverage of the company

Year Particulars

2014 7.46

2015 8.30

2016 8.28

2017 7.85

As the ratio is fluctuating from 7.46 in the year 2014 to 7.85 in the year 2017 which means that

the assets are mainly financed through debt than equity (Genworth Financial, Inc.,2015).

Return on Equity of the company

Year Particulars(in %)

2014 -8.49

A$369Million. Its Market Capitalization was $1.5 Billion and the investment portfolio was $3.4

Billion (Genworth, 2017).

The key ratios to be analyzed are financial leverage ratios, Current ratio, Quick ratios, Return on

equity and Net Profit Margin.

Financial Leverage of the company

Year Particulars

2014 7.46

2015 8.30

2016 8.28

2017 7.85

As the ratio is fluctuating from 7.46 in the year 2014 to 7.85 in the year 2017 which means that

the assets are mainly financed through debt than equity (Genworth Financial, Inc.,2015).

Return on Equity of the company

Year Particulars(in %)

2014 -8.49

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Auditing and Ethics 7

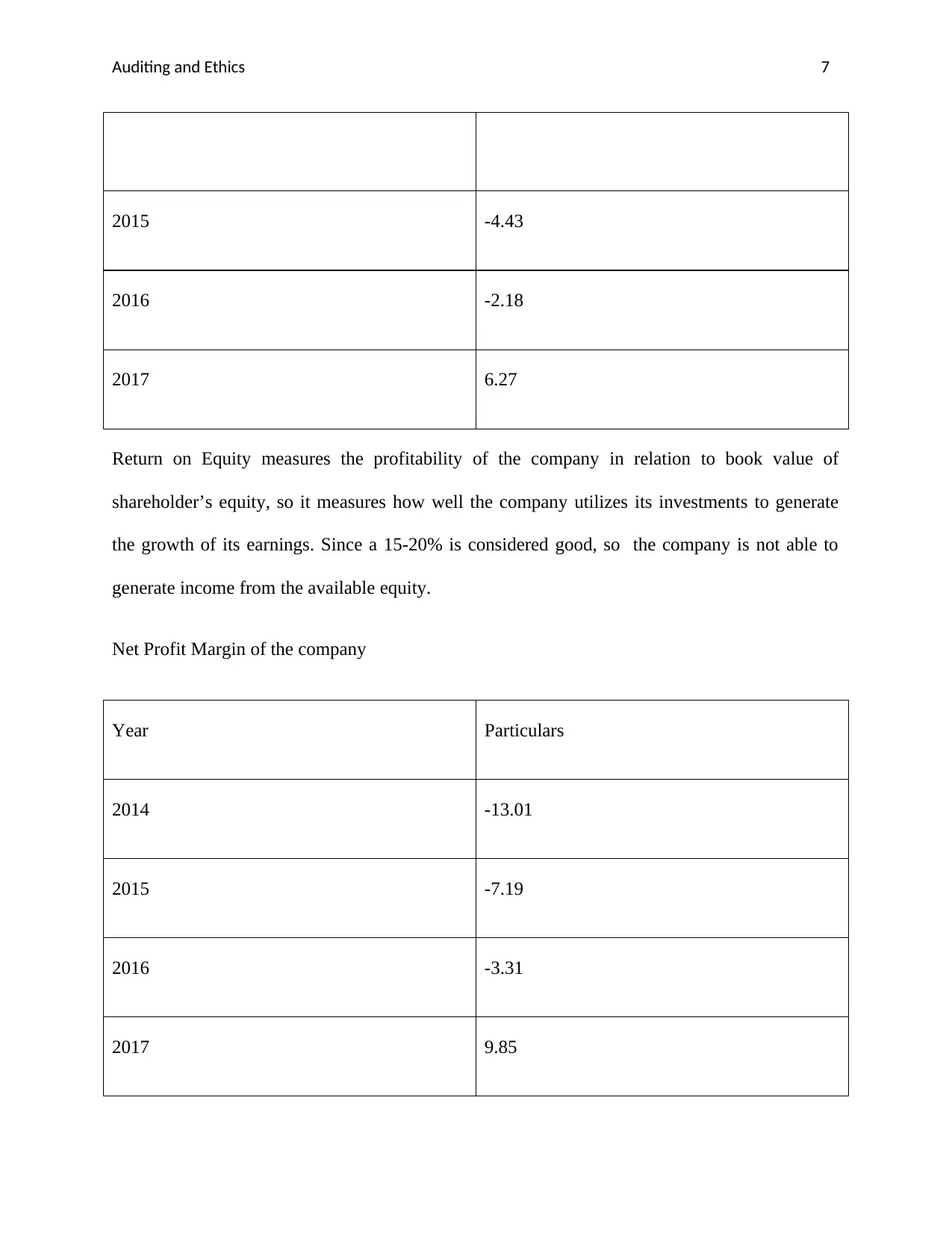

2015 -4.43

2016 -2.18

2017 6.27

Return on Equity measures the profitability of the company in relation to book value of

shareholder’s equity, so it measures how well the company utilizes its investments to generate

the growth of its earnings. Since a 15-20% is considered good, so the company is not able to

generate income from the available equity.

Net Profit Margin of the company

Year Particulars

2014 -13.01

2015 -7.19

2016 -3.31

2017 9.85

2015 -4.43

2016 -2.18

2017 6.27

Return on Equity measures the profitability of the company in relation to book value of

shareholder’s equity, so it measures how well the company utilizes its investments to generate

the growth of its earnings. Since a 15-20% is considered good, so the company is not able to

generate income from the available equity.

Net Profit Margin of the company

Year Particulars

2014 -13.01

2015 -7.19

2016 -3.31

2017 9.85

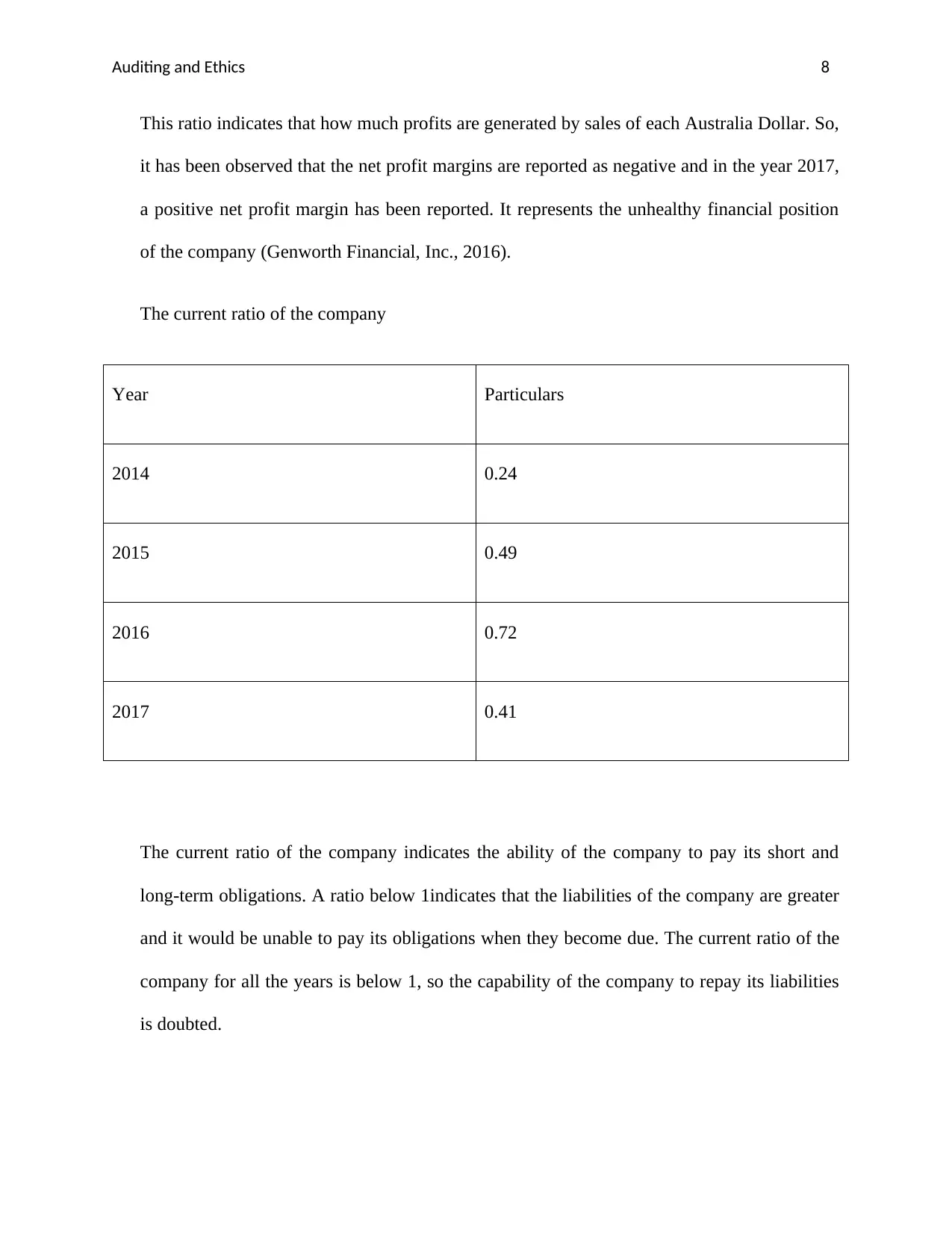

Auditing and Ethics 8

This ratio indicates that how much profits are generated by sales of each Australia Dollar. So,

it has been observed that the net profit margins are reported as negative and in the year 2017,

a positive net profit margin has been reported. It represents the unhealthy financial position

of the company (Genworth Financial, Inc., 2016).

The current ratio of the company

Year Particulars

2014 0.24

2015 0.49

2016 0.72

2017 0.41

The current ratio of the company indicates the ability of the company to pay its short and

long-term obligations. A ratio below 1indicates that the liabilities of the company are greater

and it would be unable to pay its obligations when they become due. The current ratio of the

company for all the years is below 1, so the capability of the company to repay its liabilities

is doubted.

This ratio indicates that how much profits are generated by sales of each Australia Dollar. So,

it has been observed that the net profit margins are reported as negative and in the year 2017,

a positive net profit margin has been reported. It represents the unhealthy financial position

of the company (Genworth Financial, Inc., 2016).

The current ratio of the company

Year Particulars

2014 0.24

2015 0.49

2016 0.72

2017 0.41

The current ratio of the company indicates the ability of the company to pay its short and

long-term obligations. A ratio below 1indicates that the liabilities of the company are greater

and it would be unable to pay its obligations when they become due. The current ratio of the

company for all the years is below 1, so the capability of the company to repay its liabilities

is doubted.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Auditing and Ethics 9

The key risk areas to be addressed to be addressed in the audit plan are an assessment of

audit areas which are affected by economic factors, analyzing the recurring audit

deficiencies. They should increase the transparency through new disclosers and focus on the

independence of auditors (Hall, 2015).

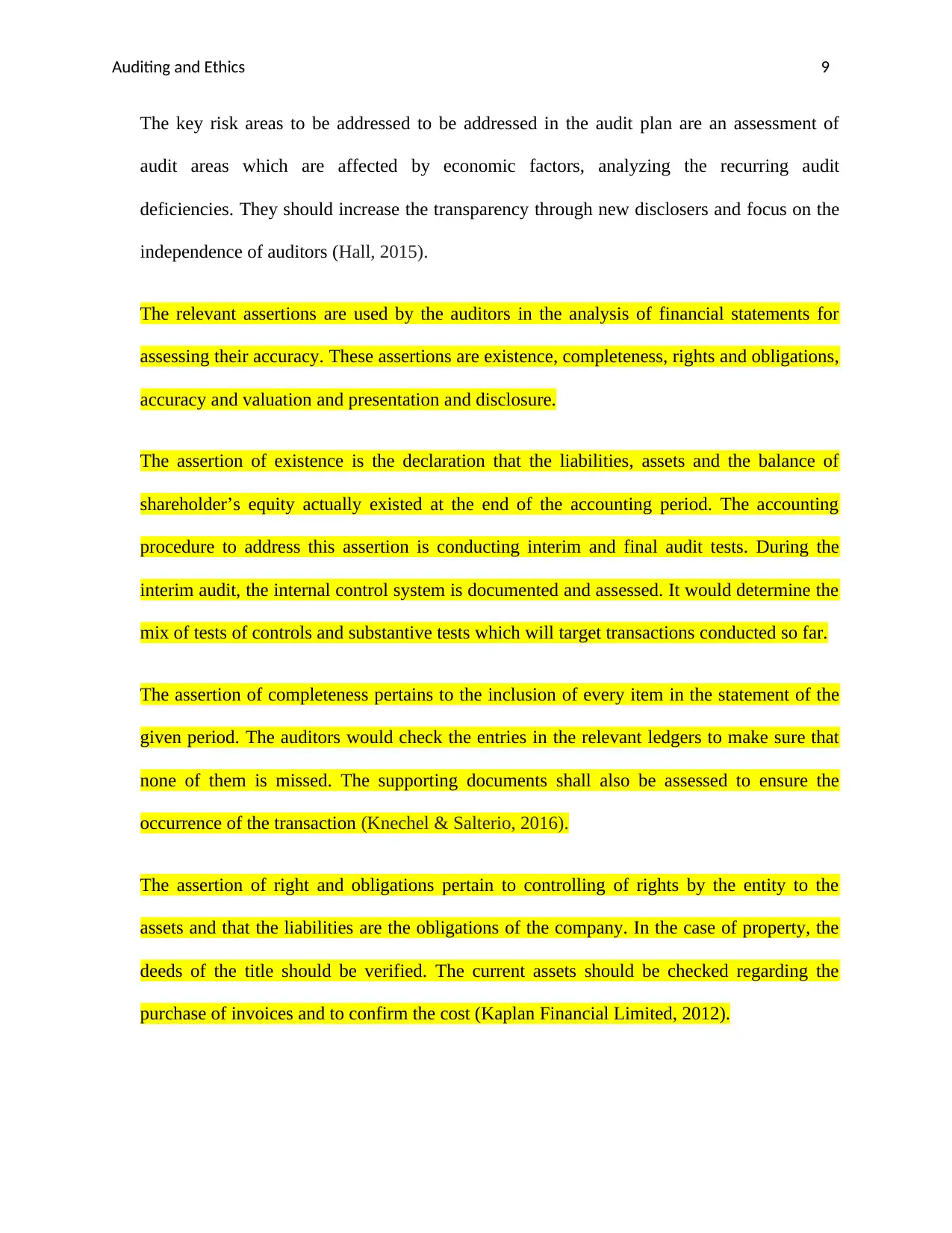

The relevant assertions are used by the auditors in the analysis of financial statements for

assessing their accuracy. These assertions are existence, completeness, rights and obligations,

accuracy and valuation and presentation and disclosure.

The assertion of existence is the declaration that the liabilities, assets and the balance of

shareholder’s equity actually existed at the end of the accounting period. The accounting

procedure to address this assertion is conducting interim and final audit tests. During the

interim audit, the internal control system is documented and assessed. It would determine the

mix of tests of controls and substantive tests which will target transactions conducted so far.

The assertion of completeness pertains to the inclusion of every item in the statement of the

given period. The auditors would check the entries in the relevant ledgers to make sure that

none of them is missed. The supporting documents shall also be assessed to ensure the

occurrence of the transaction (Knechel & Salterio, 2016).

The assertion of right and obligations pertain to controlling of rights by the entity to the

assets and that the liabilities are the obligations of the company. In the case of property, the

deeds of the title should be verified. The current assets should be checked regarding the

purchase of invoices and to confirm the cost (Kaplan Financial Limited, 2012).

The key risk areas to be addressed to be addressed in the audit plan are an assessment of

audit areas which are affected by economic factors, analyzing the recurring audit

deficiencies. They should increase the transparency through new disclosers and focus on the

independence of auditors (Hall, 2015).

The relevant assertions are used by the auditors in the analysis of financial statements for

assessing their accuracy. These assertions are existence, completeness, rights and obligations,

accuracy and valuation and presentation and disclosure.

The assertion of existence is the declaration that the liabilities, assets and the balance of

shareholder’s equity actually existed at the end of the accounting period. The accounting

procedure to address this assertion is conducting interim and final audit tests. During the

interim audit, the internal control system is documented and assessed. It would determine the

mix of tests of controls and substantive tests which will target transactions conducted so far.

The assertion of completeness pertains to the inclusion of every item in the statement of the

given period. The auditors would check the entries in the relevant ledgers to make sure that

none of them is missed. The supporting documents shall also be assessed to ensure the

occurrence of the transaction (Knechel & Salterio, 2016).

The assertion of right and obligations pertain to controlling of rights by the entity to the

assets and that the liabilities are the obligations of the company. In the case of property, the

deeds of the title should be verified. The current assets should be checked regarding the

purchase of invoices and to confirm the cost (Kaplan Financial Limited, 2012).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Auditing and Ethics 10

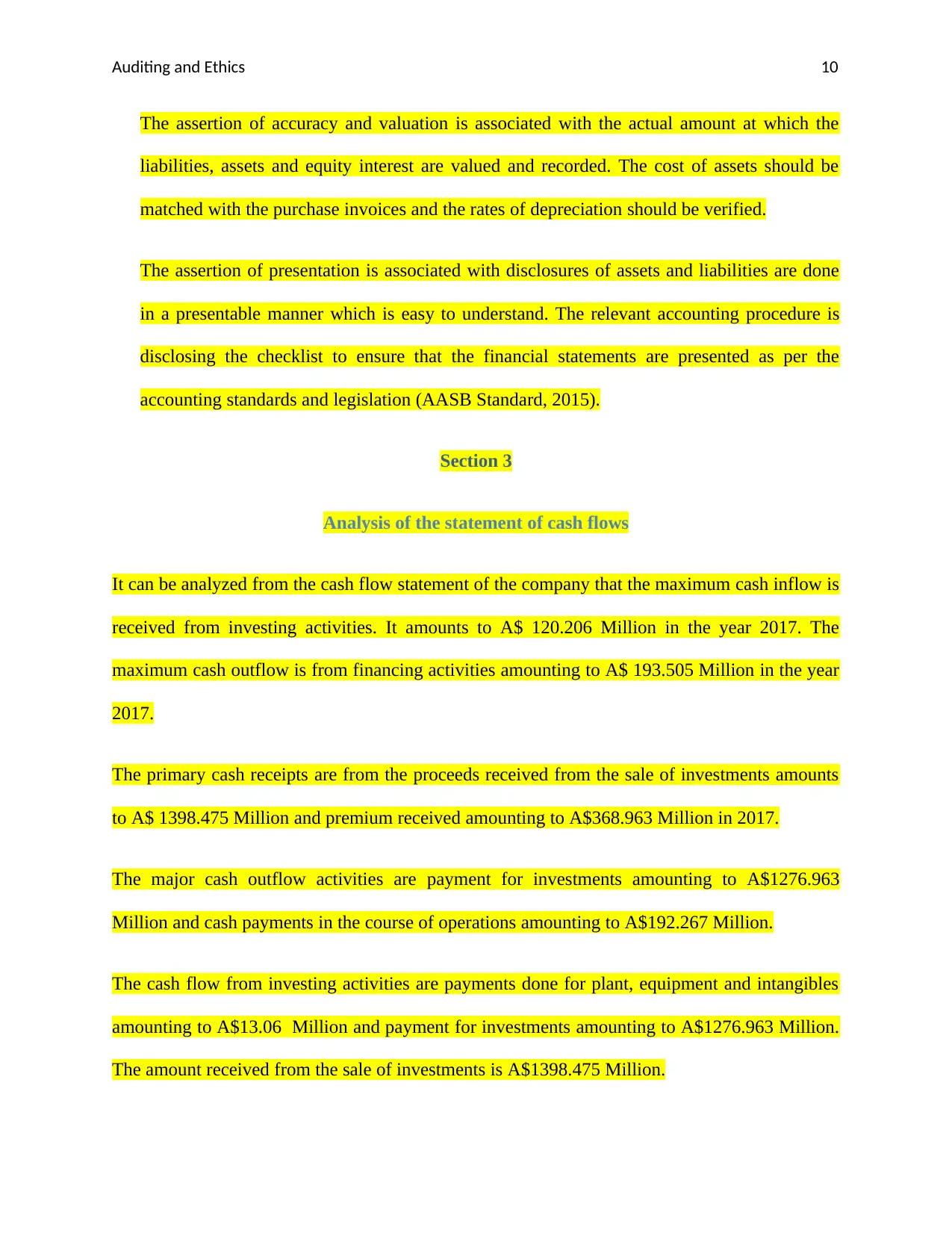

The assertion of accuracy and valuation is associated with the actual amount at which the

liabilities, assets and equity interest are valued and recorded. The cost of assets should be

matched with the purchase invoices and the rates of depreciation should be verified.

The assertion of presentation is associated with disclosures of assets and liabilities are done

in a presentable manner which is easy to understand. The relevant accounting procedure is

disclosing the checklist to ensure that the financial statements are presented as per the

accounting standards and legislation (AASB Standard, 2015).

Section 3

Analysis of the statement of cash flows

It can be analyzed from the cash flow statement of the company that the maximum cash inflow is

received from investing activities. It amounts to A$ 120.206 Million in the year 2017. The

maximum cash outflow is from financing activities amounting to A$ 193.505 Million in the year

2017.

The primary cash receipts are from the proceeds received from the sale of investments amounts

to A$ 1398.475 Million and premium received amounting to A$368.963 Million in 2017.

The major cash outflow activities are payment for investments amounting to A$1276.963

Million and cash payments in the course of operations amounting to A$192.267 Million.

The cash flow from investing activities are payments done for plant, equipment and intangibles

amounting to A$13.06 Million and payment for investments amounting to A$1276.963 Million.

The amount received from the sale of investments is A$1398.475 Million.

The assertion of accuracy and valuation is associated with the actual amount at which the

liabilities, assets and equity interest are valued and recorded. The cost of assets should be

matched with the purchase invoices and the rates of depreciation should be verified.

The assertion of presentation is associated with disclosures of assets and liabilities are done

in a presentable manner which is easy to understand. The relevant accounting procedure is

disclosing the checklist to ensure that the financial statements are presented as per the

accounting standards and legislation (AASB Standard, 2015).

Section 3

Analysis of the statement of cash flows

It can be analyzed from the cash flow statement of the company that the maximum cash inflow is

received from investing activities. It amounts to A$ 120.206 Million in the year 2017. The

maximum cash outflow is from financing activities amounting to A$ 193.505 Million in the year

2017.

The primary cash receipts are from the proceeds received from the sale of investments amounts

to A$ 1398.475 Million and premium received amounting to A$368.963 Million in 2017.

The major cash outflow activities are payment for investments amounting to A$1276.963

Million and cash payments in the course of operations amounting to A$192.267 Million.

The cash flow from investing activities are payments done for plant, equipment and intangibles

amounting to A$13.06 Million and payment for investments amounting to A$1276.963 Million.

The amount received from the sale of investments is A$1398.475 Million.

Auditing and Ethics 11

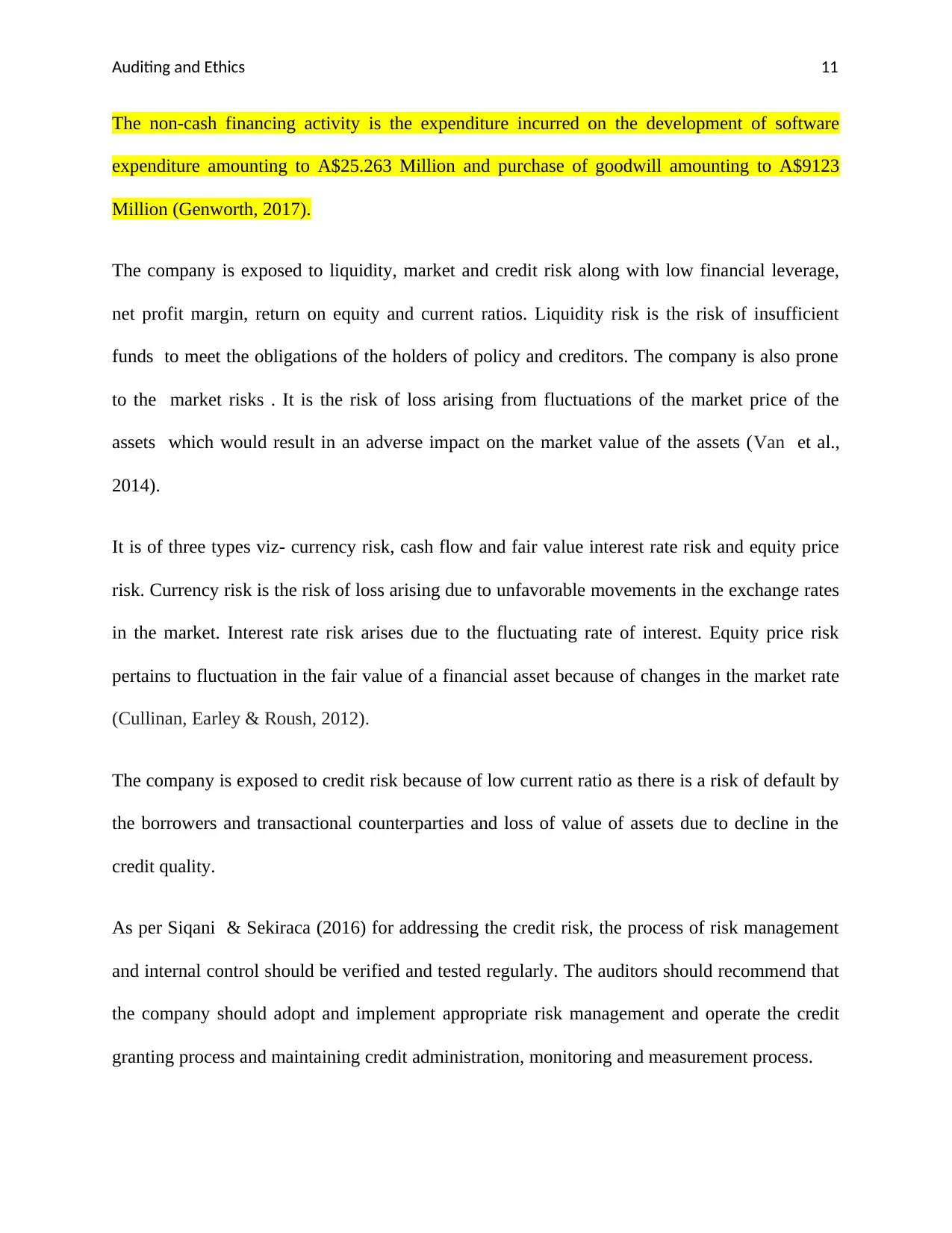

The non-cash financing activity is the expenditure incurred on the development of software

expenditure amounting to A$25.263 Million and purchase of goodwill amounting to A$9123

Million (Genworth, 2017).

The company is exposed to liquidity, market and credit risk along with low financial leverage,

net profit margin, return on equity and current ratios. Liquidity risk is the risk of insufficient

funds to meet the obligations of the holders of policy and creditors. The company is also prone

to the market risks . It is the risk of loss arising from fluctuations of the market price of the

assets which would result in an adverse impact on the market value of the assets (Van et al.,

2014).

It is of three types viz- currency risk, cash flow and fair value interest rate risk and equity price

risk. Currency risk is the risk of loss arising due to unfavorable movements in the exchange rates

in the market. Interest rate risk arises due to the fluctuating rate of interest. Equity price risk

pertains to fluctuation in the fair value of a financial asset because of changes in the market rate

(Cullinan, Earley & Roush, 2012).

The company is exposed to credit risk because of low current ratio as there is a risk of default by

the borrowers and transactional counterparties and loss of value of assets due to decline in the

credit quality.

As per Siqani & Sekiraca (2016) for addressing the credit risk, the process of risk management

and internal control should be verified and tested regularly. The auditors should recommend that

the company should adopt and implement appropriate risk management and operate the credit

granting process and maintaining credit administration, monitoring and measurement process.

The non-cash financing activity is the expenditure incurred on the development of software

expenditure amounting to A$25.263 Million and purchase of goodwill amounting to A$9123

Million (Genworth, 2017).

The company is exposed to liquidity, market and credit risk along with low financial leverage,

net profit margin, return on equity and current ratios. Liquidity risk is the risk of insufficient

funds to meet the obligations of the holders of policy and creditors. The company is also prone

to the market risks . It is the risk of loss arising from fluctuations of the market price of the

assets which would result in an adverse impact on the market value of the assets (Van et al.,

2014).

It is of three types viz- currency risk, cash flow and fair value interest rate risk and equity price

risk. Currency risk is the risk of loss arising due to unfavorable movements in the exchange rates

in the market. Interest rate risk arises due to the fluctuating rate of interest. Equity price risk

pertains to fluctuation in the fair value of a financial asset because of changes in the market rate

(Cullinan, Earley & Roush, 2012).

The company is exposed to credit risk because of low current ratio as there is a risk of default by

the borrowers and transactional counterparties and loss of value of assets due to decline in the

credit quality.

As per Siqani & Sekiraca (2016) for addressing the credit risk, the process of risk management

and internal control should be verified and tested regularly. The auditors should recommend that

the company should adopt and implement appropriate risk management and operate the credit

granting process and maintaining credit administration, monitoring and measurement process.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 16

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.