Comprehensive Auditing and Financial Analysis of DIPL Ltd

VerifiedAdded on 2020/03/01

|9

|2344

|68

Report

AI Summary

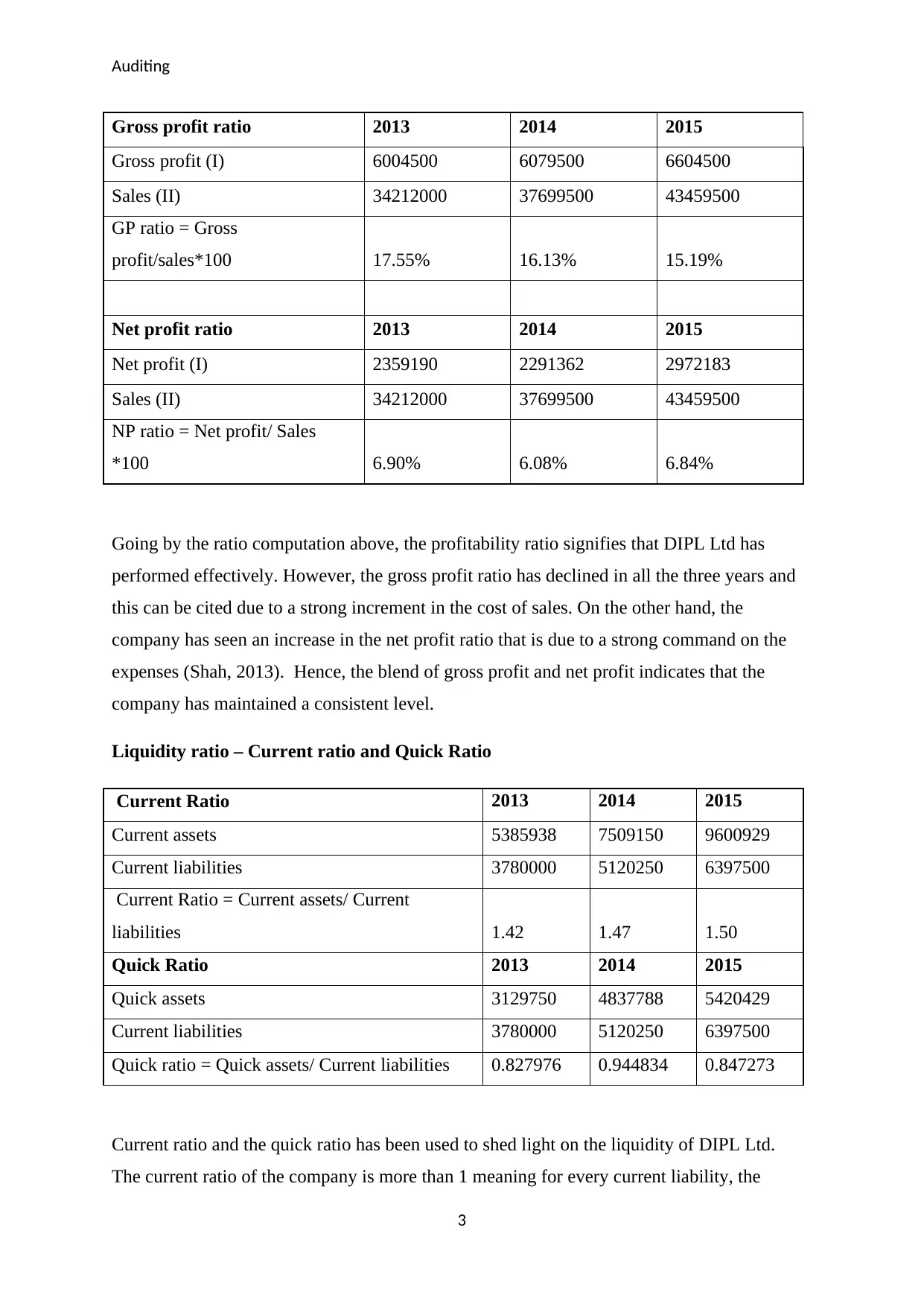

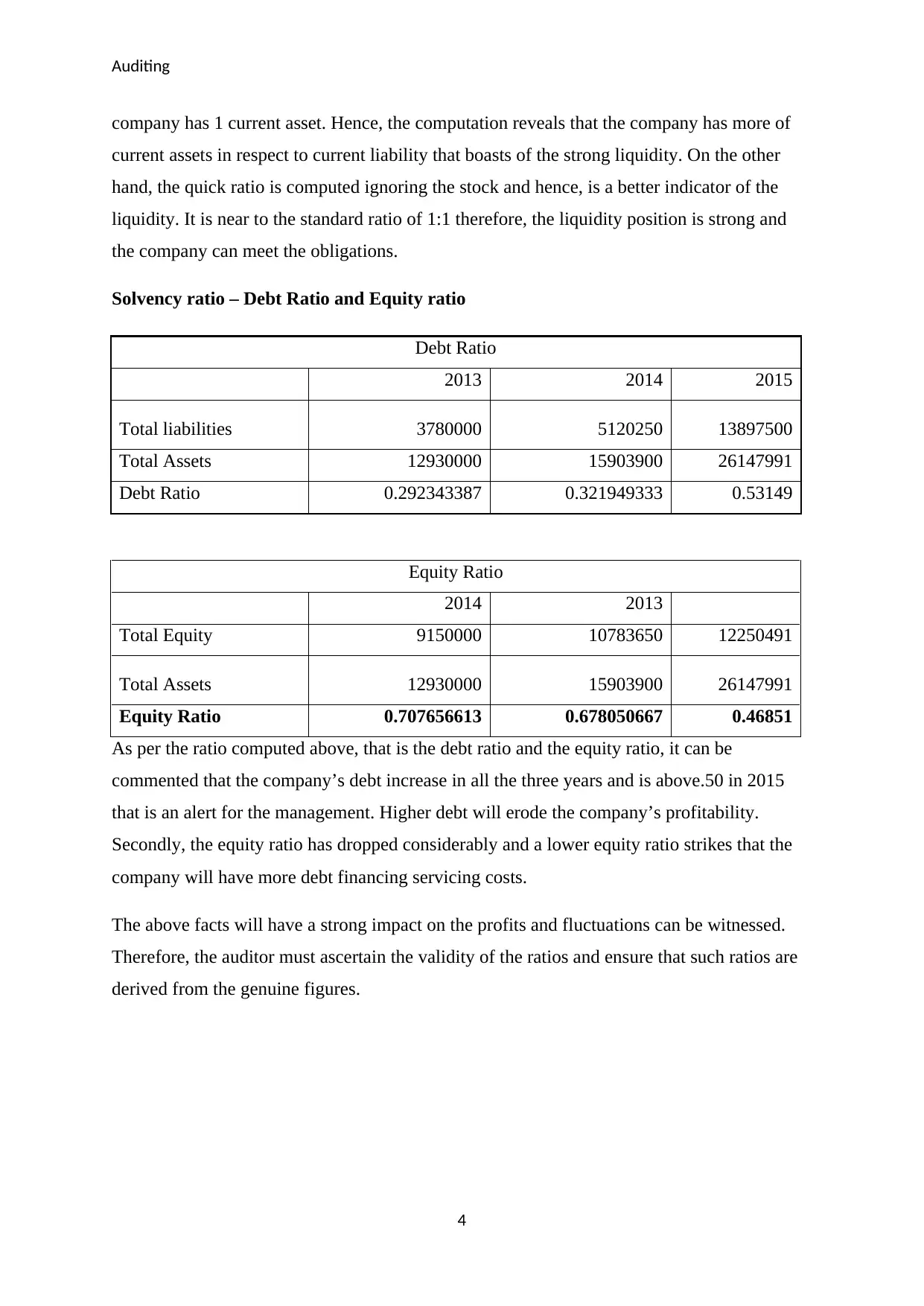

This report provides a detailed auditing analysis of DIPL Ltd. It begins with an overview of analytical procedures, comparing financial data over three years and with industry standards. The report then delves into ratio analysis, examining profitability (gross and net profit margins), liquidity (current and quick ratios), and solvency (debt and equity ratios) from 2013 to 2015. The analysis highlights trends, strengths, and weaknesses in DIPL Ltd's financial performance. Furthermore, the report identifies inherent risks, such as errors in a new IT system and unethical CEO appointments, and fraud risks, including the abandonment of the old IT system and inventory valuation issues. The impact of these risks on the audit process and the auditor's responsibilities in providing a true and fair view are also discussed, including the potential for qualified opinions and the need for detailed analysis to ensure audit quality. The report emphasizes the importance of auditors applying reasonable skills and cross-checking data to provide an unqualified opinion.

1 out of 9

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.