Auditing & Assurance: Business Risks, Fraud Impact, Audit Risks, and Testing

VerifiedAdded on 2022/11/07

|13

|3550

|89

AI Summary

This document discusses the business risks, fraud impact, audit risks, and testing related to auditing and assurance. It also includes additional audit work, key questions, audit strategy, environment control, customer payments testing, and accounts payable tests.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

1Running Head: AUDITING & ASSURANCE

Auditing & Assurance

Author’s Name

Institutional Affiliation

Auditing & Assurance

Author’s Name

Institutional Affiliation

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

2AUDITING & ASSURANCE

Auditing & Assurance

To: Jek Porkins

From: Audit Manager

Date:

Subject: Dudley Health Limited (DHL) Assignment

Business Risks

Business Risk Impact

Based on the case scenario, it has been found that Samway Baker Fitzgerald (SBF) is an

organization, which has a branch in Pellegrino Shores. The senior staff member of this branch

had conducted a fraud associated with the payment of residents in Port Macquarie. Moreover, the

senior employees were found to be involved in a scam, which created a tremendous impact on

the organization and the business in an effective manner. In the initial stage, it can increase the

risk of misstatement, which can further create an issue in the transactional balance of the

company. In addition, it can also affect the organizational integrity within the market. The key

authorities may face issues in operating a business in the existing market because the fraud can

manipulate the accounting activities to a large extent (Ftms, 2013).

The financial background of the company may be affected badly, as the company may

face major financial pressure within the market. In addition, it can lead to the creation of a vague

financial report, which can lead the company towards incurring a complete loss in the market. As

the secret payment of residents was not recorded in the financial book, it can create two major

risks namely detection risk and control risk (Ftms, 2013). Lack of detection can contribute to

Auditing & Assurance

To: Jek Porkins

From: Audit Manager

Date:

Subject: Dudley Health Limited (DHL) Assignment

Business Risks

Business Risk Impact

Based on the case scenario, it has been found that Samway Baker Fitzgerald (SBF) is an

organization, which has a branch in Pellegrino Shores. The senior staff member of this branch

had conducted a fraud associated with the payment of residents in Port Macquarie. Moreover, the

senior employees were found to be involved in a scam, which created a tremendous impact on

the organization and the business in an effective manner. In the initial stage, it can increase the

risk of misstatement, which can further create an issue in the transactional balance of the

company. In addition, it can also affect the organizational integrity within the market. The key

authorities may face issues in operating a business in the existing market because the fraud can

manipulate the accounting activities to a large extent (Ftms, 2013).

The financial background of the company may be affected badly, as the company may

face major financial pressure within the market. In addition, it can lead to the creation of a vague

financial report, which can lead the company towards incurring a complete loss in the market. As

the secret payment of residents was not recorded in the financial book, it can create two major

risks namely detection risk and control risk (Ftms, 2013). Lack of detection can contribute to

3AUDITING & ASSURANCE

manipulating the organization towards the wrong control, which can further be considered as

harmful for the company.

Impact of Fraud at Pellegrino Shores

Based on the fraud scenario, certain accounts have been affected, which can create a

misstatement in the financial books. In the initial stage, the book of the resident database

associated with the room rent has been affected. In addition, the money allocated for the various

services to the resident also affected the fraud activity. The company also created a limited

money structure of room rent and services on the basis of the period of stay. Hence, the money

value can be changed due to the fraudulent activities, wherein the resident can claim for the

services in relation to the money paid by them. A major manipulation can be seen in the

calculation of their salary and wages, which affected the expense accounts i.e. employee

insurance, profit and loss account, balance sheet and trial balance book among others largely. It

may even lead the company towards facing audit risk i.e. lack of opportunity to grow, less

rationalization in the business operation and higher volume of financial pressure to control the

loss due to fraud (Dallas, 2011).

Additional Audit Work

Associated Audit Risks

The fraudulent activity not only affects the business operation but also increases the audit

risks, which can harm the financial activities of SBF. The management of net working capital

can get affected tremendously. It can further help in determining financial maturity and

organizational ability to invest. Hence, the secretly collected amount will create an issue in

adjusting the working capital in the financial book. In addition, it can create an issue in

manipulating the organization towards the wrong control, which can further be considered as

harmful for the company.

Impact of Fraud at Pellegrino Shores

Based on the fraud scenario, certain accounts have been affected, which can create a

misstatement in the financial books. In the initial stage, the book of the resident database

associated with the room rent has been affected. In addition, the money allocated for the various

services to the resident also affected the fraud activity. The company also created a limited

money structure of room rent and services on the basis of the period of stay. Hence, the money

value can be changed due to the fraudulent activities, wherein the resident can claim for the

services in relation to the money paid by them. A major manipulation can be seen in the

calculation of their salary and wages, which affected the expense accounts i.e. employee

insurance, profit and loss account, balance sheet and trial balance book among others largely. It

may even lead the company towards facing audit risk i.e. lack of opportunity to grow, less

rationalization in the business operation and higher volume of financial pressure to control the

loss due to fraud (Dallas, 2011).

Additional Audit Work

Associated Audit Risks

The fraudulent activity not only affects the business operation but also increases the audit

risks, which can harm the financial activities of SBF. The management of net working capital

can get affected tremendously. It can further help in determining financial maturity and

organizational ability to invest. Hence, the secretly collected amount will create an issue in

adjusting the working capital in the financial book. In addition, it can create an issue in

4AUDITING & ASSURANCE

measuring the organizational tax, wherein the auditor may find a wrong interpretation of taxation

in the financial records, thereby creating a major audit risk in the organization (KPMG AG.,

2019).

According to Nikolovskia, Zdravkoskib, Menkinoskic, Dičevskad, and Karadјova,

(2016), three types of audit risks are mainly faced by an organization i.e. control risk, detection

risk and inherent risk. In relation to the control risk, the incorrect claims of material or service

have been checked properly by the auditor. Hence, any type of activity related to the incorrect

claim in relation with time can create audit risk. With respect to the case, the resident can claim

services for their secret payment, which can, in turn, create an audit risk during the period of

audit. On the other hand, fault in transactions and its balance adjustment in account books can be

considered as an inherent risk. In relation to SBF, the misadjustment of the secret payment will

create an inherent risk. Inadequate supervision in financial activities can be considered in the

detection risk, wherein the key authorities are unable to control fraud. The key associates of SBF

will also face the detection risk during the period of audit. Hence, they need to create proper

strategies for handling the issues associated with patient revenue in St Neville's or else, the

organization will face major loss within the market (Nikolovskia et al., 2016).

Key Questions

Based on the scenario, two questions can be asked by the internal auditing team to the

associates in Pellegrino Shores. The following questions must be resolved properly, wherein the

organization can control the loss associated with the fraud activity.

Question 1. Which materials have been claimed by the residents in Pellegrino Shores?

All the services have been provided properly but for what was the extra amount paid?

measuring the organizational tax, wherein the auditor may find a wrong interpretation of taxation

in the financial records, thereby creating a major audit risk in the organization (KPMG AG.,

2019).

According to Nikolovskia, Zdravkoskib, Menkinoskic, Dičevskad, and Karadјova,

(2016), three types of audit risks are mainly faced by an organization i.e. control risk, detection

risk and inherent risk. In relation to the control risk, the incorrect claims of material or service

have been checked properly by the auditor. Hence, any type of activity related to the incorrect

claim in relation with time can create audit risk. With respect to the case, the resident can claim

services for their secret payment, which can, in turn, create an audit risk during the period of

audit. On the other hand, fault in transactions and its balance adjustment in account books can be

considered as an inherent risk. In relation to SBF, the misadjustment of the secret payment will

create an inherent risk. Inadequate supervision in financial activities can be considered in the

detection risk, wherein the key authorities are unable to control fraud. The key associates of SBF

will also face the detection risk during the period of audit. Hence, they need to create proper

strategies for handling the issues associated with patient revenue in St Neville's or else, the

organization will face major loss within the market (Nikolovskia et al., 2016).

Key Questions

Based on the scenario, two questions can be asked by the internal auditing team to the

associates in Pellegrino Shores. The following questions must be resolved properly, wherein the

organization can control the loss associated with the fraud activity.

Question 1. Which materials have been claimed by the residents in Pellegrino Shores?

All the services have been provided properly but for what was the extra amount paid?

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

5AUDITING & ASSURANCE

Question 2. The amount received from the resident has not been adjusted in the financial

book. Which account will these amounts be recorded? What are the purpose of these amounts

and its transaction?

Audit Strategy

The key managers of the company need to create a team including experienced officers and

employees, who can understand the financial activities. It can help them to assess and control the

internal activities, which reduces audit risk. The future risks and challenges must be assessed by

this team so that financial activities can be performed in an effective manner. Most importantly,

the organization must conduct short time audit activities which can easily resolve the issues

similar to the fraud and secret payments. Maintaining documents of each financial activities and

its proper record in the financial books can reduce the issue associated with the patient revenue

in St Neville's. The audit team or committee must take instant decision to control all the

fraudulent activities. They must implement audit policy, wherein each employee must ensure

financial activities with the documents. Proper document of all fees, salary and wages among

others can help the employees to establish a fair relationship with the organization. It also

eliminates issues associated with the secret payment and fraud activities and the issues associated

with patient revenue at St Neville's within SBF. Moreover, transparent transactions with the

residents as well as others such as consumers and suppliers can lead SBF to reduce the risks

associated with patient revenue in St Neville's (KPMG LLP, 2014: Worldbank, 2002).

Acuity Vison's Sale of Medical Supplies

Risk Associated With Key Account Balance & Financial Assertions

Question 2. The amount received from the resident has not been adjusted in the financial

book. Which account will these amounts be recorded? What are the purpose of these amounts

and its transaction?

Audit Strategy

The key managers of the company need to create a team including experienced officers and

employees, who can understand the financial activities. It can help them to assess and control the

internal activities, which reduces audit risk. The future risks and challenges must be assessed by

this team so that financial activities can be performed in an effective manner. Most importantly,

the organization must conduct short time audit activities which can easily resolve the issues

similar to the fraud and secret payments. Maintaining documents of each financial activities and

its proper record in the financial books can reduce the issue associated with the patient revenue

in St Neville's. The audit team or committee must take instant decision to control all the

fraudulent activities. They must implement audit policy, wherein each employee must ensure

financial activities with the documents. Proper document of all fees, salary and wages among

others can help the employees to establish a fair relationship with the organization. It also

eliminates issues associated with the secret payment and fraud activities and the issues associated

with patient revenue at St Neville's within SBF. Moreover, transparent transactions with the

residents as well as others such as consumers and suppliers can lead SBF to reduce the risks

associated with patient revenue in St Neville's (KPMG LLP, 2014: Worldbank, 2002).

Acuity Vison's Sale of Medical Supplies

Risk Associated With Key Account Balance & Financial Assertions

6AUDITING & ASSURANCE

As per the case scenario, the general ledger and customer account balance can be

considered as the source of the key account balance of the company. Fundamentally, the ledger

is one of the most effective financial processes, wherein all the journal entries have been verified

properly. It is a useful process of the double-entry system. Only financial transactions have been

included in this process (Nos, 2008). On the other hand, the customer account balance only

covers the consumer activities associated with sales. The organization does not follow any

accounts associated with the sales team and their need. It can, therefore, decrease employee

satisfaction within the organization. It can further create a major risk associated with

organizational sales due to low payment. The accounts related to the sales such as cash account,

profitability account, salary or wages account and sales account among others can be considered

to be of high risk due to low payment of sales team. The company also faces a major risk with

respect to employee satisfaction.

Besides, the sales team conducts direct sales within the market for generating an adequate

sum of revenue at the end of the. The company mainly focuses on consumers instead of sales

team employees. The numbers of sales executive can be reduced, which can highly affect the

cash flow within the organization. The working capital account and the book of cash flow can

also be affected due to the labor shortage. The financial position of an organization has been

properly projected through the cash flow account (Ncert, 2019). Hence, the labor shortage can

affect the financial background of the organization as well. Additionally, the organizational

potential associated with investment was affected in case labor shortage posed an impact on

working capital account the. These two can be considered as the major risks of SBF in its

existing market.

Environment Control in DHL

As per the case scenario, the general ledger and customer account balance can be

considered as the source of the key account balance of the company. Fundamentally, the ledger

is one of the most effective financial processes, wherein all the journal entries have been verified

properly. It is a useful process of the double-entry system. Only financial transactions have been

included in this process (Nos, 2008). On the other hand, the customer account balance only

covers the consumer activities associated with sales. The organization does not follow any

accounts associated with the sales team and their need. It can, therefore, decrease employee

satisfaction within the organization. It can further create a major risk associated with

organizational sales due to low payment. The accounts related to the sales such as cash account,

profitability account, salary or wages account and sales account among others can be considered

to be of high risk due to low payment of sales team. The company also faces a major risk with

respect to employee satisfaction.

Besides, the sales team conducts direct sales within the market for generating an adequate

sum of revenue at the end of the. The company mainly focuses on consumers instead of sales

team employees. The numbers of sales executive can be reduced, which can highly affect the

cash flow within the organization. The working capital account and the book of cash flow can

also be affected due to the labor shortage. The financial position of an organization has been

properly projected through the cash flow account (Ncert, 2019). Hence, the labor shortage can

affect the financial background of the organization as well. Additionally, the organizational

potential associated with investment was affected in case labor shortage posed an impact on

working capital account the. These two can be considered as the major risks of SBF in its

existing market.

Environment Control in DHL

7AUDITING & ASSURANCE

The environment can be considered as one of the effective aspects of any organization

because it develops organizational productivity and profitability. In relation to the SBF, the

company needs to develop its communicational areas in order to resolve the issues associated

with patient revenue. The internal co-operation will be developed which can further enhance

company performance within the market. Proper relationship strength must also be developed for

controlling the environment, which can lead the managers towards maintaining proper decorum.

Most importantly, the company must improve the ability of the accounting team to resolve fraud

and misstatement issue. Only proper skills and behavior of the employees can develop the

organizational environment. The issue related to the low salary can be easily mitigated through

this strategy. Moreover, SBF must provide value to the sales team in order to increase sales

within the market (Schultz & Doerr, 2015).

Customer Payments Testing

SBF must test the payments of the consumers in order to resolve the issues associated

with the new revenue system. Proper payments system and its testing can increase the

organizational trust within the market, which will provide adequate subsidies to the elder and

other patients. Furthermore, new payment system testing can introduce the required electronic

device to the customer, wherein the speed of the payments and its benefits can be increased. A

cost-effective payment network can further be introduced. In addition, the security of the

payment system will enhance, wherein each consumer can pay their bills safely. Most

importantly, the efficiency of the company will increase, which will, in turn, increase the success

rate in the international market. A proper collaboration and business relationship can further be

created through the payment testing of the consumers. These factors can thus be considered as

the major effectiveness of SBF’s customer payment testing (Federal Reserve Banks, 2016).

The environment can be considered as one of the effective aspects of any organization

because it develops organizational productivity and profitability. In relation to the SBF, the

company needs to develop its communicational areas in order to resolve the issues associated

with patient revenue. The internal co-operation will be developed which can further enhance

company performance within the market. Proper relationship strength must also be developed for

controlling the environment, which can lead the managers towards maintaining proper decorum.

Most importantly, the company must improve the ability of the accounting team to resolve fraud

and misstatement issue. Only proper skills and behavior of the employees can develop the

organizational environment. The issue related to the low salary can be easily mitigated through

this strategy. Moreover, SBF must provide value to the sales team in order to increase sales

within the market (Schultz & Doerr, 2015).

Customer Payments Testing

SBF must test the payments of the consumers in order to resolve the issues associated

with the new revenue system. Proper payments system and its testing can increase the

organizational trust within the market, which will provide adequate subsidies to the elder and

other patients. Furthermore, new payment system testing can introduce the required electronic

device to the customer, wherein the speed of the payments and its benefits can be increased. A

cost-effective payment network can further be introduced. In addition, the security of the

payment system will enhance, wherein each consumer can pay their bills safely. Most

importantly, the efficiency of the company will increase, which will, in turn, increase the success

rate in the international market. A proper collaboration and business relationship can further be

created through the payment testing of the consumers. These factors can thus be considered as

the major effectiveness of SBF’s customer payment testing (Federal Reserve Banks, 2016).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

8AUDITING & ASSURANCE

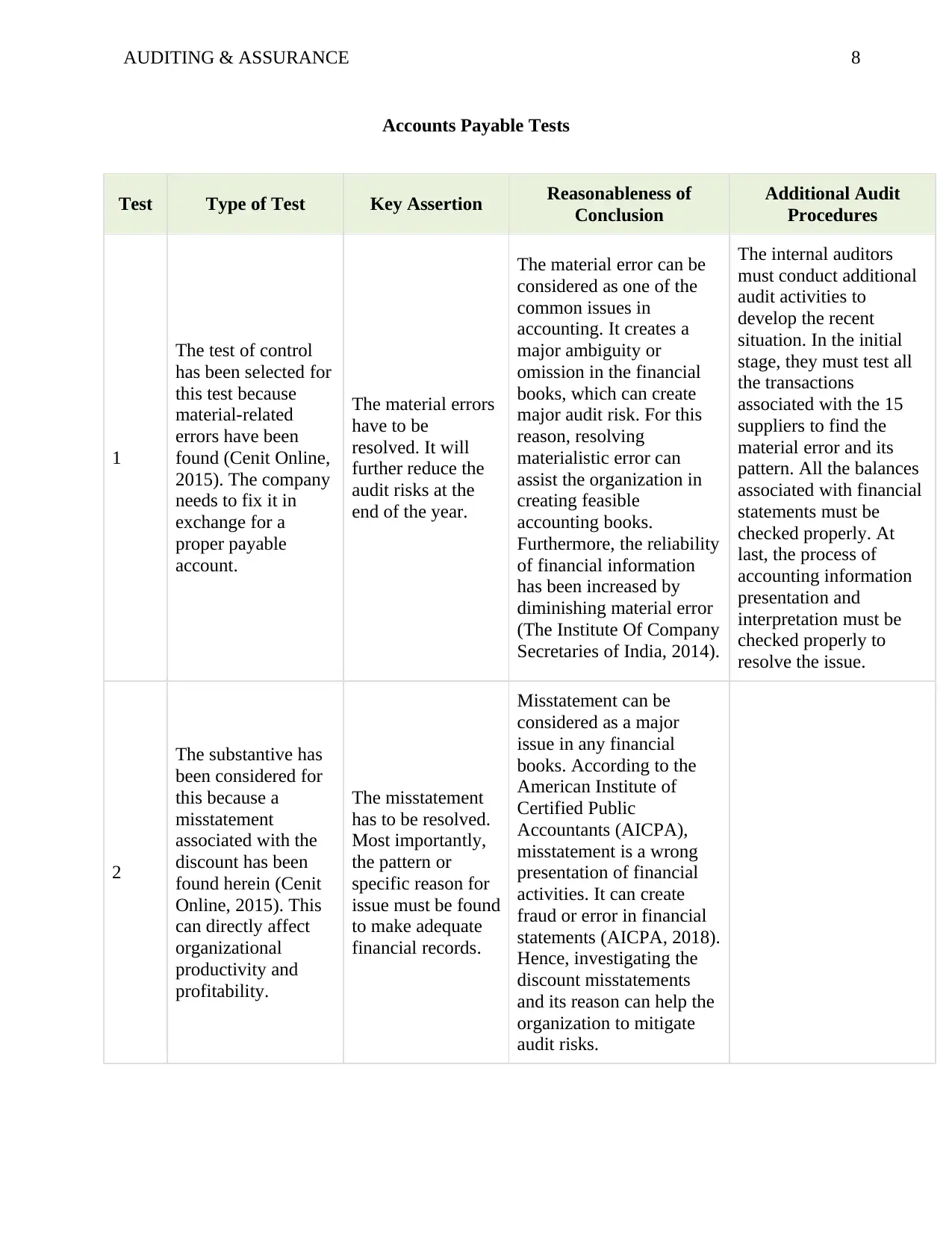

Accounts Payable Tests

Test Type of Test Key Assertion Reasonableness of

Conclusion

Additional Audit

Procedures

1

The test of control

has been selected for

this test because

material-related

errors have been

found (Cenit Online,

2015). The company

needs to fix it in

exchange for a

proper payable

account.

The material errors

have to be

resolved. It will

further reduce the

audit risks at the

end of the year.

The material error can be

considered as one of the

common issues in

accounting. It creates a

major ambiguity or

omission in the financial

books, which can create

major audit risk. For this

reason, resolving

materialistic error can

assist the organization in

creating feasible

accounting books.

Furthermore, the reliability

of financial information

has been increased by

diminishing material error

(The Institute Of Company

Secretaries of India, 2014).

The internal auditors

must conduct additional

audit activities to

develop the recent

situation. In the initial

stage, they must test all

the transactions

associated with the 15

suppliers to find the

material error and its

pattern. All the balances

associated with financial

statements must be

checked properly. At

last, the process of

accounting information

presentation and

interpretation must be

checked properly to

resolve the issue.

2

The substantive has

been considered for

this because a

misstatement

associated with the

discount has been

found herein (Cenit

Online, 2015). This

can directly affect

organizational

productivity and

profitability.

The misstatement

has to be resolved.

Most importantly,

the pattern or

specific reason for

issue must be found

to make adequate

financial records.

Misstatement can be

considered as a major

issue in any financial

books. According to the

American Institute of

Certified Public

Accountants (AICPA),

misstatement is a wrong

presentation of financial

activities. It can create

fraud or error in financial

statements (AICPA, 2018).

Hence, investigating the

discount misstatements

and its reason can help the

organization to mitigate

audit risks.

Accounts Payable Tests

Test Type of Test Key Assertion Reasonableness of

Conclusion

Additional Audit

Procedures

1

The test of control

has been selected for

this test because

material-related

errors have been

found (Cenit Online,

2015). The company

needs to fix it in

exchange for a

proper payable

account.

The material errors

have to be

resolved. It will

further reduce the

audit risks at the

end of the year.

The material error can be

considered as one of the

common issues in

accounting. It creates a

major ambiguity or

omission in the financial

books, which can create

major audit risk. For this

reason, resolving

materialistic error can

assist the organization in

creating feasible

accounting books.

Furthermore, the reliability

of financial information

has been increased by

diminishing material error

(The Institute Of Company

Secretaries of India, 2014).

The internal auditors

must conduct additional

audit activities to

develop the recent

situation. In the initial

stage, they must test all

the transactions

associated with the 15

suppliers to find the

material error and its

pattern. All the balances

associated with financial

statements must be

checked properly. At

last, the process of

accounting information

presentation and

interpretation must be

checked properly to

resolve the issue.

2

The substantive has

been considered for

this because a

misstatement

associated with the

discount has been

found herein (Cenit

Online, 2015). This

can directly affect

organizational

productivity and

profitability.

The misstatement

has to be resolved.

Most importantly,

the pattern or

specific reason for

issue must be found

to make adequate

financial records.

Misstatement can be

considered as a major

issue in any financial

books. According to the

American Institute of

Certified Public

Accountants (AICPA),

misstatement is a wrong

presentation of financial

activities. It can create

fraud or error in financial

statements (AICPA, 2018).

Hence, investigating the

discount misstatements

and its reason can help the

organization to mitigate

audit risks.

9AUDITING & ASSURANCE

Key Assertion at Risk

Overtime in Pellegrino Shores

Overtime payment activity within SBF can create various risks within the company. In

the initial stage, both unskilled and skilled employees will take the earning opportunity, wherein

the recruitment of the new talent can be reduced. Hence, the growth of the organization may

slow down. However, an employee needs proper skills to conduct overtime works because it

needs physical as well as mental ability. For this reason, unskilled or low skilled employees may

feel exploited within the organization. It can be considered as one of the major issues because it

reduces the service quality of the organization, which can harm the consumer and employee

satisfaction to a large extent. Change in pay legislation in the country can badly affect the

overtime workers and their payments. In addition, the organizational policy can change, which

further creates major issues in the payment system for the overtime workers (Oaxaca, 2014).

Most importantly, the motivation of the employees can affect badly due to the mentioned reason.

Hence, SBF needs to take adequate internal control process to assess and resolve overtime

payment issues. Hence, two processes of control has been discussed below i.e. Preventative

Internal Control and Detective Internal Control. It can thus, resolve the issues associated with the

payment of overtime workers.

Preventative Internal Control

Preventive control can also be considered as one of the effective control it can help to

assess undesirable events being conducted in future. A proper strategy and plan have been

created for future risk. It mainly helps to handle the unexpected future phenomenon associated

with the business operation. In relation to the SBF, the key authorities of the organization must

assume future events such as financial crisis, organizational loss and government legislation

Key Assertion at Risk

Overtime in Pellegrino Shores

Overtime payment activity within SBF can create various risks within the company. In

the initial stage, both unskilled and skilled employees will take the earning opportunity, wherein

the recruitment of the new talent can be reduced. Hence, the growth of the organization may

slow down. However, an employee needs proper skills to conduct overtime works because it

needs physical as well as mental ability. For this reason, unskilled or low skilled employees may

feel exploited within the organization. It can be considered as one of the major issues because it

reduces the service quality of the organization, which can harm the consumer and employee

satisfaction to a large extent. Change in pay legislation in the country can badly affect the

overtime workers and their payments. In addition, the organizational policy can change, which

further creates major issues in the payment system for the overtime workers (Oaxaca, 2014).

Most importantly, the motivation of the employees can affect badly due to the mentioned reason.

Hence, SBF needs to take adequate internal control process to assess and resolve overtime

payment issues. Hence, two processes of control has been discussed below i.e. Preventative

Internal Control and Detective Internal Control. It can thus, resolve the issues associated with the

payment of overtime workers.

Preventative Internal Control

Preventive control can also be considered as one of the effective control it can help to

assess undesirable events being conducted in future. A proper strategy and plan have been

created for future risk. It mainly helps to handle the unexpected future phenomenon associated

with the business operation. In relation to the SBF, the key authorities of the organization must

assume future events such as financial crisis, organizational loss and government legislation

10AUDITING & ASSURANCE

among others. Making a proper strategy for future events can help the organization to take an

adequate decision in case the event occurs. Hence, change in overtime payment policy and its

effect must be assumed. The current decision, as well as pay structure, must be developed

through future events. Using this internal control, a successful payment system for the overtime

workers can possible be established. It will thus lead the organization towards attaining success

in its existing international market (Savannahstate, 2011).

Detective Internal Control

Detective internal control is another process, which can help in assessing and resolving

the future acts associated with the documents and activities. It further helps to measure the

variance of work activities and lead the managers towards reviewing as well as analyzing the

documents along with the organizational inventories so as to make a proper strategy for future

activities. Auditing is one of the major aspects of this control and its process. In relation to SBF,

the key associates must create a proper budget for the overtime payment. During the overtime

activities, they can easily measure the cost condition, which can help them to make the required

decision to mitigate upcoming risk. This detection can help the organization to prevent future

losses associated with the overtime pay. In addition, the financial books can also be audited

properly through this control, wherein SBF can implement effective overtime payment system

for the employees (Savannahstate, 2011).

among others. Making a proper strategy for future events can help the organization to take an

adequate decision in case the event occurs. Hence, change in overtime payment policy and its

effect must be assumed. The current decision, as well as pay structure, must be developed

through future events. Using this internal control, a successful payment system for the overtime

workers can possible be established. It will thus lead the organization towards attaining success

in its existing international market (Savannahstate, 2011).

Detective Internal Control

Detective internal control is another process, which can help in assessing and resolving

the future acts associated with the documents and activities. It further helps to measure the

variance of work activities and lead the managers towards reviewing as well as analyzing the

documents along with the organizational inventories so as to make a proper strategy for future

activities. Auditing is one of the major aspects of this control and its process. In relation to SBF,

the key associates must create a proper budget for the overtime payment. During the overtime

activities, they can easily measure the cost condition, which can help them to make the required

decision to mitigate upcoming risk. This detection can help the organization to prevent future

losses associated with the overtime pay. In addition, the financial books can also be audited

properly through this control, wherein SBF can implement effective overtime payment system

for the employees (Savannahstate, 2011).

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

11AUDITING & ASSURANCE

References

AICPA. (2018). Evaluation of misstatements identified during the audit. AU-C Section 450, 375-

383.

Bunget, O. C. & Dumitrescu, A.C. (2009). Detecting and reporting the frauds and errors by the

auditor. Annales Universitatis Apulensis Series Oeconomica, 11(1), 117-125.

Cenit Online. (2015). Topic 34: substantive audit procedures – inventory. CPA P1 Auditing, 1-

10.

Dallas, S. (2011). The impact and reality of fraud auditing evolution of auditing: how the

recession is changing the industry. ACFE, 1-16.

Federal Reserve Banks. (2016). Faster payments effectiveness criteria. Faster Payments

Effectiveness Criteria–Final Version, 1-31.

Ftms. (2013). Audit risk and business risk. Session 6, 1-5.

KPMG AG. (2019). 20 key risks to consider by Internal Audit before 2020. Are you aware of the

risks concerning Internal Audit today and in the near future?, 1-27.

KPMG LLP. (2014). Nottingham city homes. Audit Strategy and Planning Memorandum, 2-12.

Ncert, (2019). Cash Flow Statement. Retrieved September 16, 2019, from

http://ncert.nic.in/textbook/pdf/leac206.pdf

Nikolovskia , P., Zdravkoskib, I., Menkinoskic, G., Dičevskad, S., & Karadјova, V. (2016). The

concept of audit risk. International Journal of Sciences: Basic and Applied Research,

27(1), 22-31.

Nos. (2008). Ledger. Module - 1 Notes Ledger Basic Accounting, 100-118.

References

AICPA. (2018). Evaluation of misstatements identified during the audit. AU-C Section 450, 375-

383.

Bunget, O. C. & Dumitrescu, A.C. (2009). Detecting and reporting the frauds and errors by the

auditor. Annales Universitatis Apulensis Series Oeconomica, 11(1), 117-125.

Cenit Online. (2015). Topic 34: substantive audit procedures – inventory. CPA P1 Auditing, 1-

10.

Dallas, S. (2011). The impact and reality of fraud auditing evolution of auditing: how the

recession is changing the industry. ACFE, 1-16.

Federal Reserve Banks. (2016). Faster payments effectiveness criteria. Faster Payments

Effectiveness Criteria–Final Version, 1-31.

Ftms. (2013). Audit risk and business risk. Session 6, 1-5.

KPMG AG. (2019). 20 key risks to consider by Internal Audit before 2020. Are you aware of the

risks concerning Internal Audit today and in the near future?, 1-27.

KPMG LLP. (2014). Nottingham city homes. Audit Strategy and Planning Memorandum, 2-12.

Ncert, (2019). Cash Flow Statement. Retrieved September 16, 2019, from

http://ncert.nic.in/textbook/pdf/leac206.pdf

Nikolovskia , P., Zdravkoskib, I., Menkinoskic, G., Dičevskad, S., & Karadјova, V. (2016). The

concept of audit risk. International Journal of Sciences: Basic and Applied Research,

27(1), 22-31.

Nos. (2008). Ledger. Module - 1 Notes Ledger Basic Accounting, 100-118.

12AUDITING & ASSURANCE

Oaxaca, R.L. (2014). The effect of overtime regulations on employment There is no evidence

that being strict with overtime hours and pay boosts employment—it could even lower it.

University of Arizona, 1-10.

PCAOB. (2017). Auditing standards of the public company accounting oversight board. Auditing

Standards, 4-724.

Savannahstate. (2011). Understanding internal controls. A Reference Guide for Managing

University Business Practices, 1-22.

Schultz, M. & Doerr, J. (2015). 5 keys to maximizing sales with existing accounts. RAIN Group,

1-20.

The Institute Of Company Secretaries of India. (2014). Fundamentals of accounting and

auditing. Foundation Programme, 3-361.

Worldbank. (2002). Good practice guide audit strategy. Government Internal Audit Standards, 3-

25.

Oaxaca, R.L. (2014). The effect of overtime regulations on employment There is no evidence

that being strict with overtime hours and pay boosts employment—it could even lower it.

University of Arizona, 1-10.

PCAOB. (2017). Auditing standards of the public company accounting oversight board. Auditing

Standards, 4-724.

Savannahstate. (2011). Understanding internal controls. A Reference Guide for Managing

University Business Practices, 1-22.

Schultz, M. & Doerr, J. (2015). 5 keys to maximizing sales with existing accounts. RAIN Group,

1-20.

The Institute Of Company Secretaries of India. (2014). Fundamentals of accounting and

auditing. Foundation Programme, 3-361.

Worldbank. (2002). Good practice guide audit strategy. Government Internal Audit Standards, 3-

25.

13AUDITING & ASSURANCE

Bibliography

AICPA. (2013). Performing audit procedures in response to assessed risks and evaluating the

audit evidence obtained. AU Section 318, 1781- 1803.

Eilifsen, A. & Messier, W.F.(2015). Materiality guidance of the major public accounting firms. A

Journal of Practice & Theory, 34(2), 3–26.

ICAI. (2016). Financial accounting. The Institute of Cost Accountants of India, 1.1-12.59.

Bibliography

AICPA. (2013). Performing audit procedures in response to assessed risks and evaluating the

audit evidence obtained. AU Section 318, 1781- 1803.

Eilifsen, A. & Messier, W.F.(2015). Materiality guidance of the major public accounting firms. A

Journal of Practice & Theory, 34(2), 3–26.

ICAI. (2016). Financial accounting. The Institute of Cost Accountants of India, 1.1-12.59.

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.