AMP Limited Audit Report Analysis

VerifiedAdded on 2020/11/23

|13

|3394

|249

Report

AI Summary

This assignment presents an audit report for AMP Limited. The report analyzes various aspects crucial to the organization's operations, including auditor independence, non-audit services, key audit matters with procedures, and the type of auditor's opinion provided. It also highlights the responsibilities of directors and auditors, addressing missing materiality information. The analysis demonstrates the significance of audits in evaluating an organization's financial position.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Auditing , Assurance

and Compliance

and Compliance

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

EXECUTIVE SUMMARY

The assignment is about the audit, assurance and compliance. This report is consisted of

auditing of the AMP limited company. Report includes the various aspects of auditor reporting

which are beneficial for the organization in identifying the position of the company. The report

includes audit declared that with respect to the Corporation Act 2001 with relation to the audit

the organizations has fulfilled all the independence requirements of the auditors without any

infringement of laws. The directors of the organization were satisfied that the auditors fulfilled

all the conditions of non audit services with the general standards if independence for auditors

obligatory by the Corporations Act, 2011. In accordance with the auditors independence

requirements of the corporation act 2001 auditors are the independence of group. In report it is

clearly found that auditors has attendant financial statements of AMP limited which was

consisted of balance sheet as of December 31, 2017 and all the financial statements of income ,

cash flows and related notes to the financial statements. The directors of the organization is liable

for preparing the financial report which shows true and fair value according to the Australian

Accounting Standards and the Corporation Act 2001. By analysing the report it is found that

the organization has not implemented customers social responsibilities. Therefore, it can be

concluded that audit plays an important role in assessing position of the company.

The assignment is about the audit, assurance and compliance. This report is consisted of

auditing of the AMP limited company. Report includes the various aspects of auditor reporting

which are beneficial for the organization in identifying the position of the company. The report

includes audit declared that with respect to the Corporation Act 2001 with relation to the audit

the organizations has fulfilled all the independence requirements of the auditors without any

infringement of laws. The directors of the organization were satisfied that the auditors fulfilled

all the conditions of non audit services with the general standards if independence for auditors

obligatory by the Corporations Act, 2011. In accordance with the auditors independence

requirements of the corporation act 2001 auditors are the independence of group. In report it is

clearly found that auditors has attendant financial statements of AMP limited which was

consisted of balance sheet as of December 31, 2017 and all the financial statements of income ,

cash flows and related notes to the financial statements. The directors of the organization is liable

for preparing the financial report which shows true and fair value according to the Australian

Accounting Standards and the Corporation Act 2001. By analysing the report it is found that

the organization has not implemented customers social responsibilities. Therefore, it can be

concluded that audit plays an important role in assessing position of the company.

Table of Contents

INTRODUCTION...........................................................................................................................5

A. Has auditor has compliance with independence requirements...............................................5

B.If there were non-audit services provided, what was the nature of such services...................5

C. Is there is an audit committee members in the AMP limited. ...............................................6

D.What type of Audit Opinion was expressed............................................................................6

E. Key audit matters of AMP limited..........................................................................................7

F. How directors and management responsibilities differ from auditors responsibilities. .......10

G. Were there any material subsequent events ........................................................................10

H. Recommending the effectiveness of materiality done by the auditors.................................10

I. Consider whether there is any material information which could be missing, under-reported

...................................................................................................................................................11

J. Providing an analysis of the Auditor’s remuneration in a table with prior year comparisons.

Include percentage changes and explanations of the remuneration..........................................11

CONCLUSION .............................................................................................................................11

REFERENCES..............................................................................................................................13

INTRODUCTION...........................................................................................................................5

A. Has auditor has compliance with independence requirements...............................................5

B.If there were non-audit services provided, what was the nature of such services...................5

C. Is there is an audit committee members in the AMP limited. ...............................................6

D.What type of Audit Opinion was expressed............................................................................6

E. Key audit matters of AMP limited..........................................................................................7

F. How directors and management responsibilities differ from auditors responsibilities. .......10

G. Were there any material subsequent events ........................................................................10

H. Recommending the effectiveness of materiality done by the auditors.................................10

I. Consider whether there is any material information which could be missing, under-reported

...................................................................................................................................................11

J. Providing an analysis of the Auditor’s remuneration in a table with prior year comparisons.

Include percentage changes and explanations of the remuneration..........................................11

CONCLUSION .............................................................................................................................11

REFERENCES..............................................................................................................................13

INTRODUCTION

The assignment is about the auditing, assurance and compliance of the AMP Limited an

Australian company. It is a organization which deals with the financial. This organization serves

the superannuation, investment products , financial advice and banking products including loan

and saving amount. This research has focused mainly the audit of the company. Audit plays an

important role in analyzing the financial position of the AMP limited. The report will provide the

information about auditors independence requirements. The assignment will present the non

auditors services and their nature. It will also present the various members of committee. The

assignment will provide the deep insight of various key audit matters and their procedures.

Later, the report will provide the information auditor's responsibilities with comparison to

management and directors.

A. Has auditor has compliance with independence requirements

The auditors for the AMP Limited has compliance with independence requirements for

the financial year 31st December 2017. In his audit he has declared that with respect to the

Corporation Act 2001 with relation to the audit the organizations has fulfilled all the

independence requirements of the auditors without any infringement of laws. He has also

declared that no violation of any relevant code of professional conduct in relation to the audit.

B.If there were non-audit services provided, what was the nature of such services

During the year ended 31st December 2017 the audit committee has reviewed the details

of the amount which paid or yet to paid is given to the AMP group for the non audit services.

The directors of the organization were satisfied that the auditors fulfilled all the conditions of

non audit services with the general standards if independence for auditors obligatory by the

Corporations Act, 2011(Chan and Vasarhelyi, 2018).

Nature of non audit services

The chief financial officer , or his nominated delegate, or the chairman of the Audit

Committee were approved the all non audit assignments.

There are some Non Audit assignments which were specifically excluded by the charter

of audit independence of AMP were carried out.

The fees which is offered for non – audit services is 12% of total fees, decreasing 9 % on

prior year.

The assignment is about the auditing, assurance and compliance of the AMP Limited an

Australian company. It is a organization which deals with the financial. This organization serves

the superannuation, investment products , financial advice and banking products including loan

and saving amount. This research has focused mainly the audit of the company. Audit plays an

important role in analyzing the financial position of the AMP limited. The report will provide the

information about auditors independence requirements. The assignment will present the non

auditors services and their nature. It will also present the various members of committee. The

assignment will provide the deep insight of various key audit matters and their procedures.

Later, the report will provide the information auditor's responsibilities with comparison to

management and directors.

A. Has auditor has compliance with independence requirements

The auditors for the AMP Limited has compliance with independence requirements for

the financial year 31st December 2017. In his audit he has declared that with respect to the

Corporation Act 2001 with relation to the audit the organizations has fulfilled all the

independence requirements of the auditors without any infringement of laws. He has also

declared that no violation of any relevant code of professional conduct in relation to the audit.

B.If there were non-audit services provided, what was the nature of such services

During the year ended 31st December 2017 the audit committee has reviewed the details

of the amount which paid or yet to paid is given to the AMP group for the non audit services.

The directors of the organization were satisfied that the auditors fulfilled all the conditions of

non audit services with the general standards if independence for auditors obligatory by the

Corporations Act, 2011(Chan and Vasarhelyi, 2018).

Nature of non audit services

The chief financial officer , or his nominated delegate, or the chairman of the Audit

Committee were approved the all non audit assignments.

There are some Non Audit assignments which were specifically excluded by the charter

of audit independence of AMP were carried out.

The fees which is offered for non – audit services is 12% of total fees, decreasing 9 % on

prior year.

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

C. Is there is an audit committee members in the AMP limited.

Audit committee members

Patricia (Patty) Akopiantz

AMP limited has appointed her in board and people remuneration committee in march

2011. she became chairman of that committee. She has been appointed as a director AMP bank

limited and later she became a audit committee member.

Andrews Harmos

He was appointed to the AMP limited board and it became member of the Audit

Committee. Andrews Harmos became the chairman of the audit committees in both the

organization in may 2016 .

Holly Kramer

In October 2015 Holly Kramer was appointed to the AMP limited board and later he was

appointed as a member of audit Committee in November 2015 (Marques, 2017).

Geoff Roberts : He was appointed to the amp limited as a chairman of the audit committee in

July 2016.

Therefore, the integrity of financial statements is the responsibility of the audit

committee of AMP limited. There are several more functions of the like supporting the decision

of the directors of internal audit and external auditor, and monitoring the performance ,

reviewing the effectiveness if AMP's risk management structure and satisfactory and

independence of the internal and external audit functions.

D.What type of Audit Opinion was expressed

Opinion

the financial reports of AMP limited and its subsidiaries has been audited by the auditors,

which is consisted of consolidated balance sheet , income statements, statements of

comprehensive income , the statement of changes in working capital, cash flow statements with

the summary of significant accounting policies and the directors declaration (Groomer and

Murthy, 2018).

The auditors opinion with respect to the financial report of the AMP Limited according to the

Corporation act 2001 includes-

Audit committee members

Patricia (Patty) Akopiantz

AMP limited has appointed her in board and people remuneration committee in march

2011. she became chairman of that committee. She has been appointed as a director AMP bank

limited and later she became a audit committee member.

Andrews Harmos

He was appointed to the AMP limited board and it became member of the Audit

Committee. Andrews Harmos became the chairman of the audit committees in both the

organization in may 2016 .

Holly Kramer

In October 2015 Holly Kramer was appointed to the AMP limited board and later he was

appointed as a member of audit Committee in November 2015 (Marques, 2017).

Geoff Roberts : He was appointed to the amp limited as a chairman of the audit committee in

July 2016.

Therefore, the integrity of financial statements is the responsibility of the audit

committee of AMP limited. There are several more functions of the like supporting the decision

of the directors of internal audit and external auditor, and monitoring the performance ,

reviewing the effectiveness if AMP's risk management structure and satisfactory and

independence of the internal and external audit functions.

D.What type of Audit Opinion was expressed

Opinion

the financial reports of AMP limited and its subsidiaries has been audited by the auditors,

which is consisted of consolidated balance sheet , income statements, statements of

comprehensive income , the statement of changes in working capital, cash flow statements with

the summary of significant accounting policies and the directors declaration (Groomer and

Murthy, 2018).

The auditors opinion with respect to the financial report of the AMP Limited according to the

Corporation act 2001 includes-

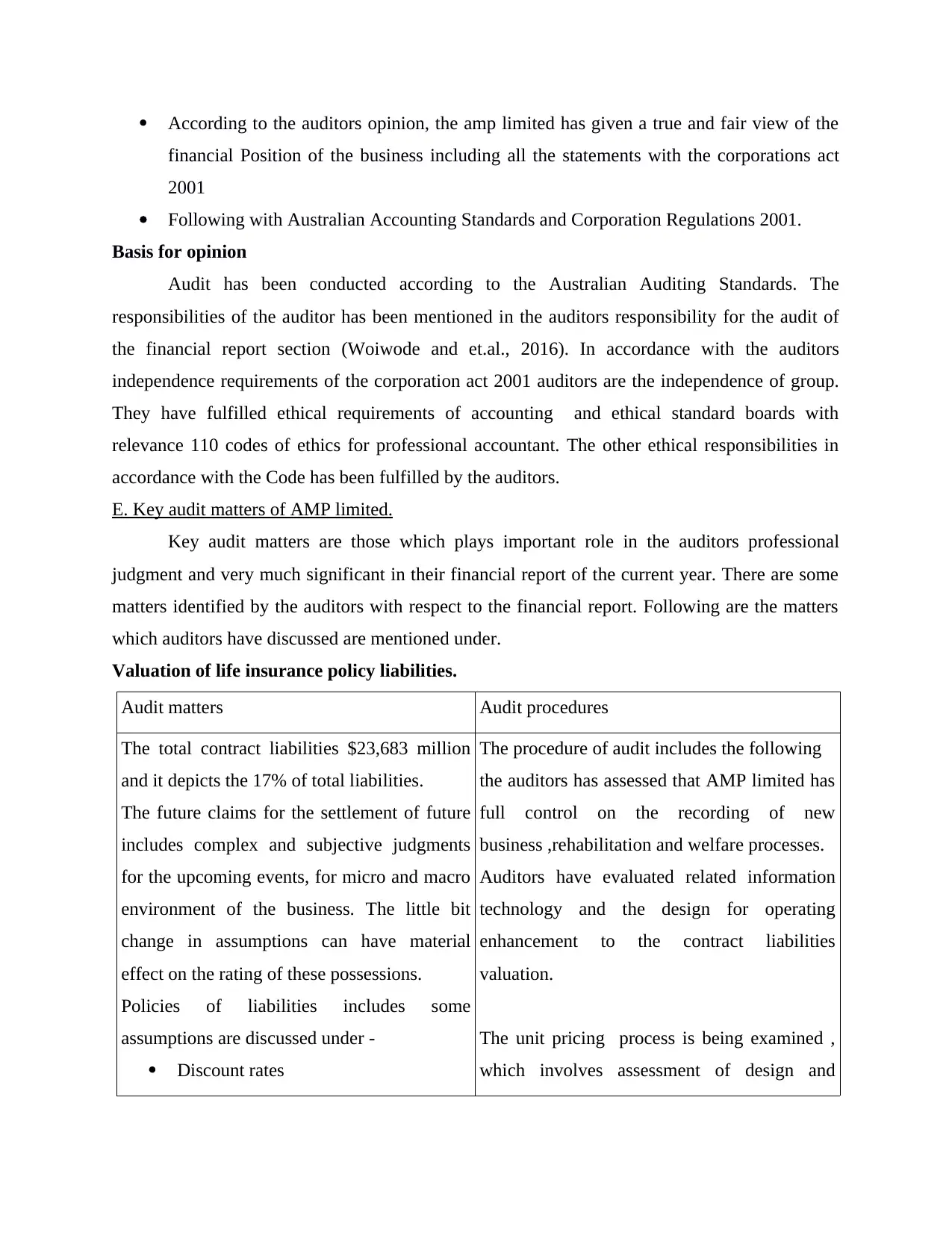

According to the auditors opinion, the amp limited has given a true and fair view of the

financial Position of the business including all the statements with the corporations act

2001

Following with Australian Accounting Standards and Corporation Regulations 2001.

Basis for opinion

Audit has been conducted according to the Australian Auditing Standards. The

responsibilities of the auditor has been mentioned in the auditors responsibility for the audit of

the financial report section (Woiwode and et.al., 2016). In accordance with the auditors

independence requirements of the corporation act 2001 auditors are the independence of group.

They have fulfilled ethical requirements of accounting and ethical standard boards with

relevance 110 codes of ethics for professional accountant. The other ethical responsibilities in

accordance with the Code has been fulfilled by the auditors.

E. Key audit matters of AMP limited.

Key audit matters are those which plays important role in the auditors professional

judgment and very much significant in their financial report of the current year. There are some

matters identified by the auditors with respect to the financial report. Following are the matters

which auditors have discussed are mentioned under.

Valuation of life insurance policy liabilities.

Audit matters Audit procedures

The total contract liabilities $23,683 million

and it depicts the 17% of total liabilities.

The future claims for the settlement of future

includes complex and subjective judgments

for the upcoming events, for micro and macro

environment of the business. The little bit

change in assumptions can have material

effect on the rating of these possessions.

Policies of liabilities includes some

assumptions are discussed under -

Discount rates

The procedure of audit includes the following

the auditors has assessed that AMP limited has

full control on the recording of new

business ,rehabilitation and welfare processes.

Auditors have evaluated related information

technology and the design for operating

enhancement to the contract liabilities

valuation.

The unit pricing process is being examined ,

which involves assessment of design and

financial Position of the business including all the statements with the corporations act

2001

Following with Australian Accounting Standards and Corporation Regulations 2001.

Basis for opinion

Audit has been conducted according to the Australian Auditing Standards. The

responsibilities of the auditor has been mentioned in the auditors responsibility for the audit of

the financial report section (Woiwode and et.al., 2016). In accordance with the auditors

independence requirements of the corporation act 2001 auditors are the independence of group.

They have fulfilled ethical requirements of accounting and ethical standard boards with

relevance 110 codes of ethics for professional accountant. The other ethical responsibilities in

accordance with the Code has been fulfilled by the auditors.

E. Key audit matters of AMP limited.

Key audit matters are those which plays important role in the auditors professional

judgment and very much significant in their financial report of the current year. There are some

matters identified by the auditors with respect to the financial report. Following are the matters

which auditors have discussed are mentioned under.

Valuation of life insurance policy liabilities.

Audit matters Audit procedures

The total contract liabilities $23,683 million

and it depicts the 17% of total liabilities.

The future claims for the settlement of future

includes complex and subjective judgments

for the upcoming events, for micro and macro

environment of the business. The little bit

change in assumptions can have material

effect on the rating of these possessions.

Policies of liabilities includes some

assumptions are discussed under -

Discount rates

The procedure of audit includes the following

the auditors has assessed that AMP limited has

full control on the recording of new

business ,rehabilitation and welfare processes.

Auditors have evaluated related information

technology and the design for operating

enhancement to the contract liabilities

valuation.

The unit pricing process is being examined ,

which involves assessment of design and

inflation and indexation

Forecast lapse rates, particularly for

wealth protection book of business

future maintenance and investment

expenses Taxation

Surrender values Mortality and

morbidity

testing controls associated with the process.

The recalculation of the total investment

contract liabilities have been done with the

systems activity process , consistent the

investments declaration possession to the fair

value of inherent assets.

Valuation of complex and non- liquid financial statements

Key matters Key procedures

The 92 % of total assets has been represented

and the investments in financial assets are

$136,675 in total.

The requirements by accounting standards has

been fulfilled by categorizing the 3 levels of

note 2.5 , the portfolio in accordance with the

fair value of heir achy. The best estimates of

fair value the assets are exercised by the AMP

group .

For all level the valuation specialist and model

ling methodologies were used in prevailing the

key market conditions.

Assets are recorded within controlled unit

trusts and there were not the necessities of

specific local reporting. The auditors have don

the valuation according to the sample provided

by external investment manager.

Recoverability of goodwill and intangible assets

Audit matters Audit procedures

The 2 % of total assets were represented. And

goodwill and intangible assets were $3,218

million.

The goodwill of AMP limited has been

recognized by representing the fair value of

assets acquired. The goodwill has been

allocated to the applicable cash generating

units.

The requirement of Australian accounting

standards possess the impairment assessment

purposes by the AMP Limited.

Discount rate has been used in the assessment

of methodologies and assumptions by

including as the rate of market benchmarks.

The sensitivity analysis on key assumptions

has been informed by including the

Forecast lapse rates, particularly for

wealth protection book of business

future maintenance and investment

expenses Taxation

Surrender values Mortality and

morbidity

testing controls associated with the process.

The recalculation of the total investment

contract liabilities have been done with the

systems activity process , consistent the

investments declaration possession to the fair

value of inherent assets.

Valuation of complex and non- liquid financial statements

Key matters Key procedures

The 92 % of total assets has been represented

and the investments in financial assets are

$136,675 in total.

The requirements by accounting standards has

been fulfilled by categorizing the 3 levels of

note 2.5 , the portfolio in accordance with the

fair value of heir achy. The best estimates of

fair value the assets are exercised by the AMP

group .

For all level the valuation specialist and model

ling methodologies were used in prevailing the

key market conditions.

Assets are recorded within controlled unit

trusts and there were not the necessities of

specific local reporting. The auditors have don

the valuation according to the sample provided

by external investment manager.

Recoverability of goodwill and intangible assets

Audit matters Audit procedures

The 2 % of total assets were represented. And

goodwill and intangible assets were $3,218

million.

The goodwill of AMP limited has been

recognized by representing the fair value of

assets acquired. The goodwill has been

allocated to the applicable cash generating

units.

The requirement of Australian accounting

standards possess the impairment assessment

purposes by the AMP Limited.

Discount rate has been used in the assessment

of methodologies and assumptions by

including as the rate of market benchmarks.

The sensitivity analysis on key assumptions

has been informed by including the

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

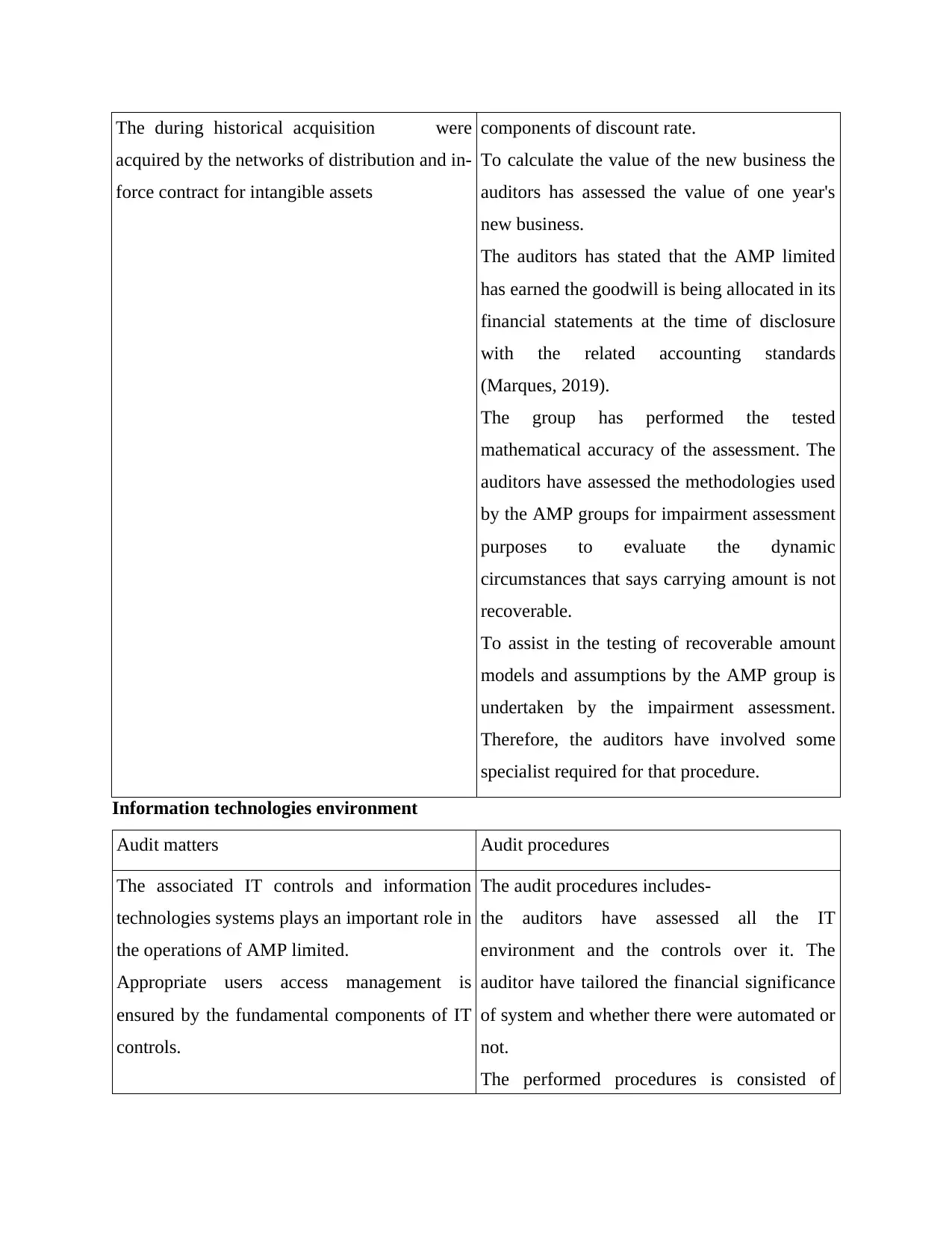

The during historical acquisition were

acquired by the networks of distribution and in-

force contract for intangible assets

components of discount rate.

To calculate the value of the new business the

auditors has assessed the value of one year's

new business.

The auditors has stated that the AMP limited

has earned the goodwill is being allocated in its

financial statements at the time of disclosure

with the related accounting standards

(Marques, 2019).

The group has performed the tested

mathematical accuracy of the assessment. The

auditors have assessed the methodologies used

by the AMP groups for impairment assessment

purposes to evaluate the dynamic

circumstances that says carrying amount is not

recoverable.

To assist in the testing of recoverable amount

models and assumptions by the AMP group is

undertaken by the impairment assessment.

Therefore, the auditors have involved some

specialist required for that procedure.

Information technologies environment

Audit matters Audit procedures

The associated IT controls and information

technologies systems plays an important role in

the operations of AMP limited.

Appropriate users access management is

ensured by the fundamental components of IT

controls.

The audit procedures includes-

the auditors have assessed all the IT

environment and the controls over it. The

auditor have tailored the financial significance

of system and whether there were automated or

not.

The performed procedures is consisted of

acquired by the networks of distribution and in-

force contract for intangible assets

components of discount rate.

To calculate the value of the new business the

auditors has assessed the value of one year's

new business.

The auditors has stated that the AMP limited

has earned the goodwill is being allocated in its

financial statements at the time of disclosure

with the related accounting standards

(Marques, 2019).

The group has performed the tested

mathematical accuracy of the assessment. The

auditors have assessed the methodologies used

by the AMP groups for impairment assessment

purposes to evaluate the dynamic

circumstances that says carrying amount is not

recoverable.

To assist in the testing of recoverable amount

models and assumptions by the AMP group is

undertaken by the impairment assessment.

Therefore, the auditors have involved some

specialist required for that procedure.

Information technologies environment

Audit matters Audit procedures

The associated IT controls and information

technologies systems plays an important role in

the operations of AMP limited.

Appropriate users access management is

ensured by the fundamental components of IT

controls.

The audit procedures includes-

the auditors have assessed all the IT

environment and the controls over it. The

auditor have tailored the financial significance

of system and whether there were automated or

not.

The performed procedures is consisted of

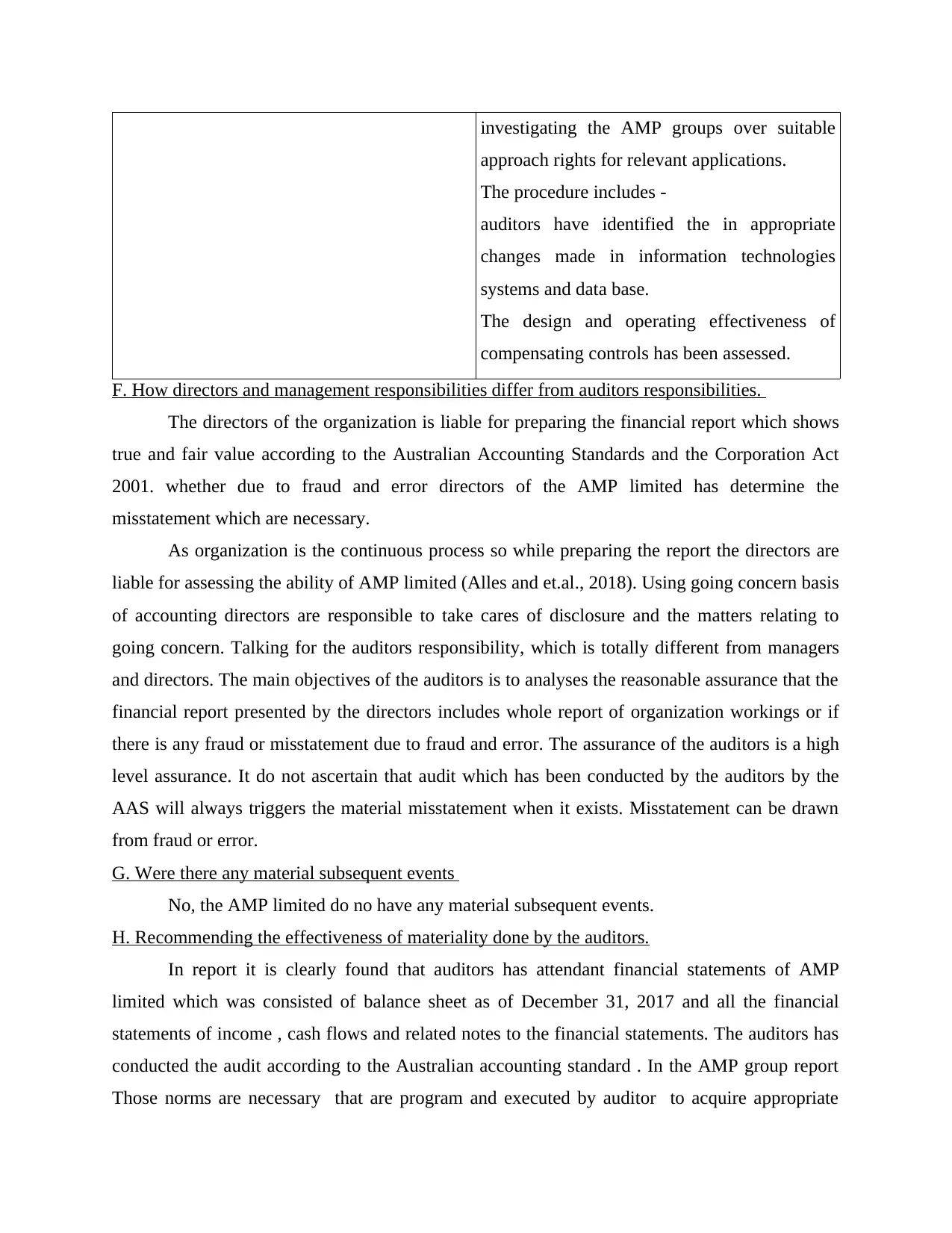

investigating the AMP groups over suitable

approach rights for relevant applications.

The procedure includes -

auditors have identified the in appropriate

changes made in information technologies

systems and data base.

The design and operating effectiveness of

compensating controls has been assessed.

F. How directors and management responsibilities differ from auditors responsibilities.

The directors of the organization is liable for preparing the financial report which shows

true and fair value according to the Australian Accounting Standards and the Corporation Act

2001. whether due to fraud and error directors of the AMP limited has determine the

misstatement which are necessary.

As organization is the continuous process so while preparing the report the directors are

liable for assessing the ability of AMP limited (Alles and et.al., 2018). Using going concern basis

of accounting directors are responsible to take cares of disclosure and the matters relating to

going concern. Talking for the auditors responsibility, which is totally different from managers

and directors. The main objectives of the auditors is to analyses the reasonable assurance that the

financial report presented by the directors includes whole report of organization workings or if

there is any fraud or misstatement due to fraud and error. The assurance of the auditors is a high

level assurance. It do not ascertain that audit which has been conducted by the auditors by the

AAS will always triggers the material misstatement when it exists. Misstatement can be drawn

from fraud or error.

G. Were there any material subsequent events

No, the AMP limited do no have any material subsequent events.

H. Recommending the effectiveness of materiality done by the auditors.

In report it is clearly found that auditors has attendant financial statements of AMP

limited which was consisted of balance sheet as of December 31, 2017 and all the financial

statements of income , cash flows and related notes to the financial statements. The auditors has

conducted the audit according to the Australian accounting standard . In the AMP group report

Those norms are necessary that are program and executed by auditor to acquire appropriate

approach rights for relevant applications.

The procedure includes -

auditors have identified the in appropriate

changes made in information technologies

systems and data base.

The design and operating effectiveness of

compensating controls has been assessed.

F. How directors and management responsibilities differ from auditors responsibilities.

The directors of the organization is liable for preparing the financial report which shows

true and fair value according to the Australian Accounting Standards and the Corporation Act

2001. whether due to fraud and error directors of the AMP limited has determine the

misstatement which are necessary.

As organization is the continuous process so while preparing the report the directors are

liable for assessing the ability of AMP limited (Alles and et.al., 2018). Using going concern basis

of accounting directors are responsible to take cares of disclosure and the matters relating to

going concern. Talking for the auditors responsibility, which is totally different from managers

and directors. The main objectives of the auditors is to analyses the reasonable assurance that the

financial report presented by the directors includes whole report of organization workings or if

there is any fraud or misstatement due to fraud and error. The assurance of the auditors is a high

level assurance. It do not ascertain that audit which has been conducted by the auditors by the

AAS will always triggers the material misstatement when it exists. Misstatement can be drawn

from fraud or error.

G. Were there any material subsequent events

No, the AMP limited do no have any material subsequent events.

H. Recommending the effectiveness of materiality done by the auditors.

In report it is clearly found that auditors has attendant financial statements of AMP

limited which was consisted of balance sheet as of December 31, 2017 and all the financial

statements of income , cash flows and related notes to the financial statements. The auditors has

conducted the audit according to the Australian accounting standard . In the AMP group report

Those norms are necessary that are program and executed by auditor to acquire appropriate

assurance about whether the financial statements are free of material misstatement. An audit

consisted of study, on a test basis on the grounds supporting of sum and disclosures in the

financial statements. Auditors have also includes evaluation the accounting principles utilized

and important calculation successfully created by management, or measure overall financial

statement presentation. Auditor has covered all the information of materiality very well in the

report

I. Consider whether there is any material information which could be missing, under-reported

The report has almost covered all the information which is mandatory. By analyzing the

report it is found that the organization has not implemented customers social responsibilities.

CSR is a internal organizational policy (Knechel and Salterio, 2016). CSR helps in changing the

business beliefs , practices and profits. In CSR company overtook the responsibilities for the

social and environmental impacts of businesses operations. The implementation of customers

social responsibility provide lots of benefits to the AMP Limited.

Following are the benefits of the implementation of CSR

It provide lots of benefits like improving the brand of company's.

It helps in engaging customers.

It helps the organization to stands out from the competitions.

It attracts more investors for the investments in business.

J. Providing an analysis of the Auditor’s remuneration in a table with prior year comparisons.

Include percentage changes and explanations of the remuneration

Particulars 2015 2016 % change 2017 % change

Total audit services fees(cons) 11761 6616 -0.44 6931 0.05

Total non audit services fees(cons) 3421 1693 -0.51 1599 -0.06

Total audit services fees (other

entities) 140 7041 49.29 7280 0.03

Total non audit services fees (other

entities) 0 396 0 305 -0.23

The above report is reflecting the remuneration report of past three years that are 2015 ,

2016 and 2017. It can be observed in the report that from 2016 to 2017 the auditors remuneration

has been decreased creased by 0.45 % in total audit service fees. In total non audit services the

consisted of study, on a test basis on the grounds supporting of sum and disclosures in the

financial statements. Auditors have also includes evaluation the accounting principles utilized

and important calculation successfully created by management, or measure overall financial

statement presentation. Auditor has covered all the information of materiality very well in the

report

I. Consider whether there is any material information which could be missing, under-reported

The report has almost covered all the information which is mandatory. By analyzing the

report it is found that the organization has not implemented customers social responsibilities.

CSR is a internal organizational policy (Knechel and Salterio, 2016). CSR helps in changing the

business beliefs , practices and profits. In CSR company overtook the responsibilities for the

social and environmental impacts of businesses operations. The implementation of customers

social responsibility provide lots of benefits to the AMP Limited.

Following are the benefits of the implementation of CSR

It provide lots of benefits like improving the brand of company's.

It helps in engaging customers.

It helps the organization to stands out from the competitions.

It attracts more investors for the investments in business.

J. Providing an analysis of the Auditor’s remuneration in a table with prior year comparisons.

Include percentage changes and explanations of the remuneration

Particulars 2015 2016 % change 2017 % change

Total audit services fees(cons) 11761 6616 -0.44 6931 0.05

Total non audit services fees(cons) 3421 1693 -0.51 1599 -0.06

Total audit services fees (other

entities) 140 7041 49.29 7280 0.03

Total non audit services fees (other

entities) 0 396 0 305 -0.23

The above report is reflecting the remuneration report of past three years that are 2015 ,

2016 and 2017. It can be observed in the report that from 2016 to 2017 the auditors remuneration

has been decreased creased by 0.45 % in total audit service fees. In total non audit services the

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

fees has been decreased from the year 2016 to 2017 by 49.26 % which is due to. In the total

audit fees for the other entities for the year 2016 to 2017 it has been increased by 0.03 % and in

non audit fees has also increased by decreased by 0.23%.

CONCLUSION

The above report is the audit report of the AMP Limited. This report makes the

involvement of the process and importance of auditing and compliance within company. For

every organization audit is very important task to be done periodically. The report is based on the

audit of the company which includes various aspects which are necessary for the organization to

be covered. The report has covered the complied independence requirements of the auditors ,

non audit services and its nature. Key audit matters of the organization's has been also discussed

with their procedure. The report has also provided the type of auditors opinion, with directors

and auditors responsibility. The report has covered missing materiality information. Therefore, it

can be concluded that audit plays an important role in assessing position of the company.

audit fees for the other entities for the year 2016 to 2017 it has been increased by 0.03 % and in

non audit fees has also increased by decreased by 0.23%.

CONCLUSION

The above report is the audit report of the AMP Limited. This report makes the

involvement of the process and importance of auditing and compliance within company. For

every organization audit is very important task to be done periodically. The report is based on the

audit of the company which includes various aspects which are necessary for the organization to

be covered. The report has covered the complied independence requirements of the auditors ,

non audit services and its nature. Key audit matters of the organization's has been also discussed

with their procedure. The report has also provided the type of auditors opinion, with directors

and auditors responsibility. The report has covered missing materiality information. Therefore, it

can be concluded that audit plays an important role in assessing position of the company.

REFERENCES

Books and Journals

Knechel, W.R. and Salterio, S.E., 2016. Auditing: Assurance and risk. Routledge.

Alles, M., Brennan, G., Kogan, A. and Vasarhelyi, M.A., 2018. Continuous monitoring of

business process controls: A pilot implementation of a continuous auditing system at

Siemens. In Continuous Auditing: Theory and Application (pp. 219-246). Emerald

Publishing Limited.

Marques, R.P.F., 2019. Continuous Assurance and the Use of Technology for Business

Compliance. In Advanced Methodologies and Technologies in Business Operations and

Management (pp. 429-441). IGI Global.

Woiwode, R. and et.al., 2016. Compliance of large feedyards in the northern high plains with the

Beef Quality Assurance Feedyard Assessment. The Professional Animal Scientist. 32(6).

pp.750-757.

Chan, D.Y. and Vasarhelyi, M.A., 2018. Innovation and practice of continuous auditing. In

Continuous Auditing: Theory and Application (pp. 271-283). Emerald Publishing Limited.

DeFond, M. and Zhang, J., 2014. A review of archival auditing research. Journal of

Accounting and Economics. 58(2-3). pp.275-326.

Groomer, S.M. and Murthy, U.S., 2018. Continuous auditing of database applications:

An embedded audit module approach. In Continuous Auditing: Theory and Application (pp. 105-

124). Emerald Publishing Limited.

Marques, R.P., 2017. Continuous assurance and business compliance in enterprise

information systems. In Enterprise information systems and the digitalization of business

functions (pp. 99-119). IGI Global.

ONLINE

. [Online]. Available through :<>.

. [Online]. Available through :<>.

. [Online]. Available through :<>.

. [Online]. Available through :<>.

Books and Journals

Knechel, W.R. and Salterio, S.E., 2016. Auditing: Assurance and risk. Routledge.

Alles, M., Brennan, G., Kogan, A. and Vasarhelyi, M.A., 2018. Continuous monitoring of

business process controls: A pilot implementation of a continuous auditing system at

Siemens. In Continuous Auditing: Theory and Application (pp. 219-246). Emerald

Publishing Limited.

Marques, R.P.F., 2019. Continuous Assurance and the Use of Technology for Business

Compliance. In Advanced Methodologies and Technologies in Business Operations and

Management (pp. 429-441). IGI Global.

Woiwode, R. and et.al., 2016. Compliance of large feedyards in the northern high plains with the

Beef Quality Assurance Feedyard Assessment. The Professional Animal Scientist. 32(6).

pp.750-757.

Chan, D.Y. and Vasarhelyi, M.A., 2018. Innovation and practice of continuous auditing. In

Continuous Auditing: Theory and Application (pp. 271-283). Emerald Publishing Limited.

DeFond, M. and Zhang, J., 2014. A review of archival auditing research. Journal of

Accounting and Economics. 58(2-3). pp.275-326.

Groomer, S.M. and Murthy, U.S., 2018. Continuous auditing of database applications:

An embedded audit module approach. In Continuous Auditing: Theory and Application (pp. 105-

124). Emerald Publishing Limited.

Marques, R.P., 2017. Continuous assurance and business compliance in enterprise

information systems. In Enterprise information systems and the digitalization of business

functions (pp. 99-119). IGI Global.

ONLINE

. [Online]. Available through :<>.

. [Online]. Available through :<>.

. [Online]. Available through :<>.

. [Online]. Available through :<>.

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.