PACC6002 - Auditing and Assurance: Analytical Procedures Report

VerifiedAdded on 2023/06/03

|11

|1615

|291

Report

AI Summary

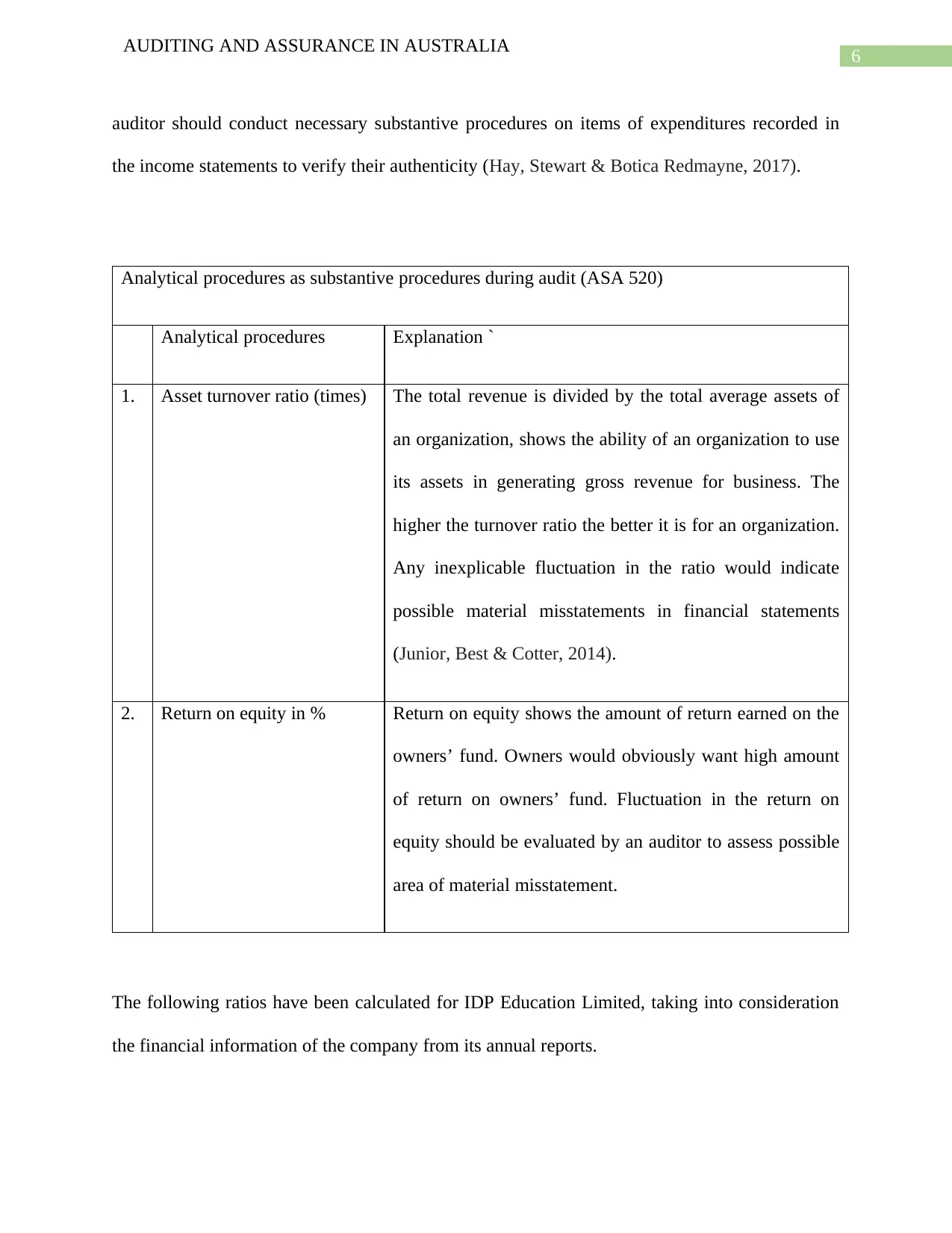

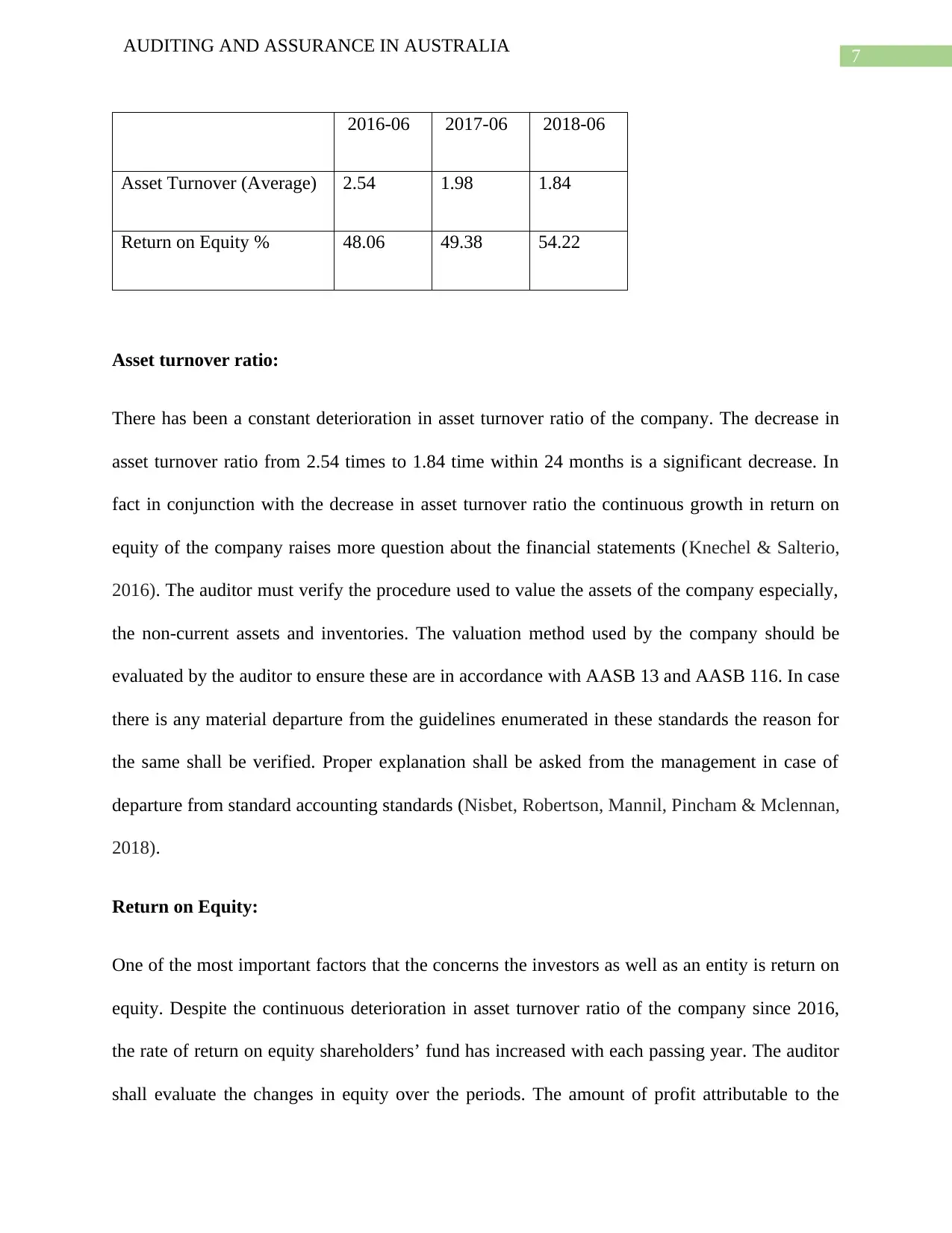

This report provides an in-depth analysis of analytical procedures in auditing and assurance, focusing on the application of ASA 315 (risk assessment procedures) and ASA 520 (substantive procedures). The report uses the financial statements of IDP Education Limited to illustrate how auditors utilize various analytical techniques, such as gross profit ratio, net profit ratio, asset turnover ratio, and return on equity, to identify potential areas of material misstatement. The analysis includes calculations and interpretations of these ratios over a three-year period, highlighting trends and fluctuations that warrant further investigation. The report emphasizes the importance of analytical procedures in both the risk assessment phase and the substantive testing phase of an audit, demonstrating how these procedures can help auditors gain a better understanding of a company's financial performance and identify potential areas of concern. The conclusion summarizes the findings and underscores the value of analytical procedures in forming an opinion on the fairness of financial statements.

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.