Auditing & Assurance: Review of International Insurance Inc.

VerifiedAdded on 2023/06/15

|7

|1480

|248

Report

AI Summary

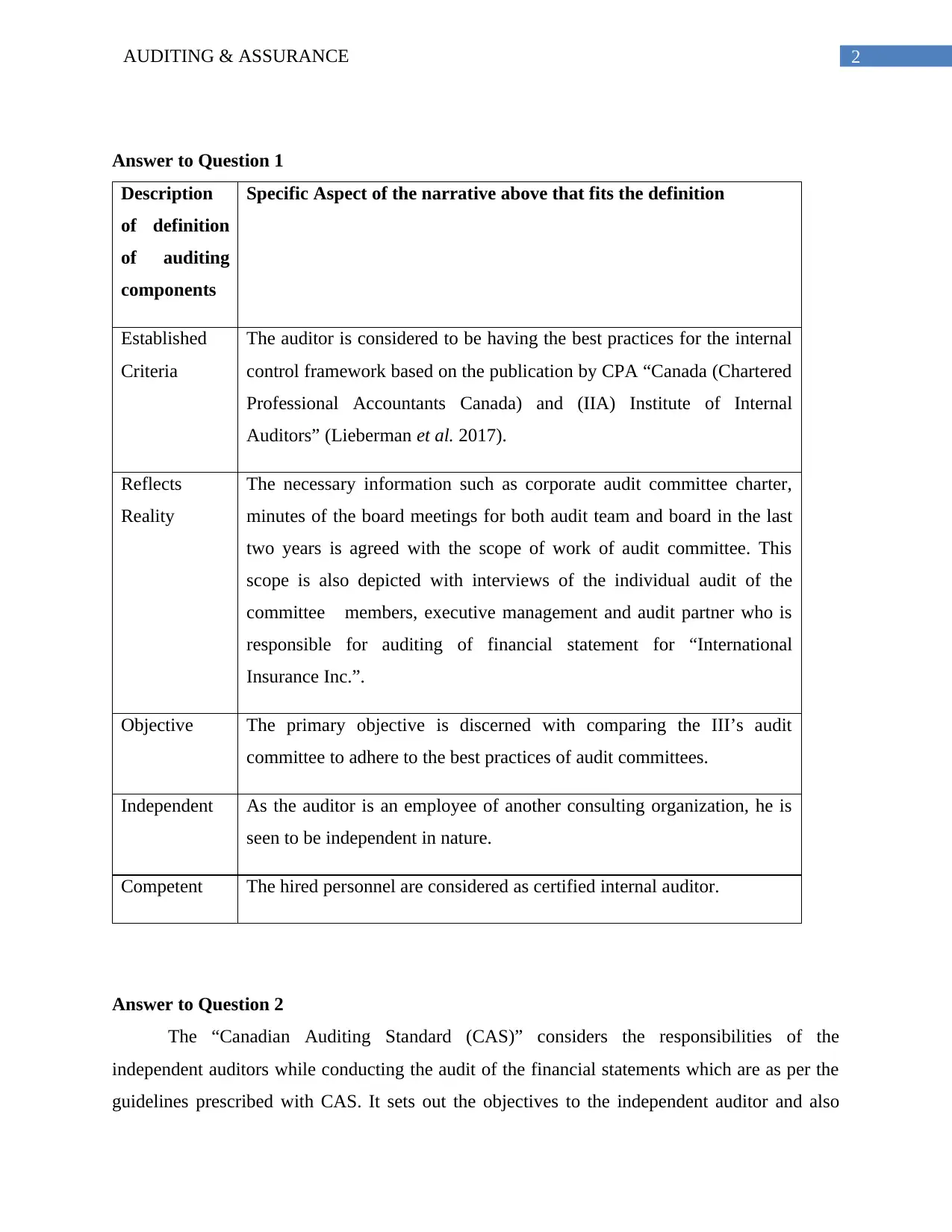

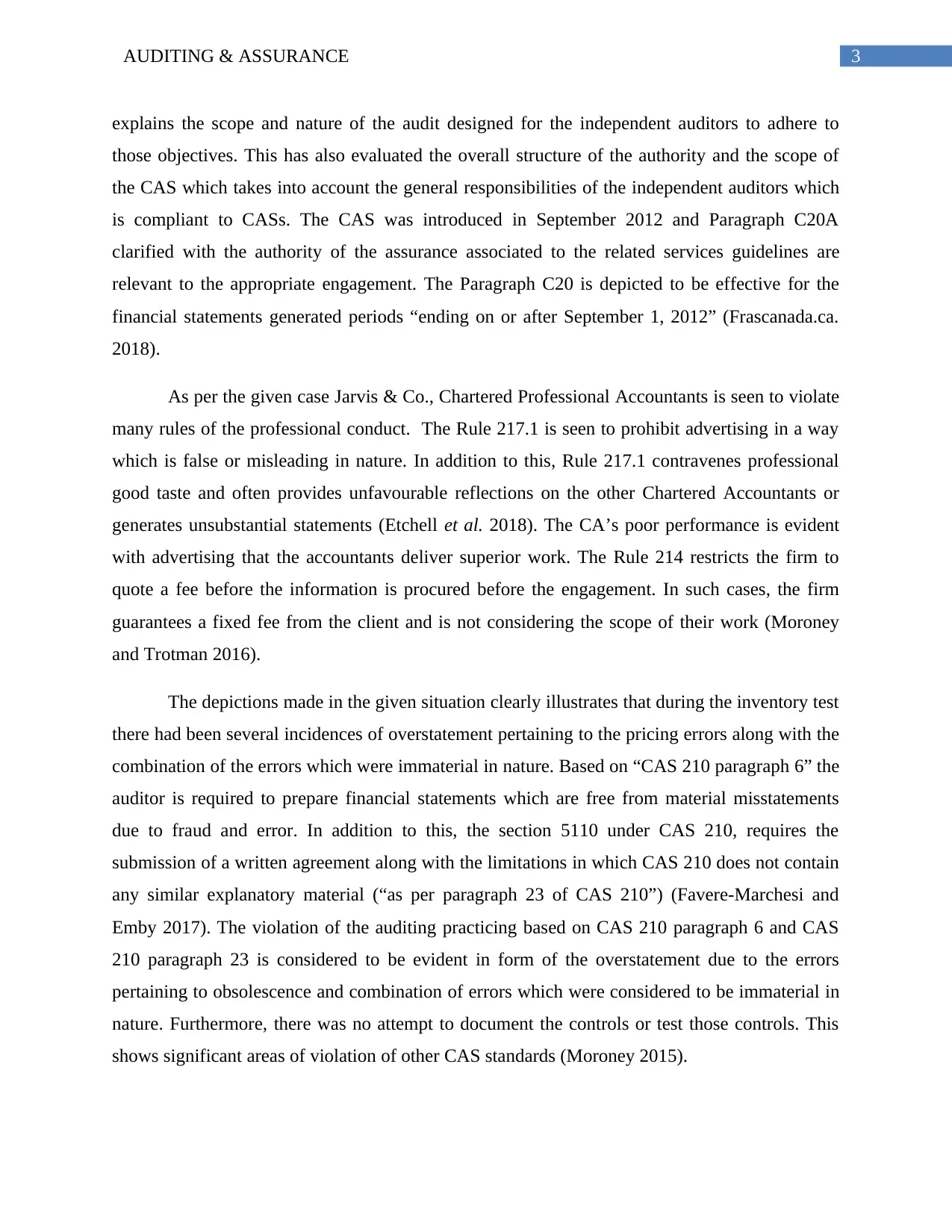

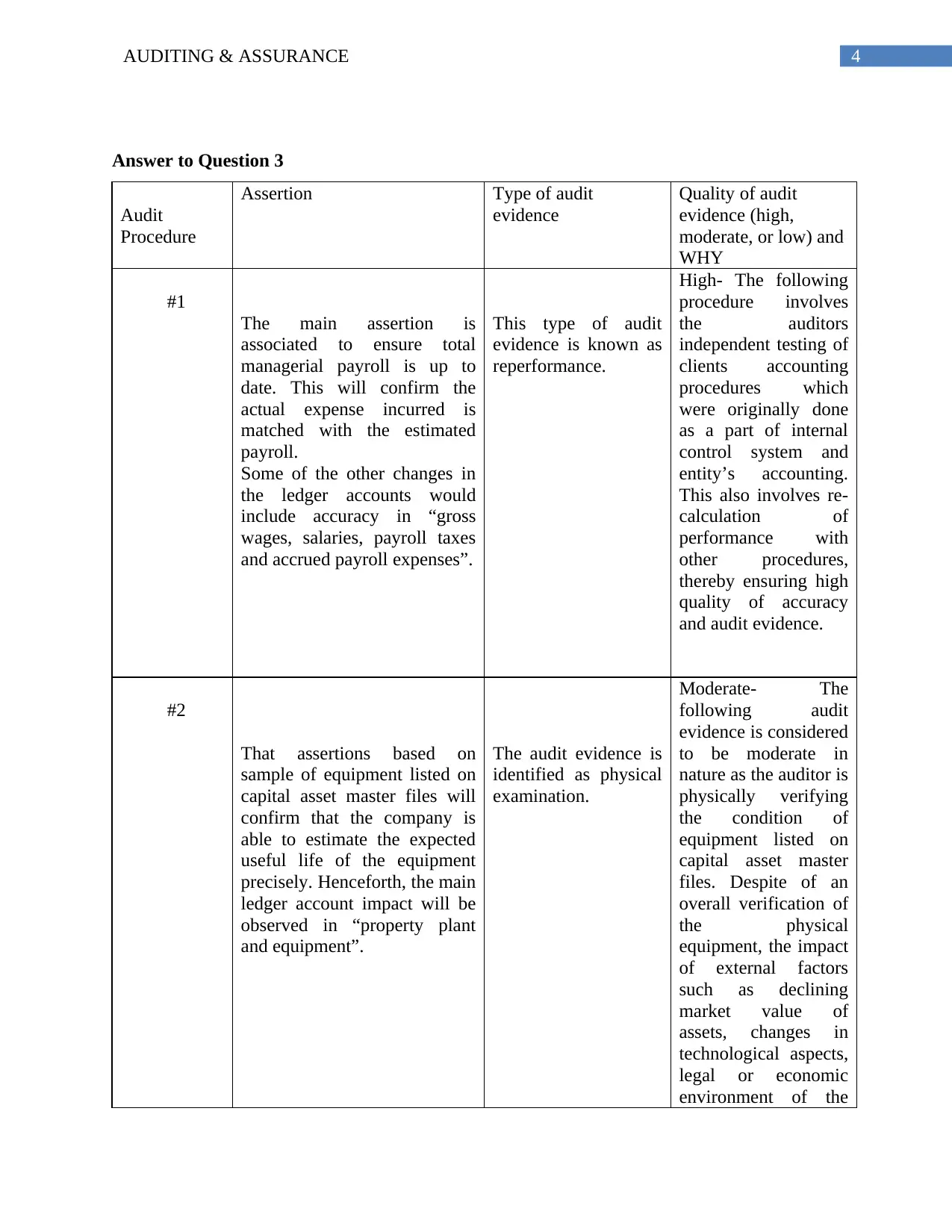

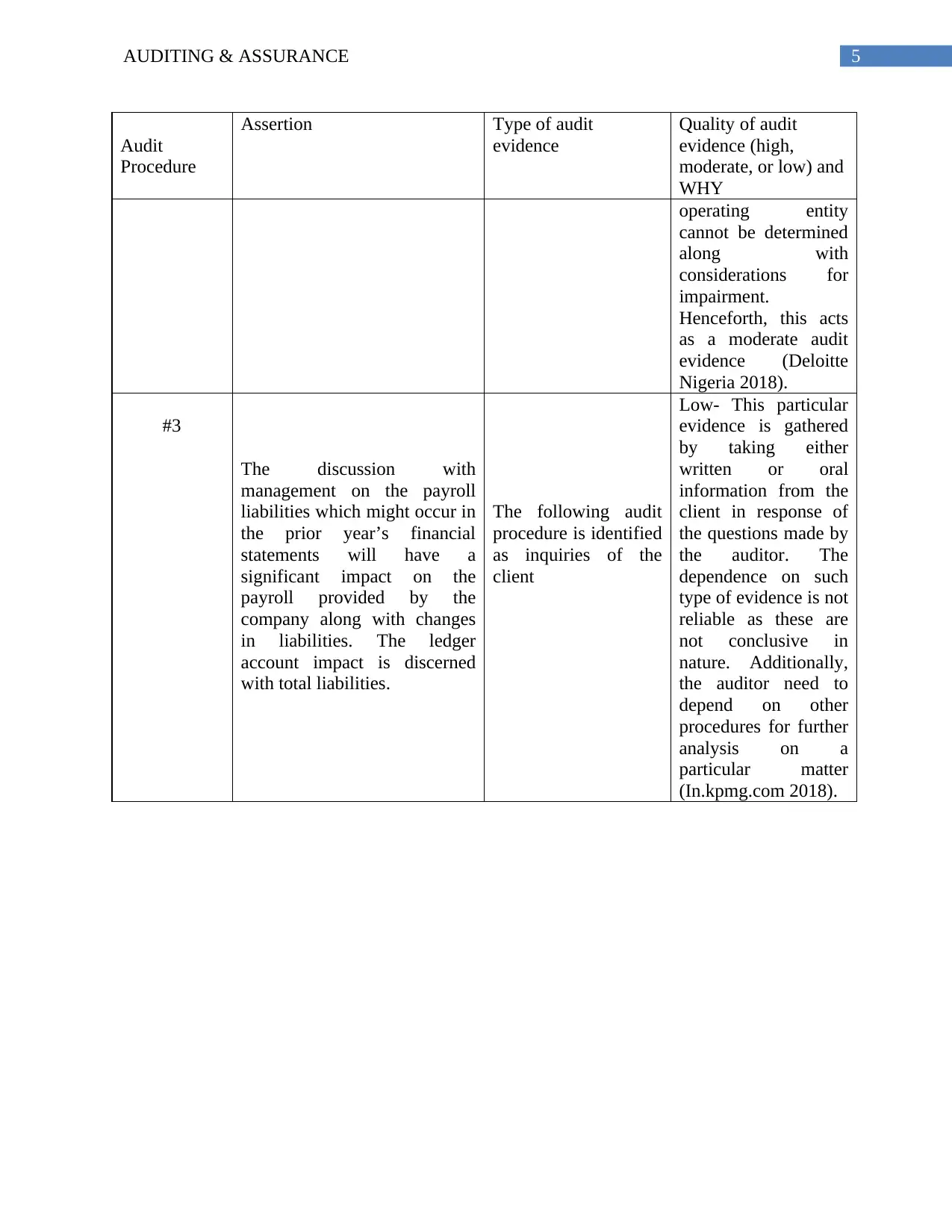

This auditing and assurance report provides an analysis of audit committee practices at International Insurance Inc. (III). It begins by defining auditing components and then compares III’s audit committee practices to published best practices based on internal control frameworks from CPA Canada and the Institute of Internal Auditors (IIA). The report assesses specific aspects of III's practices, including established criteria, reflection of reality, objectivity, independence, and competence. It further evaluates potential violations of Canadian Auditing Standards (CAS), particularly concerning advertising practices, fee quotations, and handling of misstatements. The report also examines the quality of audit evidence obtained through various procedures, such as re-performance of payroll calculations, physical examination of equipment, and inquiries of management, categorizing the evidence as high, moderate, or low based on its reliability and relevance.

1 out of 7

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.