Auditing and Assurance: Detailed Financial Performance Analysis

VerifiedAdded on 2023/06/18

|6

|1265

|99

Report

AI Summary

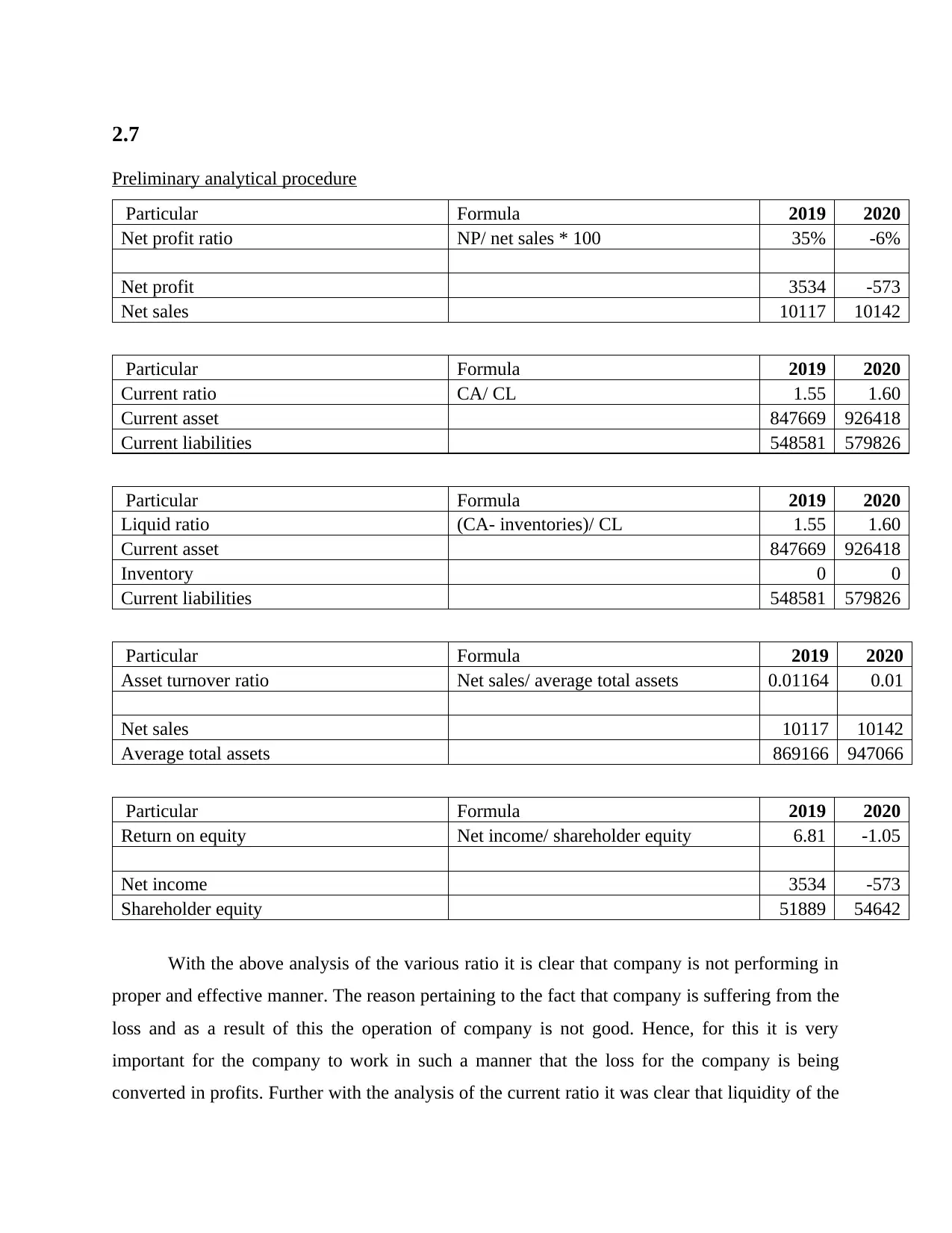

This report presents an auditing and assurance analysis focusing on financial performance, utilizing ratio analysis to assess a company's profitability, liquidity, and asset utilization. The analysis reveals potential issues such as declining net profit ratio and challenges in asset turnover, alongside improvements in liquidity. Key performance indicators like earnings per share (EPS) are examined, highlighting potential impacts on investor confidence. The report also discusses business objectives, strategies, and associated financial risks, particularly concerning expansion into emerging economies and potential impacts on financial statements, emphasizing the importance of auditing the company's accounting practices. The analysis underscores the need for improved business operations to enhance profitability and ensure the company's long-term viability.

1 out of 6

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

© 2024 | Zucol Services PVT LTD | All rights reserved.