HI6026 - DIPL Audit Case Study: Materiality Factors & Expert Use

VerifiedAdded on 2023/06/15

|11

|2997

|136

Case Study

AI Summary

This case study provides an in-depth analysis of the Double Ink Printers Ltd (DIPL) audit, examining the factors influencing the preliminary materiality figure and the need for expert auditor services. It discusses the importance of expert auditors in providing assurance regarding financial performance and position, referencing Auditing Standard 620. The analysis covers factors affecting overall materiality, including the relative nature of materiality, qualitative factors, expected financial statement distribution, and acceptable audit risk. It also identifies specific factors in the DIPL case, such as changes in accounting policies, implementation of a new IT system, management changes, internal auditing implementation, and fluctuations in account balances. The study highlights the relevance of these factors in determining the nature, timing, and extent of audit procedures, emphasizing the interplay between quantitative and qualitative aspects of materiality and their impact on audit risk and the reliability of financial statements.

AUDITING AND

ASSURANCE

ASSURANCE

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Auditing and Assurance 1

Table of Contents

Introduction......................................................................................................................................2

Need for the Services of an Expert Auditor.....................................................................................2

Five Factors Influencing Overall Materiality of DIPL....................................................................4

Relevancy of the Factors.................................................................................................................5

Material Factors...........................................................................................................................5

Quantitative factors......................................................................................................................5

Qualitative Factors.......................................................................................................................7

Factors influencing Preliminary Figure...........................................................................................7

References........................................................................................................................................9

Table of Contents

Introduction......................................................................................................................................2

Need for the Services of an Expert Auditor.....................................................................................2

Five Factors Influencing Overall Materiality of DIPL....................................................................4

Relevancy of the Factors.................................................................................................................5

Material Factors...........................................................................................................................5

Quantitative factors......................................................................................................................5

Qualitative Factors.......................................................................................................................7

Factors influencing Preliminary Figure...........................................................................................7

References........................................................................................................................................9

Auditing and Assurance 2

Introduction

This report contains the analysis of the case study given for DIPL where the services of an expert

is used by the company to collect evidences for material misstatements which was founded in

financial reports. It is important for a company to prevent material misstatements in the financial

records and statements. For this purpose company conduct internal and external audit depending

on the demand needed for the type of auditing required. The questions been asked in the case

study in relation to the factors which influence the preliminary figure determined for materiality

in the audit of DIPL. The factors which are being identified are explained well to showcase the

relevancy in calculating the materiality in the audit planning process.

Need for the Services of an Expert Auditor

On the basis of the case study given for the company DIPL, it is necessary to conduct audit from

an expert for the sole purpose that it provides assurance to the management that presents a true

and fair picture of the financial performance and position. There is an auditing standard 620

which explains the guidance to use the work of an expert in audit as evidence (Auasb.gov.au,

2009). An expert here means a person or a firm who possess some special skills and expertise in

their particular field (Accaglobal.com, 2011).

As per the case of DIPL, where few issues were arising in the accounting department and auditor

fails to maintain the financial ratios under the provided benchmarks. The new CEO William

Jackson pounded a recommendation to introduce a new internal control system in the department

to resolve the issues arising in the financial statement and also decides to invest in IT system

which will automate the whole process of finance and accounting and integrate the current

accounting process within the organization. But the IT manager had issues in implementing the

IT system installation and the way it was handled. It was found out that there was not enough

staff available to do the required reconciliation and testing. The testing which was conducted

before implementing IT system into the accounting process various errors are found out in the

transactions and its value allocation. Though there were staff appointed at each stage in the

department but it happens to be showing non reliable results. Due to such weak system of

finance and accounting department the need for the use of expert in audit is highly required

where the expert will collect audit evidences of the company as per the new internal control

system introduced it will be helpful for expert. The auditor must have to rely on the audit

Introduction

This report contains the analysis of the case study given for DIPL where the services of an expert

is used by the company to collect evidences for material misstatements which was founded in

financial reports. It is important for a company to prevent material misstatements in the financial

records and statements. For this purpose company conduct internal and external audit depending

on the demand needed for the type of auditing required. The questions been asked in the case

study in relation to the factors which influence the preliminary figure determined for materiality

in the audit of DIPL. The factors which are being identified are explained well to showcase the

relevancy in calculating the materiality in the audit planning process.

Need for the Services of an Expert Auditor

On the basis of the case study given for the company DIPL, it is necessary to conduct audit from

an expert for the sole purpose that it provides assurance to the management that presents a true

and fair picture of the financial performance and position. There is an auditing standard 620

which explains the guidance to use the work of an expert in audit as evidence (Auasb.gov.au,

2009). An expert here means a person or a firm who possess some special skills and expertise in

their particular field (Accaglobal.com, 2011).

As per the case of DIPL, where few issues were arising in the accounting department and auditor

fails to maintain the financial ratios under the provided benchmarks. The new CEO William

Jackson pounded a recommendation to introduce a new internal control system in the department

to resolve the issues arising in the financial statement and also decides to invest in IT system

which will automate the whole process of finance and accounting and integrate the current

accounting process within the organization. But the IT manager had issues in implementing the

IT system installation and the way it was handled. It was found out that there was not enough

staff available to do the required reconciliation and testing. The testing which was conducted

before implementing IT system into the accounting process various errors are found out in the

transactions and its value allocation. Though there were staff appointed at each stage in the

department but it happens to be showing non reliable results. Due to such weak system of

finance and accounting department the need for the use of expert in audit is highly required

where the expert will collect audit evidences of the company as per the new internal control

system introduced it will be helpful for expert. The auditor must have to rely on the audit

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Auditing and Assurance 3

evidences given by expert. To be ensured about the qualification and expertise that an expert

must consist and align the whole procedure with the new IT system introduced in the company

and a complete study should be conducted about the assurance of expert’s qualifications (Boritz,

Robinson, Wong, and Kochetova-Kozloski, 2014).

In the given case study, auditor will determine the need first to use the work of an expert while

considering:

The company’s team knowledge and the past experiences of the matter of the company

here is being considered.

The risk involve of material misstatement in the financial report of DIPL is considered

where complexity, nature and materiality will be taken.

Obtaining the quality and quantity of audit evidence which has been expected are done.

There is a need to obtain the understanding of DIPL and perform the procedure further in

assessment of risk, the auditor requires in combined with company and individually the audit

evidences that consists of reports, valuations, opinions and statements of an expert. For example

the evidences must include the following:

- The valuations required of various type of assets of the company including ink, printers,

property, plant and equipment;

- The condition of assets physically or quantities available and the useful life of fixed

assets which is remaining;

- The type of valuation that has been followed to determine amounts and what techniques

or methods have been used while valuation for example DIPL is following actuarial

valuation;

- Work is measured to see if completed or in progress and take advice accordingly;

(Messier, and Schmidt, 2017.).

- The opinions in concern with interpretations of agreements, statutes and regulation been

followed by the company (Ifac.org, 2017).

While planning to use the work of expert in audit of the DIPL, it is the responsibility of

auditor to look out for the competence of the expert in profession. The auditor of the

company must consider that an expert carries a professional certification, licensed or acquire

evidences given by expert. To be ensured about the qualification and expertise that an expert

must consist and align the whole procedure with the new IT system introduced in the company

and a complete study should be conducted about the assurance of expert’s qualifications (Boritz,

Robinson, Wong, and Kochetova-Kozloski, 2014).

In the given case study, auditor will determine the need first to use the work of an expert while

considering:

The company’s team knowledge and the past experiences of the matter of the company

here is being considered.

The risk involve of material misstatement in the financial report of DIPL is considered

where complexity, nature and materiality will be taken.

Obtaining the quality and quantity of audit evidence which has been expected are done.

There is a need to obtain the understanding of DIPL and perform the procedure further in

assessment of risk, the auditor requires in combined with company and individually the audit

evidences that consists of reports, valuations, opinions and statements of an expert. For example

the evidences must include the following:

- The valuations required of various type of assets of the company including ink, printers,

property, plant and equipment;

- The condition of assets physically or quantities available and the useful life of fixed

assets which is remaining;

- The type of valuation that has been followed to determine amounts and what techniques

or methods have been used while valuation for example DIPL is following actuarial

valuation;

- Work is measured to see if completed or in progress and take advice accordingly;

(Messier, and Schmidt, 2017.).

- The opinions in concern with interpretations of agreements, statutes and regulation been

followed by the company (Ifac.org, 2017).

While planning to use the work of expert in audit of the DIPL, it is the responsibility of

auditor to look out for the competence of the expert in profession. The auditor of the

company must consider that an expert carries a professional certification, licensed or acquire

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Auditing and Assurance 4

a membership in a professional body. The experience and reputation an expert is having in

the field where the auditor requires audit evidence. Also the objectivity of the expert is being

evaluated that an expert must not be related to entity by way of employment or dependent

financially, having an investment in the same company. After the evaluation done the auditor

will discuss with management whatever is required and then it is decided to use the work of

an expert.

Five Factors Influencing Overall Materiality of DIPL

The preliminary figure for overall materiality are the maximum amount from which financial

statements could be misstated. There are factors which will affect the preliminary figure about

the overall materiality of DIPL:

One of the main factor is the materiality is more of relative rather than an absolute

concept because to check if the misstatement found out are material or not there should

have been a base for the same. The base can be used by auditor namely net income before

taxes, current assets, and working capital and total assets.

Another factor that might influence preliminary judgment for overall materiality is the

bases, which is explained above and are needed to support the relative concept of

materiality.

There are few qualitative factors that affect materiality decisions in various manner. As

few types of misstatement are significant for users than others.

Preliminary judgment is affected by the expected distribution of the financial statements.

The preliminary figure is set low in case the financial statements are not widely

distributed as expected.

The preliminary judgment of materiality is affected by the level of acceptable audit risk

(Lakis, and Masiulevičius, 2017).

The factors that are affecting the preliminary figure of overall materiality in the audit of

DIPL are given hereunder:

Changes in the accounting policies and estimates

The new IT system has been implemented in the company

Top management changes

a membership in a professional body. The experience and reputation an expert is having in

the field where the auditor requires audit evidence. Also the objectivity of the expert is being

evaluated that an expert must not be related to entity by way of employment or dependent

financially, having an investment in the same company. After the evaluation done the auditor

will discuss with management whatever is required and then it is decided to use the work of

an expert.

Five Factors Influencing Overall Materiality of DIPL

The preliminary figure for overall materiality are the maximum amount from which financial

statements could be misstated. There are factors which will affect the preliminary figure about

the overall materiality of DIPL:

One of the main factor is the materiality is more of relative rather than an absolute

concept because to check if the misstatement found out are material or not there should

have been a base for the same. The base can be used by auditor namely net income before

taxes, current assets, and working capital and total assets.

Another factor that might influence preliminary judgment for overall materiality is the

bases, which is explained above and are needed to support the relative concept of

materiality.

There are few qualitative factors that affect materiality decisions in various manner. As

few types of misstatement are significant for users than others.

Preliminary judgment is affected by the expected distribution of the financial statements.

The preliminary figure is set low in case the financial statements are not widely

distributed as expected.

The preliminary judgment of materiality is affected by the level of acceptable audit risk

(Lakis, and Masiulevičius, 2017).

The factors that are affecting the preliminary figure of overall materiality in the audit of

DIPL are given hereunder:

Changes in the accounting policies and estimates

The new IT system has been implemented in the company

Top management changes

Auditing and Assurance 5

Internal auditing implementation in company.

The fluctuations in over past three years of account receivables, inventory and cash

balance are severe.

Relevancy of the Factors

The key purpose of preliminary materiality judgment is to determine the nature, timing and

extent of procedures of audit and guide the auditor. The judgment will include the materiality of

management’s financial statement where amounts may be higher or lower according to the risk

and needs of the audit process. The factors mentioned above for determining the preliminary

judgment which influence overall materiality have relevancy in calculating the preliminary

figures that are explained below:

Material Factors

Materiality is not an absolute concept but more of a relative concept. It basically means material

for one company may not be material for another company. The amount of information that is

omitted, undisclosed or misstated affects economic decisions taken by users of financial

statements or the management who discharge their accountability (Edgley, Jones, and Atkins,

2015). While evaluating materiality of the company the base is needed and the primary base for

the same would be net income before taxes and bases will come under quantitative factors. While

determining overall materiality there are some questions that need to be answered for example

the major users of financial report, the use of information to make economic decisions and

discharge their responsibilities on it. The factor of materiality is relevant for calculating

preliminary figure for overall materiality as the relationship between materiality and the level of

audit risk contrary (Asare, Majoor, and Wright, 2017). If materiality decreases then audit risk

will increase and vice versa, for example if there is a decrease found out in materiality amount

from $100,000 to $10,000 and same audit evidence has been collected then audit risk will

increase. Low level of misstatements are difficult to detect so it is hard enough to rely on

evidences. An auditor must collect additional audit evidence if the level of audit risk and

materiality levels are same. The materiality factors contains both the quantitative and qualitative

aspects with it (Hux, 2017).

Internal auditing implementation in company.

The fluctuations in over past three years of account receivables, inventory and cash

balance are severe.

Relevancy of the Factors

The key purpose of preliminary materiality judgment is to determine the nature, timing and

extent of procedures of audit and guide the auditor. The judgment will include the materiality of

management’s financial statement where amounts may be higher or lower according to the risk

and needs of the audit process. The factors mentioned above for determining the preliminary

judgment which influence overall materiality have relevancy in calculating the preliminary

figures that are explained below:

Material Factors

Materiality is not an absolute concept but more of a relative concept. It basically means material

for one company may not be material for another company. The amount of information that is

omitted, undisclosed or misstated affects economic decisions taken by users of financial

statements or the management who discharge their accountability (Edgley, Jones, and Atkins,

2015). While evaluating materiality of the company the base is needed and the primary base for

the same would be net income before taxes and bases will come under quantitative factors. While

determining overall materiality there are some questions that need to be answered for example

the major users of financial report, the use of information to make economic decisions and

discharge their responsibilities on it. The factor of materiality is relevant for calculating

preliminary figure for overall materiality as the relationship between materiality and the level of

audit risk contrary (Asare, Majoor, and Wright, 2017). If materiality decreases then audit risk

will increase and vice versa, for example if there is a decrease found out in materiality amount

from $100,000 to $10,000 and same audit evidence has been collected then audit risk will

increase. Low level of misstatements are difficult to detect so it is hard enough to rely on

evidences. An auditor must collect additional audit evidence if the level of audit risk and

materiality levels are same. The materiality factors contains both the quantitative and qualitative

aspects with it (Hux, 2017).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Auditing and Assurance 6

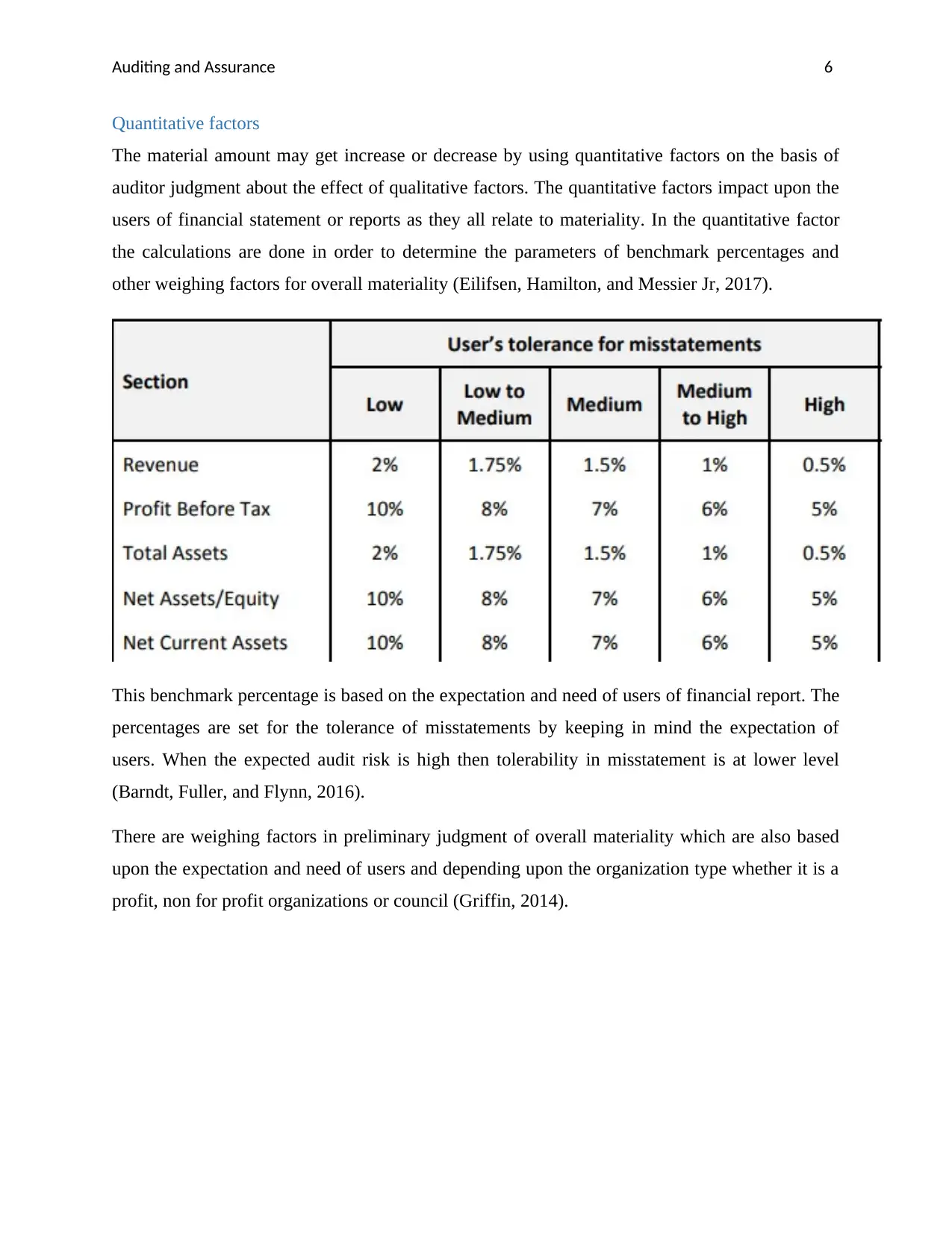

Quantitative factors

The material amount may get increase or decrease by using quantitative factors on the basis of

auditor judgment about the effect of qualitative factors. The quantitative factors impact upon the

users of financial statement or reports as they all relate to materiality. In the quantitative factor

the calculations are done in order to determine the parameters of benchmark percentages and

other weighing factors for overall materiality (Eilifsen, Hamilton, and Messier Jr, 2017).

This benchmark percentage is based on the expectation and need of users of financial report. The

percentages are set for the tolerance of misstatements by keeping in mind the expectation of

users. When the expected audit risk is high then tolerability in misstatement is at lower level

(Barndt, Fuller, and Flynn, 2016).

There are weighing factors in preliminary judgment of overall materiality which are also based

upon the expectation and need of users and depending upon the organization type whether it is a

profit, non for profit organizations or council (Griffin, 2014).

Quantitative factors

The material amount may get increase or decrease by using quantitative factors on the basis of

auditor judgment about the effect of qualitative factors. The quantitative factors impact upon the

users of financial statement or reports as they all relate to materiality. In the quantitative factor

the calculations are done in order to determine the parameters of benchmark percentages and

other weighing factors for overall materiality (Eilifsen, Hamilton, and Messier Jr, 2017).

This benchmark percentage is based on the expectation and need of users of financial report. The

percentages are set for the tolerance of misstatements by keeping in mind the expectation of

users. When the expected audit risk is high then tolerability in misstatement is at lower level

(Barndt, Fuller, and Flynn, 2016).

There are weighing factors in preliminary judgment of overall materiality which are also based

upon the expectation and need of users and depending upon the organization type whether it is a

profit, non for profit organizations or council (Griffin, 2014).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Auditing and Assurance 7

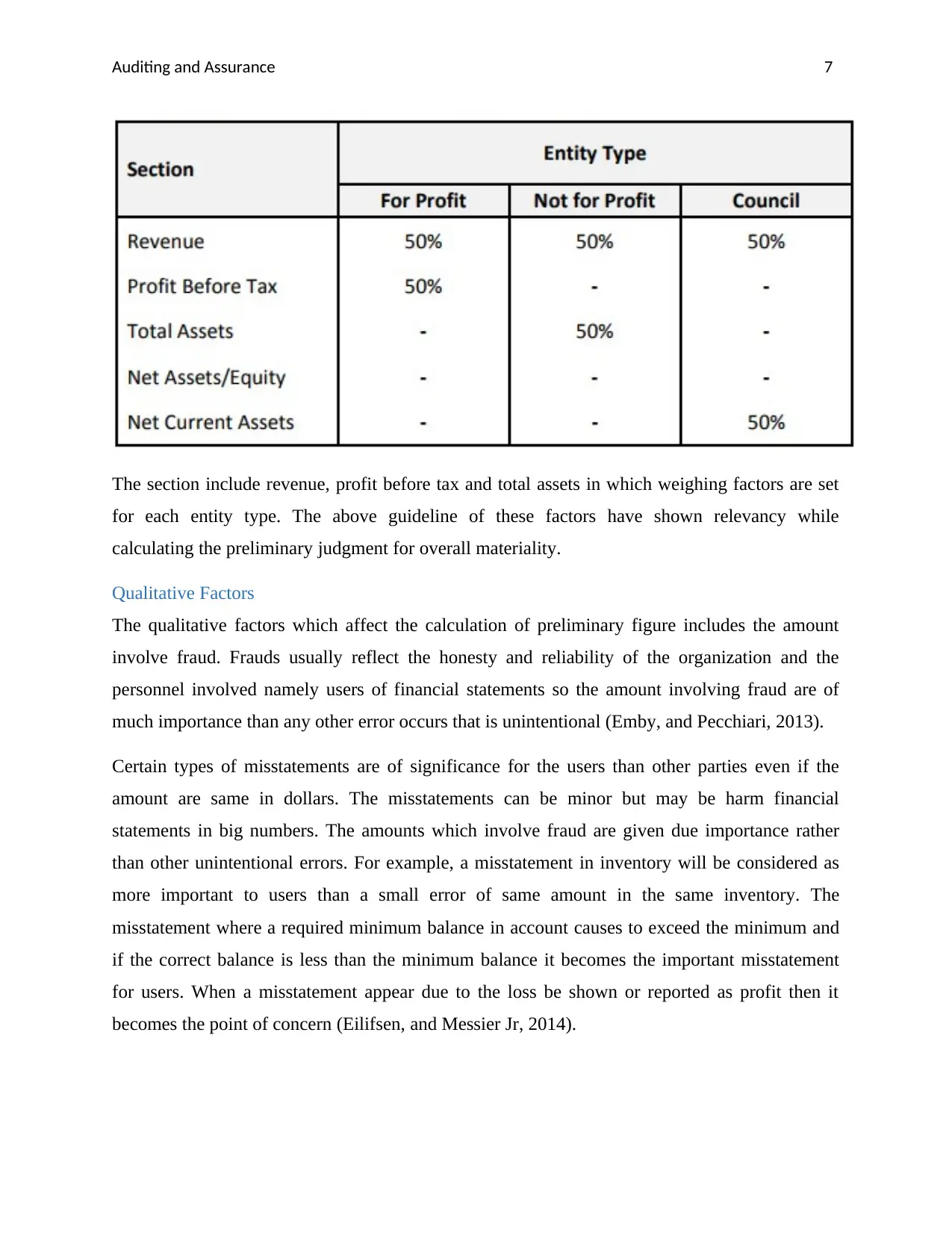

The section include revenue, profit before tax and total assets in which weighing factors are set

for each entity type. The above guideline of these factors have shown relevancy while

calculating the preliminary judgment for overall materiality.

Qualitative Factors

The qualitative factors which affect the calculation of preliminary figure includes the amount

involve fraud. Frauds usually reflect the honesty and reliability of the organization and the

personnel involved namely users of financial statements so the amount involving fraud are of

much importance than any other error occurs that is unintentional (Emby, and Pecchiari, 2013).

Certain types of misstatements are of significance for the users than other parties even if the

amount are same in dollars. The misstatements can be minor but may be harm financial

statements in big numbers. The amounts which involve fraud are given due importance rather

than other unintentional errors. For example, a misstatement in inventory will be considered as

more important to users than a small error of same amount in the same inventory. The

misstatement where a required minimum balance in account causes to exceed the minimum and

if the correct balance is less than the minimum balance it becomes the important misstatement

for users. When a misstatement appear due to the loss be shown or reported as profit then it

becomes the point of concern (Eilifsen, and Messier Jr, 2014).

The section include revenue, profit before tax and total assets in which weighing factors are set

for each entity type. The above guideline of these factors have shown relevancy while

calculating the preliminary judgment for overall materiality.

Qualitative Factors

The qualitative factors which affect the calculation of preliminary figure includes the amount

involve fraud. Frauds usually reflect the honesty and reliability of the organization and the

personnel involved namely users of financial statements so the amount involving fraud are of

much importance than any other error occurs that is unintentional (Emby, and Pecchiari, 2013).

Certain types of misstatements are of significance for the users than other parties even if the

amount are same in dollars. The misstatements can be minor but may be harm financial

statements in big numbers. The amounts which involve fraud are given due importance rather

than other unintentional errors. For example, a misstatement in inventory will be considered as

more important to users than a small error of same amount in the same inventory. The

misstatement where a required minimum balance in account causes to exceed the minimum and

if the correct balance is less than the minimum balance it becomes the important misstatement

for users. When a misstatement appear due to the loss be shown or reported as profit then it

becomes the point of concern (Eilifsen, and Messier Jr, 2014).

Auditing and Assurance 8

Factors influencing Preliminary Figure

The five factors that are being identified in the case study of DIPL which would affect the

preliminary figure of overall materiality in audit planning process of the company. The first

factor which is change in accounting policies and estimates where the change in the valuation of

inventory, provision for inventory obsolesces and the life of printing machine. It creates the

situation where auditor needs to check in detail, the areas where changes has taken place and the

materiality level will be set by auditor at low level so as to make the checking extended.

Therefore, the depreciation on machinery, closing inventory and provision for obsolescence will

cause the auditor to set their preliminary figure of overall materiality at low (Saha, and Roy,

2017).

The second factor is the new IT system implementation and it causes the audit risk to go high so

that the amount of materiality will be set at low level. The auditor is required to check all the

classes of accounting transactions in order to ensure that risk of material misstatement is

reduced. Another factor where the change in top management happened and it made the auditor

to materiality level at low stage. When auditor believes the management honesty then the

assessment of risk is low therefore, materiality level is also set at low level and the extent of

checking can be increased (Ruhnke, Pronobis, and Michel, 2014). The implementation of

internal audit reduces the risk of material misstatement which further reduces audit risk. It cause

the auditor to reduce the level of materiality because an auditor can rely upon internal audit and

allowed to reduce the extent of checking on his/her side.

The fluctuations in the amount of account receivables, inventory and cash balance will be taken

into account by auditor while determining materiality amount. These severe fluctuations depicts

manipulations and the risk of material misstatement. It made auditor to check in more detail with

a purpose to collect evidences therefore, materiality level would be set low.

Factors influencing Preliminary Figure

The five factors that are being identified in the case study of DIPL which would affect the

preliminary figure of overall materiality in audit planning process of the company. The first

factor which is change in accounting policies and estimates where the change in the valuation of

inventory, provision for inventory obsolesces and the life of printing machine. It creates the

situation where auditor needs to check in detail, the areas where changes has taken place and the

materiality level will be set by auditor at low level so as to make the checking extended.

Therefore, the depreciation on machinery, closing inventory and provision for obsolescence will

cause the auditor to set their preliminary figure of overall materiality at low (Saha, and Roy,

2017).

The second factor is the new IT system implementation and it causes the audit risk to go high so

that the amount of materiality will be set at low level. The auditor is required to check all the

classes of accounting transactions in order to ensure that risk of material misstatement is

reduced. Another factor where the change in top management happened and it made the auditor

to materiality level at low stage. When auditor believes the management honesty then the

assessment of risk is low therefore, materiality level is also set at low level and the extent of

checking can be increased (Ruhnke, Pronobis, and Michel, 2014). The implementation of

internal audit reduces the risk of material misstatement which further reduces audit risk. It cause

the auditor to reduce the level of materiality because an auditor can rely upon internal audit and

allowed to reduce the extent of checking on his/her side.

The fluctuations in the amount of account receivables, inventory and cash balance will be taken

into account by auditor while determining materiality amount. These severe fluctuations depicts

manipulations and the risk of material misstatement. It made auditor to check in more detail with

a purpose to collect evidences therefore, materiality level would be set low.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Auditing and Assurance 9

References

Accaglobal.com. 2011. Using the work of an auditor’s expert. [Online] Available at:

http://www.accaglobal.com/content/dam/acca/global/PDF-students/2012s/

sa_may11_cat8_fau_expert.pdf [Accessed 11 December. 2017].

Asare, S.K., Majoor, B. and Wright, A., 2017. The occurrence and awareness of a misstatement

effect in auditors' internal control severity judgments. International Journal of Auditing.

Auasb.gov.au. 2009. Auditing Standard ASA 620 Using the Work of an Auditor's Expert.

[Online]. Available at: http://www.auasb.gov.au/admin/file/content102/c3/ASA_620_27-10-

09.pdf [Accessed 11 December. 2017].

Barndt, R.J., Fuller, L.R. and Flynn, K.E., 2016. Teaching Inherent Risk and Tolerable

Misstatement in Auditing: A Modified Delphi Method as a Teaching Tool. In Advances in

Accounting Education: Teaching and Curriculum Innovations (pp. 125-140). Emerald Group

Publishing Limited.

Boritz, J.E., Robinson, L.A., Wong, C. and Kochetova-Kozloski, N., 2014. Auditors’ and

specialists’ views about the use of specialists during an audit.

Edgley, C., Jones, M.J. and Atkins, J., 2015. The adoption of the materiality concept in social

and environmental reporting assurance: A field study approach. The British Accounting Review,

47(1), pp.1-18.

Eilifsen, A. and Messier Jr, W.F., 2014. Materiality guidance of the major public accounting

firms. Auditing: A Journal of Practice & Theory, 34(2), pp.3-26.

Eilifsen, A., Hamilton, E.L. and Messier Jr, W.F., 2017. The Importance of Quantifying

Uncertainty: Examining the Effect of Audit Materiality and Sensitivity Analysis Disclosures on

Investors’ Judgments and Decisions.

Emby, C. and Pecchiari, N., 2013. An Empirical Investigation of the Influence of Qualitative

Risk Factors on Canadian Auditors’ Determination of Performance Materiality. Accounting

Perspectives, 12(4), pp.281-299.

References

Accaglobal.com. 2011. Using the work of an auditor’s expert. [Online] Available at:

http://www.accaglobal.com/content/dam/acca/global/PDF-students/2012s/

sa_may11_cat8_fau_expert.pdf [Accessed 11 December. 2017].

Asare, S.K., Majoor, B. and Wright, A., 2017. The occurrence and awareness of a misstatement

effect in auditors' internal control severity judgments. International Journal of Auditing.

Auasb.gov.au. 2009. Auditing Standard ASA 620 Using the Work of an Auditor's Expert.

[Online]. Available at: http://www.auasb.gov.au/admin/file/content102/c3/ASA_620_27-10-

09.pdf [Accessed 11 December. 2017].

Barndt, R.J., Fuller, L.R. and Flynn, K.E., 2016. Teaching Inherent Risk and Tolerable

Misstatement in Auditing: A Modified Delphi Method as a Teaching Tool. In Advances in

Accounting Education: Teaching and Curriculum Innovations (pp. 125-140). Emerald Group

Publishing Limited.

Boritz, J.E., Robinson, L.A., Wong, C. and Kochetova-Kozloski, N., 2014. Auditors’ and

specialists’ views about the use of specialists during an audit.

Edgley, C., Jones, M.J. and Atkins, J., 2015. The adoption of the materiality concept in social

and environmental reporting assurance: A field study approach. The British Accounting Review,

47(1), pp.1-18.

Eilifsen, A. and Messier Jr, W.F., 2014. Materiality guidance of the major public accounting

firms. Auditing: A Journal of Practice & Theory, 34(2), pp.3-26.

Eilifsen, A., Hamilton, E.L. and Messier Jr, W.F., 2017. The Importance of Quantifying

Uncertainty: Examining the Effect of Audit Materiality and Sensitivity Analysis Disclosures on

Investors’ Judgments and Decisions.

Emby, C. and Pecchiari, N., 2013. An Empirical Investigation of the Influence of Qualitative

Risk Factors on Canadian Auditors’ Determination of Performance Materiality. Accounting

Perspectives, 12(4), pp.281-299.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Auditing and Assurance

10

Griffin, J.B., 2014. The effects of uncertainty and disclosure on auditors' fair value materiality

decisions. Journal of Accounting Research, 52(5), pp.1165-1193.

Hux, C.T., 2017. Use of specialists on audit engagements: A research synthesis and directions

for future research. Journal of Accounting Literature, 39, pp.23-51.

Ifac.org. 2017. International Standard on Auditing 620 Using the Work of an Expert. [Online]

Available at:

http://www.ifac.org/system/files/downloads/2008_Auditing_Handbook_A190_ISA_620.pdf

[Accessed 11 December. 2017].

Lakis, V. and Masiulevičius, A., 2017. ACCEPTABLE AUDIT MATERIALITY FOR USERS

OF FINANCIAL STATEMENTS. Journal of Management, 2(31).

Messier, Jr, W.F. and Schmidt, M., 2017. Offsetting Misstatements: The Effect of Misstatement

Distribution, Quantitative Materiality and Client Pressure on Auditors' Judgments. The

Accounting Review.

Ruhnke, K., Pronobis, P. and Michel, M., 2014. Audit materiality disclosures and credit lending

decisions.

Saha, S.S. and Roy, M.N., 2017. Quality Control Procedure for Statutory Financial Audit: An

Empirical Study.

10

Griffin, J.B., 2014. The effects of uncertainty and disclosure on auditors' fair value materiality

decisions. Journal of Accounting Research, 52(5), pp.1165-1193.

Hux, C.T., 2017. Use of specialists on audit engagements: A research synthesis and directions

for future research. Journal of Accounting Literature, 39, pp.23-51.

Ifac.org. 2017. International Standard on Auditing 620 Using the Work of an Expert. [Online]

Available at:

http://www.ifac.org/system/files/downloads/2008_Auditing_Handbook_A190_ISA_620.pdf

[Accessed 11 December. 2017].

Lakis, V. and Masiulevičius, A., 2017. ACCEPTABLE AUDIT MATERIALITY FOR USERS

OF FINANCIAL STATEMENTS. Journal of Management, 2(31).

Messier, Jr, W.F. and Schmidt, M., 2017. Offsetting Misstatements: The Effect of Misstatement

Distribution, Quantitative Materiality and Client Pressure on Auditors' Judgments. The

Accounting Review.

Ruhnke, K., Pronobis, P. and Michel, M., 2014. Audit materiality disclosures and credit lending

decisions.

Saha, S.S. and Roy, M.N., 2017. Quality Control Procedure for Statutory Financial Audit: An

Empirical Study.

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.