Auditing and Assurance Service: Analysis of Financial Statement Risks

VerifiedAdded on 2023/06/03

|9

|1343

|287

Report

AI Summary

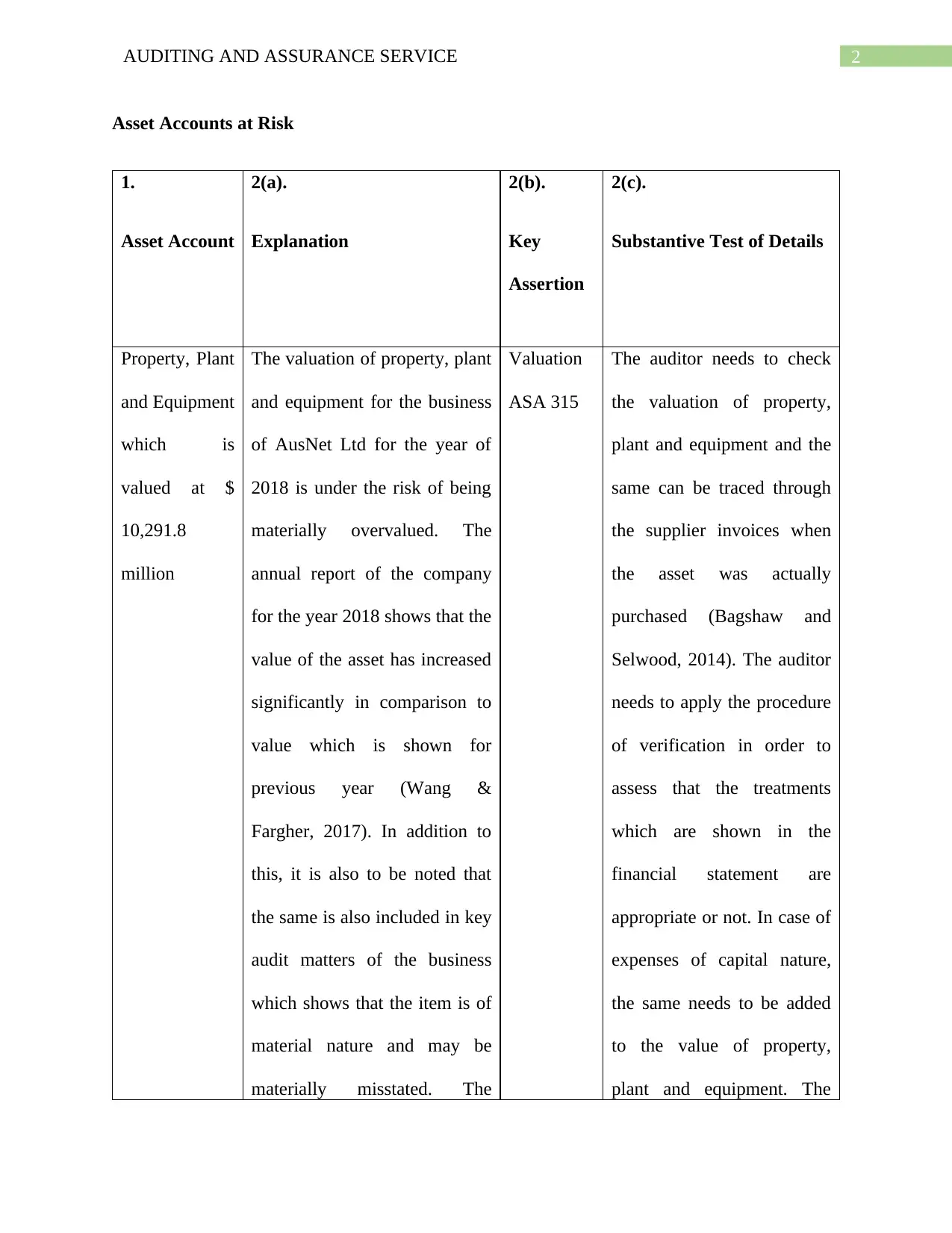

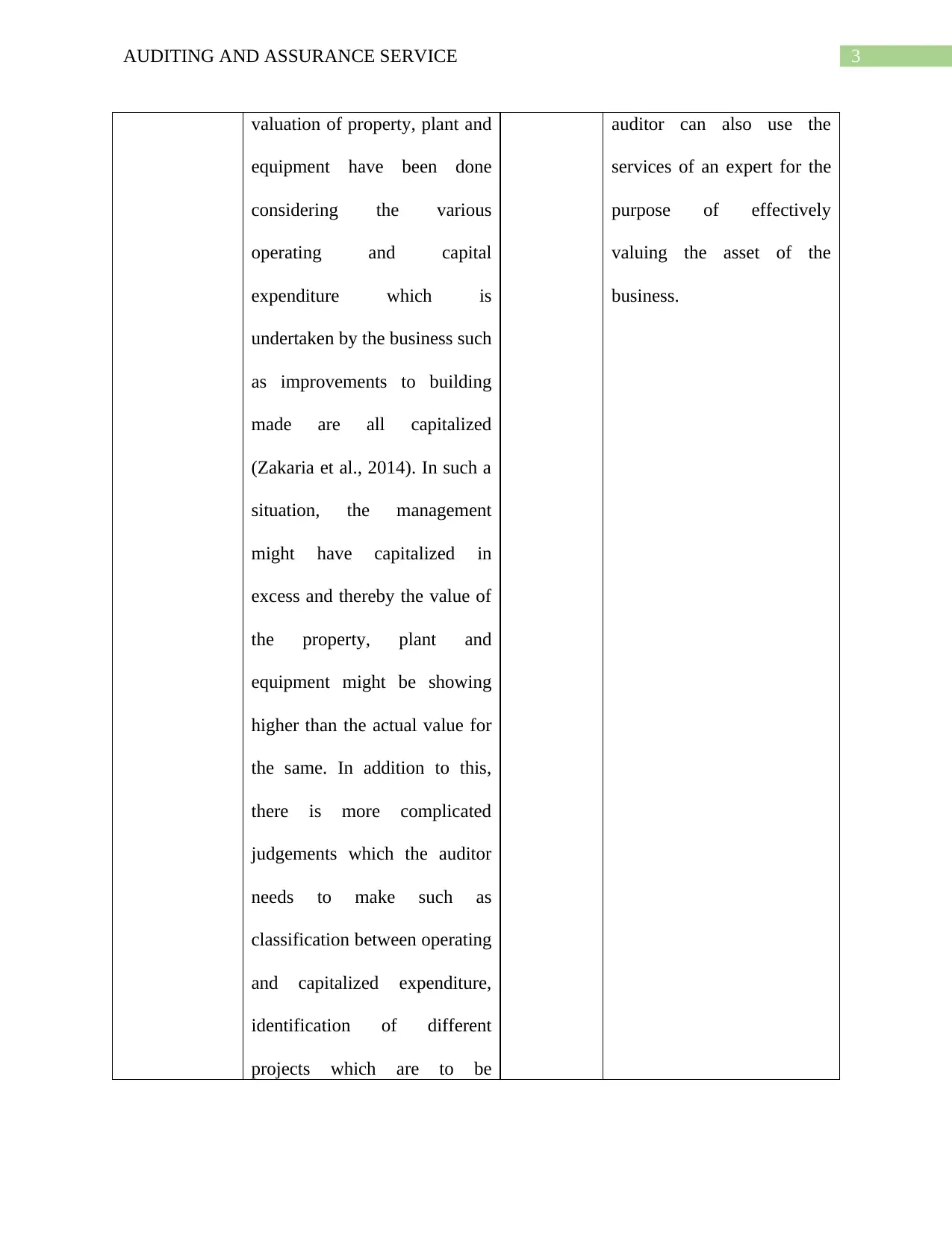

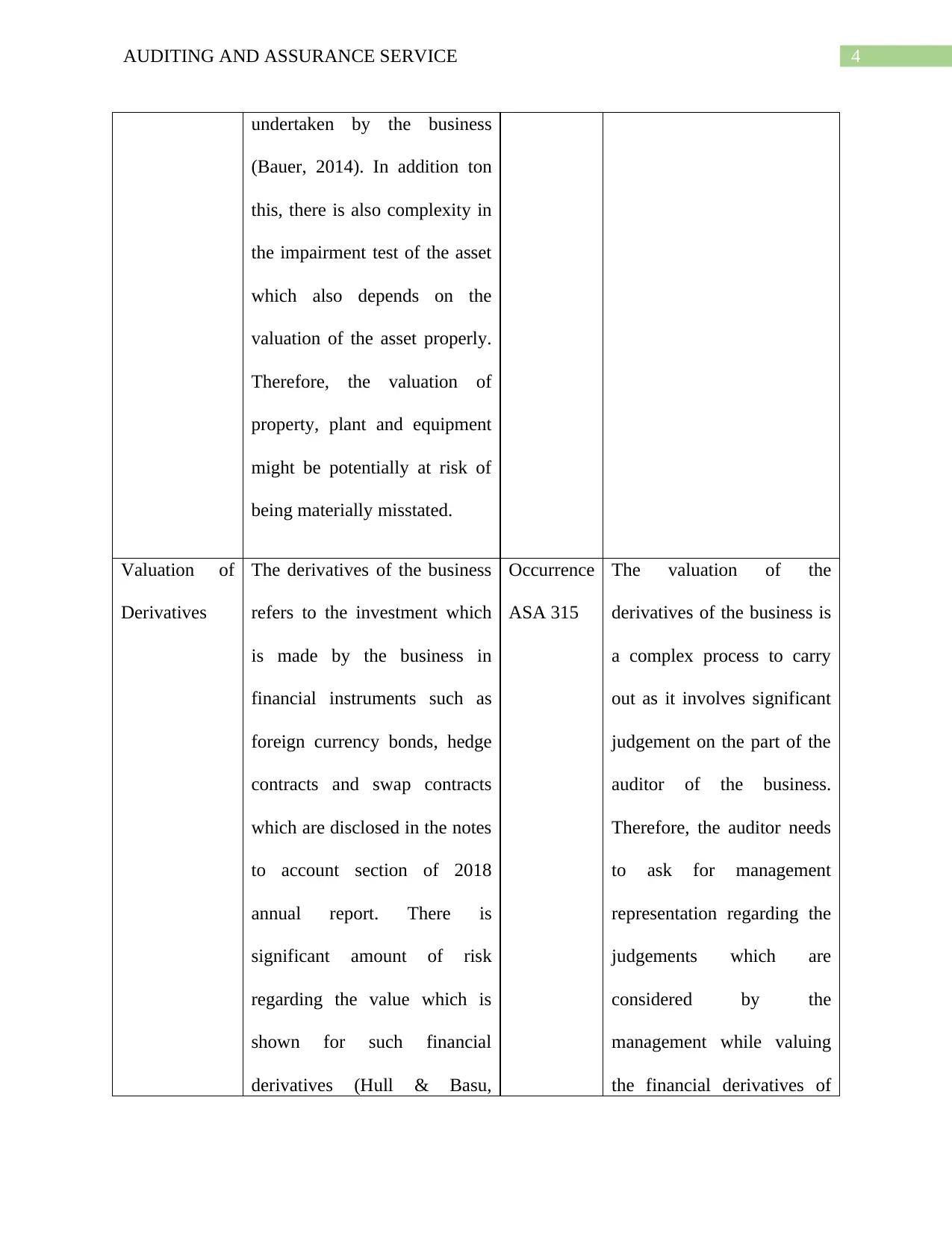

This report provides an in-depth analysis of auditing and assurance services, focusing on the risk assessment of asset accounts and expenses. It identifies key areas of concern, such as the valuation of property, plant, and equipment, as well as derivatives, highlighting the potential for material misstatement. The report also examines operating lease expenses and the importance of adhering to AASB 16 for proper disclosure. Substantive tests of detail are suggested to verify the accuracy and completeness of financial statement items. The document emphasizes the auditor's role in evaluating management's judgments and ensuring that financial statements present a true and fair view. Desklib offers a wide array of solved assignments and past papers for students seeking assistance with their studies.

1 out of 9

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.