Auditing, Assurance & Services: A Deep Dive into ASA 701 and ASA 570

VerifiedAdded on 2024/05/31

|17

|3574

|245

AI Summary

This report delves into the crucial auditing standards ASA 701 and ASA 570, focusing on the auditor's responsibilities regarding going concern assumptions and key audit matters. It examines the scope and application of ASA 701, including the identification and reporting of key audit matters, using real-world examples from AGL Energy Limited, ADX-energy Limited, and Acacia Coal Limited. The report also explores the scope and applicability of ASA 570, outlining the auditor's and management's responsibilities in assessing and reporting on going concern. By understanding these standards, readers gain valuable insights into the auditor's role in ensuring the accuracy and reliability of financial statements.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Auditing, Assurance & Services

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Executive summary:

Auditing is an important event which is conducted to ensure the true and fair view of financial

statements. ASA 701 and ASA 570 are related to investor interest and this assessment is made to

give depth knowledge of these auditing standards. ASA 701 “Communicating Key Audit Matters

in the Independent Auditor’s Report” explains the liability of auditor to disclose the Key matter

of financial statement which is founded in the auditing process. ASA 570 “Going Concern” also

defines the responsibility of auditor to investigate and report the going concern ability of a listed

company.

Present scope: AGL energy limited, ADX-energy limited and Acacia Coal Limited is leading

companies in Australia which is engaged in the generation and distribution of energy resources.

The assessment explains the auditor discloser requirements about the key matters under ASA

701 and ASA 570. On the basis of this assessment, the user will be able to understand the key

facts of these two standards along with the disclosers which are made by the auditors of above

companies.

Auditing is an important event which is conducted to ensure the true and fair view of financial

statements. ASA 701 and ASA 570 are related to investor interest and this assessment is made to

give depth knowledge of these auditing standards. ASA 701 “Communicating Key Audit Matters

in the Independent Auditor’s Report” explains the liability of auditor to disclose the Key matter

of financial statement which is founded in the auditing process. ASA 570 “Going Concern” also

defines the responsibility of auditor to investigate and report the going concern ability of a listed

company.

Present scope: AGL energy limited, ADX-energy limited and Acacia Coal Limited is leading

companies in Australia which is engaged in the generation and distribution of energy resources.

The assessment explains the auditor discloser requirements about the key matters under ASA

701 and ASA 570. On the basis of this assessment, the user will be able to understand the key

facts of these two standards along with the disclosers which are made by the auditors of above

companies.

Table of Contents

Introduction:....................................................................................................................................4

ASA 701 “Communicating Key Audit Matters in the Independent Auditor’s Report”..................5

ASA 570 “Going Concern”...........................................................................................................11

Conclusion:....................................................................................................................................15

References:....................................................................................................................................16

Introduction:....................................................................................................................................4

ASA 701 “Communicating Key Audit Matters in the Independent Auditor’s Report”..................5

ASA 570 “Going Concern”...........................................................................................................11

Conclusion:....................................................................................................................................15

References:....................................................................................................................................16

Introduction:

ASA 701 and ASA 570 are going to be explained in this report and the explanation is based on

the responsibility of auditor regarding the compliance and reporting of going concern assumption

and key auditing matter. The report describes the ASA 701 “Communicating Key Audit Matters

in the Independent Auditor’s Report” along with the scope of the standard and mean of key

auditing matters. The report also includes an overview of the Key auditing matters of three ASX

listed companies which are reported by the auditor of these companies. ASA 570 “Going

Concern” is also going to be explained in this report. The explanation includes the scope of

standard and applicability of standard along with the responsibility of auditor and management.

After the learning of this description, the learner will be capable to deeply understand the object

and importance of these two auditing standards.

ASA 701 and ASA 570 are going to be explained in this report and the explanation is based on

the responsibility of auditor regarding the compliance and reporting of going concern assumption

and key auditing matter. The report describes the ASA 701 “Communicating Key Audit Matters

in the Independent Auditor’s Report” along with the scope of the standard and mean of key

auditing matters. The report also includes an overview of the Key auditing matters of three ASX

listed companies which are reported by the auditor of these companies. ASA 570 “Going

Concern” is also going to be explained in this report. The explanation includes the scope of

standard and applicability of standard along with the responsibility of auditor and management.

After the learning of this description, the learner will be capable to deeply understand the object

and importance of these two auditing standards.

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

ASA 701 “Communicating Key Audit Matters in the Independent Auditor’s

Report”

The financial statement related to period completing after December -15-2016, are coming under

the surveillance of ASA 701. Standard is applicable to the financial reports of a company and

describes the responsibility of auditor to explain the Key auditing matters in his report.

Key Audit Matter:

Those issues that, inside the analyst's master judgment have been of most centrality within the

audit of a financial paper of the present time era. Key survey topics are browsed issues talked

with the ones blamed for business enterprise (AASB, 2015).

Generally, following Terms are known as Key Audit Matters:

(a): Areas which contains high risk or significant risks of material misstatement (ASA 315)

(b): Those matters which have a significant impact on audit (paragraph 25)

(c): judgement regarding zones inside the cash related report that included simple agency

judgment, together with accounting tests that have been diagnosed as having excessive

estimation uncertainty.

The scope of the standard:

This Auditing Standard offers with the evaluator's commitment to skip on input survey topics in

the inspector's document. It is proposed to address both the examiner's judgment with reference

to what to pass on inside the commentator's record and the casing and substance of such

correspondence. The motive at the back of giving key audit topics is to overtake the beneficial

estimation of the evaluator's record by means of giving more great straightforwardness about the

survey that becomes performed (Seyam and Brickman, 2016). Passing on key audit subjects

offers additional information to customers of the cash associated reaction to help them in know-

how those problems that, inside the evaluator's master judgment, have been of most centrality in

the survey of the financial record of the present time allotment. Granting key survey subjects

may also in like manner help arranged clients in know-how the factor and districts of primary

corporation judgment in the analysed financial record (Paragraph A1 to A4).

Report”

The financial statement related to period completing after December -15-2016, are coming under

the surveillance of ASA 701. Standard is applicable to the financial reports of a company and

describes the responsibility of auditor to explain the Key auditing matters in his report.

Key Audit Matter:

Those issues that, inside the analyst's master judgment have been of most centrality within the

audit of a financial paper of the present time era. Key survey topics are browsed issues talked

with the ones blamed for business enterprise (AASB, 2015).

Generally, following Terms are known as Key Audit Matters:

(a): Areas which contains high risk or significant risks of material misstatement (ASA 315)

(b): Those matters which have a significant impact on audit (paragraph 25)

(c): judgement regarding zones inside the cash related report that included simple agency

judgment, together with accounting tests that have been diagnosed as having excessive

estimation uncertainty.

The scope of the standard:

This Auditing Standard offers with the evaluator's commitment to skip on input survey topics in

the inspector's document. It is proposed to address both the examiner's judgment with reference

to what to pass on inside the commentator's record and the casing and substance of such

correspondence. The motive at the back of giving key audit topics is to overtake the beneficial

estimation of the evaluator's record by means of giving more great straightforwardness about the

survey that becomes performed (Seyam and Brickman, 2016). Passing on key audit subjects

offers additional information to customers of the cash associated reaction to help them in know-

how those problems that, inside the evaluator's master judgment, have been of most centrality in

the survey of the financial record of the present time allotment. Granting key survey subjects

may also in like manner help arranged clients in know-how the factor and districts of primary

corporation judgment in the analysed financial record (Paragraph A1 to A4).

Documentation related to Key audit matters:

AS per the ASA 230, an auditor should make proper documentation for audit work to provide

supportively proves his opinion.

Concerning key audit matters, those grasp judgements be a part of the confirmation, from the

issues talked with the ones blamed for the company, of the troubles that required critical

commentator idea, and what is more paying little mind to whether or not every one of these

issues is a key survey rely on. The evaluator's judgements in such manner are maximum in all

likelihood going to be maintained by using the documentation of the analyst's exchanges with the

ones blamed for the agency and the survey documentation regarding each man or woman trouble

and furthermore sure other audit documentation of the simple problems rising inside the midst of

the survey

Reporting of Key Auditing Matters

Putting the one of a kind Key Audit Matters territory in proximity to the inspector's selection can

also offer unmistakable fine to such information and perceive the clean estimation of obligation

particular statistics to proposed customers (AASB, 2015). Company asked for the demonstration

of different individual troubles in the Key Audit Matters territory consists of successful

judgment. Exactly while comparative financial statistics is shown, the right off the bat vernacular

of a Key Audit Matters segment is uniquely crafted to attract in keenness in regards to the

manner that the key survey topics portrayed relate to only the survey of the coins related

document of the existing time span.

AS per the ASA 230, an auditor should make proper documentation for audit work to provide

supportively proves his opinion.

Concerning key audit matters, those grasp judgements be a part of the confirmation, from the

issues talked with the ones blamed for the company, of the troubles that required critical

commentator idea, and what is more paying little mind to whether or not every one of these

issues is a key survey rely on. The evaluator's judgements in such manner are maximum in all

likelihood going to be maintained by using the documentation of the analyst's exchanges with the

ones blamed for the agency and the survey documentation regarding each man or woman trouble

and furthermore sure other audit documentation of the simple problems rising inside the midst of

the survey

Reporting of Key Auditing Matters

Putting the one of a kind Key Audit Matters territory in proximity to the inspector's selection can

also offer unmistakable fine to such information and perceive the clean estimation of obligation

particular statistics to proposed customers (AASB, 2015). Company asked for the demonstration

of different individual troubles in the Key Audit Matters territory consists of successful

judgment. Exactly while comparative financial statistics is shown, the right off the bat vernacular

of a Key Audit Matters segment is uniquely crafted to attract in keenness in regards to the

manner that the key survey topics portrayed relate to only the survey of the coins related

document of the existing time span.

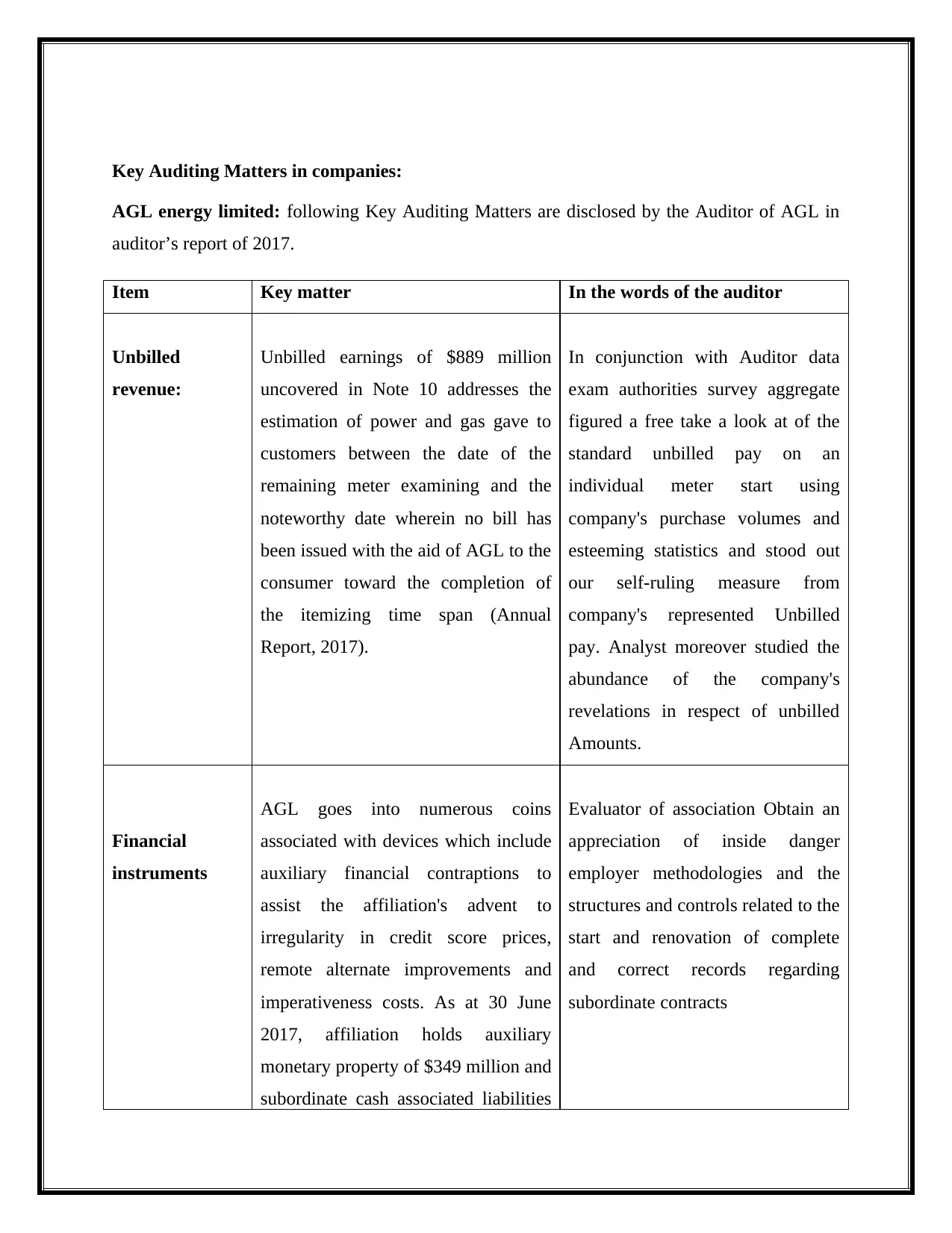

Key Auditing Matters in companies:

AGL energy limited: following Key Auditing Matters are disclosed by the Auditor of AGL in

auditor’s report of 2017.

Item Key matter In the words of the auditor

Unbilled

revenue:

Unbilled earnings of $889 million

uncovered in Note 10 addresses the

estimation of power and gas gave to

customers between the date of the

remaining meter examining and the

noteworthy date wherein no bill has

been issued with the aid of AGL to the

consumer toward the completion of

the itemizing time span (Annual

Report, 2017).

In conjunction with Auditor data

exam authorities survey aggregate

figured a free take a look at of the

standard unbilled pay on an

individual meter start using

company's purchase volumes and

esteeming statistics and stood out

our self-ruling measure from

company's represented Unbilled

pay. Analyst moreover studied the

abundance of the company's

revelations in respect of unbilled

Amounts.

Financial

instruments

AGL goes into numerous coins

associated with devices which include

auxiliary financial contraptions to

assist the affiliation's advent to

irregularity in credit score prices,

remote alternate improvements and

imperativeness costs. As at 30 June

2017, affiliation holds auxiliary

monetary property of $349 million and

subordinate cash associated liabilities

Evaluator of association Obtain an

appreciation of inside danger

employer methodologies and the

structures and controls related to the

start and renovation of complete

and correct records regarding

subordinate contracts

AGL energy limited: following Key Auditing Matters are disclosed by the Auditor of AGL in

auditor’s report of 2017.

Item Key matter In the words of the auditor

Unbilled

revenue:

Unbilled earnings of $889 million

uncovered in Note 10 addresses the

estimation of power and gas gave to

customers between the date of the

remaining meter examining and the

noteworthy date wherein no bill has

been issued with the aid of AGL to the

consumer toward the completion of

the itemizing time span (Annual

Report, 2017).

In conjunction with Auditor data

exam authorities survey aggregate

figured a free take a look at of the

standard unbilled pay on an

individual meter start using

company's purchase volumes and

esteeming statistics and stood out

our self-ruling measure from

company's represented Unbilled

pay. Analyst moreover studied the

abundance of the company's

revelations in respect of unbilled

Amounts.

Financial

instruments

AGL goes into numerous coins

associated with devices which include

auxiliary financial contraptions to

assist the affiliation's advent to

irregularity in credit score prices,

remote alternate improvements and

imperativeness costs. As at 30 June

2017, affiliation holds auxiliary

monetary property of $349 million and

subordinate cash associated liabilities

Evaluator of association Obtain an

appreciation of inside danger

employer methodologies and the

structures and controls related to the

start and renovation of complete

and correct records regarding

subordinate contracts

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

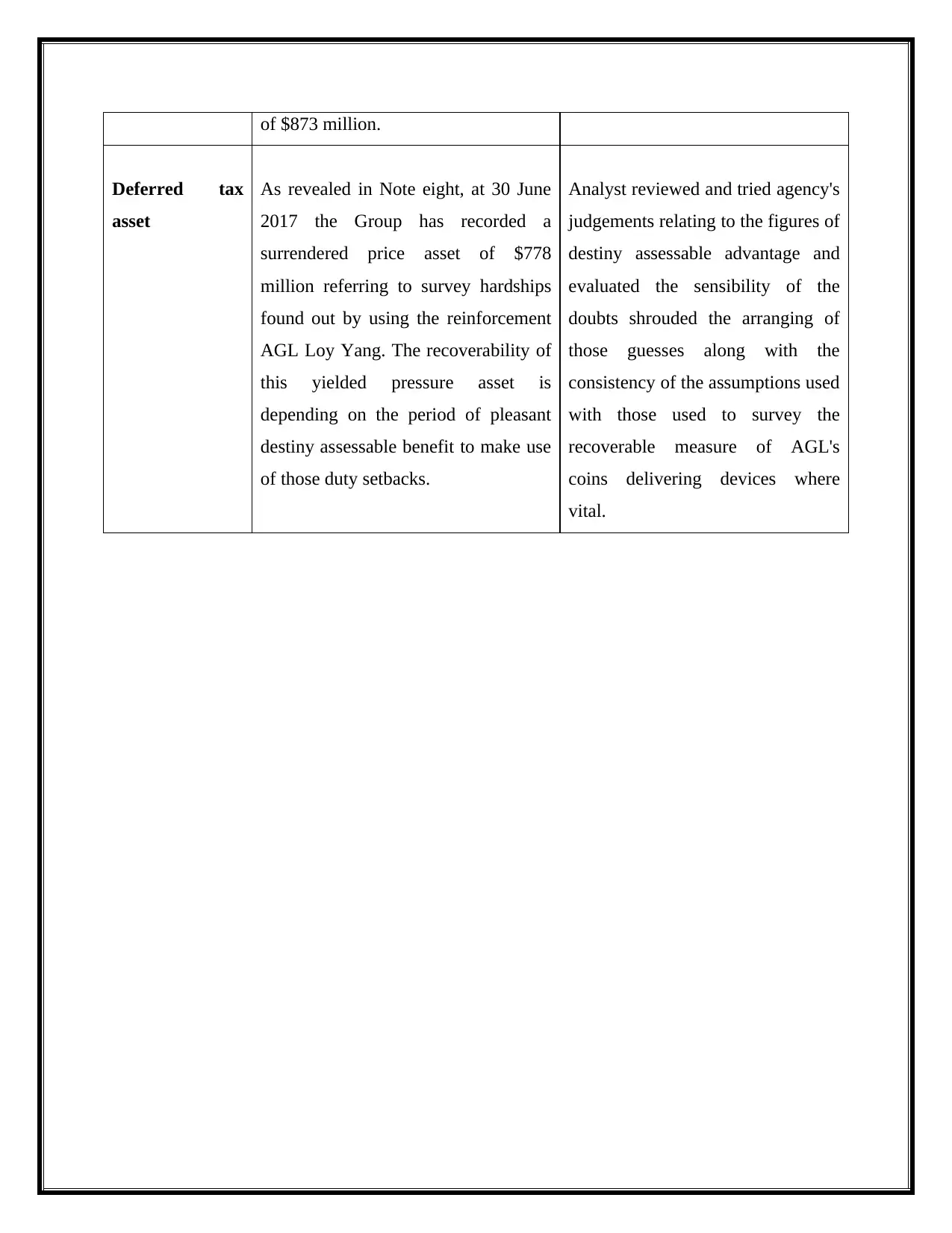

of $873 million.

Deferred tax

asset

As revealed in Note eight, at 30 June

2017 the Group has recorded a

surrendered price asset of $778

million referring to survey hardships

found out by using the reinforcement

AGL Loy Yang. The recoverability of

this yielded pressure asset is

depending on the period of pleasant

destiny assessable benefit to make use

of those duty setbacks.

Analyst reviewed and tried agency's

judgements relating to the figures of

destiny assessable advantage and

evaluated the sensibility of the

doubts shrouded the arranging of

those guesses along with the

consistency of the assumptions used

with those used to survey the

recoverable measure of AGL's

coins delivering devices where

vital.

Deferred tax

asset

As revealed in Note eight, at 30 June

2017 the Group has recorded a

surrendered price asset of $778

million referring to survey hardships

found out by using the reinforcement

AGL Loy Yang. The recoverability of

this yielded pressure asset is

depending on the period of pleasant

destiny assessable benefit to make use

of those duty setbacks.

Analyst reviewed and tried agency's

judgements relating to the figures of

destiny assessable advantage and

evaluated the sensibility of the

doubts shrouded the arranging of

those guesses along with the

consistency of the assumptions used

with those used to survey the

recoverable measure of AGL's

coins delivering devices where

vital.

Acacia Coal Limited:

Following Key Auditing Matters are disclosed by the Auditor of Acacia Coal Limited in

auditor’s report of 2017.

Key matters:

The Group holds a non-current asset held accessible to be sold regarded at $750,000 talking to a

fundamental phase (40. %) of the company's total belongings.

The appraisal of the recoverable measure of this advantage is depending on the getting

substance's ability to obtain posting on the ASX and their potential to elevate enough resources

from which to assist the favourable position obtaining.

The evaluation of the recoverable measure of this preferred point of view calls for excellent

judgment as for recognizing the parts to assure utilize and perceiving recommendations of

inability.

Actions performed by the auditor:

The auditor gets a awareness of the important thing controls associated with the game plan of the

valuation models used to overview the recoverable degree of the Group's held on hand to be

received property. Outside attestation took through the Auditor approximately the predominant

mining loft is held via the Group as at modifying date. Auditor coordinates a evaluation of ASX

releases on 29 September 2017 concerning the offer of the noncurrent asset held reachable to be

acquired. Analyst in like way coordinated an exam of contracts as for the pending asset bargain

for signs supporting the passing on satisfactory and appropriateness of the collection of the

favoured point of view.

Following Key Auditing Matters are disclosed by the Auditor of Acacia Coal Limited in

auditor’s report of 2017.

Key matters:

The Group holds a non-current asset held accessible to be sold regarded at $750,000 talking to a

fundamental phase (40. %) of the company's total belongings.

The appraisal of the recoverable measure of this advantage is depending on the getting

substance's ability to obtain posting on the ASX and their potential to elevate enough resources

from which to assist the favourable position obtaining.

The evaluation of the recoverable measure of this preferred point of view calls for excellent

judgment as for recognizing the parts to assure utilize and perceiving recommendations of

inability.

Actions performed by the auditor:

The auditor gets a awareness of the important thing controls associated with the game plan of the

valuation models used to overview the recoverable degree of the Group's held on hand to be

received property. Outside attestation took through the Auditor approximately the predominant

mining loft is held via the Group as at modifying date. Auditor coordinates a evaluation of ASX

releases on 29 September 2017 concerning the offer of the noncurrent asset held reachable to be

acquired. Analyst in like way coordinated an exam of contracts as for the pending asset bargain

for signs supporting the passing on satisfactory and appropriateness of the collection of the

favoured point of view.

ADX-energy limited: The auditor of ADX Limited informed following points as Key Auditing

matter:

Cash: The Group's cash makes up 92% of general property via regard and is thought to be the

important thing driver of the Group's assignments and exam works out. We don't see cash as at a

high peril of notable blunder, or to be obligated to a huge level of judgment because it is a liquid

asset. In any case in view of the materiality regarding the cash related decrees quite often, Cash

is thought to be the district which had the best effect on our trendy strategy and segment of

benefits in organizing and completing our survey.

Auditor action:

Auditor of the company identified and investigates the internal control on the cash transaction.

Auditor also receives the confirmation from the third party about the cash holdings.

matter:

Cash: The Group's cash makes up 92% of general property via regard and is thought to be the

important thing driver of the Group's assignments and exam works out. We don't see cash as at a

high peril of notable blunder, or to be obligated to a huge level of judgment because it is a liquid

asset. In any case in view of the materiality regarding the cash related decrees quite often, Cash

is thought to be the district which had the best effect on our trendy strategy and segment of

benefits in organizing and completing our survey.

Auditor action:

Auditor of the company identified and investigates the internal control on the cash transaction.

Auditor also receives the confirmation from the third party about the cash holdings.

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

ASA 570 “Going Concern”

This ASA is applicable to those financial statements which are prepared after the December-15-

2018. This standard explains the responsibility of an auditor on the assessment and reporting of

going concern assumption (Feng and Neely, 2017).

Mean of going concern Assumption:

Going concern is an essential hid assumption in accounting. The supposition is that an

association or company will have the capacity to retain operating for a term that is sufficient to

finish its obligations, obligations, targets, and so forth. Toward the day's give up, the affiliation

may not trade or be compelled bankrupt inside a realistic time span.

Management responsibility for going concern assumption: Auditing standard makes

management more responsible to ensure the compliance of going concern assumption. Australian

Accounting Standard AASB 101 elucidates that management will make an examination of a

substance's ability to retain as a going concern (Berglund, 2015). The factor through guide

necessities with deference toward business enterprise's responsibility to assess the thing's ability

to continue as a going challenge and related cash related assertion disclosures can also in like

manner be set out in law or control.

Corporation act 2001 also describes a formal liability of management to give a clarification

about the going concern ability. This clarification is also a part of financial reporting to ensure

quality reporting.

The responsibility of auditor for going concern:

The commitments of evaluator are to get sufficient becoming audit confirm as for, and close on,

the appropriateness of employer's usage of the going problem introduce of accounting in the

arranging of the budgetary record, and to complete, in attitude of the survey demonstrate

procured, paying little heed to whether a material helplessness exists approximately the

substance's ability to keep as a going concern (Chen, 2016). These commitments exist paying

little appreciate to whether the economic maintaining framework used as a bit of the practice of

the cash related record excludes an unequivocal important for an organization to make a specific

evaluation of the substance's capacity to retain as a going issue.

This ASA is applicable to those financial statements which are prepared after the December-15-

2018. This standard explains the responsibility of an auditor on the assessment and reporting of

going concern assumption (Feng and Neely, 2017).

Mean of going concern Assumption:

Going concern is an essential hid assumption in accounting. The supposition is that an

association or company will have the capacity to retain operating for a term that is sufficient to

finish its obligations, obligations, targets, and so forth. Toward the day's give up, the affiliation

may not trade or be compelled bankrupt inside a realistic time span.

Management responsibility for going concern assumption: Auditing standard makes

management more responsible to ensure the compliance of going concern assumption. Australian

Accounting Standard AASB 101 elucidates that management will make an examination of a

substance's ability to retain as a going concern (Berglund, 2015). The factor through guide

necessities with deference toward business enterprise's responsibility to assess the thing's ability

to continue as a going challenge and related cash related assertion disclosures can also in like

manner be set out in law or control.

Corporation act 2001 also describes a formal liability of management to give a clarification

about the going concern ability. This clarification is also a part of financial reporting to ensure

quality reporting.

The responsibility of auditor for going concern:

The commitments of evaluator are to get sufficient becoming audit confirm as for, and close on,

the appropriateness of employer's usage of the going problem introduce of accounting in the

arranging of the budgetary record, and to complete, in attitude of the survey demonstrate

procured, paying little heed to whether a material helplessness exists approximately the

substance's ability to keep as a going concern (Chen, 2016). These commitments exist paying

little appreciate to whether the economic maintaining framework used as a bit of the practice of

the cash related record excludes an unequivocal important for an organization to make a specific

evaluation of the substance's capacity to retain as a going issue.

ASA 2002 additionally gives basic elucidation about the identical. ASA 2002 depicts the ability

consequences of intrinsic boundaries at the analyst's potential to understand material

misrepresentations are more imperative for destiny events or situations which can have an impact

on a substance to stop to preserve as a going situation (Read, 2015). The controller cannot

suspect such future events or conditions. In like manner, the nonattendance of any connection

with a cloth weak point approximately the substance's ability to keep as a going strain in a

commentator's document cannot be viewed as an accreditation with appreciate to the element's

capacity to continue as a going challenge.

Some examples of ASA 570 “Going concern” discloser:

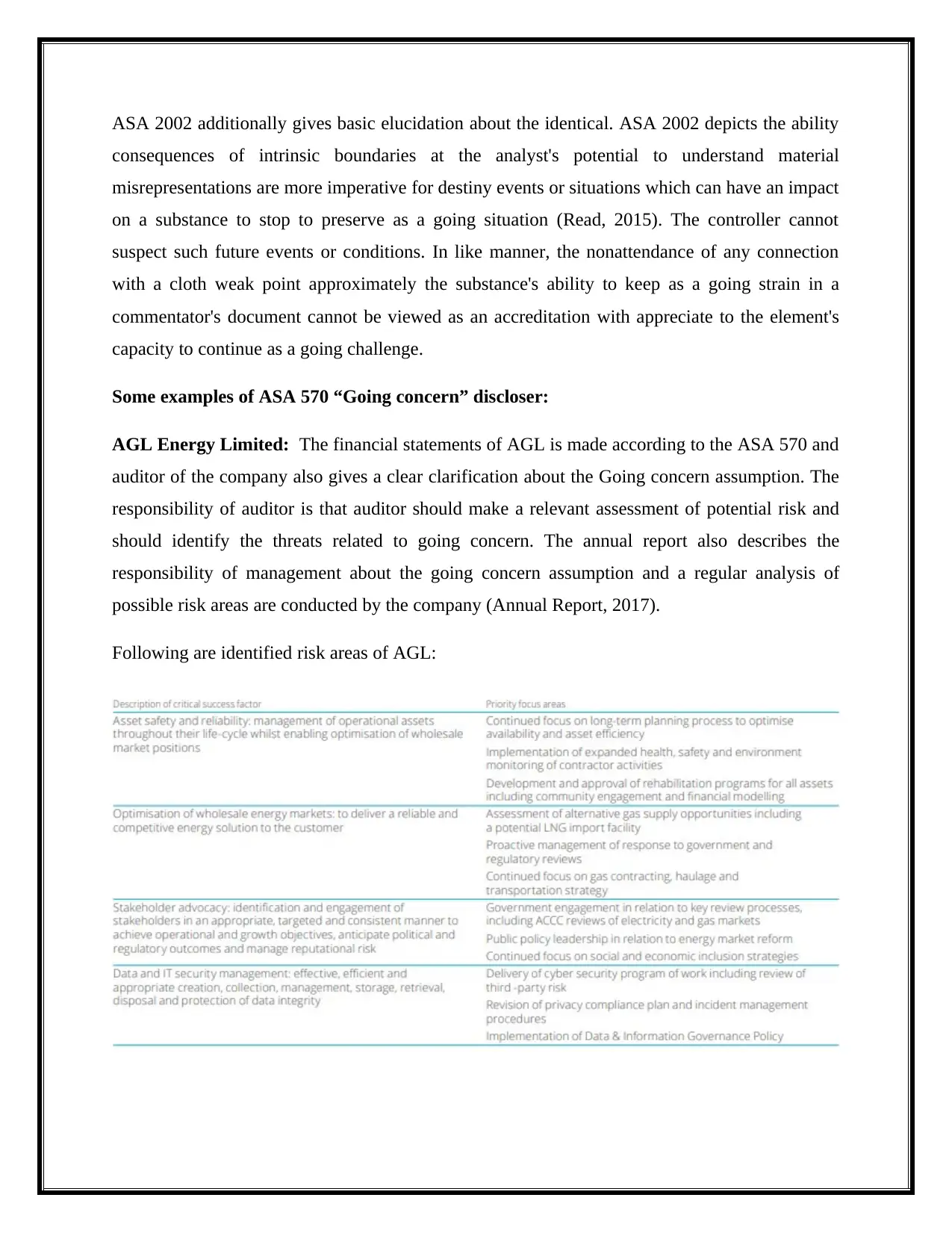

AGL Energy Limited: The financial statements of AGL is made according to the ASA 570 and

auditor of the company also gives a clear clarification about the Going concern assumption. The

responsibility of auditor is that auditor should make a relevant assessment of potential risk and

should identify the threats related to going concern. The annual report also describes the

responsibility of management about the going concern assumption and a regular analysis of

possible risk areas are conducted by the company (Annual Report, 2017).

Following are identified risk areas of AGL:

consequences of intrinsic boundaries at the analyst's potential to understand material

misrepresentations are more imperative for destiny events or situations which can have an impact

on a substance to stop to preserve as a going situation (Read, 2015). The controller cannot

suspect such future events or conditions. In like manner, the nonattendance of any connection

with a cloth weak point approximately the substance's ability to keep as a going strain in a

commentator's document cannot be viewed as an accreditation with appreciate to the element's

capacity to continue as a going challenge.

Some examples of ASA 570 “Going concern” discloser:

AGL Energy Limited: The financial statements of AGL is made according to the ASA 570 and

auditor of the company also gives a clear clarification about the Going concern assumption. The

responsibility of auditor is that auditor should make a relevant assessment of potential risk and

should identify the threats related to going concern. The annual report also describes the

responsibility of management about the going concern assumption and a regular analysis of

possible risk areas are conducted by the company (Annual Report, 2017).

Following are identified risk areas of AGL:

ADX-energy limited: going concern status of ADX Limited is as follows:

The budgetary variables have been set up on the possibility that the Company will hang on

meeting its duties and may on this way proceed with ordinary business undertaking practices and

famous resources and settle liabilities inside the typical course of business. As an examination

gathering, the Company and its controlled elements don't make cash streams from their working

games to bring down back these physical exercises. As a final product, the capacity of the

Company to continue as a going circumstance is hard to the satisfaction of capital hoisting guide,

far mounts of endeavours or diverse financing openings. The Directors assume that the Company

will proceed as a going concern. Along these lines, the financial data has been introduced on a

going circumstance start (Annual Report, 2017). At any rate, should hoist help, some separation

mounts or any non-required financing openings be unsuccessful, the Company will most likely

be not able to continue as a going subject.

The budgetary variables have been set up on the possibility that the Company will hang on

meeting its duties and may on this way proceed with ordinary business undertaking practices and

famous resources and settle liabilities inside the typical course of business. As an examination

gathering, the Company and its controlled elements don't make cash streams from their working

games to bring down back these physical exercises. As a final product, the capacity of the

Company to continue as a going circumstance is hard to the satisfaction of capital hoisting guide,

far mounts of endeavours or diverse financing openings. The Directors assume that the Company

will proceed as a going concern. Along these lines, the financial data has been introduced on a

going circumstance start (Annual Report, 2017). At any rate, should hoist help, some separation

mounts or any non-required financing openings be unsuccessful, the Company will most likely

be not able to continue as a going subject.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

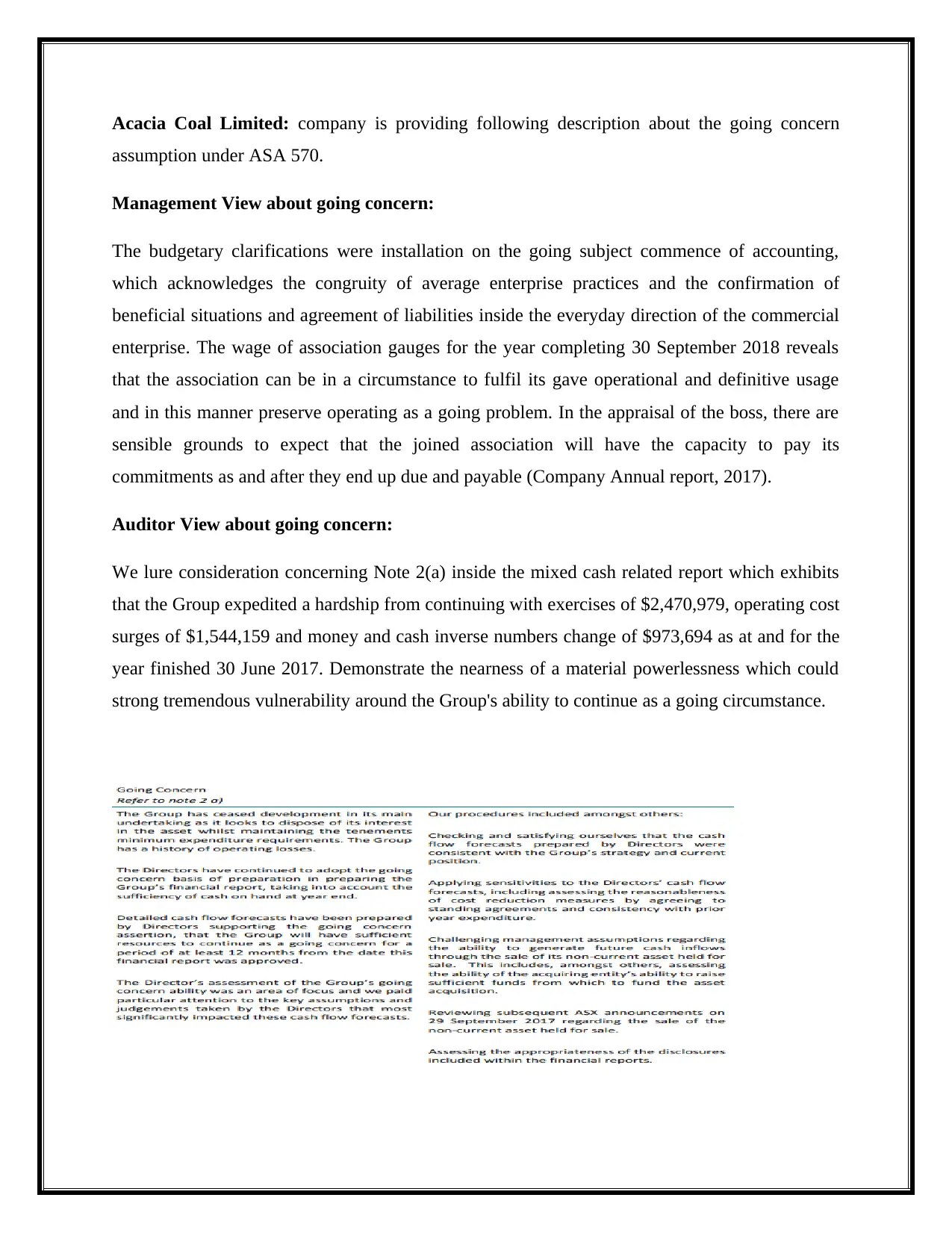

Acacia Coal Limited: company is providing following description about the going concern

assumption under ASA 570.

Management View about going concern:

The budgetary clarifications were installation on the going subject commence of accounting,

which acknowledges the congruity of average enterprise practices and the confirmation of

beneficial situations and agreement of liabilities inside the everyday direction of the commercial

enterprise. The wage of association gauges for the year completing 30 September 2018 reveals

that the association can be in a circumstance to fulfil its gave operational and definitive usage

and in this manner preserve operating as a going problem. In the appraisal of the boss, there are

sensible grounds to expect that the joined association will have the capacity to pay its

commitments as and after they end up due and payable (Company Annual report, 2017).

Auditor View about going concern:

We lure consideration concerning Note 2(a) inside the mixed cash related report which exhibits

that the Group expedited a hardship from continuing with exercises of $2,470,979, operating cost

surges of $1,544,159 and money and cash inverse numbers change of $973,694 as at and for the

year finished 30 June 2017. Demonstrate the nearness of a material powerlessness which could

strong tremendous vulnerability around the Group's ability to continue as a going circumstance.

assumption under ASA 570.

Management View about going concern:

The budgetary clarifications were installation on the going subject commence of accounting,

which acknowledges the congruity of average enterprise practices and the confirmation of

beneficial situations and agreement of liabilities inside the everyday direction of the commercial

enterprise. The wage of association gauges for the year completing 30 September 2018 reveals

that the association can be in a circumstance to fulfil its gave operational and definitive usage

and in this manner preserve operating as a going problem. In the appraisal of the boss, there are

sensible grounds to expect that the joined association will have the capacity to pay its

commitments as and after they end up due and payable (Company Annual report, 2017).

Auditor View about going concern:

We lure consideration concerning Note 2(a) inside the mixed cash related report which exhibits

that the Group expedited a hardship from continuing with exercises of $2,470,979, operating cost

surges of $1,544,159 and money and cash inverse numbers change of $973,694 as at and for the

year finished 30 June 2017. Demonstrate the nearness of a material powerlessness which could

strong tremendous vulnerability around the Group's ability to continue as a going circumstance.

Conclusion:

Auditing standards are very important part of audit process because these are useful for auditor

and user both. On the basis of auditing standard, a user can easily evaluate the opinion of the

auditor, on another hand; auditor can conduct more quality audit as per legal requirements. In the

above-discussed report, auditing standard 701 and 570 is explained and the explanation

concludes that both standards are introduced to make the auditor more responsible for their

opinion. ASA 570 proves that the management is also responsible to investigate and ensure the

going concern assumption in accounting and financial statements. Above report also involves a

discussion about the discloser of key auditing matters and proves that these items are explained

separately in the auditor’s report which is the part of financial statements.

Auditing standards are very important part of audit process because these are useful for auditor

and user both. On the basis of auditing standard, a user can easily evaluate the opinion of the

auditor, on another hand; auditor can conduct more quality audit as per legal requirements. In the

above-discussed report, auditing standard 701 and 570 is explained and the explanation

concludes that both standards are introduced to make the auditor more responsible for their

opinion. ASA 570 proves that the management is also responsible to investigate and ensure the

going concern assumption in accounting and financial statements. Above report also involves a

discussion about the discloser of key auditing matters and proves that these items are explained

separately in the auditor’s report which is the part of financial statements.

References:

1. Bedard, J., Gonthier-Besacier, N. and Schatt, A., 2015. Analysis of the Consequences of

the Disclosure of Key Audit Matters.

2. Motahary, H. and Emami, T., 2016. Key audit matters-the answer?: An exploratory study

investigating auditors possibility to accomplish the purpose of the new audit report.

3. Myers, L.A., Shipman, J.E., Swanquist, Q.T. and Whited, R.L., 2015. Disclosure timing

and the market response to first-time going concern modifications and earnings

announcements. Working paper available at http://papers. ssrn. com/sol3/papers. cfm.

4. Zaher, A.A., 2015. GOING-CONCERN OPINIONS, EXECUTIVE TENURE AND

GENDER. CORPORATE OWNERSHIP & CONTROL, p.19.

5. Myers, L.A., Schmidt, J. and Wilkins, M., 2014. An investigation of recent changes in

going concern reporting decisions among Big N and non-Big N auditors. Review of

Quantitative Finance and Accounting, 43(1), pp.155-172.

6. AASB, 2016. Auditing Standard ASA 570 Going Concern. Available at:

http://www.auasb.gov.au/admin/file/content102/c3/ASA_570_2015.pdf [accessed on 23-

may-2018]

7. Auditing and Assurance Standards Board, 2015. Auditing Standard ASA 701

Communicating Key Audit Matters in the Independent Auditor’s Report. Available at:

http://www.auasb.gov.au/admin/file/content102/c3/ASA_701_2015.pdf [accessed on 23-

may-2018]

8. KPMG, 2014. FASB Issues Going Concern Standard. Available at:

https://www.kpmg.at/uploads/media/FN_DI14_47.pdf [accessed on 23-may-2018]

9. Seyam, A.A. and Brickman, S., 2016. The going concern assumptions and presentation

on financial statements. The Business & Management Review, 7(3), p.241.

10. Feng, N.C. and Neely, D.G., 2017. Going concern disclosure for local governments.

Journal of Public and Nonprofit Affairs, 3(2), pp.176-196.

11. IISB, 2015. Auditor Reporting – Key Audit Matters. Available at:

https://www.ifac.org/system/files/meetings/files/Supplement_to_Agenda_Item_D_Audito

r-Reporting-Key_Audit_Matters-final.pdf [accessed on 23-may-2018]

12. Australian National Audit Office, 2015. Audits of the Financial Statements of Australian

Government Entities for the Period Ended 30 June 2015. Available at:

1. Bedard, J., Gonthier-Besacier, N. and Schatt, A., 2015. Analysis of the Consequences of

the Disclosure of Key Audit Matters.

2. Motahary, H. and Emami, T., 2016. Key audit matters-the answer?: An exploratory study

investigating auditors possibility to accomplish the purpose of the new audit report.

3. Myers, L.A., Shipman, J.E., Swanquist, Q.T. and Whited, R.L., 2015. Disclosure timing

and the market response to first-time going concern modifications and earnings

announcements. Working paper available at http://papers. ssrn. com/sol3/papers. cfm.

4. Zaher, A.A., 2015. GOING-CONCERN OPINIONS, EXECUTIVE TENURE AND

GENDER. CORPORATE OWNERSHIP & CONTROL, p.19.

5. Myers, L.A., Schmidt, J. and Wilkins, M., 2014. An investigation of recent changes in

going concern reporting decisions among Big N and non-Big N auditors. Review of

Quantitative Finance and Accounting, 43(1), pp.155-172.

6. AASB, 2016. Auditing Standard ASA 570 Going Concern. Available at:

http://www.auasb.gov.au/admin/file/content102/c3/ASA_570_2015.pdf [accessed on 23-

may-2018]

7. Auditing and Assurance Standards Board, 2015. Auditing Standard ASA 701

Communicating Key Audit Matters in the Independent Auditor’s Report. Available at:

http://www.auasb.gov.au/admin/file/content102/c3/ASA_701_2015.pdf [accessed on 23-

may-2018]

8. KPMG, 2014. FASB Issues Going Concern Standard. Available at:

https://www.kpmg.at/uploads/media/FN_DI14_47.pdf [accessed on 23-may-2018]

9. Seyam, A.A. and Brickman, S., 2016. The going concern assumptions and presentation

on financial statements. The Business & Management Review, 7(3), p.241.

10. Feng, N.C. and Neely, D.G., 2017. Going concern disclosure for local governments.

Journal of Public and Nonprofit Affairs, 3(2), pp.176-196.

11. IISB, 2015. Auditor Reporting – Key Audit Matters. Available at:

https://www.ifac.org/system/files/meetings/files/Supplement_to_Agenda_Item_D_Audito

r-Reporting-Key_Audit_Matters-final.pdf [accessed on 23-may-2018]

12. Australian National Audit Office, 2015. Audits of the Financial Statements of Australian

Government Entities for the Period Ended 30 June 2015. Available at:

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

https://www.anao.gov.au/sites/g/files/net616/f/ANAO_Report_2015-2016_15.pdf

[accessed on 23-may-2018]

13. Kopecká, N., 2016. The IFRS 8 Segment Reporting Disclosure: Evidence on the Czech

Listed Companies. European Financial and Accounting Journal, 2016(2), pp.5-20.

14. Pacter, P., 2016. Pocket Guide to IFRS Standards: the global financial reporting

language. IFRS Foundation.

15. Berglund, N.R., 2015. Managerial ability and the going concern opinion (Doctoral

dissertation, Oklahoma State University).

16. Noori, T.M. and Rashid, C.A., 2017. EXTERNAL AUDITOR’S RESPONSIBILITY

REGARDYING TO GOING CONCERN ASSUMPTION IN HIS/HERS REPORT:

CASE OF KURDISTAN REGION/IRAQ.

17. Chen, P.F., He, S., Ma, Z. and Stice, D., 2016. The information role of audit opinions in

debt contracting. Journal of Accounting and Economics, 61(1), pp.121-144.

18. Read, W.J., 2015. Auditor Fees and Going-Concern Reporting Decisions on Bankrupt

Companies: Additional Evidence. Current Issues in Auditing, 9(1), pp.A13-A27.

[accessed on 23-may-2018]

13. Kopecká, N., 2016. The IFRS 8 Segment Reporting Disclosure: Evidence on the Czech

Listed Companies. European Financial and Accounting Journal, 2016(2), pp.5-20.

14. Pacter, P., 2016. Pocket Guide to IFRS Standards: the global financial reporting

language. IFRS Foundation.

15. Berglund, N.R., 2015. Managerial ability and the going concern opinion (Doctoral

dissertation, Oklahoma State University).

16. Noori, T.M. and Rashid, C.A., 2017. EXTERNAL AUDITOR’S RESPONSIBILITY

REGARDYING TO GOING CONCERN ASSUMPTION IN HIS/HERS REPORT:

CASE OF KURDISTAN REGION/IRAQ.

17. Chen, P.F., He, S., Ma, Z. and Stice, D., 2016. The information role of audit opinions in

debt contracting. Journal of Accounting and Economics, 61(1), pp.121-144.

18. Read, W.J., 2015. Auditor Fees and Going-Concern Reporting Decisions on Bankrupt

Companies: Additional Evidence. Current Issues in Auditing, 9(1), pp.A13-A27.

1 out of 17

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.