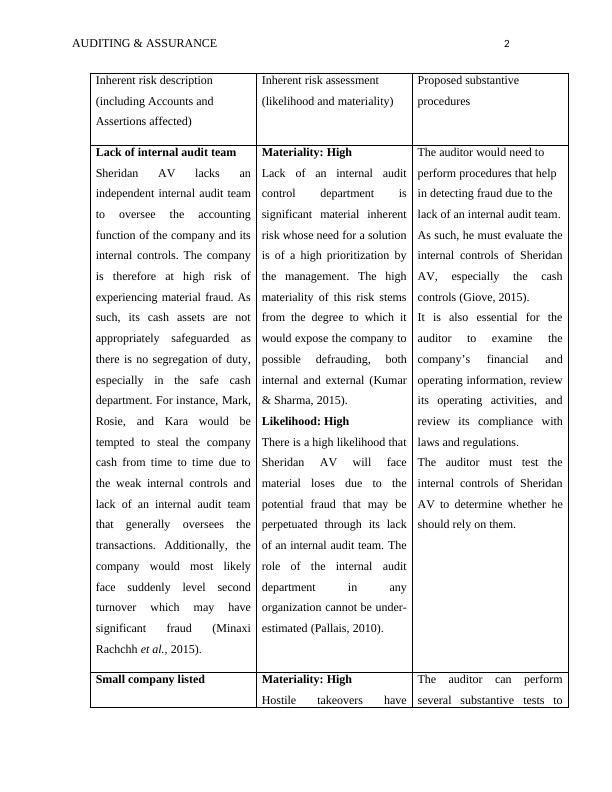

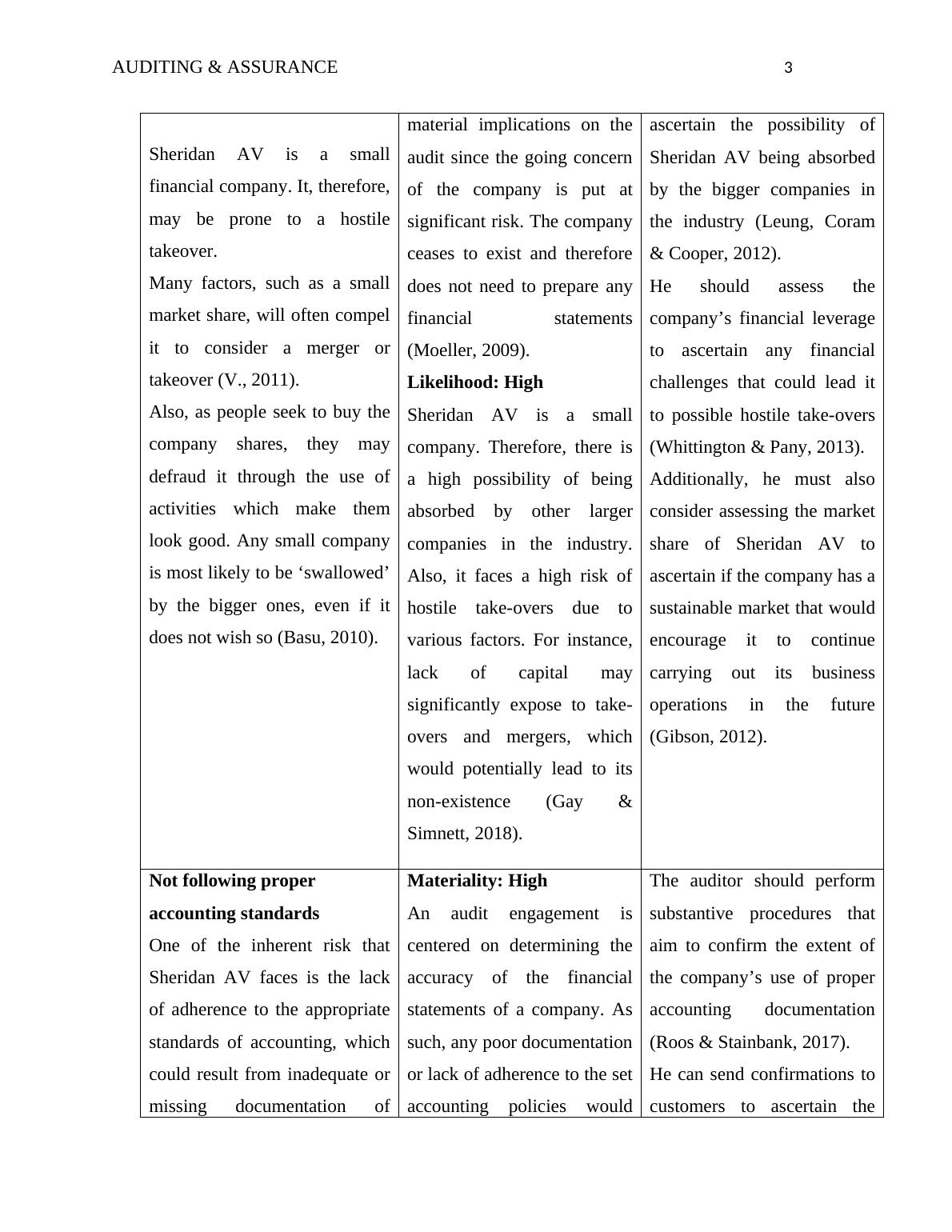

Inherent Risk in Auditing & Assurance

This assignment is designed to facilitate learning of key skills and knowledge needed for a financial report audit of a company, using the case study of Sheridan AV.

6 Pages1195 Words379 Views

Added on 2023-04-08

About This Document

This article discusses the inherent risks in auditing and assurance, including lack of internal audit team, hostile takeovers, and non-adherence to accounting standards. It also provides recommendations for auditors to mitigate these risks.

Inherent Risk in Auditing & Assurance

This assignment is designed to facilitate learning of key skills and knowledge needed for a financial report audit of a company, using the case study of Sheridan AV.

Added on 2023-04-08

ShareRelated Documents

End of preview

Want to access all the pages? Upload your documents or become a member.

Sheridan AV Case Study 13

|14

|3570

|212

Acct1059 Letter to Sheridan AV 2022

|13

|3363

|14

HI6026 Report | Audit, Assurance and Compliance

|9

|2366

|148

Importance of Risk Assessment in DIPL : Case Study

|13

|2335

|71

Audit Theory and Assurance | Project Report

|8

|1562

|29

IT Audit & Control TABLE OF CONTENTS

|7

|1531

|168