Auditing

VerifiedAdded on 2023/03/30

|19

|3004

|344

AI Summary

This document provides an overview of auditing and assurance standards in New Zealand. It discusses the political, economic, social, and technological factors affecting a company's operations. It also assesses the risk in an audit and analyzes the financial statements of a company.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Running head: AUDITING

Auditing

Name of the Student:

Name of the University:

Authors Note:

Auditing

Name of the Student:

Name of the University:

Authors Note:

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

1

AUDITING

Contents

Introduction:....................................................................................................................................2

Part A:..............................................................................................................................................2

Part B:............................................................................................................................................14

Part C:............................................................................................................................................15

Conclusion:....................................................................................................................................15

References:....................................................................................................................................17

AUDITING

Contents

Introduction:....................................................................................................................................2

Part A:..............................................................................................................................................2

Part B:............................................................................................................................................14

Part C:............................................................................................................................................15

Conclusion:....................................................................................................................................15

References:....................................................................................................................................17

2

AUDITING

Introduction:

External Reporting Board (XRB) is the highest authoritative body in New Zealand to regulate

and control the auditing related requirements in the country for business and non-business

organizations. XRB has set the framework for auditing and assurance standards in the country.

Auditors and professional accountants have to comply with these standards on auditing and

assurance issued by XRB to discharge their responsibilities properly. Auditing of financial

reports of companies operating in the country shall be governed by these standards. Thus, the

auditors given responsibility to conduct audit of financial statements of an entity in the country

must comply with the auditing and assurance standards framework of XRB to carry out an

effective audit.

Part A:

Sub part a:

In order to perform a strategic business risk assessment of Lucy’s Quality Food Limited (LQFL)

and to understand the ability of the company to deal with ever changing working atmosphere and

environment in general, PEST analysis on the company is carried out here.

AUDITING

Introduction:

External Reporting Board (XRB) is the highest authoritative body in New Zealand to regulate

and control the auditing related requirements in the country for business and non-business

organizations. XRB has set the framework for auditing and assurance standards in the country.

Auditors and professional accountants have to comply with these standards on auditing and

assurance issued by XRB to discharge their responsibilities properly. Auditing of financial

reports of companies operating in the country shall be governed by these standards. Thus, the

auditors given responsibility to conduct audit of financial statements of an entity in the country

must comply with the auditing and assurance standards framework of XRB to carry out an

effective audit.

Part A:

Sub part a:

In order to perform a strategic business risk assessment of Lucy’s Quality Food Limited (LQFL)

and to understand the ability of the company to deal with ever changing working atmosphere and

environment in general, PEST analysis on the company is carried out here.

3

AUDITING

Political factors:

The company, i.e. LQFL is based in New Zealand and operates in the domestic market only.

Considering the stable political establishment in the country it can be stated that there is

absolutely no imminent political risk to the company and its operations. However, the company

is looking to expand its business beyond the domestic market and is looking to expand its

operations to the neighbouring country Australia. In this regard it is important that the company

considers the possible risks and implications of investing in Australia. From political point of

view there is again nothing to be afraid of as Australia also has a stable political establishment

(Suthan, 2007).

Economic factors:

New Zealand economy has been growing at a steady pace over the last decade and more. The

economy has shown no sign of slowing down and hence, there is no threat of economic

slowdown in the near future adversely affecting the company and its operations. In addition,

AUDITING

Political factors:

The company, i.e. LQFL is based in New Zealand and operates in the domestic market only.

Considering the stable political establishment in the country it can be stated that there is

absolutely no imminent political risk to the company and its operations. However, the company

is looking to expand its business beyond the domestic market and is looking to expand its

operations to the neighbouring country Australia. In this regard it is important that the company

considers the possible risks and implications of investing in Australia. From political point of

view there is again nothing to be afraid of as Australia also has a stable political establishment

(Suthan, 2007).

Economic factors:

New Zealand economy has been growing at a steady pace over the last decade and more. The

economy has shown no sign of slowing down and hence, there is no threat of economic

slowdown in the near future adversely affecting the company and its operations. In addition,

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

4

AUDITING

Australia provides a huge market to the company if it decides to expand its business and start

operations in Australia. Thus, both the existing market as well as the proposed market are

economically strong markets providing substantial business opportunity to the company.

However, the autocratic decision making system within the company is certainly a weakness to

the company and its strategy to deal with any changes in the economic factors. The rigidity in the

decision making system with on person trying to control everything is not in favour of the

company and is definitely a detriment to the ability of the company to respond to changes in

economic environment within the country and outside where the company operates or will

operate in the future ("The New Requirements of State Audit Rose from Political Economic and

Social Development", 2012).

Social factors:

Social factors are the factors present in the society that affects the functioning of an organization.

These include social environment, working culture in a country, the business atmosphere in

general, the administrative system in the country and other such factors which are beyond the

control of an organization but have significant effect on the functioning of an organization. The

company must have a proper strategy in place to deal with social changes whenever such

changes occur in the country. At present the company seems quite unprepared to cope with

sudden changes in social environment as it lacks a cooperative environment within the

organization to deal with such eventualities swiftly (Van Linden & Hardies, 2018).

Technological factors:

AUDITING

Australia provides a huge market to the company if it decides to expand its business and start

operations in Australia. Thus, both the existing market as well as the proposed market are

economically strong markets providing substantial business opportunity to the company.

However, the autocratic decision making system within the company is certainly a weakness to

the company and its strategy to deal with any changes in the economic factors. The rigidity in the

decision making system with on person trying to control everything is not in favour of the

company and is definitely a detriment to the ability of the company to respond to changes in

economic environment within the country and outside where the company operates or will

operate in the future ("The New Requirements of State Audit Rose from Political Economic and

Social Development", 2012).

Social factors:

Social factors are the factors present in the society that affects the functioning of an organization.

These include social environment, working culture in a country, the business atmosphere in

general, the administrative system in the country and other such factors which are beyond the

control of an organization but have significant effect on the functioning of an organization. The

company must have a proper strategy in place to deal with social changes whenever such

changes occur in the country. At present the company seems quite unprepared to cope with

sudden changes in social environment as it lacks a cooperative environment within the

organization to deal with such eventualities swiftly (Van Linden & Hardies, 2018).

Technological factors:

5

AUDITING

The company sells food products to food retail stores and should look to improve its products by

using advance technology. The company operates in New Zealand that provides significant

scope to use technological advancement and growth to improve its product quality.

The existing political, economic, social and technological environment in New Zealand certainly

allow business organizations such as LQFL to grow and expand its operations significantly as all

the factors are in favour of a business organization and its growth in the country. However, the

ability of LQFL to use these opportunities to grow in the future is certainly questionable

considering its operating style (서서서 & Junesun Choi, 2010).

Sub part b:

In order to assess the risk in an audit it is important to understand the entity and its environment.

Assessing the internal controls within the organization and their effectiveness is important to

determine the overall audit risk for an organization.

LQFL is involved in sourcing and supplying of food ingredients in New Zealand. After a focused

marketing and promotional strategy the company has become the market leader in the boutique

food and beverage industry in last two years. The company is controlled and operated in an

autocratic manner by Lucy Elkington (Accounting, auditing and governance standards for

Islamic financial institutions, 2010). The company is looking to expand its business by selling its

products in markets across Australia. The company though maintains perpetual inventory system

but fails to conduct stock taking at the end of each month. In fact the company only carries out

stock taking once at the end of each quarter. The primary evolution of internal control shows that

these are not strong in case of certain transactions.

AUDITING

The company sells food products to food retail stores and should look to improve its products by

using advance technology. The company operates in New Zealand that provides significant

scope to use technological advancement and growth to improve its product quality.

The existing political, economic, social and technological environment in New Zealand certainly

allow business organizations such as LQFL to grow and expand its operations significantly as all

the factors are in favour of a business organization and its growth in the country. However, the

ability of LQFL to use these opportunities to grow in the future is certainly questionable

considering its operating style (서서서 & Junesun Choi, 2010).

Sub part b:

In order to assess the risk in an audit it is important to understand the entity and its environment.

Assessing the internal controls within the organization and their effectiveness is important to

determine the overall audit risk for an organization.

LQFL is involved in sourcing and supplying of food ingredients in New Zealand. After a focused

marketing and promotional strategy the company has become the market leader in the boutique

food and beverage industry in last two years. The company is controlled and operated in an

autocratic manner by Lucy Elkington (Accounting, auditing and governance standards for

Islamic financial institutions, 2010). The company is looking to expand its business by selling its

products in markets across Australia. The company though maintains perpetual inventory system

but fails to conduct stock taking at the end of each month. In fact the company only carries out

stock taking once at the end of each quarter. The primary evolution of internal control shows that

these are not strong in case of certain transactions.

6

AUDITING

Thus, considering the above information and preliminary assessment of the company and its

environment the overall audit risk associated with company is certainly not low but it is also not

very high. Thus, the audit risk in case of LQFL is medium especially considering the weak

internal controls for certain class of transactions (Allen & Woodland, 2010).

Sub part c:

Inherent risk:

Inherent risk is the risk of error or omission in financial statements due to no failure of internal

control or humanly error. In case transactions are complex requiring significant judgment and

estimates will be exposed to high degree of inherent risk as opposed to simple transactions. In

case of LQFL, the company is involved in selling food products and ingredients to upmarket

retail stores in all across New Zealand. The company maintains perpetual inventory and takes

stock at the end of each quarter. The company has installed a new computer system in place and

has a relatively experience management team (Armitage, 2008). In addition the internal control

systems are quite efficient except certain class of transactions thus, in totality the inherent risk in

the audit of financial statements of the company is medium. This is mainly because the company

maintains perpetual inventory system and only physically verified its stocks at the end of each

quarter. Thus, there is significant risk in inventory control system along with the risk of internal

control system for certain class of transactions. Hence, the inherent risk in the audit of financial

statements of LQFL is medium.

Sub part d:

The inherent risk in the audit of financial statements of the company has been assessed at

medium. The risk of material misstatement is the risk that the financial statements of an entity

AUDITING

Thus, considering the above information and preliminary assessment of the company and its

environment the overall audit risk associated with company is certainly not low but it is also not

very high. Thus, the audit risk in case of LQFL is medium especially considering the weak

internal controls for certain class of transactions (Allen & Woodland, 2010).

Sub part c:

Inherent risk:

Inherent risk is the risk of error or omission in financial statements due to no failure of internal

control or humanly error. In case transactions are complex requiring significant judgment and

estimates will be exposed to high degree of inherent risk as opposed to simple transactions. In

case of LQFL, the company is involved in selling food products and ingredients to upmarket

retail stores in all across New Zealand. The company maintains perpetual inventory and takes

stock at the end of each quarter. The company has installed a new computer system in place and

has a relatively experience management team (Armitage, 2008). In addition the internal control

systems are quite efficient except certain class of transactions thus, in totality the inherent risk in

the audit of financial statements of the company is medium. This is mainly because the company

maintains perpetual inventory system and only physically verified its stocks at the end of each

quarter. Thus, there is significant risk in inventory control system along with the risk of internal

control system for certain class of transactions. Hence, the inherent risk in the audit of financial

statements of LQFL is medium.

Sub part d:

The inherent risk in the audit of financial statements of the company has been assessed at

medium. The risk of material misstatement is the risk that the financial statements of an entity

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7

AUDITING

contains an error / errors which have not been identified and discovered in the audit of such

financial statements. In case LQFL the risk of material misstatement in the financial statement is

quite low simply because the nature transactions within the entity is not very complex and does

not require significant amount of assumptions and judgments by the management (Asthana,

2012). The company also has a computerised system in place to record financial transactions

thus, reducing the chances of error in recording financial transactions in the books of accounts of

the company. However, the company has installed a new computer system and laid off its two

accounting employees very recently in 2018. Thus, the auditor must assure himself that the

computerized system is effective and correctly records the financial transactions in the books of

accounts of the company. Also the auditor must satisfy himself that the employees using the

computer system to record financial transactions are qualified and capable of handling such

system to record financial transactions properly in the books of accounts of the company.

Thus, the risk of material misstatements in the audit of financial statements of LQFL is quite

low.

Sub part e:

Café revenue has increased from $47,640 of 2018 to $58,048 in 2019. Store revenue has also

increased to $253,366 in 2019 from $249,612 in previous year. Revenue from ready to cook

range has increased to $18,122 in 2018 from $9,328 in 2018. Total revenue of the company in

2019 has increased to $329,536 from $306,580 of previous year. However, in comparison to

revenue the gross profit of the company has not increased proportionately. As compared to gross

profit of $147,448 in 2018 the company has earned $152,480 in 2019. Thus, considering the

increase in revenue in 2019 is $22,956 the increase in gross profit is only $5,032. The net profit

AUDITING

contains an error / errors which have not been identified and discovered in the audit of such

financial statements. In case LQFL the risk of material misstatement in the financial statement is

quite low simply because the nature transactions within the entity is not very complex and does

not require significant amount of assumptions and judgments by the management (Asthana,

2012). The company also has a computerised system in place to record financial transactions

thus, reducing the chances of error in recording financial transactions in the books of accounts of

the company. However, the company has installed a new computer system and laid off its two

accounting employees very recently in 2018. Thus, the auditor must assure himself that the

computerized system is effective and correctly records the financial transactions in the books of

accounts of the company. Also the auditor must satisfy himself that the employees using the

computer system to record financial transactions are qualified and capable of handling such

system to record financial transactions properly in the books of accounts of the company.

Thus, the risk of material misstatements in the audit of financial statements of LQFL is quite

low.

Sub part e:

Café revenue has increased from $47,640 of 2018 to $58,048 in 2019. Store revenue has also

increased to $253,366 in 2019 from $249,612 in previous year. Revenue from ready to cook

range has increased to $18,122 in 2018 from $9,328 in 2018. Total revenue of the company in

2019 has increased to $329,536 from $306,580 of previous year. However, in comparison to

revenue the gross profit of the company has not increased proportionately. As compared to gross

profit of $147,448 in 2018 the company has earned $152,480 in 2019. Thus, considering the

increase in revenue in 2019 is $22,956 the increase in gross profit is only $5,032. The net profit

8

AUDITING

of the company has increased by $7,322 in 2019 to $63,562 as can be seen in the income

statement of the company (Cosserat & Rodda, 2009).

While analysing the Balance sheet of the company the very first thing noticed is the huge

discrepancy in the cash balance of the company. In 2019 the cash balance is $110 as compared to

$37,064 of 2018. The property, plant and equipment has increased by $63,054 in net suggesting

that new additions have been made to PPE in 2019. Creditors have reduced in 20196 suggesting

that payment has been made to the creditors in the current year. Borrowings have stayed the

same in 2019 as it was in 2018 suggesting no additional borrowings have been made in the

current year.

Thus, from the horizontal and vertical analysis of financial statements of the company it is clear

that the company has successfully increased its gross revenue, gross profit and net profit in 2019

as compared to gross revenue, gross profit and net profit of the company of 2018 (Goswami,

2018).

Analytical review:

Profitability ratios:

Particulars 2019 2018

Gross revenue 329,536.00 306,580.00

Gross profit 152,480.00 147,448.00

Gross profit 46.27 48.09

Sales 329,536.00 306,580.00

AUDITING

of the company has increased by $7,322 in 2019 to $63,562 as can be seen in the income

statement of the company (Cosserat & Rodda, 2009).

While analysing the Balance sheet of the company the very first thing noticed is the huge

discrepancy in the cash balance of the company. In 2019 the cash balance is $110 as compared to

$37,064 of 2018. The property, plant and equipment has increased by $63,054 in net suggesting

that new additions have been made to PPE in 2019. Creditors have reduced in 20196 suggesting

that payment has been made to the creditors in the current year. Borrowings have stayed the

same in 2019 as it was in 2018 suggesting no additional borrowings have been made in the

current year.

Thus, from the horizontal and vertical analysis of financial statements of the company it is clear

that the company has successfully increased its gross revenue, gross profit and net profit in 2019

as compared to gross revenue, gross profit and net profit of the company of 2018 (Goswami,

2018).

Analytical review:

Profitability ratios:

Particulars 2019 2018

Gross revenue 329,536.00 306,580.00

Gross profit 152,480.00 147,448.00

Gross profit 46.27 48.09

Sales 329,536.00 306,580.00

9

AUDITING

Net profit 63,562.00 56,240.00

Net profit ratio 19.29 18.34

Gross profit ratio has decreased to 46.27% in 2019 from 48.09% in 2018. However, the net profit

margin has increased to 19.29% in 2019 as compared to 18.34% in 2018. The reason for

decrease in gross profit margin is the increase in cost of sales whereas the net profit ratio has

increased in 2019 due to increase in efficiency of the company (Gray, Manson & Crawford,

2015).

Liquidity ratios:

Particulars 2019 2018

Total current assets 290,13

8.00

316,394.00

Total current liabilities 269,99

2.00

296,794.00

Current ratio 1.

0746

1.0660

AUDITING

Net profit 63,562.00 56,240.00

Net profit ratio 19.29 18.34

Gross profit ratio has decreased to 46.27% in 2019 from 48.09% in 2018. However, the net profit

margin has increased to 19.29% in 2019 as compared to 18.34% in 2018. The reason for

decrease in gross profit margin is the increase in cost of sales whereas the net profit ratio has

increased in 2019 due to increase in efficiency of the company (Gray, Manson & Crawford,

2015).

Liquidity ratios:

Particulars 2019 2018

Total current assets 290,13

8.00

316,394.00

Total current liabilities 269,99

2.00

296,794.00

Current ratio 1.

0746

1.0660

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

10

AUDITING

Current ratio 1.0746: 1 in 2019 as compared to 1.0660: 1 in 2018, thus, the ability of the

company to repay its current liabilities by using current assets of the company.

2019 2018

Acid test ratio

Current assets less inventories 134,9

68.00

161,754

.00

Total current liabilities 269,9

92.00

296,794

.00

Acid test ratio 0

.4999

0.

5450

Acid test ratio in 2019 is 0.4999 compared to 0.5450 of 2018 indicates improvement in the

ability of the company to repay its current liabilities from current assets less current inventories.

Solvency ratios:

Particulars 2019 2018

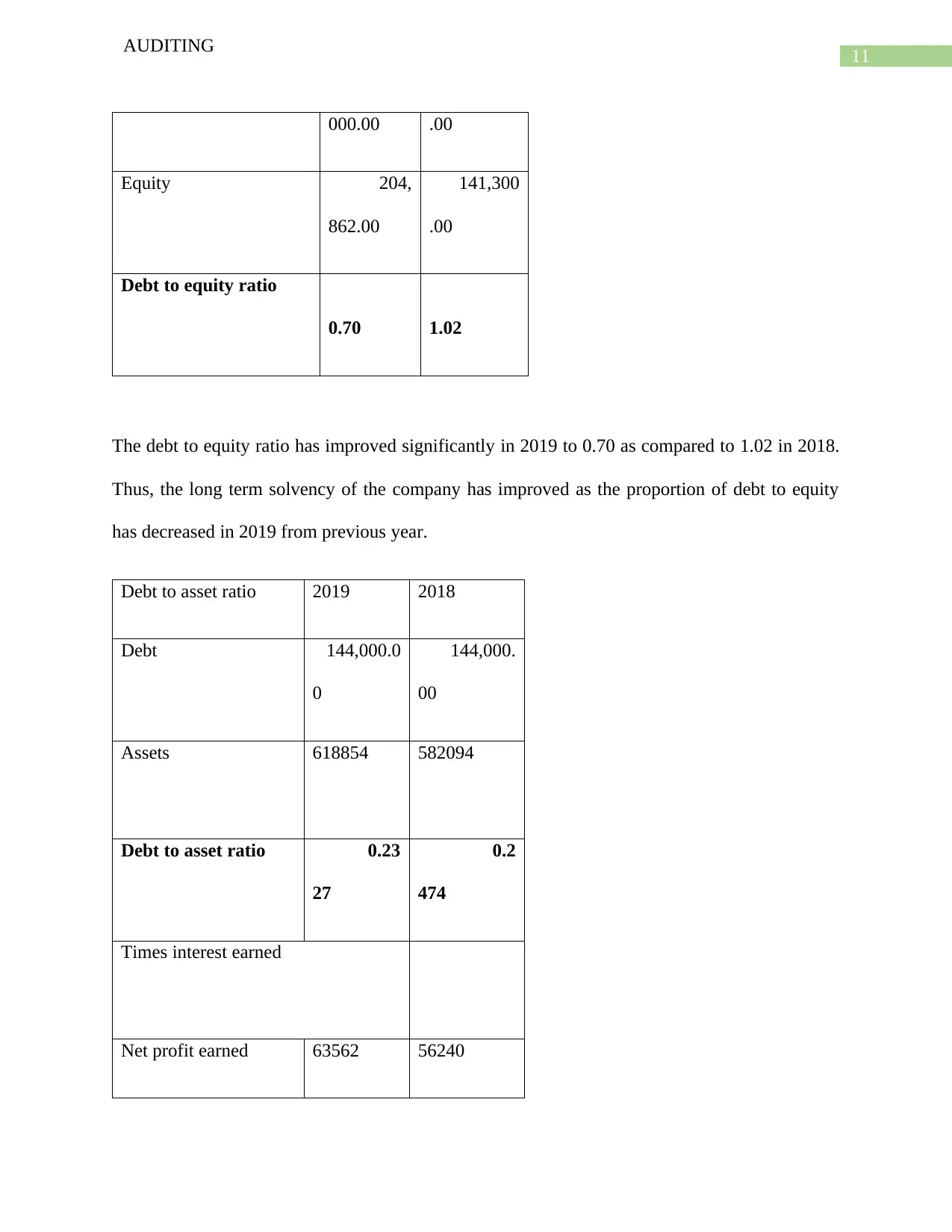

Debt to equity ratio

Debt 144, 144,000

AUDITING

Current ratio 1.0746: 1 in 2019 as compared to 1.0660: 1 in 2018, thus, the ability of the

company to repay its current liabilities by using current assets of the company.

2019 2018

Acid test ratio

Current assets less inventories 134,9

68.00

161,754

.00

Total current liabilities 269,9

92.00

296,794

.00

Acid test ratio 0

.4999

0.

5450

Acid test ratio in 2019 is 0.4999 compared to 0.5450 of 2018 indicates improvement in the

ability of the company to repay its current liabilities from current assets less current inventories.

Solvency ratios:

Particulars 2019 2018

Debt to equity ratio

Debt 144, 144,000

11

AUDITING

000.00 .00

Equity 204,

862.00

141,300

.00

Debt to equity ratio

0.70 1.02

The debt to equity ratio has improved significantly in 2019 to 0.70 as compared to 1.02 in 2018.

Thus, the long term solvency of the company has improved as the proportion of debt to equity

has decreased in 2019 from previous year.

Debt to asset ratio 2019 2018

Debt 144,000.0

0

144,000.

00

Assets 618854 582094

Debt to asset ratio 0.23

27

0.2

474

Times interest earned

Net profit earned 63562 56240

AUDITING

000.00 .00

Equity 204,

862.00

141,300

.00

Debt to equity ratio

0.70 1.02

The debt to equity ratio has improved significantly in 2019 to 0.70 as compared to 1.02 in 2018.

Thus, the long term solvency of the company has improved as the proportion of debt to equity

has decreased in 2019 from previous year.

Debt to asset ratio 2019 2018

Debt 144,000.0

0

144,000.

00

Assets 618854 582094

Debt to asset ratio 0.23

27

0.2

474

Times interest earned

Net profit earned 63562 56240

12

AUDITING

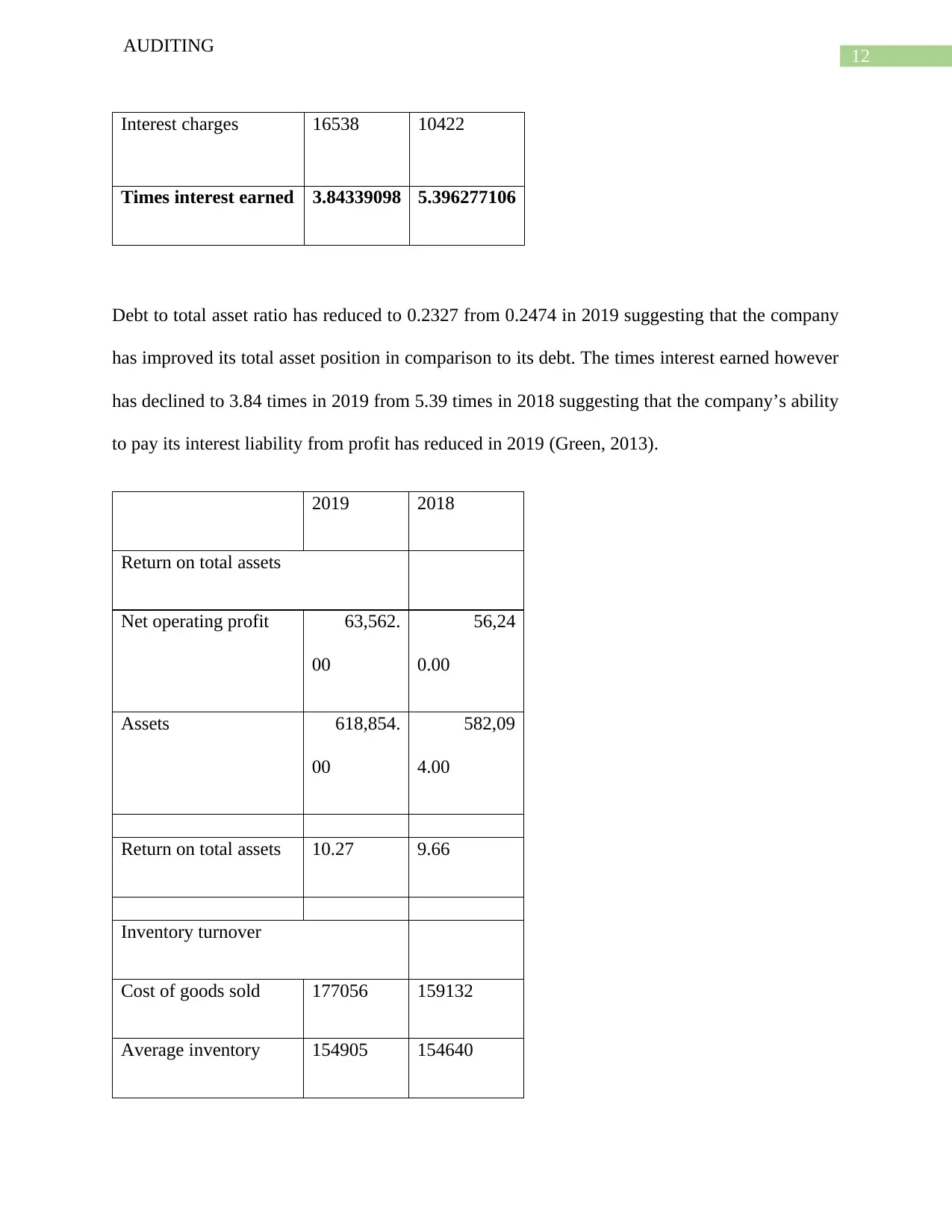

Interest charges 16538 10422

Times interest earned 3.84339098 5.396277106

Debt to total asset ratio has reduced to 0.2327 from 0.2474 in 2019 suggesting that the company

has improved its total asset position in comparison to its debt. The times interest earned however

has declined to 3.84 times in 2019 from 5.39 times in 2018 suggesting that the company’s ability

to pay its interest liability from profit has reduced in 2019 (Green, 2013).

2019 2018

Return on total assets

Net operating profit 63,562.

00

56,24

0.00

Assets 618,854.

00

582,09

4.00

Return on total assets 10.27 9.66

Inventory turnover

Cost of goods sold 177056 159132

Average inventory 154905 154640

AUDITING

Interest charges 16538 10422

Times interest earned 3.84339098 5.396277106

Debt to total asset ratio has reduced to 0.2327 from 0.2474 in 2019 suggesting that the company

has improved its total asset position in comparison to its debt. The times interest earned however

has declined to 3.84 times in 2019 from 5.39 times in 2018 suggesting that the company’s ability

to pay its interest liability from profit has reduced in 2019 (Green, 2013).

2019 2018

Return on total assets

Net operating profit 63,562.

00

56,24

0.00

Assets 618,854.

00

582,09

4.00

Return on total assets 10.27 9.66

Inventory turnover

Cost of goods sold 177056 159132

Average inventory 154905 154640

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

13

AUDITING

Inventory turnover 1.143 1.029

Days sales inventory

Ending inventory 155,170 154,640

Cost of goods sold 177,056 159,132

Days sales inventory 319.88212

8

354.70

Inventory turnover ratio has improved significantly in 2019 suggesting increase in efficiency of

the company in utilizing its resources in business operations. Return on total assets of the

company has also improved in 2019 along with the ability of the company to turnover its

inventory.

Sub part f:

(i) In planning and performing an audit often auditors determine the materiality levels in

the audit. This is generally items of financial statements and the amount which is

considered material to the overall audit. Generally, a percentage is used to calculate

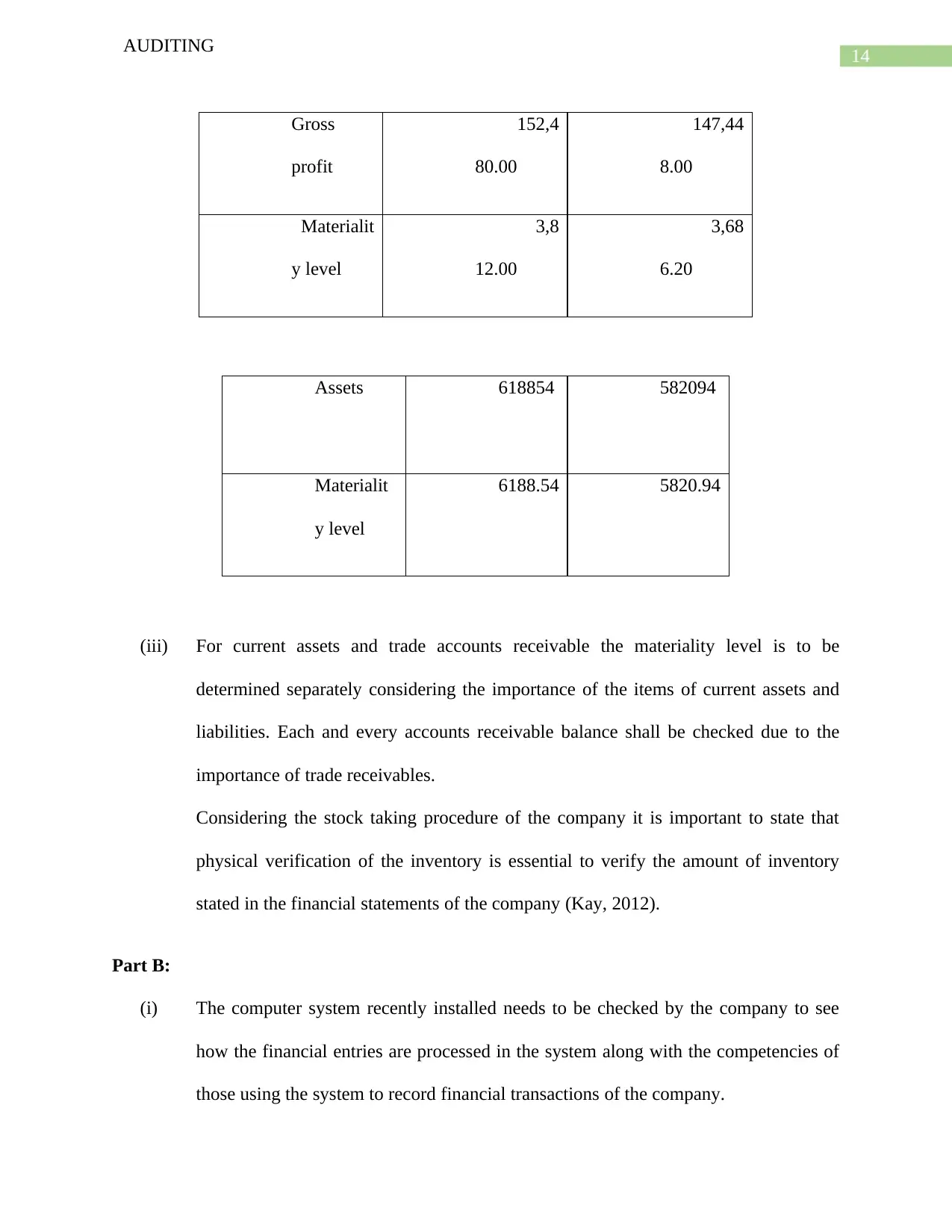

the materiality level. In this case the materiality level can be determined by taking

2.5% of gross profit of the company. For items of assets and liabilities 5% of total

assets and liabilities can be considered as material (Iatridis, 2010).

(ii) Thus, the materiality level is calculated below for items of income and expenditure.

AUDITING

Inventory turnover 1.143 1.029

Days sales inventory

Ending inventory 155,170 154,640

Cost of goods sold 177,056 159,132

Days sales inventory 319.88212

8

354.70

Inventory turnover ratio has improved significantly in 2019 suggesting increase in efficiency of

the company in utilizing its resources in business operations. Return on total assets of the

company has also improved in 2019 along with the ability of the company to turnover its

inventory.

Sub part f:

(i) In planning and performing an audit often auditors determine the materiality levels in

the audit. This is generally items of financial statements and the amount which is

considered material to the overall audit. Generally, a percentage is used to calculate

the materiality level. In this case the materiality level can be determined by taking

2.5% of gross profit of the company. For items of assets and liabilities 5% of total

assets and liabilities can be considered as material (Iatridis, 2010).

(ii) Thus, the materiality level is calculated below for items of income and expenditure.

14

AUDITING

Gross

profit

152,4

80.00

147,44

8.00

Materialit

y level

3,8

12.00

3,68

6.20

Assets 618854 582094

Materialit

y level

6188.54 5820.94

(iii) For current assets and trade accounts receivable the materiality level is to be

determined separately considering the importance of the items of current assets and

liabilities. Each and every accounts receivable balance shall be checked due to the

importance of trade receivables.

Considering the stock taking procedure of the company it is important to state that

physical verification of the inventory is essential to verify the amount of inventory

stated in the financial statements of the company (Kay, 2012).

Part B:

(i) The computer system recently installed needs to be checked by the company to see

how the financial entries are processed in the system along with the competencies of

those using the system to record financial transactions of the company.

AUDITING

Gross

profit

152,4

80.00

147,44

8.00

Materialit

y level

3,8

12.00

3,68

6.20

Assets 618854 582094

Materialit

y level

6188.54 5820.94

(iii) For current assets and trade accounts receivable the materiality level is to be

determined separately considering the importance of the items of current assets and

liabilities. Each and every accounts receivable balance shall be checked due to the

importance of trade receivables.

Considering the stock taking procedure of the company it is important to state that

physical verification of the inventory is essential to verify the amount of inventory

stated in the financial statements of the company (Kay, 2012).

Part B:

(i) The computer system recently installed needs to be checked by the company to see

how the financial entries are processed in the system along with the competencies of

those using the system to record financial transactions of the company.

15

AUDITING

(ii) A walk through procedure helps an auditor to understand the complete process in

respect of a financial transaction. In case of purchase and sales the company should

conduct at-least few walk through test to verify the procedures in place within the

company.

(iii) The internal control risk for certain class of transactions is not strong and the same

needs to be assessed and verified by the auditor.

(iv) The tests of the control shall be tested by recording proxy transactions if necessary to

assess the strengths and weaknesses in internal control system of the company.

Part C:

As an auditor in such a situation it is important to verify the sales ledger with proper sales orders

and vouchers. The payment of sales shall also be verified to check whether there has been any

payment that has been misplaced by the officers and employees of the company. In addition a

walk through test shall be conducted to ascertain the possible area of weakness in the internal

control system of the company in respect of sales transactions. Reconciliation of stock register

with sales requisitions shall help an auditor to identify possible area of fraud within the

organization (Santiso, 2016).

Conclusion:

Taking into consideration the discussion above it would be safe to state that the LQFL is an

entity which has efficient internal control systems in place except for certain class of transactions

and thus, the risk of material error and fraud in the audit of financial statements of the company

is relatively low. However, all necessary substantive and analytical procedures have been

conducted and nothing suspicious have been identified in the financial statements of the

company.

AUDITING

(ii) A walk through procedure helps an auditor to understand the complete process in

respect of a financial transaction. In case of purchase and sales the company should

conduct at-least few walk through test to verify the procedures in place within the

company.

(iii) The internal control risk for certain class of transactions is not strong and the same

needs to be assessed and verified by the auditor.

(iv) The tests of the control shall be tested by recording proxy transactions if necessary to

assess the strengths and weaknesses in internal control system of the company.

Part C:

As an auditor in such a situation it is important to verify the sales ledger with proper sales orders

and vouchers. The payment of sales shall also be verified to check whether there has been any

payment that has been misplaced by the officers and employees of the company. In addition a

walk through test shall be conducted to ascertain the possible area of weakness in the internal

control system of the company in respect of sales transactions. Reconciliation of stock register

with sales requisitions shall help an auditor to identify possible area of fraud within the

organization (Santiso, 2016).

Conclusion:

Taking into consideration the discussion above it would be safe to state that the LQFL is an

entity which has efficient internal control systems in place except for certain class of transactions

and thus, the risk of material error and fraud in the audit of financial statements of the company

is relatively low. However, all necessary substantive and analytical procedures have been

conducted and nothing suspicious have been identified in the financial statements of the

company.

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

16

AUDITING

AUDITING

17

AUDITING

References:

Accounting and Auditing Organization for Islamic Financial Institutions. (2010). Accounting,

auditing and governance standards for Islamic financial institutions. Bahrain.

Allen, A., & Woodland, A. (2010). Education Requirements, Audit Fees, and Audit

Quality. AUDITING: A Journal Of Practice & Theory, 29(2), 1-25. doi:

10.2308/aud.2010.29.2.1

Armitage, J. (2008). Changes in the importance of topics in auditing education: 2000‐

2005. Managerial Auditing Journal, 23(9), 935-959. doi: 10.1108/02686900810908463

Asthana, S. (2012). Diversification by the Audit Office and Its Impact on Audit Quality. SSRN

Electronic Journal, 2(4), 17. doi: 10.2139/ssrn.2157681

Cosserat, G., & Rodda, N. (2009). Modern auditing. Chichester, UK: John Wiley & Sons.

Goswami, A. (2018). Human Resource Management and Its Importance for Today’s

Organizations. Journal Of Advances And Scholarly Researches In Allied Education, 15(3),

128-135. doi: 10.29070/15/57308

Gray, I., Manson, S., & Crawford, L. (2015). The audit process. Andover, Hampshire, U.K.:

Cengage Learning.

Green, J. (2013). Financial Statement Analysis and Equity Valuation. SSRN Electronic

Journal, 2(1), 12-32. doi: 10.2139/ssrn.2271238

AUDITING

References:

Accounting and Auditing Organization for Islamic Financial Institutions. (2010). Accounting,

auditing and governance standards for Islamic financial institutions. Bahrain.

Allen, A., & Woodland, A. (2010). Education Requirements, Audit Fees, and Audit

Quality. AUDITING: A Journal Of Practice & Theory, 29(2), 1-25. doi:

10.2308/aud.2010.29.2.1

Armitage, J. (2008). Changes in the importance of topics in auditing education: 2000‐

2005. Managerial Auditing Journal, 23(9), 935-959. doi: 10.1108/02686900810908463

Asthana, S. (2012). Diversification by the Audit Office and Its Impact on Audit Quality. SSRN

Electronic Journal, 2(4), 17. doi: 10.2139/ssrn.2157681

Cosserat, G., & Rodda, N. (2009). Modern auditing. Chichester, UK: John Wiley & Sons.

Goswami, A. (2018). Human Resource Management and Its Importance for Today’s

Organizations. Journal Of Advances And Scholarly Researches In Allied Education, 15(3),

128-135. doi: 10.29070/15/57308

Gray, I., Manson, S., & Crawford, L. (2015). The audit process. Andover, Hampshire, U.K.:

Cengage Learning.

Green, J. (2013). Financial Statement Analysis and Equity Valuation. SSRN Electronic

Journal, 2(1), 12-32. doi: 10.2139/ssrn.2271238

18

AUDITING

Iatridis, G. (2010). International Financial Reporting Standards and the quality of financial

statement information. International Review Of Financial Analysis, 19(3), 193-204. doi:

10.1016/j.irfa.2010.02.004

Kay, J. (2012). Combining ISO/IEC 17025:2005 and European Commission Decision 2002/657

audit requirements: A practical way forward. Drug Testing And Analysis, 4(5), 25-27. doi:

10.1002/dta.1353

Santiso, C. (2016). Political economy of government auditing (pp. 181-235). [Place of

publication not identified]: Routledge-Cavendish.

Suthan, A. (2007). Fundamental of Financial Statement Analysis. SSRN Electronic Journal, 4(5),

18-39. doi: 10.2139/ssrn.1588981

The New Requirements of State Audit Rose from Political Economic and Social Development.

(2012). International Journal Of Digital Content Technology And Its Applications, 6(22),

205-211. doi: 10.4156/jdcta.vol6.issue22.22

Van Linden, C., & Hardies, K. (2018). Entrance requirements to the audit profession within the

EU and audit quality. International Journal Of Auditing, 22(3), 360-373. doi:

10.1111/ijau.12127

서서서, & Junesun Choi. (2010). A Study on the Internal Control System - Focused on financial

institution's internal control system -. Sungkyunkwan Law Review, 22(3), 847-870. doi:

10.17008/skklr.2010.22.3.029

AUDITING

Iatridis, G. (2010). International Financial Reporting Standards and the quality of financial

statement information. International Review Of Financial Analysis, 19(3), 193-204. doi:

10.1016/j.irfa.2010.02.004

Kay, J. (2012). Combining ISO/IEC 17025:2005 and European Commission Decision 2002/657

audit requirements: A practical way forward. Drug Testing And Analysis, 4(5), 25-27. doi:

10.1002/dta.1353

Santiso, C. (2016). Political economy of government auditing (pp. 181-235). [Place of

publication not identified]: Routledge-Cavendish.

Suthan, A. (2007). Fundamental of Financial Statement Analysis. SSRN Electronic Journal, 4(5),

18-39. doi: 10.2139/ssrn.1588981

The New Requirements of State Audit Rose from Political Economic and Social Development.

(2012). International Journal Of Digital Content Technology And Its Applications, 6(22),

205-211. doi: 10.4156/jdcta.vol6.issue22.22

Van Linden, C., & Hardies, K. (2018). Entrance requirements to the audit profession within the

EU and audit quality. International Journal Of Auditing, 22(3), 360-373. doi:

10.1111/ijau.12127

서서서, & Junesun Choi. (2010). A Study on the Internal Control System - Focused on financial

institution's internal control system -. Sungkyunkwan Law Review, 22(3), 847-870. doi:

10.17008/skklr.2010.22.3.029

1 out of 19

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.