Auditing

VerifiedAdded on 2023/03/21

|13

|2699

|76

AI Summary

This document provides an overview of the complexity in auditing in modern business environment and discusses the inherent risks in the audit of cloud 9. It also includes information on the key assertions at risk for PPE additions and the substantive tests of details to be conducted. The document is suitable for students studying auditing.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Running head: AUDITING

Auditing

Name of the Student:

Name of the University:

Authors Note:

Auditing

Name of the Student:

Name of the University:

Authors Note:

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

1

AUDITING

Contents

Introduction:....................................................................................................................................2

Part 1:...............................................................................................................................................2

Part 2:...............................................................................................................................................4

Conclusion:....................................................................................................................................10

References:....................................................................................................................................11

AUDITING

Contents

Introduction:....................................................................................................................................2

Part 1:...............................................................................................................................................2

Part 2:...............................................................................................................................................4

Conclusion:....................................................................................................................................10

References:....................................................................................................................................11

2

AUDITING

Research question:

Introduction:

With the innovation of new technology and ever increasing use of the same in each and every

facets of business operations the complexity in auditing has multiplied by many folds. Earlier

there was visible audit trails when most of the works used to take place manually. However, the

way innovation and technology have evolved over the years to influence the activities within an

organization the complexity of auditing have reached new heights. The inherent risk in the audit

of cloud 9 has been discussed as part of the discussion on ever increasing complexity in auditing

in modern business environment.

Part 1:

Inherent risk in the audit of cloud 9:

Inherent risks in audit of cloud 9 are discussed in brief here to allow the users to have specific

idea about these risks.

Lack of audit trails: With the organizations using advanced and cutting edge state of the art

technology to conduct different business operations the availability of audit trails has reduced

significantly. As a result it has become difficult to verify the financial transaction with proper

audit trails (A Review on Auditing in Cloud, 2016).

Use of computer assisted auditing tools (CAATs): The use of computer assisted auditing tools is

a risky proposition since most of the auditors are not supposed to have expert knowledge in using

CAATs.

AUDITING

Research question:

Introduction:

With the innovation of new technology and ever increasing use of the same in each and every

facets of business operations the complexity in auditing has multiplied by many folds. Earlier

there was visible audit trails when most of the works used to take place manually. However, the

way innovation and technology have evolved over the years to influence the activities within an

organization the complexity of auditing have reached new heights. The inherent risk in the audit

of cloud 9 has been discussed as part of the discussion on ever increasing complexity in auditing

in modern business environment.

Part 1:

Inherent risk in the audit of cloud 9:

Inherent risks in audit of cloud 9 are discussed in brief here to allow the users to have specific

idea about these risks.

Lack of audit trails: With the organizations using advanced and cutting edge state of the art

technology to conduct different business operations the availability of audit trails has reduced

significantly. As a result it has become difficult to verify the financial transaction with proper

audit trails (A Review on Auditing in Cloud, 2016).

Use of computer assisted auditing tools (CAATs): The use of computer assisted auditing tools is

a risky proposition since most of the auditors are not supposed to have expert knowledge in using

CAATs.

3

AUDITING

No visible documents: The lack of documentation is another inherent problem in cloud 9

auditing as most of the operations are carried out in the computers and machines without

generating proper documents against each and every operations (A Survey on Cloud Storage

Privacy Preserving Public Auditing for Regenerating Code, 2015).

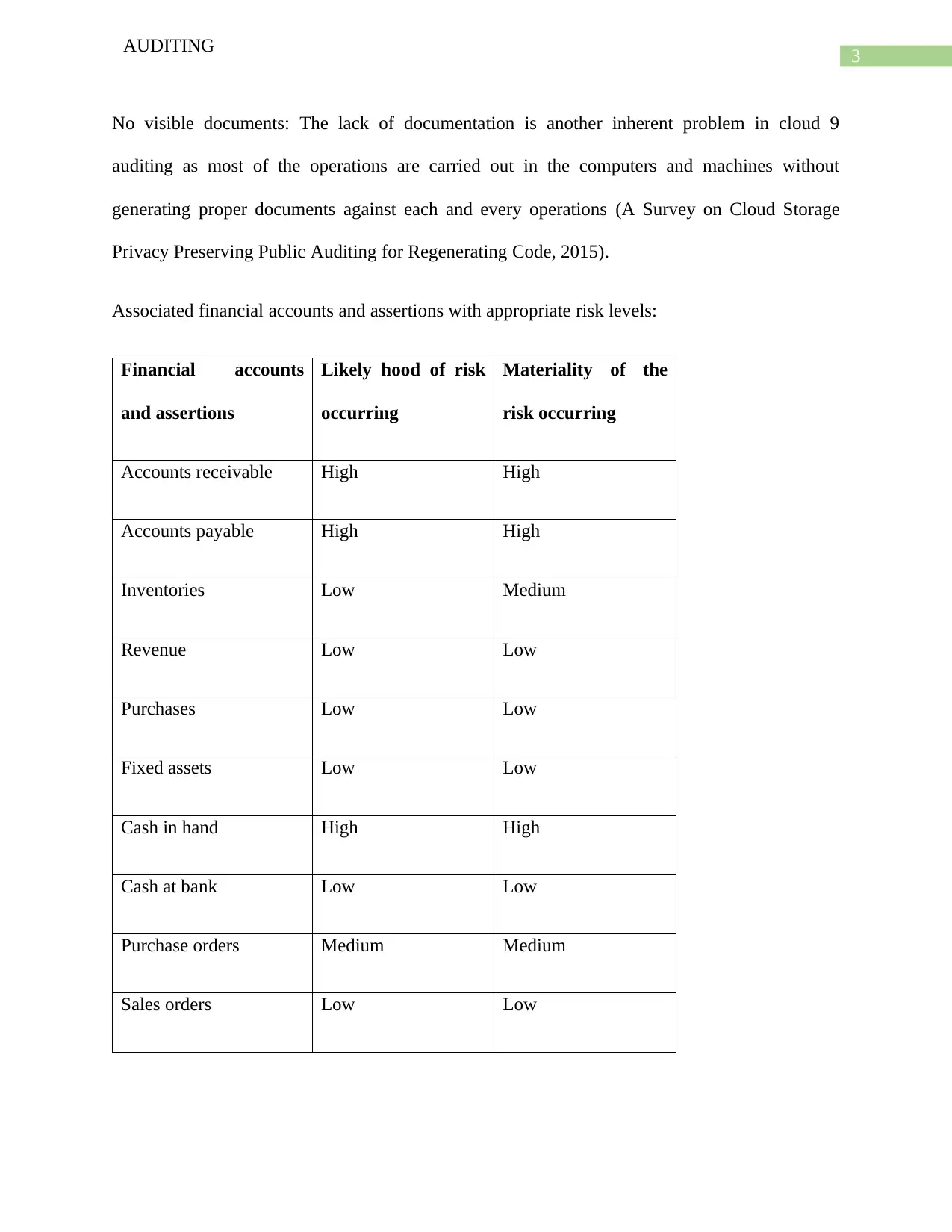

Associated financial accounts and assertions with appropriate risk levels:

Financial accounts

and assertions

Likely hood of risk

occurring

Materiality of the

risk occurring

Accounts receivable High High

Accounts payable High High

Inventories Low Medium

Revenue Low Low

Purchases Low Low

Fixed assets Low Low

Cash in hand High High

Cash at bank Low Low

Purchase orders Medium Medium

Sales orders Low Low

AUDITING

No visible documents: The lack of documentation is another inherent problem in cloud 9

auditing as most of the operations are carried out in the computers and machines without

generating proper documents against each and every operations (A Survey on Cloud Storage

Privacy Preserving Public Auditing for Regenerating Code, 2015).

Associated financial accounts and assertions with appropriate risk levels:

Financial accounts

and assertions

Likely hood of risk

occurring

Materiality of the

risk occurring

Accounts receivable High High

Accounts payable High High

Inventories Low Medium

Revenue Low Low

Purchases Low Low

Fixed assets Low Low

Cash in hand High High

Cash at bank Low Low

Purchase orders Medium Medium

Sales orders Low Low

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

4

AUDITING

Accounts receivable: The reason for high risk associated with accounts receivable is the lack of

visible document and audit trail to verify the amount dues from the customers as well as the

amount that have received from them.

Accounts payable: Similar to the accounts receivable accounts payables are paid by making

payments to the vendors. However, since the discount as well as trade rebates provided by them

are automatically calculated in the system thus, it is not possible to verify the discounts received

form the vendors and thus, the final amount due to customers cannot be properly verified with

audit trails and manual documents (Integrity Auditing for Dynamic Cloud Using Homomorphic

Encryption with Group User Revocation, 2016).

Inventories: Inventories are received within an organization thus, the inventories department will

maintain appropriate register which can be verified with the orders placed. Thus, the risk with

inventories is quite low.

Revenue, purchases and fixed assets: Revenue, purchases and fixed assets are all identified to

have quite low risk as all these accounts can be verified with proper documents and even

physical verification can be carried out for fixed assets (Privacy-Preserving Auditing Protocol for

Dynamic Group Cloud Environment, 2016).

Cash in hand: Cash in hand will have significantly higher risk as the risk in general associated

with cash in hand is always quite high.

Cash at bank: Cash at bank has significantly low risk in both likelihood and materiality aspects.

Part 2:

AUDITING

Accounts receivable: The reason for high risk associated with accounts receivable is the lack of

visible document and audit trail to verify the amount dues from the customers as well as the

amount that have received from them.

Accounts payable: Similar to the accounts receivable accounts payables are paid by making

payments to the vendors. However, since the discount as well as trade rebates provided by them

are automatically calculated in the system thus, it is not possible to verify the discounts received

form the vendors and thus, the final amount due to customers cannot be properly verified with

audit trails and manual documents (Integrity Auditing for Dynamic Cloud Using Homomorphic

Encryption with Group User Revocation, 2016).

Inventories: Inventories are received within an organization thus, the inventories department will

maintain appropriate register which can be verified with the orders placed. Thus, the risk with

inventories is quite low.

Revenue, purchases and fixed assets: Revenue, purchases and fixed assets are all identified to

have quite low risk as all these accounts can be verified with proper documents and even

physical verification can be carried out for fixed assets (Privacy-Preserving Auditing Protocol for

Dynamic Group Cloud Environment, 2016).

Cash in hand: Cash in hand will have significantly higher risk as the risk in general associated

with cash in hand is always quite high.

Cash at bank: Cash at bank has significantly low risk in both likelihood and materiality aspects.

Part 2:

5

AUDITING

Sub part (a):

In order to ensure that the work performed by an auditor on the inventory in foreign countries is

as per the required standard for the company to correctly ascertain the quality and quantity of

inventory and its value, it is important to follow the standard procedures for engaging component

auditors to perform the work on the inventory. The standard procedures are enumerated below.

I. Hiring an expert component auditor to conduct the work on the inventory in China

and USA. A person who has knowledge in the field of inventory valuation should be

sent to do the job.

II. A person who has significant knowledge in the matter of foreign exchange shall

accompany the component auditor in USA and China for inventory audit.

III. The auditor must have necessary knowledge to conduct inventory audit in cloud 9.

IV. All documentation shall be maintained for the work on inventory.

V. Quality and quantity of inventory both shall be checked and verified (TURAN, 2015).

Sub part (b):

Suzie can use the help of a derivative expert but the expert must possess advanced knowledge on

financial instruments including derivative and foreign exchange market. Apart from that the

expert should have sound knowledge of accounting and must be capable of understanding the

financial statements properly. Suzie should take interviews of experts to select a suitable person

as the derivative expert. The expert should be told about the duties and responsibilities that he

must perform and discharge along with the fees to be paid for the services to be rendered by him.

The financial value of derivatives along with underlying assets of different derivatives and the

value of these assets are some of the important information about the derivatives which must be

AUDITING

Sub part (a):

In order to ensure that the work performed by an auditor on the inventory in foreign countries is

as per the required standard for the company to correctly ascertain the quality and quantity of

inventory and its value, it is important to follow the standard procedures for engaging component

auditors to perform the work on the inventory. The standard procedures are enumerated below.

I. Hiring an expert component auditor to conduct the work on the inventory in China

and USA. A person who has knowledge in the field of inventory valuation should be

sent to do the job.

II. A person who has significant knowledge in the matter of foreign exchange shall

accompany the component auditor in USA and China for inventory audit.

III. The auditor must have necessary knowledge to conduct inventory audit in cloud 9.

IV. All documentation shall be maintained for the work on inventory.

V. Quality and quantity of inventory both shall be checked and verified (TURAN, 2015).

Sub part (b):

Suzie can use the help of a derivative expert but the expert must possess advanced knowledge on

financial instruments including derivative and foreign exchange market. Apart from that the

expert should have sound knowledge of accounting and must be capable of understanding the

financial statements properly. Suzie should take interviews of experts to select a suitable person

as the derivative expert. The expert should be told about the duties and responsibilities that he

must perform and discharge along with the fees to be paid for the services to be rendered by him.

The financial value of derivatives along with underlying assets of different derivatives and the

value of these assets are some of the important information about the derivatives which must be

6

AUDITING

provided to Suzie. Expert must be the one to do all the work in relation to derivatives and not

Suzie.

The audit trails under new aged technology availability of

Part (b):

Australian Auditing Standards and Professional Ethics provide standard guidelines to be

followed by the Auditors and accountants in Australia while conducting audit of financial

statements. The alleged action of Freihling would have grossly violated the professional code of

conduct for the auditors in Australia. Auditors and accountants are subjected to the professional

code of conduct of the country and must comply with these standards while discharging their

attest functions as auditors and accountants in the country (Hansen, 2017). The auditors must use

necessary skills and knowledge required to conduct an audit. An auditor must be prudent and

should be careful while conducting audit of financial statements. It is the responsibility of an

auditor to verify whether the financial statements of an organization is in accordance with the

relevant accounting standards applicable to the organization and make report on the same. The

fact that Friehling has been grossly negligent in his behaviour as he has just rubber stamped each

and every report of Madoff without even bother to verify these is completely against the

professional code of conduct and auditing standards and professional ethics in Australia.

Substantive testing of PPE:

AUDITING

provided to Suzie. Expert must be the one to do all the work in relation to derivatives and not

Suzie.

The audit trails under new aged technology availability of

Part (b):

Australian Auditing Standards and Professional Ethics provide standard guidelines to be

followed by the Auditors and accountants in Australia while conducting audit of financial

statements. The alleged action of Freihling would have grossly violated the professional code of

conduct for the auditors in Australia. Auditors and accountants are subjected to the professional

code of conduct of the country and must comply with these standards while discharging their

attest functions as auditors and accountants in the country (Hansen, 2017). The auditors must use

necessary skills and knowledge required to conduct an audit. An auditor must be prudent and

should be careful while conducting audit of financial statements. It is the responsibility of an

auditor to verify whether the financial statements of an organization is in accordance with the

relevant accounting standards applicable to the organization and make report on the same. The

fact that Friehling has been grossly negligent in his behaviour as he has just rubber stamped each

and every report of Madoff without even bother to verify these is completely against the

professional code of conduct and auditing standards and professional ethics in Australia.

Substantive testing of PPE:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7

AUDITING

Property, plant and equipment (PPE) is one of most important components in fixed assets of any

organization. An auditor conducting an audit of an organization which has significant amount of

its total assets in the form of PPE must use appropriate audit procedures to properly verify the

PPE (Hay, 2014).

Key assertions at risk for PPE additions:

The key assertions at PPE additions are explained below:

Confirmation of acquisitions and receiving the item of PPE by the organization: The first and

foremost important assertion in PPE additions is to confirm that the acquisitions have been made

and the item has been received within the organization in proper condition.

Confirmation of ownership: Ownership of the PPE additions must be confirmed, i.e. the PPE

additions shall be in the name of organization. PPE additions must be in the name of the

organization and thus it should be verified in the audit (Millichamp and Taylor, 2012).

Inspection: The PPE additions must be inspected properly by the auditor to ensure that these

have been received in proper condition and are not damaged. In addition the brand and the

company of the item of PPE should also be properly verified and checked.

Higher price paid for additions: Often the price paid for PPE additions is too high. It is important

to conduct thorough analysis of the PPE additions and the prices paid to acquire these additions.

Often higher prices are charged by the vendor which would result in loss of funds to an

organization (Owens and Shores, 2010).

Why is at risk?

AUDITING

Property, plant and equipment (PPE) is one of most important components in fixed assets of any

organization. An auditor conducting an audit of an organization which has significant amount of

its total assets in the form of PPE must use appropriate audit procedures to properly verify the

PPE (Hay, 2014).

Key assertions at risk for PPE additions:

The key assertions at PPE additions are explained below:

Confirmation of acquisitions and receiving the item of PPE by the organization: The first and

foremost important assertion in PPE additions is to confirm that the acquisitions have been made

and the item has been received within the organization in proper condition.

Confirmation of ownership: Ownership of the PPE additions must be confirmed, i.e. the PPE

additions shall be in the name of organization. PPE additions must be in the name of the

organization and thus it should be verified in the audit (Millichamp and Taylor, 2012).

Inspection: The PPE additions must be inspected properly by the auditor to ensure that these

have been received in proper condition and are not damaged. In addition the brand and the

company of the item of PPE should also be properly verified and checked.

Higher price paid for additions: Often the price paid for PPE additions is too high. It is important

to conduct thorough analysis of the PPE additions and the prices paid to acquire these additions.

Often higher prices are charged by the vendor which would result in loss of funds to an

organization (Owens and Shores, 2010).

Why is at risk?

8

AUDITING

The above key risks with PPE additions is mainly due to the fact that PPE additions are made at

rapid speed at Flinders Limited. This has certainly increased the risk with PPE additions.

Companies generally have a standard procedure such as invitation of tender verification of tender

and then placing orders after technical and price verification of different tenders. However, with

an eye on starting the new manufacturing processing as soon as possible the risk in PPE

additions have increase significantly. There is certainly a possibility that proper procedure may

not have been followed in making additions to the PPE. Thus all necessary procedures shall be

conducted on PPE additions to make appropriate assertion on the matter (West, 2017).

Part (b)

Identification of substantive tests of details considering the risks identified at the preceding

point:

Existence of PPE additions: In order to assess the completeness and existence of PPE firstly, the

financial statements shall be checked. Subsequent to that the general ledger and asset register

shall be checked. Finally after the verification of financial statements, general ledger and asset

register, the auditor shall conduct physical verification of the asset.

Valuation of PPE additions: The valuation report shall be checked to consider the reasonableness

of the value calculated and reported in the financial statements. In this respect it is important to

evaluate the depreciation rates also to ensure the rates are in accordance with the accounting

standards applicable in the country.

Ownership: In order to assess the ownership of PPE including new additions the auditor must

verify the ownership document including title deed of PPE existing as well as new additions. In

AUDITING

The above key risks with PPE additions is mainly due to the fact that PPE additions are made at

rapid speed at Flinders Limited. This has certainly increased the risk with PPE additions.

Companies generally have a standard procedure such as invitation of tender verification of tender

and then placing orders after technical and price verification of different tenders. However, with

an eye on starting the new manufacturing processing as soon as possible the risk in PPE

additions have increase significantly. There is certainly a possibility that proper procedure may

not have been followed in making additions to the PPE. Thus all necessary procedures shall be

conducted on PPE additions to make appropriate assertion on the matter (West, 2017).

Part (b)

Identification of substantive tests of details considering the risks identified at the preceding

point:

Existence of PPE additions: In order to assess the completeness and existence of PPE firstly, the

financial statements shall be checked. Subsequent to that the general ledger and asset register

shall be checked. Finally after the verification of financial statements, general ledger and asset

register, the auditor shall conduct physical verification of the asset.

Valuation of PPE additions: The valuation report shall be checked to consider the reasonableness

of the value calculated and reported in the financial statements. In this respect it is important to

evaluate the depreciation rates also to ensure the rates are in accordance with the accounting

standards applicable in the country.

Ownership: In order to assess the ownership of PPE including new additions the auditor must

verify the ownership document including title deed of PPE existing as well as new additions. In

9

AUDITING

addition to title deed the insurance documents shall also be checked properly to ensure that the

insurance that the quantum of insurance taken in correct in relation to the asset and its value.

Inspection shall be conducted regularly: The auditor shall make specific recommendation to the

management to conduct regular periodic inspection of PPE.

Verification of standard procedure followed by the company: The auditor must verify the

standard procedure followed by the company to make additions to the PPE. In case there is any

weaknesses in the procedure then necessary recommendations shall be made to strengthen the

process of acquisition and additions to PPE.

IAS 16 requirements: Disclosure made by the company shall be reviewed by the auditor ensure

these are in compliance with the disclosure requirements of IAS 16.

In case the additions to the PPE have been manufactured by the company in-house using its own

resources, engineers and tool makers instead of purchasing the PPE additions from outside there

would have been significant changes to the substantive tests of details as mentioned in part (b) of

this report. A detail discussion on the substantive test of details is provided below in case the

additions to PPE were manufactured in-house by Flinders using its own engineers, toolmakers

and other resources.

Verification of the materials and resources used in developing PPE additions: The materials and

resources used in developing PPE must be checked and verified to ascertain that these have ben

correctly valued.

Engineers’ work and its valuation: The engineers who have worked to build PPE must be paid

accordingly. The value of their efforts shall be correct and appropriate to properly value the PPE

additions.

AUDITING

addition to title deed the insurance documents shall also be checked properly to ensure that the

insurance that the quantum of insurance taken in correct in relation to the asset and its value.

Inspection shall be conducted regularly: The auditor shall make specific recommendation to the

management to conduct regular periodic inspection of PPE.

Verification of standard procedure followed by the company: The auditor must verify the

standard procedure followed by the company to make additions to the PPE. In case there is any

weaknesses in the procedure then necessary recommendations shall be made to strengthen the

process of acquisition and additions to PPE.

IAS 16 requirements: Disclosure made by the company shall be reviewed by the auditor ensure

these are in compliance with the disclosure requirements of IAS 16.

In case the additions to the PPE have been manufactured by the company in-house using its own

resources, engineers and tool makers instead of purchasing the PPE additions from outside there

would have been significant changes to the substantive tests of details as mentioned in part (b) of

this report. A detail discussion on the substantive test of details is provided below in case the

additions to PPE were manufactured in-house by Flinders using its own engineers, toolmakers

and other resources.

Verification of the materials and resources used in developing PPE additions: The materials and

resources used in developing PPE must be checked and verified to ascertain that these have ben

correctly valued.

Engineers’ work and its valuation: The engineers who have worked to build PPE must be paid

accordingly. The value of their efforts shall be correct and appropriate to properly value the PPE

additions.

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

10

AUDITING

Recording each and every single transaction properly to account for all the expenditures in

connection to the development of PPE additions: All the expenditures incurred in connection

with in-house development of PPE shall be properly accounted for to correctly value the PPE

additions. Auditors must verify that all the expenditures and transactions in relation to the PPE

additions have been correctly recorded to value the cost of PPE.

Correct accounting treatment: All the expenditures incurred in relation to PPE additions in-house

shall be debited to the PPE account. Thus, expenditures directly and indirectly incurred for PPE

additions must be capitalized in PPE account. The auditor must verify the accounting treatment

followed by the company to ensure that the financial statements correctly reflect the value of

PPE developed in-house (Millichamp and Taylor, 2012)..

Conclusion:

Taking into concussion the discussion above it would be safe to say that the auditors have huge

responsibility towards ensuring proper financial reporting. In fact directly and indirectly the

quality of financial reporting to a large extent is dependent on the ability of the auditor to use

appropriate audit procedures to efficiently audit the financial statements of the company. In both

Madoff investment scandal as well as in case of Flinders Limited the importance of Auditors is

quite easily understandable from the above discussion.

AUDITING

Recording each and every single transaction properly to account for all the expenditures in

connection to the development of PPE additions: All the expenditures incurred in connection

with in-house development of PPE shall be properly accounted for to correctly value the PPE

additions. Auditors must verify that all the expenditures and transactions in relation to the PPE

additions have been correctly recorded to value the cost of PPE.

Correct accounting treatment: All the expenditures incurred in relation to PPE additions in-house

shall be debited to the PPE account. Thus, expenditures directly and indirectly incurred for PPE

additions must be capitalized in PPE account. The auditor must verify the accounting treatment

followed by the company to ensure that the financial statements correctly reflect the value of

PPE developed in-house (Millichamp and Taylor, 2012)..

Conclusion:

Taking into concussion the discussion above it would be safe to say that the auditors have huge

responsibility towards ensuring proper financial reporting. In fact directly and indirectly the

quality of financial reporting to a large extent is dependent on the ability of the auditor to use

appropriate audit procedures to efficiently audit the financial statements of the company. In both

Madoff investment scandal as well as in case of Flinders Limited the importance of Auditors is

quite easily understandable from the above discussion.

11

AUDITING

References:

A Review on Auditing in Cloud. (2016). International Journal of Science and Research (IJSR),

5(5), pp.1312-1317.

A Survey on Cloud Storage Privacy Preserving Public Auditing for Regenerating Code.

(2015). International Journal of Science and Research (IJSR), 4(12), pp.39-42.

Dimmock, S. and Gerken, W. (2011). Finding Bernie Madoff: Detecting Fraud by Investment

Managers. SSRN Electronic Journal, 3(7), pp.17-29.

Hansen, J. (2017). Introductory Audit Homework Handouts: A Bridge from Class to Auditors'

Professional Responsibilities. Current Issues in Auditing, 11(2), pp.I1-I21.

Hay, D. (2014). Auditing, International Auditing and the International Journal of Auditing:

Editorial. International Journal of Auditing, 18(1), pp.1-1.

Millichamp, A. and Taylor, J. (2012). Auditing. Andover, Hampshire: Cengage Learning EMEA.

Owens, E. and Shores, M. (2010). Informal Networks and White Collar Crime: Evidence from

the Madoff Scandal. SSRN Electronic Journal, 2(5), pp.12-15.

Privacy-Preserving Auditing Protocol for Dynamic Group Cloud Environment.

(2016). International Journal of Science and Research (IJSR), 5(3), pp.791-795.

TURAN, M. (2015). Cloud Computing And Its Financial Effects: Tax On Cloud. Bilgi Dünyasi,

15(2), pp.25-30.

West, A. (2017). The ethics of professional accountants: an Aristotelian perspective. Accounting,

Auditing & Accountability Journal, 30(2), pp.328-351.

AUDITING

References:

A Review on Auditing in Cloud. (2016). International Journal of Science and Research (IJSR),

5(5), pp.1312-1317.

A Survey on Cloud Storage Privacy Preserving Public Auditing for Regenerating Code.

(2015). International Journal of Science and Research (IJSR), 4(12), pp.39-42.

Dimmock, S. and Gerken, W. (2011). Finding Bernie Madoff: Detecting Fraud by Investment

Managers. SSRN Electronic Journal, 3(7), pp.17-29.

Hansen, J. (2017). Introductory Audit Homework Handouts: A Bridge from Class to Auditors'

Professional Responsibilities. Current Issues in Auditing, 11(2), pp.I1-I21.

Hay, D. (2014). Auditing, International Auditing and the International Journal of Auditing:

Editorial. International Journal of Auditing, 18(1), pp.1-1.

Millichamp, A. and Taylor, J. (2012). Auditing. Andover, Hampshire: Cengage Learning EMEA.

Owens, E. and Shores, M. (2010). Informal Networks and White Collar Crime: Evidence from

the Madoff Scandal. SSRN Electronic Journal, 2(5), pp.12-15.

Privacy-Preserving Auditing Protocol for Dynamic Group Cloud Environment.

(2016). International Journal of Science and Research (IJSR), 5(3), pp.791-795.

TURAN, M. (2015). Cloud Computing And Its Financial Effects: Tax On Cloud. Bilgi Dünyasi,

15(2), pp.25-30.

West, A. (2017). The ethics of professional accountants: an Aristotelian perspective. Accounting,

Auditing & Accountability Journal, 30(2), pp.328-351.

12

AUDITING

Integrity Auditing for Dynamic Cloud Using Homomorphic Encryption with Group User

Revocation. (2016). International Journal of Science and Research (IJSR), 5(4), pp.1093-1096.

AUDITING

Integrity Auditing for Dynamic Cloud Using Homomorphic Encryption with Group User

Revocation. (2016). International Journal of Science and Research (IJSR), 5(4), pp.1093-1096.

1 out of 13

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.