Always Precise Instruments (API) Audit Risks Discussion Memo

VerifiedAdded on 2023/03/20

|13

|3341

|63

Report

AI Summary

This report, presented as a memo to the audit manager, analyzes the audit risks associated with Always Precise Instruments Pty Limited (API). It examines the company's financial statements, focusing on ratio analysis and internal control procedures related to inventory. The report highlights potential audit risks, including those revealed through key ratios like the current ratio, return on equity, quick asset ratio, return on total assets, gross margin, marketing expenses, administration expenses, times interest earned, days in inventory, days in receivables, and debt-to-equity ratio. Furthermore, the memo discusses weaknesses in internal control for inventory management and their associated audit risks. The analysis includes audit procedures and sampling tests, aiming to identify potential material misstatements in API's financial reporting. The memo concludes by emphasizing the importance of effective audit procedures to ensure the accuracy and fairness of the financial statements.

Running head: AUDITING

Auditing

Name of the Student:

Name of the University:

Author’s Note:

Auditing

Name of the Student:

Name of the University:

Author’s Note:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1

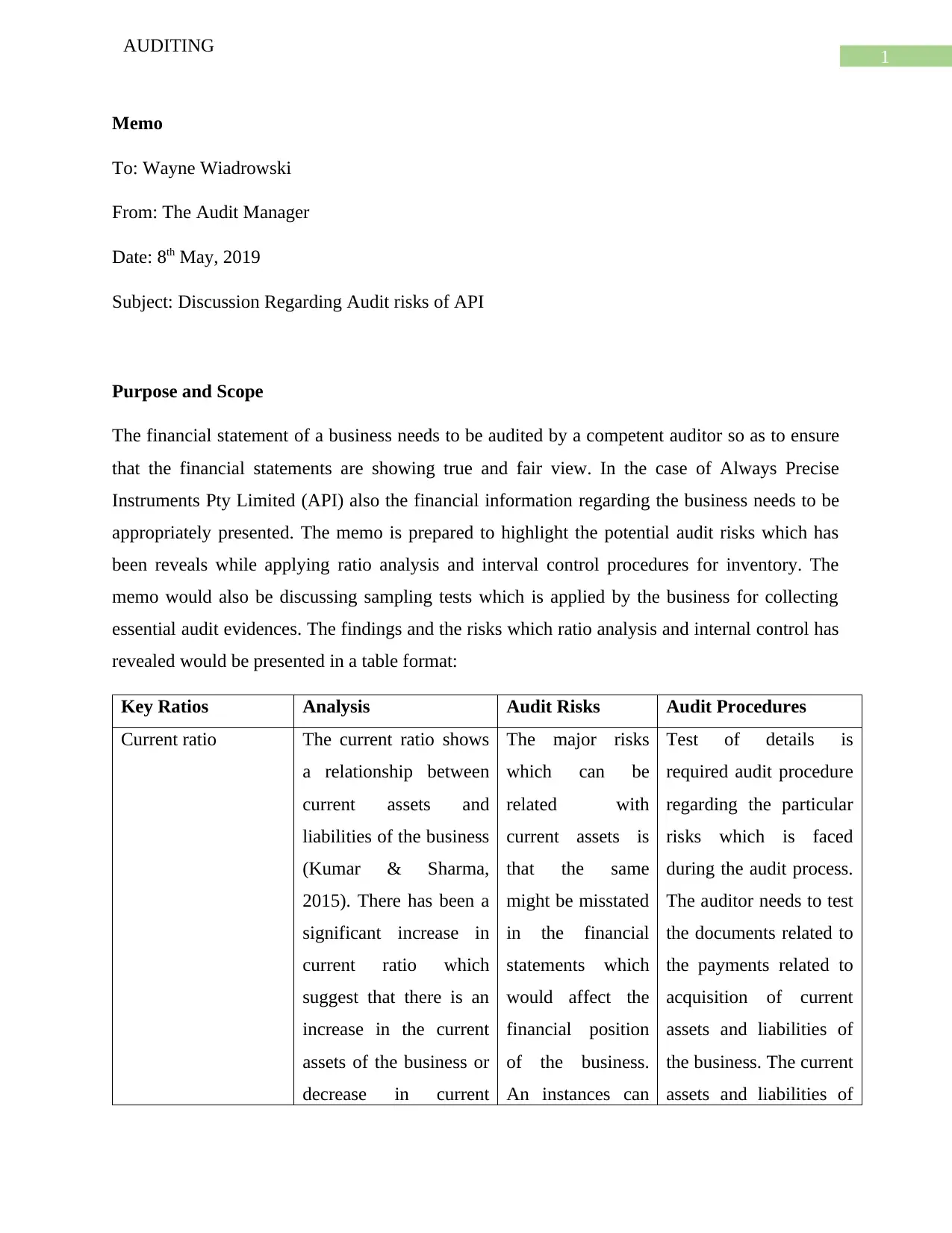

AUDITING

Memo

To: Wayne Wiadrowski

From: The Audit Manager

Date: 8th May, 2019

Subject: Discussion Regarding Audit risks of API

Purpose and Scope

The financial statement of a business needs to be audited by a competent auditor so as to ensure

that the financial statements are showing true and fair view. In the case of Always Precise

Instruments Pty Limited (API) also the financial information regarding the business needs to be

appropriately presented. The memo is prepared to highlight the potential audit risks which has

been reveals while applying ratio analysis and interval control procedures for inventory. The

memo would also be discussing sampling tests which is applied by the business for collecting

essential audit evidences. The findings and the risks which ratio analysis and internal control has

revealed would be presented in a table format:

Key Ratios Analysis Audit Risks Audit Procedures

Current ratio The current ratio shows

a relationship between

current assets and

liabilities of the business

(Kumar & Sharma,

2015). There has been a

significant increase in

current ratio which

suggest that there is an

increase in the current

assets of the business or

decrease in current

The major risks

which can be

related with

current assets is

that the same

might be misstated

in the financial

statements which

would affect the

financial position

of the business.

An instances can

Test of details is

required audit procedure

regarding the particular

risks which is faced

during the audit process.

The auditor needs to test

the documents related to

the payments related to

acquisition of current

assets and liabilities of

the business. The current

assets and liabilities of

AUDITING

Memo

To: Wayne Wiadrowski

From: The Audit Manager

Date: 8th May, 2019

Subject: Discussion Regarding Audit risks of API

Purpose and Scope

The financial statement of a business needs to be audited by a competent auditor so as to ensure

that the financial statements are showing true and fair view. In the case of Always Precise

Instruments Pty Limited (API) also the financial information regarding the business needs to be

appropriately presented. The memo is prepared to highlight the potential audit risks which has

been reveals while applying ratio analysis and interval control procedures for inventory. The

memo would also be discussing sampling tests which is applied by the business for collecting

essential audit evidences. The findings and the risks which ratio analysis and internal control has

revealed would be presented in a table format:

Key Ratios Analysis Audit Risks Audit Procedures

Current ratio The current ratio shows

a relationship between

current assets and

liabilities of the business

(Kumar & Sharma,

2015). There has been a

significant increase in

current ratio which

suggest that there is an

increase in the current

assets of the business or

decrease in current

The major risks

which can be

related with

current assets is

that the same

might be misstated

in the financial

statements which

would affect the

financial position

of the business.

An instances can

Test of details is

required audit procedure

regarding the particular

risks which is faced

during the audit process.

The auditor needs to test

the documents related to

the payments related to

acquisition of current

assets and liabilities of

the business. The current

assets and liabilities of

2

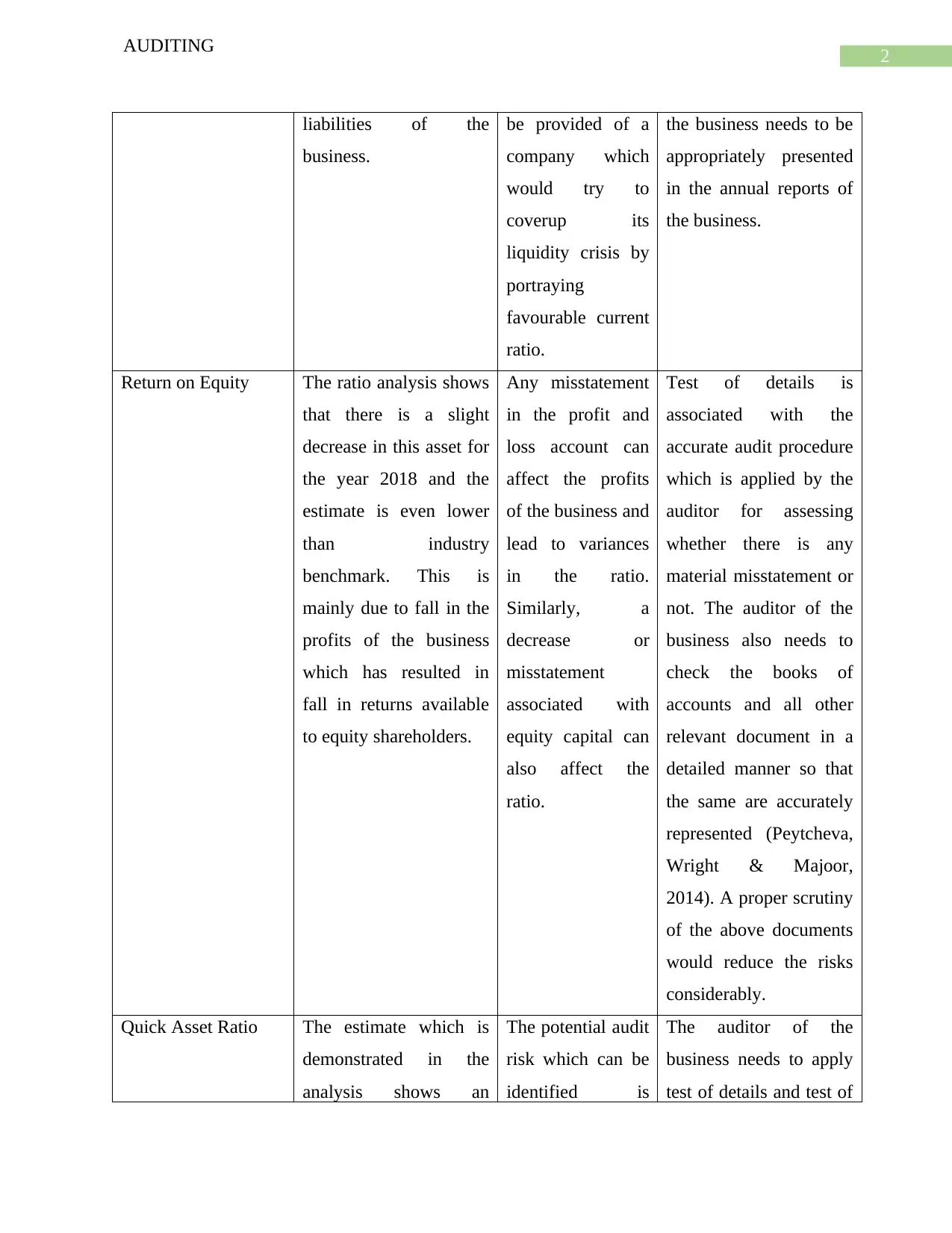

AUDITING

liabilities of the

business.

be provided of a

company which

would try to

coverup its

liquidity crisis by

portraying

favourable current

ratio.

the business needs to be

appropriately presented

in the annual reports of

the business.

Return on Equity The ratio analysis shows

that there is a slight

decrease in this asset for

the year 2018 and the

estimate is even lower

than industry

benchmark. This is

mainly due to fall in the

profits of the business

which has resulted in

fall in returns available

to equity shareholders.

Any misstatement

in the profit and

loss account can

affect the profits

of the business and

lead to variances

in the ratio.

Similarly, a

decrease or

misstatement

associated with

equity capital can

also affect the

ratio.

Test of details is

associated with the

accurate audit procedure

which is applied by the

auditor for assessing

whether there is any

material misstatement or

not. The auditor of the

business also needs to

check the books of

accounts and all other

relevant document in a

detailed manner so that

the same are accurately

represented (Peytcheva,

Wright & Majoor,

2014). A proper scrutiny

of the above documents

would reduce the risks

considerably.

Quick Asset Ratio The estimate which is

demonstrated in the

analysis shows an

The potential audit

risk which can be

identified is

The auditor of the

business needs to apply

test of details and test of

AUDITING

liabilities of the

business.

be provided of a

company which

would try to

coverup its

liquidity crisis by

portraying

favourable current

ratio.

the business needs to be

appropriately presented

in the annual reports of

the business.

Return on Equity The ratio analysis shows

that there is a slight

decrease in this asset for

the year 2018 and the

estimate is even lower

than industry

benchmark. This is

mainly due to fall in the

profits of the business

which has resulted in

fall in returns available

to equity shareholders.

Any misstatement

in the profit and

loss account can

affect the profits

of the business and

lead to variances

in the ratio.

Similarly, a

decrease or

misstatement

associated with

equity capital can

also affect the

ratio.

Test of details is

associated with the

accurate audit procedure

which is applied by the

auditor for assessing

whether there is any

material misstatement or

not. The auditor of the

business also needs to

check the books of

accounts and all other

relevant document in a

detailed manner so that

the same are accurately

represented (Peytcheva,

Wright & Majoor,

2014). A proper scrutiny

of the above documents

would reduce the risks

considerably.

Quick Asset Ratio The estimate which is

demonstrated in the

analysis shows an

The potential audit

risk which can be

identified is

The auditor of the

business needs to apply

test of details and test of

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3

AUDITING

increase in the same.

The management of the

company is maintaining

its quick assets so that

the current liabilities of

the business can be

effectively met.

material

misstatement in

the current assets

and current

liabilities as the

same might be

overstated or

understated

thereby affecting

the accuracy of the

financial

statements of the

business.

control which is related

to assessing the assets

and liabilities of the

business (William Jr,

Glover & Prawitt, 2016).

The auditor needs to

appropriately assess

whether the accounts are

representing true and

fair view and whether

the same is not

materially misstated by

the business.

Return on Total Asset As per the ratio analysis

which is shown in the

case, there is a slight

decrease in the return on

assets estimate of API in

2018 which suggest that

the company is not using

the assets of the business

appropriately and

thereby the same is

affecting the profits of

the business (Zakari,

2013).

The major risks

which can be

identified in such a

case is material

misstatement in

valuing the assets

of the business or

misstatement in

disclosing the

profits of the

business. A

misstatement of

profit would

decrease the ratio

which is the case

in the present

scenario.

The auditor need to

apply test of details as

proper review is

required for every

account balances

associated with the

assets of the business

and transactions which

are undertaken by the

management of the

company. This

procedure would

appropriately help the

auditor to check the trail

of transactions and

thereby collect

appropriate evidences

whether the financial

AUDITING

increase in the same.

The management of the

company is maintaining

its quick assets so that

the current liabilities of

the business can be

effectively met.

material

misstatement in

the current assets

and current

liabilities as the

same might be

overstated or

understated

thereby affecting

the accuracy of the

financial

statements of the

business.

control which is related

to assessing the assets

and liabilities of the

business (William Jr,

Glover & Prawitt, 2016).

The auditor needs to

appropriately assess

whether the accounts are

representing true and

fair view and whether

the same is not

materially misstated by

the business.

Return on Total Asset As per the ratio analysis

which is shown in the

case, there is a slight

decrease in the return on

assets estimate of API in

2018 which suggest that

the company is not using

the assets of the business

appropriately and

thereby the same is

affecting the profits of

the business (Zakari,

2013).

The major risks

which can be

identified in such a

case is material

misstatement in

valuing the assets

of the business or

misstatement in

disclosing the

profits of the

business. A

misstatement of

profit would

decrease the ratio

which is the case

in the present

scenario.

The auditor need to

apply test of details as

proper review is

required for every

account balances

associated with the

assets of the business

and transactions which

are undertaken by the

management of the

company. This

procedure would

appropriately help the

auditor to check the trail

of transactions and

thereby collect

appropriate evidences

whether the financial

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4

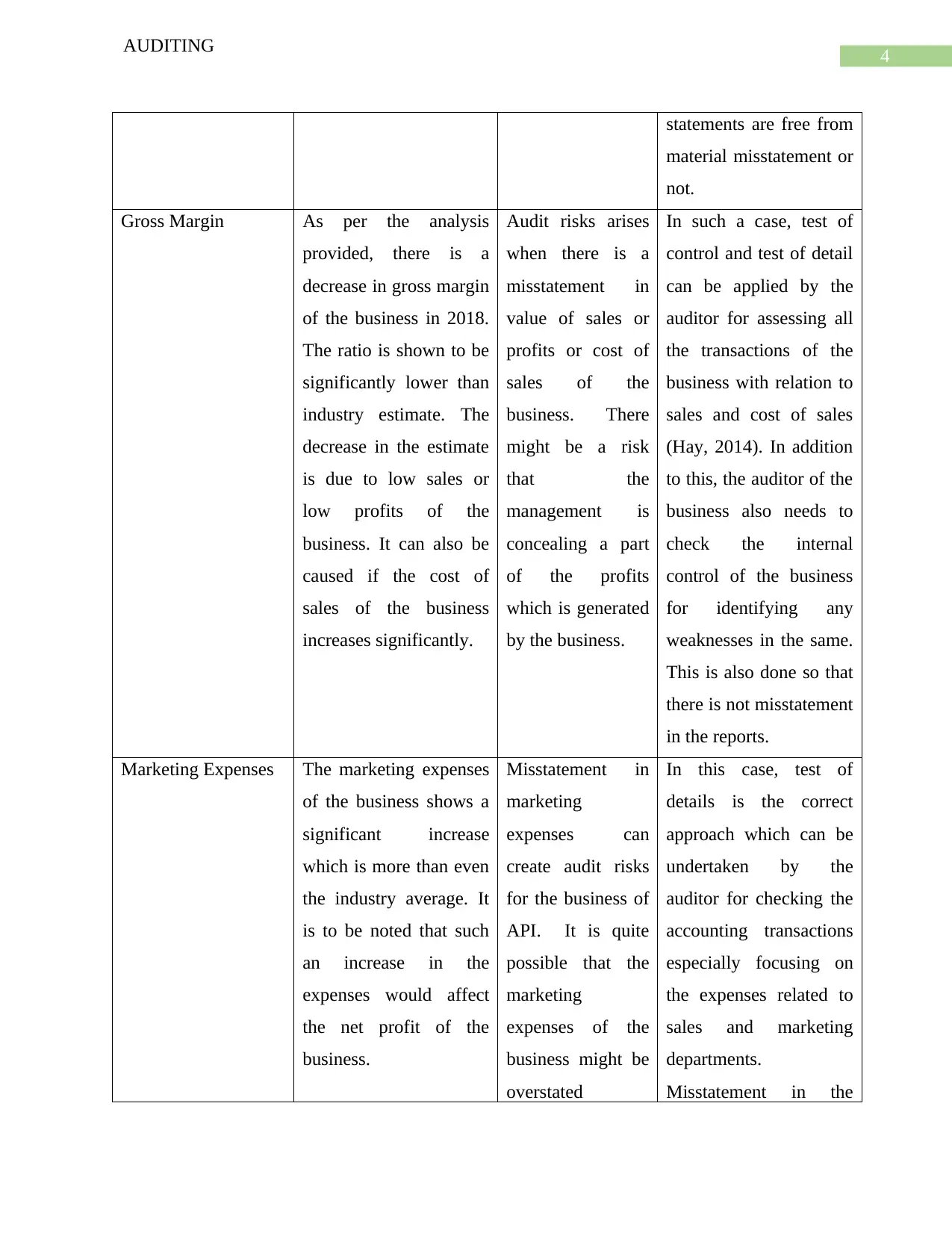

AUDITING

statements are free from

material misstatement or

not.

Gross Margin As per the analysis

provided, there is a

decrease in gross margin

of the business in 2018.

The ratio is shown to be

significantly lower than

industry estimate. The

decrease in the estimate

is due to low sales or

low profits of the

business. It can also be

caused if the cost of

sales of the business

increases significantly.

Audit risks arises

when there is a

misstatement in

value of sales or

profits or cost of

sales of the

business. There

might be a risk

that the

management is

concealing a part

of the profits

which is generated

by the business.

In such a case, test of

control and test of detail

can be applied by the

auditor for assessing all

the transactions of the

business with relation to

sales and cost of sales

(Hay, 2014). In addition

to this, the auditor of the

business also needs to

check the internal

control of the business

for identifying any

weaknesses in the same.

This is also done so that

there is not misstatement

in the reports.

Marketing Expenses The marketing expenses

of the business shows a

significant increase

which is more than even

the industry average. It

is to be noted that such

an increase in the

expenses would affect

the net profit of the

business.

Misstatement in

marketing

expenses can

create audit risks

for the business of

API. It is quite

possible that the

marketing

expenses of the

business might be

overstated

In this case, test of

details is the correct

approach which can be

undertaken by the

auditor for checking the

accounting transactions

especially focusing on

the expenses related to

sales and marketing

departments.

Misstatement in the

AUDITING

statements are free from

material misstatement or

not.

Gross Margin As per the analysis

provided, there is a

decrease in gross margin

of the business in 2018.

The ratio is shown to be

significantly lower than

industry estimate. The

decrease in the estimate

is due to low sales or

low profits of the

business. It can also be

caused if the cost of

sales of the business

increases significantly.

Audit risks arises

when there is a

misstatement in

value of sales or

profits or cost of

sales of the

business. There

might be a risk

that the

management is

concealing a part

of the profits

which is generated

by the business.

In such a case, test of

control and test of detail

can be applied by the

auditor for assessing all

the transactions of the

business with relation to

sales and cost of sales

(Hay, 2014). In addition

to this, the auditor of the

business also needs to

check the internal

control of the business

for identifying any

weaknesses in the same.

This is also done so that

there is not misstatement

in the reports.

Marketing Expenses The marketing expenses

of the business shows a

significant increase

which is more than even

the industry average. It

is to be noted that such

an increase in the

expenses would affect

the net profit of the

business.

Misstatement in

marketing

expenses can

create audit risks

for the business of

API. It is quite

possible that the

marketing

expenses of the

business might be

overstated

In this case, test of

details is the correct

approach which can be

undertaken by the

auditor for checking the

accounting transactions

especially focusing on

the expenses related to

sales and marketing

departments.

Misstatement in the

5

AUDITING

(Knechel &

Salterio, 2016).

accounting records can

be identified y applying

vouching practices in the

business. Effective

identification of the

audit risks reduces the

chance of material

misstatement of annual

reports.

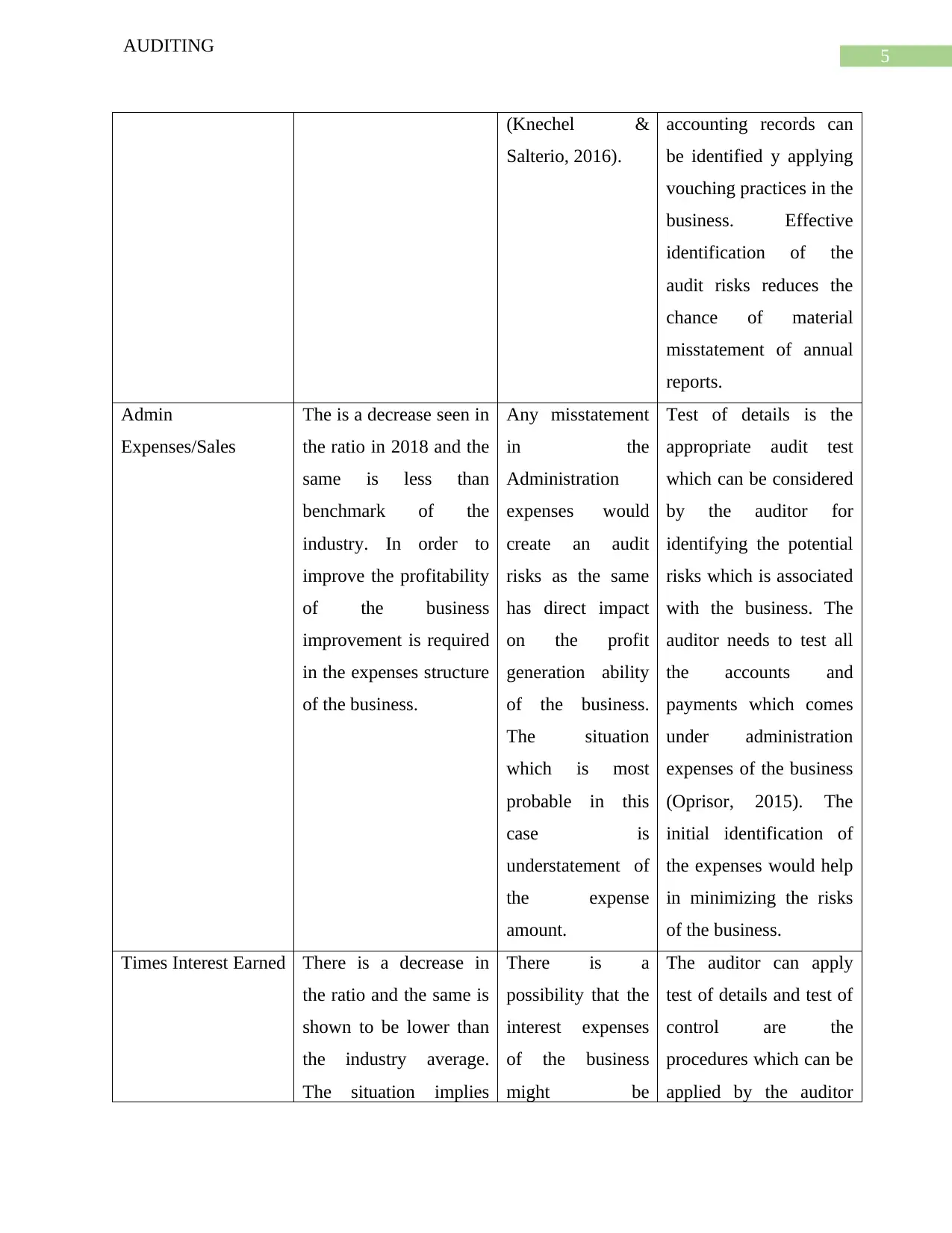

Admin

Expenses/Sales

The is a decrease seen in

the ratio in 2018 and the

same is less than

benchmark of the

industry. In order to

improve the profitability

of the business

improvement is required

in the expenses structure

of the business.

Any misstatement

in the

Administration

expenses would

create an audit

risks as the same

has direct impact

on the profit

generation ability

of the business.

The situation

which is most

probable in this

case is

understatement of

the expense

amount.

Test of details is the

appropriate audit test

which can be considered

by the auditor for

identifying the potential

risks which is associated

with the business. The

auditor needs to test all

the accounts and

payments which comes

under administration

expenses of the business

(Oprisor, 2015). The

initial identification of

the expenses would help

in minimizing the risks

of the business.

Times Interest Earned There is a decrease in

the ratio and the same is

shown to be lower than

the industry average.

The situation implies

There is a

possibility that the

interest expenses

of the business

might be

The auditor can apply

test of details and test of

control are the

procedures which can be

applied by the auditor

AUDITING

(Knechel &

Salterio, 2016).

accounting records can

be identified y applying

vouching practices in the

business. Effective

identification of the

audit risks reduces the

chance of material

misstatement of annual

reports.

Admin

Expenses/Sales

The is a decrease seen in

the ratio in 2018 and the

same is less than

benchmark of the

industry. In order to

improve the profitability

of the business

improvement is required

in the expenses structure

of the business.

Any misstatement

in the

Administration

expenses would

create an audit

risks as the same

has direct impact

on the profit

generation ability

of the business.

The situation

which is most

probable in this

case is

understatement of

the expense

amount.

Test of details is the

appropriate audit test

which can be considered

by the auditor for

identifying the potential

risks which is associated

with the business. The

auditor needs to test all

the accounts and

payments which comes

under administration

expenses of the business

(Oprisor, 2015). The

initial identification of

the expenses would help

in minimizing the risks

of the business.

Times Interest Earned There is a decrease in

the ratio and the same is

shown to be lower than

the industry average.

The situation implies

There is a

possibility that the

interest expenses

of the business

might be

The auditor can apply

test of details and test of

control are the

procedures which can be

applied by the auditor

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6

AUDITING

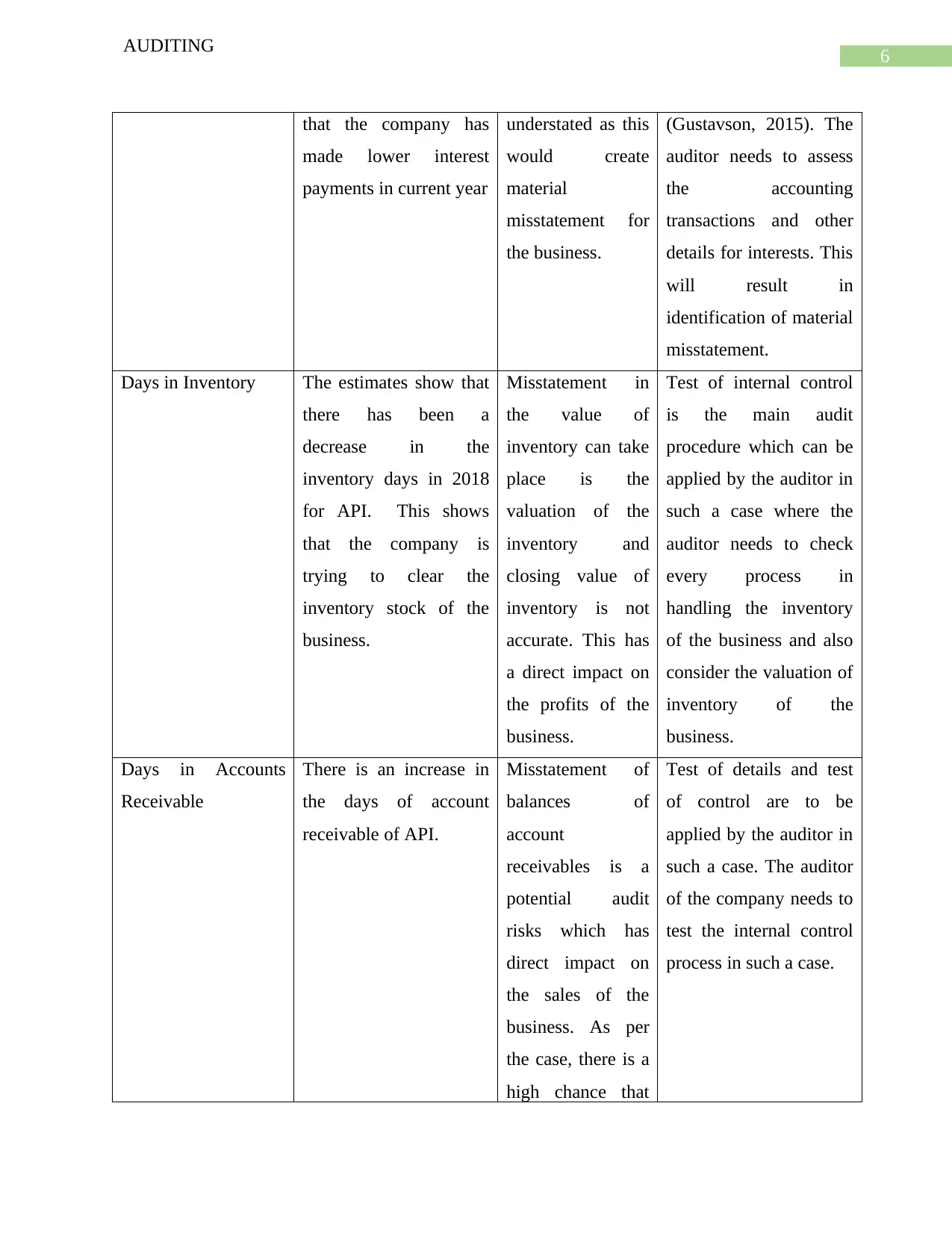

that the company has

made lower interest

payments in current year

understated as this

would create

material

misstatement for

the business.

(Gustavson, 2015). The

auditor needs to assess

the accounting

transactions and other

details for interests. This

will result in

identification of material

misstatement.

Days in Inventory The estimates show that

there has been a

decrease in the

inventory days in 2018

for API. This shows

that the company is

trying to clear the

inventory stock of the

business.

Misstatement in

the value of

inventory can take

place is the

valuation of the

inventory and

closing value of

inventory is not

accurate. This has

a direct impact on

the profits of the

business.

Test of internal control

is the main audit

procedure which can be

applied by the auditor in

such a case where the

auditor needs to check

every process in

handling the inventory

of the business and also

consider the valuation of

inventory of the

business.

Days in Accounts

Receivable

There is an increase in

the days of account

receivable of API.

Misstatement of

balances of

account

receivables is a

potential audit

risks which has

direct impact on

the sales of the

business. As per

the case, there is a

high chance that

Test of details and test

of control are to be

applied by the auditor in

such a case. The auditor

of the company needs to

test the internal control

process in such a case.

AUDITING

that the company has

made lower interest

payments in current year

understated as this

would create

material

misstatement for

the business.

(Gustavson, 2015). The

auditor needs to assess

the accounting

transactions and other

details for interests. This

will result in

identification of material

misstatement.

Days in Inventory The estimates show that

there has been a

decrease in the

inventory days in 2018

for API. This shows

that the company is

trying to clear the

inventory stock of the

business.

Misstatement in

the value of

inventory can take

place is the

valuation of the

inventory and

closing value of

inventory is not

accurate. This has

a direct impact on

the profits of the

business.

Test of internal control

is the main audit

procedure which can be

applied by the auditor in

such a case where the

auditor needs to check

every process in

handling the inventory

of the business and also

consider the valuation of

inventory of the

business.

Days in Accounts

Receivable

There is an increase in

the days of account

receivable of API.

Misstatement of

balances of

account

receivables is a

potential audit

risks which has

direct impact on

the sales of the

business. As per

the case, there is a

high chance that

Test of details and test

of control are to be

applied by the auditor in

such a case. The auditor

of the company needs to

test the internal control

process in such a case.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7

AUDITING

the balances might

be overstated

which may be due

to internal control

weaknesses.

Debt to Equity Ratio There is a decrease in

the ratio in 2018. This is

mainly due to increase

in the debt capital which

is used by the business.

Misstatement in

the amount of debt

which is shown

can create audit

risks as

overstatement of

capital can cause

inaccurate

presentation of

financial position

of the business.

Test of details is the

main audit procedure

which can be undertaken

by the auditor in the

case. The auditor needs

to ascertain whether the

company has taken

additional debt capital

during the year as to

assess the reasons of

hike in the debt capital

of the business (Needles,

Powers & Crosson,

2013).

Weaknesses in Internal control for Inventory and Audit Risks

Internal Control

Weaknesses

Audit Risks Audit Procedures

As per the case which is

provided, a computer system

is responsible for generating

orders regarding purchases

but this can be regarded as a

weakness as any malfunction

of the computerized system

The audit risk which is

associated with this aspect

clearly depicts a weakness in

the internal control system. If

the flow of purchases in the

business is affected than the

same would result in losses

The auditor of the business

can examine the internal

control risks of the audit. The

responsibility of the auditor is

to ensure that such a

computerised system is

operating effectively.

AUDITING

the balances might

be overstated

which may be due

to internal control

weaknesses.

Debt to Equity Ratio There is a decrease in

the ratio in 2018. This is

mainly due to increase

in the debt capital which

is used by the business.

Misstatement in

the amount of debt

which is shown

can create audit

risks as

overstatement of

capital can cause

inaccurate

presentation of

financial position

of the business.

Test of details is the

main audit procedure

which can be undertaken

by the auditor in the

case. The auditor needs

to ascertain whether the

company has taken

additional debt capital

during the year as to

assess the reasons of

hike in the debt capital

of the business (Needles,

Powers & Crosson,

2013).

Weaknesses in Internal control for Inventory and Audit Risks

Internal Control

Weaknesses

Audit Risks Audit Procedures

As per the case which is

provided, a computer system

is responsible for generating

orders regarding purchases

but this can be regarded as a

weakness as any malfunction

of the computerized system

The audit risk which is

associated with this aspect

clearly depicts a weakness in

the internal control system. If

the flow of purchases in the

business is affected than the

same would result in losses

The auditor of the business

can examine the internal

control risks of the audit. The

responsibility of the auditor is

to ensure that such a

computerised system is

operating effectively.

8

AUDITING

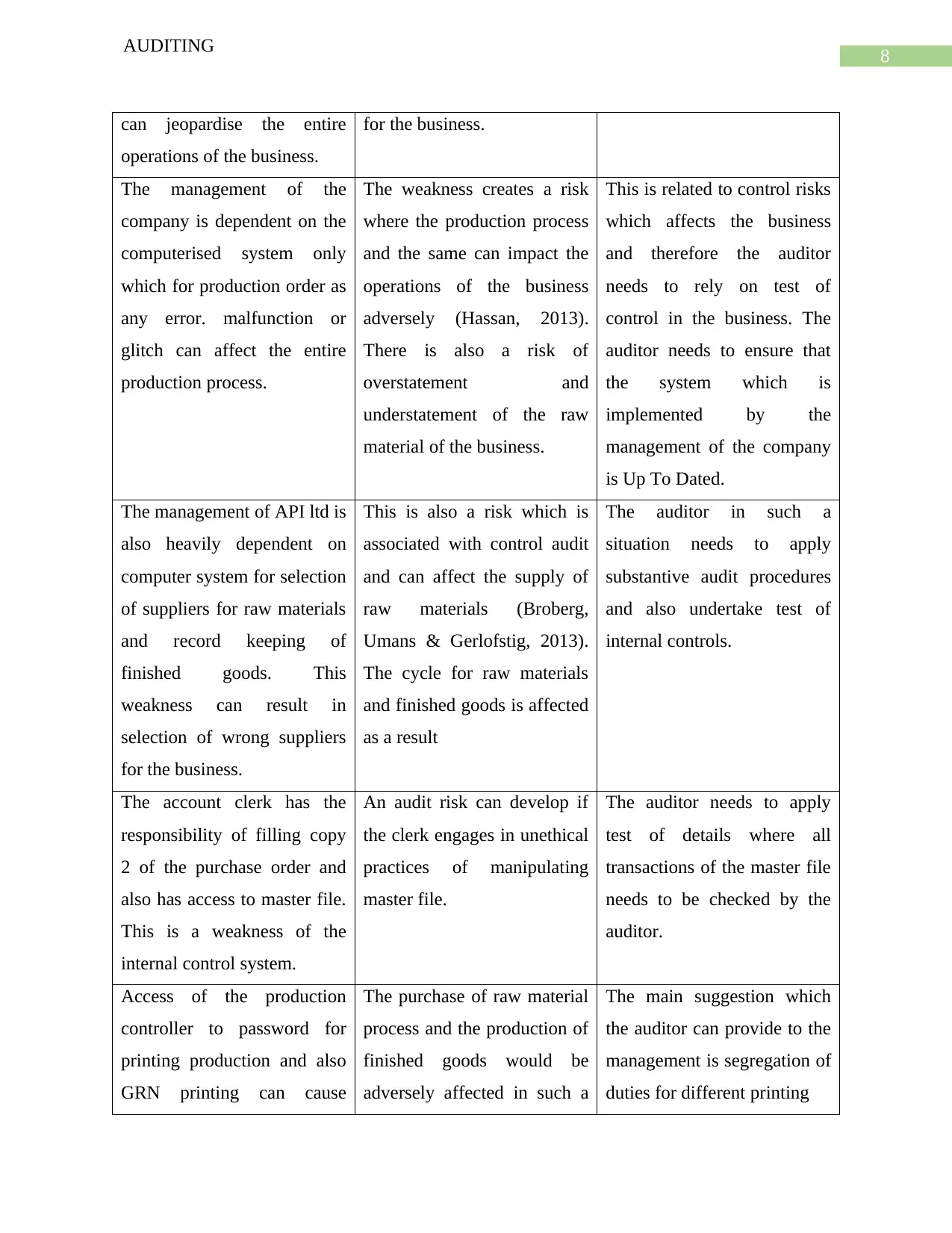

can jeopardise the entire

operations of the business.

for the business.

The management of the

company is dependent on the

computerised system only

which for production order as

any error. malfunction or

glitch can affect the entire

production process.

The weakness creates a risk

where the production process

and the same can impact the

operations of the business

adversely (Hassan, 2013).

There is also a risk of

overstatement and

understatement of the raw

material of the business.

This is related to control risks

which affects the business

and therefore the auditor

needs to rely on test of

control in the business. The

auditor needs to ensure that

the system which is

implemented by the

management of the company

is Up To Dated.

The management of API ltd is

also heavily dependent on

computer system for selection

of suppliers for raw materials

and record keeping of

finished goods. This

weakness can result in

selection of wrong suppliers

for the business.

This is also a risk which is

associated with control audit

and can affect the supply of

raw materials (Broberg,

Umans & Gerlofstig, 2013).

The cycle for raw materials

and finished goods is affected

as a result

The auditor in such a

situation needs to apply

substantive audit procedures

and also undertake test of

internal controls.

The account clerk has the

responsibility of filling copy

2 of the purchase order and

also has access to master file.

This is a weakness of the

internal control system.

An audit risk can develop if

the clerk engages in unethical

practices of manipulating

master file.

The auditor needs to apply

test of details where all

transactions of the master file

needs to be checked by the

auditor.

Access of the production

controller to password for

printing production and also

GRN printing can cause

The purchase of raw material

process and the production of

finished goods would be

adversely affected in such a

The main suggestion which

the auditor can provide to the

management is segregation of

duties for different printing

AUDITING

can jeopardise the entire

operations of the business.

for the business.

The management of the

company is dependent on the

computerised system only

which for production order as

any error. malfunction or

glitch can affect the entire

production process.

The weakness creates a risk

where the production process

and the same can impact the

operations of the business

adversely (Hassan, 2013).

There is also a risk of

overstatement and

understatement of the raw

material of the business.

This is related to control risks

which affects the business

and therefore the auditor

needs to rely on test of

control in the business. The

auditor needs to ensure that

the system which is

implemented by the

management of the company

is Up To Dated.

The management of API ltd is

also heavily dependent on

computer system for selection

of suppliers for raw materials

and record keeping of

finished goods. This

weakness can result in

selection of wrong suppliers

for the business.

This is also a risk which is

associated with control audit

and can affect the supply of

raw materials (Broberg,

Umans & Gerlofstig, 2013).

The cycle for raw materials

and finished goods is affected

as a result

The auditor in such a

situation needs to apply

substantive audit procedures

and also undertake test of

internal controls.

The account clerk has the

responsibility of filling copy

2 of the purchase order and

also has access to master file.

This is a weakness of the

internal control system.

An audit risk can develop if

the clerk engages in unethical

practices of manipulating

master file.

The auditor needs to apply

test of details where all

transactions of the master file

needs to be checked by the

auditor.

Access of the production

controller to password for

printing production and also

GRN printing can cause

The purchase of raw material

process and the production of

finished goods would be

adversely affected in such a

The main suggestion which

the auditor can provide to the

management is segregation of

duties for different printing

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9

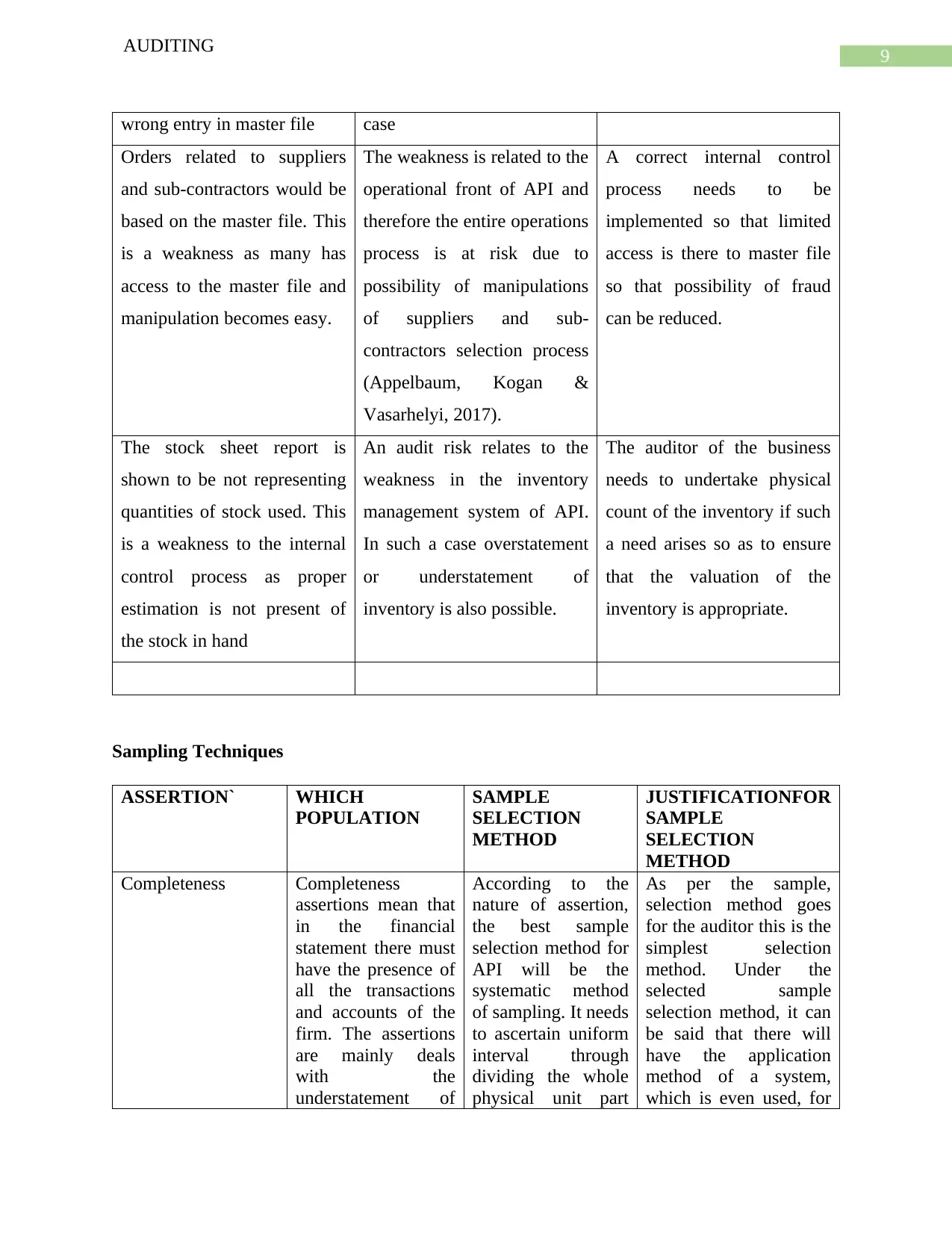

AUDITING

wrong entry in master file case

Orders related to suppliers

and sub-contractors would be

based on the master file. This

is a weakness as many has

access to the master file and

manipulation becomes easy.

The weakness is related to the

operational front of API and

therefore the entire operations

process is at risk due to

possibility of manipulations

of suppliers and sub-

contractors selection process

(Appelbaum, Kogan &

Vasarhelyi, 2017).

A correct internal control

process needs to be

implemented so that limited

access is there to master file

so that possibility of fraud

can be reduced.

The stock sheet report is

shown to be not representing

quantities of stock used. This

is a weakness to the internal

control process as proper

estimation is not present of

the stock in hand

An audit risk relates to the

weakness in the inventory

management system of API.

In such a case overstatement

or understatement of

inventory is also possible.

The auditor of the business

needs to undertake physical

count of the inventory if such

a need arises so as to ensure

that the valuation of the

inventory is appropriate.

Sampling Techniques

ASSERTION` WHICH

POPULATION

SAMPLE

SELECTION

METHOD

JUSTIFICATIONFOR

SAMPLE

SELECTION

METHOD

Completeness Completeness

assertions mean that

in the financial

statement there must

have the presence of

all the transactions

and accounts of the

firm. The assertions

are mainly deals

with the

understatement of

According to the

nature of assertion,

the best sample

selection method for

API will be the

systematic method

of sampling. It needs

to ascertain uniform

interval through

dividing the whole

physical unit part

As per the sample,

selection method goes

for the auditor this is the

simplest selection

method. Under the

selected sample

selection method, it can

be said that there will

have the application

method of a system,

which is even used, for

AUDITING

wrong entry in master file case

Orders related to suppliers

and sub-contractors would be

based on the master file. This

is a weakness as many has

access to the master file and

manipulation becomes easy.

The weakness is related to the

operational front of API and

therefore the entire operations

process is at risk due to

possibility of manipulations

of suppliers and sub-

contractors selection process

(Appelbaum, Kogan &

Vasarhelyi, 2017).

A correct internal control

process needs to be

implemented so that limited

access is there to master file

so that possibility of fraud

can be reduced.

The stock sheet report is

shown to be not representing

quantities of stock used. This

is a weakness to the internal

control process as proper

estimation is not present of

the stock in hand

An audit risk relates to the

weakness in the inventory

management system of API.

In such a case overstatement

or understatement of

inventory is also possible.

The auditor of the business

needs to undertake physical

count of the inventory if such

a need arises so as to ensure

that the valuation of the

inventory is appropriate.

Sampling Techniques

ASSERTION` WHICH

POPULATION

SAMPLE

SELECTION

METHOD

JUSTIFICATIONFOR

SAMPLE

SELECTION

METHOD

Completeness Completeness

assertions mean that

in the financial

statement there must

have the presence of

all the transactions

and accounts of the

firm. The assertions

are mainly deals

with the

understatement of

According to the

nature of assertion,

the best sample

selection method for

API will be the

systematic method

of sampling. It needs

to ascertain uniform

interval through

dividing the whole

physical unit part

As per the sample,

selection method goes

for the auditor this is the

simplest selection

method. Under the

selected sample

selection method, it can

be said that there will

have the application

method of a system,

which is even used, for

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10

AUDITING

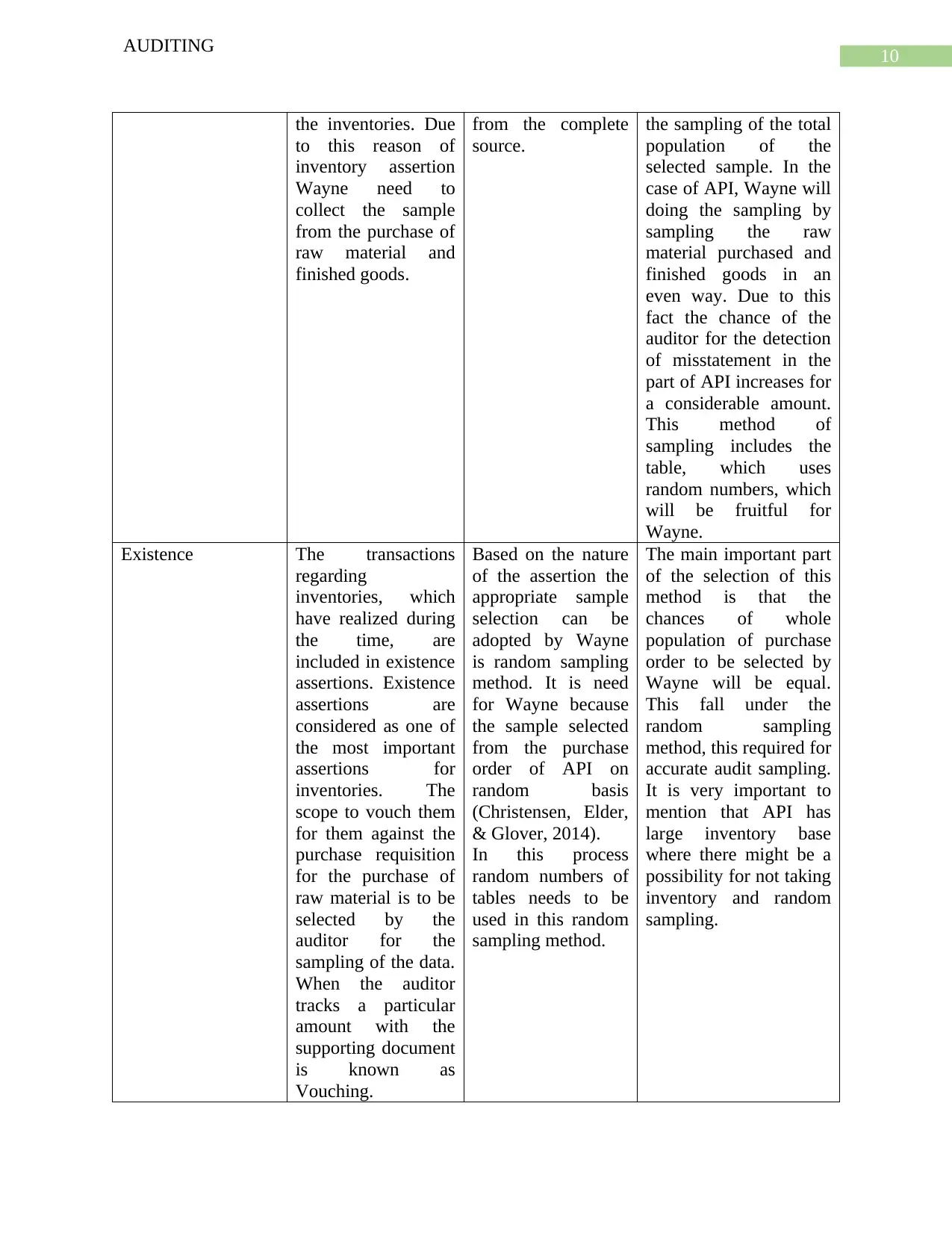

the inventories. Due

to this reason of

inventory assertion

Wayne need to

collect the sample

from the purchase of

raw material and

finished goods.

from the complete

source.

the sampling of the total

population of the

selected sample. In the

case of API, Wayne will

doing the sampling by

sampling the raw

material purchased and

finished goods in an

even way. Due to this

fact the chance of the

auditor for the detection

of misstatement in the

part of API increases for

a considerable amount.

This method of

sampling includes the

table, which uses

random numbers, which

will be fruitful for

Wayne.

Existence The transactions

regarding

inventories, which

have realized during

the time, are

included in existence

assertions. Existence

assertions are

considered as one of

the most important

assertions for

inventories. The

scope to vouch them

for them against the

purchase requisition

for the purchase of

raw material is to be

selected by the

auditor for the

sampling of the data.

When the auditor

tracks a particular

amount with the

supporting document

is known as

Vouching.

Based on the nature

of the assertion the

appropriate sample

selection can be

adopted by Wayne

is random sampling

method. It is need

for Wayne because

the sample selected

from the purchase

order of API on

random basis

(Christensen, Elder,

& Glover, 2014).

In this process

random numbers of

tables needs to be

used in this random

sampling method.

The main important part

of the selection of this

method is that the

chances of whole

population of purchase

order to be selected by

Wayne will be equal.

This fall under the

random sampling

method, this required for

accurate audit sampling.

It is very important to

mention that API has

large inventory base

where there might be a

possibility for not taking

inventory and random

sampling.

AUDITING

the inventories. Due

to this reason of

inventory assertion

Wayne need to

collect the sample

from the purchase of

raw material and

finished goods.

from the complete

source.

the sampling of the total

population of the

selected sample. In the

case of API, Wayne will

doing the sampling by

sampling the raw

material purchased and

finished goods in an

even way. Due to this

fact the chance of the

auditor for the detection

of misstatement in the

part of API increases for

a considerable amount.

This method of

sampling includes the

table, which uses

random numbers, which

will be fruitful for

Wayne.

Existence The transactions

regarding

inventories, which

have realized during

the time, are

included in existence

assertions. Existence

assertions are

considered as one of

the most important

assertions for

inventories. The

scope to vouch them

for them against the

purchase requisition

for the purchase of

raw material is to be

selected by the

auditor for the

sampling of the data.

When the auditor

tracks a particular

amount with the

supporting document

is known as

Vouching.

Based on the nature

of the assertion the

appropriate sample

selection can be

adopted by Wayne

is random sampling

method. It is need

for Wayne because

the sample selected

from the purchase

order of API on

random basis

(Christensen, Elder,

& Glover, 2014).

In this process

random numbers of

tables needs to be

used in this random

sampling method.

The main important part

of the selection of this

method is that the

chances of whole

population of purchase

order to be selected by

Wayne will be equal.

This fall under the

random sampling

method, this required for

accurate audit sampling.

It is very important to

mention that API has

large inventory base

where there might be a

possibility for not taking

inventory and random

sampling.

11

AUDITING

Reference

Appelbaum, D., Kogan, A., & Vasarhelyi, M. A. (2017). Big Data and analytics in the modern

audit engagement: Research needs. Auditing: A Journal of Practice & Theory, 36(4), 1-

27.

Broberg, P., Umans, T., & Gerlofstig, C. (2013). Balance between auditing and marketing: An

explorative study. Journal of International Accounting, Auditing and Taxation, 22(1), 57-

70.

Christensen, B. E., Elder, R. J., & Glover, S. M. (2014). Behind the numbers: Insights into large

audit firm sampling policies. Accounting Horizons, 29(1), 61-81.

Gustavson, M. (2015). Does good auditing generate quality of government?.

Hassan, M. K. (2013). Ethical principles of Islamic financial institutions. Journal of Economic

Cooperation and Development, 34(1), 63-90.

Hay, D. (2014). Auditing, international auditing and the International Journal of

Auditing. International Journal of Auditing, 18(1), 1-1.

Knechel, W. R., & Salterio, S. E. (2016). Auditing: Assurance and risk. Routledge.

Kumar, R., & Sharma, V. (2015). Auditing: Principles and practice. PHI Learning Pvt. Ltd..

Needles, B. E., Powers, M., & Crosson, S. V. (2013). Principles of accounting. Cengage

Learning.

Oprisor, T. (2015). Auditing integrated reports: Are there solutions to this puzzle?. Procedia

Economics and Finance, 25, 87-95.

AUDITING

Reference

Appelbaum, D., Kogan, A., & Vasarhelyi, M. A. (2017). Big Data and analytics in the modern

audit engagement: Research needs. Auditing: A Journal of Practice & Theory, 36(4), 1-

27.

Broberg, P., Umans, T., & Gerlofstig, C. (2013). Balance between auditing and marketing: An

explorative study. Journal of International Accounting, Auditing and Taxation, 22(1), 57-

70.

Christensen, B. E., Elder, R. J., & Glover, S. M. (2014). Behind the numbers: Insights into large

audit firm sampling policies. Accounting Horizons, 29(1), 61-81.

Gustavson, M. (2015). Does good auditing generate quality of government?.

Hassan, M. K. (2013). Ethical principles of Islamic financial institutions. Journal of Economic

Cooperation and Development, 34(1), 63-90.

Hay, D. (2014). Auditing, international auditing and the International Journal of

Auditing. International Journal of Auditing, 18(1), 1-1.

Knechel, W. R., & Salterio, S. E. (2016). Auditing: Assurance and risk. Routledge.

Kumar, R., & Sharma, V. (2015). Auditing: Principles and practice. PHI Learning Pvt. Ltd..

Needles, B. E., Powers, M., & Crosson, S. V. (2013). Principles of accounting. Cengage

Learning.

Oprisor, T. (2015). Auditing integrated reports: Are there solutions to this puzzle?. Procedia

Economics and Finance, 25, 87-95.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13