Auditing Report: QEM Limited Financial Statement and Risk Analysis

VerifiedAdded on 2022/11/29

|18

|4182

|438

Report

AI Summary

This report provides a detailed analysis of the auditing process for QEM Limited, an ASX-listed company involved in energy exploration and development. The report begins with an introduction to auditing and its importance in assessing financial statements. It then explores the nature of QEM Limited, its business risks (operational, financial reporting, and compliance risks), and the application of the audit risk model to determine detection risk. Analytical procedures, including ratio analysis (ROCE, current ratio, accounts receivable turnover, and ROE), are performed to identify potential misstatements. The report also covers the calculation of materiality for audit planning. Furthermore, the report analyzes account balances, audit assertions (revenue, expenses, income tax, and cash and cash equivalents), and outlines appropriate audit works and sampling plans for each assertion. The conclusion summarizes the key findings and the overall auditing process for QEM Limited.

Running head: AUDITING

Auditing

Name of the Student

Name of the University

Author’s Note

Auditing

Name of the Student

Name of the University

Author’s Note

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1AUDITING

Table of Contents

Introduction................................................................................................................................2

Nature of the Entity, Business Risks and Risk Assessment.......................................................2

Analytical Procedures................................................................................................................4

Material Balances and Materiality for Planning........................................................................6

Analysis of Accounts Balances, Assertions, Audit Works and Sampling Plan.........................7

Conclusion................................................................................................................................12

References................................................................................................................................13

Table of Contents

Introduction................................................................................................................................2

Nature of the Entity, Business Risks and Risk Assessment.......................................................2

Analytical Procedures................................................................................................................4

Material Balances and Materiality for Planning........................................................................6

Analysis of Accounts Balances, Assertions, Audit Works and Sampling Plan.........................7

Conclusion................................................................................................................................12

References................................................................................................................................13

2AUDITING

Introduction

Auditing refers to the process to inspect and examine the financial records and

statements of the audit clients for assessing whether there is any material misstatements in

them and whether they have been prepared in accordance with the required accounting rules,

regulations and principles (William Jr, Glover and Prawitt 2016). Analysis of audit risk is one

of the major responsibilities of the auditors whether it is needed to determine the level of

inherent risk, control risk and detection risk. After the process of risk assessment, it is

required for the auditors to adopt the suitable audit procedures for reducing the risk to an

acceptable level. Analytical procedures in auditing involve analysis of ratios that helps in

showing the areas with potential risk of material misstatements (Knechel and Salterio 2016).

In addition, the auditors are needed to assess the audit assertions while developing

appropriate substantive audit procedures and sample plans for them. The main aim of the

report is the analysis of different aspects of auditing for QEM Limited.

Nature of the Entity, Business Risks and Risk Assessment

Nature of Entity – QEM Limited is an ASX listed company involves in the exploration and

development of its flagship Julia Creek Project that covers 249.6 Km2 in the area of Julia

Creek of North Western Queensland. QEM Limited’s shale project is considered as a world

class unique resource that has the potential of delivering innovative energy solutions by

producing energy fuels and vanadium pentoxide. It indicates that QEM Limited operates in

the energy sector and it is involves in complex business operations (qldem.com.au 2019).

Business Risks – It can be seen from the Corporate Governance Plan of QEM Limited that

there are three types of business risks to which the business operations of QEM Limited are

exposed to. These risks are Operational risk, financial reporting risks and compliance risk.

Operational risk in QEM Limited refers to the loss of the company from insufficient or failed

Introduction

Auditing refers to the process to inspect and examine the financial records and

statements of the audit clients for assessing whether there is any material misstatements in

them and whether they have been prepared in accordance with the required accounting rules,

regulations and principles (William Jr, Glover and Prawitt 2016). Analysis of audit risk is one

of the major responsibilities of the auditors whether it is needed to determine the level of

inherent risk, control risk and detection risk. After the process of risk assessment, it is

required for the auditors to adopt the suitable audit procedures for reducing the risk to an

acceptable level. Analytical procedures in auditing involve analysis of ratios that helps in

showing the areas with potential risk of material misstatements (Knechel and Salterio 2016).

In addition, the auditors are needed to assess the audit assertions while developing

appropriate substantive audit procedures and sample plans for them. The main aim of the

report is the analysis of different aspects of auditing for QEM Limited.

Nature of the Entity, Business Risks and Risk Assessment

Nature of Entity – QEM Limited is an ASX listed company involves in the exploration and

development of its flagship Julia Creek Project that covers 249.6 Km2 in the area of Julia

Creek of North Western Queensland. QEM Limited’s shale project is considered as a world

class unique resource that has the potential of delivering innovative energy solutions by

producing energy fuels and vanadium pentoxide. It indicates that QEM Limited operates in

the energy sector and it is involves in complex business operations (qldem.com.au 2019).

Business Risks – It can be seen from the Corporate Governance Plan of QEM Limited that

there are three types of business risks to which the business operations of QEM Limited are

exposed to. These risks are Operational risk, financial reporting risks and compliance risk.

Operational risk in QEM Limited refers to the loss of the company from insufficient or failed

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3AUDITING

processes, procedures and systems within the organization. Financial reporting risk refers to

the risk of material misstatements due to the effects of external environment, external

environmental factors and others. Compliance risk is the risk of exposing to the legal

penalties, material losses and financial forfeitures due to the failure in complying with the

required laws, regulations, internal policies and practices (qldem.com.au 2019).

Risk Assessment – Audit risk is the risk that incorrect opinion is issued by the auditor. The

use of audit risk model can be seen by the auditor and it is as follows:

Audit Risk (AR) = Inherent Risk (IR) × Control Risk (CR) × Detection Risk (DR)

It can be seen from the above that there are three types of audit risks; they are

Inherent Risk, Control Risk and Detection Risk. Inherent risk is the risk of material

misstatements in the financial statements rising because of the errors or omission due to the

results of factors other than the control failures (Griffiths 2016). It can be seen that QEM

Limited is involved in highly complex business environment that can lead to material

misstatements. After that, competition in the industry in which QEM Limited operate is

highly competitive that can lead to material mistsement. Therefore, this risk is high for QEM

Limited.

Control risk is the risk of material misstatement in the financial statement rising

because of the absence or failure of internal control or other relevant controls (Botez 2015).

As per the Corporate Governance Plan of QEM Limited, the company has implemented

effective internal control for the business that includes effective structure of board,

monitoring, risk and compliance management, delegation of authority and others. All these

show that this risk is medium in QEM Limited.

It is assumed that the policy of the audit firm of QEM Limited is to keep the overall

risk below 10%. The inherent risk is assumed to be 70% and control risk is assumed to be

processes, procedures and systems within the organization. Financial reporting risk refers to

the risk of material misstatements due to the effects of external environment, external

environmental factors and others. Compliance risk is the risk of exposing to the legal

penalties, material losses and financial forfeitures due to the failure in complying with the

required laws, regulations, internal policies and practices (qldem.com.au 2019).

Risk Assessment – Audit risk is the risk that incorrect opinion is issued by the auditor. The

use of audit risk model can be seen by the auditor and it is as follows:

Audit Risk (AR) = Inherent Risk (IR) × Control Risk (CR) × Detection Risk (DR)

It can be seen from the above that there are three types of audit risks; they are

Inherent Risk, Control Risk and Detection Risk. Inherent risk is the risk of material

misstatements in the financial statements rising because of the errors or omission due to the

results of factors other than the control failures (Griffiths 2016). It can be seen that QEM

Limited is involved in highly complex business environment that can lead to material

misstatements. After that, competition in the industry in which QEM Limited operate is

highly competitive that can lead to material mistsement. Therefore, this risk is high for QEM

Limited.

Control risk is the risk of material misstatement in the financial statement rising

because of the absence or failure of internal control or other relevant controls (Botez 2015).

As per the Corporate Governance Plan of QEM Limited, the company has implemented

effective internal control for the business that includes effective structure of board,

monitoring, risk and compliance management, delegation of authority and others. All these

show that this risk is medium in QEM Limited.

It is assumed that the policy of the audit firm of QEM Limited is to keep the overall

risk below 10%. The inherent risk is assumed to be 70% and control risk is assumed to be

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4AUDITING

40%. The following discussion shows the application of audit risk model to get the detection

risk level.

AR = IR × CR × DR

0.10 = 0.70 × 0.40 × DR

0.10 / (0.70 × 0.40) = DR

DR = 0.3571 or 35.71%

It implies that the detection risk has to be 35.71% in order to maintain the overall risk

level 10%. It needs to be mentioned that the detection risk is of medium level which required

the application of substantive audit procedures to acquire the required audit evidences (Chou

2015).

Analytical Procedures

The main purpose of performing analytical procedures is to identify the existence of

uncommon financial transactions and events for the purpose of identifying material

misstatements in the financial statements (Plumlee, Rixom and Rosman 2014). The following

discussion shows the analysis of ratios of QEM Limited for the purpose of analytical

procedure

40%. The following discussion shows the application of audit risk model to get the detection

risk level.

AR = IR × CR × DR

0.10 = 0.70 × 0.40 × DR

0.10 / (0.70 × 0.40) = DR

DR = 0.3571 or 35.71%

It implies that the detection risk has to be 35.71% in order to maintain the overall risk

level 10%. It needs to be mentioned that the detection risk is of medium level which required

the application of substantive audit procedures to acquire the required audit evidences (Chou

2015).

Analytical Procedures

The main purpose of performing analytical procedures is to identify the existence of

uncommon financial transactions and events for the purpose of identifying material

misstatements in the financial statements (Plumlee, Rixom and Rosman 2014). The following

discussion shows the analysis of ratios of QEM Limited for the purpose of analytical

procedure

5AUDITING

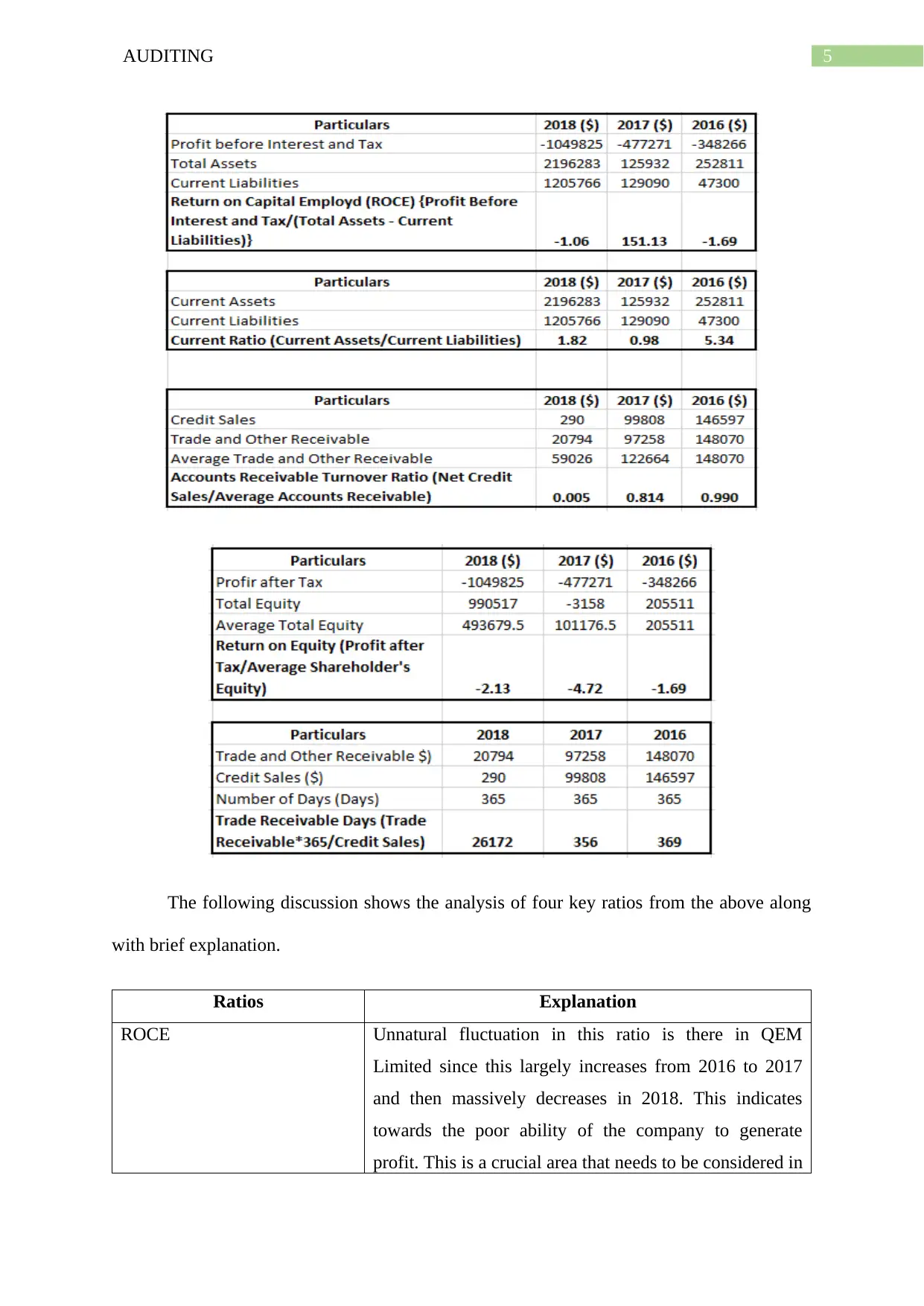

The following discussion shows the analysis of four key ratios from the above along

with brief explanation.

Ratios Explanation

ROCE Unnatural fluctuation in this ratio is there in QEM

Limited since this largely increases from 2016 to 2017

and then massively decreases in 2018. This indicates

towards the poor ability of the company to generate

profit. This is a crucial area that needs to be considered in

The following discussion shows the analysis of four key ratios from the above along

with brief explanation.

Ratios Explanation

ROCE Unnatural fluctuation in this ratio is there in QEM

Limited since this largely increases from 2016 to 2017

and then massively decreases in 2018. This indicates

towards the poor ability of the company to generate

profit. This is a crucial area that needs to be considered in

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6AUDITING

the audit of QEM Limited for assessing any kind of

manipulation in this (Jans, Alles and Vasarhelyi 2014).

Current ratio This ratio has largely decreases in 2017 and then

increases in 2018. This indicates towards the potential of

the occurrence of any kind of manipulation with the

current account balances for increasing the liquidity of

QEM Limited in manipulative manner. For this reason,

this ratio needs to be considered in the final audit of the

company (Titera 2013).

Accounts Receivable Turnover This particular ratio has a decreasing trend since it has

decreased from 2016 to 2018. This indicates towards the

decreased ability of QEM Limited to collect its average

accounts receivable. This is a crucial aspect in the final

audit of the company which indicates towards the

presence of material misstatements in the financial

statements (Jans, Alles and Vasarhelyi 2014).

ROE It can be seen that QEM Limited has not been able in

registering positive ROE from 2016 to 2018. In addition,

there is major fluctuation in this ratio. This is a crucial

aspect that must be considered in the audit of QEM

Limited since there can be manipulation in the balances

of equity and profitability of QEM Limited (Titera 2013).

Materiality for Planning

Calculation of materiality is a crucial aspect in audit planning. There are certain steps

that need to be considered for the calculation of materiality. They are as follows:

1. It is needed to select the appropriate base or benchmark in order for the determination

of materiality and certain aspects like nature of the business entity and nature of the

industry are needed to be considered for this. The commonly used bases are profit

the audit of QEM Limited for assessing any kind of

manipulation in this (Jans, Alles and Vasarhelyi 2014).

Current ratio This ratio has largely decreases in 2017 and then

increases in 2018. This indicates towards the potential of

the occurrence of any kind of manipulation with the

current account balances for increasing the liquidity of

QEM Limited in manipulative manner. For this reason,

this ratio needs to be considered in the final audit of the

company (Titera 2013).

Accounts Receivable Turnover This particular ratio has a decreasing trend since it has

decreased from 2016 to 2018. This indicates towards the

decreased ability of QEM Limited to collect its average

accounts receivable. This is a crucial aspect in the final

audit of the company which indicates towards the

presence of material misstatements in the financial

statements (Jans, Alles and Vasarhelyi 2014).

ROE It can be seen that QEM Limited has not been able in

registering positive ROE from 2016 to 2018. In addition,

there is major fluctuation in this ratio. This is a crucial

aspect that must be considered in the audit of QEM

Limited since there can be manipulation in the balances

of equity and profitability of QEM Limited (Titera 2013).

Materiality for Planning

Calculation of materiality is a crucial aspect in audit planning. There are certain steps

that need to be considered for the calculation of materiality. They are as follows:

1. It is needed to select the appropriate base or benchmark in order for the determination

of materiality and certain aspects like nature of the business entity and nature of the

industry are needed to be considered for this. The commonly used bases are profit

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7AUDITING

before tax, total assets, revenue and others. In case of QEM Limited, total assets

($2,196,283) is selected as the base (Eilifsen and Messier Jr 2014).

2. Selection of appropriate percentage is required that will be charged on the selected

base. Professional judgments of the auditors plays a crucial role in this selection. As

per AASB 1031 Materiality, this percentage can be either greater than or equal to

10% of less than or equal to 5%. Based on the judgement of the auditors, 5% is

considered as the appropriate percentage that needs to be charged on the selected base

(Vîlsănoiu and Buzenche 2014).

3. Based on the above-selected base and percentage, the calculation of the materiality of

QEM Limited is done. The calculation is shown below:

Materiality = Total Assets × 5%

= $2,196,283 × 5%

= $109,814 (approximately)

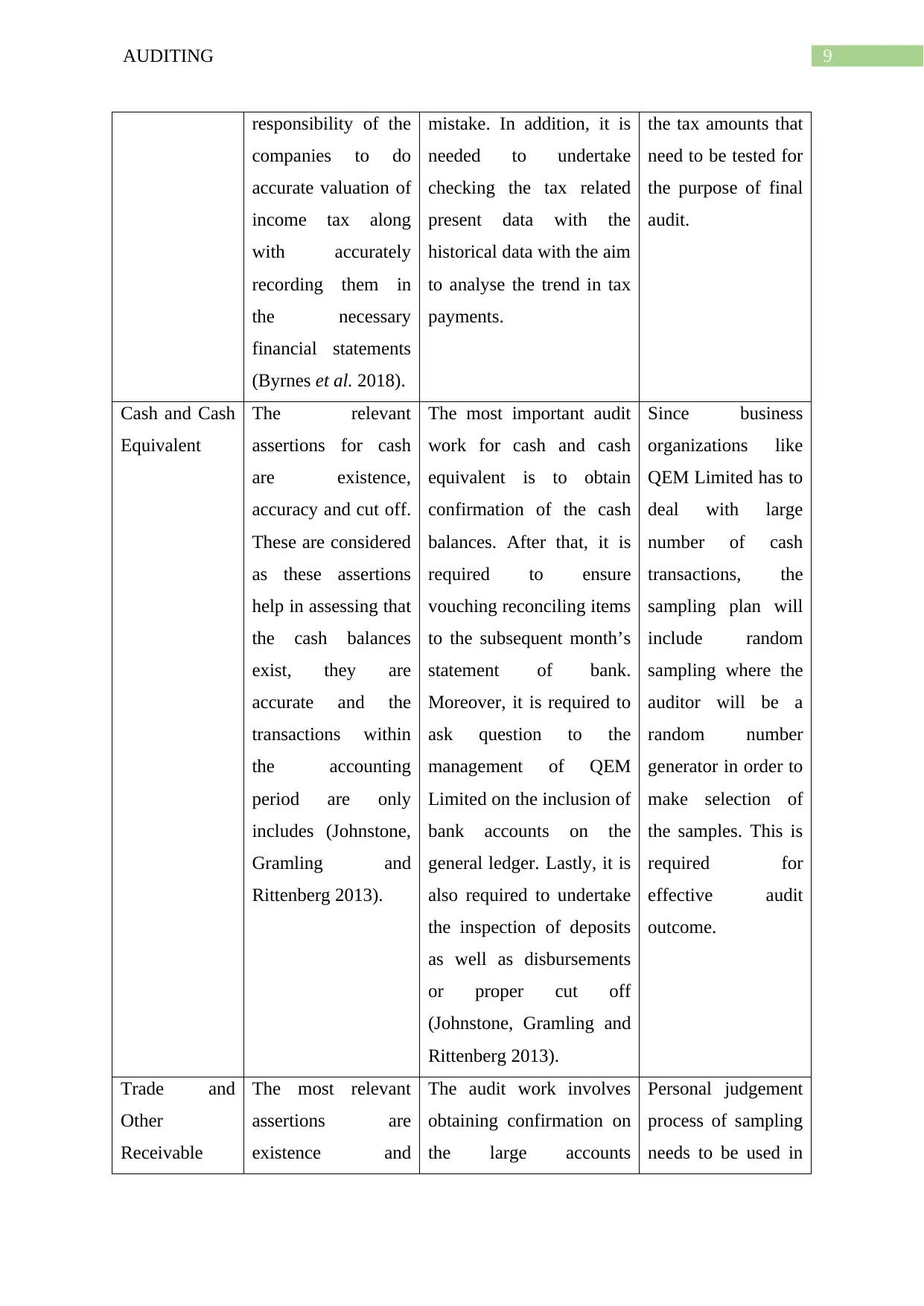

Analysis of Accounts Balances, Assertions, Audit Works and Sampling Plan

Material

Account

Balances

Assertions Comprehensive Set of

Audit Works

Sampling Plan

Revenue The most relevant

assertion for revenue

is relevance because

it helps in

ascertaining that

whether revenues

have occurred or not

(Kharisova and

Kozlova 2014).

The audit work is the

development of

comparative summaries of

all the major revenue

accounts while comparing

the date of the present year

with the data of the past

years. Moreover, it is

needed to check the

invoices in order to get

It is needed to adopt

random sampling

for the testing of

revenue where it is

needed to select

certain samples

from the large

population of

revenue. In this

process, it is needed

before tax, total assets, revenue and others. In case of QEM Limited, total assets

($2,196,283) is selected as the base (Eilifsen and Messier Jr 2014).

2. Selection of appropriate percentage is required that will be charged on the selected

base. Professional judgments of the auditors plays a crucial role in this selection. As

per AASB 1031 Materiality, this percentage can be either greater than or equal to

10% of less than or equal to 5%. Based on the judgement of the auditors, 5% is

considered as the appropriate percentage that needs to be charged on the selected base

(Vîlsănoiu and Buzenche 2014).

3. Based on the above-selected base and percentage, the calculation of the materiality of

QEM Limited is done. The calculation is shown below:

Materiality = Total Assets × 5%

= $2,196,283 × 5%

= $109,814 (approximately)

Analysis of Accounts Balances, Assertions, Audit Works and Sampling Plan

Material

Account

Balances

Assertions Comprehensive Set of

Audit Works

Sampling Plan

Revenue The most relevant

assertion for revenue

is relevance because

it helps in

ascertaining that

whether revenues

have occurred or not

(Kharisova and

Kozlova 2014).

The audit work is the

development of

comparative summaries of

all the major revenue

accounts while comparing

the date of the present year

with the data of the past

years. Moreover, it is

needed to check the

invoices in order to get

It is needed to adopt

random sampling

for the testing of

revenue where it is

needed to select

certain samples

from the large

population of

revenue. In this

process, it is needed

8AUDITING

confirmation on the

occurrence of sales. In

addition, it is needed to

verify QEM Limited’s

completeness of revenue,

accuracy of financial data,

recognition of revenue and

others.

to ensure that the

samples are being

collected from the

revenue sources

which are material

as well as complex

in nature. This will

lead to effective

audit results (Elder

et al. 2013).

Expenses Completeness and

cut off are the two

most relevant

assertions associated

with expenses. At

the time of recording

the expenses by

period-end, QEM

Limited is needed to

ensure that they are

completed and they

are recorded for the

right period (Brown-

Liburd and

Vasarhelyi 2015).

The audit work involves in

the scanning of the check

register of QEM Limited.

After that, the expenses

are required to be sorted

by the vendors. It is

required to scan the check

register in order to obtain

information on the fact

that whether double

payment has been made to

the same vendor. Lastly, it

is required to enquire

about the payments made

to the same vendor

(Byrnes et al. 2018).

It is needed to adopt

random sampling

strategy due to the

large amount of

expenses of QEM

Limited. In this

process, a random

number generator

will be used with the

aim to collect the

samples from the

large population of

expenses. This is

one of the most

effective techniques

of sampling.

Income Tax The main audit

assertion related to

income tax is

accuracy. The main

reason for selecting

this assertion is that

it is the

The main audit work in

order to obtain the

required audit evidence on

income tax is to check the

tax calculation mechanism

of the company in order to

make sure it is free from

In order to test this

particular aspect,

personal judgment

sampling technique

needs to be used due

to the fact that the

auditor will select

confirmation on the

occurrence of sales. In

addition, it is needed to

verify QEM Limited’s

completeness of revenue,

accuracy of financial data,

recognition of revenue and

others.

to ensure that the

samples are being

collected from the

revenue sources

which are material

as well as complex

in nature. This will

lead to effective

audit results (Elder

et al. 2013).

Expenses Completeness and

cut off are the two

most relevant

assertions associated

with expenses. At

the time of recording

the expenses by

period-end, QEM

Limited is needed to

ensure that they are

completed and they

are recorded for the

right period (Brown-

Liburd and

Vasarhelyi 2015).

The audit work involves in

the scanning of the check

register of QEM Limited.

After that, the expenses

are required to be sorted

by the vendors. It is

required to scan the check

register in order to obtain

information on the fact

that whether double

payment has been made to

the same vendor. Lastly, it

is required to enquire

about the payments made

to the same vendor

(Byrnes et al. 2018).

It is needed to adopt

random sampling

strategy due to the

large amount of

expenses of QEM

Limited. In this

process, a random

number generator

will be used with the

aim to collect the

samples from the

large population of

expenses. This is

one of the most

effective techniques

of sampling.

Income Tax The main audit

assertion related to

income tax is

accuracy. The main

reason for selecting

this assertion is that

it is the

The main audit work in

order to obtain the

required audit evidence on

income tax is to check the

tax calculation mechanism

of the company in order to

make sure it is free from

In order to test this

particular aspect,

personal judgment

sampling technique

needs to be used due

to the fact that the

auditor will select

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9AUDITING

responsibility of the

companies to do

accurate valuation of

income tax along

with accurately

recording them in

the necessary

financial statements

(Byrnes et al. 2018).

mistake. In addition, it is

needed to undertake

checking the tax related

present data with the

historical data with the aim

to analyse the trend in tax

payments.

the tax amounts that

need to be tested for

the purpose of final

audit.

Cash and Cash

Equivalent

The relevant

assertions for cash

are existence,

accuracy and cut off.

These are considered

as these assertions

help in assessing that

the cash balances

exist, they are

accurate and the

transactions within

the accounting

period are only

includes (Johnstone,

Gramling and

Rittenberg 2013).

The most important audit

work for cash and cash

equivalent is to obtain

confirmation of the cash

balances. After that, it is

required to ensure

vouching reconciling items

to the subsequent month’s

statement of bank.

Moreover, it is required to

ask question to the

management of QEM

Limited on the inclusion of

bank accounts on the

general ledger. Lastly, it is

also required to undertake

the inspection of deposits

as well as disbursements

or proper cut off

(Johnstone, Gramling and

Rittenberg 2013).

Since business

organizations like

QEM Limited has to

deal with large

number of cash

transactions, the

sampling plan will

include random

sampling where the

auditor will be a

random number

generator in order to

make selection of

the samples. This is

required for

effective audit

outcome.

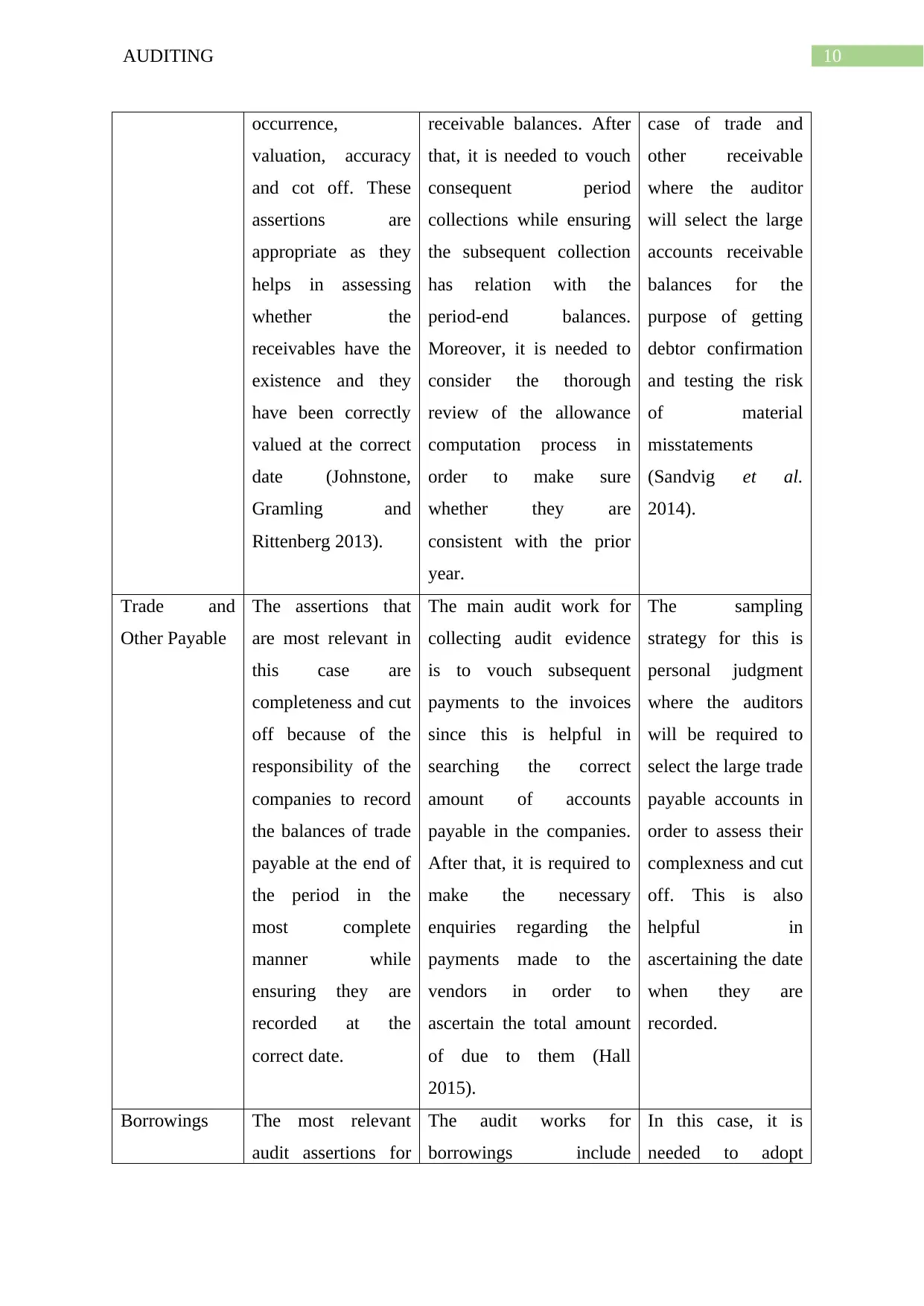

Trade and

Other

Receivable

The most relevant

assertions are

existence and

The audit work involves

obtaining confirmation on

the large accounts

Personal judgement

process of sampling

needs to be used in

responsibility of the

companies to do

accurate valuation of

income tax along

with accurately

recording them in

the necessary

financial statements

(Byrnes et al. 2018).

mistake. In addition, it is

needed to undertake

checking the tax related

present data with the

historical data with the aim

to analyse the trend in tax

payments.

the tax amounts that

need to be tested for

the purpose of final

audit.

Cash and Cash

Equivalent

The relevant

assertions for cash

are existence,

accuracy and cut off.

These are considered

as these assertions

help in assessing that

the cash balances

exist, they are

accurate and the

transactions within

the accounting

period are only

includes (Johnstone,

Gramling and

Rittenberg 2013).

The most important audit

work for cash and cash

equivalent is to obtain

confirmation of the cash

balances. After that, it is

required to ensure

vouching reconciling items

to the subsequent month’s

statement of bank.

Moreover, it is required to

ask question to the

management of QEM

Limited on the inclusion of

bank accounts on the

general ledger. Lastly, it is

also required to undertake

the inspection of deposits

as well as disbursements

or proper cut off

(Johnstone, Gramling and

Rittenberg 2013).

Since business

organizations like

QEM Limited has to

deal with large

number of cash

transactions, the

sampling plan will

include random

sampling where the

auditor will be a

random number

generator in order to

make selection of

the samples. This is

required for

effective audit

outcome.

Trade and

Other

Receivable

The most relevant

assertions are

existence and

The audit work involves

obtaining confirmation on

the large accounts

Personal judgement

process of sampling

needs to be used in

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10AUDITING

occurrence,

valuation, accuracy

and cot off. These

assertions are

appropriate as they

helps in assessing

whether the

receivables have the

existence and they

have been correctly

valued at the correct

date (Johnstone,

Gramling and

Rittenberg 2013).

receivable balances. After

that, it is needed to vouch

consequent period

collections while ensuring

the subsequent collection

has relation with the

period-end balances.

Moreover, it is needed to

consider the thorough

review of the allowance

computation process in

order to make sure

whether they are

consistent with the prior

year.

case of trade and

other receivable

where the auditor

will select the large

accounts receivable

balances for the

purpose of getting

debtor confirmation

and testing the risk

of material

misstatements

(Sandvig et al.

2014).

Trade and

Other Payable

The assertions that

are most relevant in

this case are

completeness and cut

off because of the

responsibility of the

companies to record

the balances of trade

payable at the end of

the period in the

most complete

manner while

ensuring they are

recorded at the

correct date.

The main audit work for

collecting audit evidence

is to vouch subsequent

payments to the invoices

since this is helpful in

searching the correct

amount of accounts

payable in the companies.

After that, it is required to

make the necessary

enquiries regarding the

payments made to the

vendors in order to

ascertain the total amount

of due to them (Hall

2015).

The sampling

strategy for this is

personal judgment

where the auditors

will be required to

select the large trade

payable accounts in

order to assess their

complexness and cut

off. This is also

helpful in

ascertaining the date

when they are

recorded.

Borrowings The most relevant

audit assertions for

The audit works for

borrowings include

In this case, it is

needed to adopt

occurrence,

valuation, accuracy

and cot off. These

assertions are

appropriate as they

helps in assessing

whether the

receivables have the

existence and they

have been correctly

valued at the correct

date (Johnstone,

Gramling and

Rittenberg 2013).

receivable balances. After

that, it is needed to vouch

consequent period

collections while ensuring

the subsequent collection

has relation with the

period-end balances.

Moreover, it is needed to

consider the thorough

review of the allowance

computation process in

order to make sure

whether they are

consistent with the prior

year.

case of trade and

other receivable

where the auditor

will select the large

accounts receivable

balances for the

purpose of getting

debtor confirmation

and testing the risk

of material

misstatements

(Sandvig et al.

2014).

Trade and

Other Payable

The assertions that

are most relevant in

this case are

completeness and cut

off because of the

responsibility of the

companies to record

the balances of trade

payable at the end of

the period in the

most complete

manner while

ensuring they are

recorded at the

correct date.

The main audit work for

collecting audit evidence

is to vouch subsequent

payments to the invoices

since this is helpful in

searching the correct

amount of accounts

payable in the companies.

After that, it is required to

make the necessary

enquiries regarding the

payments made to the

vendors in order to

ascertain the total amount

of due to them (Hall

2015).

The sampling

strategy for this is

personal judgment

where the auditors

will be required to

select the large trade

payable accounts in

order to assess their

complexness and cut

off. This is also

helpful in

ascertaining the date

when they are

recorded.

Borrowings The most relevant

audit assertions for

The audit works for

borrowings include

In this case, it is

needed to adopt

11AUDITING

borrowings are

completeness and

classification. When

a firm shows debt on

the balance sheet, it

assets that it has

correctly completed

as well as classified

them. It implies they

have correctly

classified them as

long-term or short-

term basis (Byrnes

et al. 2018).

summarization as well as

testing of the debt

agreements. After that, it is

needed to review new

leases for determining in

case there is any

possibility to record them.

Moreover, confirmation of

all major debts with the

lenders need to be

obtained. After that, it is

required to determine that

there is the classification

of all debts appropriately.

It is needed to agree on the

end-period balances in the

general ledger to the

schedule of amortization.

Lastly, it is needed to

review the accruals for

major amount of interests

while reviewing the

interest expenses by

comparing the current and

prior year.

personal judgment

form of sampling

where the auditor

will select the major

debt accounts with

the aim to analyse

them. This sampling

procedure is

significant for

gaining the

appropriate audit

outcome for the

auditors.

Reserves There are two

assertions that are

relevant to reserve

which are

completeness and

accuracy as the

managements of the

companies assert that

The main audit work is to

review and check the

suitability of methodology

that have been used for the

purpose of calculating

reserves. After that, it is

needed to assess the fact

that whether the company

In case of reserves,

the need is to adopt

personal judgement

as the sampling

procedure where it

will be needed for

the auditor to select

the specific balances

borrowings are

completeness and

classification. When

a firm shows debt on

the balance sheet, it

assets that it has

correctly completed

as well as classified

them. It implies they

have correctly

classified them as

long-term or short-

term basis (Byrnes

et al. 2018).

summarization as well as

testing of the debt

agreements. After that, it is

needed to review new

leases for determining in

case there is any

possibility to record them.

Moreover, confirmation of

all major debts with the

lenders need to be

obtained. After that, it is

required to determine that

there is the classification

of all debts appropriately.

It is needed to agree on the

end-period balances in the

general ledger to the

schedule of amortization.

Lastly, it is needed to

review the accruals for

major amount of interests

while reviewing the

interest expenses by

comparing the current and

prior year.

personal judgment

form of sampling

where the auditor

will select the major

debt accounts with

the aim to analyse

them. This sampling

procedure is

significant for

gaining the

appropriate audit

outcome for the

auditors.

Reserves There are two

assertions that are

relevant to reserve

which are

completeness and

accuracy as the

managements of the

companies assert that

The main audit work is to

review and check the

suitability of methodology

that have been used for the

purpose of calculating

reserves. After that, it is

needed to assess the fact

that whether the company

In case of reserves,

the need is to adopt

personal judgement

as the sampling

procedure where it

will be needed for

the auditor to select

the specific balances

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 18

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.