Audit of Cloud 9 Inc.: Planning Materiality, Analytical Procedures

VerifiedAdded on 2023/04/25

|13

|2171

|486

Report

AI Summary

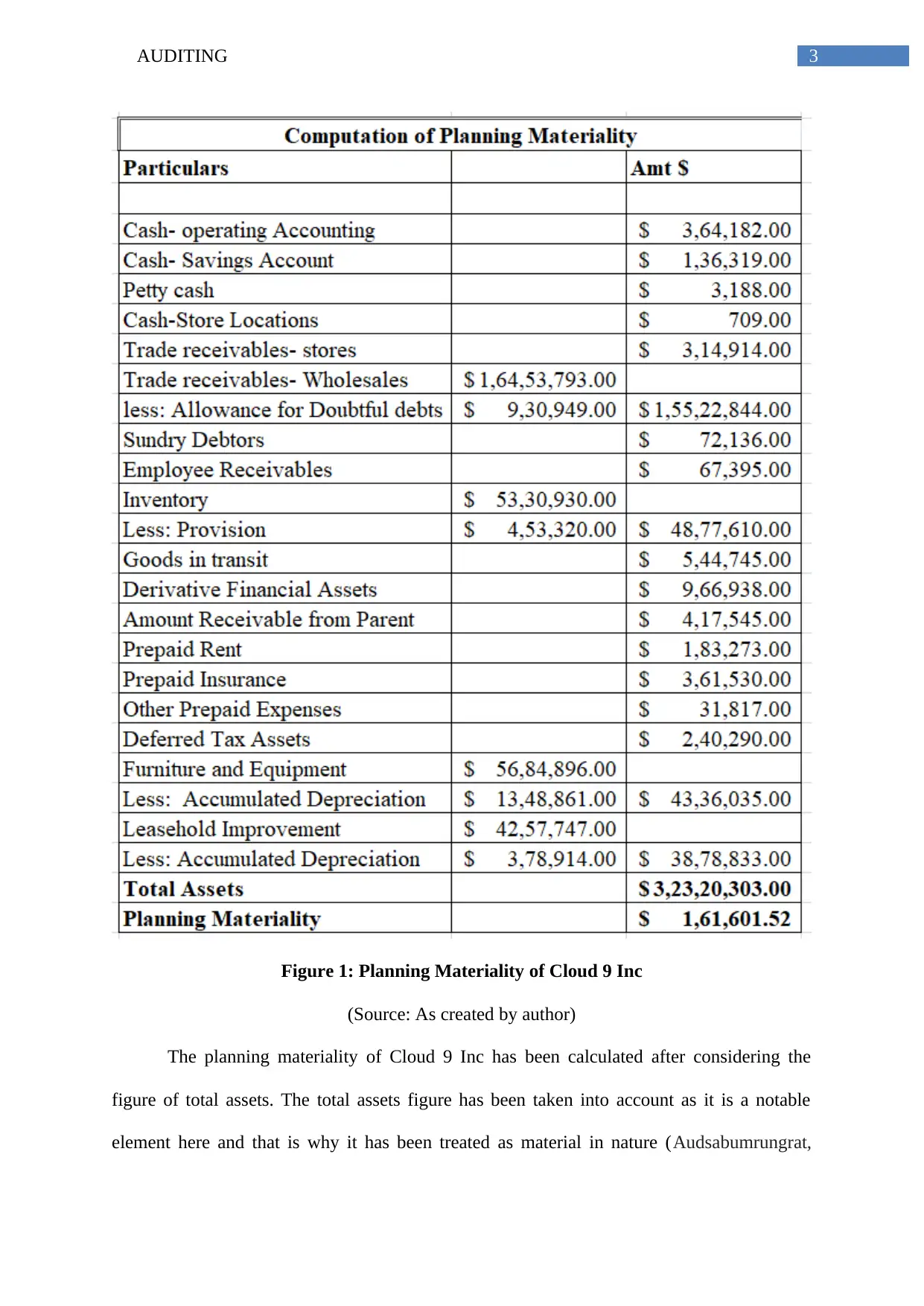

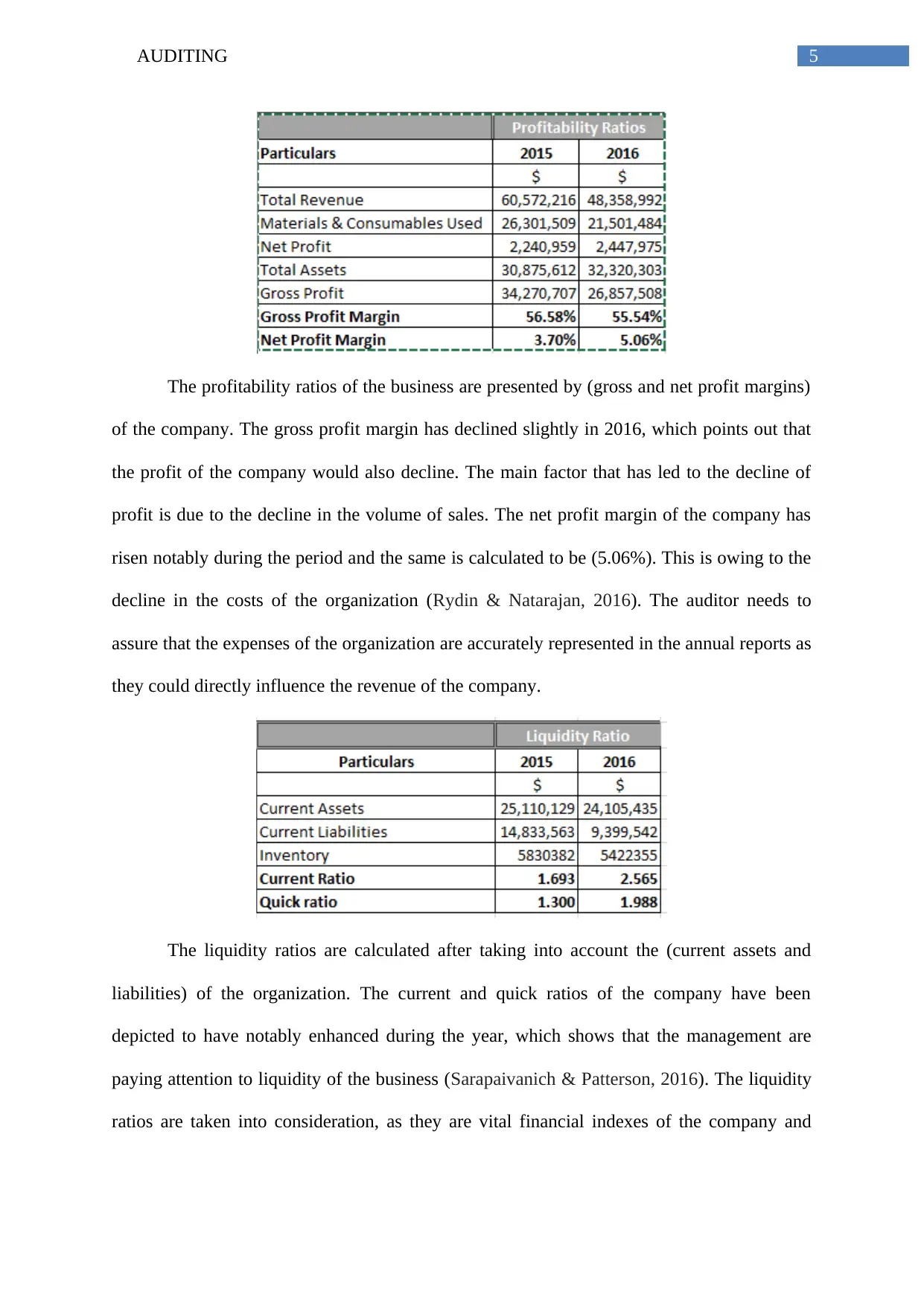

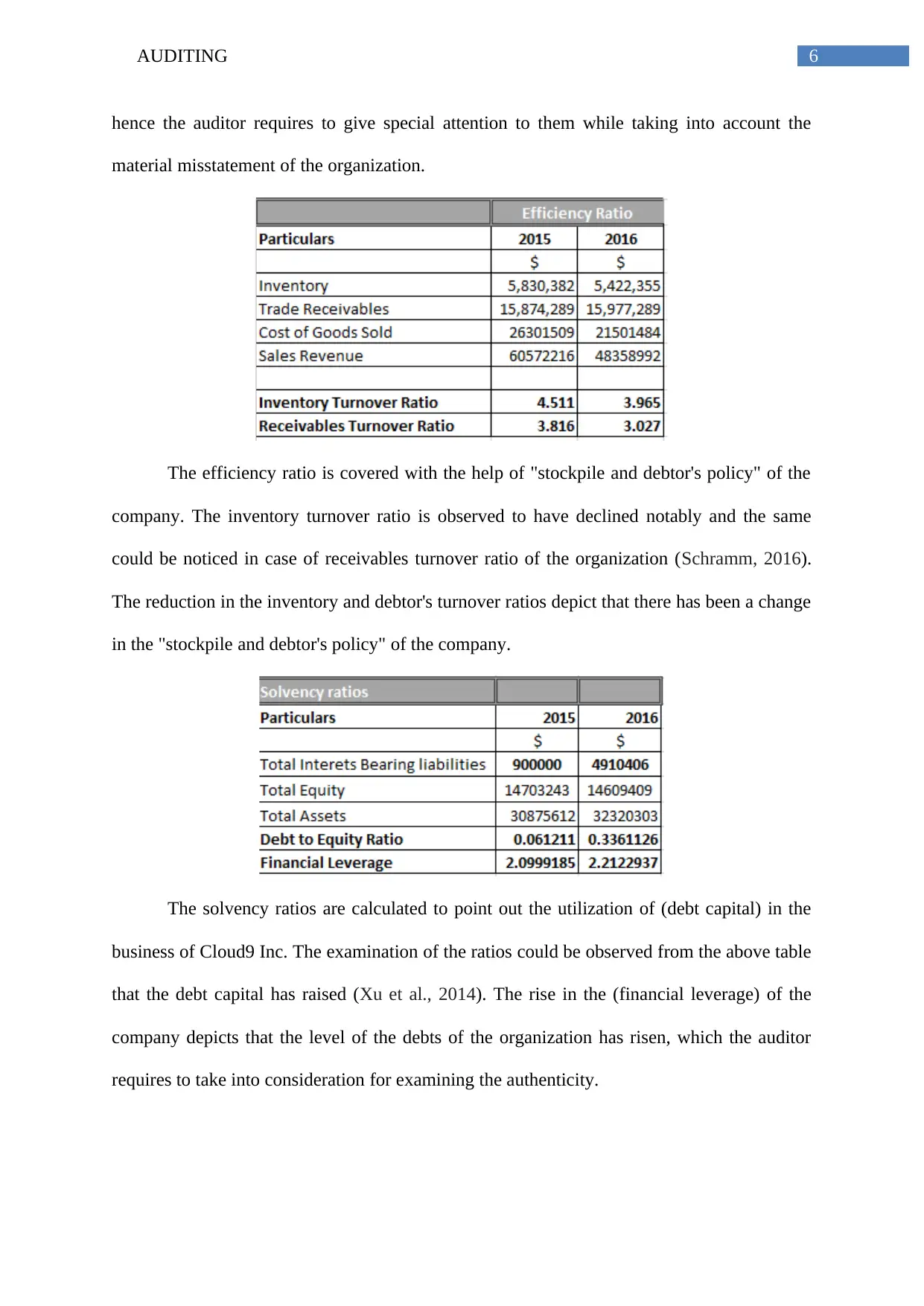

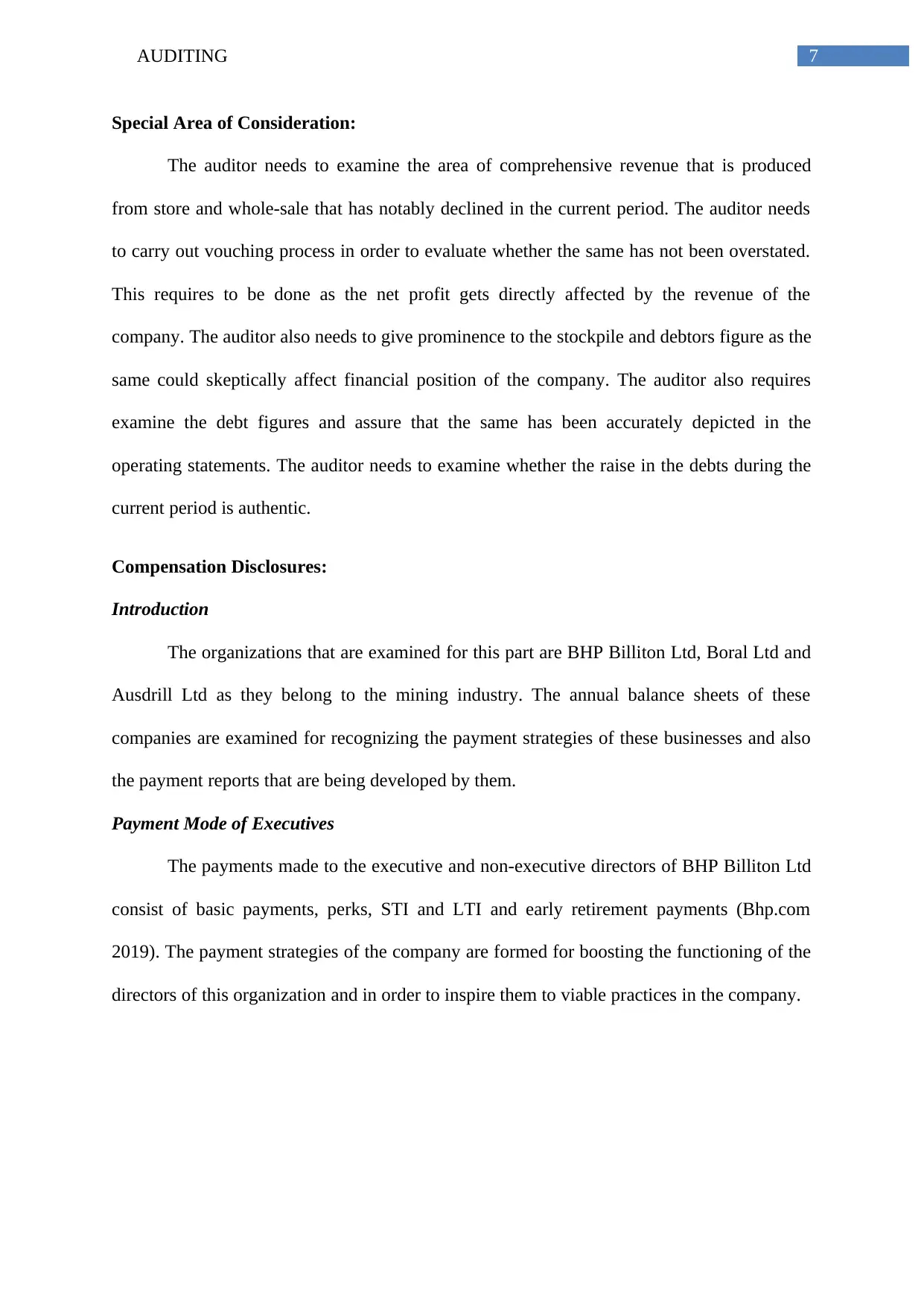

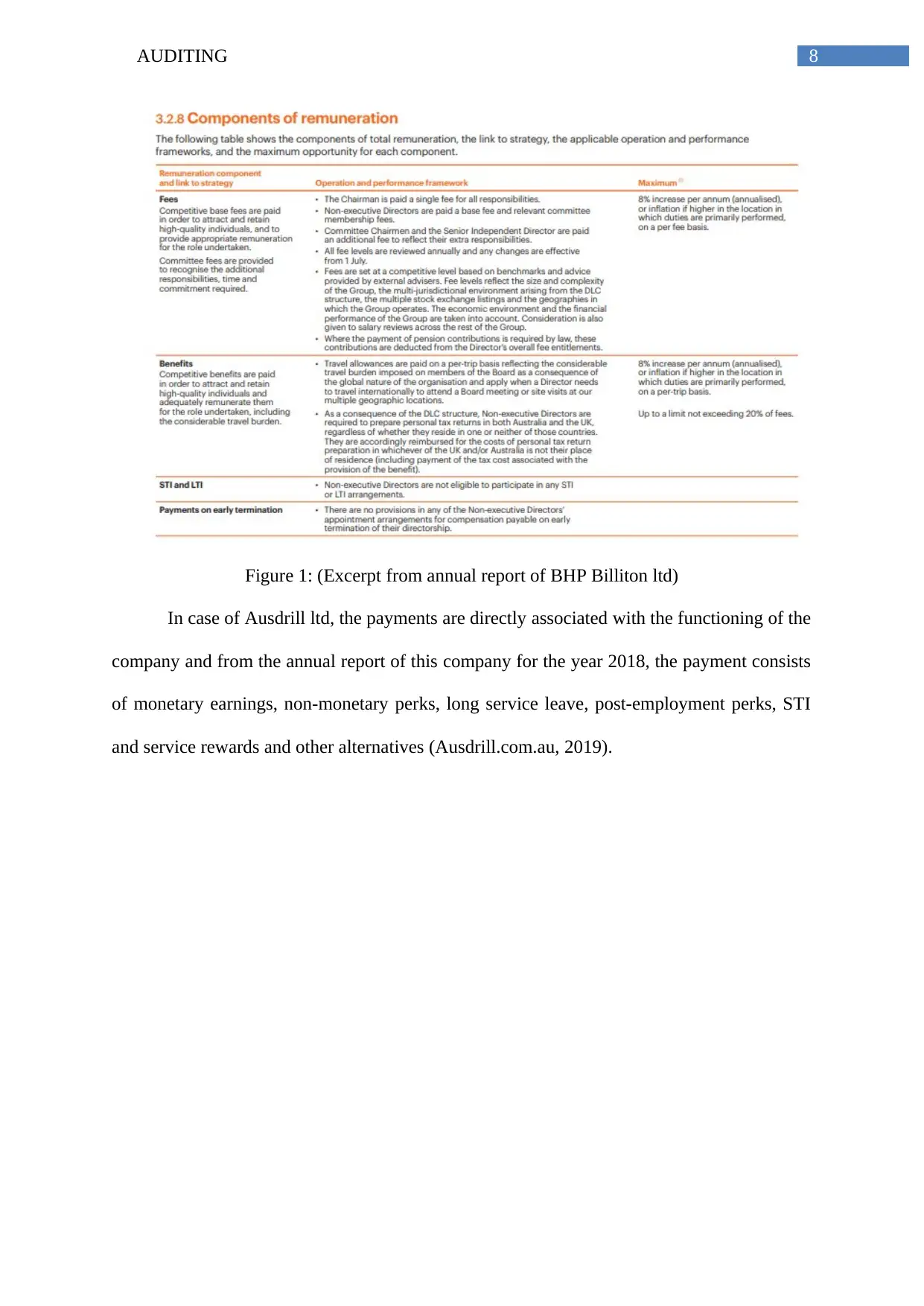

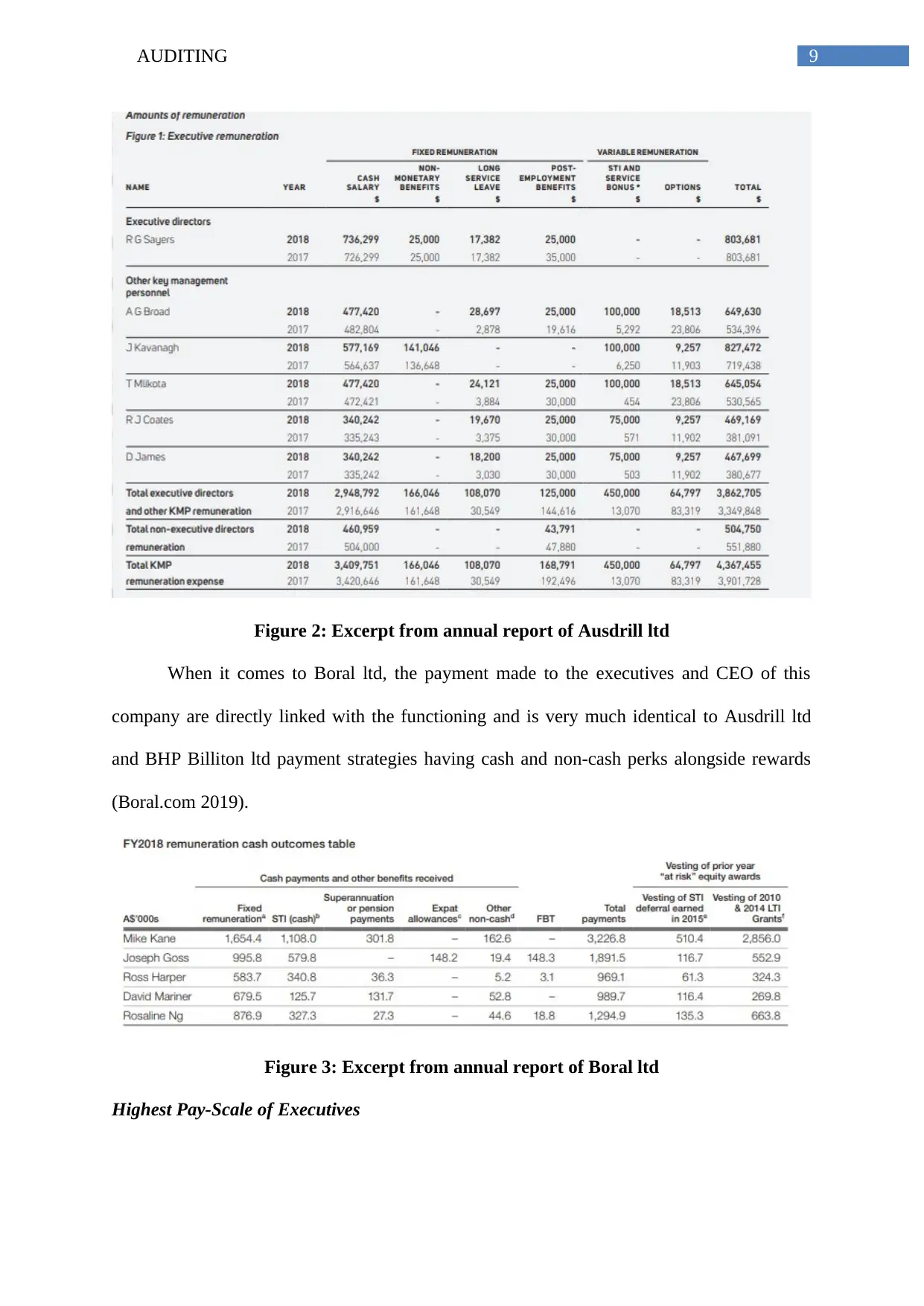

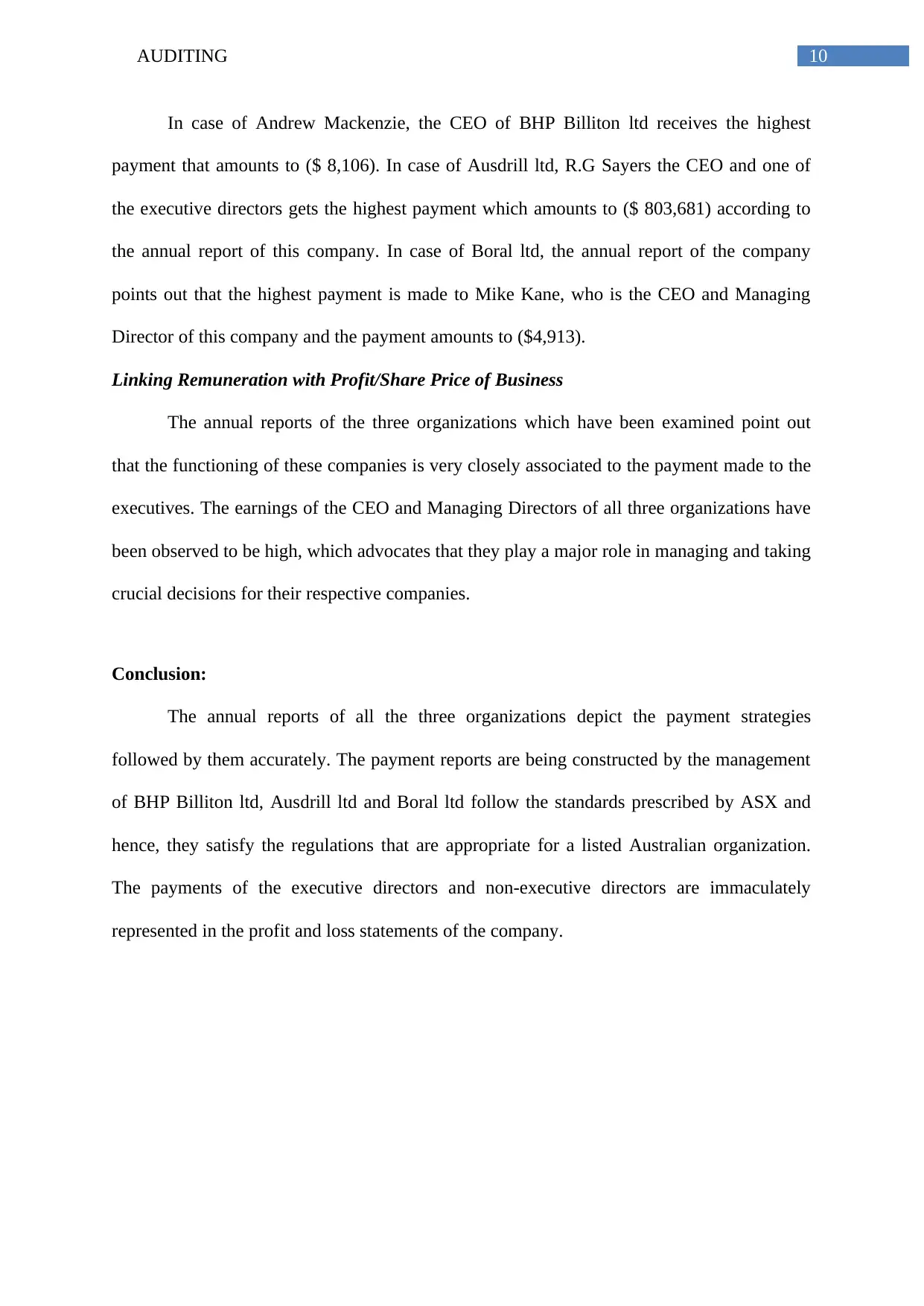

This report provides a detailed analysis of auditing procedures, focusing on the computation of planning materiality and the application of analytical procedures. It begins by defining planning materiality and its importance in assessing the misstatement level of an organization's operating statements, using Cloud 9 Inc., a basketball shoe manufacturer, as a case study. The report includes a calculation of Cloud 9 Inc.'s planning materiality based on total assets, highlighting the significance of current assets. Furthermore, it examines the company's operating statement through financial ratio analysis, covering profitability, liquidity, efficiency, and solvency. Special attention is given to areas such as revenue from store and wholesale activities, stockpile and debtors figures, and debt figures. The report also delves into compensation disclosures within the mining industry, examining BHP Billiton Ltd, Boral Ltd, and Ausdrill Ltd, and linking executive remuneration with company performance. The report concludes that the payment reports are being constructed by the management of BHP Billiton ltd, Ausdrill ltd and Boral ltd follow the standards prescribed by ASX.

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.