ACCT20075 - Auditing and Ethics Report: Financial Analysis and Opinion

VerifiedAdded on 2023/06/07

|11

|3043

|409

Report

AI Summary

This report provides an analysis of auditing and ethics principles, focusing on the case of Beach Energy Limited. It begins with an examination of materiality, adhering to ISA 320, and determining materiality levels based on revenue, profit, and other expenses. The report then addresses the risk-prone area of related party transactions, establishing materiality and performance levels. Subsequently, it delves into analytical review, evaluating the company's financial performance through various ratios such as current ratio, quick ratio, debt-to-equity ratio, debt-to-assets ratio, gross profit ratio, and net profit margin. The analysis includes a comparison of the company's performance over several years, highlighting trends and potential risks. The report concludes by summarizing the findings and offering insights into the company's financial position, based on the application of auditing standards and procedures.

Auditing & Ethics

Auditing & Ethics

1 | P a g e

Auditing & Ethics

1 | P a g e

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Auditing & Ethics

Table of Contents

Brief:......................................................................................................................................................3

Materiality:............................................................................................................................................3

Analytical Review:..................................................................................................................................4

Cash Flow Analysis:................................................................................................................................6

Opinion:.................................................................................................................................................7

References:............................................................................................................................................8

2 | P a g e

Table of Contents

Brief:......................................................................................................................................................3

Materiality:............................................................................................................................................3

Analytical Review:..................................................................................................................................4

Cash Flow Analysis:................................................................................................................................6

Opinion:.................................................................................................................................................7

References:............................................................................................................................................8

2 | P a g e

Auditing & Ethics

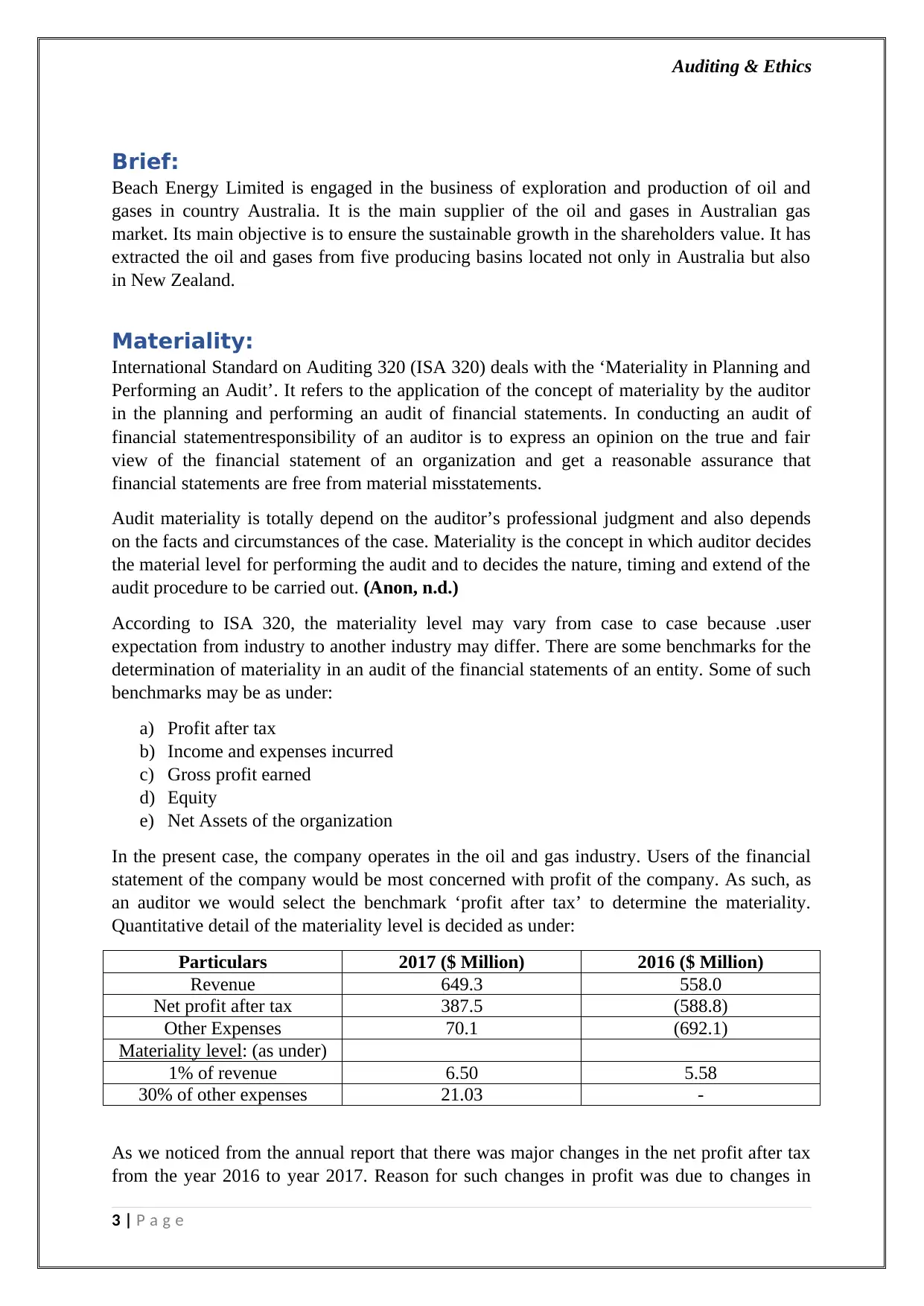

Brief:

Beach Energy Limited is engaged in the business of exploration and production of oil and

gases in country Australia. It is the main supplier of the oil and gases in Australian gas

market. Its main objective is to ensure the sustainable growth in the shareholders value. It has

extracted the oil and gases from five producing basins located not only in Australia but also

in New Zealand.

Materiality:

International Standard on Auditing 320 (ISA 320) deals with the ‘Materiality in Planning and

Performing an Audit’. It refers to the application of the concept of materiality by the auditor

in the planning and performing an audit of financial statements. In conducting an audit of

financial statementresponsibility of an auditor is to express an opinion on the true and fair

view of the financial statement of an organization and get a reasonable assurance that

financial statements are free from material misstatements.

Audit materiality is totally depend on the auditor’s professional judgment and also depends

on the facts and circumstances of the case. Materiality is the concept in which auditor decides

the material level for performing the audit and to decides the nature, timing and extend of the

audit procedure to be carried out. (Anon, n.d.)

According to ISA 320, the materiality level may vary from case to case because .user

expectation from industry to another industry may differ. There are some benchmarks for the

determination of materiality in an audit of the financial statements of an entity. Some of such

benchmarks may be as under:

a) Profit after tax

b) Income and expenses incurred

c) Gross profit earned

d) Equity

e) Net Assets of the organization

In the present case, the company operates in the oil and gas industry. Users of the financial

statement of the company would be most concerned with profit of the company. As such, as

an auditor we would select the benchmark ‘profit after tax’ to determine the materiality.

Quantitative detail of the materiality level is decided as under:

Particulars 2017 ($ Million) 2016 ($ Million)

Revenue 649.3 558.0

Net profit after tax 387.5 (588.8)

Other Expenses 70.1 (692.1)

Materiality level: (as under)

1% of revenue 6.50 5.58

30% of other expenses 21.03 -

As we noticed from the annual report that there was major changes in the net profit after tax

from the year 2016 to year 2017. Reason for such changes in profit was due to changes in

3 | P a g e

Brief:

Beach Energy Limited is engaged in the business of exploration and production of oil and

gases in country Australia. It is the main supplier of the oil and gases in Australian gas

market. Its main objective is to ensure the sustainable growth in the shareholders value. It has

extracted the oil and gases from five producing basins located not only in Australia but also

in New Zealand.

Materiality:

International Standard on Auditing 320 (ISA 320) deals with the ‘Materiality in Planning and

Performing an Audit’. It refers to the application of the concept of materiality by the auditor

in the planning and performing an audit of financial statements. In conducting an audit of

financial statementresponsibility of an auditor is to express an opinion on the true and fair

view of the financial statement of an organization and get a reasonable assurance that

financial statements are free from material misstatements.

Audit materiality is totally depend on the auditor’s professional judgment and also depends

on the facts and circumstances of the case. Materiality is the concept in which auditor decides

the material level for performing the audit and to decides the nature, timing and extend of the

audit procedure to be carried out. (Anon, n.d.)

According to ISA 320, the materiality level may vary from case to case because .user

expectation from industry to another industry may differ. There are some benchmarks for the

determination of materiality in an audit of the financial statements of an entity. Some of such

benchmarks may be as under:

a) Profit after tax

b) Income and expenses incurred

c) Gross profit earned

d) Equity

e) Net Assets of the organization

In the present case, the company operates in the oil and gas industry. Users of the financial

statement of the company would be most concerned with profit of the company. As such, as

an auditor we would select the benchmark ‘profit after tax’ to determine the materiality.

Quantitative detail of the materiality level is decided as under:

Particulars 2017 ($ Million) 2016 ($ Million)

Revenue 649.3 558.0

Net profit after tax 387.5 (588.8)

Other Expenses 70.1 (692.1)

Materiality level: (as under)

1% of revenue 6.50 5.58

30% of other expenses 21.03 -

As we noticed from the annual report that there was major changes in the net profit after tax

from the year 2016 to year 2017. Reason for such changes in profit was due to changes in

3 | P a g e

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Auditing & Ethics

other expenses. The revenue was also increased but percentage of increased in profit since

last year was more than the percentage of increase in the other expenses since last year.

As such, sound increase in the net profit after tax in comparison to the previous financial

year, lead us to conclude that a more appropriate basis of materiality for this year would be 1

percent of total revenue.

Other expense has majorly impacted the both year’s profit. It also gives a led to decide the

materiality level for checking the variation in such expenses.We would cover the 30 percent

of other expenses during the performance of an audit.

In the present case, the quantitative estimate of materiality will be as under:

i) 1% of total sales revenue i.e. $ 6.50m

ii) 30% of other expenses i.e. $ 21.03m

iii) 3% of gross profit i.e. $ 5.57m

In addition to determination of overall materiality, ISA 320 also dealt with the determination

of performance materiality. Performance materiality refers to the level of amount below the

overall materiality to ensure that the cumulative effect of undetected misstatements would not

exceed the overall materiality.

In the present case, there is major variation in other expenses. If we have decided the material

level 30 percent but there may be a chance of some misstatements, cumulative effect thereof

can exceeds the decided materiality level.

Reason for the variation in other expenses is reversal of impairment on property, plant and

equipment, petroleum assets etc. Reversal of impairment has a greatest proportion in the

variation of other expenses. As such, we have decided the performance materiality of 55

percent of the overall materiality i.e. 30 percent of total other expenses.

Related Party transaction: This is the risk prone area as transaction between the related parties

may not be at arm length price. In the audit of financial statement of the company we would

determine the materiality level at high as these transactions are more sensitive to minor

changes, which may lead to serious fraud or misstatements in an organization(Anon, n.d.).

We will decide the material level as well as performance level in this regards, which are as

follows:

Materiality level and performance level:

Related Parties Amount paid ($) Material Level ($) Performance Level

($)

DMAW Lawyer 64,742 45,319 30,000

Director fees directly

paid to DMAW

Lawyer

2,50,000 1,25,000 1,25,000

4 | P a g e

other expenses. The revenue was also increased but percentage of increased in profit since

last year was more than the percentage of increase in the other expenses since last year.

As such, sound increase in the net profit after tax in comparison to the previous financial

year, lead us to conclude that a more appropriate basis of materiality for this year would be 1

percent of total revenue.

Other expense has majorly impacted the both year’s profit. It also gives a led to decide the

materiality level for checking the variation in such expenses.We would cover the 30 percent

of other expenses during the performance of an audit.

In the present case, the quantitative estimate of materiality will be as under:

i) 1% of total sales revenue i.e. $ 6.50m

ii) 30% of other expenses i.e. $ 21.03m

iii) 3% of gross profit i.e. $ 5.57m

In addition to determination of overall materiality, ISA 320 also dealt with the determination

of performance materiality. Performance materiality refers to the level of amount below the

overall materiality to ensure that the cumulative effect of undetected misstatements would not

exceed the overall materiality.

In the present case, there is major variation in other expenses. If we have decided the material

level 30 percent but there may be a chance of some misstatements, cumulative effect thereof

can exceeds the decided materiality level.

Reason for the variation in other expenses is reversal of impairment on property, plant and

equipment, petroleum assets etc. Reversal of impairment has a greatest proportion in the

variation of other expenses. As such, we have decided the performance materiality of 55

percent of the overall materiality i.e. 30 percent of total other expenses.

Related Party transaction: This is the risk prone area as transaction between the related parties

may not be at arm length price. In the audit of financial statement of the company we would

determine the materiality level at high as these transactions are more sensitive to minor

changes, which may lead to serious fraud or misstatements in an organization(Anon, n.d.).

We will decide the material level as well as performance level in this regards, which are as

follows:

Materiality level and performance level:

Related Parties Amount paid ($) Material Level ($) Performance Level

($)

DMAW Lawyer 64,742 45,319 30,000

Director fees directly

paid to DMAW

Lawyer

2,50,000 1,25,000 1,25,000

4 | P a g e

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Auditing & Ethics

Analytical Review:

As an auditor, in this section, we proceeds to comparison between the account’s balances and

ensure their reasonableness. We conduct the systematic analysis of the trends and ratios of

the company and ensure its reasonableness as compared to related industry.(Anon, 2017)

We have calculated the ratios of the company which are as follows:

i) Current Ratio: This ratio represents the liquidity of an organization. It represents

the ability of the company to pay off its current liabilities. The ideal ratio is

considered as 2:1. In the present case, current ratio of the company in year 2017 is

4.14, which represents the company’s strength to manage its liabilities.

Analytical Review: The current ratio of the company is continuously increasing

year by year. The current ratio of the company in the year 2014 was 1.59 which

comes to 4.14 in the year 2017. Reason thereof is increase in current assets and

corresponding decrease in the current liabilities. On the hand, the ratio goes

double in the year 2017 as compared to the year 2016 due to major increase in

cash and cash equivalent in the year 2017. It is the better sign for the company.

There is no risk in this ratio but the auditor should not rely on such ratio until he

checked it. The ratio has changed unusually in the year 2017 as compared to the

year 2016. As such, the auditor should proceed to extensive audit procedure.

ii) Quick Ratio: This ratio is also calculated to analyze the liquidity of the company.

In liquidity analysis, we analyze the short term liquidity of the company to ensure

that it will be able to pay off the short term debts. In calculating this ratio

inventories of the company are not taken into consideration because this ratio

ensures the quick assets availability with the company to discharge its short term

liabilities.

In this company, quick ratio of the company in the year 2017 is 3.74 which ensure

the sound position of the company towards its current debts maturing in next

twelve months. As ideal ratio is considered is 1:1. The quick ratio of the company

was greater than 1 since the year 2014. As such, company is sound enough from

the liquidity point of view.

The trend of ratio is good but in the year 2017 liquid assets ratio proportionately

increased as compared to previous years. Reason thereof is the amount of

inventory was no more in the year 2017 and current liability got reduced.

From the audit perspective, there is no such risk in the company as the ratio is

good. But the auditor should take into consideration the review of liquid assets in

its audit procedure because there may be a risk of change in the user decisions.

iii) Debt to Equity Ratio: This ratio refers to the analysis of financial stability of the

company. This ratio describes that how much financing is being done from

5 | P a g e

Analytical Review:

As an auditor, in this section, we proceeds to comparison between the account’s balances and

ensure their reasonableness. We conduct the systematic analysis of the trends and ratios of

the company and ensure its reasonableness as compared to related industry.(Anon, 2017)

We have calculated the ratios of the company which are as follows:

i) Current Ratio: This ratio represents the liquidity of an organization. It represents

the ability of the company to pay off its current liabilities. The ideal ratio is

considered as 2:1. In the present case, current ratio of the company in year 2017 is

4.14, which represents the company’s strength to manage its liabilities.

Analytical Review: The current ratio of the company is continuously increasing

year by year. The current ratio of the company in the year 2014 was 1.59 which

comes to 4.14 in the year 2017. Reason thereof is increase in current assets and

corresponding decrease in the current liabilities. On the hand, the ratio goes

double in the year 2017 as compared to the year 2016 due to major increase in

cash and cash equivalent in the year 2017. It is the better sign for the company.

There is no risk in this ratio but the auditor should not rely on such ratio until he

checked it. The ratio has changed unusually in the year 2017 as compared to the

year 2016. As such, the auditor should proceed to extensive audit procedure.

ii) Quick Ratio: This ratio is also calculated to analyze the liquidity of the company.

In liquidity analysis, we analyze the short term liquidity of the company to ensure

that it will be able to pay off the short term debts. In calculating this ratio

inventories of the company are not taken into consideration because this ratio

ensures the quick assets availability with the company to discharge its short term

liabilities.

In this company, quick ratio of the company in the year 2017 is 3.74 which ensure

the sound position of the company towards its current debts maturing in next

twelve months. As ideal ratio is considered is 1:1. The quick ratio of the company

was greater than 1 since the year 2014. As such, company is sound enough from

the liquidity point of view.

The trend of ratio is good but in the year 2017 liquid assets ratio proportionately

increased as compared to previous years. Reason thereof is the amount of

inventory was no more in the year 2017 and current liability got reduced.

From the audit perspective, there is no such risk in the company as the ratio is

good. But the auditor should take into consideration the review of liquid assets in

its audit procedure because there may be a risk of change in the user decisions.

iii) Debt to Equity Ratio: This ratio refers to the analysis of financial stability of the

company. This ratio describes that how much financing is being done from

5 | P a g e

Auditing & Ethics

external sources as compared to the investors financing. Each company should try

to keep this ratio as minimum level because if the ratio is high, outside financers

would have more stakes in the company’s assets.

In this company, the debt to equity ratio was slightly increased in the year 2016 to

0.14 from 0.11 in the year 2015. Reason thereof was the decrease in the equity as

compared to decrease in the debt in the financial year 2016. But overall, it can be

said that company has low risk because of less dependency on external financing.

There may be risk of non-recognition of debt according to prevailing accounting

policies. The auditor should review the compliance of policies in recognition of

debt as current and non-current.

iv) Debt to Assets Ratio: This ratio is calculated to analyze the fact that how much

portion of the assets has been financed by the external financiers. In other words,

this ratio ensures the percentage of the assets owned by the creditors etc. Higher

the ratio will be more risky to the company and investor would not be interested in

such company.

In the present case, in the year 2017 the ratio is 0.08 which is minor amount and it

is a good indicator to the company that it has low taken less financing from

creditors etc. The low ratio ensures the investors about the assets of the company

that they have a greatest proportion in the company’s assets. As such, company’s

position is sound enough.

The ratio is good for the company but there may be risk of overvaluation of assets.

As such, auditor should record the valuation of assets in his audit plan and will

should to the same following the compliance of applicable standards.

v) Gross Profit Ratio: This ratio is calculated to ensure the effectiveness of the

operating activities of the company i.e. how effectively it produces the goods and

sale thereof. If the ratio is high it means company’s operations are effective. In

other words, this ratio measures the company’s efficiency in using material and

labour.

In the present case, the company has gross profit ratio of 28.63 in the year 2017.

The ratio is good and shows the company’s operational activities are good. The

ratio was very less in the year 2016 because of reduction in the sales and

corresponding decrease in the gross profit. But in the year 2017, it has recovered

itself and maintained the gross profit margin as it maintained in 2015 and 2014.

There is an unusual trend in the gross profit ratio. There is risk of overstatement of

revenues by the company and understatement of expenses. The audit plan should

cover the review of both the revenue and expenses.

6 | P a g e

external sources as compared to the investors financing. Each company should try

to keep this ratio as minimum level because if the ratio is high, outside financers

would have more stakes in the company’s assets.

In this company, the debt to equity ratio was slightly increased in the year 2016 to

0.14 from 0.11 in the year 2015. Reason thereof was the decrease in the equity as

compared to decrease in the debt in the financial year 2016. But overall, it can be

said that company has low risk because of less dependency on external financing.

There may be risk of non-recognition of debt according to prevailing accounting

policies. The auditor should review the compliance of policies in recognition of

debt as current and non-current.

iv) Debt to Assets Ratio: This ratio is calculated to analyze the fact that how much

portion of the assets has been financed by the external financiers. In other words,

this ratio ensures the percentage of the assets owned by the creditors etc. Higher

the ratio will be more risky to the company and investor would not be interested in

such company.

In the present case, in the year 2017 the ratio is 0.08 which is minor amount and it

is a good indicator to the company that it has low taken less financing from

creditors etc. The low ratio ensures the investors about the assets of the company

that they have a greatest proportion in the company’s assets. As such, company’s

position is sound enough.

The ratio is good for the company but there may be risk of overvaluation of assets.

As such, auditor should record the valuation of assets in his audit plan and will

should to the same following the compliance of applicable standards.

v) Gross Profit Ratio: This ratio is calculated to ensure the effectiveness of the

operating activities of the company i.e. how effectively it produces the goods and

sale thereof. If the ratio is high it means company’s operations are effective. In

other words, this ratio measures the company’s efficiency in using material and

labour.

In the present case, the company has gross profit ratio of 28.63 in the year 2017.

The ratio is good and shows the company’s operational activities are good. The

ratio was very less in the year 2016 because of reduction in the sales and

corresponding decrease in the gross profit. But in the year 2017, it has recovered

itself and maintained the gross profit margin as it maintained in 2015 and 2014.

There is an unusual trend in the gross profit ratio. There is risk of overstatement of

revenues by the company and understatement of expenses. The audit plan should

cover the review of both the revenue and expenses.

6 | P a g e

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Auditing & Ethics

vi) Net Profit Margin: This ratio is a measure of company’s profitability. It is the

proportion of sales after meeting all the expenses, which is available to

shareholders. It can be considered as basic tool of the company, which will be

useful in case of adverse situations.

In the present company, the ratio in the year 2015 and 2016 was adverse, which

show the companies worst position. In other words, it can be said that there was

nothing available to shareholders. Reason for the same was provision of

impairment on property, plant and equipment etc. But in the year 2017, it has

reported the good profit and ration come up at 59.68. The reason for such

increment in the net profit is the reversal of the impairment on property, plant and

equipment etc.

This ratio shows the increase in the ratio abnormally since previous year. It is a

risk prone area in term of showing the better position of the company. The auditor

needs to extend the audit procedure to verify the calculation of net profit.

From the audit perspective, the trend of the ratios is good and also it is as per industry

averages except the net profit ratio. We have to analyze the reason thereof in detail and have

to pay the more attention in this area with the revised nature, timing and extent of audit

procedure.

Cash Flow Analysis:

For every organization cash flow statement is the integral part of the financial statements.

From the audit perspective it should be thoroughly reviewed to get an understanding about

the movement of the cash in the organization.(Anon, n.d.)

As we have reviewed the cash flow statement of the company and found the company have

more cash inflows from the operating activities. In the operating activities it has received the

cash and cash equivalent from the oil and gas operation, which is its main activity. As far as,

cash outflow is concerned, the operating activities have more cash outflow as the operating

and personal expenses are very high. Also there is an outflow in the investing activities but

which is lower as compared to operating activities.

Primary cash receipts are from the operating activities. And cash payments are major part

from operation and some of the cash payments made for the investing activities. Cash

Payments are also made for financing activities as dividend. A cash receipt is made from the

sale of subsidiary. The company has sold investment into the subsidiary company.

There are many times activities are done but the cash inflow and outflows are not affected. If

the assets is purchased or sale on credit basis then there is no cash flow but the activity is

made. In the same way if any dividend declared but not paid then the same will be out of the

cash flow. Further sometime interest over debt is due but there is no payment in the current

7 | P a g e

vi) Net Profit Margin: This ratio is a measure of company’s profitability. It is the

proportion of sales after meeting all the expenses, which is available to

shareholders. It can be considered as basic tool of the company, which will be

useful in case of adverse situations.

In the present company, the ratio in the year 2015 and 2016 was adverse, which

show the companies worst position. In other words, it can be said that there was

nothing available to shareholders. Reason for the same was provision of

impairment on property, plant and equipment etc. But in the year 2017, it has

reported the good profit and ration come up at 59.68. The reason for such

increment in the net profit is the reversal of the impairment on property, plant and

equipment etc.

This ratio shows the increase in the ratio abnormally since previous year. It is a

risk prone area in term of showing the better position of the company. The auditor

needs to extend the audit procedure to verify the calculation of net profit.

From the audit perspective, the trend of the ratios is good and also it is as per industry

averages except the net profit ratio. We have to analyze the reason thereof in detail and have

to pay the more attention in this area with the revised nature, timing and extent of audit

procedure.

Cash Flow Analysis:

For every organization cash flow statement is the integral part of the financial statements.

From the audit perspective it should be thoroughly reviewed to get an understanding about

the movement of the cash in the organization.(Anon, n.d.)

As we have reviewed the cash flow statement of the company and found the company have

more cash inflows from the operating activities. In the operating activities it has received the

cash and cash equivalent from the oil and gas operation, which is its main activity. As far as,

cash outflow is concerned, the operating activities have more cash outflow as the operating

and personal expenses are very high. Also there is an outflow in the investing activities but

which is lower as compared to operating activities.

Primary cash receipts are from the operating activities. And cash payments are major part

from operation and some of the cash payments made for the investing activities. Cash

Payments are also made for financing activities as dividend. A cash receipt is made from the

sale of subsidiary. The company has sold investment into the subsidiary company.

There are many times activities are done but the cash inflow and outflows are not affected. If

the assets is purchased or sale on credit basis then there is no cash flow but the activity is

made. In the same way if any dividend declared but not paid then the same will be out of the

cash flow. Further sometime interest over debt is due but there is no payment in the current

7 | P a g e

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Auditing & Ethics

financial year i.e. interest due but not paid is claimed as expenditure but not affected the cash

flow.

Opinion:

We have reviewed the annual report of the company for the year 2017. Based on which, we

have determined the materiality level for decided benchmarks and analyzed the ratios and

trend thereof. We have to follow the detailed audit procedure in respect of other expenses.

Our opinion will depend on the outcome of the audit procedure that wee we have selected.

8 | P a g e

financial year i.e. interest due but not paid is claimed as expenditure but not affected the cash

flow.

Opinion:

We have reviewed the annual report of the company for the year 2017. Based on which, we

have determined the materiality level for decided benchmarks and analyzed the ratios and

trend thereof. We have to follow the detailed audit procedure in respect of other expenses.

Our opinion will depend on the outcome of the audit procedure that wee we have selected.

8 | P a g e

Auditing & Ethics

References:

Anon, n.d., Annual Report 2017, available at

http://www.beachenergy.com.au/irm/PDF/6793_0/2017annualreport?

IncludeUnapproved=83324855 [Online] [Assessed on 02/09/2018]

Anon. n.d., Annual Report 2015, available at

http://www.beachenergy.com.au/irm/PDF/4440_0/2015BeachEnergyLtdAnnualReport

[Online] [Assessed on 02/09/2018]

Anon, n.d., Materiality in the Audit of Financial Statements, available at

https://www.icaew.com/international-accounting-and-auditing/audit-planning/materiality-in-

the-audit-of-financial-statements [Online] [Assessed on 02/09/2018]

Anon, n.d., Materiality in Planning and Performing an Audit, available at

https://www.legislation.gov.au/Details/F2016C00029 [Online] [Assessed on 02/09/2018]

IFAC, n.d., Materiality in Planning and Performing an Audit, Available at

http://www.ifac.org/system/files/downloads/a018-2010-iaasb-handbook-isa-320.pdf [Online]

[Assessed on 02/09/2018]

Anon, 2017, Analytical Review, Available at

https://www.accountingtools.com/articles/2017/8/30/analytical-review [Online] [Assessed on

02/09/2018]

Anon, n.d., Net Profit Ratio, Available at

http://www.accountingexplanation.com/net_profit_ratio.htm [Online] [Assessed on

02/09/2018]

Anon, n.d., Key Ratios, Available at https://www.investopedia.com/terms/k/key-ratio.asp

[Online] [Assessed on 02/09/2018]

Anon, n.d., Performance Materiality: What’s all that about?, Available at

https://www.accountingweb.co.uk/practice/general-practice/performance-materiality-whats-

all-that-about[Online] [Assessed on 02/09/2018]

9 | P a g e

References:

Anon, n.d., Annual Report 2017, available at

http://www.beachenergy.com.au/irm/PDF/6793_0/2017annualreport?

IncludeUnapproved=83324855 [Online] [Assessed on 02/09/2018]

Anon. n.d., Annual Report 2015, available at

http://www.beachenergy.com.au/irm/PDF/4440_0/2015BeachEnergyLtdAnnualReport

[Online] [Assessed on 02/09/2018]

Anon, n.d., Materiality in the Audit of Financial Statements, available at

https://www.icaew.com/international-accounting-and-auditing/audit-planning/materiality-in-

the-audit-of-financial-statements [Online] [Assessed on 02/09/2018]

Anon, n.d., Materiality in Planning and Performing an Audit, available at

https://www.legislation.gov.au/Details/F2016C00029 [Online] [Assessed on 02/09/2018]

IFAC, n.d., Materiality in Planning and Performing an Audit, Available at

http://www.ifac.org/system/files/downloads/a018-2010-iaasb-handbook-isa-320.pdf [Online]

[Assessed on 02/09/2018]

Anon, 2017, Analytical Review, Available at

https://www.accountingtools.com/articles/2017/8/30/analytical-review [Online] [Assessed on

02/09/2018]

Anon, n.d., Net Profit Ratio, Available at

http://www.accountingexplanation.com/net_profit_ratio.htm [Online] [Assessed on

02/09/2018]

Anon, n.d., Key Ratios, Available at https://www.investopedia.com/terms/k/key-ratio.asp

[Online] [Assessed on 02/09/2018]

Anon, n.d., Performance Materiality: What’s all that about?, Available at

https://www.accountingweb.co.uk/practice/general-practice/performance-materiality-whats-

all-that-about[Online] [Assessed on 02/09/2018]

9 | P a g e

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Auditing & Ethics

Anon, n.d., Overall vs. Performance Materiality, Available at

https://www.icas.com/education-and-qualifications/back-to-basics-overall-vs-performance-

materiality-student-blog [Online] [Assessed on 02/09/2018]

James, n.d., Fundamental Analysis: The Cash Flow Statement, Available at

https://www.investopedia.com/university/fundamentalanalysis/fundanalysis8.asp [Online]

[Assessed on 02/09/2018]

KenFaulkenberry, n.d., Cash Flow Statement Analysis: Purpose, Components and Format,

Available at http://www.arborinvestmentplanner.com/cash-flow-statement-analysis-purpose-

components-and-format/ [Online] [Assessed on 02/09/2018]

Anon, n.d., Audit Procedure, Available at https://www.wikiaccounting.com/audit-

procedures-meaning-example-prepare/ [Online] [Assessed on 02/09/2018]

Nicole, 2018, Five Types of Testing Methods Used during Audit Procedures, Available at

https://linfordco.com/blog/audit-procedures-testing/ [Online] [Assessed on 02/09/2018]

Anon, 2016, Materiality & Performance Materiality (ISA 320), Available at

https://www.readyratios.com/news/audit/3198.html[Online] [Assessed on 02/09/2018]

Anon, 2018, Auditor’s or Accountant’s Opinion, Statement, Report, Available at

https://www.business-case-analysis.com/auditors-opinion.html[Online] [Assessed on

02/09/2018]

10 | P a g e

Anon, n.d., Overall vs. Performance Materiality, Available at

https://www.icas.com/education-and-qualifications/back-to-basics-overall-vs-performance-

materiality-student-blog [Online] [Assessed on 02/09/2018]

James, n.d., Fundamental Analysis: The Cash Flow Statement, Available at

https://www.investopedia.com/university/fundamentalanalysis/fundanalysis8.asp [Online]

[Assessed on 02/09/2018]

KenFaulkenberry, n.d., Cash Flow Statement Analysis: Purpose, Components and Format,

Available at http://www.arborinvestmentplanner.com/cash-flow-statement-analysis-purpose-

components-and-format/ [Online] [Assessed on 02/09/2018]

Anon, n.d., Audit Procedure, Available at https://www.wikiaccounting.com/audit-

procedures-meaning-example-prepare/ [Online] [Assessed on 02/09/2018]

Nicole, 2018, Five Types of Testing Methods Used during Audit Procedures, Available at

https://linfordco.com/blog/audit-procedures-testing/ [Online] [Assessed on 02/09/2018]

Anon, 2016, Materiality & Performance Materiality (ISA 320), Available at

https://www.readyratios.com/news/audit/3198.html[Online] [Assessed on 02/09/2018]

Anon, 2018, Auditor’s or Accountant’s Opinion, Statement, Report, Available at

https://www.business-case-analysis.com/auditors-opinion.html[Online] [Assessed on

02/09/2018]

10 | P a g e

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Auditing & Ethics

11 | P a g e

11 | P a g e

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.