Auditing LLC Company (landlease group) - ACCT20075 Assessment Task 2

VerifiedAdded on 2023/06/07

|14

|3325

|288

AI Summary

This report discusses the auditing process of LLC Company (landlease group) for ACCT20075 Assessment Task 2. It covers materiality, review of draft notes and disclosures, preliminary analytical review, analysis of cash flow statement, and more.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

LLC Company (landlease group)

ACCT20075 – Auditing and Ethic

Assessment Task 2 - Term 2, 2018

Name of the author

[Pick the date]

ACCT20075 – Auditing and Ethic

Assessment Task 2 - Term 2, 2018

Name of the author

[Pick the date]

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Auditing

Table of Contents

INTRODUCTION...........................................................................................................................2

ABOUT THE COMPANY..............................................................................................................2

SECTION 1.....................................................................................................................................2

ALL ABOUT MATERIALITY...................................................................................................2

REVIEW OF DRAFT NOTES AND DISCLOSURES..............................................................4

SECTION 2.....................................................................................................................................4

PRELIMINARY ANALYTICAL REVIEW...............................................................................4

SECTION 3.....................................................................................................................................6

ANALYSIS OF CASH FLOW STATEMENT...........................................................................6

NON-CASH FINANCIAL AND INVESTING ACTIVITIES...................................................7

RISK REGARDING GOING CONCERN..................................................................................7

REVIEW OF THE AUDIT REPORT.........................................................................................7

REFERENCES................................................................................................................................7

1

Table of Contents

INTRODUCTION...........................................................................................................................2

ABOUT THE COMPANY..............................................................................................................2

SECTION 1.....................................................................................................................................2

ALL ABOUT MATERIALITY...................................................................................................2

REVIEW OF DRAFT NOTES AND DISCLOSURES..............................................................4

SECTION 2.....................................................................................................................................4

PRELIMINARY ANALYTICAL REVIEW...............................................................................4

SECTION 3.....................................................................................................................................6

ANALYSIS OF CASH FLOW STATEMENT...........................................................................6

NON-CASH FINANCIAL AND INVESTING ACTIVITIES...................................................7

RISK REGARDING GOING CONCERN..................................................................................7

REVIEW OF THE AUDIT REPORT.........................................................................................7

REFERENCES................................................................................................................................7

1

Auditing

INTRODUCTION

To gain success, any business needs a satisfied base of stakeholders. The stakeholders need

transparency to generate trust on the company. This transparency is tried to be generated with the

publication of financial information. The stakeholders get all the information they desire about

the entity through these reports made for financial information. However, the reports seem

sceptical unless they are reviewed and opined by an independent professional. In this report, LLC

Company (landlease group) has been chosen to prepare this assignment. It is difficult to rely on

whatever the company has published until the reliability is verified. This verification regarding

the fairness is to be done only by a qualified professional. Auditor is the most appropriate

professional meant for this work.

Auditing refers to the function wherein the auditor inspects and examines the financial accounts

of an entity. After the examination is made and the control environment of the entity is analysed,

the auditor frames an opinion. The opinion relates to whether, the accounts are being prepared

truly and fairly, in all important and material aspects, in harmonisation with the relevant

accounting standards and policies. This opinion acts as a trust binding agent for the users of

information. An appraisal in this form by an unbiased third party, adds value to the financial

reports. However, auditing is not a single day function, and encompasses several aspects. The

current report is a discussion regarding those different aspects. The company chosen for the

study purpose is Landlease Group (Louwers, Ramsay, Sinason, Strawser & Thibodeau, 2015).

ABOUT THE COMPANY

LLC Company (landlease group) was founded in the year 1958 in Sydney. The vision behind the

incorporation of this company has been the creation of a successful corporation that combines

the aspects of construction, investment and development. Having operations diversified in

Australia, Europe, Asia and the America, LLC Company (landlease group) has proven to be a

top international infrastructure and property group. The annual reports issued by the company

consist of the directors’ report, remuneration report and the financial statements for the financial

year. The analysis of same as required is done in the following segments of report (Psaros &

Seamer, 2015).

2

INTRODUCTION

To gain success, any business needs a satisfied base of stakeholders. The stakeholders need

transparency to generate trust on the company. This transparency is tried to be generated with the

publication of financial information. The stakeholders get all the information they desire about

the entity through these reports made for financial information. However, the reports seem

sceptical unless they are reviewed and opined by an independent professional. In this report, LLC

Company (landlease group) has been chosen to prepare this assignment. It is difficult to rely on

whatever the company has published until the reliability is verified. This verification regarding

the fairness is to be done only by a qualified professional. Auditor is the most appropriate

professional meant for this work.

Auditing refers to the function wherein the auditor inspects and examines the financial accounts

of an entity. After the examination is made and the control environment of the entity is analysed,

the auditor frames an opinion. The opinion relates to whether, the accounts are being prepared

truly and fairly, in all important and material aspects, in harmonisation with the relevant

accounting standards and policies. This opinion acts as a trust binding agent for the users of

information. An appraisal in this form by an unbiased third party, adds value to the financial

reports. However, auditing is not a single day function, and encompasses several aspects. The

current report is a discussion regarding those different aspects. The company chosen for the

study purpose is Landlease Group (Louwers, Ramsay, Sinason, Strawser & Thibodeau, 2015).

ABOUT THE COMPANY

LLC Company (landlease group) was founded in the year 1958 in Sydney. The vision behind the

incorporation of this company has been the creation of a successful corporation that combines

the aspects of construction, investment and development. Having operations diversified in

Australia, Europe, Asia and the America, LLC Company (landlease group) has proven to be a

top international infrastructure and property group. The annual reports issued by the company

consist of the directors’ report, remuneration report and the financial statements for the financial

year. The analysis of same as required is done in the following segments of report (Psaros &

Seamer, 2015).

2

Auditing

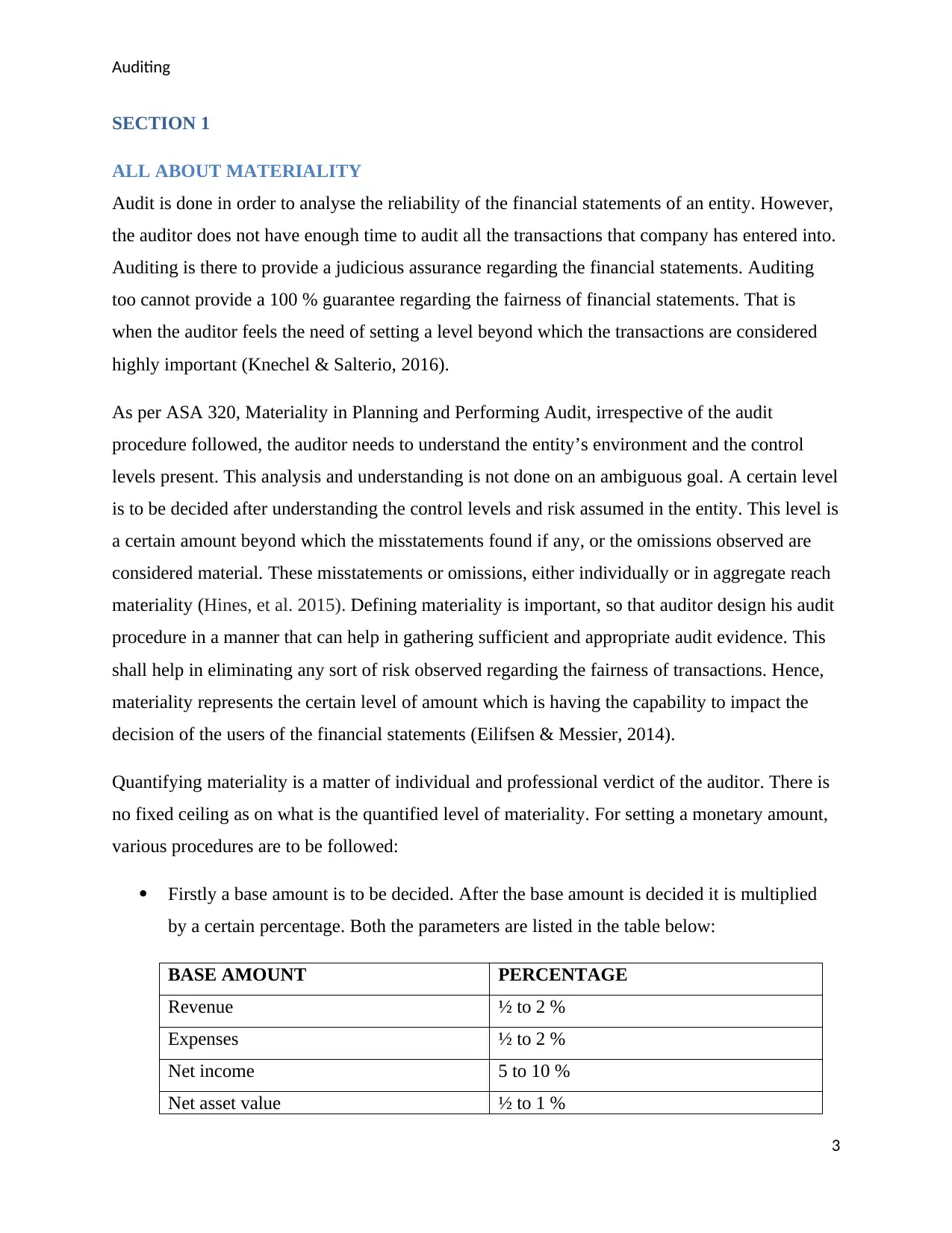

SECTION 1

ALL ABOUT MATERIALITY

Audit is done in order to analyse the reliability of the financial statements of an entity. However,

the auditor does not have enough time to audit all the transactions that company has entered into.

Auditing is there to provide a judicious assurance regarding the financial statements. Auditing

too cannot provide a 100 % guarantee regarding the fairness of financial statements. That is

when the auditor feels the need of setting a level beyond which the transactions are considered

highly important (Knechel & Salterio, 2016).

As per ASA 320, Materiality in Planning and Performing Audit, irrespective of the audit

procedure followed, the auditor needs to understand the entity’s environment and the control

levels present. This analysis and understanding is not done on an ambiguous goal. A certain level

is to be decided after understanding the control levels and risk assumed in the entity. This level is

a certain amount beyond which the misstatements found if any, or the omissions observed are

considered material. These misstatements or omissions, either individually or in aggregate reach

materiality (Hines, et al. 2015). Defining materiality is important, so that auditor design his audit

procedure in a manner that can help in gathering sufficient and appropriate audit evidence. This

shall help in eliminating any sort of risk observed regarding the fairness of transactions. Hence,

materiality represents the certain level of amount which is having the capability to impact the

decision of the users of the financial statements (Eilifsen & Messier, 2014).

Quantifying materiality is a matter of individual and professional verdict of the auditor. There is

no fixed ceiling as on what is the quantified level of materiality. For setting a monetary amount,

various procedures are to be followed:

Firstly a base amount is to be decided. After the base amount is decided it is multiplied

by a certain percentage. Both the parameters are listed in the table below:

BASE AMOUNT PERCENTAGE

Revenue ½ to 2 %

Expenses ½ to 2 %

Net income 5 to 10 %

Net asset value ½ to 1 %

3

SECTION 1

ALL ABOUT MATERIALITY

Audit is done in order to analyse the reliability of the financial statements of an entity. However,

the auditor does not have enough time to audit all the transactions that company has entered into.

Auditing is there to provide a judicious assurance regarding the financial statements. Auditing

too cannot provide a 100 % guarantee regarding the fairness of financial statements. That is

when the auditor feels the need of setting a level beyond which the transactions are considered

highly important (Knechel & Salterio, 2016).

As per ASA 320, Materiality in Planning and Performing Audit, irrespective of the audit

procedure followed, the auditor needs to understand the entity’s environment and the control

levels present. This analysis and understanding is not done on an ambiguous goal. A certain level

is to be decided after understanding the control levels and risk assumed in the entity. This level is

a certain amount beyond which the misstatements found if any, or the omissions observed are

considered material. These misstatements or omissions, either individually or in aggregate reach

materiality (Hines, et al. 2015). Defining materiality is important, so that auditor design his audit

procedure in a manner that can help in gathering sufficient and appropriate audit evidence. This

shall help in eliminating any sort of risk observed regarding the fairness of transactions. Hence,

materiality represents the certain level of amount which is having the capability to impact the

decision of the users of the financial statements (Eilifsen & Messier, 2014).

Quantifying materiality is a matter of individual and professional verdict of the auditor. There is

no fixed ceiling as on what is the quantified level of materiality. For setting a monetary amount,

various procedures are to be followed:

Firstly a base amount is to be decided. After the base amount is decided it is multiplied

by a certain percentage. Both the parameters are listed in the table below:

BASE AMOUNT PERCENTAGE

Revenue ½ to 2 %

Expenses ½ to 2 %

Net income 5 to 10 %

Net asset value ½ to 1 %

3

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Auditing

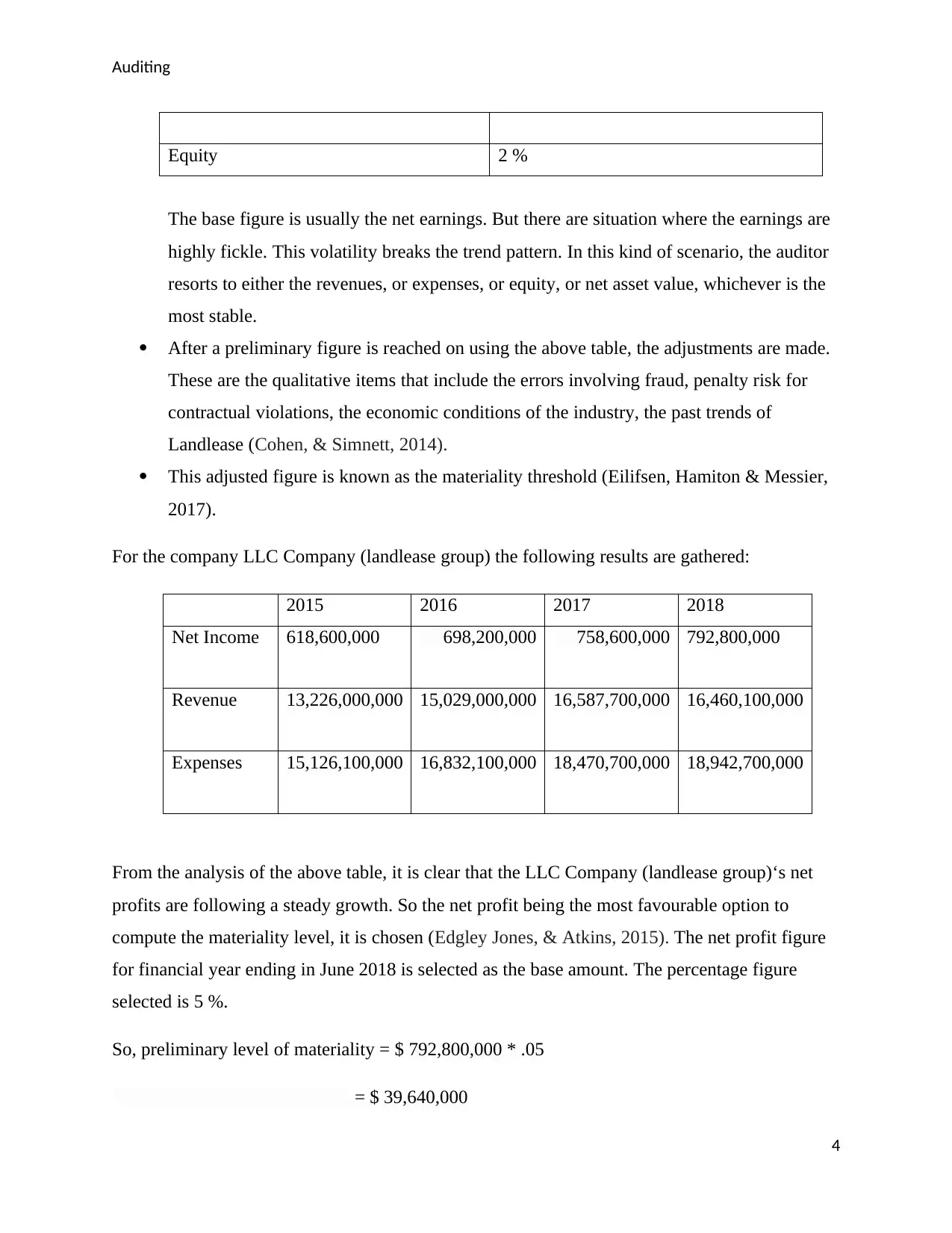

Equity 2 %

The base figure is usually the net earnings. But there are situation where the earnings are

highly fickle. This volatility breaks the trend pattern. In this kind of scenario, the auditor

resorts to either the revenues, or expenses, or equity, or net asset value, whichever is the

most stable.

After a preliminary figure is reached on using the above table, the adjustments are made.

These are the qualitative items that include the errors involving fraud, penalty risk for

contractual violations, the economic conditions of the industry, the past trends of

Landlease (Cohen, & Simnett, 2014).

This adjusted figure is known as the materiality threshold (Eilifsen, Hamiton & Messier,

2017).

For the company LLC Company (landlease group) the following results are gathered:

2015 2016 2017 2018

Net Income 618,600,000 698,200,000 758,600,000 792,800,000

Revenue 13,226,000,000 15,029,000,000 16,587,700,000 16,460,100,000

Expenses 15,126,100,000 16,832,100,000 18,470,700,000 18,942,700,000

From the analysis of the above table, it is clear that the LLC Company (landlease group)‘s net

profits are following a steady growth. So the net profit being the most favourable option to

compute the materiality level, it is chosen (Edgley Jones, & Atkins, 2015). The net profit figure

for financial year ending in June 2018 is selected as the base amount. The percentage figure

selected is 5 %.

So, preliminary level of materiality = $ 792,800,000 * .05

= $ 39,640,000

4

Equity 2 %

The base figure is usually the net earnings. But there are situation where the earnings are

highly fickle. This volatility breaks the trend pattern. In this kind of scenario, the auditor

resorts to either the revenues, or expenses, or equity, or net asset value, whichever is the

most stable.

After a preliminary figure is reached on using the above table, the adjustments are made.

These are the qualitative items that include the errors involving fraud, penalty risk for

contractual violations, the economic conditions of the industry, the past trends of

Landlease (Cohen, & Simnett, 2014).

This adjusted figure is known as the materiality threshold (Eilifsen, Hamiton & Messier,

2017).

For the company LLC Company (landlease group) the following results are gathered:

2015 2016 2017 2018

Net Income 618,600,000 698,200,000 758,600,000 792,800,000

Revenue 13,226,000,000 15,029,000,000 16,587,700,000 16,460,100,000

Expenses 15,126,100,000 16,832,100,000 18,470,700,000 18,942,700,000

From the analysis of the above table, it is clear that the LLC Company (landlease group)‘s net

profits are following a steady growth. So the net profit being the most favourable option to

compute the materiality level, it is chosen (Edgley Jones, & Atkins, 2015). The net profit figure

for financial year ending in June 2018 is selected as the base amount. The percentage figure

selected is 5 %.

So, preliminary level of materiality = $ 792,800,000 * .05

= $ 39,640,000

4

Auditing

Making the adjustments as mentioned above, the materiality figure taken is $ 40,000,000.

REVIEW OF DRAFT NOTES AND DISCLOSURES

As per the analysis of the drafts disclosed after the financial statements of o Landlease Group,

certain matters that may cast significance on the audit are mentioned as follows:

CAPITALISATION OF DEVELOPMENT COST INTO INVENTORY:

LLC Company (landlease group) is following the practice of capitalising the development costs

incurred in the projects as inventory. The capitalisation is done over the lifetime. The method

used for carrying this inventory is lower of cost or net realisable value. This involves forecasting

the future sales, sales price, and the related costs. However, for the long term projects, there lies

a huge uncertainty and complexity in forecasting (Fisher & Krumwiede, 2015).

In this situation, the auditor of LLC Company (landlease group) must seek the help of an expert

as per ASA 620, using the work of an Auditor’s Expert. The expert can help in analysing the

forecasts for a few text sample projects selected. This way reliability can be established for the

valuation done by entity (Kanatov, Atymtayeva & Yagaliyeva, 2014).

Audit procedure

In understanding the nature of LLC Company (landlease group) and its working, the auditor at

times need to perform analytical audit procedures. These are those audit procedures that help the

auditor to gather sufficient and appropriate audit evidence. It is done by setting and establishing a

relationship between the financials available for the entity. The same relationship is tried to be

used for the non-financial data.

SECTION 2

PRELIMINARY ANALYTICAL REVIEW

As per ASA 300, planning an Audit of Financial Report, this analysis is useful at the planning

stage itself. Key ratios related to the balance sheet and profit and loss statement are calculated to

perform a trend analysis (Brown-Liburd, Issa & Lombardi, 2015). The following table presents

the key ratios that are computed from the financials of Landlease Group:

5

Making the adjustments as mentioned above, the materiality figure taken is $ 40,000,000.

REVIEW OF DRAFT NOTES AND DISCLOSURES

As per the analysis of the drafts disclosed after the financial statements of o Landlease Group,

certain matters that may cast significance on the audit are mentioned as follows:

CAPITALISATION OF DEVELOPMENT COST INTO INVENTORY:

LLC Company (landlease group) is following the practice of capitalising the development costs

incurred in the projects as inventory. The capitalisation is done over the lifetime. The method

used for carrying this inventory is lower of cost or net realisable value. This involves forecasting

the future sales, sales price, and the related costs. However, for the long term projects, there lies

a huge uncertainty and complexity in forecasting (Fisher & Krumwiede, 2015).

In this situation, the auditor of LLC Company (landlease group) must seek the help of an expert

as per ASA 620, using the work of an Auditor’s Expert. The expert can help in analysing the

forecasts for a few text sample projects selected. This way reliability can be established for the

valuation done by entity (Kanatov, Atymtayeva & Yagaliyeva, 2014).

Audit procedure

In understanding the nature of LLC Company (landlease group) and its working, the auditor at

times need to perform analytical audit procedures. These are those audit procedures that help the

auditor to gather sufficient and appropriate audit evidence. It is done by setting and establishing a

relationship between the financials available for the entity. The same relationship is tried to be

used for the non-financial data.

SECTION 2

PRELIMINARY ANALYTICAL REVIEW

As per ASA 300, planning an Audit of Financial Report, this analysis is useful at the planning

stage itself. Key ratios related to the balance sheet and profit and loss statement are calculated to

perform a trend analysis (Brown-Liburd, Issa & Lombardi, 2015). The following table presents

the key ratios that are computed from the financials of Landlease Group:

5

Auditing

KEY RATIOS 2014 2015 2016 2017 2018

CURRENT

RATIO

.68 0.67 0.66 0.58 0.96

Quick ratio .38 .42 045 040 .69

NET MARGIN

(%)

4.69 4.68 4.65 4.57 4.82

RETURN ON

ASSETS (%)

3.59 3.56 3.72 3.85 4.19

RETURN ON

EQUITY (%)

12.50 12.34 12.96 12.99 12.71

RETURN ON

INVESTED

CAPITAL (%)

9.62 9.54 10.21 10.41 9.95

RECEIVABLES

TURNOVER

11.55 11.01 12.98 13.67 11.48

Payable

turnover

15.5 16.5 17.5 16.7 18.5

FIXED ASSETS

TURNOVER

37.89 37.30 38.48 38.66 36.97

Inventory

turnover ratio

17.7 19.9 22.5 18.5 22.5

Debt to capital

ratio

15.69 15.5 17.5 19.5 22

Interest

coverage ratio

17.7 18.5 19.5 16.5 20.5

Dividend pay-

out ratio

7.7 % 8.5% 9.5 % 11.5 % 12 %

As per the above table the following results are analysed:

Current ratio : improved

Net margin : improved

6

KEY RATIOS 2014 2015 2016 2017 2018

CURRENT

RATIO

.68 0.67 0.66 0.58 0.96

Quick ratio .38 .42 045 040 .69

NET MARGIN

(%)

4.69 4.68 4.65 4.57 4.82

RETURN ON

ASSETS (%)

3.59 3.56 3.72 3.85 4.19

RETURN ON

EQUITY (%)

12.50 12.34 12.96 12.99 12.71

RETURN ON

INVESTED

CAPITAL (%)

9.62 9.54 10.21 10.41 9.95

RECEIVABLES

TURNOVER

11.55 11.01 12.98 13.67 11.48

Payable

turnover

15.5 16.5 17.5 16.7 18.5

FIXED ASSETS

TURNOVER

37.89 37.30 38.48 38.66 36.97

Inventory

turnover ratio

17.7 19.9 22.5 18.5 22.5

Debt to capital

ratio

15.69 15.5 17.5 19.5 22

Interest

coverage ratio

17.7 18.5 19.5 16.5 20.5

Dividend pay-

out ratio

7.7 % 8.5% 9.5 % 11.5 % 12 %

As per the above table the following results are analysed:

Current ratio : improved

Net margin : improved

6

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Auditing

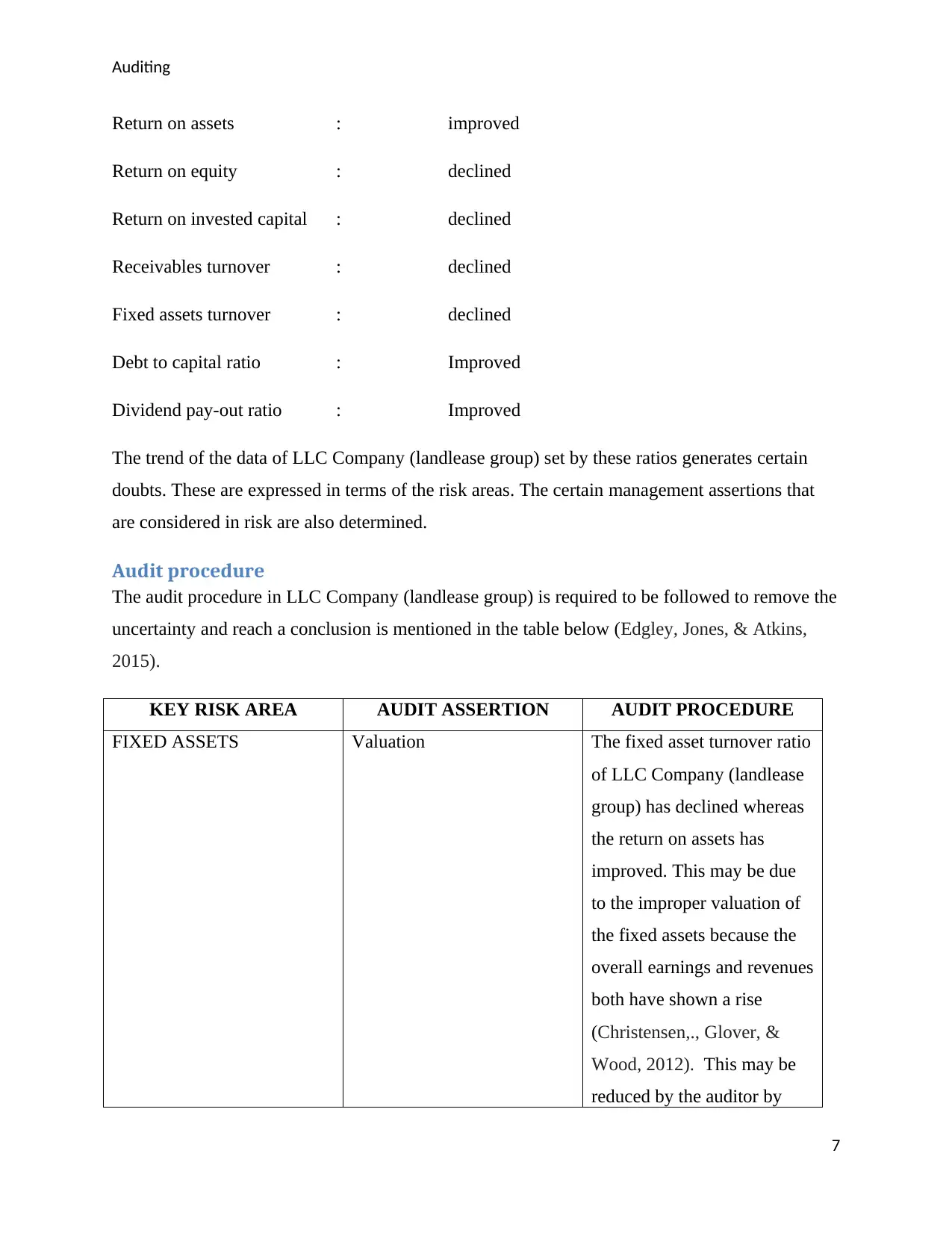

Return on assets : improved

Return on equity : declined

Return on invested capital : declined

Receivables turnover : declined

Fixed assets turnover : declined

Debt to capital ratio : Improved

Dividend pay-out ratio : Improved

The trend of the data of LLC Company (landlease group) set by these ratios generates certain

doubts. These are expressed in terms of the risk areas. The certain management assertions that

are considered in risk are also determined.

Audit procedure

The audit procedure in LLC Company (landlease group) is required to be followed to remove the

uncertainty and reach a conclusion is mentioned in the table below (Edgley, Jones, & Atkins,

2015).

KEY RISK AREA AUDIT ASSERTION AUDIT PROCEDURE

FIXED ASSETS Valuation The fixed asset turnover ratio

of LLC Company (landlease

group) has declined whereas

the return on assets has

improved. This may be due

to the improper valuation of

the fixed assets because the

overall earnings and revenues

both have shown a rise

(Christensen,., Glover, &

Wood, 2012). This may be

reduced by the auditor by

7

Return on assets : improved

Return on equity : declined

Return on invested capital : declined

Receivables turnover : declined

Fixed assets turnover : declined

Debt to capital ratio : Improved

Dividend pay-out ratio : Improved

The trend of the data of LLC Company (landlease group) set by these ratios generates certain

doubts. These are expressed in terms of the risk areas. The certain management assertions that

are considered in risk are also determined.

Audit procedure

The audit procedure in LLC Company (landlease group) is required to be followed to remove the

uncertainty and reach a conclusion is mentioned in the table below (Edgley, Jones, & Atkins,

2015).

KEY RISK AREA AUDIT ASSERTION AUDIT PROCEDURE

FIXED ASSETS Valuation The fixed asset turnover ratio

of LLC Company (landlease

group) has declined whereas

the return on assets has

improved. This may be due

to the improper valuation of

the fixed assets because the

overall earnings and revenues

both have shown a rise

(Christensen,., Glover, &

Wood, 2012). This may be

reduced by the auditor by

7

Auditing

physically verifying the

condition of the assets and

taking the help of a valuation

professional to correctly

value them.

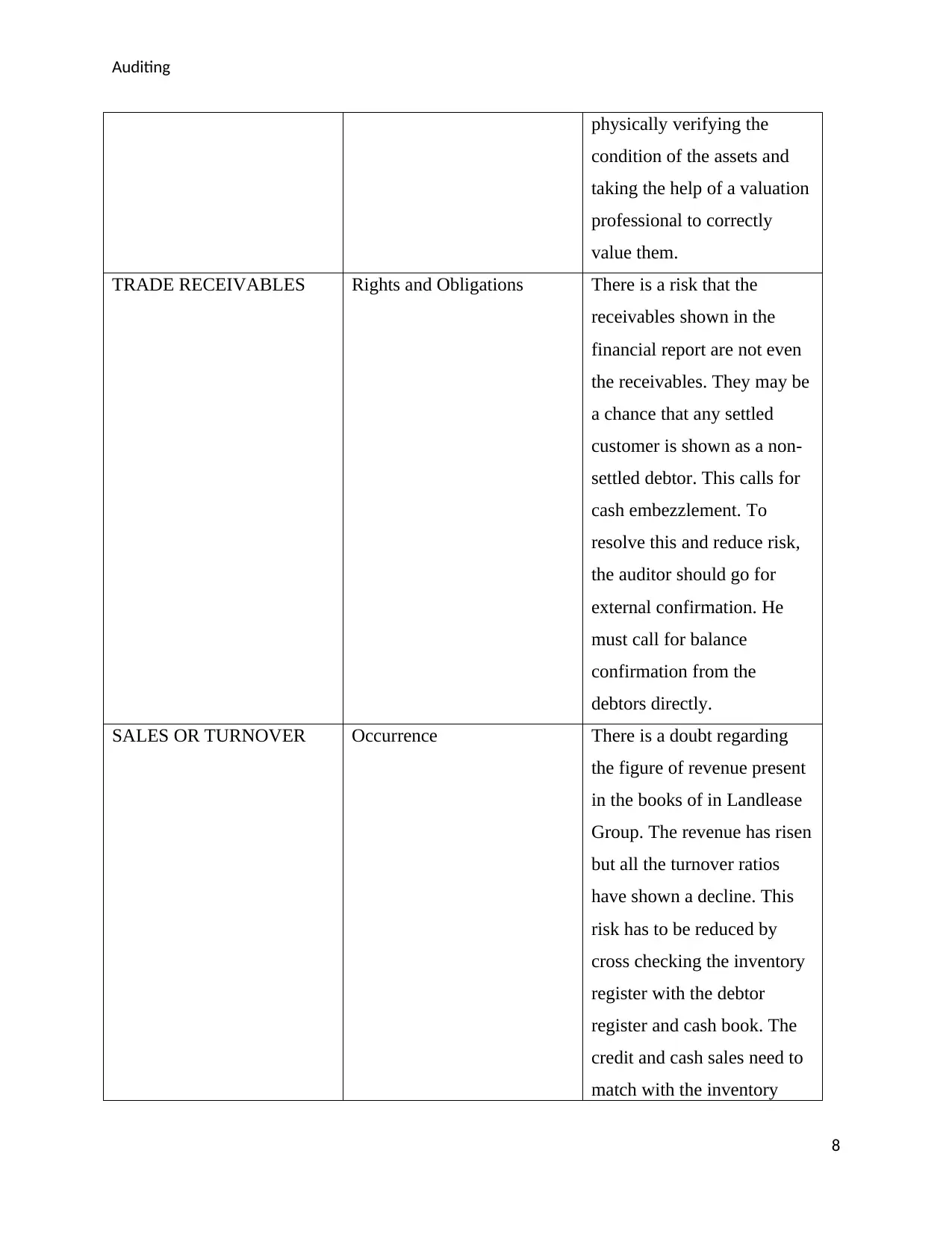

TRADE RECEIVABLES Rights and Obligations There is a risk that the

receivables shown in the

financial report are not even

the receivables. They may be

a chance that any settled

customer is shown as a non-

settled debtor. This calls for

cash embezzlement. To

resolve this and reduce risk,

the auditor should go for

external confirmation. He

must call for balance

confirmation from the

debtors directly.

SALES OR TURNOVER Occurrence There is a doubt regarding

the figure of revenue present

in the books of in Landlease

Group. The revenue has risen

but all the turnover ratios

have shown a decline. This

risk has to be reduced by

cross checking the inventory

register with the debtor

register and cash book. The

credit and cash sales need to

match with the inventory

8

physically verifying the

condition of the assets and

taking the help of a valuation

professional to correctly

value them.

TRADE RECEIVABLES Rights and Obligations There is a risk that the

receivables shown in the

financial report are not even

the receivables. They may be

a chance that any settled

customer is shown as a non-

settled debtor. This calls for

cash embezzlement. To

resolve this and reduce risk,

the auditor should go for

external confirmation. He

must call for balance

confirmation from the

debtors directly.

SALES OR TURNOVER Occurrence There is a doubt regarding

the figure of revenue present

in the books of in Landlease

Group. The revenue has risen

but all the turnover ratios

have shown a decline. This

risk has to be reduced by

cross checking the inventory

register with the debtor

register and cash book. The

credit and cash sales need to

match with the inventory

8

Auditing

register.

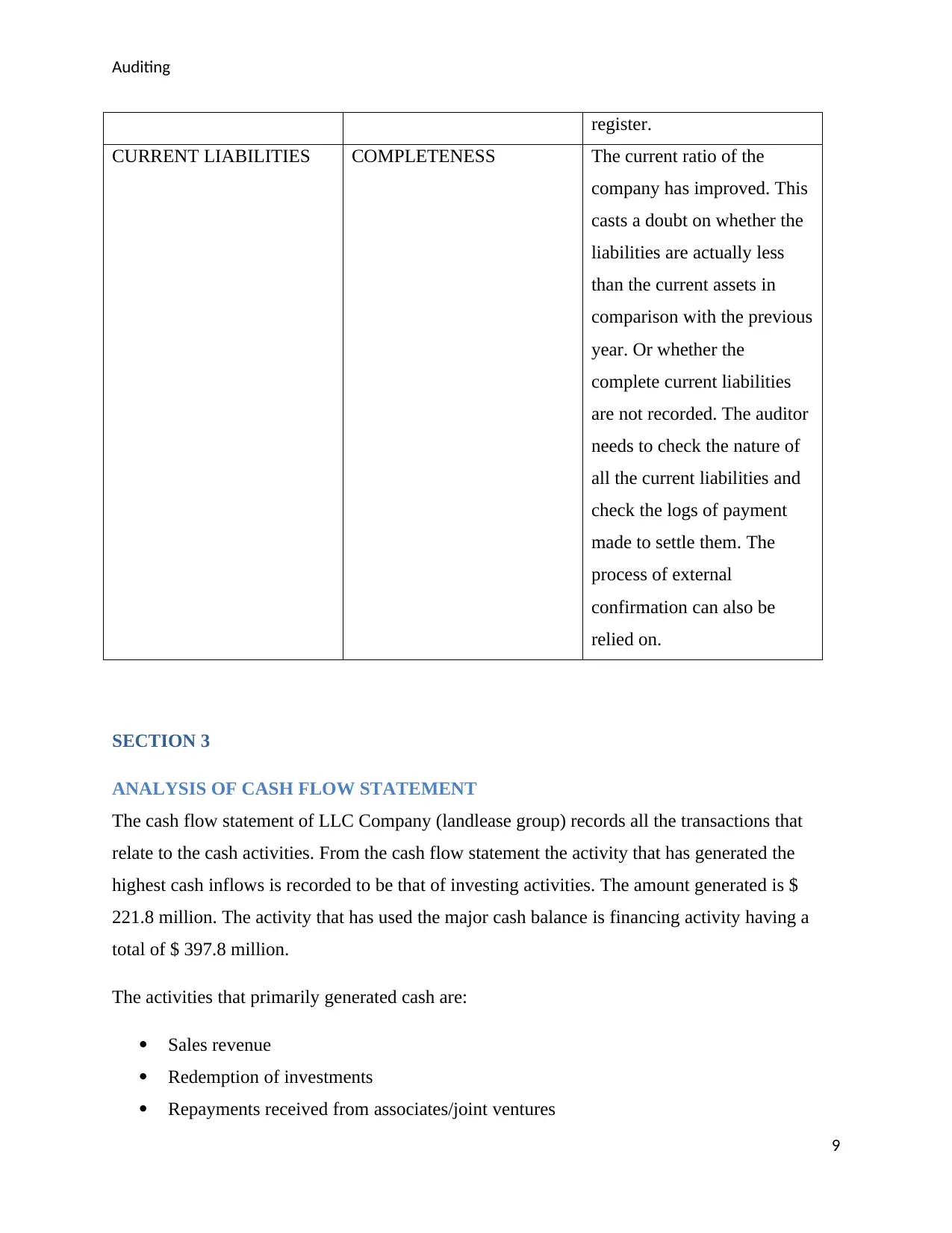

CURRENT LIABILITIES COMPLETENESS The current ratio of the

company has improved. This

casts a doubt on whether the

liabilities are actually less

than the current assets in

comparison with the previous

year. Or whether the

complete current liabilities

are not recorded. The auditor

needs to check the nature of

all the current liabilities and

check the logs of payment

made to settle them. The

process of external

confirmation can also be

relied on.

SECTION 3

ANALYSIS OF CASH FLOW STATEMENT

The cash flow statement of LLC Company (landlease group) records all the transactions that

relate to the cash activities. From the cash flow statement the activity that has generated the

highest cash inflows is recorded to be that of investing activities. The amount generated is $

221.8 million. The activity that has used the major cash balance is financing activity having a

total of $ 397.8 million.

The activities that primarily generated cash are:

Sales revenue

Redemption of investments

Repayments received from associates/joint ventures

9

register.

CURRENT LIABILITIES COMPLETENESS The current ratio of the

company has improved. This

casts a doubt on whether the

liabilities are actually less

than the current assets in

comparison with the previous

year. Or whether the

complete current liabilities

are not recorded. The auditor

needs to check the nature of

all the current liabilities and

check the logs of payment

made to settle them. The

process of external

confirmation can also be

relied on.

SECTION 3

ANALYSIS OF CASH FLOW STATEMENT

The cash flow statement of LLC Company (landlease group) records all the transactions that

relate to the cash activities. From the cash flow statement the activity that has generated the

highest cash inflows is recorded to be that of investing activities. The amount generated is $

221.8 million. The activity that has used the major cash balance is financing activity having a

total of $ 397.8 million.

The activities that primarily generated cash are:

Sales revenue

Redemption of investments

Repayments received from associates/joint ventures

9

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Auditing

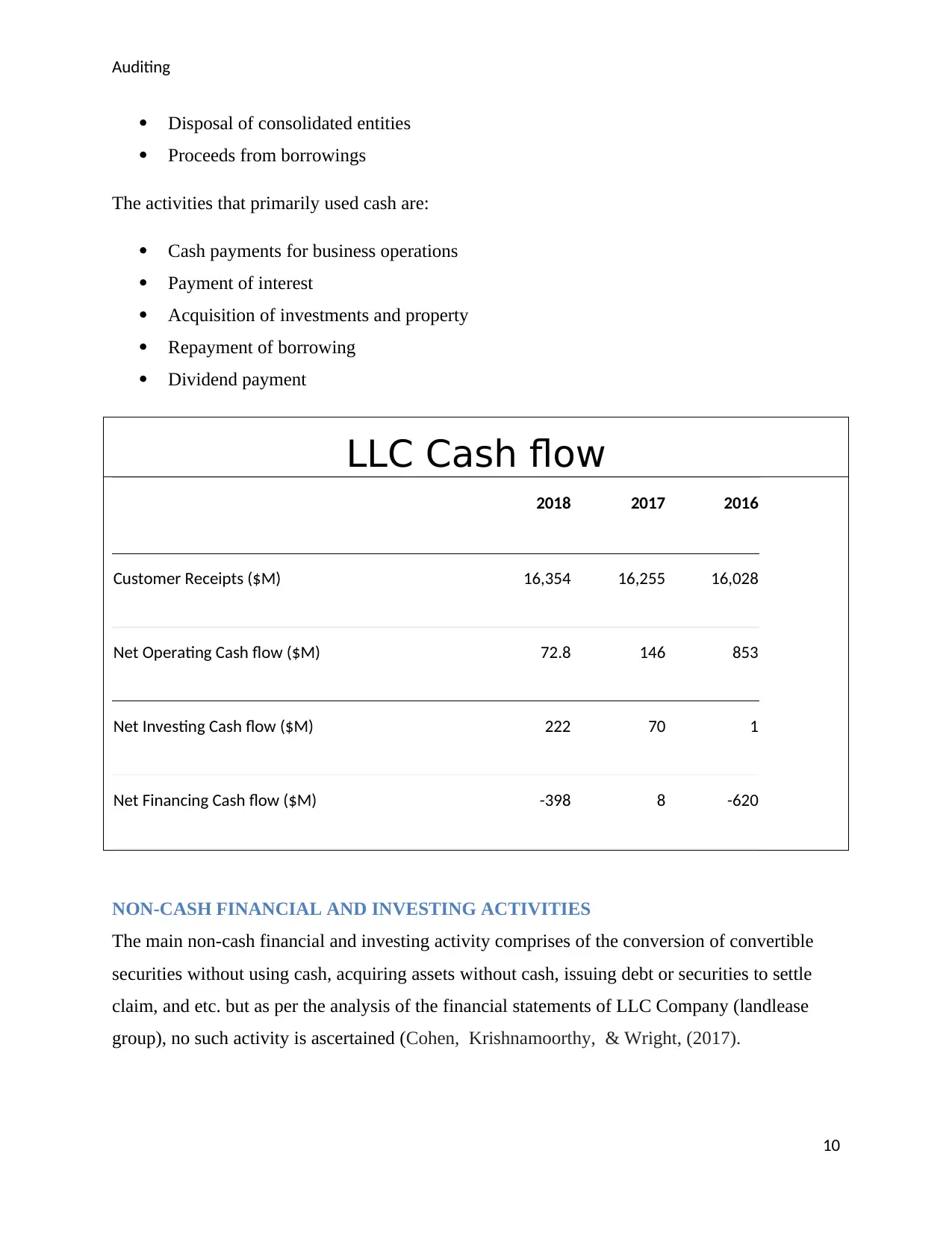

Disposal of consolidated entities

Proceeds from borrowings

The activities that primarily used cash are:

Cash payments for business operations

Payment of interest

Acquisition of investments and property

Repayment of borrowing

Dividend payment

LLC Cash flow

2018 2017 2016

Customer Receipts ($M) 16,354 16,255 16,028

Net Operating Cash flow ($M) 72.8 146 853

Net Investing Cash flow ($M) 222 70 1

Net Financing Cash flow ($M) -398 8 -620

NON-CASH FINANCIAL AND INVESTING ACTIVITIES

The main non-cash financial and investing activity comprises of the conversion of convertible

securities without using cash, acquiring assets without cash, issuing debt or securities to settle

claim, and etc. but as per the analysis of the financial statements of LLC Company (landlease

group), no such activity is ascertained (Cohen, Krishnamoorthy, & Wright, (2017).

10

Disposal of consolidated entities

Proceeds from borrowings

The activities that primarily used cash are:

Cash payments for business operations

Payment of interest

Acquisition of investments and property

Repayment of borrowing

Dividend payment

LLC Cash flow

2018 2017 2016

Customer Receipts ($M) 16,354 16,255 16,028

Net Operating Cash flow ($M) 72.8 146 853

Net Investing Cash flow ($M) 222 70 1

Net Financing Cash flow ($M) -398 8 -620

NON-CASH FINANCIAL AND INVESTING ACTIVITIES

The main non-cash financial and investing activity comprises of the conversion of convertible

securities without using cash, acquiring assets without cash, issuing debt or securities to settle

claim, and etc. but as per the analysis of the financial statements of LLC Company (landlease

group), no such activity is ascertained (Cohen, Krishnamoorthy, & Wright, (2017).

10

Auditing

RISK REGARDING GOING CONCERN

The only activity that can cast a doubt on the going concern of the LLC Company (landlease

group) is the disposal of the consolidated entities by the company. However, the management

has asserted no doubts regarding the company’s position to continue business. To remove the

doubt that the auditor might have regarding the ability of the company to continue due to this

transaction, he must try to analyse the same. The reasons for the disposal must be asked for and

the sale agreement should be checked.

Audit procedure to manage the risk

The main audit procedure which will be followed to address the audit risk would be

implementing AUDIT ASSERTION test.

REVIEW OF THE AUDIT REPORT

The independent auditors have issued and clean and unmodified report for LLC Company

(landlease group). There are no additional sections or paragraphs highlighting any issues. Only

as per the requirements of standards, the auditor have separately mentioned certain key audit

matters relation to inventories, construction and development revenue and equity accounted

investments.

Additional section

Audit matters relation to inventories, construction and development revenue and equity

accounted investments. However, there is no separate opinion on them.

Nature of the issue

These are the capital nature issues. They are the most significant matters, which auditor thinks

that the shareholders should be aware of (Czerney, Schmidt & Thompson, 2014).

Audit opinion

Company has given the opinion that company has complied with the all the applicable rules and

regulations. It has given un-qualified audit opinion that company has no issues with the

corporate governance.

11

RISK REGARDING GOING CONCERN

The only activity that can cast a doubt on the going concern of the LLC Company (landlease

group) is the disposal of the consolidated entities by the company. However, the management

has asserted no doubts regarding the company’s position to continue business. To remove the

doubt that the auditor might have regarding the ability of the company to continue due to this

transaction, he must try to analyse the same. The reasons for the disposal must be asked for and

the sale agreement should be checked.

Audit procedure to manage the risk

The main audit procedure which will be followed to address the audit risk would be

implementing AUDIT ASSERTION test.

REVIEW OF THE AUDIT REPORT

The independent auditors have issued and clean and unmodified report for LLC Company

(landlease group). There are no additional sections or paragraphs highlighting any issues. Only

as per the requirements of standards, the auditor have separately mentioned certain key audit

matters relation to inventories, construction and development revenue and equity accounted

investments.

Additional section

Audit matters relation to inventories, construction and development revenue and equity

accounted investments. However, there is no separate opinion on them.

Nature of the issue

These are the capital nature issues. They are the most significant matters, which auditor thinks

that the shareholders should be aware of (Czerney, Schmidt & Thompson, 2014).

Audit opinion

Company has given the opinion that company has complied with the all the applicable rules and

regulations. It has given un-qualified audit opinion that company has no issues with the

corporate governance.

11

Auditing

REFERENCES

Brown-Liburd, H., Issa, H., & Lombardi, D. (2015). Behavioral implications of Big Data's

impact on audit judgment and decision making and future research directions. Accounting

Horizons, 29(2), 451-468.

Christensen, B. E., Glover, S. M., & Wood, D. A. (2012). Extreme estimation uncertainty in fair

value estimates: Implications for audit assurance. Auditing: A Journal of Practice &

Theory, 31(1), 127-146.

Cohen, J., Krishnamoorthy, G. & Wright, A., (2017). Enterprise risk management and the

financial reporting process: The experiences of audit committee members, CFOs, and

external auditors. Contemporary Accounting Research, 34(2), pp.1178-1209.

Cohen, J.R. & Simnett, R., (2014). CSR and assurance services: A research agenda. Auditing: A

Journal of Practice & Theory, 34(1), pp.59-74.

Czerney, K., Schmidt, J. J., & Thompson, A. M. (2014). Does auditor explanatory language in

unqualified audit reports indicate increased financial misstatement risk?. The Accounting

Review, 89(6), 2115-2149.

Edgley, C., Jones, M.J. & Atkins, J., (2015). The adoption of the materiality concept in social

and environmental reporting assurance: A field study approach. The British Accounting

Review, 47(1), pp.1-18.

Edgley, C., Jones, M.J. & Atkins, J., (2015). The adoption of the materiality concept in social

and environmental reporting assurance: A field study approach. The British Accounting

Review, 47(1), pp.1-18.

Eilifsen, A., & Messier Jr, W. F. (2014). Materiality guidance of the major public accounting

firms. Auditing: A Journal of Practice & Theory, 34(2), 3-26.

Eilifsen, A., Hamilton, E., & Messier, W. F. (2017). The Importance of Quantifying Uncertainty:

Examining the Effects of Sensitivity Analysis and Audit Materiality Disclosures on

Investors’ Judgments and Decisions.

Fisher, J. G., & Krumwiede, K. (2015). Product costing systems: finding the right

approach. Journal of Corporate Accounting & Finance, 26(4), 13-21.

12

REFERENCES

Brown-Liburd, H., Issa, H., & Lombardi, D. (2015). Behavioral implications of Big Data's

impact on audit judgment and decision making and future research directions. Accounting

Horizons, 29(2), 451-468.

Christensen, B. E., Glover, S. M., & Wood, D. A. (2012). Extreme estimation uncertainty in fair

value estimates: Implications for audit assurance. Auditing: A Journal of Practice &

Theory, 31(1), 127-146.

Cohen, J., Krishnamoorthy, G. & Wright, A., (2017). Enterprise risk management and the

financial reporting process: The experiences of audit committee members, CFOs, and

external auditors. Contemporary Accounting Research, 34(2), pp.1178-1209.

Cohen, J.R. & Simnett, R., (2014). CSR and assurance services: A research agenda. Auditing: A

Journal of Practice & Theory, 34(1), pp.59-74.

Czerney, K., Schmidt, J. J., & Thompson, A. M. (2014). Does auditor explanatory language in

unqualified audit reports indicate increased financial misstatement risk?. The Accounting

Review, 89(6), 2115-2149.

Edgley, C., Jones, M.J. & Atkins, J., (2015). The adoption of the materiality concept in social

and environmental reporting assurance: A field study approach. The British Accounting

Review, 47(1), pp.1-18.

Edgley, C., Jones, M.J. & Atkins, J., (2015). The adoption of the materiality concept in social

and environmental reporting assurance: A field study approach. The British Accounting

Review, 47(1), pp.1-18.

Eilifsen, A., & Messier Jr, W. F. (2014). Materiality guidance of the major public accounting

firms. Auditing: A Journal of Practice & Theory, 34(2), 3-26.

Eilifsen, A., Hamilton, E., & Messier, W. F. (2017). The Importance of Quantifying Uncertainty:

Examining the Effects of Sensitivity Analysis and Audit Materiality Disclosures on

Investors’ Judgments and Decisions.

Fisher, J. G., & Krumwiede, K. (2015). Product costing systems: finding the right

approach. Journal of Corporate Accounting & Finance, 26(4), 13-21.

12

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Auditing

Hines, C.S., Masli, A., Mauldin, E.G.& Peters, G.F., (2015). Board risk committees and audit

pricing. Auditing: A Journal of Practice & Theory, 34(4), pp.59-84.

Kanatov, M., Atymtayeva, L., & Yagaliyeva, B. (2014, December). Expert systems for

information security management and audit. Implementation phase issues. In Soft

Computing and Intelligent Systems (SCIS), 2014 Joint 7th International Conference on and

Advanced Intelligent Systems (ISIS), 15th International Symposium on (pp. 896-900).

IEEE.

Knechel, W. R., & Salterio, S. E. (2016). Auditing: Assurance and risk. Routledge.

Louwers, T. J., Ramsay, R. J., Sinason, D. H., Strawser, J. R., & Thibodeau, J. C.

(2015). Auditing & assurance services. McGraw-Hill Education.

Psaros, J., & Seamer, M. (2015). Ranking Corporate Governance of Australia's Top Companies:

A Decade On. Australian Accounting Review, 25(4), 405-412.

13

Hines, C.S., Masli, A., Mauldin, E.G.& Peters, G.F., (2015). Board risk committees and audit

pricing. Auditing: A Journal of Practice & Theory, 34(4), pp.59-84.

Kanatov, M., Atymtayeva, L., & Yagaliyeva, B. (2014, December). Expert systems for

information security management and audit. Implementation phase issues. In Soft

Computing and Intelligent Systems (SCIS), 2014 Joint 7th International Conference on and

Advanced Intelligent Systems (ISIS), 15th International Symposium on (pp. 896-900).

IEEE.

Knechel, W. R., & Salterio, S. E. (2016). Auditing: Assurance and risk. Routledge.

Louwers, T. J., Ramsay, R. J., Sinason, D. H., Strawser, J. R., & Thibodeau, J. C.

(2015). Auditing & assurance services. McGraw-Hill Education.

Psaros, J., & Seamer, M. (2015). Ranking Corporate Governance of Australia's Top Companies:

A Decade On. Australian Accounting Review, 25(4), 405-412.

13

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.