Auditing DHL: Procedures, Risks, and Internal Control Analysis

VerifiedAdded on 2022/11/29

|15

|3187

|342

Report

AI Summary

This memorandum provides a comprehensive audit of DHL, focusing on risk assessment, audit procedures, and internal controls. It discusses the risks associated with DHL's business, particularly concerning the new patient revenue system and the arrangements with Acuity Vision. The report covers key assertions at risk, implications for DHL's control environment, and the effectiveness of customer payment testing. It details audit procedures for accounts payable, key assertions related to overtime payments at Pellegrino Shores, and both preventive and detective internal control measures. The analysis includes the impact of business risks, such as fraud, on DHL's financial statements and the auditor's responsibilities. The report emphasizes the importance of understanding DHL's business and its risks to form relevant opinions on the financial statements, ensuring the removal of material misstatements and omissions. The document provides insights into additional audit work, key questions for internal audit, and the audit strategy to be employed, covering features of the engagement, reporting objectives, audit time, and communication nature. Furthermore, the report examines key account balances, assertions, and implications for environmental control within DHL.

Auditing

Name of the Student:

Name of the University:

Author’s note:

Name of the Student:

Name of the University:

Author’s note:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

MEMORANDUM

To: Mr. Jek Porkins

From:

CC:

Subject: Related to audit procedures and assertions with respect to key risks.

Date: 12th September 2019

Introduction

The memorandum is prepared with the objective to discuss with the audit senior of DHL

regarding what are the risk associated with its business as well as to have information about his

accounts affected through the fraud. It discusses about audit work and procedure as well as audit

risks with respect to switchover of new patient revenue system of St Neville. The memorandum

further discusses about several assertions related to risk all due to paying of sales team of Acuity

Vision (Whittington & Margheim, 2014). Further it tends to include implications for control of

environment of DHL including the discussion about several issues that the management of DHL

would consider. The memorandum has emphasized on accounts payable tests with respect to test

of control, assertions for each test , conclusion along with reasons and also involves additional

procedures related to audit that can be performed(Kiesow, Zarvic & Thomas,2014. Moreover,

the memorandum focuses to discuss on key assertions those are at risk with respect to overtime

To: Mr. Jek Porkins

From:

CC:

Subject: Related to audit procedures and assertions with respect to key risks.

Date: 12th September 2019

Introduction

The memorandum is prepared with the objective to discuss with the audit senior of DHL

regarding what are the risk associated with its business as well as to have information about his

accounts affected through the fraud. It discusses about audit work and procedure as well as audit

risks with respect to switchover of new patient revenue system of St Neville. The memorandum

further discusses about several assertions related to risk all due to paying of sales team of Acuity

Vision (Whittington & Margheim, 2014). Further it tends to include implications for control of

environment of DHL including the discussion about several issues that the management of DHL

would consider. The memorandum has emphasized on accounts payable tests with respect to test

of control, assertions for each test , conclusion along with reasons and also involves additional

procedures related to audit that can be performed(Kiesow, Zarvic & Thomas,2014. Moreover,

the memorandum focuses to discuss on key assertions those are at risk with respect to overtime

payment for Pellegrino Shores and it also involves preventive internal as well as detective

internal control measures for addressing the risk ascertained as well as identified.

Due to the fraudness caused by Pellegrino Shores business risk may be diverse and the largest

risk will get to continue for the company of DHL. The business risk that would take place due to

fraudness would cause failure into the business of DHL (Griffiths, 2016). It would take place in

the form of high level of financial risk, issues for cash flow, increase in the cost of production,

loss of profit, decrease in customers as well issues which are legal. The business risk would

impact as per the effect of fraudness by Pellegrino Shores are as follows:

Due to business risk there is an impact as top down approach to be used in audit along

with the financial statements.

Business risk would impact into merge of inherit as well as control risk for audit.

The residual risk arising due to inherent as well as control risk through the impact of

business risk need to get reduced through the action of audit.

Business risk can impact into the form of analytical process for verifying assertions of

financial statements.

Business risk might impact into business failure that might lead the auditor to consider

going concern concept of the business client.

Due to business risk the impact will be due to the fraudness is the audit should make

business more understanding such that large databases containing information is fruitful

(Knechel& Salterio, 2016).

Such business risk would enable the auditor to express further opinion that would be

relevant to financial statements. There should be removal in material misstatements as

well as removal of omission in case of financial statements (Keune & Johnstone, 2015).

internal control measures for addressing the risk ascertained as well as identified.

Due to the fraudness caused by Pellegrino Shores business risk may be diverse and the largest

risk will get to continue for the company of DHL. The business risk that would take place due to

fraudness would cause failure into the business of DHL (Griffiths, 2016). It would take place in

the form of high level of financial risk, issues for cash flow, increase in the cost of production,

loss of profit, decrease in customers as well issues which are legal. The business risk would

impact as per the effect of fraudness by Pellegrino Shores are as follows:

Due to business risk there is an impact as top down approach to be used in audit along

with the financial statements.

Business risk would impact into merge of inherit as well as control risk for audit.

The residual risk arising due to inherent as well as control risk through the impact of

business risk need to get reduced through the action of audit.

Business risk can impact into the form of analytical process for verifying assertions of

financial statements.

Business risk might impact into business failure that might lead the auditor to consider

going concern concept of the business client.

Due to business risk the impact will be due to the fraudness is the audit should make

business more understanding such that large databases containing information is fruitful

(Knechel& Salterio, 2016).

Such business risk would enable the auditor to express further opinion that would be

relevant to financial statements. There should be removal in material misstatements as

well as removal of omission in case of financial statements (Keune & Johnstone, 2015).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

The auditor becomes concerned about this business risk occurring as it might impact into

the financial statements and hence complete understanding of business of DHL is needed

to be known by the auditor as well as its risks even. As an impact of this business risk

occurring auditor shall plan the strategy of audit related to the risks of business.

Additional audit work to be undertaken with respect to new political revenue system:

a.) Associated audit risks:

There are audit risks that are associated with newly political revenue system. The risks are

Inherent risks: This kind of audit risk is associated in the form of procedures to detect the

issues (Ruhnke & Schmidt 2014). The audit work might be in the form of audit plan,

proper approach of audit and strategies of audit. There is an audit plan to conduct internal

audit. The audit approach is used in the form of risk analysis to control internal

operations.

Detection risks: The auditor should identify and correct misstatements of financial

statements at the time of auditing (Keune, & Johnstone, 2015). As a matter of audit work

there should be proper detection of risk by clear understanding of company, proper

methods to be used for identification of risk of financial report of the business.

Control risks: As the form of audit work there should be proper investigation as well as

accuracy of financial statements (Chen, 2016). Fraud should be detected and areas should

be identified related to control risks. Proper planning as well as strategy should be made

and internal control should be there for financial reporting.

the financial statements and hence complete understanding of business of DHL is needed

to be known by the auditor as well as its risks even. As an impact of this business risk

occurring auditor shall plan the strategy of audit related to the risks of business.

Additional audit work to be undertaken with respect to new political revenue system:

a.) Associated audit risks:

There are audit risks that are associated with newly political revenue system. The risks are

Inherent risks: This kind of audit risk is associated in the form of procedures to detect the

issues (Ruhnke & Schmidt 2014). The audit work might be in the form of audit plan,

proper approach of audit and strategies of audit. There is an audit plan to conduct internal

audit. The audit approach is used in the form of risk analysis to control internal

operations.

Detection risks: The auditor should identify and correct misstatements of financial

statements at the time of auditing (Keune, & Johnstone, 2015). As a matter of audit work

there should be proper detection of risk by clear understanding of company, proper

methods to be used for identification of risk of financial report of the business.

Control risks: As the form of audit work there should be proper investigation as well as

accuracy of financial statements (Chen, 2016). Fraud should be detected and areas should

be identified related to control risks. Proper planning as well as strategy should be made

and internal control should be there for financial reporting.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

b.) Two key questions to ask internal audit

How to measure internal audit and its effectiveness with respect to switchover of new

patient revenue system?

What are the different risks that would affect implementation of strategic procurement to

be successful?

c.) The audit strategy used in the case of audit in this case should be short in terms of audit

for DHL (Wahl, 2015). If there there changes in case of conditions or result of procedures

related to audit in that case there must be significant audit strategy to be used. In case

there is an alteration then reason for such should be mentioned along with relevant

documents. The proper audit plan which should be more detailed than document related

to strategy as the audit plan would reveal about time, the extent of particular procedures

of audit which is to be conducted by the team of audit. Moreover, the document

containing strategy should include statement related to all decisions required to plan

audit. Proper audit strategy would involve:

Features of the engagement

Objectives of reporting

Audit time

Communication nature

Relevant factors for engagement of efforts of the team

Additional information that is required with respect to Acquity Vision’s sale of medical supplies

will be:

How to measure internal audit and its effectiveness with respect to switchover of new

patient revenue system?

What are the different risks that would affect implementation of strategic procurement to

be successful?

c.) The audit strategy used in the case of audit in this case should be short in terms of audit

for DHL (Wahl, 2015). If there there changes in case of conditions or result of procedures

related to audit in that case there must be significant audit strategy to be used. In case

there is an alteration then reason for such should be mentioned along with relevant

documents. The proper audit plan which should be more detailed than document related

to strategy as the audit plan would reveal about time, the extent of particular procedures

of audit which is to be conducted by the team of audit. Moreover, the document

containing strategy should include statement related to all decisions required to plan

audit. Proper audit strategy would involve:

Features of the engagement

Objectives of reporting

Audit time

Communication nature

Relevant factors for engagement of efforts of the team

Additional information that is required with respect to Acquity Vision’s sale of medical supplies

will be:

a.) Key account balances well as assertions that are associated with risk due to the

arrangements to Acquity Vision’s for paying its sales team:

Account balances: There should be assertions related to whether asset, liability

exists. Even there can be assertions in the form of determining whether this

company is able to control its rights for asset or not (Knechel & Salterio, 2016).

Further completeness related to all information are completely recorded or not

should be taken into account.

Transaction classes: There should be assertions with respect to whether

transactions have been properly recorded. Further there can also be assertion that

can take place relating to accuracy where there should be amount that should be

recorded in the form of transactions appropriate manner.

Presentation as well as disclosure: The assertions must be in the form of events

disclosed transactions as well as other matters. There should be completeness

relating to all disclosures that is important to be included. On the other hand

financial information should be properly presented as well as described.

b.) The implications for the environmental control within DHL including specific issues

which the management need to consider:

The key issue would be included in the form of following:

Pollution as well as modern living would go in the same way but the costs related

to pollution are considerable as an issue (Barton & Bruder, 2014).

Waste disposal is another issue. There is a need for improved waste disposal

Climatic change also becomes an issue as it negatively would affect the

productivity of DHL.

arrangements to Acquity Vision’s for paying its sales team:

Account balances: There should be assertions related to whether asset, liability

exists. Even there can be assertions in the form of determining whether this

company is able to control its rights for asset or not (Knechel & Salterio, 2016).

Further completeness related to all information are completely recorded or not

should be taken into account.

Transaction classes: There should be assertions with respect to whether

transactions have been properly recorded. Further there can also be assertion that

can take place relating to accuracy where there should be amount that should be

recorded in the form of transactions appropriate manner.

Presentation as well as disclosure: The assertions must be in the form of events

disclosed transactions as well as other matters. There should be completeness

relating to all disclosures that is important to be included. On the other hand

financial information should be properly presented as well as described.

b.) The implications for the environmental control within DHL including specific issues

which the management need to consider:

The key issue would be included in the form of following:

Pollution as well as modern living would go in the same way but the costs related

to pollution are considerable as an issue (Barton & Bruder, 2014).

Waste disposal is another issue. There is a need for improved waste disposal

Climatic change also becomes an issue as it negatively would affect the

productivity of DHL.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Solving of complex issues also becomes a problem. It is effecting DHL’s

individual, the company itself as well as the community.

There can be specific implications with respect to environmental control of DHL. There can be

an improvement into the environmental performance. This can be possible in the form of

environmental leadership and good corporate culture establishment which should be

demonstrated through senior manager of DHL. There should be acceptance of the policies and

there should be proper governing principles, clarity in standards of performance as well as

procedures of operation technologies and there should be proper system to measure performance.

There should be system to measure as well as evaluate environmental performance.

c.) The effectiveness of customer payment testing:

Customer payment testing becomes effective when testing of payment

functionality is proper.

Proper integrations with customer payment makes it effective.

In case of customer payment testing security is considered to be most important

aspect for safety of customer payment transactions (Takanen et al., 2018)).

Performance is another effective means of customer payment testing. In order to

achieve benchmark with respect to desired performance all factors should be

considered for making customer payment test effective.

Proper database becomes another important aspect for successful customer

payment testing. Certain aspect should be considered keeping in mind about test

of customer payment that would make it to be effective.

In case of both accounts payable tests have been undertaken:

individual, the company itself as well as the community.

There can be specific implications with respect to environmental control of DHL. There can be

an improvement into the environmental performance. This can be possible in the form of

environmental leadership and good corporate culture establishment which should be

demonstrated through senior manager of DHL. There should be acceptance of the policies and

there should be proper governing principles, clarity in standards of performance as well as

procedures of operation technologies and there should be proper system to measure performance.

There should be system to measure as well as evaluate environmental performance.

c.) The effectiveness of customer payment testing:

Customer payment testing becomes effective when testing of payment

functionality is proper.

Proper integrations with customer payment makes it effective.

In case of customer payment testing security is considered to be most important

aspect for safety of customer payment transactions (Takanen et al., 2018)).

Performance is another effective means of customer payment testing. In order to

achieve benchmark with respect to desired performance all factors should be

considered for making customer payment test effective.

Proper database becomes another important aspect for successful customer

payment testing. Certain aspect should be considered keeping in mind about test

of customer payment that would make it to be effective.

In case of both accounts payable tests have been undertaken:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

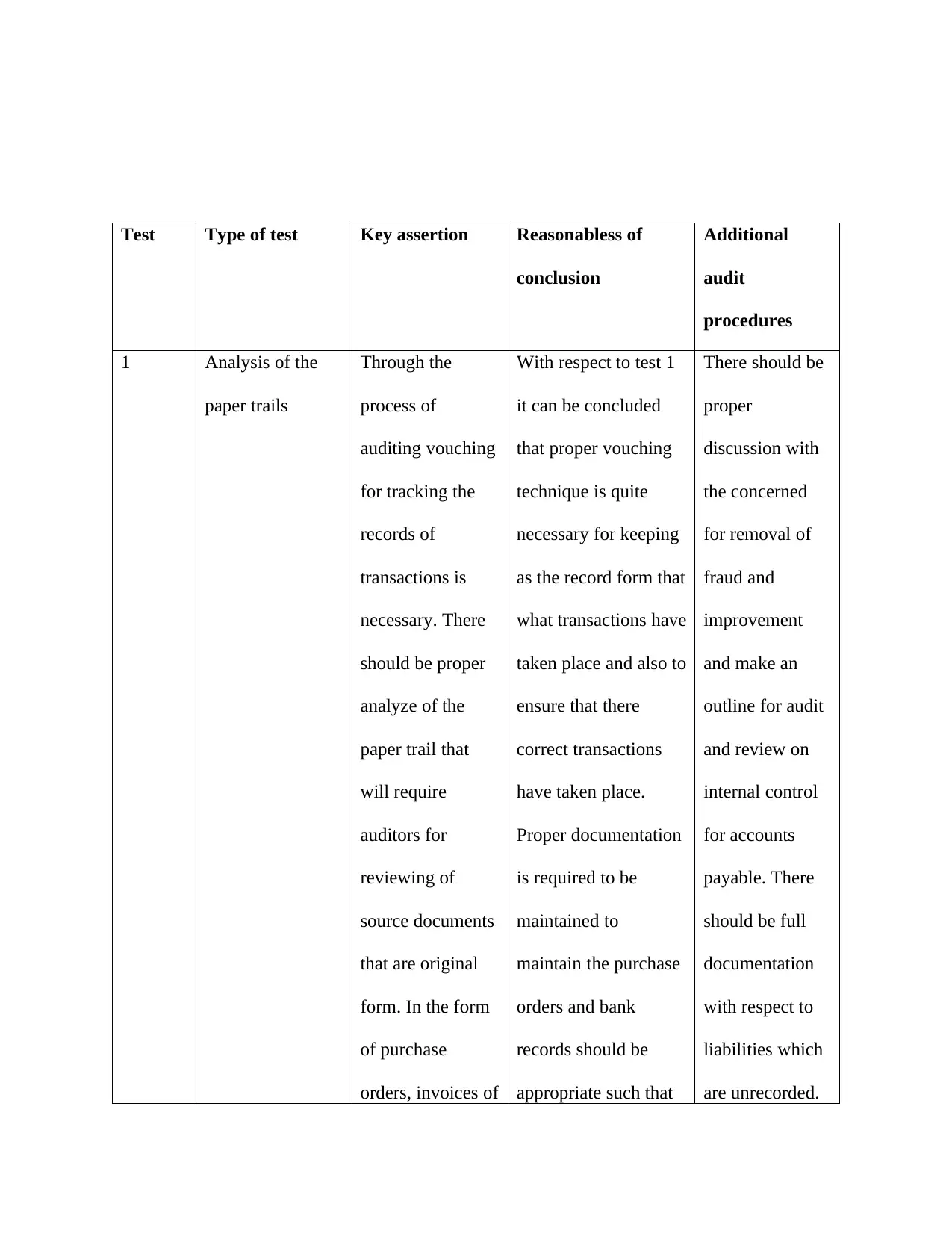

Test Type of test Key assertion Reasonabless of

conclusion

Additional

audit

procedures

1 Analysis of the

paper trails

Through the

process of

auditing vouching

for tracking the

records of

transactions is

necessary. There

should be proper

analyze of the

paper trail that

will require

auditors for

reviewing of

source documents

that are original

form. In the form

of purchase

orders, invoices of

With respect to test 1

it can be concluded

that proper vouching

technique is quite

necessary for keeping

as the record form that

what transactions have

taken place and also to

ensure that there

correct transactions

have taken place.

Proper documentation

is required to be

maintained to

maintain the purchase

orders and bank

records should be

appropriate such that

There should be

proper

discussion with

the concerned

for removal of

fraud and

improvement

and make an

outline for audit

and review on

internal control

for accounts

payable. There

should be full

documentation

with respect to

liabilities which

are unrecorded.

conclusion

Additional

audit

procedures

1 Analysis of the

paper trails

Through the

process of

auditing vouching

for tracking the

records of

transactions is

necessary. There

should be proper

analyze of the

paper trail that

will require

auditors for

reviewing of

source documents

that are original

form. In the form

of purchase

orders, invoices of

With respect to test 1

it can be concluded

that proper vouching

technique is quite

necessary for keeping

as the record form that

what transactions have

taken place and also to

ensure that there

correct transactions

have taken place.

Proper documentation

is required to be

maintained to

maintain the purchase

orders and bank

records should be

appropriate such that

There should be

proper

discussion with

the concerned

for removal of

fraud and

improvement

and make an

outline for audit

and review on

internal control

for accounts

payable. There

should be full

documentation

with respect to

liabilities which

are unrecorded.

its vendor as well

as records in

bank. It will be

the responsibility

of the team audit

for selection of

such transactions

those are accurate

and it’s necessary

to ascertain the

invoiced terms of

the DHL.

there is no error.

Moreover, correctness

as well as accuracy

through audit

procedure is essential.

Further there

should be

detailed account

payable ledger

that needs to be

maintained.

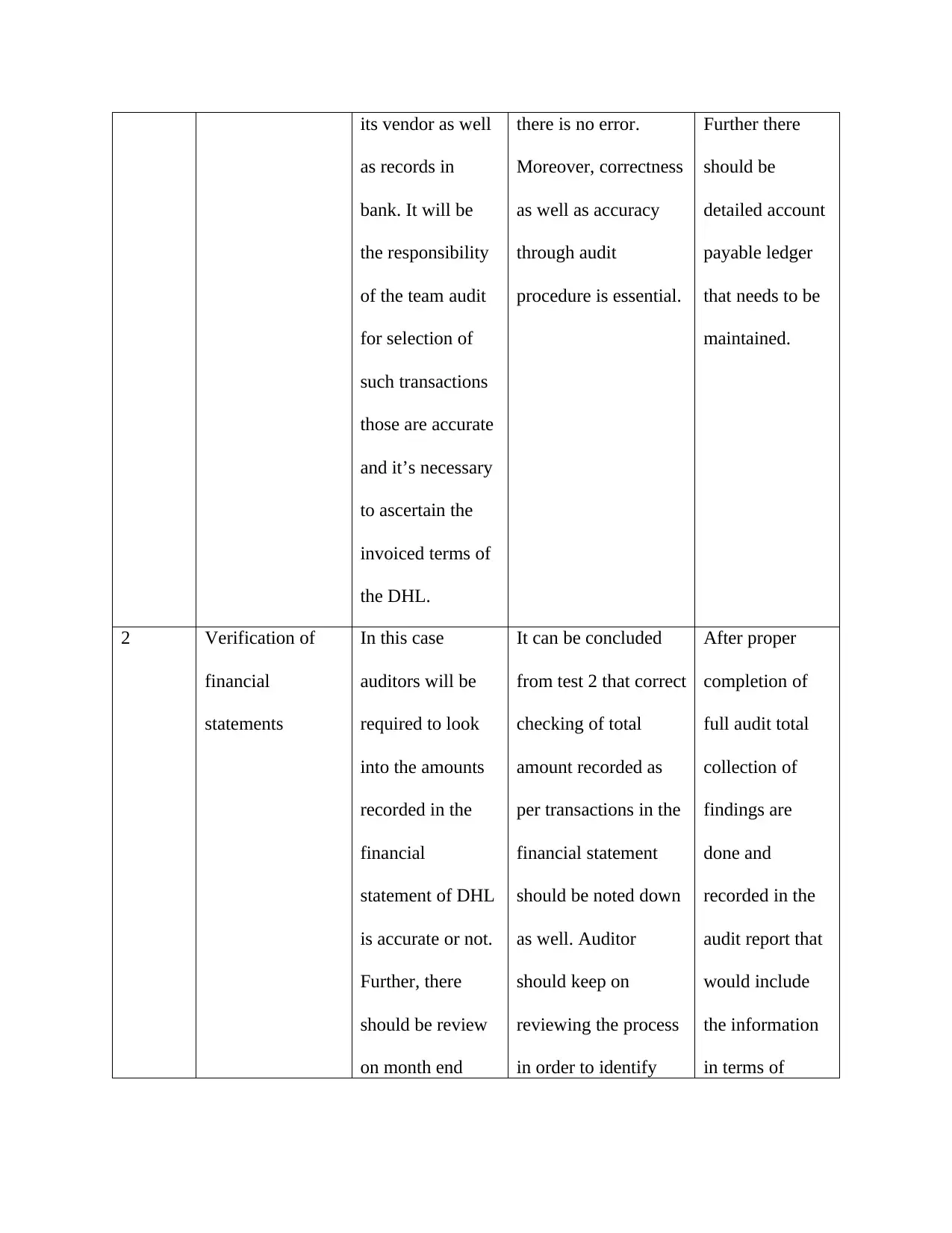

2 Verification of

financial

statements

In this case

auditors will be

required to look

into the amounts

recorded in the

financial

statement of DHL

is accurate or not.

Further, there

should be review

on month end

It can be concluded

from test 2 that correct

checking of total

amount recorded as

per transactions in the

financial statement

should be noted down

as well. Auditor

should keep on

reviewing the process

in order to identify

After proper

completion of

full audit total

collection of

findings are

done and

recorded in the

audit report that

would include

the information

in terms of

as records in

bank. It will be

the responsibility

of the team audit

for selection of

such transactions

those are accurate

and it’s necessary

to ascertain the

invoiced terms of

the DHL.

there is no error.

Moreover, correctness

as well as accuracy

through audit

procedure is essential.

Further there

should be

detailed account

payable ledger

that needs to be

maintained.

2 Verification of

financial

statements

In this case

auditors will be

required to look

into the amounts

recorded in the

financial

statement of DHL

is accurate or not.

Further, there

should be review

on month end

It can be concluded

from test 2 that correct

checking of total

amount recorded as

per transactions in the

financial statement

should be noted down

as well. Auditor

should keep on

reviewing the process

in order to identify

After proper

completion of

full audit total

collection of

findings are

done and

recorded in the

audit report that

would include

the information

in terms of

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

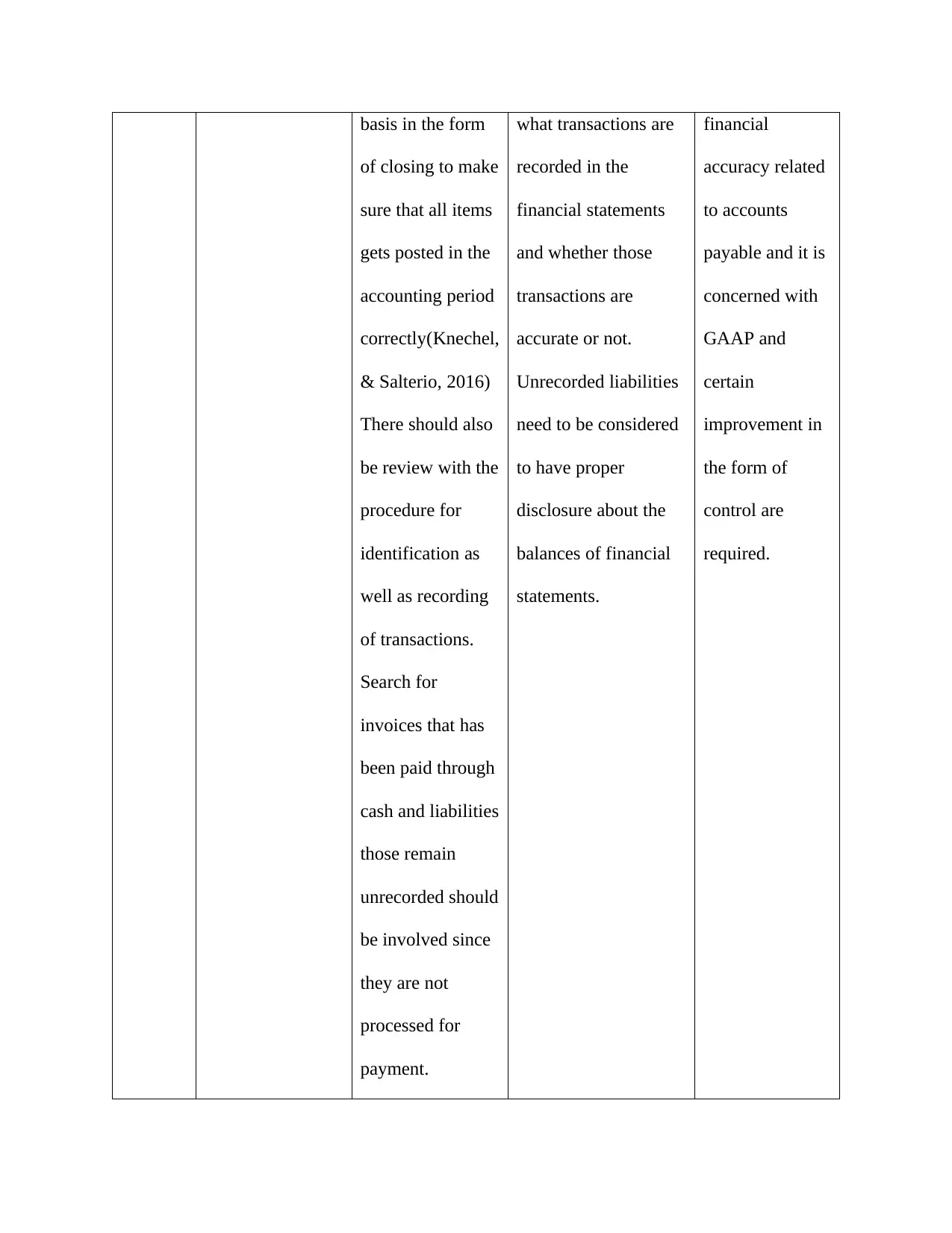

basis in the form

of closing to make

sure that all items

gets posted in the

accounting period

correctly(Knechel,

& Salterio, 2016)

There should also

be review with the

procedure for

identification as

well as recording

of transactions.

Search for

invoices that has

been paid through

cash and liabilities

those remain

unrecorded should

be involved since

they are not

processed for

payment.

what transactions are

recorded in the

financial statements

and whether those

transactions are

accurate or not.

Unrecorded liabilities

need to be considered

to have proper

disclosure about the

balances of financial

statements.

financial

accuracy related

to accounts

payable and it is

concerned with

GAAP and

certain

improvement in

the form of

control are

required.

of closing to make

sure that all items

gets posted in the

accounting period

correctly(Knechel,

& Salterio, 2016)

There should also

be review with the

procedure for

identification as

well as recording

of transactions.

Search for

invoices that has

been paid through

cash and liabilities

those remain

unrecorded should

be involved since

they are not

processed for

payment.

what transactions are

recorded in the

financial statements

and whether those

transactions are

accurate or not.

Unrecorded liabilities

need to be considered

to have proper

disclosure about the

balances of financial

statements.

financial

accuracy related

to accounts

payable and it is

concerned with

GAAP and

certain

improvement in

the form of

control are

required.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

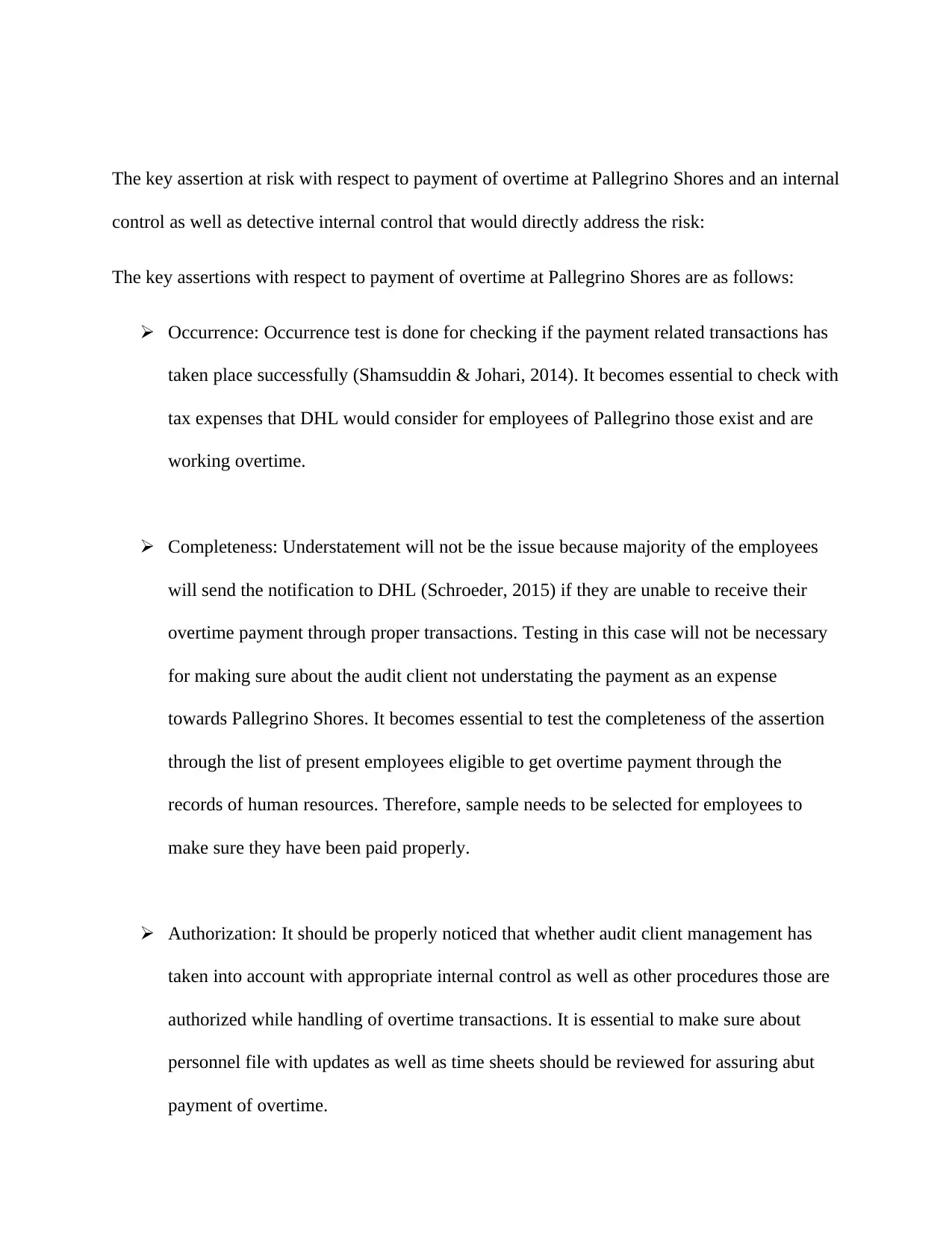

The key assertion at risk with respect to payment of overtime at Pallegrino Shores and an internal

control as well as detective internal control that would directly address the risk:

The key assertions with respect to payment of overtime at Pallegrino Shores are as follows:

Occurrence: Occurrence test is done for checking if the payment related transactions has

taken place successfully (Shamsuddin & Johari, 2014). It becomes essential to check with

tax expenses that DHL would consider for employees of Pallegrino those exist and are

working overtime.

Completeness: Understatement will not be the issue because majority of the employees

will send the notification to DHL (Schroeder, 2015) if they are unable to receive their

overtime payment through proper transactions. Testing in this case will not be necessary

for making sure about the audit client not understating the payment as an expense

towards Pallegrino Shores. It becomes essential to test the completeness of the assertion

through the list of present employees eligible to get overtime payment through the

records of human resources. Therefore, sample needs to be selected for employees to

make sure they have been paid properly.

Authorization: It should be properly noticed that whether audit client management has

taken into account with appropriate internal control as well as other procedures those are

authorized while handling of overtime transactions. It is essential to make sure about

personnel file with updates as well as time sheets should be reviewed for assuring abut

payment of overtime.

control as well as detective internal control that would directly address the risk:

The key assertions with respect to payment of overtime at Pallegrino Shores are as follows:

Occurrence: Occurrence test is done for checking if the payment related transactions has

taken place successfully (Shamsuddin & Johari, 2014). It becomes essential to check with

tax expenses that DHL would consider for employees of Pallegrino those exist and are

working overtime.

Completeness: Understatement will not be the issue because majority of the employees

will send the notification to DHL (Schroeder, 2015) if they are unable to receive their

overtime payment through proper transactions. Testing in this case will not be necessary

for making sure about the audit client not understating the payment as an expense

towards Pallegrino Shores. It becomes essential to test the completeness of the assertion

through the list of present employees eligible to get overtime payment through the

records of human resources. Therefore, sample needs to be selected for employees to

make sure they have been paid properly.

Authorization: It should be properly noticed that whether audit client management has

taken into account with appropriate internal control as well as other procedures those are

authorized while handling of overtime transactions. It is essential to make sure about

personnel file with updates as well as time sheets should be reviewed for assuring abut

payment of overtime.

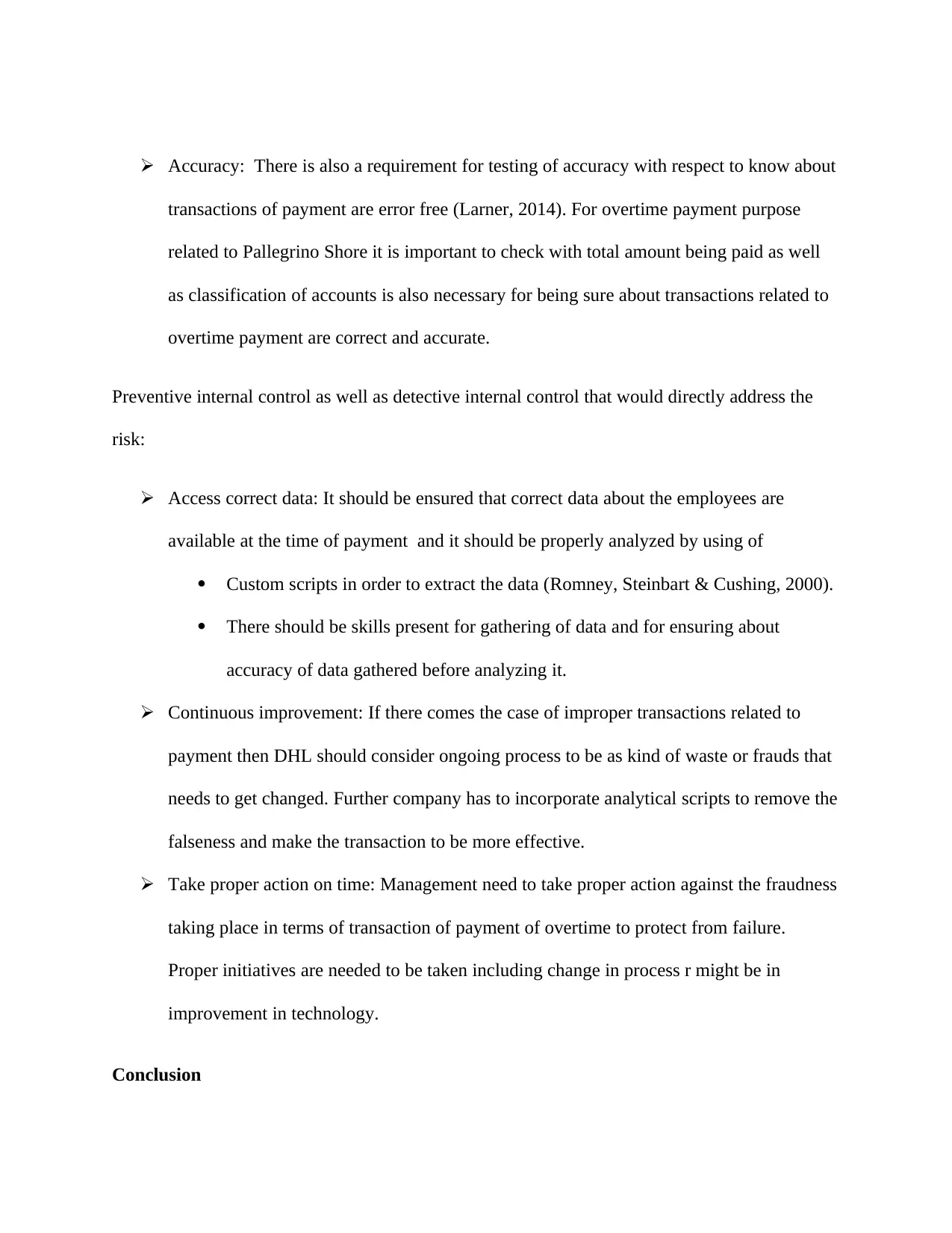

Accuracy: There is also a requirement for testing of accuracy with respect to know about

transactions of payment are error free (Larner, 2014). For overtime payment purpose

related to Pallegrino Shore it is important to check with total amount being paid as well

as classification of accounts is also necessary for being sure about transactions related to

overtime payment are correct and accurate.

Preventive internal control as well as detective internal control that would directly address the

risk:

Access correct data: It should be ensured that correct data about the employees are

available at the time of payment and it should be properly analyzed by using of

Custom scripts in order to extract the data (Romney, Steinbart & Cushing, 2000).

There should be skills present for gathering of data and for ensuring about

accuracy of data gathered before analyzing it.

Continuous improvement: If there comes the case of improper transactions related to

payment then DHL should consider ongoing process to be as kind of waste or frauds that

needs to get changed. Further company has to incorporate analytical scripts to remove the

falseness and make the transaction to be more effective.

Take proper action on time: Management need to take proper action against the fraudness

taking place in terms of transaction of payment of overtime to protect from failure.

Proper initiatives are needed to be taken including change in process r might be in

improvement in technology.

Conclusion

transactions of payment are error free (Larner, 2014). For overtime payment purpose

related to Pallegrino Shore it is important to check with total amount being paid as well

as classification of accounts is also necessary for being sure about transactions related to

overtime payment are correct and accurate.

Preventive internal control as well as detective internal control that would directly address the

risk:

Access correct data: It should be ensured that correct data about the employees are

available at the time of payment and it should be properly analyzed by using of

Custom scripts in order to extract the data (Romney, Steinbart & Cushing, 2000).

There should be skills present for gathering of data and for ensuring about

accuracy of data gathered before analyzing it.

Continuous improvement: If there comes the case of improper transactions related to

payment then DHL should consider ongoing process to be as kind of waste or frauds that

needs to get changed. Further company has to incorporate analytical scripts to remove the

falseness and make the transaction to be more effective.

Take proper action on time: Management need to take proper action against the fraudness

taking place in terms of transaction of payment of overtime to protect from failure.

Proper initiatives are needed to be taken including change in process r might be in

improvement in technology.

Conclusion

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 15

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.