Audit of Payroll Function: Hangout Restaurant Company

VerifiedAdded on 2022/11/16

|18

|3251

|125

Report

AI Summary

This report presents the findings of an audit of the payroll function and system within the Hangout Restaurant Company. The audit, conducted in accordance with Australian auditing standards, aimed to identify weaknesses, errors, and potential fraud within the payroll system. The report highlights the lack of professional qualifications of the payroll administrator, Susan Kweskia, and the potential for manipulation of employee records by restaurant managers. The audit involved an examination of payroll master files and payment records, revealing significant discrepancies between the amounts due and the amounts paid to employees. Substantive procedures were employed to investigate these discrepancies, and the report details the specific instances of overpayment and missing payments. The report concludes by emphasizing the need for improved controls and procedures to mitigate the risk of fraud and ensure the accuracy of payroll records. The audit was conducted in 2019.

Running head: AUDITING PRACTICE

Auditing Practice

Name of the Student:

Name of the University:

Authors Note:

Auditing Practice

Name of the Student:

Name of the University:

Authors Note:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1

AUDITING PRACTICE

Memorandum

: 30th May, 2019

To: Audit partner, Maxwell Smart

From: (Name of the student)

Ref.: Audit of payroll function and system in Hangout Restaurant Company.

This memorandum shall discuss the findings from the audit of payroll function in the Hangout

Restaurant Company. The focus is to find the area of weaknesses in the payroll system

maintained in the restaurant chain to improve the system as well as to unearth any error or fraud

that have taken place in the payroll function within the company in the period of audit.

In Australia, the professional responsibilities and competencies of an Auditor is governed by the

professional code of conduct applicable in the country. As per the professional code of conduct

an Auditor is required to carry necessary analytical and substantive procedures to corroborate

substantial audit evidence to express an appropriate opinion on the financial statements or a

particular function which is being audited. Auditing in the country is subjected to the auditing

and assurance standards formulated and issued by the Australian Auditing and Assurance

Standards Board (Armitage, 2008).

Auditing of payroll function and system within an organization is quite different compared to the

audit of financial statements of an organization. Thus, the process and procedures to be used by

an auditor to conduct an effective payroll audit are also different from the processes and

procedures required for audit of financial statements. In case of payroll auditing of the Hangout

AUDITING PRACTICE

Memorandum

: 30th May, 2019

To: Audit partner, Maxwell Smart

From: (Name of the student)

Ref.: Audit of payroll function and system in Hangout Restaurant Company.

This memorandum shall discuss the findings from the audit of payroll function in the Hangout

Restaurant Company. The focus is to find the area of weaknesses in the payroll system

maintained in the restaurant chain to improve the system as well as to unearth any error or fraud

that have taken place in the payroll function within the company in the period of audit.

In Australia, the professional responsibilities and competencies of an Auditor is governed by the

professional code of conduct applicable in the country. As per the professional code of conduct

an Auditor is required to carry necessary analytical and substantive procedures to corroborate

substantial audit evidence to express an appropriate opinion on the financial statements or a

particular function which is being audited. Auditing in the country is subjected to the auditing

and assurance standards formulated and issued by the Australian Auditing and Assurance

Standards Board (Armitage, 2008).

Auditing of payroll function and system within an organization is quite different compared to the

audit of financial statements of an organization. Thus, the process and procedures to be used by

an auditor to conduct an effective payroll audit are also different from the processes and

procedures required for audit of financial statements. In case of payroll auditing of the Hangout

2

AUDITING PRACTICE

Restaurant Company the audit procedures shall be carried out by keeping in mind the following

audit objectives:

Accuracy and occurrence:

Ensuring that the payroll system shows all the relevant information related to the payroll

department. Accuracy of these information and actual occurrence of the transactions as shown in

the payroll system are to be tested and verified in the audit (Carcello, 2008).

Completeness, posting and summarization:

A report shall be prepared to verify the completeness of records in the payroll system. The

correctness of positing the records and summarization shall also be verified by the auditor.

Occurrence of payment:

A report shall be made on the employees’ payments in excess of $3000 per fortnight in respect of

any employee. Thus, in case any employee / employees have been paid in excess of $3000 in a

fortnight then the report shall contain necessary details of such employees including payment

details (Carcello, 2008).

Assurance of accuracy and completeness:

Incomplete and inaccurate information will increase the chances of fraud in a payroll system of

an organization. Thus, obtaining audit assurance as to the completeness and accuracy of

information is essential to determine whether payroll system is prone to fraud or not.

Finding inaccurate and fraud entries in the payroll system:

Any inaccurate or fraud records of employees shall be identified by conducting necessary

substantive procedures is essential to the successful completion of the audit.

AUDITING PRACTICE

Restaurant Company the audit procedures shall be carried out by keeping in mind the following

audit objectives:

Accuracy and occurrence:

Ensuring that the payroll system shows all the relevant information related to the payroll

department. Accuracy of these information and actual occurrence of the transactions as shown in

the payroll system are to be tested and verified in the audit (Carcello, 2008).

Completeness, posting and summarization:

A report shall be prepared to verify the completeness of records in the payroll system. The

correctness of positing the records and summarization shall also be verified by the auditor.

Occurrence of payment:

A report shall be made on the employees’ payments in excess of $3000 per fortnight in respect of

any employee. Thus, in case any employee / employees have been paid in excess of $3000 in a

fortnight then the report shall contain necessary details of such employees including payment

details (Carcello, 2008).

Assurance of accuracy and completeness:

Incomplete and inaccurate information will increase the chances of fraud in a payroll system of

an organization. Thus, obtaining audit assurance as to the completeness and accuracy of

information is essential to determine whether payroll system is prone to fraud or not.

Finding inaccurate and fraud entries in the payroll system:

Any inaccurate or fraud records of employees shall be identified by conducting necessary

substantive procedures is essential to the successful completion of the audit.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3

AUDITING PRACTICE

Specific circumstances in respect of payroll audit of the restaurant:

ASA 315 has mentioned the importance to understand an entity and its operations properly to

plan an audit effectively. The guidelines to be followed by an auditor to understand and entity

properly are given in the standard.

In this case the restaurant has 30 employees across five different restaurants. The managers of

each restaurant keep record of the respective employees and send these records to Susan

Kweskia who is responsible to maintain the payroll and employee records of the company. The

managers of five restaurants have their respective secure passwords to send the respective data of

employees to Susan (Dobija, 2018).

Apparent weaknesses in the system identified from the payroll system and function in the

restaurants:

The employee and payroll records are maintained and calculated by Susan Kweskia. No

professional qualifications of Susan has been mentioned except the fact that she is married

Aaron. Thus, it is clear that Susan does not hold any professional qualification to warrant the

responsibility of maintaining and calculating payroll function of Hangout Restaurant Company.

Thus, an expert or professional in the field of payroll management should have been given this

crucial responsibility of maintenance and calculation of payroll and employee records of the

company (Dempsey, 2018).

The threat and risk of manipulation of employee records by the managers:

The managers at each restaurant are responsible to record the number of hours employees are

working with maximum of 80 hours per fortnight and send the details to Susan. The opportunity

of manipulation of records by the manager before sending the details to Susan is significant as

AUDITING PRACTICE

Specific circumstances in respect of payroll audit of the restaurant:

ASA 315 has mentioned the importance to understand an entity and its operations properly to

plan an audit effectively. The guidelines to be followed by an auditor to understand and entity

properly are given in the standard.

In this case the restaurant has 30 employees across five different restaurants. The managers of

each restaurant keep record of the respective employees and send these records to Susan

Kweskia who is responsible to maintain the payroll and employee records of the company. The

managers of five restaurants have their respective secure passwords to send the respective data of

employees to Susan (Dobija, 2018).

Apparent weaknesses in the system identified from the payroll system and function in the

restaurants:

The employee and payroll records are maintained and calculated by Susan Kweskia. No

professional qualifications of Susan has been mentioned except the fact that she is married

Aaron. Thus, it is clear that Susan does not hold any professional qualification to warrant the

responsibility of maintaining and calculating payroll function of Hangout Restaurant Company.

Thus, an expert or professional in the field of payroll management should have been given this

crucial responsibility of maintenance and calculation of payroll and employee records of the

company (Dempsey, 2018).

The threat and risk of manipulation of employee records by the managers:

The managers at each restaurant are responsible to record the number of hours employees are

working with maximum of 80 hours per fortnight and send the details to Susan. The opportunity

of manipulation of records by the manager before sending the details to Susan is significant as

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4

AUDITING PRACTICE

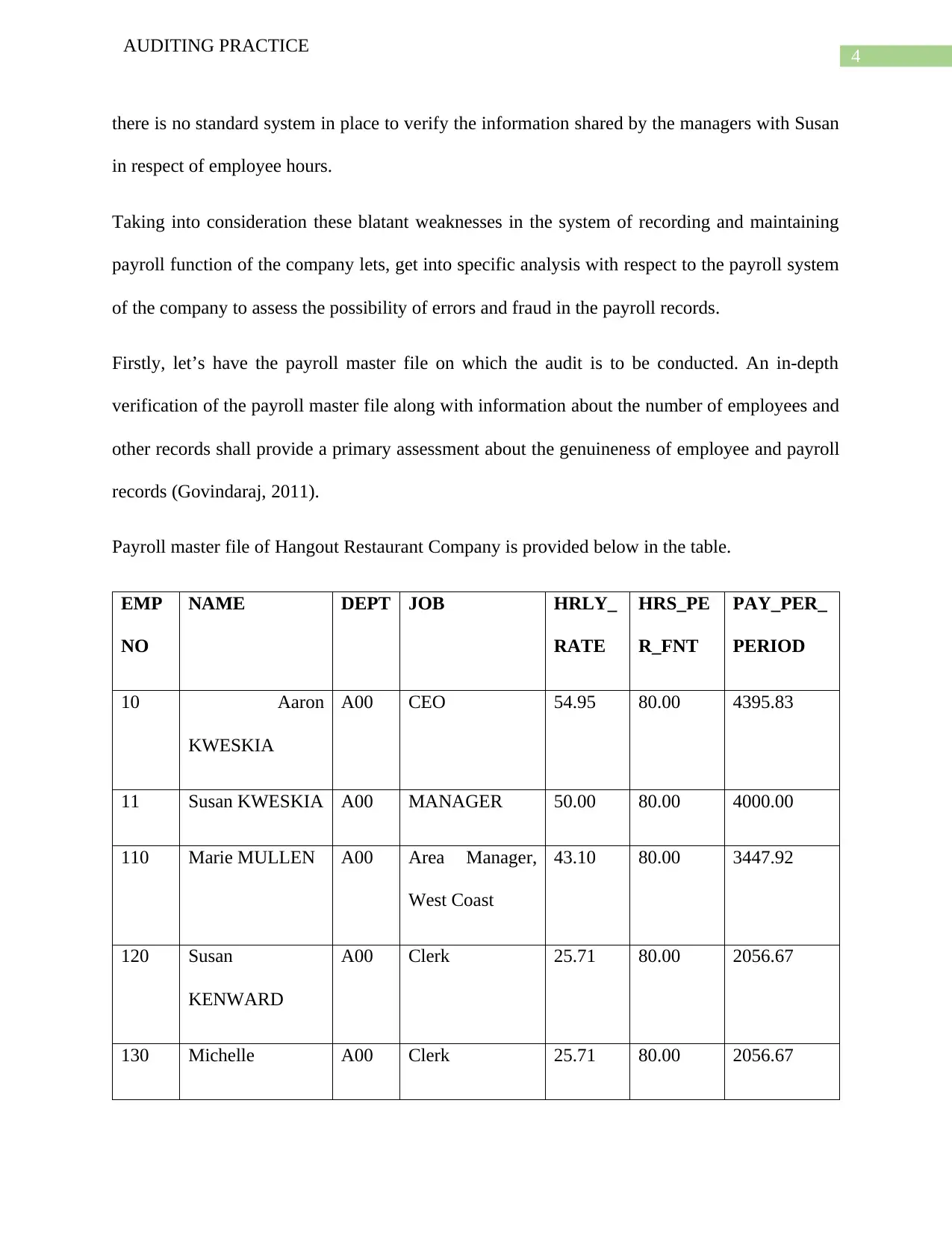

there is no standard system in place to verify the information shared by the managers with Susan

in respect of employee hours.

Taking into consideration these blatant weaknesses in the system of recording and maintaining

payroll function of the company lets, get into specific analysis with respect to the payroll system

of the company to assess the possibility of errors and fraud in the payroll records.

Firstly, let’s have the payroll master file on which the audit is to be conducted. An in-depth

verification of the payroll master file along with information about the number of employees and

other records shall provide a primary assessment about the genuineness of employee and payroll

records (Govindaraj, 2011).

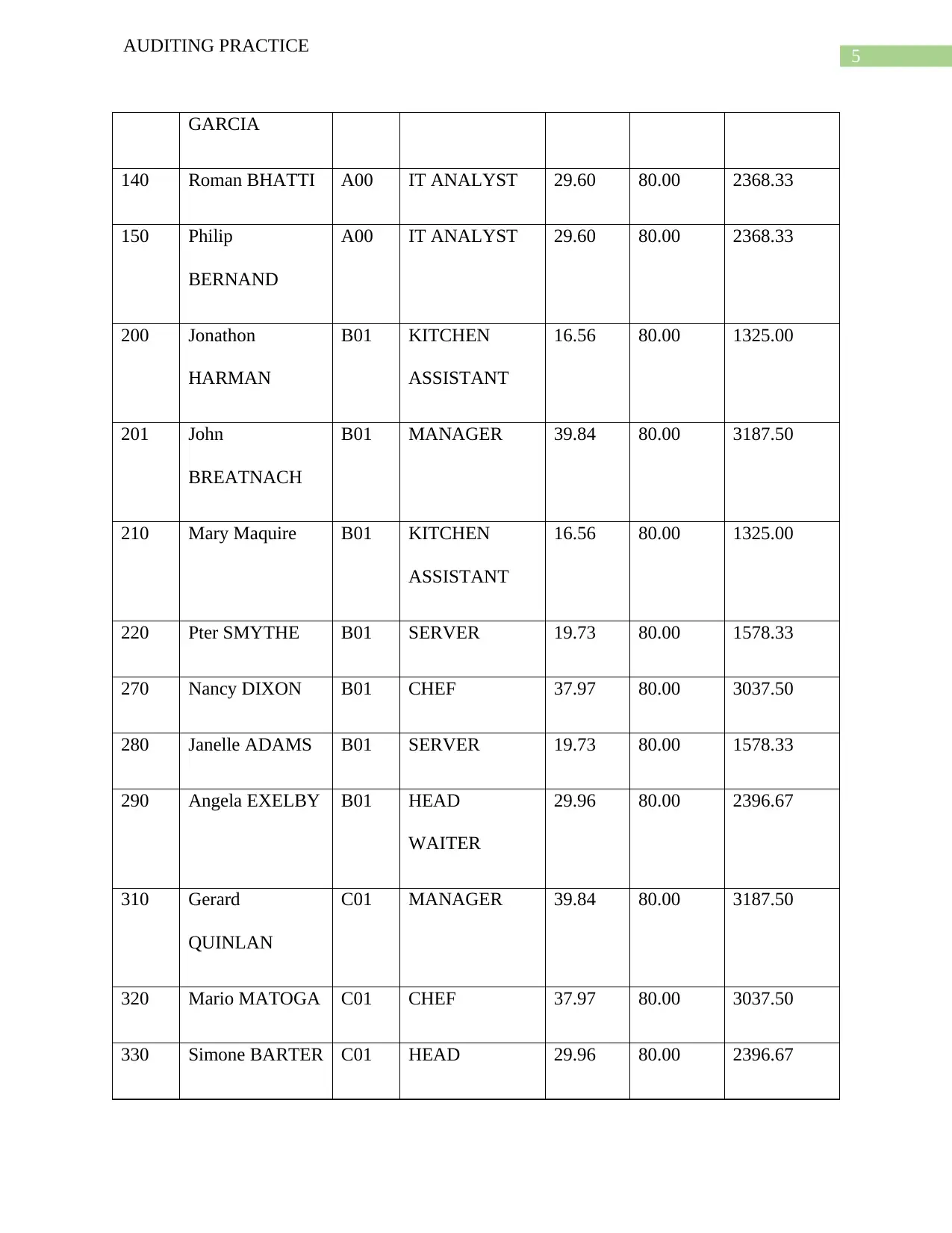

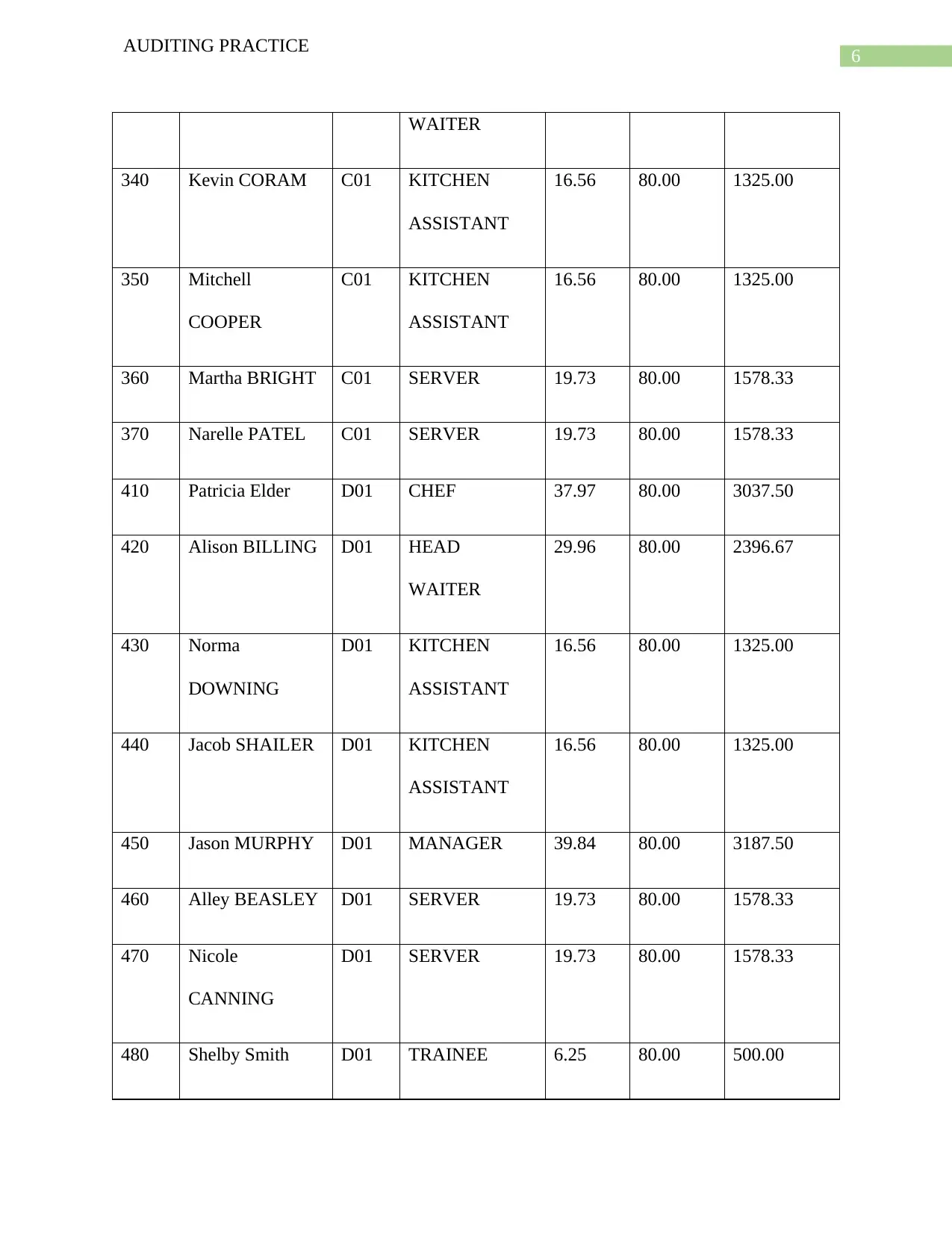

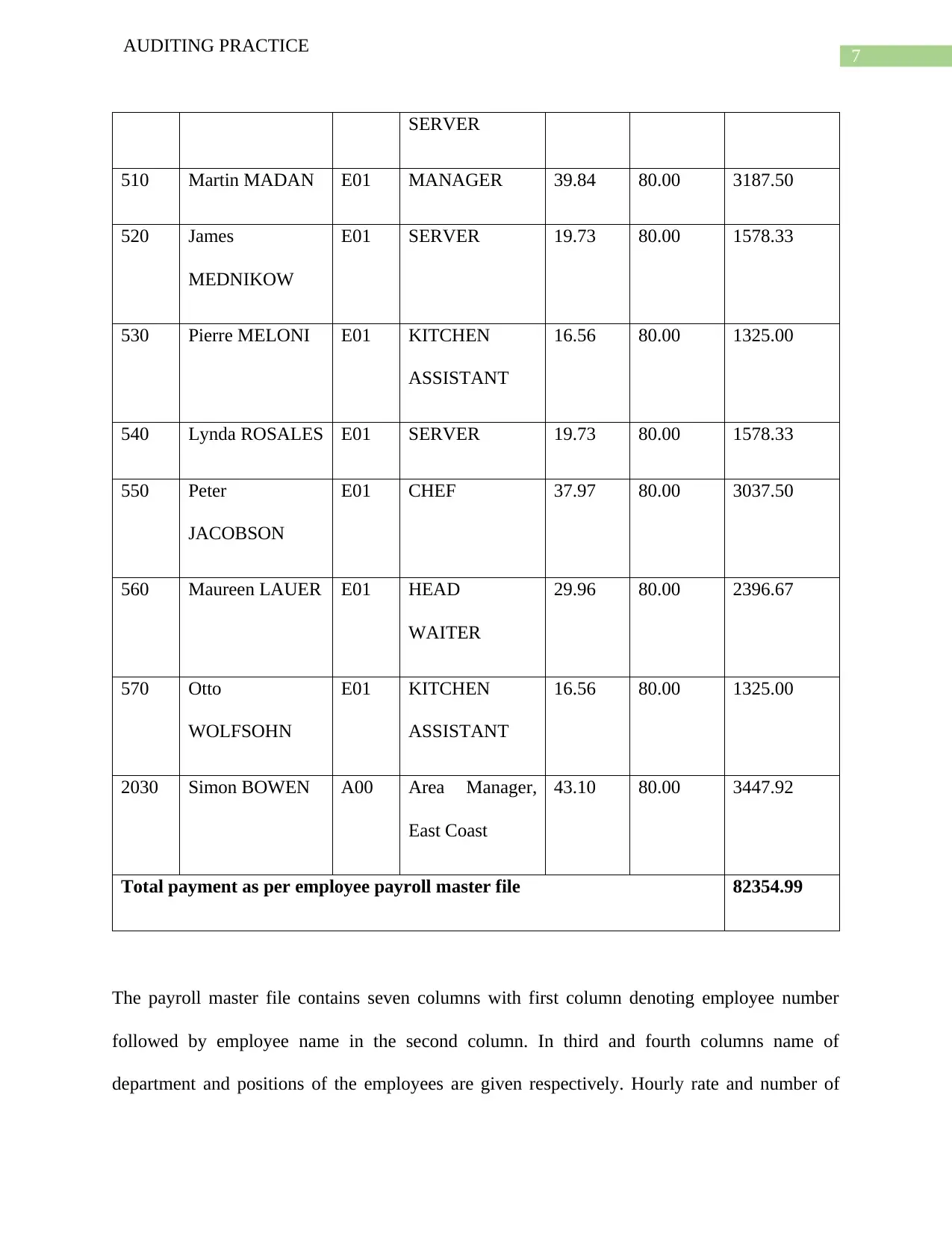

Payroll master file of Hangout Restaurant Company is provided below in the table.

EMP

NO

NAME DEPT JOB HRLY_

RATE

HRS_PE

R_FNT

PAY_PER_

PERIOD

10 Aaron

KWESKIA

A00 CEO 54.95 80.00 4395.83

11 Susan KWESKIA A00 MANAGER 50.00 80.00 4000.00

110 Marie MULLEN A00 Area Manager,

West Coast

43.10 80.00 3447.92

120 Susan

KENWARD

A00 Clerk 25.71 80.00 2056.67

130 Michelle A00 Clerk 25.71 80.00 2056.67

AUDITING PRACTICE

there is no standard system in place to verify the information shared by the managers with Susan

in respect of employee hours.

Taking into consideration these blatant weaknesses in the system of recording and maintaining

payroll function of the company lets, get into specific analysis with respect to the payroll system

of the company to assess the possibility of errors and fraud in the payroll records.

Firstly, let’s have the payroll master file on which the audit is to be conducted. An in-depth

verification of the payroll master file along with information about the number of employees and

other records shall provide a primary assessment about the genuineness of employee and payroll

records (Govindaraj, 2011).

Payroll master file of Hangout Restaurant Company is provided below in the table.

EMP

NO

NAME DEPT JOB HRLY_

RATE

HRS_PE

R_FNT

PAY_PER_

PERIOD

10 Aaron

KWESKIA

A00 CEO 54.95 80.00 4395.83

11 Susan KWESKIA A00 MANAGER 50.00 80.00 4000.00

110 Marie MULLEN A00 Area Manager,

West Coast

43.10 80.00 3447.92

120 Susan

KENWARD

A00 Clerk 25.71 80.00 2056.67

130 Michelle A00 Clerk 25.71 80.00 2056.67

5

AUDITING PRACTICE

GARCIA

140 Roman BHATTI A00 IT ANALYST 29.60 80.00 2368.33

150 Philip

BERNAND

A00 IT ANALYST 29.60 80.00 2368.33

200 Jonathon

HARMAN

B01 KITCHEN

ASSISTANT

16.56 80.00 1325.00

201 John

BREATNACH

B01 MANAGER 39.84 80.00 3187.50

210 Mary Maquire B01 KITCHEN

ASSISTANT

16.56 80.00 1325.00

220 Pter SMYTHE B01 SERVER 19.73 80.00 1578.33

270 Nancy DIXON B01 CHEF 37.97 80.00 3037.50

280 Janelle ADAMS B01 SERVER 19.73 80.00 1578.33

290 Angela EXELBY B01 HEAD

WAITER

29.96 80.00 2396.67

310 Gerard

QUINLAN

C01 MANAGER 39.84 80.00 3187.50

320 Mario MATOGA C01 CHEF 37.97 80.00 3037.50

330 Simone BARTER C01 HEAD 29.96 80.00 2396.67

AUDITING PRACTICE

GARCIA

140 Roman BHATTI A00 IT ANALYST 29.60 80.00 2368.33

150 Philip

BERNAND

A00 IT ANALYST 29.60 80.00 2368.33

200 Jonathon

HARMAN

B01 KITCHEN

ASSISTANT

16.56 80.00 1325.00

201 John

BREATNACH

B01 MANAGER 39.84 80.00 3187.50

210 Mary Maquire B01 KITCHEN

ASSISTANT

16.56 80.00 1325.00

220 Pter SMYTHE B01 SERVER 19.73 80.00 1578.33

270 Nancy DIXON B01 CHEF 37.97 80.00 3037.50

280 Janelle ADAMS B01 SERVER 19.73 80.00 1578.33

290 Angela EXELBY B01 HEAD

WAITER

29.96 80.00 2396.67

310 Gerard

QUINLAN

C01 MANAGER 39.84 80.00 3187.50

320 Mario MATOGA C01 CHEF 37.97 80.00 3037.50

330 Simone BARTER C01 HEAD 29.96 80.00 2396.67

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6

AUDITING PRACTICE

WAITER

340 Kevin CORAM C01 KITCHEN

ASSISTANT

16.56 80.00 1325.00

350 Mitchell

COOPER

C01 KITCHEN

ASSISTANT

16.56 80.00 1325.00

360 Martha BRIGHT C01 SERVER 19.73 80.00 1578.33

370 Narelle PATEL C01 SERVER 19.73 80.00 1578.33

410 Patricia Elder D01 CHEF 37.97 80.00 3037.50

420 Alison BILLING D01 HEAD

WAITER

29.96 80.00 2396.67

430 Norma

DOWNING

D01 KITCHEN

ASSISTANT

16.56 80.00 1325.00

440 Jacob SHAILER D01 KITCHEN

ASSISTANT

16.56 80.00 1325.00

450 Jason MURPHY D01 MANAGER 39.84 80.00 3187.50

460 Alley BEASLEY D01 SERVER 19.73 80.00 1578.33

470 Nicole

CANNING

D01 SERVER 19.73 80.00 1578.33

480 Shelby Smith D01 TRAINEE 6.25 80.00 500.00

AUDITING PRACTICE

WAITER

340 Kevin CORAM C01 KITCHEN

ASSISTANT

16.56 80.00 1325.00

350 Mitchell

COOPER

C01 KITCHEN

ASSISTANT

16.56 80.00 1325.00

360 Martha BRIGHT C01 SERVER 19.73 80.00 1578.33

370 Narelle PATEL C01 SERVER 19.73 80.00 1578.33

410 Patricia Elder D01 CHEF 37.97 80.00 3037.50

420 Alison BILLING D01 HEAD

WAITER

29.96 80.00 2396.67

430 Norma

DOWNING

D01 KITCHEN

ASSISTANT

16.56 80.00 1325.00

440 Jacob SHAILER D01 KITCHEN

ASSISTANT

16.56 80.00 1325.00

450 Jason MURPHY D01 MANAGER 39.84 80.00 3187.50

460 Alley BEASLEY D01 SERVER 19.73 80.00 1578.33

470 Nicole

CANNING

D01 SERVER 19.73 80.00 1578.33

480 Shelby Smith D01 TRAINEE 6.25 80.00 500.00

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7

AUDITING PRACTICE

SERVER

510 Martin MADAN E01 MANAGER 39.84 80.00 3187.50

520 James

MEDNIKOW

E01 SERVER 19.73 80.00 1578.33

530 Pierre MELONI E01 KITCHEN

ASSISTANT

16.56 80.00 1325.00

540 Lynda ROSALES E01 SERVER 19.73 80.00 1578.33

550 Peter

JACOBSON

E01 CHEF 37.97 80.00 3037.50

560 Maureen LAUER E01 HEAD

WAITER

29.96 80.00 2396.67

570 Otto

WOLFSOHN

E01 KITCHEN

ASSISTANT

16.56 80.00 1325.00

2030 Simon BOWEN A00 Area Manager,

East Coast

43.10 80.00 3447.92

Total payment as per employee payroll master file 82354.99

The payroll master file contains seven columns with first column denoting employee number

followed by employee name in the second column. In third and fourth columns name of

department and positions of the employees are given respectively. Hourly rate and number of

AUDITING PRACTICE

SERVER

510 Martin MADAN E01 MANAGER 39.84 80.00 3187.50

520 James

MEDNIKOW

E01 SERVER 19.73 80.00 1578.33

530 Pierre MELONI E01 KITCHEN

ASSISTANT

16.56 80.00 1325.00

540 Lynda ROSALES E01 SERVER 19.73 80.00 1578.33

550 Peter

JACOBSON

E01 CHEF 37.97 80.00 3037.50

560 Maureen LAUER E01 HEAD

WAITER

29.96 80.00 2396.67

570 Otto

WOLFSOHN

E01 KITCHEN

ASSISTANT

16.56 80.00 1325.00

2030 Simon BOWEN A00 Area Manager,

East Coast

43.10 80.00 3447.92

Total payment as per employee payroll master file 82354.99

The payroll master file contains seven columns with first column denoting employee number

followed by employee name in the second column. In third and fourth columns name of

department and positions of the employees are given respectively. Hourly rate and number of

8

AUDITING PRACTICE

hours worked in the fortnight are provided in fifth and sixth columns respectively with seventh

column containing the total pay in the fortnight in respect of each employees of the company. As

per the master payroll file the total amount of salaries due to the employees for the fortnight

ending on 15th September is $82,354.99 as can be seen from the above master file (Liu, Luo and

Yue, 2016).

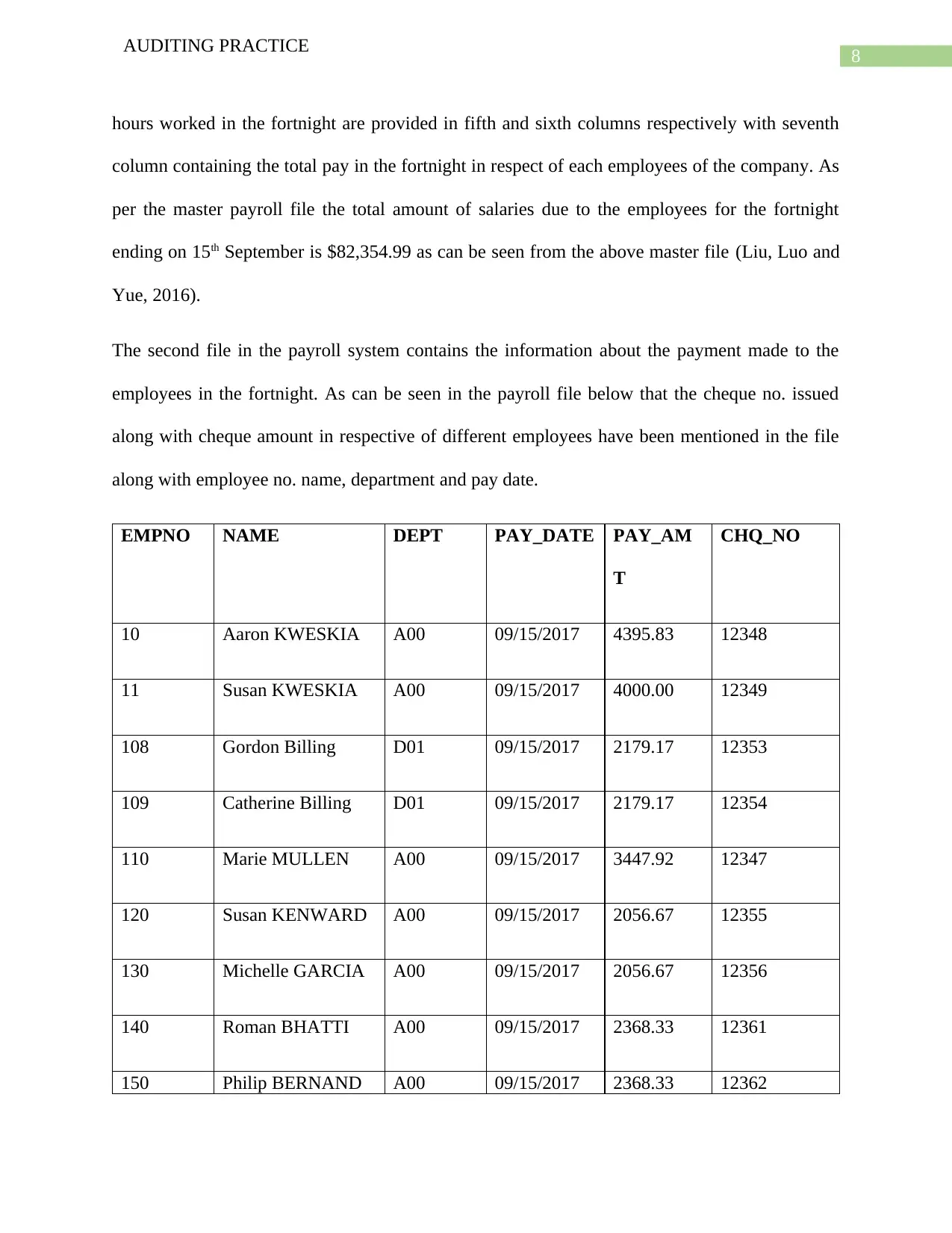

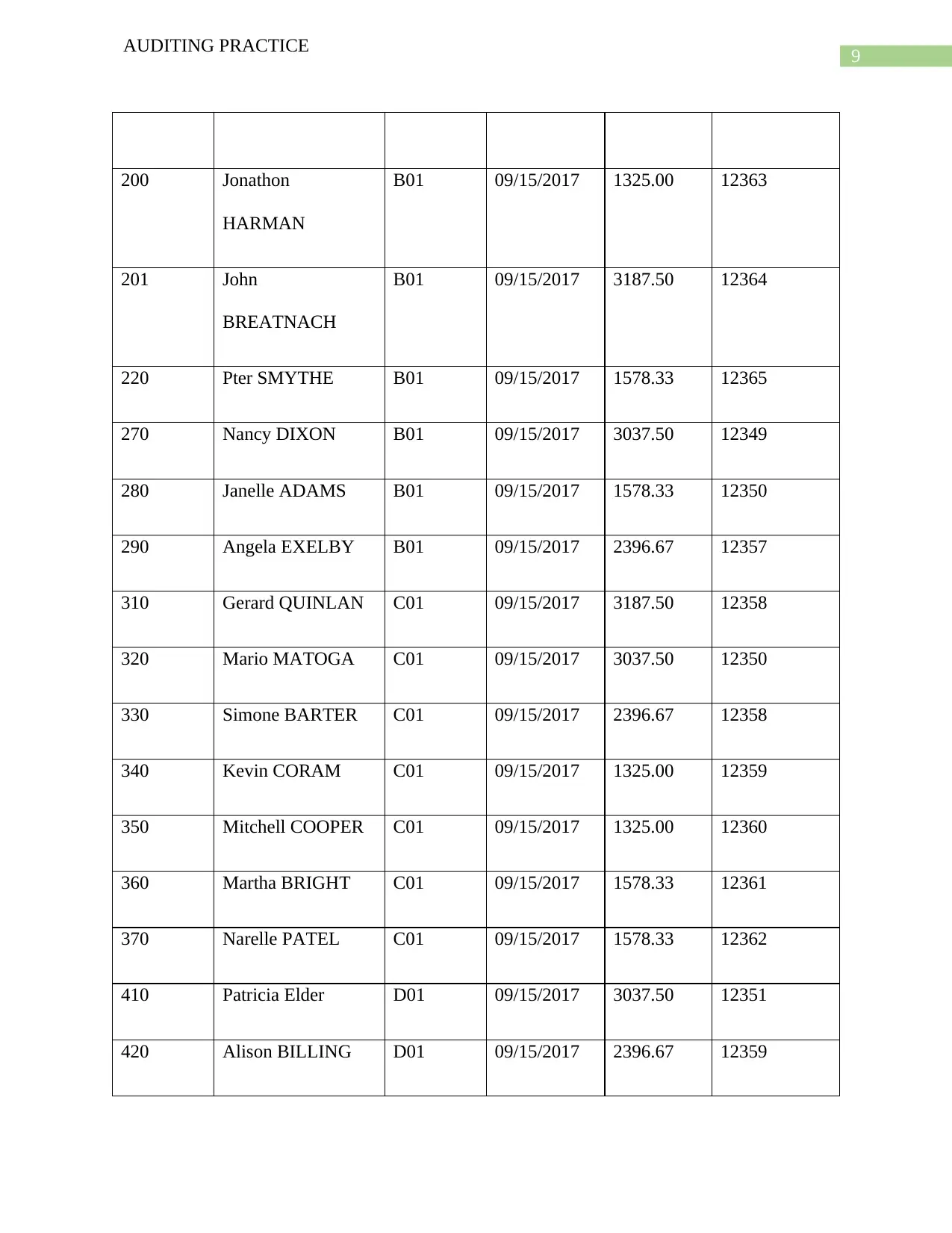

The second file in the payroll system contains the information about the payment made to the

employees in the fortnight. As can be seen in the payroll file below that the cheque no. issued

along with cheque amount in respective of different employees have been mentioned in the file

along with employee no. name, department and pay date.

EMPNO NAME DEPT PAY_DATE PAY_AM

T

CHQ_NO

10 Aaron KWESKIA A00 09/15/2017 4395.83 12348

11 Susan KWESKIA A00 09/15/2017 4000.00 12349

108 Gordon Billing D01 09/15/2017 2179.17 12353

109 Catherine Billing D01 09/15/2017 2179.17 12354

110 Marie MULLEN A00 09/15/2017 3447.92 12347

120 Susan KENWARD A00 09/15/2017 2056.67 12355

130 Michelle GARCIA A00 09/15/2017 2056.67 12356

140 Roman BHATTI A00 09/15/2017 2368.33 12361

150 Philip BERNAND A00 09/15/2017 2368.33 12362

AUDITING PRACTICE

hours worked in the fortnight are provided in fifth and sixth columns respectively with seventh

column containing the total pay in the fortnight in respect of each employees of the company. As

per the master payroll file the total amount of salaries due to the employees for the fortnight

ending on 15th September is $82,354.99 as can be seen from the above master file (Liu, Luo and

Yue, 2016).

The second file in the payroll system contains the information about the payment made to the

employees in the fortnight. As can be seen in the payroll file below that the cheque no. issued

along with cheque amount in respective of different employees have been mentioned in the file

along with employee no. name, department and pay date.

EMPNO NAME DEPT PAY_DATE PAY_AM

T

CHQ_NO

10 Aaron KWESKIA A00 09/15/2017 4395.83 12348

11 Susan KWESKIA A00 09/15/2017 4000.00 12349

108 Gordon Billing D01 09/15/2017 2179.17 12353

109 Catherine Billing D01 09/15/2017 2179.17 12354

110 Marie MULLEN A00 09/15/2017 3447.92 12347

120 Susan KENWARD A00 09/15/2017 2056.67 12355

130 Michelle GARCIA A00 09/15/2017 2056.67 12356

140 Roman BHATTI A00 09/15/2017 2368.33 12361

150 Philip BERNAND A00 09/15/2017 2368.33 12362

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9

AUDITING PRACTICE

200 Jonathon

HARMAN

B01 09/15/2017 1325.00 12363

201 John

BREATNACH

B01 09/15/2017 3187.50 12364

220 Pter SMYTHE B01 09/15/2017 1578.33 12365

270 Nancy DIXON B01 09/15/2017 3037.50 12349

280 Janelle ADAMS B01 09/15/2017 1578.33 12350

290 Angela EXELBY B01 09/15/2017 2396.67 12357

310 Gerard QUINLAN C01 09/15/2017 3187.50 12358

320 Mario MATOGA C01 09/15/2017 3037.50 12350

330 Simone BARTER C01 09/15/2017 2396.67 12358

340 Kevin CORAM C01 09/15/2017 1325.00 12359

350 Mitchell COOPER C01 09/15/2017 1325.00 12360

360 Martha BRIGHT C01 09/15/2017 1578.33 12361

370 Narelle PATEL C01 09/15/2017 1578.33 12362

410 Patricia Elder D01 09/15/2017 3037.50 12351

420 Alison BILLING D01 09/15/2017 2396.67 12359

AUDITING PRACTICE

200 Jonathon

HARMAN

B01 09/15/2017 1325.00 12363

201 John

BREATNACH

B01 09/15/2017 3187.50 12364

220 Pter SMYTHE B01 09/15/2017 1578.33 12365

270 Nancy DIXON B01 09/15/2017 3037.50 12349

280 Janelle ADAMS B01 09/15/2017 1578.33 12350

290 Angela EXELBY B01 09/15/2017 2396.67 12357

310 Gerard QUINLAN C01 09/15/2017 3187.50 12358

320 Mario MATOGA C01 09/15/2017 3037.50 12350

330 Simone BARTER C01 09/15/2017 2396.67 12358

340 Kevin CORAM C01 09/15/2017 1325.00 12359

350 Mitchell COOPER C01 09/15/2017 1325.00 12360

360 Martha BRIGHT C01 09/15/2017 1578.33 12361

370 Narelle PATEL C01 09/15/2017 1578.33 12362

410 Patricia Elder D01 09/15/2017 3037.50 12351

420 Alison BILLING D01 09/15/2017 2396.67 12359

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10

AUDITING PRACTICE

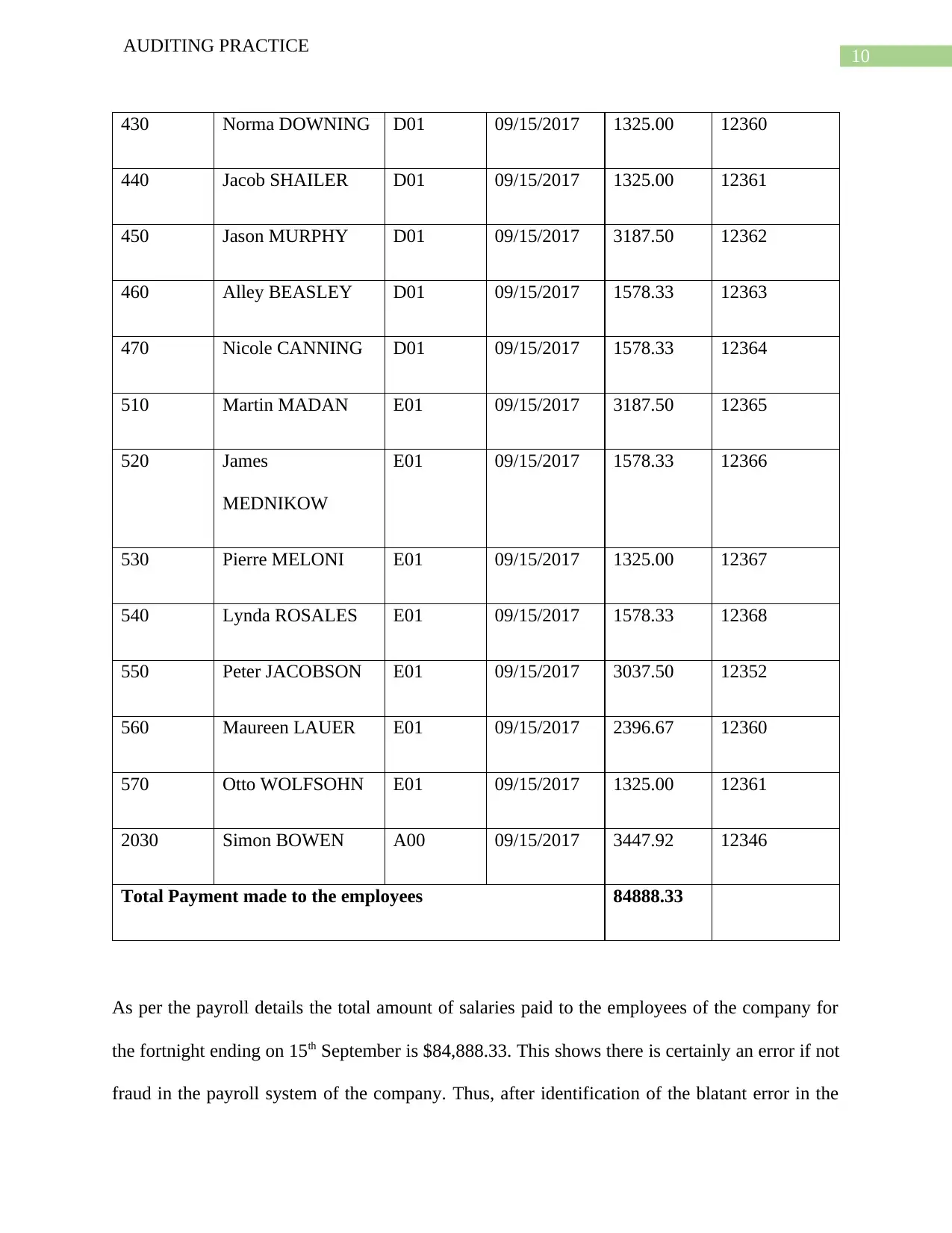

430 Norma DOWNING D01 09/15/2017 1325.00 12360

440 Jacob SHAILER D01 09/15/2017 1325.00 12361

450 Jason MURPHY D01 09/15/2017 3187.50 12362

460 Alley BEASLEY D01 09/15/2017 1578.33 12363

470 Nicole CANNING D01 09/15/2017 1578.33 12364

510 Martin MADAN E01 09/15/2017 3187.50 12365

520 James

MEDNIKOW

E01 09/15/2017 1578.33 12366

530 Pierre MELONI E01 09/15/2017 1325.00 12367

540 Lynda ROSALES E01 09/15/2017 1578.33 12368

550 Peter JACOBSON E01 09/15/2017 3037.50 12352

560 Maureen LAUER E01 09/15/2017 2396.67 12360

570 Otto WOLFSOHN E01 09/15/2017 1325.00 12361

2030 Simon BOWEN A00 09/15/2017 3447.92 12346

Total Payment made to the employees 84888.33

As per the payroll details the total amount of salaries paid to the employees of the company for

the fortnight ending on 15th September is $84,888.33. This shows there is certainly an error if not

fraud in the payroll system of the company. Thus, after identification of the blatant error in the

AUDITING PRACTICE

430 Norma DOWNING D01 09/15/2017 1325.00 12360

440 Jacob SHAILER D01 09/15/2017 1325.00 12361

450 Jason MURPHY D01 09/15/2017 3187.50 12362

460 Alley BEASLEY D01 09/15/2017 1578.33 12363

470 Nicole CANNING D01 09/15/2017 1578.33 12364

510 Martin MADAN E01 09/15/2017 3187.50 12365

520 James

MEDNIKOW

E01 09/15/2017 1578.33 12366

530 Pierre MELONI E01 09/15/2017 1325.00 12367

540 Lynda ROSALES E01 09/15/2017 1578.33 12368

550 Peter JACOBSON E01 09/15/2017 3037.50 12352

560 Maureen LAUER E01 09/15/2017 2396.67 12360

570 Otto WOLFSOHN E01 09/15/2017 1325.00 12361

2030 Simon BOWEN A00 09/15/2017 3447.92 12346

Total Payment made to the employees 84888.33

As per the payroll details the total amount of salaries paid to the employees of the company for

the fortnight ending on 15th September is $84,888.33. This shows there is certainly an error if not

fraud in the payroll system of the company. Thus, after identification of the blatant error in the

11

AUDITING PRACTICE

payroll records of the company it is essential to conduct necessary audit procedures such as

substantive and analytic procedures to identify the reason for such mismatch between amounts

due to the employees in the fortnight as per master payroll record and the actual amount paid to

the employees as per payroll (Marsh, 2011).

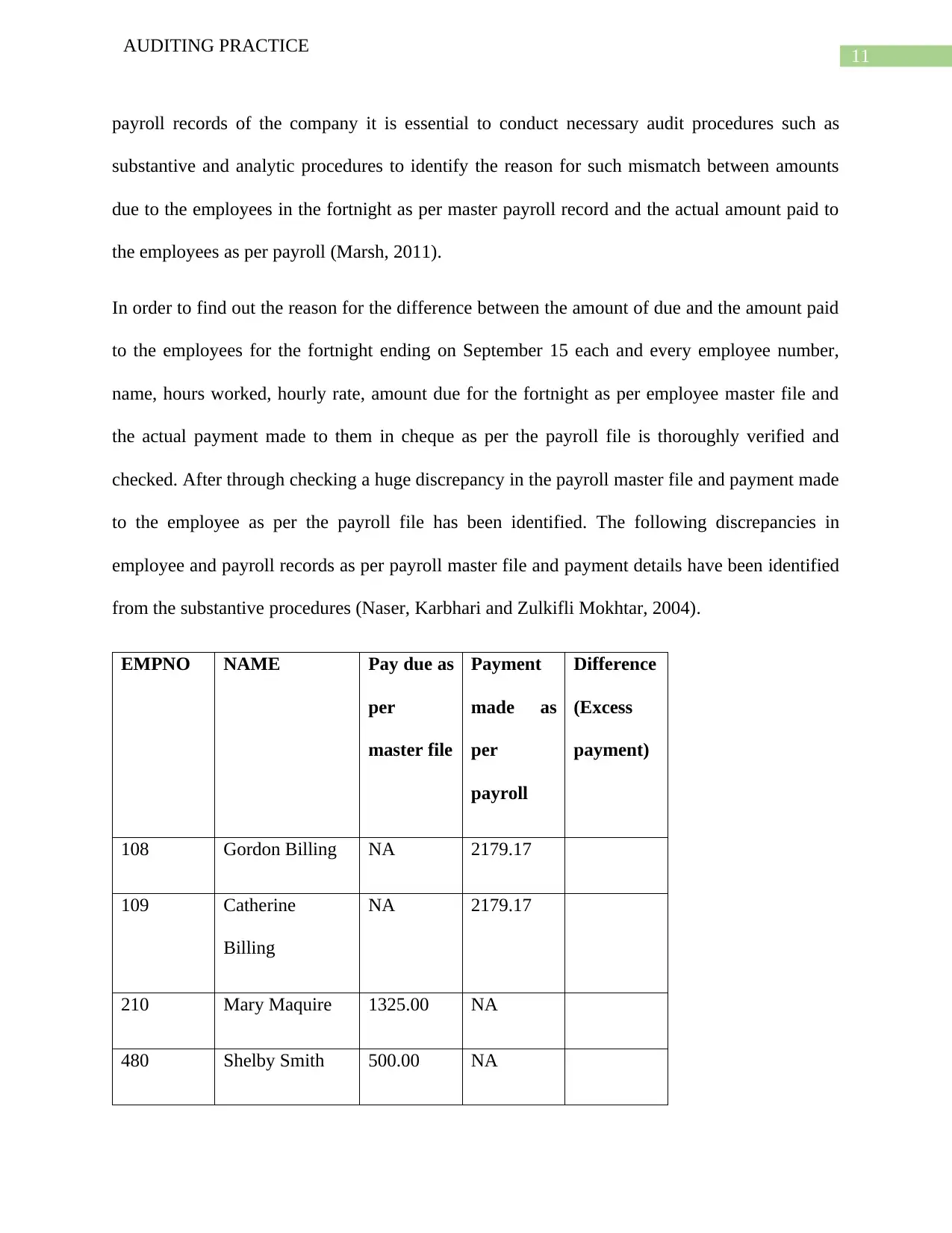

In order to find out the reason for the difference between the amount of due and the amount paid

to the employees for the fortnight ending on September 15 each and every employee number,

name, hours worked, hourly rate, amount due for the fortnight as per employee master file and

the actual payment made to them in cheque as per the payroll file is thoroughly verified and

checked. After through checking a huge discrepancy in the payroll master file and payment made

to the employee as per the payroll file has been identified. The following discrepancies in

employee and payroll records as per payroll master file and payment details have been identified

from the substantive procedures (Naser, Karbhari and Zulkifli Mokhtar, 2004).

EMPNO NAME Pay due as

per

master file

Payment

made as

per

payroll

Difference

(Excess

payment)

108 Gordon Billing NA 2179.17

109 Catherine

Billing

NA 2179.17

210 Mary Maquire 1325.00 NA

480 Shelby Smith 500.00 NA

AUDITING PRACTICE

payroll records of the company it is essential to conduct necessary audit procedures such as

substantive and analytic procedures to identify the reason for such mismatch between amounts

due to the employees in the fortnight as per master payroll record and the actual amount paid to

the employees as per payroll (Marsh, 2011).

In order to find out the reason for the difference between the amount of due and the amount paid

to the employees for the fortnight ending on September 15 each and every employee number,

name, hours worked, hourly rate, amount due for the fortnight as per employee master file and

the actual payment made to them in cheque as per the payroll file is thoroughly verified and

checked. After through checking a huge discrepancy in the payroll master file and payment made

to the employee as per the payroll file has been identified. The following discrepancies in

employee and payroll records as per payroll master file and payment details have been identified

from the substantive procedures (Naser, Karbhari and Zulkifli Mokhtar, 2004).

EMPNO NAME Pay due as

per

master file

Payment

made as

per

payroll

Difference

(Excess

payment)

108 Gordon Billing NA 2179.17

109 Catherine

Billing

NA 2179.17

210 Mary Maquire 1325.00 NA

480 Shelby Smith 500.00 NA

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 18

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.