Auditing Cadmium Enterprise: Financial Statement Analysis and Findings

VerifiedAdded on 2023/06/06

|16

|2597

|408

Report

AI Summary

This report delves into the auditing functions performed on Cadmium Enterprise, a proprietorship firm, examining various aspects of auditing within a business environment. The primary focus is identifying material misstatements through the analysis of the company's trial balance, employing tr...

Issues in Auditing Practice

1

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Executive summary

This report is concerned with the auditing functions performed on Cadmium Enterprise which

is a proprietorship firm. Various aspects of auditing in business environment are discussed in

this report. Main purpose of this report is to identify Material misstatements by analysing trial

balance of the company. Auditing technique of trend analysis will be used on income

statement to determine material misstatement that could arise during the process of auditing.

In addition to that concept of materiality for financial report is also discussed in this report.

There are two main conclusion that can be evaluated from this management report. Firstly,

net profitability of the company is effective and has improved in current financial year.

Secondly, there is a requirement of proper repair and maintenance procedure to cut down

direct expenditures.

2

This report is concerned with the auditing functions performed on Cadmium Enterprise which

is a proprietorship firm. Various aspects of auditing in business environment are discussed in

this report. Main purpose of this report is to identify Material misstatements by analysing trial

balance of the company. Auditing technique of trend analysis will be used on income

statement to determine material misstatement that could arise during the process of auditing.

In addition to that concept of materiality for financial report is also discussed in this report.

There are two main conclusion that can be evaluated from this management report. Firstly,

net profitability of the company is effective and has improved in current financial year.

Secondly, there is a requirement of proper repair and maintenance procedure to cut down

direct expenditures.

2

Contents

Executive summary....................................................................................................................2

Introduction................................................................................................................................4

Materiality in financial statements.............................................................................................5

Analytical review.......................................................................................................................6

Trend analysis............................................................................................................................7

Audit procedure..........................................................................................................................8

Fraud risk...................................................................................................................................9

Conclusion................................................................................................................................10

References................................................................................................................................11

Appendix..................................................................................................................................12

3

Executive summary....................................................................................................................2

Introduction................................................................................................................................4

Materiality in financial statements.............................................................................................5

Analytical review.......................................................................................................................6

Trend analysis............................................................................................................................7

Audit procedure..........................................................................................................................8

Fraud risk...................................................................................................................................9

Conclusion................................................................................................................................10

References................................................................................................................................11

Appendix..................................................................................................................................12

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Introduction

The function of auditing has various advantages for internal as well as external stakeholders

of a company. Main objective of an auditor is to identify material misstatements, frauds and

errors in financial statements of a particular company. It is not possible for every

shareholders to examine the financial statements of the company as they might not have

sufficient knowledge to examine and analyse financial statements (Louwers et.al, 2015). This

is the reason that shareholders and management of the company appoints auditor for

examination of financial statements and give their Independent and objective views on

financial position of the company. Important that an auditor implement due diligence and

avoid gross negligence while conducting his or her roles and responsibilities as an auditor

(Cohen and Simnett, 2014). We have prepared this report for Cadmium Enterprises which is

an individual organisation. Audit is required to be conducted and specific points are to be

discussed in this report with respect to trial balance given energy scenario. As an auditor we

have also discussed the fraud risk and material misstatements in the trail balance of the

company. Possible areas of material risk are account receivable, inventory, repair and

Maintenance and sales. We should include these factors in key auditor matters statement

which will be then discussed with those charged with governance.

4

The function of auditing has various advantages for internal as well as external stakeholders

of a company. Main objective of an auditor is to identify material misstatements, frauds and

errors in financial statements of a particular company. It is not possible for every

shareholders to examine the financial statements of the company as they might not have

sufficient knowledge to examine and analyse financial statements (Louwers et.al, 2015). This

is the reason that shareholders and management of the company appoints auditor for

examination of financial statements and give their Independent and objective views on

financial position of the company. Important that an auditor implement due diligence and

avoid gross negligence while conducting his or her roles and responsibilities as an auditor

(Cohen and Simnett, 2014). We have prepared this report for Cadmium Enterprises which is

an individual organisation. Audit is required to be conducted and specific points are to be

discussed in this report with respect to trial balance given energy scenario. As an auditor we

have also discussed the fraud risk and material misstatements in the trail balance of the

company. Possible areas of material risk are account receivable, inventory, repair and

Maintenance and sales. We should include these factors in key auditor matters statement

which will be then discussed with those charged with governance.

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Materiality in financial statements

Materiality for financial report can be defined as the level of risk that is acceptable by the

auditor of the organisation represented in financial terms. Calculation of material it is totally

dependent upon the skill and experience of the auditor working on an organisation. For

example, a particular auditor that is working in the organisation for past 3 years is expected to

calculate more accurate materiality as compared to auditor that is just started conducting

audit of the company. There are specific calculations that are required in determination of

materiality of particular financial statement. Following are some of the commonly acceptable

formulas for calculation of materiality-

1. 5% of total net profit from primary business

2. 5% of net profit distributable to equity shareholders

3. .5% to 2% of total revenue earned by whole Organisation in a financial year

4. 2 to 5% of total shareholder's equity (Lakis, V. and Masiulevičius, 2017).

One of the audit partner engaged in auditing of Cadmium Enterprise has suggested that

materiality of $15000 should be set before starting the process of auditing. Setting materiality

at the starting of the audit is totally out page from the judgement of auditor that is conducting

such audit but there are some commonly acceptable criteria for calculation that should be

considered by auditors before setting this limit. According to commonly acceptable

calculations following Maternity should be calculated-

1. 5% of total profit= (5%* 90122)= $ 4506.1

At the end of the financial year total profit earned by the company is $90122. Calculation of

the properties represent in appendix at the end of the report.

2. 2% of total revenue for the last year= 187450* 2%= $3749 (Choudhary, Merkley and

Schipper. 2018)

It can be said that estimation on part of audit partner is not as per the normal acceptable

market practices. Therefore it can be said that this estimation can affect audit process used by

audit team. Change in preliminary estimation on part of the auditor will definitely affect the

overall audit budget prepared by the auditor. If the risk of material misstatement is not

5

Materiality for financial report can be defined as the level of risk that is acceptable by the

auditor of the organisation represented in financial terms. Calculation of material it is totally

dependent upon the skill and experience of the auditor working on an organisation. For

example, a particular auditor that is working in the organisation for past 3 years is expected to

calculate more accurate materiality as compared to auditor that is just started conducting

audit of the company. There are specific calculations that are required in determination of

materiality of particular financial statement. Following are some of the commonly acceptable

formulas for calculation of materiality-

1. 5% of total net profit from primary business

2. 5% of net profit distributable to equity shareholders

3. .5% to 2% of total revenue earned by whole Organisation in a financial year

4. 2 to 5% of total shareholder's equity (Lakis, V. and Masiulevičius, 2017).

One of the audit partner engaged in auditing of Cadmium Enterprise has suggested that

materiality of $15000 should be set before starting the process of auditing. Setting materiality

at the starting of the audit is totally out page from the judgement of auditor that is conducting

such audit but there are some commonly acceptable criteria for calculation that should be

considered by auditors before setting this limit. According to commonly acceptable

calculations following Maternity should be calculated-

1. 5% of total profit= (5%* 90122)= $ 4506.1

At the end of the financial year total profit earned by the company is $90122. Calculation of

the properties represent in appendix at the end of the report.

2. 2% of total revenue for the last year= 187450* 2%= $3749 (Choudhary, Merkley and

Schipper. 2018)

It can be said that estimation on part of audit partner is not as per the normal acceptable

market practices. Therefore it can be said that this estimation can affect audit process used by

audit team. Change in preliminary estimation on part of the auditor will definitely affect the

overall audit budget prepared by the auditor. If the risk of material misstatement is not

5

appropriately estimated by the management then there are chances that audit has to introduce

additional audit staff in the audit process will increase overall budget of the audit firm.

6

additional audit staff in the audit process will increase overall budget of the audit firm.

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

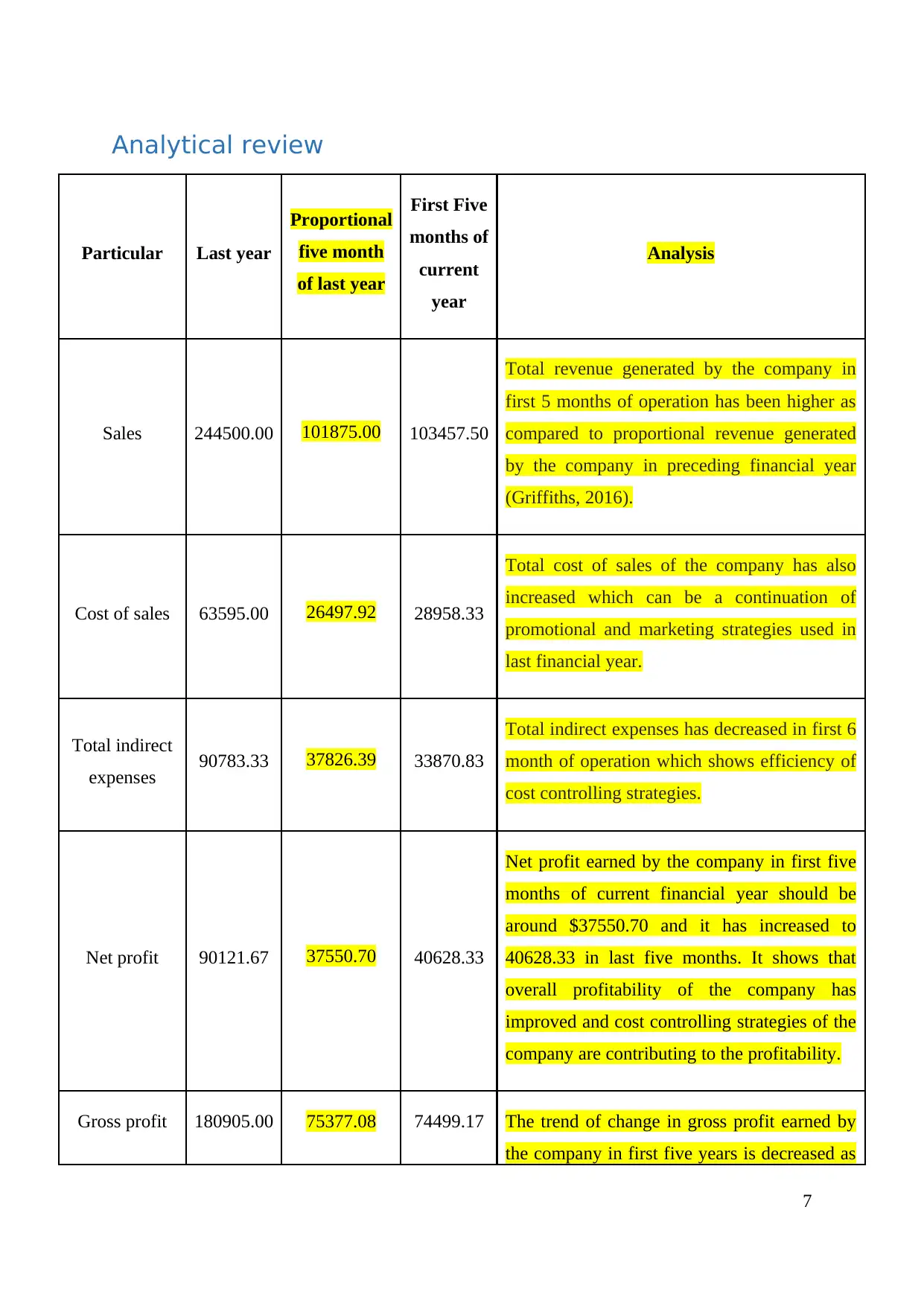

Analytical review

Particular Last year

Proportional

five month

of last year

First Five

months of

current

year

Analysis

Sales 244500.00 101875.00 103457.50

Total revenue generated by the company in

first 5 months of operation has been higher as

compared to proportional revenue generated

by the company in preceding financial year

(Griffiths, 2016).

Cost of sales 63595.00 26497.92 28958.33

Total cost of sales of the company has also

increased which can be a continuation of

promotional and marketing strategies used in

last financial year.

Total indirect

expenses 90783.33 37826.39 33870.83

Total indirect expenses has decreased in first 6

month of operation which shows efficiency of

cost controlling strategies.

Net profit 90121.67 37550.70 40628.33

Net profit earned by the company in first five

months of current financial year should be

around $37550.70 and it has increased to

40628.33 in last five months. It shows that

overall profitability of the company has

improved and cost controlling strategies of the

company are contributing to the profitability.

Gross profit 180905.00 75377.08 74499.17 The trend of change in gross profit earned by

the company in first five years is decreased as

7

Particular Last year

Proportional

five month

of last year

First Five

months of

current

year

Analysis

Sales 244500.00 101875.00 103457.50

Total revenue generated by the company in

first 5 months of operation has been higher as

compared to proportional revenue generated

by the company in preceding financial year

(Griffiths, 2016).

Cost of sales 63595.00 26497.92 28958.33

Total cost of sales of the company has also

increased which can be a continuation of

promotional and marketing strategies used in

last financial year.

Total indirect

expenses 90783.33 37826.39 33870.83

Total indirect expenses has decreased in first 6

month of operation which shows efficiency of

cost controlling strategies.

Net profit 90121.67 37550.70 40628.33

Net profit earned by the company in first five

months of current financial year should be

around $37550.70 and it has increased to

40628.33 in last five months. It shows that

overall profitability of the company has

improved and cost controlling strategies of the

company are contributing to the profitability.

Gross profit 180905.00 75377.08 74499.17 The trend of change in gross profit earned by

the company in first five years is decreased as

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

compared to last year’s proportional five

months. This decrease shows that direct

expenditures are very high as gross profit is

decreasing irrespective of the decrease in net

profit.

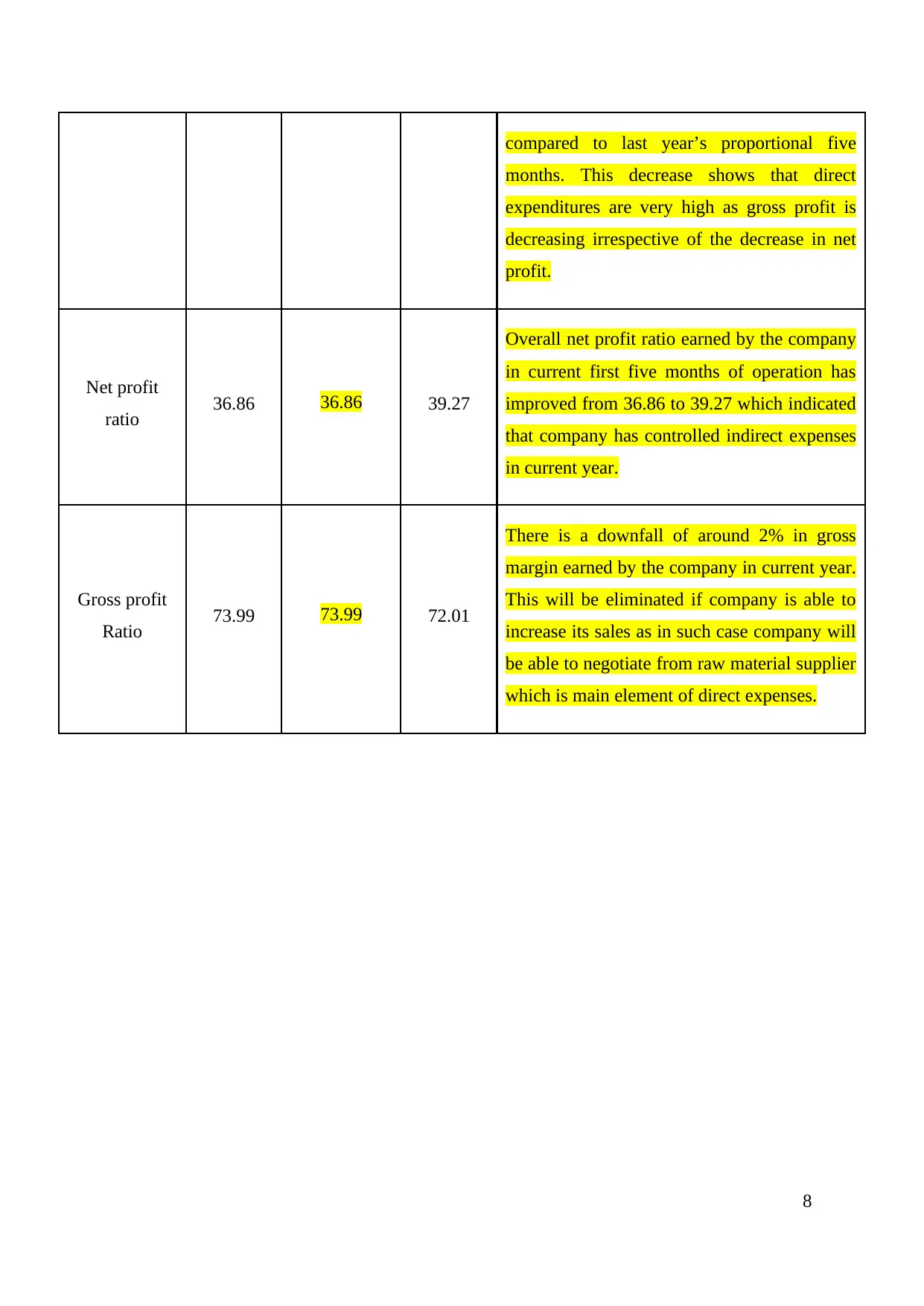

Net profit

ratio 36.86 36.86 39.27

Overall net profit ratio earned by the company

in current first five months of operation has

improved from 36.86 to 39.27 which indicated

that company has controlled indirect expenses

in current year.

Gross profit

Ratio 73.99 73.99 72.01

There is a downfall of around 2% in gross

margin earned by the company in current year.

This will be eliminated if company is able to

increase its sales as in such case company will

be able to negotiate from raw material supplier

which is main element of direct expenses.

8

months. This decrease shows that direct

expenditures are very high as gross profit is

decreasing irrespective of the decrease in net

profit.

Net profit

ratio 36.86 36.86 39.27

Overall net profit ratio earned by the company

in current first five months of operation has

improved from 36.86 to 39.27 which indicated

that company has controlled indirect expenses

in current year.

Gross profit

Ratio 73.99 73.99 72.01

There is a downfall of around 2% in gross

margin earned by the company in current year.

This will be eliminated if company is able to

increase its sales as in such case company will

be able to negotiate from raw material supplier

which is main element of direct expenses.

8

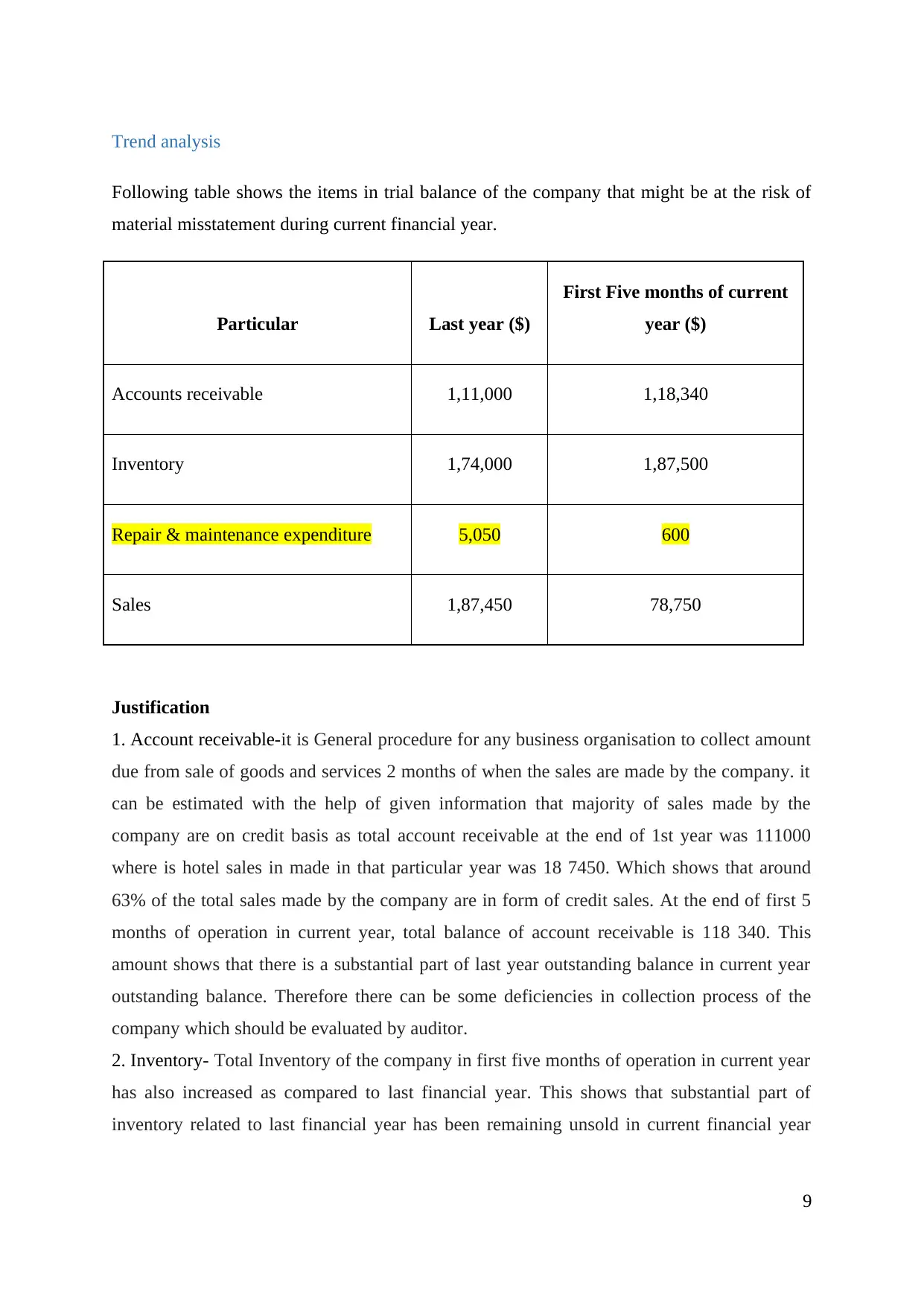

Trend analysis

Following table shows the items in trial balance of the company that might be at the risk of

material misstatement during current financial year.

Particular Last year ($)

First Five months of current

year ($)

Accounts receivable 1,11,000 1,18,340

Inventory 1,74,000 1,87,500

Repair & maintenance expenditure 5,050 600

Sales 1,87,450 78,750

Justification

1. Account receivable-it is General procedure for any business organisation to collect amount

due from sale of goods and services 2 months of when the sales are made by the company. it

can be estimated with the help of given information that majority of sales made by the

company are on credit basis as total account receivable at the end of 1st year was 111000

where is hotel sales in made in that particular year was 18 7450. Which shows that around

63% of the total sales made by the company are in form of credit sales. At the end of first 5

months of operation in current year, total balance of account receivable is 118 340. This

amount shows that there is a substantial part of last year outstanding balance in current year

outstanding balance. Therefore there can be some deficiencies in collection process of the

company which should be evaluated by auditor.

2. Inventory- Total Inventory of the company in first five months of operation in current year

has also increased as compared to last financial year. This shows that substantial part of

inventory related to last financial year has been remaining unsold in current financial year

9

Following table shows the items in trial balance of the company that might be at the risk of

material misstatement during current financial year.

Particular Last year ($)

First Five months of current

year ($)

Accounts receivable 1,11,000 1,18,340

Inventory 1,74,000 1,87,500

Repair & maintenance expenditure 5,050 600

Sales 1,87,450 78,750

Justification

1. Account receivable-it is General procedure for any business organisation to collect amount

due from sale of goods and services 2 months of when the sales are made by the company. it

can be estimated with the help of given information that majority of sales made by the

company are on credit basis as total account receivable at the end of 1st year was 111000

where is hotel sales in made in that particular year was 18 7450. Which shows that around

63% of the total sales made by the company are in form of credit sales. At the end of first 5

months of operation in current year, total balance of account receivable is 118 340. This

amount shows that there is a substantial part of last year outstanding balance in current year

outstanding balance. Therefore there can be some deficiencies in collection process of the

company which should be evaluated by auditor.

2. Inventory- Total Inventory of the company in first five months of operation in current year

has also increased as compared to last financial year. This shows that substantial part of

inventory related to last financial year has been remaining unsold in current financial year

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

(Contessotto, C. and Moroney¸2014). It can be a result of deficiency in inventory

management all the company.

3. Repair and maintenance- total repair and maintenance expenditure conducted by the

company are substantially lower as compared to last financial year as it has decreased form

$5050 in last years to just $600 in first five months of operation. In the analytical review of

financial items in trial balance it was also evaluated that total direct expenditure has also

increased in current 5 months. Repairs to machinery and increase in direct expenditure can be

directly related to each other in this scenario. Every machinery involved in the production

process required regular repair and maintenance as it can decrease efficiency of machine

which will ultimately increase direct cost of production.

4. Sales- It can be evaluated that proportional things of the company for 5 months as decrease

the as compared to last financial year but management of the company has purchased new

machinery worth $6000 in current financial year. Generally, increasing capacity of the

company also increasing the sales of the company as main purpose of acquisition of new

machinery is to boost up the sale. Quality of machinery purchased by the company should be

evaluated (Graham, Bedard and Dutta, 2018).

10

management all the company.

3. Repair and maintenance- total repair and maintenance expenditure conducted by the

company are substantially lower as compared to last financial year as it has decreased form

$5050 in last years to just $600 in first five months of operation. In the analytical review of

financial items in trial balance it was also evaluated that total direct expenditure has also

increased in current 5 months. Repairs to machinery and increase in direct expenditure can be

directly related to each other in this scenario. Every machinery involved in the production

process required regular repair and maintenance as it can decrease efficiency of machine

which will ultimately increase direct cost of production.

4. Sales- It can be evaluated that proportional things of the company for 5 months as decrease

the as compared to last financial year but management of the company has purchased new

machinery worth $6000 in current financial year. Generally, increasing capacity of the

company also increasing the sales of the company as main purpose of acquisition of new

machinery is to boost up the sale. Quality of machinery purchased by the company should be

evaluated (Graham, Bedard and Dutta, 2018).

10

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Audit procedure

Account receivable

Auditor of the company should evaluate collection procedure of the company from account

receivables. This can be done by auditor with the help of discussion with management or

person in charge of account receivable (Chan and Vasarhelyi, 2018). External confirmation

can also be obtained by management to verify that all the account received by the

management has been recorded in books of accounts.

Inventory

First of all auditor of the company should conduct physical verification of the elementary

available with the management. Auditor of the company should evaluate process used by

management to value their stocks and weather such policies are as per industry policies or

not. In addition to that it should also be evaluated that person that is conducting physical

review of inventory is not in in charge of recording inventory in financial statements

(Makarenko and Yardanova, 2015).

Repair and maintenance

Auditor shows conduct whether management of the company has prepared policies and

procedure for maintenance of plant and machinery. In addition to that, auditor should check if

these plans are properly followed by the management. All the repair and maintained should

be scheduled in accordance with the repair and maintenance guidelines provided by the

management.

Sales

Auditor should evaluate what are the main reasons that have resulted in downfall of sales in

current financial year and reason that acquisition of new machinery has not resulted in

increase of sales. Auditor today also finds out the current market value of the machinery and

other such machinery is efficient with the business processes conducted by the company.

11

Account receivable

Auditor of the company should evaluate collection procedure of the company from account

receivables. This can be done by auditor with the help of discussion with management or

person in charge of account receivable (Chan and Vasarhelyi, 2018). External confirmation

can also be obtained by management to verify that all the account received by the

management has been recorded in books of accounts.

Inventory

First of all auditor of the company should conduct physical verification of the elementary

available with the management. Auditor of the company should evaluate process used by

management to value their stocks and weather such policies are as per industry policies or

not. In addition to that it should also be evaluated that person that is conducting physical

review of inventory is not in in charge of recording inventory in financial statements

(Makarenko and Yardanova, 2015).

Repair and maintenance

Auditor shows conduct whether management of the company has prepared policies and

procedure for maintenance of plant and machinery. In addition to that, auditor should check if

these plans are properly followed by the management. All the repair and maintained should

be scheduled in accordance with the repair and maintenance guidelines provided by the

management.

Sales

Auditor should evaluate what are the main reasons that have resulted in downfall of sales in

current financial year and reason that acquisition of new machinery has not resulted in

increase of sales. Auditor today also finds out the current market value of the machinery and

other such machinery is efficient with the business processes conducted by the company.

11

Fraud risk

Main objective of an auditor is so identify material misstatements and fraud conducted by

management of organisation for any other employees working in the organisation. Audit

suggestion given by audit partner that there is no fraud risk in the company just because

management of the company seems trustworthy is not appropriate. Every conclusion made by

the auditor should have substantial amount of supporting evidence. Evaluation of fraud is one

of the most primary responsibilities of the company and any conclusion made on such behalf

should be supported by proper audit evidence (Knechel and Salterio, 2016). Therefore in this

case also auditing to conduct proper audit procedures to identify the level of fraud risk in the

organisation. From an overall analysis of trial balance of the company, it can be said that risk

of fraud in the business organisation is very low.

12

Main objective of an auditor is so identify material misstatements and fraud conducted by

management of organisation for any other employees working in the organisation. Audit

suggestion given by audit partner that there is no fraud risk in the company just because

management of the company seems trustworthy is not appropriate. Every conclusion made by

the auditor should have substantial amount of supporting evidence. Evaluation of fraud is one

of the most primary responsibilities of the company and any conclusion made on such behalf

should be supported by proper audit evidence (Knechel and Salterio, 2016). Therefore in this

case also auditing to conduct proper audit procedures to identify the level of fraud risk in the

organisation. From an overall analysis of trial balance of the company, it can be said that risk

of fraud in the business organisation is very low.

12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Conclusion

It can be concluded that role of Auditor in inspection of books of accounts of the company is

very substantial and all the audit procedures should be conducted in order to identify any

material misstatement, error and fraud. In this case, materiality of financial statement

determined by the audit partner is very high and it should be corrected. In addition to that this

report has implemented various factors that should be considered by auditor during the

process of audit.

13

It can be concluded that role of Auditor in inspection of books of accounts of the company is

very substantial and all the audit procedures should be conducted in order to identify any

material misstatement, error and fraud. In this case, materiality of financial statement

determined by the audit partner is very high and it should be corrected. In addition to that this

report has implemented various factors that should be considered by auditor during the

process of audit.

13

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

References

Chan, D.Y. and Vasarhelyi, M.A., 2018. Innovation and practice of continuous auditing.

In Continuous Auditing: Theory and Application (pp. 271-283). Emerald Publishing Limited.

Choudhary, P., Merkley, K.J. and Schipper, K., 2018. Auditors’ Quantitative Materiality

Judgments: Properties and Implications for Financial Reporting Reliability.

Cohen, J.R. and Simnett, R., 2014. CSR and assurance services: A research agenda. Auditing:

A Journal of Practice & Theory, 34(1), pp.59-74.

Contessotto, C. and Moroney, R., 2014. The association between audit committee

effectiveness and audit risk. Accounting & Finance, 54(2), pp.393-418.

Graham, L., Bedard, J.C. and Dutta, S., 2018. Managing group audit risk in a

multicomponent audit setting. International Journal of Auditing, 22(1), pp.40-54.

Griffiths, P., 2016. Risk-based auditing. Routledge.

Knechel, W.R. and Salterio, S.E., 2016. Auditing: Assurance and risk. Routledge.

Lakis, V. and Masiulevičius, A., 2017. Acceptable audit materiality for users of financial

statements. Journal of Management, 2(31).

Louwers, T.J., Ramsay, R.J., Sinason, D.H., Strawser, J.R. and Thibodeau, J.C.,

2015. Auditing & assurance services. McGraw-Hill Education.

Makarenko, A.P. and Yardanova, T.H., 2015. Development of a program of inventory

audit. Naukovi pratsi Poltavskoyi derzhavnoyi ahrarnoyi akademiyi, 2(11), pp.40-48.

14

Chan, D.Y. and Vasarhelyi, M.A., 2018. Innovation and practice of continuous auditing.

In Continuous Auditing: Theory and Application (pp. 271-283). Emerald Publishing Limited.

Choudhary, P., Merkley, K.J. and Schipper, K., 2018. Auditors’ Quantitative Materiality

Judgments: Properties and Implications for Financial Reporting Reliability.

Cohen, J.R. and Simnett, R., 2014. CSR and assurance services: A research agenda. Auditing:

A Journal of Practice & Theory, 34(1), pp.59-74.

Contessotto, C. and Moroney, R., 2014. The association between audit committee

effectiveness and audit risk. Accounting & Finance, 54(2), pp.393-418.

Graham, L., Bedard, J.C. and Dutta, S., 2018. Managing group audit risk in a

multicomponent audit setting. International Journal of Auditing, 22(1), pp.40-54.

Griffiths, P., 2016. Risk-based auditing. Routledge.

Knechel, W.R. and Salterio, S.E., 2016. Auditing: Assurance and risk. Routledge.

Lakis, V. and Masiulevičius, A., 2017. Acceptable audit materiality for users of financial

statements. Journal of Management, 2(31).

Louwers, T.J., Ramsay, R.J., Sinason, D.H., Strawser, J.R. and Thibodeau, J.C.,

2015. Auditing & assurance services. McGraw-Hill Education.

Makarenko, A.P. and Yardanova, T.H., 2015. Development of a program of inventory

audit. Naukovi pratsi Poltavskoyi derzhavnoyi ahrarnoyi akademiyi, 2(11), pp.40-48.

14

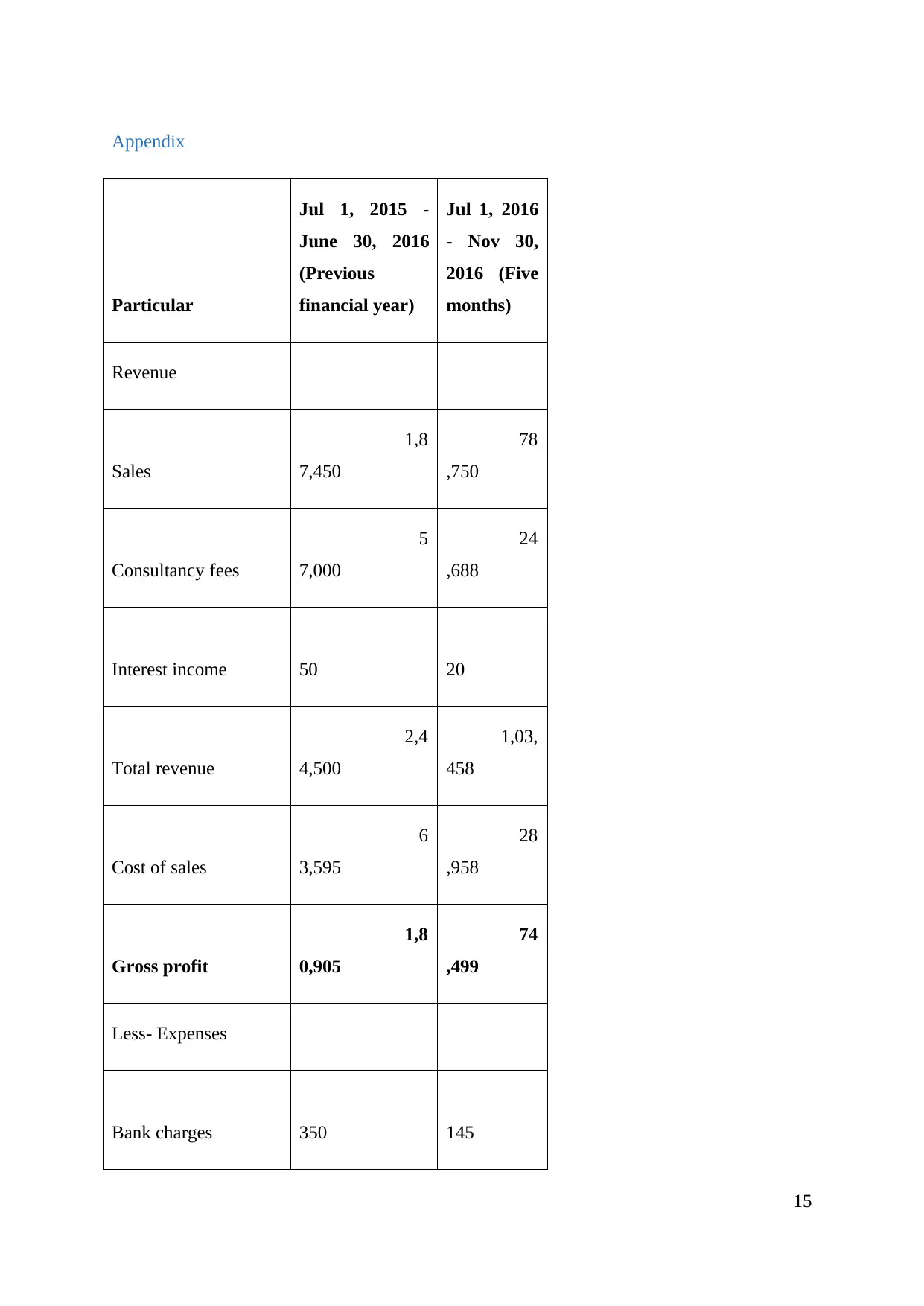

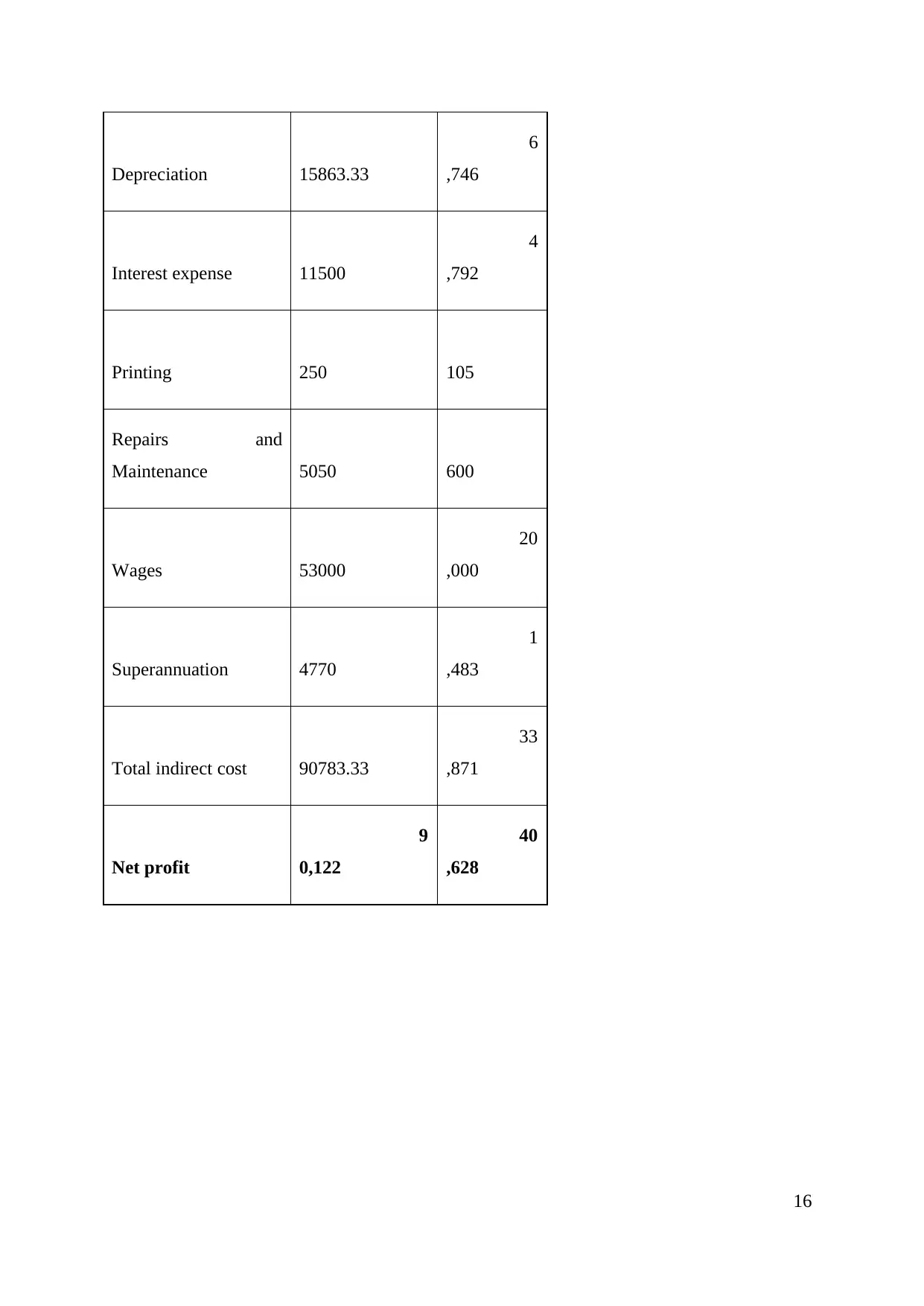

Appendix

Particular

Jul 1, 2015 -

June 30, 2016

(Previous

financial year)

Jul 1, 2016

- Nov 30,

2016 (Five

months)

Revenue

Sales

1,8

7,450

78

,750

Consultancy fees

5

7,000

24

,688

Interest income 50 20

Total revenue

2,4

4,500

1,03,

458

Cost of sales

6

3,595

28

,958

Gross profit

1,8

0,905

74

,499

Less- Expenses

Bank charges 350 145

15

Particular

Jul 1, 2015 -

June 30, 2016

(Previous

financial year)

Jul 1, 2016

- Nov 30,

2016 (Five

months)

Revenue

Sales

1,8

7,450

78

,750

Consultancy fees

5

7,000

24

,688

Interest income 50 20

Total revenue

2,4

4,500

1,03,

458

Cost of sales

6

3,595

28

,958

Gross profit

1,8

0,905

74

,499

Less- Expenses

Bank charges 350 145

15

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Depreciation 15863.33

6

,746

Interest expense 11500

4

,792

Printing 250 105

Repairs and

Maintenance 5050 600

Wages 53000

20

,000

Superannuation 4770

1

,483

Total indirect cost 90783.33

33

,871

Net profit

9

0,122

40

,628

16

6

,746

Interest expense 11500

4

,792

Printing 250 105

Repairs and

Maintenance 5050 600

Wages 53000

20

,000

Superannuation 4770

1

,483

Total indirect cost 90783.33

33

,871

Net profit

9

0,122

40

,628

16

1 out of 16

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.