ACC321 - Auditing & Professional Practice Assignment 1 Solution 2018

VerifiedAdded on 2023/06/04

|11

|2143

|286

Report

AI Summary

This assignment solution provides a detailed analysis of auditing and professional practice, focusing on Fredgrau Enterprises. It covers audit planning, identification of key accounts, determination of materiality levels, and comparative analysis using trend analysis and common size income statements for 2016 and 2017. The solution includes a preliminary analytical review to determine audit risk and design appropriate audit procedures. It also addresses fraud risk analysis, emphasizing the importance of professional skepticism and adherence to ethical standards like APES 110. Key accounts such as sales, depreciation, and interest are analyzed with specific audit assertions and recommended steps for auditing. The report concludes with recommendations for fraud risk assessment and further examination of accounts like cost of sales and superannuation expenses.

Auditing and

Professional Practice

Assignment

Professional Practice

Assignment

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1

By student name

Professor

University

Date: 25 April 2018.

1 | P a g e

By student name

Professor

University

Date: 25 April 2018.

1 | P a g e

2

Contents

Introduction.................................................................................................................................................3

Analysis and Discussion...............................................................................................................................4

Conclusion & Recommendation..................................................................................................................8

References...................................................................................................................................................9

2 | P a g e

Contents

Introduction.................................................................................................................................................3

Analysis and Discussion...............................................................................................................................4

Conclusion & Recommendation..................................................................................................................8

References...................................................................................................................................................9

2 | P a g e

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3

Introduction

Fredgrau Enterprises is a small company for which the audit planning needs to be done and

therefore the audit partner of the company has asked to the course of action to be taken about the

same. Based on the trial balance given by the company the audit procedure to be taken has been

designed besides identification of the key and critical accounts, which shows the huge deviation

(Axelsen, et al., 2017). Materiality level for the company has also been determined and the

comparative analysis of the company for 2 years 2016 and 2017 has been done via the trend

analysis and the common size income statement. This preliminary analytical review has helped

the company in determining the audit risk and thus audit procedures have been deigned

accordingly. In the end, the fraud risk analysis has also been done for the client to check if it was

a privy to any of the fraud transactions.

3 | P a g e

Introduction

Fredgrau Enterprises is a small company for which the audit planning needs to be done and

therefore the audit partner of the company has asked to the course of action to be taken about the

same. Based on the trial balance given by the company the audit procedure to be taken has been

designed besides identification of the key and critical accounts, which shows the huge deviation

(Axelsen, et al., 2017). Materiality level for the company has also been determined and the

comparative analysis of the company for 2 years 2016 and 2017 has been done via the trend

analysis and the common size income statement. This preliminary analytical review has helped

the company in determining the audit risk and thus audit procedures have been deigned

accordingly. In the end, the fraud risk analysis has also been done for the client to check if it was

a privy to any of the fraud transactions.

3 | P a g e

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4

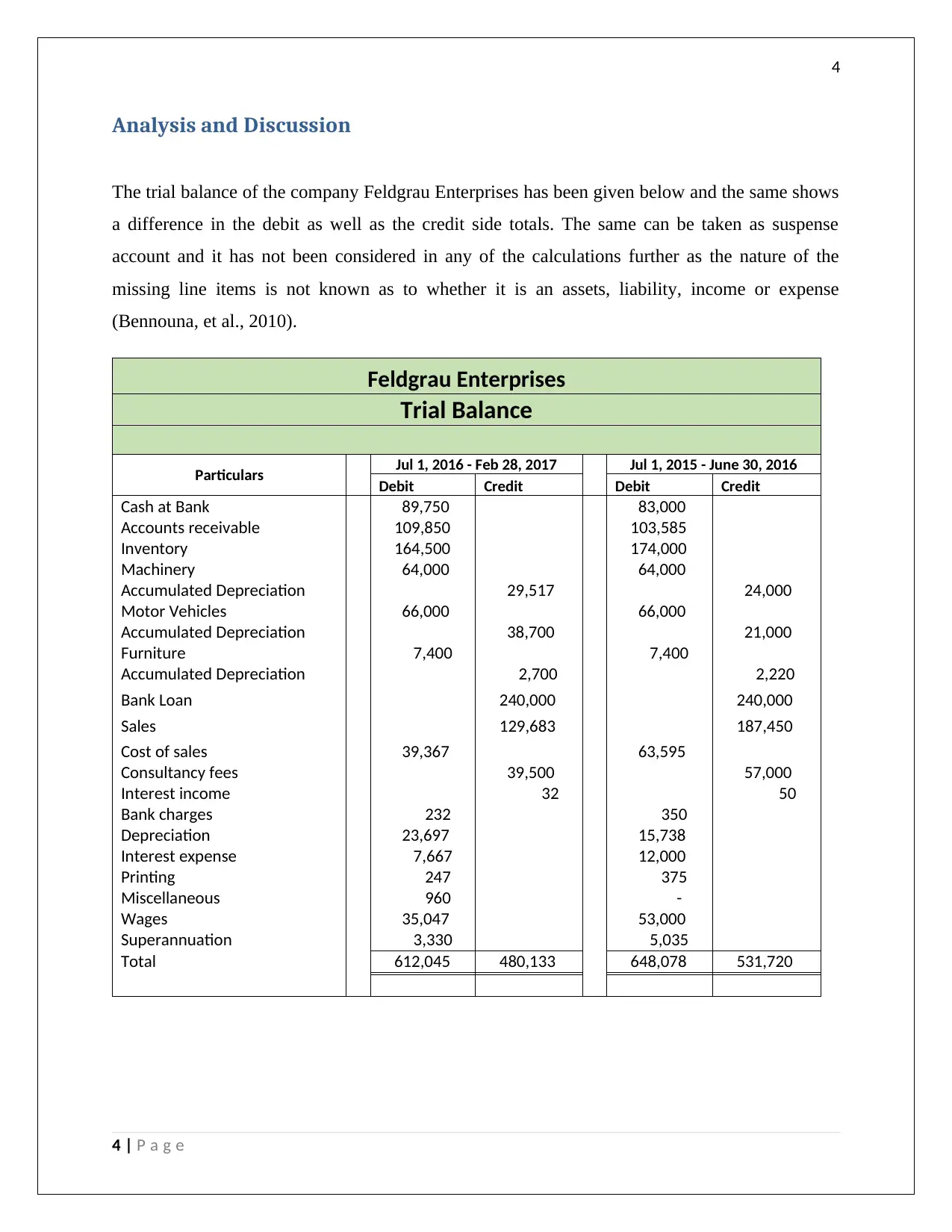

Analysis and Discussion

The trial balance of the company Feldgrau Enterprises has been given below and the same shows

a difference in the debit as well as the credit side totals. The same can be taken as suspense

account and it has not been considered in any of the calculations further as the nature of the

missing line items is not known as to whether it is an assets, liability, income or expense

(Bennouna, et al., 2010).

Feldgrau Enterprises

Trial Balance

Particulars Jul 1, 2016 - Feb 28, 2017 Jul 1, 2015 - June 30, 2016

Debit Credit Debit Credit

Cash at Bank 89,750 83,000

Accounts receivable 109,850 103,585

Inventory 164,500 174,000

Machinery 64,000 64,000

Accumulated Depreciation 29,517 24,000

Motor Vehicles 66,000 66,000

Accumulated Depreciation 38,700 21,000

Furniture 7,400 7,400

Accumulated Depreciation 2,700 2,220

Bank Loan 240,000 240,000

Sales 129,683 187,450

Cost of sales 39,367 63,595

Consultancy fees 39,500 57,000

Interest income 32 50

Bank charges 232 350

Depreciation 23,697 15,738

Interest expense 7,667 12,000

Printing 247 375

Miscellaneous 960 -

Wages 35,047 53,000

Superannuation 3,330 5,035

Total 612,045 480,133 648,078 531,720

4 | P a g e

Analysis and Discussion

The trial balance of the company Feldgrau Enterprises has been given below and the same shows

a difference in the debit as well as the credit side totals. The same can be taken as suspense

account and it has not been considered in any of the calculations further as the nature of the

missing line items is not known as to whether it is an assets, liability, income or expense

(Bennouna, et al., 2010).

Feldgrau Enterprises

Trial Balance

Particulars Jul 1, 2016 - Feb 28, 2017 Jul 1, 2015 - June 30, 2016

Debit Credit Debit Credit

Cash at Bank 89,750 83,000

Accounts receivable 109,850 103,585

Inventory 164,500 174,000

Machinery 64,000 64,000

Accumulated Depreciation 29,517 24,000

Motor Vehicles 66,000 66,000

Accumulated Depreciation 38,700 21,000

Furniture 7,400 7,400

Accumulated Depreciation 2,700 2,220

Bank Loan 240,000 240,000

Sales 129,683 187,450

Cost of sales 39,367 63,595

Consultancy fees 39,500 57,000

Interest income 32 50

Bank charges 232 350

Depreciation 23,697 15,738

Interest expense 7,667 12,000

Printing 247 375

Miscellaneous 960 -

Wages 35,047 53,000

Superannuation 3,330 5,035

Total 612,045 480,133 648,078 531,720

4 | P a g e

5

1. Materiality has been asked to be determined in the first part of the audit plan. An item can

be said to be material if it in individual or in aggregate with the similar nature line items

can change the decision of the user of the financial statements. It is something which is

very critical and important to determine from audit perspective as it helps the auditor in

knowing which all areas needs to be checked anyhow and what all areas can be ignored

for the time being (Fukukawa & Mock, 2011). Furthermore, in the given case, the audit

partner has determined the materiality to be at $ 15000, which is very high considering

the trial balance of the client. There are global accounting bodies and committees all over

the world like those of AASB and IASB as well as the reputed audit and consulting firms

like Big 4’s which have suggested that the materiality can be determined as a % of sales,

or Net profit or gross profit or total assets, or total fixed assets balance or as percentage of

shareholder’s equity. Based on these percentages the same has been calculated to be

between the range of $1105 to $ 1296 as it would help the auditors to check several other

accounts as well which were not covered earlier like those of Interest expenses,

superannuation expenses and the Furniture account (Delone & Mclean, 2004).

(in $)

Feldgrau Enterprises

Quantitative estimate of materiality

Criterion Base Amount Materiality level/range

0.5% to 1% of gross revenue Gross Revenue 129,683 648.42 to 1296.83

1% to 2% of the total assets Total Assets 430,582 4305.82 to 8611.64

1% to 2% of the gross profit Gross Profit 55,270 552.7 to 1105.4

2% - 5% of the shareholders’ equity Equity NA NA

5% to 10% of the net profit Net profit 58,670 2933.5 to 5866.99

5 | P a g e

1. Materiality has been asked to be determined in the first part of the audit plan. An item can

be said to be material if it in individual or in aggregate with the similar nature line items

can change the decision of the user of the financial statements. It is something which is

very critical and important to determine from audit perspective as it helps the auditor in

knowing which all areas needs to be checked anyhow and what all areas can be ignored

for the time being (Fukukawa & Mock, 2011). Furthermore, in the given case, the audit

partner has determined the materiality to be at $ 15000, which is very high considering

the trial balance of the client. There are global accounting bodies and committees all over

the world like those of AASB and IASB as well as the reputed audit and consulting firms

like Big 4’s which have suggested that the materiality can be determined as a % of sales,

or Net profit or gross profit or total assets, or total fixed assets balance or as percentage of

shareholder’s equity. Based on these percentages the same has been calculated to be

between the range of $1105 to $ 1296 as it would help the auditors to check several other

accounts as well which were not covered earlier like those of Interest expenses,

superannuation expenses and the Furniture account (Delone & Mclean, 2004).

(in $)

Feldgrau Enterprises

Quantitative estimate of materiality

Criterion Base Amount Materiality level/range

0.5% to 1% of gross revenue Gross Revenue 129,683 648.42 to 1296.83

1% to 2% of the total assets Total Assets 430,582 4305.82 to 8611.64

1% to 2% of the gross profit Gross Profit 55,270 552.7 to 1105.4

2% - 5% of the shareholders’ equity Equity NA NA

5% to 10% of the net profit Net profit 58,670 2933.5 to 5866.99

5 | P a g e

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6

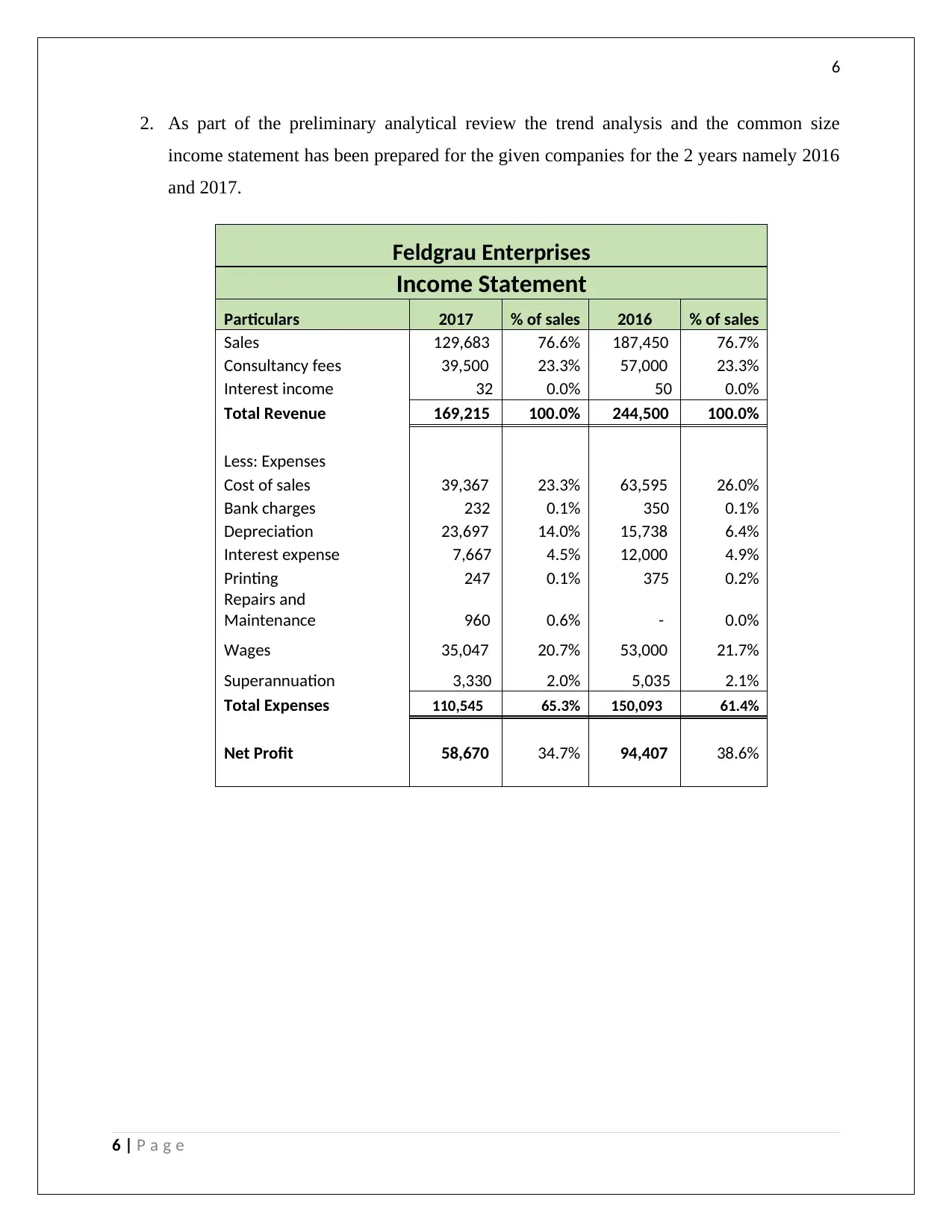

2. As part of the preliminary analytical review the trend analysis and the common size

income statement has been prepared for the given companies for the 2 years namely 2016

and 2017.

Feldgrau Enterprises

Income Statement

Particulars 2017 % of sales 2016 % of sales

Sales 129,683 76.6% 187,450 76.7%

Consultancy fees 39,500 23.3% 57,000 23.3%

Interest income 32 0.0% 50 0.0%

Total Revenue 169,215 100.0% 244,500 100.0%

Less: Expenses

Cost of sales 39,367 23.3% 63,595 26.0%

Bank charges 232 0.1% 350 0.1%

Depreciation 23,697 14.0% 15,738 6.4%

Interest expense 7,667 4.5% 12,000 4.9%

Printing 247 0.1% 375 0.2%

Repairs and

Maintenance 960 0.6% - 0.0%

Wages 35,047 20.7% 53,000 21.7%

Superannuation 3,330 2.0% 5,035 2.1%

Total Expenses 110,545 65.3% 150,093 61.4%

Net Profit 58,670 34.7% 94,407 38.6%

6 | P a g e

2. As part of the preliminary analytical review the trend analysis and the common size

income statement has been prepared for the given companies for the 2 years namely 2016

and 2017.

Feldgrau Enterprises

Income Statement

Particulars 2017 % of sales 2016 % of sales

Sales 129,683 76.6% 187,450 76.7%

Consultancy fees 39,500 23.3% 57,000 23.3%

Interest income 32 0.0% 50 0.0%

Total Revenue 169,215 100.0% 244,500 100.0%

Less: Expenses

Cost of sales 39,367 23.3% 63,595 26.0%

Bank charges 232 0.1% 350 0.1%

Depreciation 23,697 14.0% 15,738 6.4%

Interest expense 7,667 4.5% 12,000 4.9%

Printing 247 0.1% 375 0.2%

Repairs and

Maintenance 960 0.6% - 0.0%

Wages 35,047 20.7% 53,000 21.7%

Superannuation 3,330 2.0% 5,035 2.1%

Total Expenses 110,545 65.3% 150,093 61.4%

Net Profit 58,670 34.7% 94,407 38.6%

6 | P a g e

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7

Feldgrau Enterprises

Income Statement

Particulars 2017 2016 Variance

Sales 129,683 187,450 - 57,767

Consultancy fees 39,500 57,000 - 17,500

Interest income 32 50 - 18

Total Revenue 169,215 244,500 - 75,285

Less: Expenses

Cost of sales 39,367 63,595 - 24,228

Bank charges 232 350 - 118

Depreciation 23,697 15,738 7,958

Interest expense 7,667 12,000 - 4,333

Printing 247 375 - 128

Miscellaneous 960 - 960

Wages 35,047 53,000 - 17,953

Superannuation 3,330 5,035 - 1,705

Total Expenses 110,545 150,093 - 39,548

Net Profit 58,670 94,407 - 35,737

Net Profit % 34.67% 38.61%

3. Based on the above analysis, several key accounts have been selected for further review

and audit considering the criticality of the variations. Some of these are:

Sl. No. Account Name Audit Assertion and risk

1. Sales The sales has decreased by almost 31% as compared to

the last year even though as a percentage of the overall

receipts, it has been almost the same, it needs to be

properly evaluated and checked for reason of significant

drop in sales. The profit has been further impacted due

to this and dropped 38% (Zhou, 2018).

2. Depreciation When all the expenses has dropped as a result of fall in

sales the depreciation expenses have increased

drastically by 51% as compared to the last year. All the

management assertions with respect to the same like the

useful life, the rate and method of depreciation needs to

be validated in order to find the issues (Bumgarner &

Vasarhelyi, 2018).

3 Interest The interest expenses has fallen by 36% as compared to

the last year despite the bank loan balance being same.

7 | P a g e

Feldgrau Enterprises

Income Statement

Particulars 2017 2016 Variance

Sales 129,683 187,450 - 57,767

Consultancy fees 39,500 57,000 - 17,500

Interest income 32 50 - 18

Total Revenue 169,215 244,500 - 75,285

Less: Expenses

Cost of sales 39,367 63,595 - 24,228

Bank charges 232 350 - 118

Depreciation 23,697 15,738 7,958

Interest expense 7,667 12,000 - 4,333

Printing 247 375 - 128

Miscellaneous 960 - 960

Wages 35,047 53,000 - 17,953

Superannuation 3,330 5,035 - 1,705

Total Expenses 110,545 150,093 - 39,548

Net Profit 58,670 94,407 - 35,737

Net Profit % 34.67% 38.61%

3. Based on the above analysis, several key accounts have been selected for further review

and audit considering the criticality of the variations. Some of these are:

Sl. No. Account Name Audit Assertion and risk

1. Sales The sales has decreased by almost 31% as compared to

the last year even though as a percentage of the overall

receipts, it has been almost the same, it needs to be

properly evaluated and checked for reason of significant

drop in sales. The profit has been further impacted due

to this and dropped 38% (Zhou, 2018).

2. Depreciation When all the expenses has dropped as a result of fall in

sales the depreciation expenses have increased

drastically by 51% as compared to the last year. All the

management assertions with respect to the same like the

useful life, the rate and method of depreciation needs to

be validated in order to find the issues (Bumgarner &

Vasarhelyi, 2018).

3 Interest The interest expenses has fallen by 36% as compared to

the last year despite the bank loan balance being same.

7 | P a g e

8

It needs to be checked if the company has booked the

cost correctly and not shifted the same to future

accounting years (Lessambo, 2018).

4. Based on the key accounts to be audited the next year, below mentioned are few of the

steps to be undertaken to audit the same:

a. Sales: For checking the sales the vouching of the invoices need to be done and

checked if the total is matching with the ledger and journal posting. It needs to be

determined that if the sales has fallen due to fall in quantitative sales or the selling

prices or due to competitive pressure. Furthermore, the auditor should also be testing

the revenue recognition criteria followed by the entity for few of the sample cases

(Mock, et al., 2018).

b. Depreciation: About this, it needs to be checked what is the method and rates of

depreciation being used by the entity, how the company has classified its assets and

whether the annual review of the fixed assets impairment and depreciation is being

done. The auditor should check the physical verification report in order to establish

the existence of assets and completeness in recording of assets (Knechel & Salterio,

2016)

c. Interest: The interest expenses during the year needs to be cross verified from the

bank statement of the company and it needs to be checked why the same has

decreased in spite of non-repayment of the loan during the year, what the terms of the

loans and whether it is a fixed rate or floating rate interest loan (Gooley, 2016).

Conclusion & Recommendation

5. As per the professional ethics and the standards being set in APES 110 and the concept of

professional scepticism, the auditor must check the client in all the respects and basis the

trust and past relationship, any of the checking procedure should not be ignored. In the

given case, the audit partner of the company has suggested that the client should not be

checked on the criteria of fraud risk analysis as the same is trustworthy (Kuhn & Morris,

2016). However, this is against the principles mentioned above and therefore the client

should be subject to audit and fraud risk analysis. There are a few accounts which show

the possibility of fraud in the financial statements, some of which are interest account and

8 | P a g e

It needs to be checked if the company has booked the

cost correctly and not shifted the same to future

accounting years (Lessambo, 2018).

4. Based on the key accounts to be audited the next year, below mentioned are few of the

steps to be undertaken to audit the same:

a. Sales: For checking the sales the vouching of the invoices need to be done and

checked if the total is matching with the ledger and journal posting. It needs to be

determined that if the sales has fallen due to fall in quantitative sales or the selling

prices or due to competitive pressure. Furthermore, the auditor should also be testing

the revenue recognition criteria followed by the entity for few of the sample cases

(Mock, et al., 2018).

b. Depreciation: About this, it needs to be checked what is the method and rates of

depreciation being used by the entity, how the company has classified its assets and

whether the annual review of the fixed assets impairment and depreciation is being

done. The auditor should check the physical verification report in order to establish

the existence of assets and completeness in recording of assets (Knechel & Salterio,

2016)

c. Interest: The interest expenses during the year needs to be cross verified from the

bank statement of the company and it needs to be checked why the same has

decreased in spite of non-repayment of the loan during the year, what the terms of the

loans and whether it is a fixed rate or floating rate interest loan (Gooley, 2016).

Conclusion & Recommendation

5. As per the professional ethics and the standards being set in APES 110 and the concept of

professional scepticism, the auditor must check the client in all the respects and basis the

trust and past relationship, any of the checking procedure should not be ignored. In the

given case, the audit partner of the company has suggested that the client should not be

checked on the criteria of fraud risk analysis as the same is trustworthy (Kuhn & Morris,

2016). However, this is against the principles mentioned above and therefore the client

should be subject to audit and fraud risk analysis. There are a few accounts which show

the possibility of fraud in the financial statements, some of which are interest account and

8 | P a g e

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9

depreciation account for the reasons mentioned above, the cost of sales which has

declined by 38% as compared to the last year and therefore it needs to be checked if the

prices of raw materials and input has fallen or this is an instance of cost shifting.

Furthermore, the superannuation expenses account also needs to be checked as the same

has fallen by 34% and the reason for the same needs to be studied (Mubako & O'Donnell,

2018).

References

Axelsen, M., Green, P. & Ridley, G., 2017. Explaining the information systems auditor role in the public

sector financial audit. International Journal of Accounting Information Systems, 24(1), pp. 15-31.

Bennouna, K., Meredith, G. & Marchant, T., 2010. Improved capital budgeting decision making: evidence

from Canada. SCHOOL OF BUSINESS AND TOURISM, 48(2), pp. 225-247.

Bumgarner, N. & Vasarhelyi, M., 2018. Continuous auditing—a new view.. Continuous Auditing: Theory

and Application, 20(1), pp. 7-51.

Delone, W. & Mclean, E., 2004. Measuring e-Commerce Success: Applying the DeLone & McLean

Information Systems Success Model. International Journal of Electronic Commerce, 9(1).

Fukukawa, H. & Mock, T., 2011. Audit risk assessments using belief versus probability. Auditing: A

Journal of Practice & Theory, 30(1), pp. 75-99.

Gooley, J., 2016. Principles of Australian Contract Law. Australia: Lexis Nexis.

Knechel, W. & Salterio, S., 2016. Auditing:Assurance and Risk. fourth ed. New York: Routledge.

Kuhn, J. & Morris, B., 2016. IT internal control weaknesses and the market value of firms. Journal of

Enterprise Information Management, 30(6).

Lessambo, F., 2018. Audit Risks: Identification and Procedures. Auditing, Assurance Services, and

Forensics, 3(1), pp. 183-202.

Mock, T. J., Ragothaman, S. C. & Srivastava, R. P., 2018. Using Evidential Reasoning Technology to

Enhance the Audit Quality Assurance Inspection Process. Journal of Emerging Technologies in

Accounting, 15(1), pp. 29-43.

Mubako, G. & O'Donnell, E., 2018. Effect of fraud risk assessments on auditor skepticism: Unintended

consequences on evidence evaluation. International Journal of Auditing, 22(1), pp. 55-64.

9 | P a g e

depreciation account for the reasons mentioned above, the cost of sales which has

declined by 38% as compared to the last year and therefore it needs to be checked if the

prices of raw materials and input has fallen or this is an instance of cost shifting.

Furthermore, the superannuation expenses account also needs to be checked as the same

has fallen by 34% and the reason for the same needs to be studied (Mubako & O'Donnell,

2018).

References

Axelsen, M., Green, P. & Ridley, G., 2017. Explaining the information systems auditor role in the public

sector financial audit. International Journal of Accounting Information Systems, 24(1), pp. 15-31.

Bennouna, K., Meredith, G. & Marchant, T., 2010. Improved capital budgeting decision making: evidence

from Canada. SCHOOL OF BUSINESS AND TOURISM, 48(2), pp. 225-247.

Bumgarner, N. & Vasarhelyi, M., 2018. Continuous auditing—a new view.. Continuous Auditing: Theory

and Application, 20(1), pp. 7-51.

Delone, W. & Mclean, E., 2004. Measuring e-Commerce Success: Applying the DeLone & McLean

Information Systems Success Model. International Journal of Electronic Commerce, 9(1).

Fukukawa, H. & Mock, T., 2011. Audit risk assessments using belief versus probability. Auditing: A

Journal of Practice & Theory, 30(1), pp. 75-99.

Gooley, J., 2016. Principles of Australian Contract Law. Australia: Lexis Nexis.

Knechel, W. & Salterio, S., 2016. Auditing:Assurance and Risk. fourth ed. New York: Routledge.

Kuhn, J. & Morris, B., 2016. IT internal control weaknesses and the market value of firms. Journal of

Enterprise Information Management, 30(6).

Lessambo, F., 2018. Audit Risks: Identification and Procedures. Auditing, Assurance Services, and

Forensics, 3(1), pp. 183-202.

Mock, T. J., Ragothaman, S. C. & Srivastava, R. P., 2018. Using Evidential Reasoning Technology to

Enhance the Audit Quality Assurance Inspection Process. Journal of Emerging Technologies in

Accounting, 15(1), pp. 29-43.

Mubako, G. & O'Donnell, E., 2018. Effect of fraud risk assessments on auditor skepticism: Unintended

consequences on evidence evaluation. International Journal of Auditing, 22(1), pp. 55-64.

9 | P a g e

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10

Zhou, C. &. P. A., 2018. Developing creativity and learning design by information and communication

technology (ICT) in developing contexts. Encyclopedia of Information Science and Technology, pp. 4178-

4188.

10 | P a g e

Zhou, C. &. P. A., 2018. Developing creativity and learning design by information and communication

technology (ICT) in developing contexts. Encyclopedia of Information Science and Technology, pp. 4178-

4188.

10 | P a g e

1 out of 11