Auditing Report: Financial Statements and Internal Controls

VerifiedAdded on 2023/01/06

|10

|3166

|98

Report

AI Summary

This auditing report delves into various auditing concepts and their practical applications. It begins with a discussion on the meaning of sufficient appropriate audit evidence, evaluating its presence in given scenarios. The report then analyzes financial ratios for Nova Ltd, explaining their implications for the audit process. Internal control weaknesses within Everyday Supplies' cash receipts and billing functions are identified and explained. The report assesses the appropriateness of conclusions drawn by an auditing junior and describes procedures for auditing Sun Construction's revenues. Finally, it contrasts the roles and responsibilities of internal and external auditors, providing a comprehensive overview of auditing principles and practices. The report is based on the analysis of financial statements, internal controls, and audit procedures.

Auditing

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................1

QUESTION 1...................................................................................................................................1

a. Explanation of meaning of sufficient appropriate audit evidence...........................................1

b. Explanation of whether sufficient appropriate audit evidence has been obtained for each of

the situations................................................................................................................................1

QUESTION 2...................................................................................................................................2

a. Four possible explanations for the results of various ratios for Nova Ltd and explanation of

their implications for the audit.....................................................................................................2

QUESTION 3...................................................................................................................................3

a. Description of internal control weaknesses in Everyday Supplies internal control for cash

receipts and billing functions.......................................................................................................3

b. Reasons for two of the weaknesses why they are weaknesses................................................3

QUESTION 4...................................................................................................................................4

Determination of whether John has arrived at the appropriate conclusion or not.......................4

QUESTION 5...................................................................................................................................4

Description of the procedures that could be used to audit Sun Construction’s revenues............4

QUESTION 6...................................................................................................................................5

Differences and similarities of the following features of internal and external auditors.............5

CONCLUSION................................................................................................................................7

REFERENCES................................................................................................................................8

INTRODUCTION...........................................................................................................................1

QUESTION 1...................................................................................................................................1

a. Explanation of meaning of sufficient appropriate audit evidence...........................................1

b. Explanation of whether sufficient appropriate audit evidence has been obtained for each of

the situations................................................................................................................................1

QUESTION 2...................................................................................................................................2

a. Four possible explanations for the results of various ratios for Nova Ltd and explanation of

their implications for the audit.....................................................................................................2

QUESTION 3...................................................................................................................................3

a. Description of internal control weaknesses in Everyday Supplies internal control for cash

receipts and billing functions.......................................................................................................3

b. Reasons for two of the weaknesses why they are weaknesses................................................3

QUESTION 4...................................................................................................................................4

Determination of whether John has arrived at the appropriate conclusion or not.......................4

QUESTION 5...................................................................................................................................4

Description of the procedures that could be used to audit Sun Construction’s revenues............4

QUESTION 6...................................................................................................................................5

Differences and similarities of the following features of internal and external auditors.............5

CONCLUSION................................................................................................................................7

REFERENCES................................................................................................................................8

INTRODUCTION

Auditing could be defined as the process of verification of the financial statements that

are generated during the year. If the businesses will not be able to conduct audit of final accounts

then it may leave negative impact upon mind set of the stakeholders who analyse the financial

position of business for the purpose of making investment, providing credit or supplying goods.

Present report is based upon assessment of different auditing concepts (Groomer and Murthy,

2018). This assignment covers various topics such as explanation of sufficient appropriate audit

evidence, assessment of ratios, definition of internal control weaknesses, risk associates with

related party etc. Apart from this, assertions of occurrence, completeness and accuracy and notes

regarding differences and similarities of independence, reporting responsibilities etc.

QUESTION 1

a. Explanation of meaning of sufficient appropriate audit evidence

Sufficient appropriate audit evidence could be defined as the aspects that are required to

be focused by the auditors for the purpose of writing conclusion and support for the stakeholders.

There are various aspects that are focused while conducting auditing are relevancy, reliability,

accuracy, transparency etc. The auditors evaluate all the elements that are recorded in the

financial statements so that they can analyse that accurate information is recorded in the books in

context of all the receipts, payments, assets, liabilities, incomes and expenses.

b. Explanation of whether sufficient appropriate audit evidence has been obtained for each of the

situations

By analysing the two different situations it has been analysed that in the first situation

appropriate audit evidences are not been obtained. All the perceptual documents were not

provided by the entity in the case. On the other hand, in the second scenario t has been analysed

that appropriate and sufficient audit evidences were there (Minnis and Shroff, 2017). While

conducting the physical examination it was analysed by the auditor that the lucent has found five

variations between the perceptual records and the real amount which was involved were around

50000 dollars. Apart from this, it was deemed immaterial.

1

Auditing could be defined as the process of verification of the financial statements that

are generated during the year. If the businesses will not be able to conduct audit of final accounts

then it may leave negative impact upon mind set of the stakeholders who analyse the financial

position of business for the purpose of making investment, providing credit or supplying goods.

Present report is based upon assessment of different auditing concepts (Groomer and Murthy,

2018). This assignment covers various topics such as explanation of sufficient appropriate audit

evidence, assessment of ratios, definition of internal control weaknesses, risk associates with

related party etc. Apart from this, assertions of occurrence, completeness and accuracy and notes

regarding differences and similarities of independence, reporting responsibilities etc.

QUESTION 1

a. Explanation of meaning of sufficient appropriate audit evidence

Sufficient appropriate audit evidence could be defined as the aspects that are required to

be focused by the auditors for the purpose of writing conclusion and support for the stakeholders.

There are various aspects that are focused while conducting auditing are relevancy, reliability,

accuracy, transparency etc. The auditors evaluate all the elements that are recorded in the

financial statements so that they can analyse that accurate information is recorded in the books in

context of all the receipts, payments, assets, liabilities, incomes and expenses.

b. Explanation of whether sufficient appropriate audit evidence has been obtained for each of the

situations

By analysing the two different situations it has been analysed that in the first situation

appropriate audit evidences are not been obtained. All the perceptual documents were not

provided by the entity in the case. On the other hand, in the second scenario t has been analysed

that appropriate and sufficient audit evidences were there (Minnis and Shroff, 2017). While

conducting the physical examination it was analysed by the auditor that the lucent has found five

variations between the perceptual records and the real amount which was involved were around

50000 dollars. Apart from this, it was deemed immaterial.

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

QUESTION 2

a. Four possible explanations for the results of various ratios for Nova Ltd and explanation of

their implications for the audit

The explanations of ratios along with the implication on the audit is as follows for Nova Ltd:

Current ratio: From the current ratio’s result it has been determined that company’s

ability of paying short term liabilities is increased in current year because the value of actual is

higher than the budgeted one (Current ratio, 2020). Apart from this, in previous year it was very

low. Additionally, the company is also performing better than industry average that demonstrates

effective execution of business. It will impact the audit because it is very high and auditors have

to evaluate that the figures used to calculate it are correct or not.

Quick asset ratio: The actual ratio is same as budgeted and previous year that

demonstrates that the performance of entity is same. It is lower than industry average which

means it is not able to meet industry average. No improvement is being seen in the company’s

ability of paying current liabilities from quick assets. It will affect audit process as it is same as

last year (Moffitt, Rozario and Vasarhelyi, 2018).

Inventory turnover: Actual results are lower than budgeted ones which means the

company has not met its targets. The ratio is also decreased as compare to previous year that

shows its ability to convert goods in sales is decreased. Industry average is also very high as

compare to the actual results which is showing that company is not meeting the standards. It will

affect the audit process as auditors will have to evaluate ratios on different bases.

Net profit margin: Actual results are high which means actual performance is good.

Budgeted results are lower than actual one that shows organisation was not able to estimate it

properly. In previous year it was low which shows improvement in performance. The entity is

performing better than industry average because of high actual results. It will affect auditing

process as the performance is improved in current year as compared to previous year.

Gross margin: The organisation’s actual performance is good as compared to previous

year. Entity is also performing better than industry average. Its budgeted figures are very low as

compared to actual figures that shows weak estimation skills. It will affect auditing process as

the entity is improving the percentage of gross profit on sales (Song and Shmatikov, 2019).

2

a. Four possible explanations for the results of various ratios for Nova Ltd and explanation of

their implications for the audit

The explanations of ratios along with the implication on the audit is as follows for Nova Ltd:

Current ratio: From the current ratio’s result it has been determined that company’s

ability of paying short term liabilities is increased in current year because the value of actual is

higher than the budgeted one (Current ratio, 2020). Apart from this, in previous year it was very

low. Additionally, the company is also performing better than industry average that demonstrates

effective execution of business. It will impact the audit because it is very high and auditors have

to evaluate that the figures used to calculate it are correct or not.

Quick asset ratio: The actual ratio is same as budgeted and previous year that

demonstrates that the performance of entity is same. It is lower than industry average which

means it is not able to meet industry average. No improvement is being seen in the company’s

ability of paying current liabilities from quick assets. It will affect audit process as it is same as

last year (Moffitt, Rozario and Vasarhelyi, 2018).

Inventory turnover: Actual results are lower than budgeted ones which means the

company has not met its targets. The ratio is also decreased as compare to previous year that

shows its ability to convert goods in sales is decreased. Industry average is also very high as

compare to the actual results which is showing that company is not meeting the standards. It will

affect the audit process as auditors will have to evaluate ratios on different bases.

Net profit margin: Actual results are high which means actual performance is good.

Budgeted results are lower than actual one that shows organisation was not able to estimate it

properly. In previous year it was low which shows improvement in performance. The entity is

performing better than industry average because of high actual results. It will affect auditing

process as the performance is improved in current year as compared to previous year.

Gross margin: The organisation’s actual performance is good as compared to previous

year. Entity is also performing better than industry average. Its budgeted figures are very low as

compared to actual figures that shows weak estimation skills. It will affect auditing process as

the entity is improving the percentage of gross profit on sales (Song and Shmatikov, 2019).

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

QUESTION 3

a. Description of internal control weaknesses in Everyday Supplies internal control for cash

receipts and billing functions

By analysing the case of Everyday Supplies different weaknesses are identified for the

organisation. All of them could be understood with the help of following discussion:

Formulation of account receivable subsidiary ledger without a reconciliation: The

account receivable supervisor is not reconciling the account receivable subsidiary ledger

which is a weakness for the organisation. Due to this, the accuracy level of the

receivables may get affected and it will also leave negative impact upon the funding

which is used by the entity to fund operations.

Cashier not having access to the journals and ledgers: By analysing whole case of

Everyday Supplies it has been determined that the cashier of the organisation is not

having access to the journals and ledgers. It is one of the main weakness because due to

this, cashier will not able to analyse that the amount recorded in journal and ledger

accounts is accurate or not. It will also affect the accuracy and transparency of cash book

which is one of the main books used for the analysation of business performance

(Vanstraelen and Schelleman, 2017).

Large duration of credit to the contractors: The case of Everyday Supplies is

demonstrating that the duration which is provided by the organisation to the contractors is

very long and due to this the possibility of bad debts is very high. If this much time will

be provided to them then it may result in lack of funding for the organisation and will

also leave negative impact upon functionality of business.

Inappropriate management procedure: The management process of cashier,

bookkeeper and account receivable supervisor is inappropriate. They have to follow

unnecessary processes for recording the information in the books. Due to this, the time

required for formulation of reports is very high and it is affecting the effective execution

of the organisation (Libert, 2018).

b. Reasons for two of the weaknesses why they are weaknesses

Two of the main weaknesses of the organisation are as follows and these are described

with the reasons due to which these are treated as the weaknesses:

3

a. Description of internal control weaknesses in Everyday Supplies internal control for cash

receipts and billing functions

By analysing the case of Everyday Supplies different weaknesses are identified for the

organisation. All of them could be understood with the help of following discussion:

Formulation of account receivable subsidiary ledger without a reconciliation: The

account receivable supervisor is not reconciling the account receivable subsidiary ledger

which is a weakness for the organisation. Due to this, the accuracy level of the

receivables may get affected and it will also leave negative impact upon the funding

which is used by the entity to fund operations.

Cashier not having access to the journals and ledgers: By analysing whole case of

Everyday Supplies it has been determined that the cashier of the organisation is not

having access to the journals and ledgers. It is one of the main weakness because due to

this, cashier will not able to analyse that the amount recorded in journal and ledger

accounts is accurate or not. It will also affect the accuracy and transparency of cash book

which is one of the main books used for the analysation of business performance

(Vanstraelen and Schelleman, 2017).

Large duration of credit to the contractors: The case of Everyday Supplies is

demonstrating that the duration which is provided by the organisation to the contractors is

very long and due to this the possibility of bad debts is very high. If this much time will

be provided to them then it may result in lack of funding for the organisation and will

also leave negative impact upon functionality of business.

Inappropriate management procedure: The management process of cashier,

bookkeeper and account receivable supervisor is inappropriate. They have to follow

unnecessary processes for recording the information in the books. Due to this, the time

required for formulation of reports is very high and it is affecting the effective execution

of the organisation (Libert, 2018).

b. Reasons for two of the weaknesses why they are weaknesses

Two of the main weaknesses of the organisation are as follows and these are described

with the reasons due to which these are treated as the weaknesses:

3

Formulation of account receivable subsidiary ledger without a reconciliation: The

main reasons for considering it a weakness is that if the account receivable supervisor

will not focus towards reconciliation with the ledger then it will result in inaccurate

transactions in the books. Due to this, whole process of credit receiving may get impacted

because if the records will not eb reconciled then it will be very difficult to estimate that

the actual amount is received or not.

Cashier not having access to the journals and ledgers: Cashier of the organisation is

not having access of ledgers and journals due to which it will be very difficult to analyse

that actual cash is recorded in the cash book according to organisation’s receipts or not. If

the entity will not be able to deal with this weakness then it may leave negative impact

upon functionality of operations in long run (William Jr, Glover and Prawitt, 2016).

QUESTION 4

Determination of whether John has arrived at the appropriate conclusion or not

John Smith who is new junior employee in the auditing firm concluded that as all the

internal control of Taxon Ltd were working so the auditing team can use the analytical processes

alone for audit payments that are made to the related parties. BY analysing the whole situation, it

has been evaluated that John has not arrived at right conclusion because all the payments that are

made by the entity should have CFO’s signature of approval. Six out of ten payments were

having the written approval but four of them were not having it which may result in issues for the

organisation in long run. It may create the risk associated with the related party transaction

because if there will be no signature of CFO on the receipt then the receivers may raise issue and

it will create difficulties in maintenance of the transactions. Apart from this, it may also result in

the reliability of the controls within the organisation because if all the payments will not be

signed by CFO then it will affect the reliability. Due to this the payments receivers may have

issues that the receipt which is received by them is not approved by the chief finance officer of

the company (Yu and Wang, 2017).

QUESTION 5

Description of the procedures that could be used to audit Sun Construction’s revenues

The processes which could be used to audit the revenues of Sun Construction are as follows:

4

main reasons for considering it a weakness is that if the account receivable supervisor

will not focus towards reconciliation with the ledger then it will result in inaccurate

transactions in the books. Due to this, whole process of credit receiving may get impacted

because if the records will not eb reconciled then it will be very difficult to estimate that

the actual amount is received or not.

Cashier not having access to the journals and ledgers: Cashier of the organisation is

not having access of ledgers and journals due to which it will be very difficult to analyse

that actual cash is recorded in the cash book according to organisation’s receipts or not. If

the entity will not be able to deal with this weakness then it may leave negative impact

upon functionality of operations in long run (William Jr, Glover and Prawitt, 2016).

QUESTION 4

Determination of whether John has arrived at the appropriate conclusion or not

John Smith who is new junior employee in the auditing firm concluded that as all the

internal control of Taxon Ltd were working so the auditing team can use the analytical processes

alone for audit payments that are made to the related parties. BY analysing the whole situation, it

has been evaluated that John has not arrived at right conclusion because all the payments that are

made by the entity should have CFO’s signature of approval. Six out of ten payments were

having the written approval but four of them were not having it which may result in issues for the

organisation in long run. It may create the risk associated with the related party transaction

because if there will be no signature of CFO on the receipt then the receivers may raise issue and

it will create difficulties in maintenance of the transactions. Apart from this, it may also result in

the reliability of the controls within the organisation because if all the payments will not be

signed by CFO then it will affect the reliability. Due to this the payments receivers may have

issues that the receipt which is received by them is not approved by the chief finance officer of

the company (Yu and Wang, 2017).

QUESTION 5

Description of the procedures that could be used to audit Sun Construction’s revenues

The processes which could be used to audit the revenues of Sun Construction are as follows:

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Occurrence: In order to work on this assertion, the auditors can analyse all the

transactions that are made by Magi during the year as it will help to evaluate the actual occurred

transactions.

Completeness: Under this type assertion the auditor can analyse that all the receipts and

payments are mentioned in the accounting books or not so that accurate records could be

generated.

Accuracy: It is last assertion and the process which could be undertaken by the auditor

for the organisation is checking the records and the bills that are provided by Magi to the clients

as it will help to analyse the accuracy of all the transactions.

By paying attention towards above described processes appropriate audit for all the final

accounts of Sun Construction could eb conducted and the revenues could be audited in

systematic manner (Zhang, Wang and Xu, 2019).

QUESTION 6

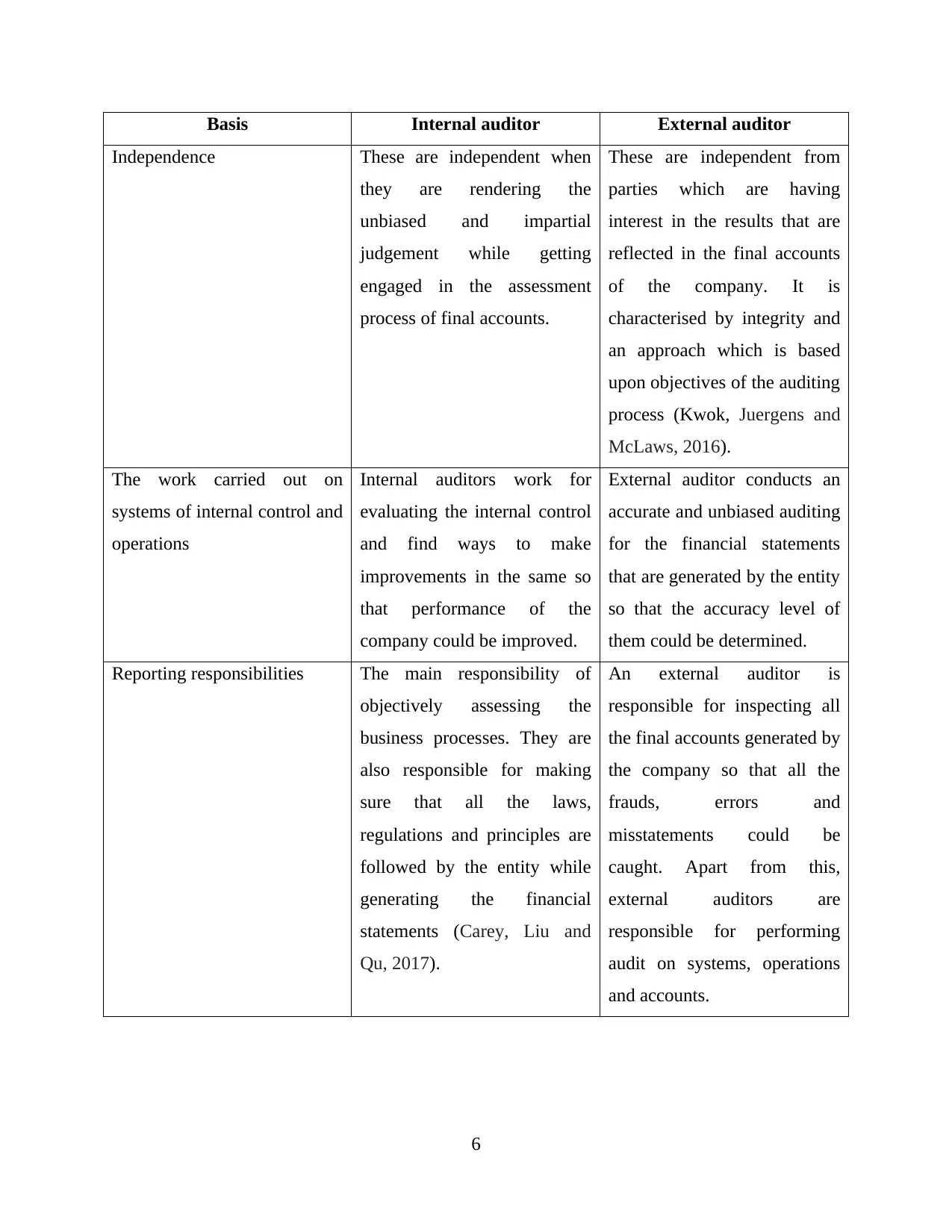

Differences and similarities of the following features of internal and external auditors

Internal auditors: A trained professional who is tasked with making independent and

accurate evaluation of the entity’ operational and financial performance. Main role of them is to

make sure that the company is following correct procedures to formulate the financial

statements. They are responsible for providing independent assurance of that the business is able

to conduct all the procedures of risk management, governance etc. in systematic manner or not.

These are the individuals who are member of board, trustees, accounting officers and the whole

audit committee of the organisation.

External auditors: The person who is a public accountant who is responsible to conduct

audit of all the final accounts, review the position of company and work for all the clients.

External auditor is an independent person who works independently for all the clients and remain

impartial to evaluate the financial statements which are formulated for evaluation of actual

performance of the entity. These are appointed by the shareholders of the company and if they do

not appoint them then directors appoint them (Simeunović, Grubor and Ristić, 2016).

Difference between external and internal auditors: There are various differences

between internal and external auditors of the company. All of them could be understood on the

basis of following discussion:

5

transactions that are made by Magi during the year as it will help to evaluate the actual occurred

transactions.

Completeness: Under this type assertion the auditor can analyse that all the receipts and

payments are mentioned in the accounting books or not so that accurate records could be

generated.

Accuracy: It is last assertion and the process which could be undertaken by the auditor

for the organisation is checking the records and the bills that are provided by Magi to the clients

as it will help to analyse the accuracy of all the transactions.

By paying attention towards above described processes appropriate audit for all the final

accounts of Sun Construction could eb conducted and the revenues could be audited in

systematic manner (Zhang, Wang and Xu, 2019).

QUESTION 6

Differences and similarities of the following features of internal and external auditors

Internal auditors: A trained professional who is tasked with making independent and

accurate evaluation of the entity’ operational and financial performance. Main role of them is to

make sure that the company is following correct procedures to formulate the financial

statements. They are responsible for providing independent assurance of that the business is able

to conduct all the procedures of risk management, governance etc. in systematic manner or not.

These are the individuals who are member of board, trustees, accounting officers and the whole

audit committee of the organisation.

External auditors: The person who is a public accountant who is responsible to conduct

audit of all the final accounts, review the position of company and work for all the clients.

External auditor is an independent person who works independently for all the clients and remain

impartial to evaluate the financial statements which are formulated for evaluation of actual

performance of the entity. These are appointed by the shareholders of the company and if they do

not appoint them then directors appoint them (Simeunović, Grubor and Ristić, 2016).

Difference between external and internal auditors: There are various differences

between internal and external auditors of the company. All of them could be understood on the

basis of following discussion:

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Basis Internal auditor External auditor

Independence These are independent when

they are rendering the

unbiased and impartial

judgement while getting

engaged in the assessment

process of final accounts.

These are independent from

parties which are having

interest in the results that are

reflected in the final accounts

of the company. It is

characterised by integrity and

an approach which is based

upon objectives of the auditing

process (Kwok, Juergens and

McLaws, 2016).

The work carried out on

systems of internal control and

operations

Internal auditors work for

evaluating the internal control

and find ways to make

improvements in the same so

that performance of the

company could be improved.

External auditor conducts an

accurate and unbiased auditing

for the financial statements

that are generated by the entity

so that the accuracy level of

them could be determined.

Reporting responsibilities The main responsibility of

objectively assessing the

business processes. They are

also responsible for making

sure that all the laws,

regulations and principles are

followed by the entity while

generating the financial

statements (Carey, Liu and

Qu, 2017).

An external auditor is

responsible for inspecting all

the final accounts generated by

the company so that all the

frauds, errors and

misstatements could be

caught. Apart from this,

external auditors are

responsible for performing

audit on systems, operations

and accounts.

6

Independence These are independent when

they are rendering the

unbiased and impartial

judgement while getting

engaged in the assessment

process of final accounts.

These are independent from

parties which are having

interest in the results that are

reflected in the final accounts

of the company. It is

characterised by integrity and

an approach which is based

upon objectives of the auditing

process (Kwok, Juergens and

McLaws, 2016).

The work carried out on

systems of internal control and

operations

Internal auditors work for

evaluating the internal control

and find ways to make

improvements in the same so

that performance of the

company could be improved.

External auditor conducts an

accurate and unbiased auditing

for the financial statements

that are generated by the entity

so that the accuracy level of

them could be determined.

Reporting responsibilities The main responsibility of

objectively assessing the

business processes. They are

also responsible for making

sure that all the laws,

regulations and principles are

followed by the entity while

generating the financial

statements (Carey, Liu and

Qu, 2017).

An external auditor is

responsible for inspecting all

the final accounts generated by

the company so that all the

frauds, errors and

misstatements could be

caught. Apart from this,

external auditors are

responsible for performing

audit on systems, operations

and accounts.

6

Similarities between external and internal auditors: There are various similarities

between internal and external auditors. All of them could be understood with the help of

following discussion:

Independence: Both type of auditors has independence of providing accurate opinion on

the actual position of the company so that engagement of stakeholders could be

maintained.

Work carried out on systems of internal control and operations: Internal as well as

external auditors work for assurance of compliance of accurate rules for auditing

(Zhaokai and Moffitt, 2019).

Reporting responsibilities: Internal and external auditors have main responsibility of

making sure that company’s records are audited properly as it is required for providing

detailed information of business to the stakeholders.

CONCLUSION

From the above project report it has been concluded that auditing is the process of

analysing accuracy of level of information which is recorded in the final accounts. It is very

important for the auditors to have appropriate audit evidences as it can help to analyse that

accurate information is recorded in the books or not. There are two different types auditors which

are internal and external and all of them have different characteristics. These are independence,

reporting responsibility and the work carried out on the systems.

7

between internal and external auditors. All of them could be understood with the help of

following discussion:

Independence: Both type of auditors has independence of providing accurate opinion on

the actual position of the company so that engagement of stakeholders could be

maintained.

Work carried out on systems of internal control and operations: Internal as well as

external auditors work for assurance of compliance of accurate rules for auditing

(Zhaokai and Moffitt, 2019).

Reporting responsibilities: Internal and external auditors have main responsibility of

making sure that company’s records are audited properly as it is required for providing

detailed information of business to the stakeholders.

CONCLUSION

From the above project report it has been concluded that auditing is the process of

analysing accuracy of level of information which is recorded in the final accounts. It is very

important for the auditors to have appropriate audit evidences as it can help to analyse that

accurate information is recorded in the books or not. There are two different types auditors which

are internal and external and all of them have different characteristics. These are independence,

reporting responsibility and the work carried out on the systems.

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

REFERENCES

Books and Journals:

Carey, P., Liu, L. and Qu, W., 2017. Voluntary corporate social responsibility reporting and

financial statement auditing in China. Journal of Contemporary Accounting &

Economics. 13(3). pp.244-262.

Groomer, S. M. and Murthy, U. S., 2018. Continuous Auditing of Database Applications: An

Embedded Audit Module Approach1. In Continuous auditing. Emerald Publishing

Limited.

Kwok, Y. L. A., Juergens, C. P. and McLaws, M. L., 2016. Automated hand hygiene auditing

with and without an intervention. American journal of infection control. 44(12).

pp.1475-1480.

Libert, T., 2018, April. An automated approach to auditing disclosure of third-party data

collection in website privacy policies. In Proceedings of the 2018 World Wide Web

Conference (pp. 207-216).

Minnis, M. and Shroff, N., 2017. Why regulate private firm disclosure and auditing?. Accounting

and Business Research. 47(5). pp.473-502.

Moffitt, K. C., Rozario, A. M. and Vasarhelyi, M. A., 2018. Robotic process automation for

auditing. Journal of Emerging Technologies in Accounting. 15(1). pp.1-10.

Simeunović, N., Grubor, G. and Ristić, N., 2016. Forensic accounting in the fraud auditing

case. The European Journal of Applied Economics. 13(2). pp.45-56.

Song, C. and Shmatikov, V., 2019, July. Auditing data provenance in text-generation models.

In Proceedings of the 25th ACM SIGKDD International Conference on Knowledge

Discovery & Data Mining (pp. 196-206).

Vanstraelen, A. and Schelleman, C., 2017. Auditing private companies: what do we

know?. Accounting and Business Research. 47(5). pp.565-584.

William Jr, M., Glover, S. and Prawitt, D., 2016. Auditing and assurance services: A systematic

approach. McGraw-Hill Education.

Yu, J. and Wang, H., 2017. Strong key-exposure resilient auditing for secure cloud storage. IEEE

Transactions on Information Forensics and Security. 12(8). pp.1931-1940.

Zhang, X., Wang, H. and Xu, C., 2019. Identity-based key-exposure resilient cloud storage

public auditing scheme from lattices. Information Sciences. 472. pp.223-234.

Zhaokai, Y. and Moffitt, K. C., 2019. Contract analytics in auditing. Accounting Horizons. 33(3).

pp.111-126.

Online

Current ratio. 2020. [Online]. Available through:

<https://www.readyratios.com/reference/liquidity/current_ratio.html>

8

Books and Journals:

Carey, P., Liu, L. and Qu, W., 2017. Voluntary corporate social responsibility reporting and

financial statement auditing in China. Journal of Contemporary Accounting &

Economics. 13(3). pp.244-262.

Groomer, S. M. and Murthy, U. S., 2018. Continuous Auditing of Database Applications: An

Embedded Audit Module Approach1. In Continuous auditing. Emerald Publishing

Limited.

Kwok, Y. L. A., Juergens, C. P. and McLaws, M. L., 2016. Automated hand hygiene auditing

with and without an intervention. American journal of infection control. 44(12).

pp.1475-1480.

Libert, T., 2018, April. An automated approach to auditing disclosure of third-party data

collection in website privacy policies. In Proceedings of the 2018 World Wide Web

Conference (pp. 207-216).

Minnis, M. and Shroff, N., 2017. Why regulate private firm disclosure and auditing?. Accounting

and Business Research. 47(5). pp.473-502.

Moffitt, K. C., Rozario, A. M. and Vasarhelyi, M. A., 2018. Robotic process automation for

auditing. Journal of Emerging Technologies in Accounting. 15(1). pp.1-10.

Simeunović, N., Grubor, G. and Ristić, N., 2016. Forensic accounting in the fraud auditing

case. The European Journal of Applied Economics. 13(2). pp.45-56.

Song, C. and Shmatikov, V., 2019, July. Auditing data provenance in text-generation models.

In Proceedings of the 25th ACM SIGKDD International Conference on Knowledge

Discovery & Data Mining (pp. 196-206).

Vanstraelen, A. and Schelleman, C., 2017. Auditing private companies: what do we

know?. Accounting and Business Research. 47(5). pp.565-584.

William Jr, M., Glover, S. and Prawitt, D., 2016. Auditing and assurance services: A systematic

approach. McGraw-Hill Education.

Yu, J. and Wang, H., 2017. Strong key-exposure resilient auditing for secure cloud storage. IEEE

Transactions on Information Forensics and Security. 12(8). pp.1931-1940.

Zhang, X., Wang, H. and Xu, C., 2019. Identity-based key-exposure resilient cloud storage

public auditing scheme from lattices. Information Sciences. 472. pp.223-234.

Zhaokai, Y. and Moffitt, K. C., 2019. Contract analytics in auditing. Accounting Horizons. 33(3).

pp.111-126.

Online

Current ratio. 2020. [Online]. Available through:

<https://www.readyratios.com/reference/liquidity/current_ratio.html>

8

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.