Auditing Report: Risk Assessment and Analysis of Blue-Circle Chemicals

VerifiedAdded on 2023/06/05

|13

|2958

|163

Report

AI Summary

This auditing report provides a detailed analysis of the audit risk associated with Blue-Circle Chemicals Limited. It begins by defining audit risk and acceptable audit risk, emphasizing the low acceptable audit risk due to internal control weaknesses. The report then assesses inherent risk, highlighting factors such as the company's import activities, foreign currency transactions, and related-party transactions, all of which contribute to a high inherent risk. Control risk is also evaluated, with the report identifying significant weaknesses in the segregation of duties, verification processes, and the overall accounting system. Ratio analysis, including quick ratio, inventory days, days to collect accounts receivable, and gross profit, is presented to highlight the company's financial performance. Finally, the report outlines follow-up audit procedures to address the identified risks and weaknesses, providing a comprehensive overview of the audit process.

Running head: AUDITING

Auditing

Name of the Student:

Name of the University:

Authors Note:

Auditing

Name of the Student:

Name of the University:

Authors Note:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1

AUDITING

Contents

Requirement 1:.................................................................................................................................2

Requirements 2:...............................................................................................................................2

Inherent risk:................................................................................................................................3

Control risk:.................................................................................................................................4

Requirement 3:.................................................................................................................................6

Ratio analysis:..............................................................................................................................6

Follow up audit procedures:........................................................................................................7

References:......................................................................................................................................9

AUDITING

Contents

Requirement 1:.................................................................................................................................2

Requirements 2:...............................................................................................................................2

Inherent risk:................................................................................................................................3

Control risk:.................................................................................................................................4

Requirement 3:.................................................................................................................................6

Ratio analysis:..............................................................................................................................6

Follow up audit procedures:........................................................................................................7

References:......................................................................................................................................9

2

AUDITING

Requirement 1:

The risk that an auditor will express an inappropriate audit opinion on the financial

statements of an entity is defined as the audit risk. Acceptable audit risk is a term that has been

coined from the concept of audit risk. Acceptable level of audit risk is determined by an auditor

specific to an entity which is being audited (Louwers, Ramsay, Sinason, Strawser & Thibodeau,

2015).

In case of Blue-Circle Chemicals Limited the acceptable audit risk is significantly low as the

likelihood of financial failure to the company is quite high with number of weaknesses in

internal controls and securities within the organization. Though the reliance of external users is

relatively less however, the lack of internal controls and securities within the company means

that the acceptable level of audit risk is quite low. The weaknesses in segregation of

responsibilities between different departments have contributed to the low level of acceptable

audit risk for the audit of the company (Ruhnke & Schmidt, 2014). The biggest weakness in the

internal controls within the entity is not to separate the accounting department of the entity with

its other departments. Hence, acceptable audit risk for the audit of the company is significantly

low.

Requirements 2:

Taking into consideration the information provided about the purchase and procurement process

of Blue-Circle Chemicals Limited, the auditor will assess inherent risk and control risk in the

audit of financial statements of the company.

Overall audit risk in an audit of an entity is dependent on the following mathematical equation:

Detection risk = Audit risk / (Inherent risk x Control risk)

AUDITING

Requirement 1:

The risk that an auditor will express an inappropriate audit opinion on the financial

statements of an entity is defined as the audit risk. Acceptable audit risk is a term that has been

coined from the concept of audit risk. Acceptable level of audit risk is determined by an auditor

specific to an entity which is being audited (Louwers, Ramsay, Sinason, Strawser & Thibodeau,

2015).

In case of Blue-Circle Chemicals Limited the acceptable audit risk is significantly low as the

likelihood of financial failure to the company is quite high with number of weaknesses in

internal controls and securities within the organization. Though the reliance of external users is

relatively less however, the lack of internal controls and securities within the company means

that the acceptable level of audit risk is quite low. The weaknesses in segregation of

responsibilities between different departments have contributed to the low level of acceptable

audit risk for the audit of the company (Ruhnke & Schmidt, 2014). The biggest weakness in the

internal controls within the entity is not to separate the accounting department of the entity with

its other departments. Hence, acceptable audit risk for the audit of the company is significantly

low.

Requirements 2:

Taking into consideration the information provided about the purchase and procurement process

of Blue-Circle Chemicals Limited, the auditor will assess inherent risk and control risk in the

audit of financial statements of the company.

Overall audit risk in an audit of an entity is dependent on the following mathematical equation:

Detection risk = Audit risk / (Inherent risk x Control risk)

You're viewing a preview

Unlock full access by subscribing today!

3

AUDITING

Inherent risk:

The risk of error and omission in financial statements due to a reason which is not related

to failure of control can be defined as the inherent risk. The level of inherent risk in an audit of

financial statements are dependent on the nature of transactions and complexity in such

transactions (Bailey, Collins & Abbott, 2017). Thus, for entities with complex financial and

accounting transactions will most likely to have high inherent risk as compared to entities where

transactions are less complicated and relatively simple. Similarly in situations where the

accountants require to sue significant amount of financial estimates and high degree of judgment,

the level of inherent risk is significantly high. In contrast where the transactions are simple and

the accountants do not need to use significant amount of accounting estimates and judgment, the

inherent risk will be quite low (Knechel & Salterio, 2016).

Blue-Circle Chemicals Limited is a publicly traded company in the Australian Securities

Exchange (ASX). As per the audit report of the company for the last financial year, there was no

material misstatements in the financial statements of the company. In 2018 however, the

company has started importing goods from Thailand with the objective of reducing the purchase

costs of the company. The payments to the exporter for such imports are made in Thai Baht. The

Australian accounting standard AASB 121 contain all the guidelines that a listed entity must

follow to record the impact of changes in foreign exchange rates in the financial statements (Cao,

Chychyla & Stewart, 2015). The objective of AASB 121 is to ensure that the changes in foreign

exchange rates are correctly recorded in the financial statements to reflect the true and fair

financial performance and position of the company as on a particular date.

The import costs of goods from Thailand are denominated in Thai Baht. A junior accounts clerk

in Blue-Circle Chemicals carries out the translation of purchase costs denominated in Thai Baht

AUDITING

Inherent risk:

The risk of error and omission in financial statements due to a reason which is not related

to failure of control can be defined as the inherent risk. The level of inherent risk in an audit of

financial statements are dependent on the nature of transactions and complexity in such

transactions (Bailey, Collins & Abbott, 2017). Thus, for entities with complex financial and

accounting transactions will most likely to have high inherent risk as compared to entities where

transactions are less complicated and relatively simple. Similarly in situations where the

accountants require to sue significant amount of financial estimates and high degree of judgment,

the level of inherent risk is significantly high. In contrast where the transactions are simple and

the accountants do not need to use significant amount of accounting estimates and judgment, the

inherent risk will be quite low (Knechel & Salterio, 2016).

Blue-Circle Chemicals Limited is a publicly traded company in the Australian Securities

Exchange (ASX). As per the audit report of the company for the last financial year, there was no

material misstatements in the financial statements of the company. In 2018 however, the

company has started importing goods from Thailand with the objective of reducing the purchase

costs of the company. The payments to the exporter for such imports are made in Thai Baht. The

Australian accounting standard AASB 121 contain all the guidelines that a listed entity must

follow to record the impact of changes in foreign exchange rates in the financial statements (Cao,

Chychyla & Stewart, 2015). The objective of AASB 121 is to ensure that the changes in foreign

exchange rates are correctly recorded in the financial statements to reflect the true and fair

financial performance and position of the company as on a particular date.

The import costs of goods from Thailand are denominated in Thai Baht. A junior accounts clerk

in Blue-Circle Chemicals carries out the translation of purchase costs denominated in Thai Baht

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4

AUDITING

into Australian dollars. Considering the technical skills and knowledge of accounting standards

required to carry out such difficult job of translating foreign exchange operations into domestic

currency, giving responsibility of it to a junior accounts clerk has obviously contributed in

increasing the inherent risk of the purchase account (Chan & Vasarhelyi, 2018).

Apart from that the company has also started purchasing from a company which is owned by one

of the directors of the company. This has also adversely effected the overall audit risk in relation

to the purchase account of the company. The directors is an agent of a company. He has a

responsibility to act in the interests of the company. However, procuring and purchasing

materials from a company owned by one of the directors of the company is a direct violation of

the concept of neutral director (Christ, Masli, Sharp & Wood, 2015). A director knowing that a

purchase will be made from his company and voting in such meetings where he is interested

would violate the provisions of the Corporations Act 2001. Thus, inherent risk in relation to the

purchase account of the company in the financial year ending on June 30, 2018 is significantly

high.

Thus, the factors affecting the inherent risk in this case are as following:

I. Unusual in nature, i.e. importing goods from Thailand for the very first time.

II. The purchases made in Thai Currency Thai Baht.

III. Translation of purchases costs in Australian Dollar would require expertise knowledge in

accounting and foreign currency rates.

IV. Honest mistake due to the fact that a junior accounts clerk has been appointed to translate the

purchases costs denominated in Thai Baht into Australian dollars.

V. Related parties transaction with purchases made from a company owned by one of the

directors.

AUDITING

into Australian dollars. Considering the technical skills and knowledge of accounting standards

required to carry out such difficult job of translating foreign exchange operations into domestic

currency, giving responsibility of it to a junior accounts clerk has obviously contributed in

increasing the inherent risk of the purchase account (Chan & Vasarhelyi, 2018).

Apart from that the company has also started purchasing from a company which is owned by one

of the directors of the company. This has also adversely effected the overall audit risk in relation

to the purchase account of the company. The directors is an agent of a company. He has a

responsibility to act in the interests of the company. However, procuring and purchasing

materials from a company owned by one of the directors of the company is a direct violation of

the concept of neutral director (Christ, Masli, Sharp & Wood, 2015). A director knowing that a

purchase will be made from his company and voting in such meetings where he is interested

would violate the provisions of the Corporations Act 2001. Thus, inherent risk in relation to the

purchase account of the company in the financial year ending on June 30, 2018 is significantly

high.

Thus, the factors affecting the inherent risk in this case are as following:

I. Unusual in nature, i.e. importing goods from Thailand for the very first time.

II. The purchases made in Thai Currency Thai Baht.

III. Translation of purchases costs in Australian Dollar would require expertise knowledge in

accounting and foreign currency rates.

IV. Honest mistake due to the fact that a junior accounts clerk has been appointed to translate the

purchases costs denominated in Thai Baht into Australian dollars.

V. Related parties transaction with purchases made from a company owned by one of the

directors.

5

AUDITING

VI. Susceptible fraudulent reporting due to non-separation of accounting department with other

operating departments.

VII. Non-disclosure of true effect of transaction with collation between accountants and othere

departments.

VIII. Risk of errors in translation of foreign currencies into Australian dollar.

IX. Use of accounting estimates while using appropriate rate foreign exchange to translate the

purchase costs (Christ, Masli, Sharp & Wood, 2015).

Control risk:

Misstatements in financial statements resulting from failure of controls within the

organization is defined as control risk. An entity requires to install necessary controls and

securities to ensure that the risk of misstatements in financial statements due to failure of

controls is as low as possible. This is to ensure that the overall audit risk is at acceptable level

(Bahr, 2014).

In case of Blue-Circle Chemicals Limited, the entity has not separated the accounting department

with other operating departments. This is a huge control risk as the accounting department

should have been separated with other operating departments to maintain independence of the

department. In relation to purchases also the non-separation of accounting department with

procurement and inventory. Apart from that a thorough evolution of the purchase and

procurement process of the company would be helpful in assessing the control risk in relation to

the purchase account of the company (Graham, Bedard & Dutta, 2018).

Only the purchase manager of Blue-Circle Chemicals Limited is authorized to use and issue pre-

numbered purchase orders. A copy of purchase order is sent to the accounting department

subsequent to the issuance of such purchase order to the supplier. All purchase orders are

AUDITING

VI. Susceptible fraudulent reporting due to non-separation of accounting department with other

operating departments.

VII. Non-disclosure of true effect of transaction with collation between accountants and othere

departments.

VIII. Risk of errors in translation of foreign currencies into Australian dollar.

IX. Use of accounting estimates while using appropriate rate foreign exchange to translate the

purchase costs (Christ, Masli, Sharp & Wood, 2015).

Control risk:

Misstatements in financial statements resulting from failure of controls within the

organization is defined as control risk. An entity requires to install necessary controls and

securities to ensure that the risk of misstatements in financial statements due to failure of

controls is as low as possible. This is to ensure that the overall audit risk is at acceptable level

(Bahr, 2014).

In case of Blue-Circle Chemicals Limited, the entity has not separated the accounting department

with other operating departments. This is a huge control risk as the accounting department

should have been separated with other operating departments to maintain independence of the

department. In relation to purchases also the non-separation of accounting department with

procurement and inventory. Apart from that a thorough evolution of the purchase and

procurement process of the company would be helpful in assessing the control risk in relation to

the purchase account of the company (Graham, Bedard & Dutta, 2018).

Only the purchase manager of Blue-Circle Chemicals Limited is authorized to use and issue pre-

numbered purchase orders. A copy of purchase order is sent to the accounting department

subsequent to the issuance of such purchase order to the supplier. All purchase orders are

You're viewing a preview

Unlock full access by subscribing today!

6

AUDITING

checked by the accounting department to assess whether there is any particular purchase order

which is missing (Hines, Masli, Mauldin & Peters, 2015). Up-to this stage in purchase

procedure, there is hardly any weakness in the internal controls within the entity in relation to

purchase account. However, subsequent to the receipts invoice from the supplier there is no

matching of such invoice with the purchase order and goods received note by the company. This

creates a potential problem to the overall control within the entity as far as the purchase account

is concerned. In case of any discrepancies between the suppliers’ invoice and purchase order

there is no controls within the entity to identify such discrepancies and take corrective actions

accordingly (Chou, 2015). Comparison of monthly statements of suppliers with general ledger

balances are carried out by a junior accounts clerk is also an area which is quite susceptible to

control risk.

Taking into consideration the overall controls in relation to purchase account and in recording

purchase entries correctly in the books of accounts of Blue-Circle Chemicals Limited, it is quite

clear that there are significant weaknesses in the existing controls to correctly record the

purchase expenditures in the financial statements. Thus, the control risk in relation to the

purchase account of the company is quite high and following factors have contributed to the

increased level of control risks in the company (Backof, Bowlin & Goodson, 2017).

I. Non segregation of accounting department with other operating departments.

II. Weak authentication and verification controls of the accounting system.

III. Manipulation of accounting records is high as the accounting system is not password

protected.

IV. No distinction between the roles and responsibilities of Chief Financial Officer of the

company and the accounting department.

AUDITING

checked by the accounting department to assess whether there is any particular purchase order

which is missing (Hines, Masli, Mauldin & Peters, 2015). Up-to this stage in purchase

procedure, there is hardly any weakness in the internal controls within the entity in relation to

purchase account. However, subsequent to the receipts invoice from the supplier there is no

matching of such invoice with the purchase order and goods received note by the company. This

creates a potential problem to the overall control within the entity as far as the purchase account

is concerned. In case of any discrepancies between the suppliers’ invoice and purchase order

there is no controls within the entity to identify such discrepancies and take corrective actions

accordingly (Chou, 2015). Comparison of monthly statements of suppliers with general ledger

balances are carried out by a junior accounts clerk is also an area which is quite susceptible to

control risk.

Taking into consideration the overall controls in relation to purchase account and in recording

purchase entries correctly in the books of accounts of Blue-Circle Chemicals Limited, it is quite

clear that there are significant weaknesses in the existing controls to correctly record the

purchase expenditures in the financial statements. Thus, the control risk in relation to the

purchase account of the company is quite high and following factors have contributed to the

increased level of control risks in the company (Backof, Bowlin & Goodson, 2017).

I. Non segregation of accounting department with other operating departments.

II. Weak authentication and verification controls of the accounting system.

III. Manipulation of accounting records is high as the accounting system is not password

protected.

IV. No distinction between the roles and responsibilities of Chief Financial Officer of the

company and the accounting department.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7

AUDITING

V. No standard procedure to verify the invoices issued by the suppliers.

VI. Purchase order and goods received note are not verified with invoices.

VII. No control in payments to the suppliers as the invoices are paid by the accountants directly.

VIII. No automatic appraisal of one’s work by another.

IX. Improper monthly reconciliation process as a junior accounts clerk verifies monthly

statements of the supplier with general ledger balances (Plumlee, Rixom & Rosman, 2014).

Requirement 3:

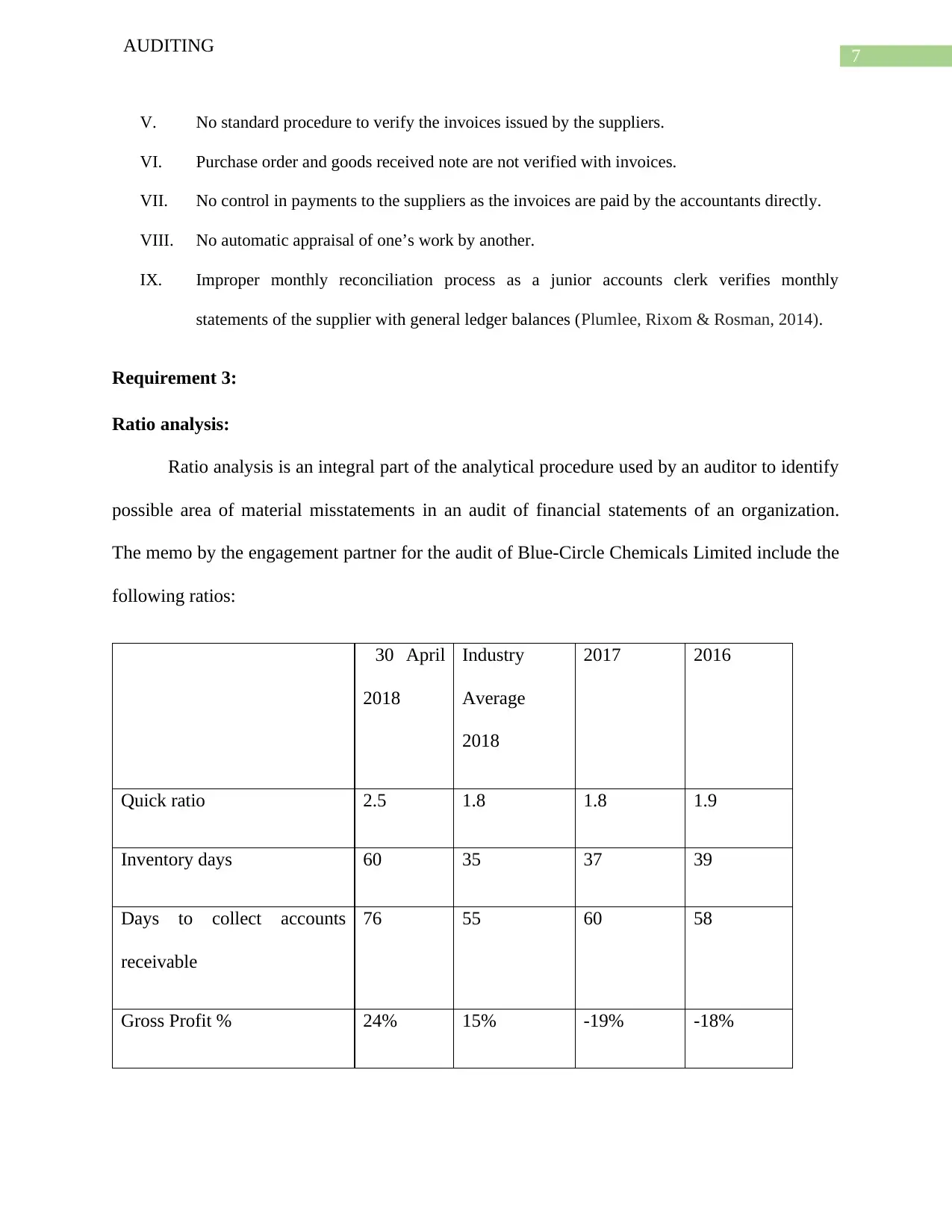

Ratio analysis:

Ratio analysis is an integral part of the analytical procedure used by an auditor to identify

possible area of material misstatements in an audit of financial statements of an organization.

The memo by the engagement partner for the audit of Blue-Circle Chemicals Limited include the

following ratios:

30 April

2018

Industry

Average

2018

2017 2016

Quick ratio 2.5 1.8 1.8 1.9

Inventory days 60 35 37 39

Days to collect accounts

receivable

76 55 60 58

Gross Profit % 24% 15% -19% -18%

AUDITING

V. No standard procedure to verify the invoices issued by the suppliers.

VI. Purchase order and goods received note are not verified with invoices.

VII. No control in payments to the suppliers as the invoices are paid by the accountants directly.

VIII. No automatic appraisal of one’s work by another.

IX. Improper monthly reconciliation process as a junior accounts clerk verifies monthly

statements of the supplier with general ledger balances (Plumlee, Rixom & Rosman, 2014).

Requirement 3:

Ratio analysis:

Ratio analysis is an integral part of the analytical procedure used by an auditor to identify

possible area of material misstatements in an audit of financial statements of an organization.

The memo by the engagement partner for the audit of Blue-Circle Chemicals Limited include the

following ratios:

30 April

2018

Industry

Average

2018

2017 2016

Quick ratio 2.5 1.8 1.8 1.9

Inventory days 60 35 37 39

Days to collect accounts

receivable

76 55 60 58

Gross Profit % 24% 15% -19% -18%

8

AUDITING

A simple analysis of the above ratios will explain how these ratios have changed and the effects

of such change on the financial performance and position.

Quick ratio: Calculated by dividing the current assets less inventories of an organization with its

current liabilities, quick ratio shows the ability of a company to pay off its current liabilities by

using its liquid assets. Quick ratio as on 30th April, 2018 of Blue-Circle Chemicals Limited with

2.5 has improved from 1.8 of 2017 and 1.9 of 2016 (Arens, Elder, Beasley & Jones, 2015).

Inventory days: The ability of an organization to use its inventories in revenue generation is

showed in inventory turnover ratio. Inventory turnover days of 60 in 2018 is a clear indication of

deterioration in the company’s ability to use its inventories in revenue generation. As in 2017

company was turning its inventory into sales with 37days as compared to 60 days it has taken for

the period ending on April 30, 2018.

Days to collect accounts receivable: Days to collect account receivable shows the efficiency of

an organization in collecting its receivables from customers. Days to collect accounts receivable

of the company has also deteriorated with 76 days in the period ending on April 30, 2018 as

compared to 60 days needed in 2017 to collect its accounts receivable (Plumlee, Rixom &

Rosman, 2014).

Gross profit: Gross profit ratio indicates the ability of an organization to earn gross profit from

its revenue. It is calculated by dividing the gross profit with the amount of sales. The gross profit

ratio of 24% indicates a huge improvement in the ability of the company to earn profit from its

business operations as compared to negative (19%) and (18%) in 2017 and 2016 respectively.

AUDITING

A simple analysis of the above ratios will explain how these ratios have changed and the effects

of such change on the financial performance and position.

Quick ratio: Calculated by dividing the current assets less inventories of an organization with its

current liabilities, quick ratio shows the ability of a company to pay off its current liabilities by

using its liquid assets. Quick ratio as on 30th April, 2018 of Blue-Circle Chemicals Limited with

2.5 has improved from 1.8 of 2017 and 1.9 of 2016 (Arens, Elder, Beasley & Jones, 2015).

Inventory days: The ability of an organization to use its inventories in revenue generation is

showed in inventory turnover ratio. Inventory turnover days of 60 in 2018 is a clear indication of

deterioration in the company’s ability to use its inventories in revenue generation. As in 2017

company was turning its inventory into sales with 37days as compared to 60 days it has taken for

the period ending on April 30, 2018.

Days to collect accounts receivable: Days to collect account receivable shows the efficiency of

an organization in collecting its receivables from customers. Days to collect accounts receivable

of the company has also deteriorated with 76 days in the period ending on April 30, 2018 as

compared to 60 days needed in 2017 to collect its accounts receivable (Plumlee, Rixom &

Rosman, 2014).

Gross profit: Gross profit ratio indicates the ability of an organization to earn gross profit from

its revenue. It is calculated by dividing the gross profit with the amount of sales. The gross profit

ratio of 24% indicates a huge improvement in the ability of the company to earn profit from its

business operations as compared to negative (19%) and (18%) in 2017 and 2016 respectively.

You're viewing a preview

Unlock full access by subscribing today!

9

AUDITING

Follow up audit procedures:

Quick ratio: The current assets of the company shall evaluated to ensure these have been

valued correctly. The auditor must verify the inventory valuation technique used by the company

to ensure it is correctly reflecting the value of inventories in the books of accounts of the

company.

Inventory days: Whether the amount of revenue correctly recorded and the value of inventory

has been correctly reflected in the books of accounts. The inventory valuation technique shall

also be evaluated to ensure it reflects true value of inventories at the end of a period.

Days to collect account receivable: Whether the credit sales have been correctly recorded in the

books of accounts of the company must be verified by the auditor. The accounts receivable

collected has been correctly recorded in the books of accounts or not should be checked by the

auditor.

Gross profit ratio: The huge improvement in gross profit ratio of the company despite

deterioration in inventory turnover days and accounts receivable collection days is a quite

surprising. The cost of goods sold recorded by the company must be verified by the auditor to

ensure the expenditures have been recorded correctly in the books of accounts of the company.

Whether sales have been inflated in the books of accounts must also be checked and verified by

the auditor.

AUDITING

Follow up audit procedures:

Quick ratio: The current assets of the company shall evaluated to ensure these have been

valued correctly. The auditor must verify the inventory valuation technique used by the company

to ensure it is correctly reflecting the value of inventories in the books of accounts of the

company.

Inventory days: Whether the amount of revenue correctly recorded and the value of inventory

has been correctly reflected in the books of accounts. The inventory valuation technique shall

also be evaluated to ensure it reflects true value of inventories at the end of a period.

Days to collect account receivable: Whether the credit sales have been correctly recorded in the

books of accounts of the company must be verified by the auditor. The accounts receivable

collected has been correctly recorded in the books of accounts or not should be checked by the

auditor.

Gross profit ratio: The huge improvement in gross profit ratio of the company despite

deterioration in inventory turnover days and accounts receivable collection days is a quite

surprising. The cost of goods sold recorded by the company must be verified by the auditor to

ensure the expenditures have been recorded correctly in the books of accounts of the company.

Whether sales have been inflated in the books of accounts must also be checked and verified by

the auditor.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10

AUDITING

AUDITING

11

AUDITING

References:

Arens, A. A., Elder, R. J., Beasley, M. S., & Jones, J. (2015). Auditing: The Art and Science

of Assurance Engagements. Pearson Canada.

Backof, A., Bowlin, K., & Goodson, B. (2017). The impact of proposed changes to the content

of the audit report on jurors’ assessments of auditor negligence.

Bahr, N. J. (2014). System safety engineering and risk assessment: a practical approach. CRC

Press.

Bailey, C., Collins, D. L., & Abbott, L. J. (2017). The Impact of Enterprise Risk Management on

the Audit Process: Evidence from Audit Fees and Audit Delay. Auditing: A Journal of

Practice & Theory, 37(3), 25-46.

Cao, M., Chychyla, R., & Stewart, T. (2015). Big Data analytics in financial statement

audits. Accounting Horizons, 29(2), 423-429.

Chan, D. Y., & Vasarhelyi, M. A. (2018). Innovation and practice of continuous auditing.

In Continuous Auditing: Theory and Application (pp. 271-283). Emerald Publishing

Limited.

Chou, D. C. (2015). Cloud computing risk and audit issues. Computer Standards &

Interfaces, 42, 137-142.

Christ, M. H., Masli, A., Sharp, N. Y., & Wood, D. A. (2015). Rotational internal audit programs

and financial reporting quality: Do compensating controls help?. Accounting,

Organizations and Society, 44, 37-59.

AUDITING

References:

Arens, A. A., Elder, R. J., Beasley, M. S., & Jones, J. (2015). Auditing: The Art and Science

of Assurance Engagements. Pearson Canada.

Backof, A., Bowlin, K., & Goodson, B. (2017). The impact of proposed changes to the content

of the audit report on jurors’ assessments of auditor negligence.

Bahr, N. J. (2014). System safety engineering and risk assessment: a practical approach. CRC

Press.

Bailey, C., Collins, D. L., & Abbott, L. J. (2017). The Impact of Enterprise Risk Management on

the Audit Process: Evidence from Audit Fees and Audit Delay. Auditing: A Journal of

Practice & Theory, 37(3), 25-46.

Cao, M., Chychyla, R., & Stewart, T. (2015). Big Data analytics in financial statement

audits. Accounting Horizons, 29(2), 423-429.

Chan, D. Y., & Vasarhelyi, M. A. (2018). Innovation and practice of continuous auditing.

In Continuous Auditing: Theory and Application (pp. 271-283). Emerald Publishing

Limited.

Chou, D. C. (2015). Cloud computing risk and audit issues. Computer Standards &

Interfaces, 42, 137-142.

Christ, M. H., Masli, A., Sharp, N. Y., & Wood, D. A. (2015). Rotational internal audit programs

and financial reporting quality: Do compensating controls help?. Accounting,

Organizations and Society, 44, 37-59.

You're viewing a preview

Unlock full access by subscribing today!

12

AUDITING

Graham, L., Bedard, J. C., & Dutta, S. (2018). Managing group audit risk in a multicomponent

audit setting. International Journal of Auditing, 22(1), 40-54.

Hines, C. S., Masli, A., Mauldin, E. G., & Peters, G. F. (2015). Board risk committees and audit

pricing. Auditing: A Journal of Practice & Theory, 34(4), 59-84.

Knechel, W. R., & Salterio, S. E. (2016). Auditing: Assurance and risk. Routledge.

Louwers, T. J., Ramsay, R. J., Sinason, D. H., Strawser, J. R., & Thibodeau, J. C.

(2015). Auditing & assurance services. McGraw-Hill Education.

Plumlee, R. D., Rixom, B. A., & Rosman, A. J. (2014). Training auditors to perform analytical

procedures using metacognitive skills. The Accounting Review, 90(1), 351-369.

Ruhnke, K., & Schmidt, M. (2014). Misstatements in financial statements: The relationship

between inherent and control risk factors and audit adjustments. Auditing: A Journal of

Practice & Theory, 33(4), 247-269.

AUDITING

Graham, L., Bedard, J. C., & Dutta, S. (2018). Managing group audit risk in a multicomponent

audit setting. International Journal of Auditing, 22(1), 40-54.

Hines, C. S., Masli, A., Mauldin, E. G., & Peters, G. F. (2015). Board risk committees and audit

pricing. Auditing: A Journal of Practice & Theory, 34(4), 59-84.

Knechel, W. R., & Salterio, S. E. (2016). Auditing: Assurance and risk. Routledge.

Louwers, T. J., Ramsay, R. J., Sinason, D. H., Strawser, J. R., & Thibodeau, J. C.

(2015). Auditing & assurance services. McGraw-Hill Education.

Plumlee, R. D., Rixom, B. A., & Rosman, A. J. (2014). Training auditors to perform analytical

procedures using metacognitive skills. The Accounting Review, 90(1), 351-369.

Ruhnke, K., & Schmidt, M. (2014). Misstatements in financial statements: The relationship

between inherent and control risk factors and audit adjustments. Auditing: A Journal of

Practice & Theory, 33(4), 247-269.

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.