Internal and Statutory Audit : Report

Added on 2020-07-22

13 Pages3744 Words82 Views

Auditing

Table of ContentsINTRODUCTION...........................................................................................................................1AUDITING......................................................................................................................................1TASK 1............................................................................................................................................11. Difference in internal and statutory Audit..........................................................................12. External and internal auditors role.....................................................................................23. Internal auditors limitations................................................................................................24. Liabilities of auditors in different situations......................................................................3TASK 2............................................................................................................................................3Problem 1................................................................................................................................3Problem 2................................................................................................................................4ADVANCE ACCOUNTING...........................................................................................................5TASK 1: consolidated income statement...............................................................................5FINANCIAL STATEMENTS ANALYSIS....................................................................................6TASK 1............................................................................................................................................61..............................................................................................................................................62..............................................................................................................................................73..............................................................................................................................................74..............................................................................................................................................75..............................................................................................................................................76..............................................................................................................................................77..............................................................................................................................................78..............................................................................................................................................89..............................................................................................................................................810............................................................................................................................................8TASK 2............................................................................................................................................9Case 1: condition of supplier..................................................................................................9Case 2: measures to overcome decline in sales......................................................................9Case 3: measure to make timely payment of bills..................................................................9CONCLUSION................................................................................................................................9REFERENCES..............................................................................................................................10

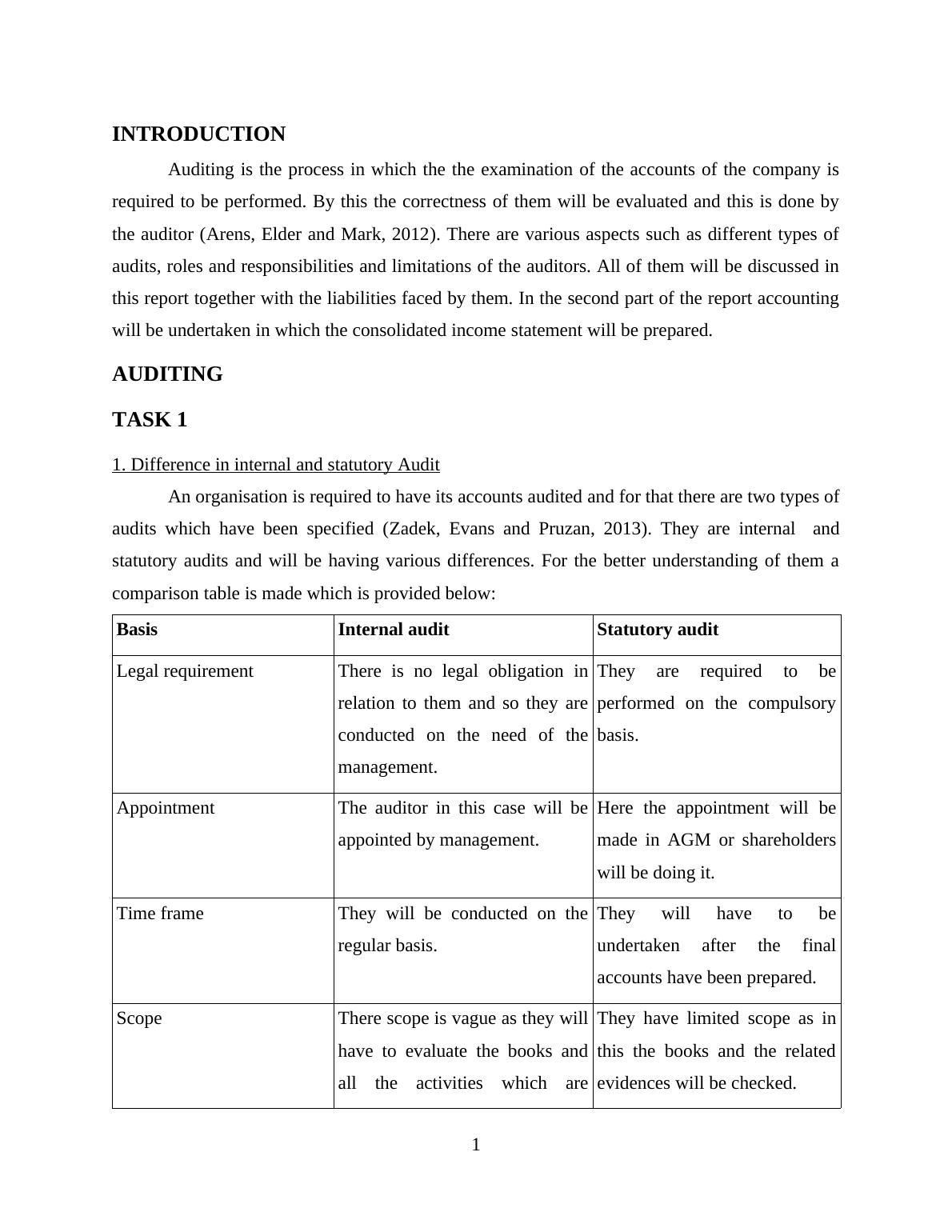

INTRODUCTIONAuditing is the process in which the the examination of the accounts of the company isrequired to be performed. By this the correctness of them will be evaluated and this is done bythe auditor (Arens, Elder and Mark, 2012). There are various aspects such as different types ofaudits, roles and responsibilities and limitations of the auditors. All of them will be discussed inthis report together with the liabilities faced by them. In the second part of the report accountingwill be undertaken in which the consolidated income statement will be prepared.AUDITINGTASK 11. Difference in internal and statutory AuditAn organisation is required to have its accounts audited and for that there are two types ofaudits which have been specified (Zadek, Evans and Pruzan, 2013). They are internal andstatutory audits and will be having various differences. For the better understanding of them acomparison table is made which is provided below:Basis Internal audit Statutory auditLegal requirementThere is no legal obligation inrelation to them and so they areconducted on the need of themanagement.They are required to beperformed on the compulsorybasis. Appointment The auditor in this case will beappointed by management.Here the appointment will bemade in AGM or shareholderswill be doing it.Time frameThey will be conducted on theregular basis.They will have to beundertaken after the finalaccounts have been prepared.ScopeThere scope is vague as they willhave to evaluate the books andall the activities which arecarried out in an organisation.They have limited scope as inthis the books and the relatedevidences will be checked.Remuneration It will be decided by theShareholders will be the ones1

End of preview

Want to access all the pages? Upload your documents or become a member.

Related Documents

Assurance And Auditing Service Reportlg...

|6

|1700

|19

Director's Report and Financial Statementslg...

|21

|2079

|10

Accounting System and Auditing Introductory Introductionlg...

|14

|4942

|432

Assignment on Strategic Financial Statement Analysislg...

|6

|1035

|309

Assignment on Managing Financial Resourcelg...

|12

|3404

|167

AAA Model Ethical Decision Makinglg...

|13

|2919

|452