Ask a question from expert

Audit (telecommunication) - Assignment

17 Pages4860 Words153 Views

Added on 2020-12-09

Audit (telecommunication) - Assignment

Added on 2020-12-09

BookmarkShareRelated Documents

AUDITING PROJECT

TABLE OF CONTENTSINTRODUCTION...........................................................................................................................11. Selecting ASX listed company ..........................................................................................12. Understanding of the nature of the entity in particular industry and identifying key businessrisks.........................................................................................................................................13. Performing analytical procedures of financial statements of using ratio analysis and trendanalysis over the past three years...........................................................................................34. Explaining material account balances and calculated materiality for planning purposes andjustification.............................................................................................................................65., 6., 7. 8. Selecting ten account balances, listing assertions for items and designingcomprehensive set of audit work steps for material account balances with appropriateevidence. Including sampling plan for testing each item of material account balances ........7CONCLUSION..............................................................................................................................14REFERENCES..............................................................................................................................14

INTRODUCTIONAuditing means to analyse the financial position of an organisation through systematicand independence examination of books of account of business. This is carried out to check theauthenticity and determination of any misrepresentation or misstatement of any transaction infinancial record of firm. In the present report auditing of listed telecommunication company ZIPTEL is conducted. In this report key business risk related with the firm are anticipated and factoreffecting both inherent and control risk are discussed. For determination of financialperformance of business ratio analysis is carried out. Material information from the financialrecord and accounts are found out and their relevancy with organisational performance ispresented. 1. Selecting ASX listed company 2. Understanding of the nature of the entity in particular industry and identifying key businessrisks.ZipTel Ltd is engaged in telecommunication sector which is the highest revenuegenerating one for Australian economy leading to growth of overall nation in the best possiblemanner. The nature of business entity is that it provides mobile SIM cards and internet dataservices which help to attain profits. It can be interpreted from the financial reports that from lastthree years ie 2014, 2015 and 2016, organisation is not able to earn profits and huge losses aresuffered. The key business risks are market risk, liquidity risk and credit risks. Risk managementprogram has been implemented in order to focus on unpredictability of financial markets and tominimise these threats. However, derivatives are not being used by company. Market risk is based on Foreign Exchange risk and cash flow and fair value interest raterisks. ZipTel Ltd has short-term nature of cash and cash equivalents (CCE) bearing interest rates.It can be analysed that due to its nature, interest rates are not vital at this time and risk is low.Credit risk is termed as a type of risk where counter party will default on making its payments tocompany and substantial loss will occur (Jespersen and Hasle, 2017). Liquidity risk on the partof company are low as counterparties are banks having high credit risks and as such, risk is low.3. Performing analytical procedures of financial statements of using ratio analysis and trendanalysis over the past three yearsParticularsFormula2016201520141

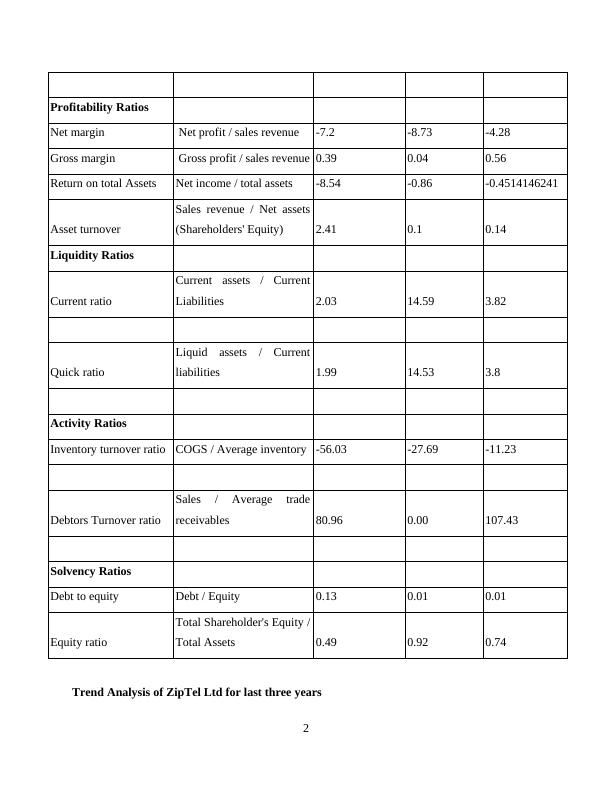

Profitability RatiosNet marginNet profit / sales revenue-7.2-8.73-4.28Gross marginGross profit / sales revenue0.390.040.56Return on total AssetsNet income / total assets-8.54-0.86-0.4514146241Asset turnoverSales revenue / Net assets(Shareholders' Equity)2.410.10.14Liquidity RatiosCurrent ratioCurrent assets / CurrentLiabilities2.0314.593.82Quick ratioLiquid assets / Currentliabilities1.9914.533.8Activity RatiosInventory turnover ratioCOGS / Average inventory-56.03-27.69-11.23Debtors Turnover ratioSales / Average tradereceivables80.960.00107.43Solvency RatiosDebt to equityDebt / Equity0.130.010.01Equity ratioTotal Shareholder's Equity /Total Assets0.490.920.74Trend Analysis of ZipTel Ltd for last three years2

End of preview

Want to access all the pages? Upload your documents or become a member.

Related Documents

Developing an Audit Program for a Selected Publically Listed Companylg...

|14

|3881

|108

Developing an Audit Program for Mako Gold Limitedlg...

|20

|985

|58

Audit Program for Ridley Corporation Limited - ATPlg...

|17

|3860

|144

Developing an Audit Program for a Publically Listed Companylg...

|20

|3755

|254

Developing An Audit Program Assignmentlg...

|21

|4058

|12

Auditing Theory and Practicelg...

|13

|3870

|117