Auditing Theory and Practice Report: Alizarin Enterprises Analysis

VerifiedAdded on 2020/03/16

|11

|1954

|202

Report

AI Summary

This report presents an analysis of auditing theory and practice, focusing on the financial statements of Alizarin Enterprises for the years ending March 31, 2016, and June 30, 2015. The report includes an income statement and balance sheet, along with a comparative analysis of key financial figures....

Running head: AUDITING THEORY AND PRACTICE

Auditing theory and practice

Name of the student

Name of the university

Author note

Auditing theory and practice

Name of the student

Name of the university

Author note

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1AUDITING THEORY AND PRACTICE

Table of Contents

Income statement of Alizarin enterprises for two years.............................................................2

Balance sheet of Alizarin Enterprises........................................................................................3

Analysis......................................................................................................................................4

Reference....................................................................................................................................7

Table of Contents

Income statement of Alizarin enterprises for two years.............................................................2

Balance sheet of Alizarin Enterprises........................................................................................3

Analysis......................................................................................................................................4

Reference....................................................................................................................................7

2AUDITING THEORY AND PRACTICE

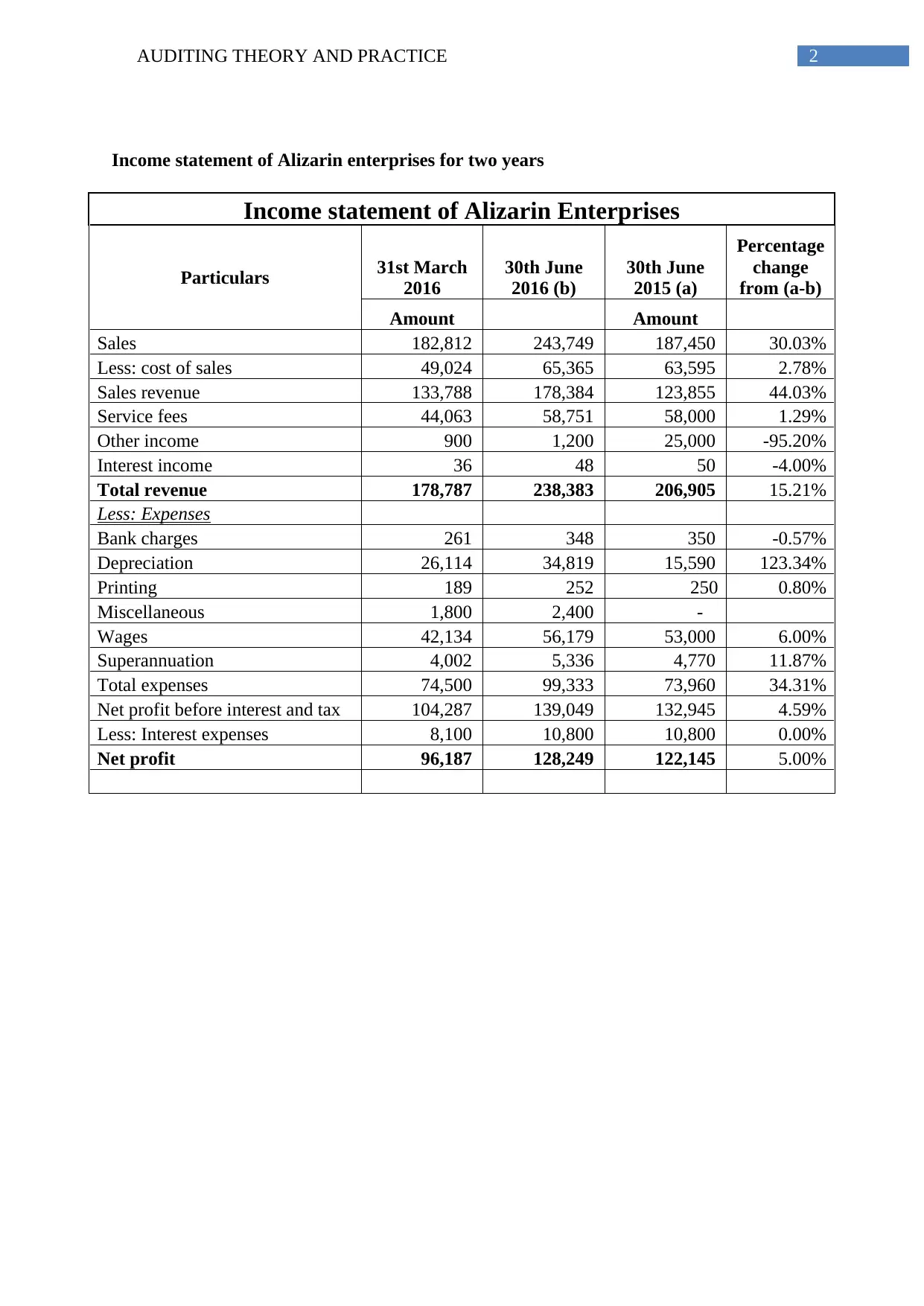

Income statement of Alizarin enterprises for two years

Income statement of Alizarin Enterprises

Particulars 31st March

2016

30th June

2016 (b)

30th June

2015 (a)

Percentage

change

from (a-b)

Amount Amount

Sales 182,812 243,749 187,450 30.03%

Less: cost of sales 49,024 65,365 63,595 2.78%

Sales revenue 133,788 178,384 123,855 44.03%

Service fees 44,063 58,751 58,000 1.29%

Other income 900 1,200 25,000 -95.20%

Interest income 36 48 50 -4.00%

Total revenue 178,787 238,383 206,905 15.21%

Less: Expenses

Bank charges 261 348 350 -0.57%

Depreciation 26,114 34,819 15,590 123.34%

Printing 189 252 250 0.80%

Miscellaneous 1,800 2,400 -

Wages 42,134 56,179 53,000 6.00%

Superannuation 4,002 5,336 4,770 11.87%

Total expenses 74,500 99,333 73,960 34.31%

Net profit before interest and tax 104,287 139,049 132,945 4.59%

Less: Interest expenses 8,100 10,800 10,800 0.00%

Net profit 96,187 128,249 122,145 5.00%

Income statement of Alizarin enterprises for two years

Income statement of Alizarin Enterprises

Particulars 31st March

2016

30th June

2016 (b)

30th June

2015 (a)

Percentage

change

from (a-b)

Amount Amount

Sales 182,812 243,749 187,450 30.03%

Less: cost of sales 49,024 65,365 63,595 2.78%

Sales revenue 133,788 178,384 123,855 44.03%

Service fees 44,063 58,751 58,000 1.29%

Other income 900 1,200 25,000 -95.20%

Interest income 36 48 50 -4.00%

Total revenue 178,787 238,383 206,905 15.21%

Less: Expenses

Bank charges 261 348 350 -0.57%

Depreciation 26,114 34,819 15,590 123.34%

Printing 189 252 250 0.80%

Miscellaneous 1,800 2,400 -

Wages 42,134 56,179 53,000 6.00%

Superannuation 4,002 5,336 4,770 11.87%

Total expenses 74,500 99,333 73,960 34.31%

Net profit before interest and tax 104,287 139,049 132,945 4.59%

Less: Interest expenses 8,100 10,800 10,800 0.00%

Net profit 96,187 128,249 122,145 5.00%

You're viewing a preview

Unlock full access by subscribing today!

3AUDITING THEORY AND PRACTICE

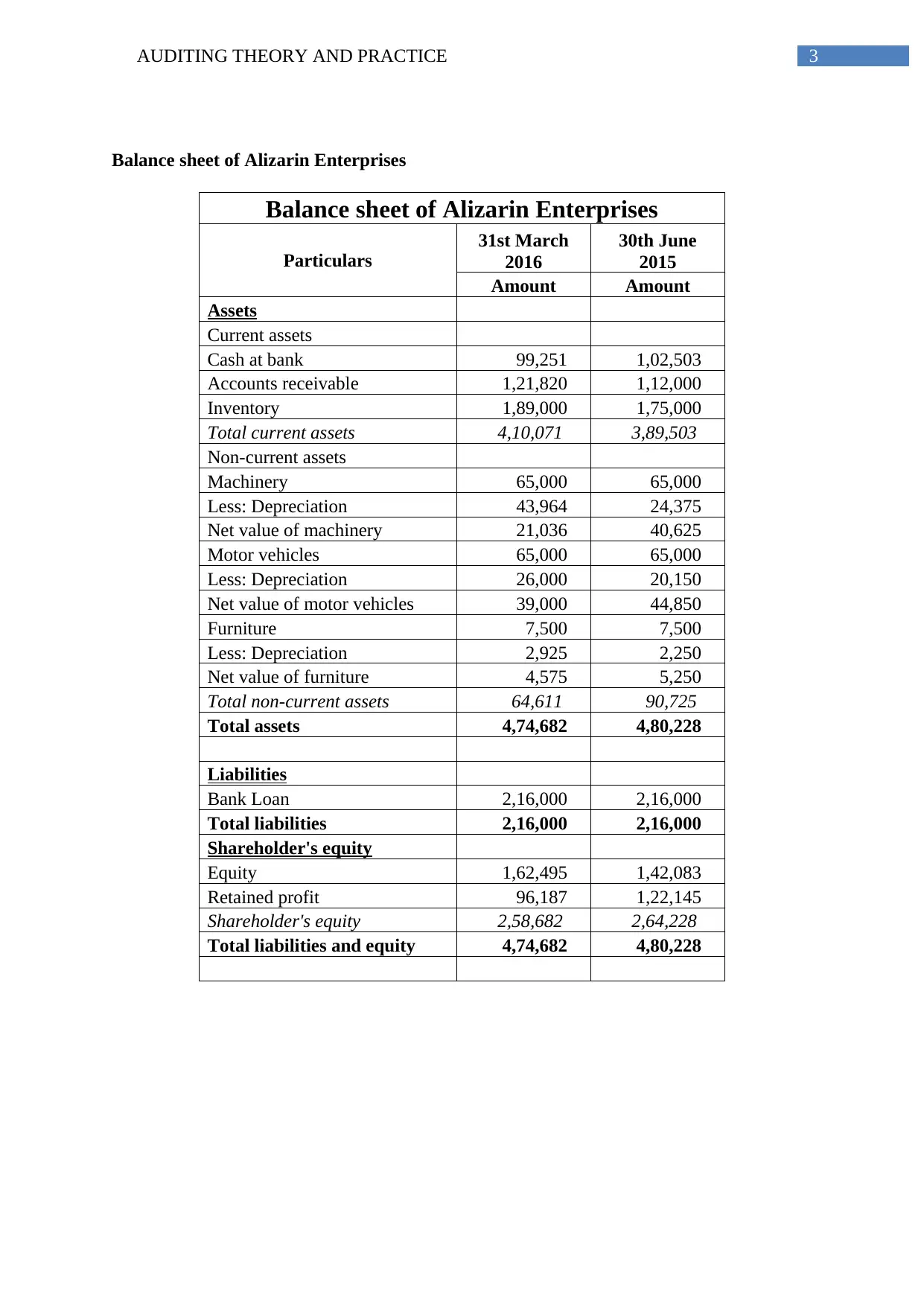

Balance sheet of Alizarin Enterprises

Balance sheet of Alizarin Enterprises

Particulars

31st March

2016

30th June

2015

Amount Amount

Assets

Current assets

Cash at bank 99,251 1,02,503

Accounts receivable 1,21,820 1,12,000

Inventory 1,89,000 1,75,000

Total current assets 4,10,071 3,89,503

Non-current assets

Machinery 65,000 65,000

Less: Depreciation 43,964 24,375

Net value of machinery 21,036 40,625

Motor vehicles 65,000 65,000

Less: Depreciation 26,000 20,150

Net value of motor vehicles 39,000 44,850

Furniture 7,500 7,500

Less: Depreciation 2,925 2,250

Net value of furniture 4,575 5,250

Total non-current assets 64,611 90,725

Total assets 4,74,682 4,80,228

Liabilities

Bank Loan 2,16,000 2,16,000

Total liabilities 2,16,000 2,16,000

Shareholder's equity

Equity 1,62,495 1,42,083

Retained profit 96,187 1,22,145

Shareholder's equity 2,58,682 2,64,228

Total liabilities and equity 4,74,682 4,80,228

Balance sheet of Alizarin Enterprises

Balance sheet of Alizarin Enterprises

Particulars

31st March

2016

30th June

2015

Amount Amount

Assets

Current assets

Cash at bank 99,251 1,02,503

Accounts receivable 1,21,820 1,12,000

Inventory 1,89,000 1,75,000

Total current assets 4,10,071 3,89,503

Non-current assets

Machinery 65,000 65,000

Less: Depreciation 43,964 24,375

Net value of machinery 21,036 40,625

Motor vehicles 65,000 65,000

Less: Depreciation 26,000 20,150

Net value of motor vehicles 39,000 44,850

Furniture 7,500 7,500

Less: Depreciation 2,925 2,250

Net value of furniture 4,575 5,250

Total non-current assets 64,611 90,725

Total assets 4,74,682 4,80,228

Liabilities

Bank Loan 2,16,000 2,16,000

Total liabilities 2,16,000 2,16,000

Shareholder's equity

Equity 1,62,495 1,42,083

Retained profit 96,187 1,22,145

Shareholder's equity 2,58,682 2,64,228

Total liabilities and equity 4,74,682 4,80,228

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4AUDITING THEORY AND PRACTICE

Analysis

1.0 Audit planning

Audit planning is an integral part of the audit procedure to identify the risk associated

segments and efficiently perform the audit. Planning of the audit involves establishment of

the overall strategies for audit to develop and engage the audit plan that specifically includes

the assessment procedure for planned risk and the planned responses for the risks associated

with the material misstatement (Titera 2013). Audit plan is not the distinct phase of the audit

rather it is the iterative and continuous procedure that immediately starts after completion of

the previous audit and it continues till the current audit’s completion.

1.1 Analytical review

This is the procedure for auditing financial statement and it helps the auditor to

identify the changes in the client’s business. It is compulsory for the auditor to perform the

procedure of risk assessment to assess and identify the material misstatement risk at assertion

and financial statement level and the procedure of risk assessment involves the analytical

procedure. It is compulsory on the part of the auditor that they shall perform the analytical

procedure towards the end of the audit process that will analyse whether financial statement

of the client is in consistent with the understanding of the audit (Moroney and Trotman

2016).

1.2 preliminary judgement for materiality

It is forecasted and identified at the financial statement level and is knows as planning

for materiality. The supervision and planning requires the auditor under the audit planning to

consider his preliminary judgement regarding the materiality levels for the purpose of audit.

While planning the audit, auditor must use her or his preliminary judgement with regard to

Analysis

1.0 Audit planning

Audit planning is an integral part of the audit procedure to identify the risk associated

segments and efficiently perform the audit. Planning of the audit involves establishment of

the overall strategies for audit to develop and engage the audit plan that specifically includes

the assessment procedure for planned risk and the planned responses for the risks associated

with the material misstatement (Titera 2013). Audit plan is not the distinct phase of the audit

rather it is the iterative and continuous procedure that immediately starts after completion of

the previous audit and it continues till the current audit’s completion.

1.1 Analytical review

This is the procedure for auditing financial statement and it helps the auditor to

identify the changes in the client’s business. It is compulsory for the auditor to perform the

procedure of risk assessment to assess and identify the material misstatement risk at assertion

and financial statement level and the procedure of risk assessment involves the analytical

procedure. It is compulsory on the part of the auditor that they shall perform the analytical

procedure towards the end of the audit process that will analyse whether financial statement

of the client is in consistent with the understanding of the audit (Moroney and Trotman

2016).

1.2 preliminary judgement for materiality

It is forecasted and identified at the financial statement level and is knows as planning

for materiality. The supervision and planning requires the auditor under the audit planning to

consider his preliminary judgement regarding the materiality levels for the purpose of audit.

While planning the audit, auditor must use her or his preliminary judgement with regard to

5AUDITING THEORY AND PRACTICE

materiality in such a way that can be forecasted to be delivered under the inherent limitation

of auditing procedure (Anugerah, Sari and Frostiana 2014). The preliminary judgement of the

auditor with regard to the materiality may be drawn on the basis of annualized interim of the

financial statement of company for one or more prior period.

2.0 1st account – Other income

2.1 Rational – the income became significantly lower and it is identified that the income from

other sources has been reduced by 95.20%. It was further recognized that that the total

revenue of the company during 2015 involves a significant amount from other income.

2.2 Assertion – there may be likelihood of fraud to suppress the income from various sources

to record the income at lower amount than actual (Moeller 2013).

2.3 Recommended procedure – the auditor shall go through the records regarding the other

income for the previous year and match it with the other income sources for the current year

documents related to other income shall be verified. It must be analysed that from which

sources income has been reduced or stopped and the justification behind that. Moreover, the

auditor may carry on the analytical procedure to check it there was any opportunity for

earning from other sources that may have been lost or not availed by the company and the

reason behind that.

3.0 2nd account – Depreciation

3.1 Rational – amount of depreciation significantly went up by 123.34% in 2016 as compared

to 2015, through there were no new purchases found from the balance sheet of the company.

3.2 Assertion – chances are there that the depreciation are overcharged to show less profit in

the current year or with a motive to show more profit in the future years (Boritz, Kochetova-

Kozloski and Robinson 2014).

materiality in such a way that can be forecasted to be delivered under the inherent limitation

of auditing procedure (Anugerah, Sari and Frostiana 2014). The preliminary judgement of the

auditor with regard to the materiality may be drawn on the basis of annualized interim of the

financial statement of company for one or more prior period.

2.0 1st account – Other income

2.1 Rational – the income became significantly lower and it is identified that the income from

other sources has been reduced by 95.20%. It was further recognized that that the total

revenue of the company during 2015 involves a significant amount from other income.

2.2 Assertion – there may be likelihood of fraud to suppress the income from various sources

to record the income at lower amount than actual (Moeller 2013).

2.3 Recommended procedure – the auditor shall go through the records regarding the other

income for the previous year and match it with the other income sources for the current year

documents related to other income shall be verified. It must be analysed that from which

sources income has been reduced or stopped and the justification behind that. Moreover, the

auditor may carry on the analytical procedure to check it there was any opportunity for

earning from other sources that may have been lost or not availed by the company and the

reason behind that.

3.0 2nd account – Depreciation

3.1 Rational – amount of depreciation significantly went up by 123.34% in 2016 as compared

to 2015, through there were no new purchases found from the balance sheet of the company.

3.2 Assertion – chances are there that the depreciation are overcharged to show less profit in

the current year or with a motive to show more profit in the future years (Boritz, Kochetova-

Kozloski and Robinson 2014).

You're viewing a preview

Unlock full access by subscribing today!

6AUDITING THEORY AND PRACTICE

3.3 Recommended procedure – the documents related to fixed assets, their useful life,

existence and method of depreciation shall be verified. The auditor shall also verify the

impairment and revaluation to assess the value of the assets for the purpose of depreciation. If

there is change in the method of depreciation, the related documents for that shall also be

verified to analyse the appropriateness. Moreover the rate of depreciation on each asset and

each asset’s useful life shall be verified.

4.0 3rd Account – Miscellaneous expenses

4.1 Rational – the miscellaneous expenditure taken place during 2016 whereas during 2015

there were no such expenses

4.2 Assertion – there is the likelihood of frauds as the expenses may be fictitious and the

management may have shown the fictitious expenses to reduce the profit level.

4.3 Recommended procedure – the receipts and vouchers related to miscellaneous expenses

shall be verified properly. The appropriateness of the expenses shall also be verified. Further,

it shall also be verified that whether the payment for the expenses were properly authorized

by the appropriate authority or not.

5.0 4th Account – Wages

5.1 Rational – wages paid for the year ended 2016 were almost 6% higher as compared to

2015.

5.2 Assertion – fraud may be involved there as payments may be charged against revenue for

fictitious employees (Brown-Liburd, Issa and Lombardi 2015)

5.3 Recommended procedure – Employee details and payment must be verified with

employee register and payment register. The auditor shall also verify whether there is any

3.3 Recommended procedure – the documents related to fixed assets, their useful life,

existence and method of depreciation shall be verified. The auditor shall also verify the

impairment and revaluation to assess the value of the assets for the purpose of depreciation. If

there is change in the method of depreciation, the related documents for that shall also be

verified to analyse the appropriateness. Moreover the rate of depreciation on each asset and

each asset’s useful life shall be verified.

4.0 3rd Account – Miscellaneous expenses

4.1 Rational – the miscellaneous expenditure taken place during 2016 whereas during 2015

there were no such expenses

4.2 Assertion – there is the likelihood of frauds as the expenses may be fictitious and the

management may have shown the fictitious expenses to reduce the profit level.

4.3 Recommended procedure – the receipts and vouchers related to miscellaneous expenses

shall be verified properly. The appropriateness of the expenses shall also be verified. Further,

it shall also be verified that whether the payment for the expenses were properly authorized

by the appropriate authority or not.

5.0 4th Account – Wages

5.1 Rational – wages paid for the year ended 2016 were almost 6% higher as compared to

2015.

5.2 Assertion – fraud may be involved there as payments may be charged against revenue for

fictitious employees (Brown-Liburd, Issa and Lombardi 2015)

5.3 Recommended procedure – Employee details and payment must be verified with

employee register and payment register. The auditor shall also verify whether there is any

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7AUDITING THEORY AND PRACTICE

arrears of wages that were paid during the year and whether the wages paid to the number of

employees matches with the number of employees under the employee registrar.

6.0 5th Account – Cash at bank

6.1 Rational – Cash is susceptible to fraud, error, misstatement and embezzlement

6.2 Assertion – cash may be recorded at lower amount or all the cash may not be transferred

to bank account

6.3 Recommended procedure – all the transactions related to cash and bank reconciliation

statement must be verified. The payment of cash made along with the voucher shall be

verified. The auditor shall also investigate whether the payment is recorded at time of making

the payment or on accrued basis. With regard to the receipt of cash, the auditor shall verify

whether the cash is transferred to the bank immediately or it is transferred on periodic basis.

If the cash is transferred on periodic basis then the method of keeping the cash and its

authorization shall be verified.

7.0 6th Account – account receivable

7.1 Rational – It represents whether the company is efficient in collecting its dues as the

inefficiency will increase the risk of bad-debts.

7.2 Assertion – there is a likelihood of fraud regarding revealing the amount of receivables.

7.3 Recommended procedure – All the sales related transactions, debtor’s information; credit

period allowed shall be verified. The auditor shall prepare a list of the debtors whose payment

is due even after the credit period got over and the reasons of failure to make payment by the

defaulters must be found out. As the amount of receivable is increased in 2016 as compared

arrears of wages that were paid during the year and whether the wages paid to the number of

employees matches with the number of employees under the employee registrar.

6.0 5th Account – Cash at bank

6.1 Rational – Cash is susceptible to fraud, error, misstatement and embezzlement

6.2 Assertion – cash may be recorded at lower amount or all the cash may not be transferred

to bank account

6.3 Recommended procedure – all the transactions related to cash and bank reconciliation

statement must be verified. The payment of cash made along with the voucher shall be

verified. The auditor shall also investigate whether the payment is recorded at time of making

the payment or on accrued basis. With regard to the receipt of cash, the auditor shall verify

whether the cash is transferred to the bank immediately or it is transferred on periodic basis.

If the cash is transferred on periodic basis then the method of keeping the cash and its

authorization shall be verified.

7.0 6th Account – account receivable

7.1 Rational – It represents whether the company is efficient in collecting its dues as the

inefficiency will increase the risk of bad-debts.

7.2 Assertion – there is a likelihood of fraud regarding revealing the amount of receivables.

7.3 Recommended procedure – All the sales related transactions, debtor’s information; credit

period allowed shall be verified. The auditor shall prepare a list of the debtors whose payment

is due even after the credit period got over and the reasons of failure to make payment by the

defaulters must be found out. As the amount of receivable is increased in 2016 as compared

8AUDITING THEORY AND PRACTICE

to 2015, the auditor shall find out the reason as increase in the credit sales or increase in the

dues.

8.0 7th Account – Inventory

8.1 Rational – Inventory is an important item that is included under the asset of the company

and it is susceptible to fraud, error, misstatement and theft (Jans, Alles and Vasarhelyi 2014)

8.2 Assertion – inventory valuation may not be made on the basis of cost or fair value,

whichever lower (Arens et al. 2016).

8.3 Recommended procedure – valuation of inventory and physical stock count must be

carried out. The method of inventory valuation and whether the company is using the method

consistently throughout the year shall be verified. Further, if there is any change in the

valuation method the justification and appropriateness for that must be identified. The

physical stock of the inventory shall be matched with the inventory registrar.

to 2015, the auditor shall find out the reason as increase in the credit sales or increase in the

dues.

8.0 7th Account – Inventory

8.1 Rational – Inventory is an important item that is included under the asset of the company

and it is susceptible to fraud, error, misstatement and theft (Jans, Alles and Vasarhelyi 2014)

8.2 Assertion – inventory valuation may not be made on the basis of cost or fair value,

whichever lower (Arens et al. 2016).

8.3 Recommended procedure – valuation of inventory and physical stock count must be

carried out. The method of inventory valuation and whether the company is using the method

consistently throughout the year shall be verified. Further, if there is any change in the

valuation method the justification and appropriateness for that must be identified. The

physical stock of the inventory shall be matched with the inventory registrar.

You're viewing a preview

Unlock full access by subscribing today!

9AUDITING THEORY AND PRACTICE

Reference

Anugerah, R., Sari, R.N. and Frostiana, R.M., 2014. The relationship between ethics,

expertise, audit experience, fraud risk assessment and audit situational factors on auditor

professional scepticism.

Arens, A.A., Elder, R.J., Beasley, M.S. and Hogan, C.E., 2016. Auditing and assurance

services. Pearson.

Boritz, J.E., Kochetova-Kozloski, N. and Robinson, L., 2014. Are fraud specialists relatively

more effective than auditors at modifying audit programs in the presence of fraud risk?. The

Accounting Review, 90(3), pp.881-915.

Brown-Liburd, H., Issa, H. and Lombardi, D., 2015. Behavioral implications of Big Data's

impact on audit judgment and decision making and future research directions. Accounting

Horizons, 29(2), pp.451-468.

Jans, M., Alles, M.G. and Vasarhelyi, M.A., 2014. A field study on the use of process mining

of event logs as an analytical procedure in auditing. The Accounting Review, 89(5), pp.1751-

1773.

Moeller, R.R., 2013. Role of Internal Audit in Enterprise Risk Management. COSO

Enterprise Risk Management: Establishing Effective Governance, Risk, and Compliance

Processes, Second Edition, pp.247-266.

Moroney, R. and Trotman, K.T., 2016. Differences in Auditors' Materiality Assessments

When Auditing Financial Statements and Sustainability Reports. Contemporary Accounting

Research, 33(2), pp.551-575.

Reference

Anugerah, R., Sari, R.N. and Frostiana, R.M., 2014. The relationship between ethics,

expertise, audit experience, fraud risk assessment and audit situational factors on auditor

professional scepticism.

Arens, A.A., Elder, R.J., Beasley, M.S. and Hogan, C.E., 2016. Auditing and assurance

services. Pearson.

Boritz, J.E., Kochetova-Kozloski, N. and Robinson, L., 2014. Are fraud specialists relatively

more effective than auditors at modifying audit programs in the presence of fraud risk?. The

Accounting Review, 90(3), pp.881-915.

Brown-Liburd, H., Issa, H. and Lombardi, D., 2015. Behavioral implications of Big Data's

impact on audit judgment and decision making and future research directions. Accounting

Horizons, 29(2), pp.451-468.

Jans, M., Alles, M.G. and Vasarhelyi, M.A., 2014. A field study on the use of process mining

of event logs as an analytical procedure in auditing. The Accounting Review, 89(5), pp.1751-

1773.

Moeller, R.R., 2013. Role of Internal Audit in Enterprise Risk Management. COSO

Enterprise Risk Management: Establishing Effective Governance, Risk, and Compliance

Processes, Second Edition, pp.247-266.

Moroney, R. and Trotman, K.T., 2016. Differences in Auditors' Materiality Assessments

When Auditing Financial Statements and Sustainability Reports. Contemporary Accounting

Research, 33(2), pp.551-575.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10AUDITING THEORY AND PRACTICE

Titera, W.R., 2013. Updating audit standard—Enabling audit data analysis. Journal of

Information Systems, 27(1), pp.325-331.

Titera, W.R., 2013. Updating audit standard—Enabling audit data analysis. Journal of

Information Systems, 27(1), pp.325-331.

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.