Auditing Theory and Practice: Internal Control and Recommendations

VerifiedAdded on 2023/06/04

|11

|2244

|207

Report

AI Summary

This report provides a detailed analysis of auditing theory and practice, with a specific focus on internal control mechanisms within business entities, particularly small businesses. It explores how internal control components are adjusted by management to prevent fraud and errors, highlighting the advantages and disadvantages of these adjustments. The report includes a case study of "Hello World," offering recommendations for internal control solutions across various departments, such as accounting and cash management, emphasizing the importance of segregation of duties and regular reconciliation. Furthermore, a management letter is presented, underscoring the significance of internal control policies in safeguarding business assets, promoting better management, and ensuring accurate financial reporting.

Running head: AUDITING THEORY AND PRACTICE

Auditing Theory and Practice

Name of the Student

Name of the University

Authors Note

Course ID

Auditing Theory and Practice

Name of the Student

Name of the University

Authors Note

Course ID

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1AUDITING THEORY AND PRACTICE

Table of Contents

Answer to question A:................................................................................................................2

Answer to Question B:...............................................................................................................4

Answer to question C:................................................................................................................6

References:.................................................................................................................................8

Table of Contents

Answer to question A:................................................................................................................2

Answer to Question B:...............................................................................................................4

Answer to question C:................................................................................................................6

References:.................................................................................................................................8

2AUDITING THEORY AND PRACTICE

Answer to question A:

Regardless of the business size, all the business entities are vulnerable to frauds

particularly the small business entities are victimized in the larger percentage of situations.

As stated by Stewart and Shamdasani (2014) the components of internal control mainly

consists of the inter-related components that are treated as the criteria in determining and

attaining the effective internal control system. The components of internal control are derived

by the corresponding management style and philosophy that are different from the entities

and are attached with the process of management. The components of internal control are

adjusted by the management in most often situations to meet the needs of the small entities

(Chan and Vasarhelyi 2018). This includes undertaking a directive approach towards

attaining the desired outcome with the clear direction and strong drive by the management of

small entities to achieve their objective. The components of internal control are adjusted in a

manner that it is related to the higher level directions with positive arrangement of

encouraging the employees.

The management of companies often direct the internal control components that are

designed to make an attempt towards preventing the undesirable violations or situations that

leads to the irregular activities and occurrence of fraud (Hayes, Gortemaker and Wallage

2014). In other words, the management of small entities designs the internal control policies

in order to avoid the loss or damage with an attempt of minimizing the risk. Management

often applies the preventive control in their regular work of employees in compliance with

the differences in the functions and accountabilities such that the division of responsibilities

and obligations with mutual supervision and validity of work is maintained (De Paula 2016).

The internal control components are adjusted by the small entities in manner that it is able to

identify and recognize the errors that may occur in the daily business activities.

Answer to question A:

Regardless of the business size, all the business entities are vulnerable to frauds

particularly the small business entities are victimized in the larger percentage of situations.

As stated by Stewart and Shamdasani (2014) the components of internal control mainly

consists of the inter-related components that are treated as the criteria in determining and

attaining the effective internal control system. The components of internal control are derived

by the corresponding management style and philosophy that are different from the entities

and are attached with the process of management. The components of internal control are

adjusted by the management in most often situations to meet the needs of the small entities

(Chan and Vasarhelyi 2018). This includes undertaking a directive approach towards

attaining the desired outcome with the clear direction and strong drive by the management of

small entities to achieve their objective. The components of internal control are adjusted in a

manner that it is related to the higher level directions with positive arrangement of

encouraging the employees.

The management of companies often direct the internal control components that are

designed to make an attempt towards preventing the undesirable violations or situations that

leads to the irregular activities and occurrence of fraud (Hayes, Gortemaker and Wallage

2014). In other words, the management of small entities designs the internal control policies

in order to avoid the loss or damage with an attempt of minimizing the risk. Management

often applies the preventive control in their regular work of employees in compliance with

the differences in the functions and accountabilities such that the division of responsibilities

and obligations with mutual supervision and validity of work is maintained (De Paula 2016).

The internal control components are adjusted by the small entities in manner that it is able to

identify and recognize the errors that may occur in the daily business activities.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3AUDITING THEORY AND PRACTICE

Adjusting the components of internal control results in positive consequences and also

advantageous in keeping a positive flow of internal controls (Louwers et al. 2015). The

advantages are as follows;

a. Better communication: The documents that are well written not only helps in getting

the message across the organization but also helps in building the picture of the

culture and procedure that are created to assure that the small entities meet their aims

and objectives.

b. Reduction in Error: Adjusting the internal control according to the needs of the

small entities helps in minimizing the errors and saves time and resources for small

entities (Kumar and Sharma 2015). The internal control helps in making sure that the

information of business is correct and the employees are responsible for their

activities.

c. Protection and Authorisation: Adjusting the internal control components as per the

needs of the small entities helps in providing comfort to the work force provided that

they act in a manner that is prescribed by the internal controls and inside the limits of

authorization (Cook, Van Bommel and Turnhout 2016). The business would not be

able to blame its staff given that they have discharged their responsibilities in good

faith and inside the specified guidelines.

Apart from the advantages of the internal control there are certain disadvantages that

are related with internal control;

a. Error in Judgement: All the business genuinely remain dependent on the number of

procedure and honesty. There may instances where small business are faced with dis-

honest people. Owners must be thorough in scrutinizing the probable employees the

records of employments and holding conversation with the previous employees

Adjusting the components of internal control results in positive consequences and also

advantageous in keeping a positive flow of internal controls (Louwers et al. 2015). The

advantages are as follows;

a. Better communication: The documents that are well written not only helps in getting

the message across the organization but also helps in building the picture of the

culture and procedure that are created to assure that the small entities meet their aims

and objectives.

b. Reduction in Error: Adjusting the internal control according to the needs of the

small entities helps in minimizing the errors and saves time and resources for small

entities (Kumar and Sharma 2015). The internal control helps in making sure that the

information of business is correct and the employees are responsible for their

activities.

c. Protection and Authorisation: Adjusting the internal control components as per the

needs of the small entities helps in providing comfort to the work force provided that

they act in a manner that is prescribed by the internal controls and inside the limits of

authorization (Cook, Van Bommel and Turnhout 2016). The business would not be

able to blame its staff given that they have discharged their responsibilities in good

faith and inside the specified guidelines.

Apart from the advantages of the internal control there are certain disadvantages that

are related with internal control;

a. Error in Judgement: All the business genuinely remain dependent on the number of

procedure and honesty. There may instances where small business are faced with dis-

honest people. Owners must be thorough in scrutinizing the probable employees the

records of employments and holding conversation with the previous employees

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4AUDITING THEORY AND PRACTICE

(Vovchenko et al. 2017). Financial stress, dissatisfaction can result people in

perverting the rules.

b. Management Override: Management and workforce might in certain situations

consider internal control as the red tape, needless and wastage of time (Li et al. 2015).

In small business, staffs are regularly found in tight budgets and would be tempted to

cut the corners. As a result, people may override the internal control for their personal

benefit and make an attempt of defrauding the business.

c. Collusion: Adjusting the internal control according to the needs of small business

may result in collusion (Lisic et al. 2016). This generally happens when two or more

people come together in an attempt to defraud. Collusion is treated as difficult to

defeat in small business.

Findings from the studies have suggested that poor internal control and override of

internal control might result in business frauds. Therefore, strong internal control system

would act as the best policy in protecting the small business from every type of fraud.

Answer to Question B:

Findings from the case study suggest that the current accounting practice of Hello

World initially involves recognition of importance of proper and adequate accounting system

for the company. The accountants are found to be taking information depending upon the

accounting records and documents or the summary of accounts voucher so that the

accountants can enter data into the computer system. Based on the understanding of the

current accounting practice at Hello World several suggestion can be made for the internal

control solutions based on the major functions of departments.

Recommendations for Accounting Department:

(Vovchenko et al. 2017). Financial stress, dissatisfaction can result people in

perverting the rules.

b. Management Override: Management and workforce might in certain situations

consider internal control as the red tape, needless and wastage of time (Li et al. 2015).

In small business, staffs are regularly found in tight budgets and would be tempted to

cut the corners. As a result, people may override the internal control for their personal

benefit and make an attempt of defrauding the business.

c. Collusion: Adjusting the internal control according to the needs of small business

may result in collusion (Lisic et al. 2016). This generally happens when two or more

people come together in an attempt to defraud. Collusion is treated as difficult to

defeat in small business.

Findings from the studies have suggested that poor internal control and override of

internal control might result in business frauds. Therefore, strong internal control system

would act as the best policy in protecting the small business from every type of fraud.

Answer to Question B:

Findings from the case study suggest that the current accounting practice of Hello

World initially involves recognition of importance of proper and adequate accounting system

for the company. The accountants are found to be taking information depending upon the

accounting records and documents or the summary of accounts voucher so that the

accountants can enter data into the computer system. Based on the understanding of the

current accounting practice at Hello World several suggestion can be made for the internal

control solutions based on the major functions of departments.

Recommendations for Accounting Department:

5AUDITING THEORY AND PRACTICE

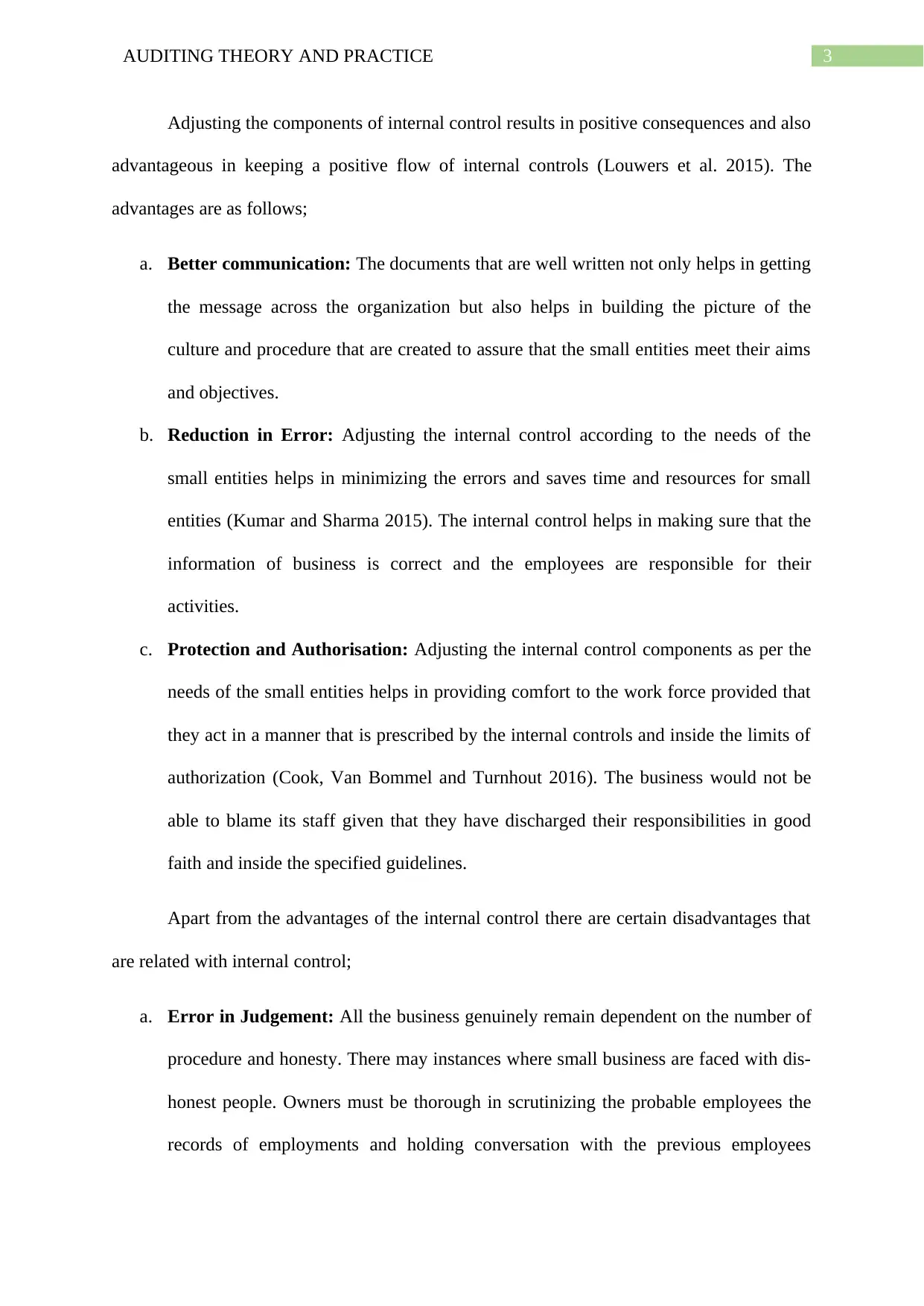

Segregation of duties can be regarded as the most preferred and effective process of

implementing control activities at the Hello World. This activity can be treated of

fundamental importance at Hello World because financial fraudulent subject is increasingly

turning out to be serious issue. If Hello World takes the advantage and implement the

preventive activity control in their computer accounting system then they prevent in advance

several misappropriate management of cash and asset. Based on the principle of segregation

of duties the related financial activities should be conducted by different people.

Figure 1: Figure representing Segregation of Duties to be conducted at Hello World

(Source: As Created by Author)

Cash Accounting: Findings suggest that the cash management and numerous accounting

data is only managed by one person who later delegates the duty to sub-ordinates. It is

necessary that segregation of duties must be done where one person cannot be held

responsible for accounting records (Clinton, Pinello and Skaife 2014). A review and

oversight on cash account should be made. Furthermore, it is recommended that each

transaction with cash must be documented by the appropriate form and signature of the cash

manager.

Segregation of duties can be regarded as the most preferred and effective process of

implementing control activities at the Hello World. This activity can be treated of

fundamental importance at Hello World because financial fraudulent subject is increasingly

turning out to be serious issue. If Hello World takes the advantage and implement the

preventive activity control in their computer accounting system then they prevent in advance

several misappropriate management of cash and asset. Based on the principle of segregation

of duties the related financial activities should be conducted by different people.

Figure 1: Figure representing Segregation of Duties to be conducted at Hello World

(Source: As Created by Author)

Cash Accounting: Findings suggest that the cash management and numerous accounting

data is only managed by one person who later delegates the duty to sub-ordinates. It is

necessary that segregation of duties must be done where one person cannot be held

responsible for accounting records (Clinton, Pinello and Skaife 2014). A review and

oversight on cash account should be made. Furthermore, it is recommended that each

transaction with cash must be documented by the appropriate form and signature of the cash

manager.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6AUDITING THEORY AND PRACTICE

Accounts receivable: The segregation of duties must be made at Hello World as accounts

receivable significantly vulnerable to fraud. The board of directors and the accounting

managers must review the reports relating to the collection, billings and writing offs. Such

activities would empower the manager to keep a check on the cash flow and forewarn the

directors regarding any unofficial write offs. The system of order must be control correctly

under the approval of the accounting manager.

Accounting reconciliation and analysis: Following the access control and description of

job, accounting reconciliation and analysis is regarded as the third most vital group of the

basic controls. One of the vital ingredients of successful frauds is the successful concealment.

It is recommended that the regular, corrective accounting reconciliation and analysis would

make the concealment difficult or impossible (Demirakos 2018). Performing of accounting

reconciliation on the monthly basis should be carried out by the board of directors in the areas

of bank reconciliation for the accounts.

The board of directors should also review and oversight the accounts receivable

reconciliation from month to month and the general ledger to sub-ledger. A review should

also be conducted by the board of directors in the areas of accounts payable reconciliation for

both month to month and the general ledger to sub-ledger. Therefore, such procedure can be

helpful in highlighting the discrepancies that results in misappropriate of accounts and cash.

Answer to question C:

Management Letter

To Tim and Abi Scott

From ABC Consultants

Date: 16-10-2018

Accounts receivable: The segregation of duties must be made at Hello World as accounts

receivable significantly vulnerable to fraud. The board of directors and the accounting

managers must review the reports relating to the collection, billings and writing offs. Such

activities would empower the manager to keep a check on the cash flow and forewarn the

directors regarding any unofficial write offs. The system of order must be control correctly

under the approval of the accounting manager.

Accounting reconciliation and analysis: Following the access control and description of

job, accounting reconciliation and analysis is regarded as the third most vital group of the

basic controls. One of the vital ingredients of successful frauds is the successful concealment.

It is recommended that the regular, corrective accounting reconciliation and analysis would

make the concealment difficult or impossible (Demirakos 2018). Performing of accounting

reconciliation on the monthly basis should be carried out by the board of directors in the areas

of bank reconciliation for the accounts.

The board of directors should also review and oversight the accounts receivable

reconciliation from month to month and the general ledger to sub-ledger. A review should

also be conducted by the board of directors in the areas of accounts payable reconciliation for

both month to month and the general ledger to sub-ledger. Therefore, such procedure can be

helpful in highlighting the discrepancies that results in misappropriate of accounts and cash.

Answer to question C:

Management Letter

To Tim and Abi Scott

From ABC Consultants

Date: 16-10-2018

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7AUDITING THEORY AND PRACTICE

Dear Tim and Abi

We wish seek your valuation attention towards our letter relating to the

importance of having internal control at Hello World. The internal control acts as the filter

throughout the entire business. The internal control policies are helpful in aligning with the

objectives of business and helps in making sure that the process of reporting that are carried

out at Hello World are in accordance with the objective of business. Having internal control

policies at Hello World would help in safeguarding the business assets as the system makes

sure that physical and monetary assets are safeguarded from fraud and errors of

misjudgement.

The internal control policies not only detect frauds and error but also helps in

promoting better management. Having internal control policies at Hello World would ensure

that systems recognize any error quickly as and when they occur. Apart from this, the internal

control policies would allow the managers to receive the appropriate information in the

timely manner regarding the performance of any target along with the vital figure than reflect

variations from the target.

The internal control policies helps in minimising the chances of unanticipated errors

at Hello World. Implementing the internal control at Hello World would ensure segregation

of duties and appropriate financial reporting. As understood maintenance of accurate and

complete reports is usually required by the legislation and management. Therefore, the

application of internal control policy would help the management in minimising the lost time

of correcting the errors and making sure that the resources of the business are effectively

managed.

We anticipate that the letter has served your purpose of implementing the internal

control policies and look forward to hear from you soon.

Dear Tim and Abi

We wish seek your valuation attention towards our letter relating to the

importance of having internal control at Hello World. The internal control acts as the filter

throughout the entire business. The internal control policies are helpful in aligning with the

objectives of business and helps in making sure that the process of reporting that are carried

out at Hello World are in accordance with the objective of business. Having internal control

policies at Hello World would help in safeguarding the business assets as the system makes

sure that physical and monetary assets are safeguarded from fraud and errors of

misjudgement.

The internal control policies not only detect frauds and error but also helps in

promoting better management. Having internal control policies at Hello World would ensure

that systems recognize any error quickly as and when they occur. Apart from this, the internal

control policies would allow the managers to receive the appropriate information in the

timely manner regarding the performance of any target along with the vital figure than reflect

variations from the target.

The internal control policies helps in minimising the chances of unanticipated errors

at Hello World. Implementing the internal control at Hello World would ensure segregation

of duties and appropriate financial reporting. As understood maintenance of accurate and

complete reports is usually required by the legislation and management. Therefore, the

application of internal control policy would help the management in minimising the lost time

of correcting the errors and making sure that the resources of the business are effectively

managed.

We anticipate that the letter has served your purpose of implementing the internal

control policies and look forward to hear from you soon.

8AUDITING THEORY AND PRACTICE

Thank You

Thank You

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9AUDITING THEORY AND PRACTICE

References:

Chan, D.Y. and Vasarhelyi, M.A., 2018. Innovation and practice of continuous auditing.

In Continuous Auditing: Theory and Application (pp. 271-283). Emerald Publishing Limited.

Clinton, S.B., Pinello, A.S. and Skaife, H.A., 2014. The implications of ineffective internal

control and SOX 404 reporting for financial analysts. Journal of Accounting and Public

Policy, 33(4), pp.303-327.

Cook, W., Van Bommel, S. and Turnhout, E., 2016. Inside environmental auditing:

effectiveness, objectivity, and transparency. Current Opinion in Environmental

Sustainability, 18, pp.33-39.

De Paula, F.R.M., 2016. The principles of auditing a practical manual for students and

practitioners. Isaac Pitman & Sons, Ltd (1919).

Demirakos, E., 2018. Internal Auditing: Assurance and Advisory Services, UL Anderson, MJ

Head, S. Ramamoorti, C. Riddle, M. Salamasick, PJ Sobel, The Internal Audit Foundation

(2017), 627 pages, $199.99, ISBN: 978-0-89413-987-1.

Hayes, R.S., Gortemaker, H. and Wallage, P., 2014. Principles of auditing: an introduction

to international standards on auditing. Prentice Hall, Financial Times.

Kumar, R. and Sharma, V., 2015. Auditing: Principles and practice. PHI Learning Pvt. Ltd..

Li, C., Raman, K.K., Sun, L. and Wu, D., 2015. The SOX 404 internal control audit: Key

regulatory events. Research in Accounting Regulation, 27(2), pp.160-164.

Lisic, L.L., Neal, T.L., Zhang, I.X. and Zhang, Y., 2016. CEO power, internal control quality,

and audit committee effectiveness in substance versus in form. Contemporary Accounting

Research, 33(3), pp.1199-1237.

References:

Chan, D.Y. and Vasarhelyi, M.A., 2018. Innovation and practice of continuous auditing.

In Continuous Auditing: Theory and Application (pp. 271-283). Emerald Publishing Limited.

Clinton, S.B., Pinello, A.S. and Skaife, H.A., 2014. The implications of ineffective internal

control and SOX 404 reporting for financial analysts. Journal of Accounting and Public

Policy, 33(4), pp.303-327.

Cook, W., Van Bommel, S. and Turnhout, E., 2016. Inside environmental auditing:

effectiveness, objectivity, and transparency. Current Opinion in Environmental

Sustainability, 18, pp.33-39.

De Paula, F.R.M., 2016. The principles of auditing a practical manual for students and

practitioners. Isaac Pitman & Sons, Ltd (1919).

Demirakos, E., 2018. Internal Auditing: Assurance and Advisory Services, UL Anderson, MJ

Head, S. Ramamoorti, C. Riddle, M. Salamasick, PJ Sobel, The Internal Audit Foundation

(2017), 627 pages, $199.99, ISBN: 978-0-89413-987-1.

Hayes, R.S., Gortemaker, H. and Wallage, P., 2014. Principles of auditing: an introduction

to international standards on auditing. Prentice Hall, Financial Times.

Kumar, R. and Sharma, V., 2015. Auditing: Principles and practice. PHI Learning Pvt. Ltd..

Li, C., Raman, K.K., Sun, L. and Wu, D., 2015. The SOX 404 internal control audit: Key

regulatory events. Research in Accounting Regulation, 27(2), pp.160-164.

Lisic, L.L., Neal, T.L., Zhang, I.X. and Zhang, Y., 2016. CEO power, internal control quality,

and audit committee effectiveness in substance versus in form. Contemporary Accounting

Research, 33(3), pp.1199-1237.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10AUDITING THEORY AND PRACTICE

Louwers, T.J., Ramsay, R.J., Sinason, D.H., Strawser, J.R. and Thibodeau, J.C.,

2015. Auditing & assurance services. McGraw-Hill Education.

Stewart, D.W. and Shamdasani, P.N., 2014. Focus groups: Theory and practice (Vol. 20).

Sage publications.

Vovchenko, G.N., Holina, G.M., Orobinskiy, S.A. and Sichev, A.R., 2017. Ensuring financial

stability of companies on the basis of international experience in construction of risks maps,

internal control and audit. European Research Studies Journal, 20(1), pp.350-368.

Louwers, T.J., Ramsay, R.J., Sinason, D.H., Strawser, J.R. and Thibodeau, J.C.,

2015. Auditing & assurance services. McGraw-Hill Education.

Stewart, D.W. and Shamdasani, P.N., 2014. Focus groups: Theory and practice (Vol. 20).

Sage publications.

Vovchenko, G.N., Holina, G.M., Orobinskiy, S.A. and Sichev, A.R., 2017. Ensuring financial

stability of companies on the basis of international experience in construction of risks maps,

internal control and audit. European Research Studies Journal, 20(1), pp.350-368.

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.