Auditing Theory and Practice

VerifiedAdded on 2023/06/07

|17

|4424

|385

AI Summary

This research paper discusses the importance of independence in auditing and the role of auditors in A-Cap Resources Limited. It evaluates the compliance of the auditor with independence requirements, the presence of non-audit services, and the analysis of auditor's remuneration. It also discusses the evaluation of the audit committee and its various parts, key audit matters, and the responsibilities of directors, managers, and auditors for the preparation of financial statements.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Running head: AUDITING THEORY AND PRACTICE

Auditing Theory and Practice

Auditing Theory and Practice

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

AUDITING THEORY AND PRACTICE

1. Executive Summary

A-Cap Resources Limited is a company, which deals with uranium and coal projects.

Financial statements are made so that the transactions can be done easily. It is important

for the auditor to intervene along with check the financial transactions so that any kind of

misstatements can be easily evaluated and assessed. This project initially explains the

company and its operations. Thus, the research paper revolves around the importance of

independence that the auditor requires so that impartial audit report is attained. After that,

the significant factors associated with the audit is assessed and evaluated so that proper

idea can be obtained relating to the significance that an auditor holds in a company. The

paper ultimately explains the responsibilities of directors, managers, and auditors for the

preparation of financial statements. Thus, the significance of the factor can be derived.

1. Executive Summary

A-Cap Resources Limited is a company, which deals with uranium and coal projects.

Financial statements are made so that the transactions can be done easily. It is important

for the auditor to intervene along with check the financial transactions so that any kind of

misstatements can be easily evaluated and assessed. This project initially explains the

company and its operations. Thus, the research paper revolves around the importance of

independence that the auditor requires so that impartial audit report is attained. After that,

the significant factors associated with the audit is assessed and evaluated so that proper

idea can be obtained relating to the significance that an auditor holds in a company. The

paper ultimately explains the responsibilities of directors, managers, and auditors for the

preparation of financial statements. Thus, the significance of the factor can be derived.

AUDITING THEORY AND PRACTICE

Table of Contents

1. Executive Summary...........................................................................................................................2

3. Introduction.......................................................................................................................................4

4. Discussion..........................................................................................................................................4

4.1. Auditor’s Compliance with Independence Requirements..........................................................4

4.2. Presence and Nature of Any Non-Audit Services........................................................................5

4.3. Analysis of Auditor’s Remuneration In Comparison To the Previous Years................................6

4.4. Related to the Key Audit Matters evaluation of the Audit Procedure........................................6

4.5. Evaluation of Audit committee and its Various Parts..................................................................8

4.6 Type of Audit Opinion................................................................................................................11

4.7. Differences of Auditor’s Responsibilities and Director and Management’s Responsibilities....11

4.8. Presence of any Material Subsequent Events in the Company.................................................12

4.9. Assessment of the Effectiveness of the Material Information..................................................12

4.10. Probability of Missing Any Material Information in the Provided Information.......................12

4.11. The follow-up questions to be asked to the Auditor...............................................................12

5. Conclusion.......................................................................................................................................13

References...........................................................................................................................................14

Bibliography.........................................................................................................................................16

6. Appendix..........................................................................................................................................17

Table of Contents

1. Executive Summary...........................................................................................................................2

3. Introduction.......................................................................................................................................4

4. Discussion..........................................................................................................................................4

4.1. Auditor’s Compliance with Independence Requirements..........................................................4

4.2. Presence and Nature of Any Non-Audit Services........................................................................5

4.3. Analysis of Auditor’s Remuneration In Comparison To the Previous Years................................6

4.4. Related to the Key Audit Matters evaluation of the Audit Procedure........................................6

4.5. Evaluation of Audit committee and its Various Parts..................................................................8

4.6 Type of Audit Opinion................................................................................................................11

4.7. Differences of Auditor’s Responsibilities and Director and Management’s Responsibilities....11

4.8. Presence of any Material Subsequent Events in the Company.................................................12

4.9. Assessment of the Effectiveness of the Material Information..................................................12

4.10. Probability of Missing Any Material Information in the Provided Information.......................12

4.11. The follow-up questions to be asked to the Auditor...............................................................12

5. Conclusion.......................................................................................................................................13

References...........................................................................................................................................14

Bibliography.........................................................................................................................................16

6. Appendix..........................................................................................................................................17

AUDITING THEORY AND PRACTICE

3. Introduction

Assured services of the auditor play an important part in the company’s annual reports, as

they can significantly influence the financial records of the company. An auditor is an

individual, who has the right with respect to conduct audit of the overall financial

statements of a company, which, in turn, assures profits maximization and loss

minimization. In order to pursue an audit of the company, it is necessary for the auditor to

look into the company’s operations, identify the financial statements, which are probably

wrong, and evaluate any occurrences of important events after the preparation of financial

statements. This also includes trying-out whether the company’s internal controls are

efficient, write to the directors informing them about any issues, which are connected with

the audit and chalk out solutions in order to deal with them. It can be well evaluated the

significant role the auditor plays in a company (Gelman, Rosenberg & Freedman, 2018).

A-CAP Resources Limited is located in Botswana and is an ASX listed Resources Company. In

addition, it mainly operates in Botswana country in South Africa. The company has the

status of being funded well by its shareholders. Furthermore, the company majorly

concentrates on the uranium prospect. Moreover, the company also operates in coal

projects. The objective of the research paper is to assess along with summarize the assured

services that are provided by the auditor of A-CAP Resources Limited in the company’s

operations.

4. Discussion

4.1. Auditor’s Compliance with Independence Requirements

The independence declaration of the company’s auditor is observed in the 307C with

respect the Corporations Act 2001. This particular declaration is often perceived to be

3. Introduction

Assured services of the auditor play an important part in the company’s annual reports, as

they can significantly influence the financial records of the company. An auditor is an

individual, who has the right with respect to conduct audit of the overall financial

statements of a company, which, in turn, assures profits maximization and loss

minimization. In order to pursue an audit of the company, it is necessary for the auditor to

look into the company’s operations, identify the financial statements, which are probably

wrong, and evaluate any occurrences of important events after the preparation of financial

statements. This also includes trying-out whether the company’s internal controls are

efficient, write to the directors informing them about any issues, which are connected with

the audit and chalk out solutions in order to deal with them. It can be well evaluated the

significant role the auditor plays in a company (Gelman, Rosenberg & Freedman, 2018).

A-CAP Resources Limited is located in Botswana and is an ASX listed Resources Company. In

addition, it mainly operates in Botswana country in South Africa. The company has the

status of being funded well by its shareholders. Furthermore, the company majorly

concentrates on the uranium prospect. Moreover, the company also operates in coal

projects. The objective of the research paper is to assess along with summarize the assured

services that are provided by the auditor of A-CAP Resources Limited in the company’s

operations.

4. Discussion

4.1. Auditor’s Compliance with Independence Requirements

The independence declaration of the company’s auditor is observed in the 307C with

respect the Corporations Act 2001. This particular declaration is often perceived to be

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

AUDITING THEORY AND PRACTICE

developed by the director of the A-CAP Resources Limited along with its subsidiaries. It

states that there are no instances of infringement relate to the requirement for

independence of the auditor relating to the Corporations Act 2001, which is based on the

context of an audit. Moreover, it is also stated that there are no instances of contraventions

in any applied codes of professional conduct on the basis of audit (A-Cap, 2017).

Over the years, it has been observed that the independence requirements of the auditor

have become important while doing the audit. Additionally, the independence of the

auditor directly affects the quality of the audit. The quality of the audit directs towards their

action of uncovering the breach. In addition, it also helps in directing towards the report of

the breach. Thus, it does not require providence of immense importance to the auditor (Lin

& Tepalagul, n.d.). Thus, any kind of failure in providing the required independence to the

auditor will lead to less or minimal irregularities in the reports observed by the auditor. The

independence of the auditor directs towards the mental attitude in which all the issues,

which are found in the financial statements are reported by remaining unbiased. This also

focuses on seeking all the requirements that are necessary for the wrongs committed.

Hence, it can be understood that it is important for a company to provide the auditor with

the probable independence requirements (Patrick, Vitalis & Mdoom, 2017).

4.2. Presence and Nature of Any Non-Audit Services

Non-audit services signify those professional services, which are provided by a public

accountant during the auditing process that is being conducted within the company. It is

actually not at all connected to evaluate or audit of the financial statements of the

organization (Zhang, Hay & Holm, 2016). In this context, A-CAP Resources Limited provided

developed by the director of the A-CAP Resources Limited along with its subsidiaries. It

states that there are no instances of infringement relate to the requirement for

independence of the auditor relating to the Corporations Act 2001, which is based on the

context of an audit. Moreover, it is also stated that there are no instances of contraventions

in any applied codes of professional conduct on the basis of audit (A-Cap, 2017).

Over the years, it has been observed that the independence requirements of the auditor

have become important while doing the audit. Additionally, the independence of the

auditor directly affects the quality of the audit. The quality of the audit directs towards their

action of uncovering the breach. In addition, it also helps in directing towards the report of

the breach. Thus, it does not require providence of immense importance to the auditor (Lin

& Tepalagul, n.d.). Thus, any kind of failure in providing the required independence to the

auditor will lead to less or minimal irregularities in the reports observed by the auditor. The

independence of the auditor directs towards the mental attitude in which all the issues,

which are found in the financial statements are reported by remaining unbiased. This also

focuses on seeking all the requirements that are necessary for the wrongs committed.

Hence, it can be understood that it is important for a company to provide the auditor with

the probable independence requirements (Patrick, Vitalis & Mdoom, 2017).

4.2. Presence and Nature of Any Non-Audit Services

Non-audit services signify those professional services, which are provided by a public

accountant during the auditing process that is being conducted within the company. It is

actually not at all connected to evaluate or audit of the financial statements of the

organization (Zhang, Hay & Holm, 2016). In this context, A-CAP Resources Limited provided

AUDITING THEORY AND PRACTICE

did not pay a specific fee to any kind of non-audit services to the external auditor, as

recorded in the year 2017.

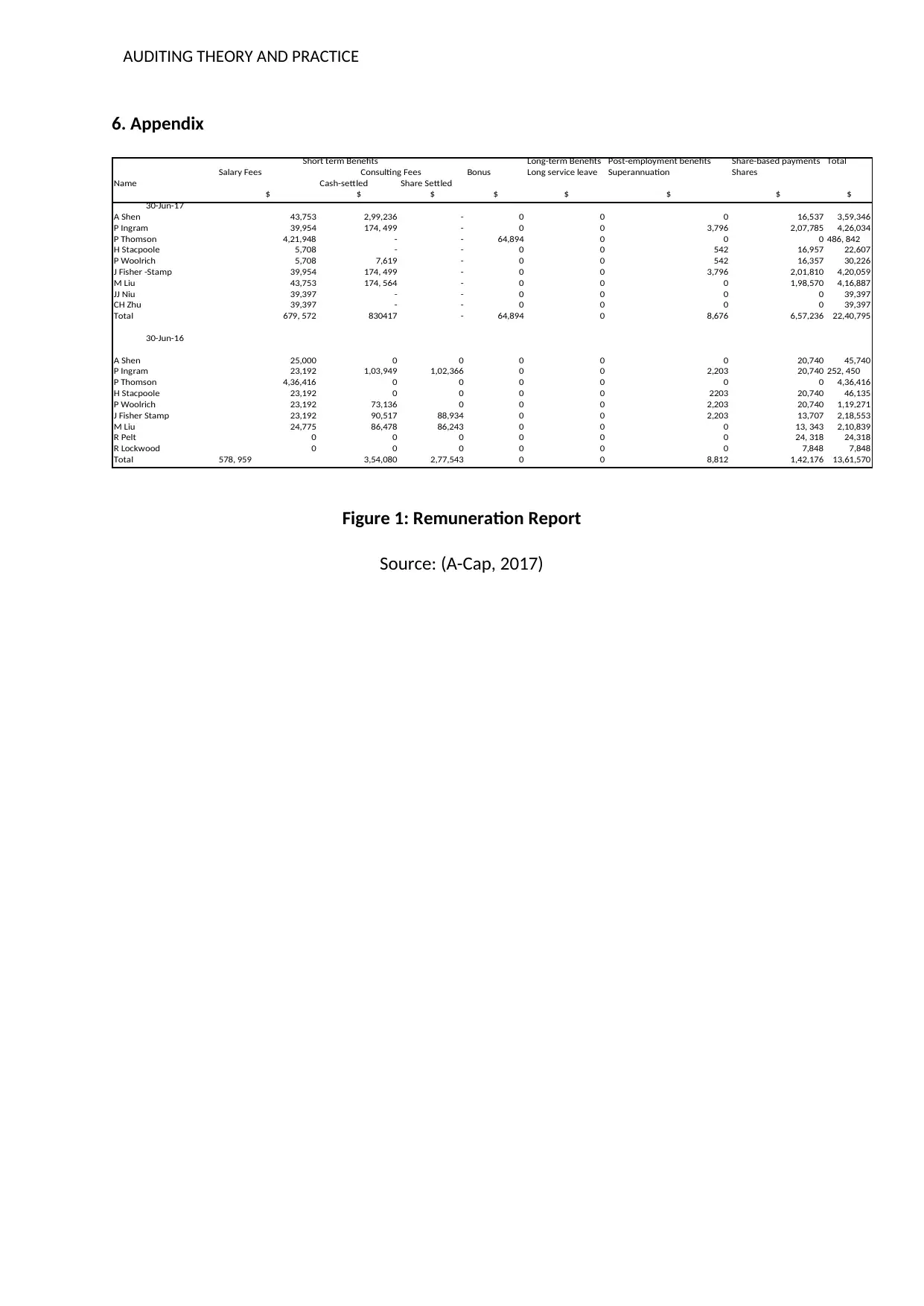

4.3. Analysis of Auditor’s Remuneration In Comparison To the Previous Years

The analysis of remuneration report (refer to appendices, Fig 1), which has been obtained

from the company signifies the percentage change that has taken place between the years

2016 and 2017. The percentage change can be observed from the report is that there is a

difference of $ 879,225 with respect to two years, which explains the increased rate that has

been obtained in terms of remuneration (A-Cap, 2017).

4.4. Key Audit Matters Associated with of the Audit Procedure

Key Audit Matters (KAM) indicates issues, which are of high significance according to a

professional auditor. The inclusion of these matters in an audit report is highly essential to

the financial statements relating to the current period. KAM are chosen from those issues

that are communicated by the individual, who is in charge of the company (Arnold, 2017).

An auditor in order to determine the key audit matters has to bring some factors into

consideration. In this context, it is important to consider key areas, which are often

associated with higher risks or conditions of material misstatement. In addition, the factors

include important judgments of the auditor with respect to the specific areas of financial

statements. This, in turn, includes significant judgment of the management. Moreover, the

areas related to the accounting estimates are observed to be engaged in high risks and

uncertainty. Furthermore, observing the impact that had been initiated by the occurrences

of any kind of events or important transactions, which occurred. The final area is to evaluate

the process utilized for addressing the matter in the audit (Arnold, 2017). A-CAP Resources

Limited abides by the standards of Australian Auditing Standards to ensure that there are no

did not pay a specific fee to any kind of non-audit services to the external auditor, as

recorded in the year 2017.

4.3. Analysis of Auditor’s Remuneration In Comparison To the Previous Years

The analysis of remuneration report (refer to appendices, Fig 1), which has been obtained

from the company signifies the percentage change that has taken place between the years

2016 and 2017. The percentage change can be observed from the report is that there is a

difference of $ 879,225 with respect to two years, which explains the increased rate that has

been obtained in terms of remuneration (A-Cap, 2017).

4.4. Key Audit Matters Associated with of the Audit Procedure

Key Audit Matters (KAM) indicates issues, which are of high significance according to a

professional auditor. The inclusion of these matters in an audit report is highly essential to

the financial statements relating to the current period. KAM are chosen from those issues

that are communicated by the individual, who is in charge of the company (Arnold, 2017).

An auditor in order to determine the key audit matters has to bring some factors into

consideration. In this context, it is important to consider key areas, which are often

associated with higher risks or conditions of material misstatement. In addition, the factors

include important judgments of the auditor with respect to the specific areas of financial

statements. This, in turn, includes significant judgment of the management. Moreover, the

areas related to the accounting estimates are observed to be engaged in high risks and

uncertainty. Furthermore, observing the impact that had been initiated by the occurrences

of any kind of events or important transactions, which occurred. The final area is to evaluate

the process utilized for addressing the matter in the audit (Arnold, 2017). A-CAP Resources

Limited abides by the standards of Australian Auditing Standards to ensure that there are no

AUDITING THEORY AND PRACTICE

possibilities of material misstatements during the audit it is ensured that there is no

presence of it in the final audit report during the audit process. Misstatements in an audit

report can occur due to any kinds of errors or fraud. The most common form of

misstatements is material misstatements. It is observed that this type of error can influence

the economic decisions of the individuals with respect to financial report (A-Cap, 2017).

The company in its audit tries to execute professional judgment along with skepticism. It

also exercises other factors that involve the assessment and identification of the risks, which

are imposed due to the presence of material misstatements. The risks are considered to be

higher if the presence of misstatement is not detected as compared to the risks involved

with the occurrence of the error. Generally, the term fraud signifies forgery,

misinterpretations, omissions, override of the internal control, and collusion. In addition,

evaluation relating to the appropriateness of accounting policies has been implemented.

The audit also tends to check the justification of the accounting estimates, which are

provided by the directors of the company. Additionally, it tries to obtain a precise

understanding relating to the internal control, which is associated with audit so that an

audit procedure can be designed in accordance with the situation. However, all of these are

not performed or executed so that declaration can be made with respect to the company’s

control over its internal operations. Furthermore, the audit of the company evaluates the

overall structure, presentation, along with financial report’s content as well as the

disclosures. The audit of the company tends to check the financial report in order to

understand whether it represents all the underlying transactions and important events. This

has immense importance in the financial presentation. In addition, it acquires the necessary

audit evidence concerning the financial information relating to the activities that occurred in

possibilities of material misstatements during the audit it is ensured that there is no

presence of it in the final audit report during the audit process. Misstatements in an audit

report can occur due to any kinds of errors or fraud. The most common form of

misstatements is material misstatements. It is observed that this type of error can influence

the economic decisions of the individuals with respect to financial report (A-Cap, 2017).

The company in its audit tries to execute professional judgment along with skepticism. It

also exercises other factors that involve the assessment and identification of the risks, which

are imposed due to the presence of material misstatements. The risks are considered to be

higher if the presence of misstatement is not detected as compared to the risks involved

with the occurrence of the error. Generally, the term fraud signifies forgery,

misinterpretations, omissions, override of the internal control, and collusion. In addition,

evaluation relating to the appropriateness of accounting policies has been implemented.

The audit also tends to check the justification of the accounting estimates, which are

provided by the directors of the company. Additionally, it tries to obtain a precise

understanding relating to the internal control, which is associated with audit so that an

audit procedure can be designed in accordance with the situation. However, all of these are

not performed or executed so that declaration can be made with respect to the company’s

control over its internal operations. Furthermore, the audit of the company evaluates the

overall structure, presentation, along with financial report’s content as well as the

disclosures. The audit of the company tends to check the financial report in order to

understand whether it represents all the underlying transactions and important events. This

has immense importance in the financial presentation. In addition, it acquires the necessary

audit evidence concerning the financial information relating to the activities that occurred in

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

AUDITING THEORY AND PRACTICE

the place within the company so that an opinion could be formed relating to the financial

report (A-Cap, 2017).

The Company’s audit report also provides a statement that verifies the fact that the

institution has abided by all the requirements of the auditor’s independence so that there

are no such issues raised against the issue. After informing the directors of the significant

matters, the most significant is determined for a current time period. This indicates the key

audit matters of the company. A-CAP Resources Limited describes the KAM in the report

presented by the auditors does not disclose it until and unless there is an order provided for

doing so. Another situation in which the key audit matters are not included in the report is

when the probable outcomes are adverse in comparison with the benefits provided to the

interest of the public (A-Cap, 2017).

4.5. Evaluation of Audit committee and its Various Parts

A-CAP Resources Limited does have an audit committee. In addition, there are non-

executive directors in the audit committee. This includes John Fisher-Stamp, Chenghu Zhu,

Michael Liu, Henry J. Stacpoole, and Jijing Niu (A-Cap, 2017). In addition, there is an audit

committee charter, which is engaged in designing the roles and responsibilities of the audit

members in a specific way.

Structure of the audit committee members involves a rule, which focuses on stating the

involvement of four members is board of the company. In addition, among all, three will be

independent directors. Among the four members, at least one has to bear the required

experience and qualification for providing proper guidance and insights at the time of crisis.

Occasionally, non-committee individuals could be invited in the meetings held by the

committee, only if it is considered apposite (A-Cap, 2018).

the place within the company so that an opinion could be formed relating to the financial

report (A-Cap, 2017).

The Company’s audit report also provides a statement that verifies the fact that the

institution has abided by all the requirements of the auditor’s independence so that there

are no such issues raised against the issue. After informing the directors of the significant

matters, the most significant is determined for a current time period. This indicates the key

audit matters of the company. A-CAP Resources Limited describes the KAM in the report

presented by the auditors does not disclose it until and unless there is an order provided for

doing so. Another situation in which the key audit matters are not included in the report is

when the probable outcomes are adverse in comparison with the benefits provided to the

interest of the public (A-Cap, 2017).

4.5. Evaluation of Audit committee and its Various Parts

A-CAP Resources Limited does have an audit committee. In addition, there are non-

executive directors in the audit committee. This includes John Fisher-Stamp, Chenghu Zhu,

Michael Liu, Henry J. Stacpoole, and Jijing Niu (A-Cap, 2017). In addition, there is an audit

committee charter, which is engaged in designing the roles and responsibilities of the audit

members in a specific way.

Structure of the audit committee members involves a rule, which focuses on stating the

involvement of four members is board of the company. In addition, among all, three will be

independent directors. Among the four members, at least one has to bear the required

experience and qualification for providing proper guidance and insights at the time of crisis.

Occasionally, non-committee individuals could be invited in the meetings held by the

committee, only if it is considered apposite (A-Cap, 2018).

AUDITING THEORY AND PRACTICE

The roles of the audit committee involve many significant factors. The first role of the audit

committee members includes supervising along with assessing the integrity of the entity’s

financial report. In addition, they also involve in evaluating important financial reporting

judgments. In addition, the auditor committee also scrutinizes along with evaluates to

comply with respect Company’s whistleblower policy and Code of Conduct. Assessment of

the internal financial control as well risk management is also done by the audit committee.

Reviewing along with monitoring, and administering the functions of external audit includes

matters that concerns the appointment and salary, independence & non-audit services.

Additionally, the audit members are liable to perform other specific functions, which are

instructed by the Company’s Constitution and law or the board of the company (A-Cap,

2018).

The responsibilities, which are assigned to the audit committee members of the company,

are explained precisely below:

The responsibility of the members toward the internal controls and financial reporting

comprises properly evaluating annual, half-year, and even quarterly financial statements.

Secondly, reviewing the report presented by the external auditor is appropriate or not for

satiating the needs of the shareholder. This further includes scrutinizing the selection of the

management with respect to the accounting principles and policies. Furthermore, it also

considers the internal controls and Company’s policies and procedures so that financial risks

can be assessed (A-Cap, 2018).

In case of annual meeting with the auditor, the audit members of the committee remain

assigned with responsibilities. The first responsibility is to discuss the choices made by the

company with regard to the accounting methods and principles along with changes to be

The roles of the audit committee involve many significant factors. The first role of the audit

committee members includes supervising along with assessing the integrity of the entity’s

financial report. In addition, they also involve in evaluating important financial reporting

judgments. In addition, the auditor committee also scrutinizes along with evaluates to

comply with respect Company’s whistleblower policy and Code of Conduct. Assessment of

the internal financial control as well risk management is also done by the audit committee.

Reviewing along with monitoring, and administering the functions of external audit includes

matters that concerns the appointment and salary, independence & non-audit services.

Additionally, the audit members are liable to perform other specific functions, which are

instructed by the Company’s Constitution and law or the board of the company (A-Cap,

2018).

The responsibilities, which are assigned to the audit committee members of the company,

are explained precisely below:

The responsibility of the members toward the internal controls and financial reporting

comprises properly evaluating annual, half-year, and even quarterly financial statements.

Secondly, reviewing the report presented by the external auditor is appropriate or not for

satiating the needs of the shareholder. This further includes scrutinizing the selection of the

management with respect to the accounting principles and policies. Furthermore, it also

considers the internal controls and Company’s policies and procedures so that financial risks

can be assessed (A-Cap, 2018).

In case of annual meeting with the auditor, the audit members of the committee remain

assigned with responsibilities. The first responsibility is to discuss the choices made by the

company with regard to the accounting methods and principles along with changes to be

AUDITING THEORY AND PRACTICE

recommended. The second responsibility includes discussion of any kind of disputes or

disagreements that are encountered by the management during the audit process. In this

context, the issues can be in terms of restrictions or right to use any required information.

Another essential responsibility of the members is to discuss the capability and potential of

the company’s capability for controlling the internal matters (A-Cap, 2018).

In case of the external auditor, the responsibility of the members involves scrutinizing the

overall procedure in the process of selection, rotation along with recruiting external auditor.

The members are also highly responsible for assessing the performance of the external

auditor. In addition, they also recommend the Board to either appoint or eliminate the

external auditor or to support the conditions in which he/she is working. In addition, they

are liable for confirming external auditor’s independence related to the non-audit services

of the company as well as fees (A-Cap, 2018).

Internal communications along with reporting is another dimension in which the audit

members of the company need to report, which is explained in the clause 5 relating to Audit

Committee Charter. Additionally, for ensuring that the board is all alert of the matter that

impacts the financial aspects of the company. Additionally, the audit members are also

engaged in updating the board regularly with the activities of the committee and provide

recommendations that are required (A-Cap, 2018). Another responsibility involves verifying

the committee’s membership on the basis of the Audit Committee Charter. It also focuses

on examining and accessing the action points and Audit committee charter. Additionally,

their role also comprises reviewing the independence relating to the committee members

on the basis of the Company’s policies, which engages in determining the independence of

directors. In addition, the audit members are also involved in developing and overseeing the

recommended. The second responsibility includes discussion of any kind of disputes or

disagreements that are encountered by the management during the audit process. In this

context, the issues can be in terms of restrictions or right to use any required information.

Another essential responsibility of the members is to discuss the capability and potential of

the company’s capability for controlling the internal matters (A-Cap, 2018).

In case of the external auditor, the responsibility of the members involves scrutinizing the

overall procedure in the process of selection, rotation along with recruiting external auditor.

The members are also highly responsible for assessing the performance of the external

auditor. In addition, they also recommend the Board to either appoint or eliminate the

external auditor or to support the conditions in which he/she is working. In addition, they

are liable for confirming external auditor’s independence related to the non-audit services

of the company as well as fees (A-Cap, 2018).

Internal communications along with reporting is another dimension in which the audit

members of the company need to report, which is explained in the clause 5 relating to Audit

Committee Charter. Additionally, for ensuring that the board is all alert of the matter that

impacts the financial aspects of the company. Additionally, the audit members are also

engaged in updating the board regularly with the activities of the committee and provide

recommendations that are required (A-Cap, 2018). Another responsibility involves verifying

the committee’s membership on the basis of the Audit Committee Charter. It also focuses

on examining and accessing the action points and Audit committee charter. Additionally,

their role also comprises reviewing the independence relating to the committee members

on the basis of the Company’s policies, which engages in determining the independence of

directors. In addition, the audit members are also involved in developing and overseeing the

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

AUDITING THEORY AND PRACTICE

procedures related to the complaints or any kind of issues associated with the employee of

the Company. This may include auditing issues, inside accounting controls, accounting, and

violation of the organization’s code of Conduct (A-Cap, 2018).

4.6 Type of Audit Opinion

The directors of the company in its audit opinion declared that the financial statements are

based on the Corporations Act 2001. This includes complying with the accounting standards

of Australia along with Corporations Regulations 2001, which provides combined financial

position as on 31st December 2017. Moreover, the directors of the A-Cap Resources have

presented an opinion in the audit that the company is capable of paying off their debts as

and when required (A-Cap, 2017).

4.7. Differences of Auditor’s Responsibilities and Director and Management’s

Responsibilities

There are differences between the responsibilities of the management and the directors of

the company relating to its financial report. In addition, it is observed that directors are

legally accountable for filing the company’s annual return along with the account at the

right time. They are also liable for ensuring that the details of the company are updated.

Moreover, the information that is provided by him will be enlisted in a public register, which

will be viewed during the public inspection (Companies & Intellectual Property Commission,

2018). The responsibility of the manager in relation to the financial report is that they are

entirely liable for preparing based on the provided financial framework. In addition, the

directors are also responsible for evaluating the company’s ability for determining whether

the company can continue as an ongoing concern. In this context, the utilizing and disclosing

matters of the ongoing concerns are to be evaluated by the management alone. Finally, the

procedures related to the complaints or any kind of issues associated with the employee of

the Company. This may include auditing issues, inside accounting controls, accounting, and

violation of the organization’s code of Conduct (A-Cap, 2018).

4.6 Type of Audit Opinion

The directors of the company in its audit opinion declared that the financial statements are

based on the Corporations Act 2001. This includes complying with the accounting standards

of Australia along with Corporations Regulations 2001, which provides combined financial

position as on 31st December 2017. Moreover, the directors of the A-Cap Resources have

presented an opinion in the audit that the company is capable of paying off their debts as

and when required (A-Cap, 2017).

4.7. Differences of Auditor’s Responsibilities and Director and Management’s

Responsibilities

There are differences between the responsibilities of the management and the directors of

the company relating to its financial report. In addition, it is observed that directors are

legally accountable for filing the company’s annual return along with the account at the

right time. They are also liable for ensuring that the details of the company are updated.

Moreover, the information that is provided by him will be enlisted in a public register, which

will be viewed during the public inspection (Companies & Intellectual Property Commission,

2018). The responsibility of the manager in relation to the financial report is that they are

entirely liable for preparing based on the provided financial framework. In addition, the

directors are also responsible for evaluating the company’s ability for determining whether

the company can continue as an ongoing concern. In this context, the utilizing and disclosing

matters of the ongoing concerns are to be evaluated by the management alone. Finally, the

AUDITING THEORY AND PRACTICE

responsibility of the auditor is to conclude the overall suitability with respect to the ongoing

concern on the basis of accounting. Thus, this involves initiating the formation of the

financial statements. Moreover, through the audit, the auditor explains any kind of material

uncertainty that exists within the financial report. This might disrupt the ability of the

company as an ongoing concern (International Federation of Accountants, 2018).

4.8. Presence of any Material Subsequent Events in the Company

There have been no records relating to subsequent events within the organization (A-Cap,

2017).

4.9. Assessment of the Effectiveness of the Material Information

The material information, which has been provided by A-Cap Resources Limited Company, is

that preparing financial statements are conducted based on accruals and are entirely based

on the historical costs, which are verified when required for the measurement of financial

assets, non-current assets along with financial liabilities (A-Cap, 2017).

4.10. The probability of Missing Any Material Information in the Provided Information

The information that is provided by A-Cap Resource Limited includes all the significant

aspects, which are required for the audit. This helps identifying the fact that there is no

information that remained unexplained in the process (A-Cap, 2017).

4.11. The follow-up questions to be asked to the Auditor

i. Has audit’s scope altered from the past years? If yes, then in which specific areas?

ii. How will the Company’s risk be managed with respect to the financial accounting?

iii. What audit issues have been identified to have high risks and how will they be

solved? (BDO Canada LLP, 2015).

responsibility of the auditor is to conclude the overall suitability with respect to the ongoing

concern on the basis of accounting. Thus, this involves initiating the formation of the

financial statements. Moreover, through the audit, the auditor explains any kind of material

uncertainty that exists within the financial report. This might disrupt the ability of the

company as an ongoing concern (International Federation of Accountants, 2018).

4.8. Presence of any Material Subsequent Events in the Company

There have been no records relating to subsequent events within the organization (A-Cap,

2017).

4.9. Assessment of the Effectiveness of the Material Information

The material information, which has been provided by A-Cap Resources Limited Company, is

that preparing financial statements are conducted based on accruals and are entirely based

on the historical costs, which are verified when required for the measurement of financial

assets, non-current assets along with financial liabilities (A-Cap, 2017).

4.10. The probability of Missing Any Material Information in the Provided Information

The information that is provided by A-Cap Resource Limited includes all the significant

aspects, which are required for the audit. This helps identifying the fact that there is no

information that remained unexplained in the process (A-Cap, 2017).

4.11. The follow-up questions to be asked to the Auditor

i. Has audit’s scope altered from the past years? If yes, then in which specific areas?

ii. How will the Company’s risk be managed with respect to the financial accounting?

iii. What audit issues have been identified to have high risks and how will they be

solved? (BDO Canada LLP, 2015).

AUDITING THEORY AND PRACTICE

5. Conclusion

The auditors play important role in each company’s operation, as that it suggests the issues,

which are related to the financial statements of the organization. In A-CAP Resources

Limited’s annual reports, the company’s auditor has identified all the evidence that is

required for proper evaluation of the audit process. It has also presented details relating to

organization’s audit for describing the impact of KAM in its formation. Basically, without an

auditor, a company cannot sustain in the industry, which has been precisely explained by

the annual report of the company.

5. Conclusion

The auditors play important role in each company’s operation, as that it suggests the issues,

which are related to the financial statements of the organization. In A-CAP Resources

Limited’s annual reports, the company’s auditor has identified all the evidence that is

required for proper evaluation of the audit process. It has also presented details relating to

organization’s audit for describing the impact of KAM in its formation. Basically, without an

auditor, a company cannot sustain in the industry, which has been precisely explained by

the annual report of the company.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

AUDITING THEORY AND PRACTICE

References

Gelman, Rosenberg & Freedman, 2018, What an auditor does and doesn’t do, Resources,

viewed 12 September 2018, <https://www.grfcpa.com/resource/auditor-responsibilities/>

Lin, L. & Tepalagul, N. K, No Date, ‘Auditor Independence and Audit Quality: A literature

review’. Boston University, pp. 1-54.

Patrick, Z. I.mVitalis, K & Mdoom, I., 2017, ‘Effect of auditor independence on audit quality:

A review of literature’. International Journal of Business and Management Invention, vol. 6,

iss. 3, pp. 51-59.

Zhang, Y., Hay, D. & Holm, C., 2016. ‘Non-audit services and auditor independence:

Norwegian evidence’. Cogent Business & Management, Vol. 3, No. 1215223, pp. 1-17.

Arnold, C., 2017, Auditor reporting standards implementation: Key Audit Matters, Auditor

Reporting Standards Implementation: Key Audit Matters, viewed 12 September 2018.

<https://www.ifac.org/global-knowledge-gateway/audit-assurance/discussion/auditor-

reporting-standards-implementation-key>

Bédard, J., Gonthier-Besacier, N. & Schatt, A., 2014, Costs and benefits of reporting Key Audit

Matters in the audit report: The French experience. In International Symposium on Audit

Research, viewed at 12 September 2018, <http://documents. escdijon.

eu/pdf/cig2014/ACTESDUCOLLOQUE/BEDARD_GONTHIER_BESACIER_SCHATT. pdf.>

A-Cap, 2018. Audit committee charter. A-Cap Resources Limited, viewed 13 September 2018

<https://acap.com.au/audit-committee-charter/>

References

Gelman, Rosenberg & Freedman, 2018, What an auditor does and doesn’t do, Resources,

viewed 12 September 2018, <https://www.grfcpa.com/resource/auditor-responsibilities/>

Lin, L. & Tepalagul, N. K, No Date, ‘Auditor Independence and Audit Quality: A literature

review’. Boston University, pp. 1-54.

Patrick, Z. I.mVitalis, K & Mdoom, I., 2017, ‘Effect of auditor independence on audit quality:

A review of literature’. International Journal of Business and Management Invention, vol. 6,

iss. 3, pp. 51-59.

Zhang, Y., Hay, D. & Holm, C., 2016. ‘Non-audit services and auditor independence:

Norwegian evidence’. Cogent Business & Management, Vol. 3, No. 1215223, pp. 1-17.

Arnold, C., 2017, Auditor reporting standards implementation: Key Audit Matters, Auditor

Reporting Standards Implementation: Key Audit Matters, viewed 12 September 2018.

<https://www.ifac.org/global-knowledge-gateway/audit-assurance/discussion/auditor-

reporting-standards-implementation-key>

Bédard, J., Gonthier-Besacier, N. & Schatt, A., 2014, Costs and benefits of reporting Key Audit

Matters in the audit report: The French experience. In International Symposium on Audit

Research, viewed at 12 September 2018, <http://documents. escdijon.

eu/pdf/cig2014/ACTESDUCOLLOQUE/BEDARD_GONTHIER_BESACIER_SCHATT. pdf.>

A-Cap, 2018. Audit committee charter. A-Cap Resources Limited, viewed 13 September 2018

<https://acap.com.au/audit-committee-charter/>

AUDITING THEORY AND PRACTICE

A-Cap Resources LTD, 2016, ‘A-Cap Resources Limited and its controlled entities’. Half-Year

Repor, pp. 2-22.

International Federation of Accountants, 2018, ‘Auditor Reporting—management and

auditor responsibility statements,’ IAASB Main Agenda (September 2014), pp. 1-4.

A-Cap, 2017, ‘Report 2017’, A-Cap Resources Ltd, pp 2-64.

Companies & Intellectual Property Commission, 2018, Companies & Intellectual Property

Commission, Legislation, viewed 13 September, 2018 <http://www.cipc.co.za/index.php?

cID=590>

BDO Canada LLP, 2015, 10 essential questions you should ask your auditor, BDO, viewed 14

September 2018. <https://www.bdo.ca/getattachment/cfe83f3e-160e-4d12-8c72-

575462ecee99/attachment.aspx>

A-Cap Resources LTD, 2016, ‘A-Cap Resources Limited and its controlled entities’. Half-Year

Repor, pp. 2-22.

International Federation of Accountants, 2018, ‘Auditor Reporting—management and

auditor responsibility statements,’ IAASB Main Agenda (September 2014), pp. 1-4.

A-Cap, 2017, ‘Report 2017’, A-Cap Resources Ltd, pp 2-64.

Companies & Intellectual Property Commission, 2018, Companies & Intellectual Property

Commission, Legislation, viewed 13 September, 2018 <http://www.cipc.co.za/index.php?

cID=590>

BDO Canada LLP, 2015, 10 essential questions you should ask your auditor, BDO, viewed 14

September 2018. <https://www.bdo.ca/getattachment/cfe83f3e-160e-4d12-8c72-

575462ecee99/attachment.aspx>

AUDITING THEORY AND PRACTICE

Bibliography

Cohen, J.R., Gaynor, L.M., Krishnamoorthy, G. & Wright, A.M., 2011, ‘The impact on auditor

judgments of CEO influence on audit committee independence’. Auditing: A Journal of

Practice & Theory, vol. 30, no. 4, pp. 129-147.

Coram, P., Ferguson, C. & Moroney, R., 2008, ‘Internal audit, alternative internal audit

structures and the level of misappropriation of assets fraud’. Accounting & Finance, vol. 48,

no. 4, pp. 543-559.

Dao, M., Mishra, S. & Raghunandan, K., 2008, ‘Auditor tenure and shareholder ratification of

the auditor’, Accounting Horizons, vol. 22, no. 3, pp. 297-314.

Humphrey, C., Loft, A. & Woods, M., 2009, ‘The global audit profession and the international

financial architecture: Understanding regulatory relationships at a time of financial crisis’.

Accounting, organizations and society, vol. 34, no. 6-7, pp. 810-825.

Lisic, L.L., 2014, ‘Auditor-provided tax services and earnings management in tax expense:

The importance of audit committees’. Journal of Accounting, Auditing & Finance, vol. 29, no.

3, pp. 340-366.

Skinner, D.J. & Srinivasan, S., 2012, ‘Audit quality and auditor reputation: Evidence from

Japan’, The Accounting Review, vol.87, no.5, pp.1737-1765.

Bibliography

Cohen, J.R., Gaynor, L.M., Krishnamoorthy, G. & Wright, A.M., 2011, ‘The impact on auditor

judgments of CEO influence on audit committee independence’. Auditing: A Journal of

Practice & Theory, vol. 30, no. 4, pp. 129-147.

Coram, P., Ferguson, C. & Moroney, R., 2008, ‘Internal audit, alternative internal audit

structures and the level of misappropriation of assets fraud’. Accounting & Finance, vol. 48,

no. 4, pp. 543-559.

Dao, M., Mishra, S. & Raghunandan, K., 2008, ‘Auditor tenure and shareholder ratification of

the auditor’, Accounting Horizons, vol. 22, no. 3, pp. 297-314.

Humphrey, C., Loft, A. & Woods, M., 2009, ‘The global audit profession and the international

financial architecture: Understanding regulatory relationships at a time of financial crisis’.

Accounting, organizations and society, vol. 34, no. 6-7, pp. 810-825.

Lisic, L.L., 2014, ‘Auditor-provided tax services and earnings management in tax expense:

The importance of audit committees’. Journal of Accounting, Auditing & Finance, vol. 29, no.

3, pp. 340-366.

Skinner, D.J. & Srinivasan, S., 2012, ‘Audit quality and auditor reputation: Evidence from

Japan’, The Accounting Review, vol.87, no.5, pp.1737-1765.

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

AUDITING THEORY AND PRACTICE

6. Appendix

Long-term Benefits Post-employment benefits Share-based payments Total

Salary Fees Bonus Long service leave Superannuation Shares

Name Cash-settled Share Settled

$ $ $ $ $ $ $ $

30-Jun-17

A Shen 43,753 2,99,236 - 0 0 0 16,537 3,59,346

P Ingram 39,954 174, 499 - 0 0 3,796 2,07,785 4,26,034

P Thomson 4,21,948 - - 64,894 0 0 0 486, 842

H Stacpoole 5,708 - - 0 0 542 16,957 22,607

P Woolrich 5,708 7,619 - 0 0 542 16,357 30,226

J Fisher -Stamp 39,954 174, 499 - 0 0 3,796 2,01,810 4,20,059

M Liu 43,753 174, 564 - 0 0 0 1,98,570 4,16,887

JJ Niu 39,397 - - 0 0 0 0 39,397

CH Zhu 39,397 - - 0 0 0 0 39,397

Total 679, 572 830417 - 64,894 0 8,676 6,57,236 22,40,795

30-Jun-16

A Shen 25,000 0 0 0 0 0 20,740 45,740

P Ingram 23,192 1,03,949 1,02,366 0 0 2,203 20,740 252, 450

P Thomson 4,36,416 0 0 0 0 0 0 4,36,416

H Stacpoole 23,192 0 0 0 0 2203 20,740 46,135

P Woolrich 23,192 73,136 0 0 0 2,203 20,740 1,19,271

J Fisher Stamp 23,192 90,517 88,934 0 0 2,203 13,707 2,18,553

M Liu 24,775 86,478 86,243 0 0 0 13, 343 2,10,839

R Pelt 0 0 0 0 0 0 24, 318 24,318

R Lockwood 0 0 0 0 0 0 7,848 7,848

Total 578, 959 3,54,080 2,77,543 0 0 8,812 1,42,176 13,61,570

Short term Benefits

Consulting Fees

Figure 1: Remuneration Report

Source: (A-Cap, 2017)

6. Appendix

Long-term Benefits Post-employment benefits Share-based payments Total

Salary Fees Bonus Long service leave Superannuation Shares

Name Cash-settled Share Settled

$ $ $ $ $ $ $ $

30-Jun-17

A Shen 43,753 2,99,236 - 0 0 0 16,537 3,59,346

P Ingram 39,954 174, 499 - 0 0 3,796 2,07,785 4,26,034

P Thomson 4,21,948 - - 64,894 0 0 0 486, 842

H Stacpoole 5,708 - - 0 0 542 16,957 22,607

P Woolrich 5,708 7,619 - 0 0 542 16,357 30,226

J Fisher -Stamp 39,954 174, 499 - 0 0 3,796 2,01,810 4,20,059

M Liu 43,753 174, 564 - 0 0 0 1,98,570 4,16,887

JJ Niu 39,397 - - 0 0 0 0 39,397

CH Zhu 39,397 - - 0 0 0 0 39,397

Total 679, 572 830417 - 64,894 0 8,676 6,57,236 22,40,795

30-Jun-16

A Shen 25,000 0 0 0 0 0 20,740 45,740

P Ingram 23,192 1,03,949 1,02,366 0 0 2,203 20,740 252, 450

P Thomson 4,36,416 0 0 0 0 0 0 4,36,416

H Stacpoole 23,192 0 0 0 0 2203 20,740 46,135

P Woolrich 23,192 73,136 0 0 0 2,203 20,740 1,19,271

J Fisher Stamp 23,192 90,517 88,934 0 0 2,203 13,707 2,18,553

M Liu 24,775 86,478 86,243 0 0 0 13, 343 2,10,839

R Pelt 0 0 0 0 0 0 24, 318 24,318

R Lockwood 0 0 0 0 0 0 7,848 7,848

Total 578, 959 3,54,080 2,77,543 0 0 8,812 1,42,176 13,61,570

Short term Benefits

Consulting Fees

Figure 1: Remuneration Report

Source: (A-Cap, 2017)

1 out of 17

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.