Audit Report: GPSA - Internal Control and Financial Risk Analysis

VerifiedAdded on 2020/03/28

|14

|3085

|227

Report

AI Summary

This report presents an audit analysis of GPSA, a medical equipment distributor, focusing on internal control effectiveness and financial risk assessment. The report examines key accounting areas, including accounts receivable, intangible assets, research and development, property assets, and current investments, identifying associated audit risks and mitigation strategies. Ratio analysis is performed on financial data from 2015-2017, revealing trends and their impact on the audit plan. The report evaluates GPSA's internal control system, highlighting strengths like password protection and bonus payment reviews, while also identifying weaknesses such as lack of segregation of duties in trade receivables. Finally, the report suggests steps to address identified weaknesses and improve internal controls, aiming to reduce audit risks and enhance financial reporting accuracy.

Running head: AUDITING THEORY AND PRACTICE

Auditing

Name of the University

Name of the student

Authors note

Auditing

Name of the University

Name of the student

Authors note

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1AUDITING THEORY AND PRACTICE

Executive summary:

The report is prepared to analyse the internal control effectiveness of GPSA that is engaged

in wide variety of activities. Analysis of risks of several accounts are done by using ratio

analysis. Internal control has been evaluated in terms of risk alleviation, text of control and

their effectiveness. Later part of report deals with division on the weakness of internal control

system and steps taken by auditor to reduce such risks.

Executive summary:

The report is prepared to analyse the internal control effectiveness of GPSA that is engaged

in wide variety of activities. Analysis of risks of several accounts are done by using ratio

analysis. Internal control has been evaluated in terms of risk alleviation, text of control and

their effectiveness. Later part of report deals with division on the weakness of internal control

system and steps taken by auditor to reduce such risks.

2AUDITING THEORY AND PRACTICE

Table of Contents

Introduction:...............................................................................................................................3

Answer to question 1A:..............................................................................................................3

Answer to question 1B:..............................................................................................................6

Answer to question 2A:..............................................................................................................8

Internal control system:..............................................................................................................8

Risk alleviated-...........................................................................................................................9

Answer to question 2b:.............................................................................................................11

Weakness identified in the internal control for sales system and trade receivables of GPSA:11

Conclusion:..............................................................................................................................11

References:...............................................................................................................................12

Table of Contents

Introduction:...............................................................................................................................3

Answer to question 1A:..............................................................................................................3

Answer to question 1B:..............................................................................................................6

Answer to question 2A:..............................................................................................................8

Internal control system:..............................................................................................................8

Risk alleviated-...........................................................................................................................9

Answer to question 2b:.............................................................................................................11

Weakness identified in the internal control for sales system and trade receivables of GPSA:11

Conclusion:..............................................................................................................................11

References:...............................................................................................................................12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3AUDITING THEORY AND PRACTICE

Introduction:

GPSA is an organization that is engaged in distributing, supplying the medical

equipment to medical practitioners. One of the long-standing client of MYH is GPA that is

required to conduct an audit plan for organization. While carrying out task of audit, several

areas of accounts are analysed using analytical procedures.

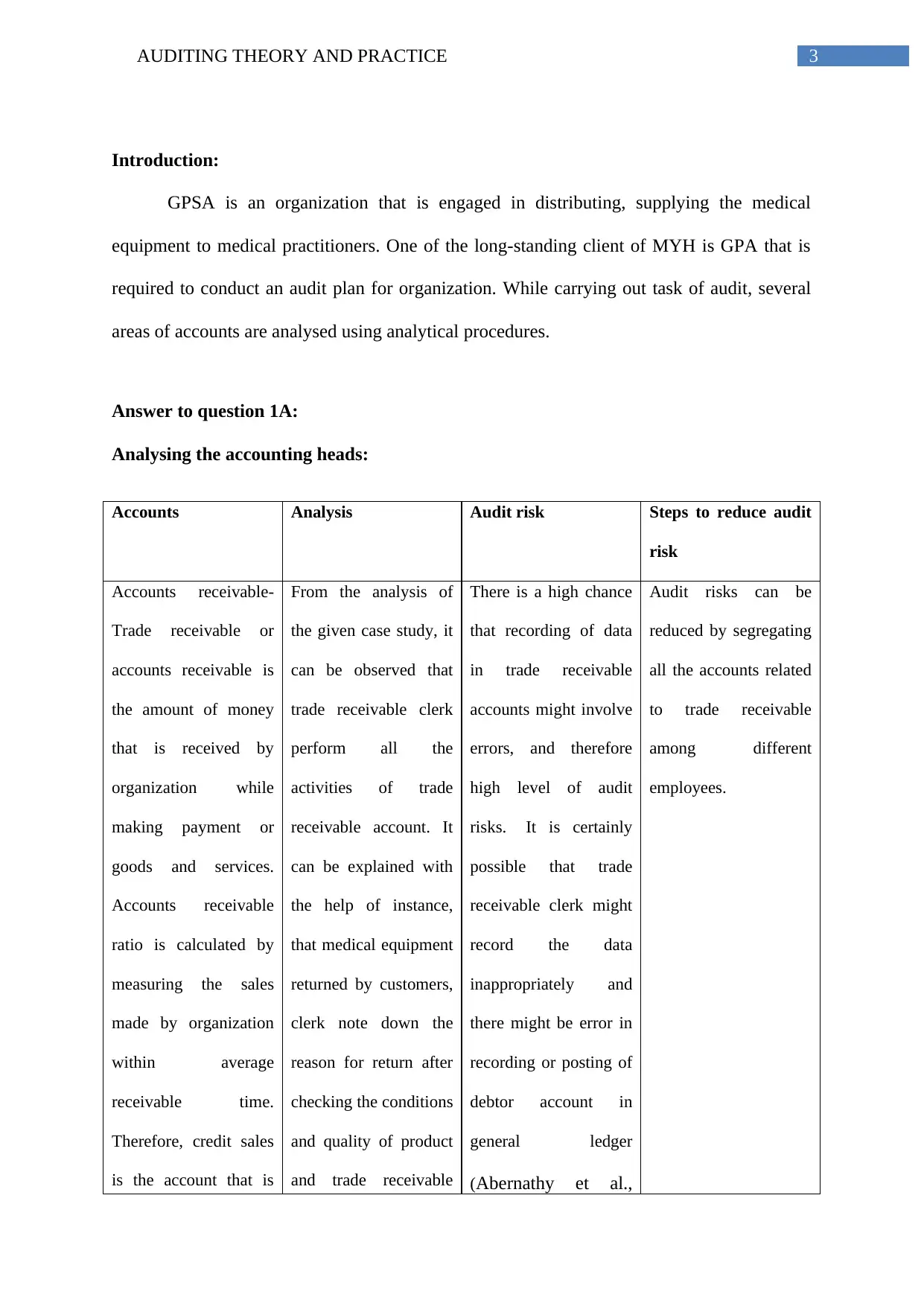

Answer to question 1A:

Analysing the accounting heads:

Accounts Analysis Audit risk Steps to reduce audit

risk

Accounts receivable-

Trade receivable or

accounts receivable is

the amount of money

that is received by

organization while

making payment or

goods and services.

Accounts receivable

ratio is calculated by

measuring the sales

made by organization

within average

receivable time.

Therefore, credit sales

is the account that is

From the analysis of

the given case study, it

can be observed that

trade receivable clerk

perform all the

activities of trade

receivable account. It

can be explained with

the help of instance,

that medical equipment

returned by customers,

clerk note down the

reason for return after

checking the conditions

and quality of product

and trade receivable

There is a high chance

that recording of data

in trade receivable

accounts might involve

errors, and therefore

high level of audit

risks. It is certainly

possible that trade

receivable clerk might

record the data

inappropriately and

there might be error in

recording or posting of

debtor account in

general ledger

(Abernathy et al.,

Audit risks can be

reduced by segregating

all the accounts related

to trade receivable

among different

employees.

Introduction:

GPSA is an organization that is engaged in distributing, supplying the medical

equipment to medical practitioners. One of the long-standing client of MYH is GPA that is

required to conduct an audit plan for organization. While carrying out task of audit, several

areas of accounts are analysed using analytical procedures.

Answer to question 1A:

Analysing the accounting heads:

Accounts Analysis Audit risk Steps to reduce audit

risk

Accounts receivable-

Trade receivable or

accounts receivable is

the amount of money

that is received by

organization while

making payment or

goods and services.

Accounts receivable

ratio is calculated by

measuring the sales

made by organization

within average

receivable time.

Therefore, credit sales

is the account that is

From the analysis of

the given case study, it

can be observed that

trade receivable clerk

perform all the

activities of trade

receivable account. It

can be explained with

the help of instance,

that medical equipment

returned by customers,

clerk note down the

reason for return after

checking the conditions

and quality of product

and trade receivable

There is a high chance

that recording of data

in trade receivable

accounts might involve

errors, and therefore

high level of audit

risks. It is certainly

possible that trade

receivable clerk might

record the data

inappropriately and

there might be error in

recording or posting of

debtor account in

general ledger

(Abernathy et al.,

Audit risks can be

reduced by segregating

all the accounts related

to trade receivable

among different

employees.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4AUDITING THEORY AND PRACTICE

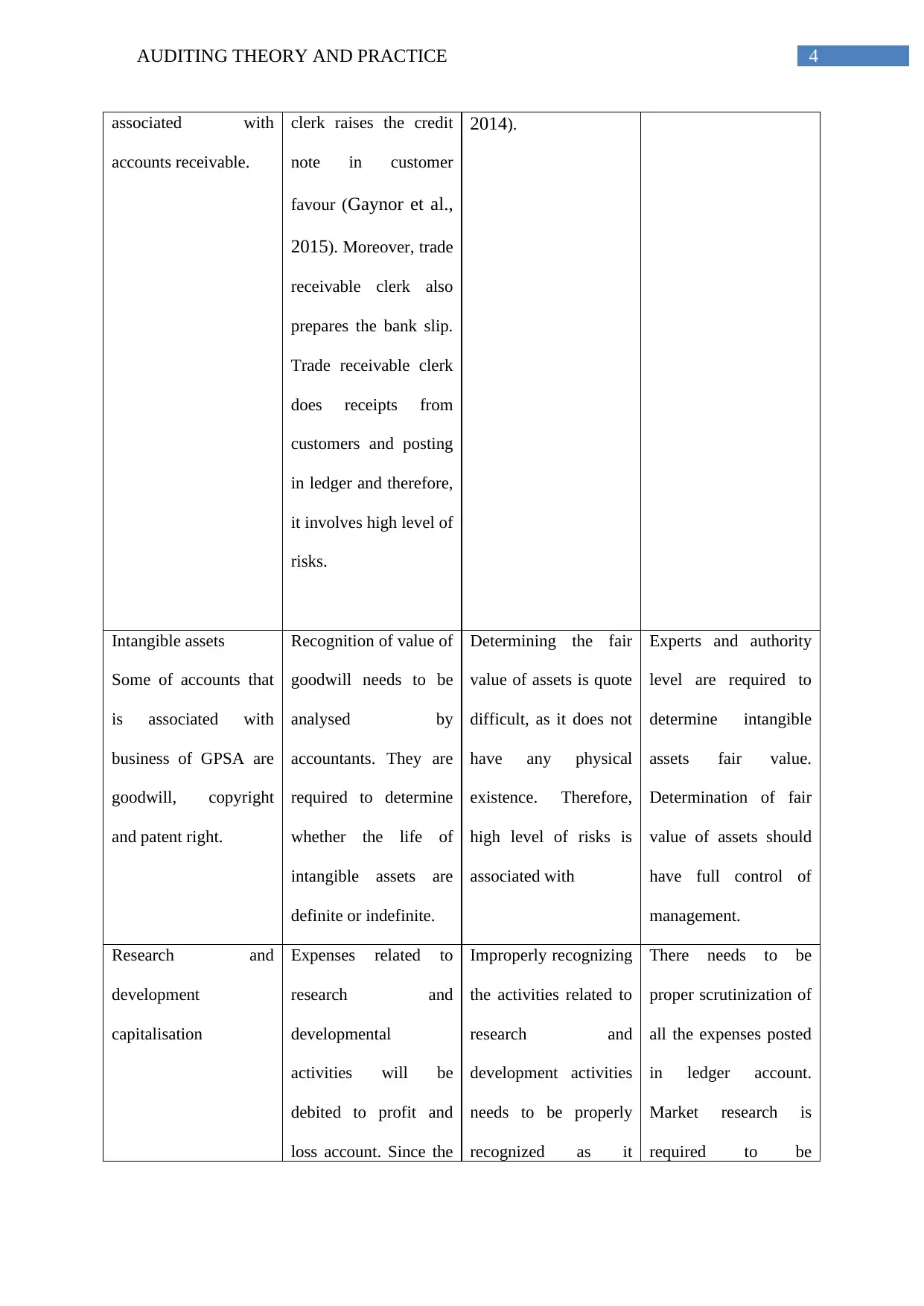

associated with

accounts receivable.

clerk raises the credit

note in customer

favour (Gaynor et al.,

2015). Moreover, trade

receivable clerk also

prepares the bank slip.

Trade receivable clerk

does receipts from

customers and posting

in ledger and therefore,

it involves high level of

risks.

2014).

Intangible assets

Some of accounts that

is associated with

business of GPSA are

goodwill, copyright

and patent right.

Recognition of value of

goodwill needs to be

analysed by

accountants. They are

required to determine

whether the life of

intangible assets are

definite or indefinite.

Determining the fair

value of assets is quote

difficult, as it does not

have any physical

existence. Therefore,

high level of risks is

associated with

Experts and authority

level are required to

determine intangible

assets fair value.

Determination of fair

value of assets should

have full control of

management.

Research and

development

capitalisation

Expenses related to

research and

developmental

activities will be

debited to profit and

loss account. Since the

Improperly recognizing

the activities related to

research and

development activities

needs to be properly

recognized as it

There needs to be

proper scrutinization of

all the expenses posted

in ledger account.

Market research is

required to be

associated with

accounts receivable.

clerk raises the credit

note in customer

favour (Gaynor et al.,

2015). Moreover, trade

receivable clerk also

prepares the bank slip.

Trade receivable clerk

does receipts from

customers and posting

in ledger and therefore,

it involves high level of

risks.

2014).

Intangible assets

Some of accounts that

is associated with

business of GPSA are

goodwill, copyright

and patent right.

Recognition of value of

goodwill needs to be

analysed by

accountants. They are

required to determine

whether the life of

intangible assets are

definite or indefinite.

Determining the fair

value of assets is quote

difficult, as it does not

have any physical

existence. Therefore,

high level of risks is

associated with

Experts and authority

level are required to

determine intangible

assets fair value.

Determination of fair

value of assets should

have full control of

management.

Research and

development

capitalisation

Expenses related to

research and

developmental

activities will be

debited to profit and

loss account. Since the

Improperly recognizing

the activities related to

research and

development activities

needs to be properly

recognized as it

There needs to be

proper scrutinization of

all the expenses posted

in ledger account.

Market research is

required to be

5AUDITING THEORY AND PRACTICE

development was

successful, expenses

related to them will be

capitalized.

involves high amount

of costs

conducted before

launching any

equipment in market.

Property assets

Property assets account

of GPSA involves

depreciation account

and fixed asset

account.

Financial statement of

organization will be

greatly impacted if

there is improper

recording of

depreciation amount

and carrying value of

assets.

Improper recording of

assets wold enable the

auditors to differentiate

the duration of

existence of assets

whether they are less

than 180 days or for

more than 180 days.

Sales and purchase of

property assets needs

to be scrutinized

properly and it is also

essential to check

several impairments

related to assets.

Current investments

Current investments is

related to accounts that

is converted into cash

within short time

period that is within a

period of 3 to 12

months. Current assets

such as cash and cash

equivalent is recorded

under current

investments (Beasley,

2015).

Under different

accounting system

treatment of investment

account is different and

it can be said that

medium level risks is

associated with current

investments.

Audit risk involved

with current investment

is making investments

without evaluation of

risks.

There needs to be

regularly checking of

return generated from

investments. It is also

essential to evaluate

the past trend of

investment growth

performance.

development was

successful, expenses

related to them will be

capitalized.

involves high amount

of costs

conducted before

launching any

equipment in market.

Property assets

Property assets account

of GPSA involves

depreciation account

and fixed asset

account.

Financial statement of

organization will be

greatly impacted if

there is improper

recording of

depreciation amount

and carrying value of

assets.

Improper recording of

assets wold enable the

auditors to differentiate

the duration of

existence of assets

whether they are less

than 180 days or for

more than 180 days.

Sales and purchase of

property assets needs

to be scrutinized

properly and it is also

essential to check

several impairments

related to assets.

Current investments

Current investments is

related to accounts that

is converted into cash

within short time

period that is within a

period of 3 to 12

months. Current assets

such as cash and cash

equivalent is recorded

under current

investments (Beasley,

2015).

Under different

accounting system

treatment of investment

account is different and

it can be said that

medium level risks is

associated with current

investments.

Audit risk involved

with current investment

is making investments

without evaluation of

risks.

There needs to be

regularly checking of

return generated from

investments. It is also

essential to evaluate

the past trend of

investment growth

performance.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6AUDITING THEORY AND PRACTICE

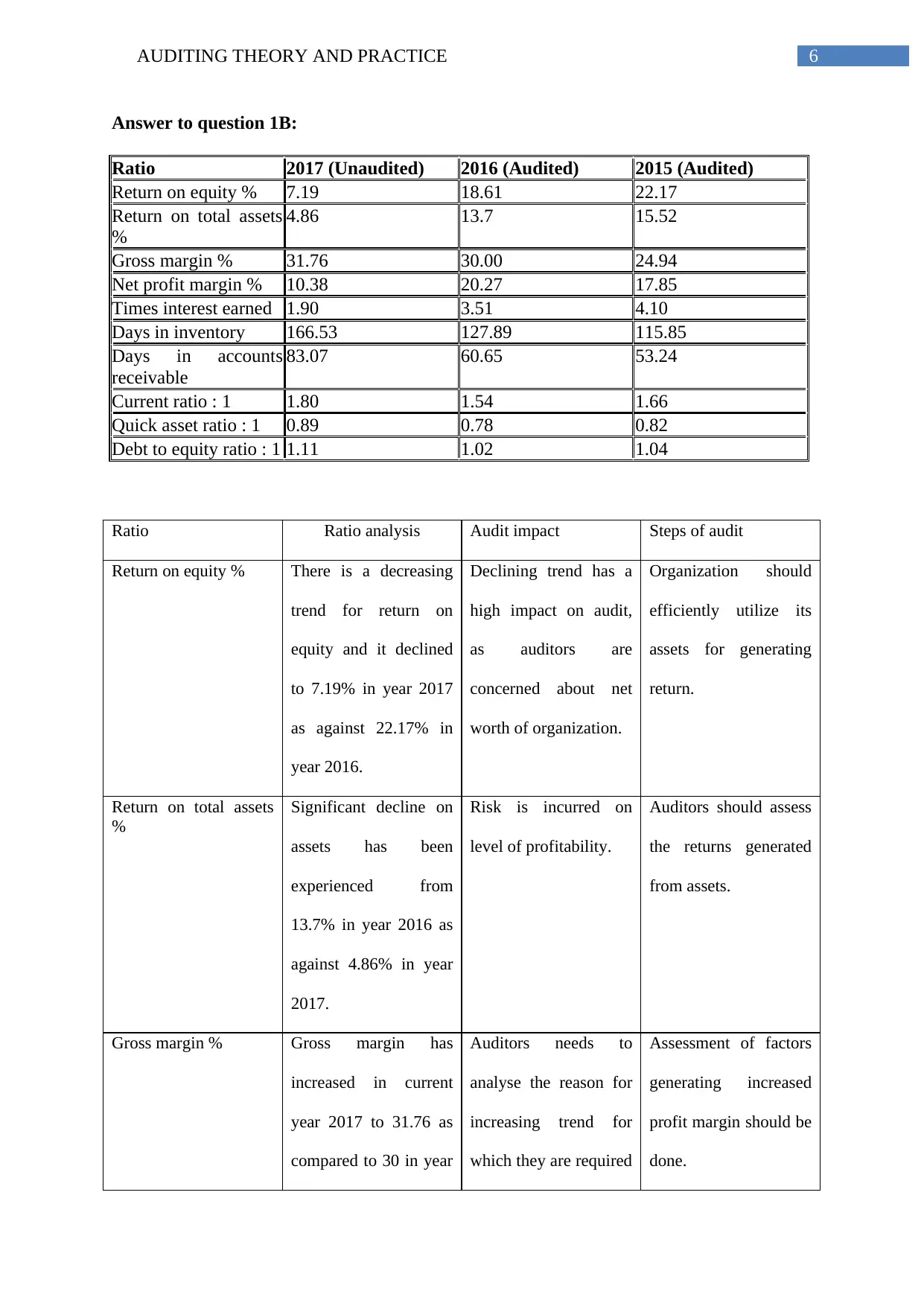

Answer to question 1B:

Ratio 2017 (Unaudited) 2016 (Audited) 2015 (Audited)

Return on equity % 7.19 18.61 22.17

Return on total assets

%

4.86 13.7 15.52

Gross margin % 31.76 30.00 24.94

Net profit margin % 10.38 20.27 17.85

Times interest earned 1.90 3.51 4.10

Days in inventory 166.53 127.89 115.85

Days in accounts

receivable

83.07 60.65 53.24

Current ratio : 1 1.80 1.54 1.66

Quick asset ratio : 1 0.89 0.78 0.82

Debt to equity ratio : 1 1.11 1.02 1.04

Ratio Ratio analysis Audit impact Steps of audit

Return on equity % There is a decreasing

trend for return on

equity and it declined

to 7.19% in year 2017

as against 22.17% in

year 2016.

Declining trend has a

high impact on audit,

as auditors are

concerned about net

worth of organization.

Organization should

efficiently utilize its

assets for generating

return.

Return on total assets

%

Significant decline on

assets has been

experienced from

13.7% in year 2016 as

against 4.86% in year

2017.

Risk is incurred on

level of profitability.

Auditors should assess

the returns generated

from assets.

Gross margin % Gross margin has

increased in current

year 2017 to 31.76 as

compared to 30 in year

Auditors needs to

analyse the reason for

increasing trend for

which they are required

Assessment of factors

generating increased

profit margin should be

done.

Answer to question 1B:

Ratio 2017 (Unaudited) 2016 (Audited) 2015 (Audited)

Return on equity % 7.19 18.61 22.17

Return on total assets

%

4.86 13.7 15.52

Gross margin % 31.76 30.00 24.94

Net profit margin % 10.38 20.27 17.85

Times interest earned 1.90 3.51 4.10

Days in inventory 166.53 127.89 115.85

Days in accounts

receivable

83.07 60.65 53.24

Current ratio : 1 1.80 1.54 1.66

Quick asset ratio : 1 0.89 0.78 0.82

Debt to equity ratio : 1 1.11 1.02 1.04

Ratio Ratio analysis Audit impact Steps of audit

Return on equity % There is a decreasing

trend for return on

equity and it declined

to 7.19% in year 2017

as against 22.17% in

year 2016.

Declining trend has a

high impact on audit,

as auditors are

concerned about net

worth of organization.

Organization should

efficiently utilize its

assets for generating

return.

Return on total assets

%

Significant decline on

assets has been

experienced from

13.7% in year 2016 as

against 4.86% in year

2017.

Risk is incurred on

level of profitability.

Auditors should assess

the returns generated

from assets.

Gross margin % Gross margin has

increased in current

year 2017 to 31.76 as

compared to 30 in year

Auditors needs to

analyse the reason for

increasing trend for

which they are required

Assessment of factors

generating increased

profit margin should be

done.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

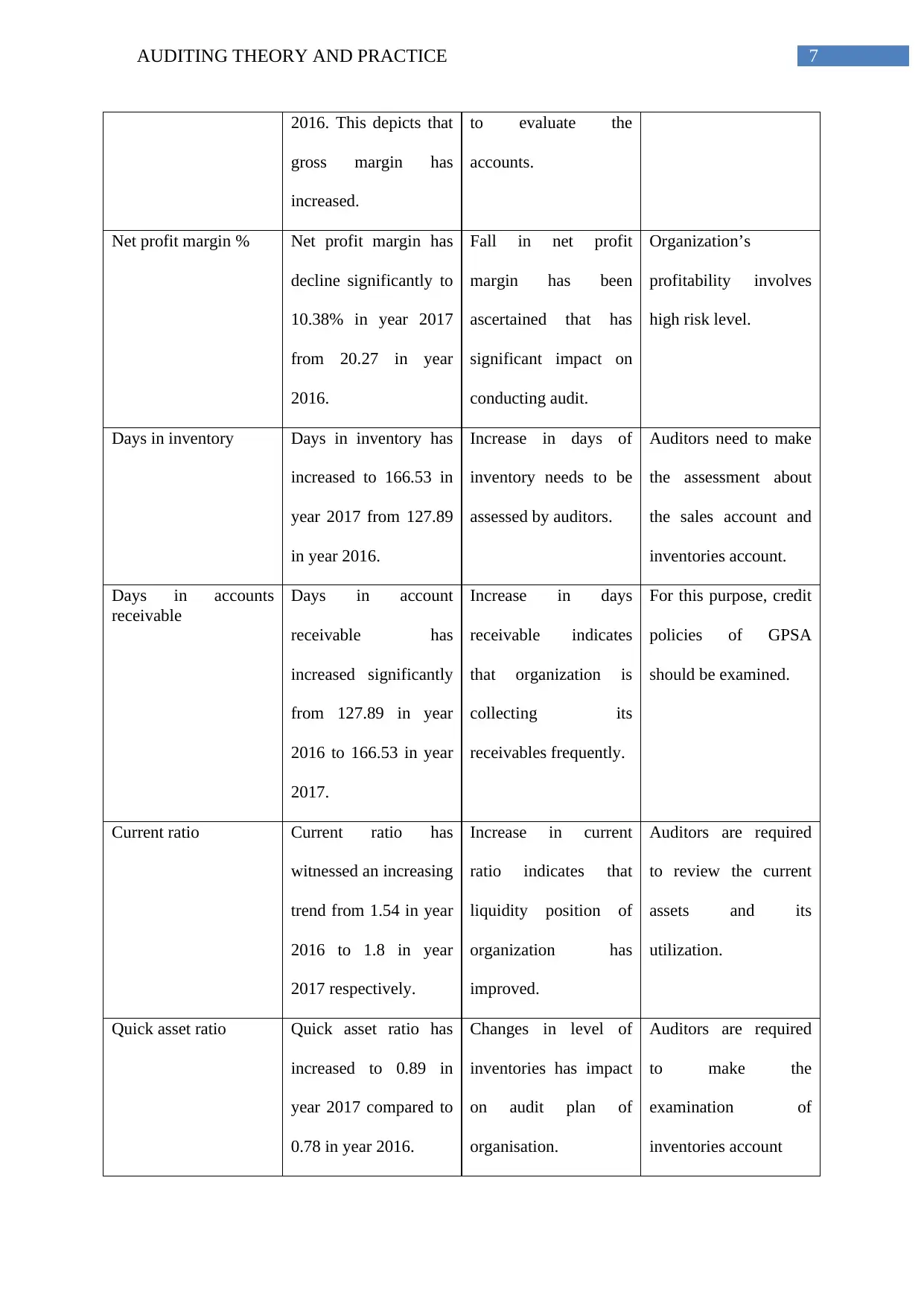

7AUDITING THEORY AND PRACTICE

2016. This depicts that

gross margin has

increased.

to evaluate the

accounts.

Net profit margin % Net profit margin has

decline significantly to

10.38% in year 2017

from 20.27 in year

2016.

Fall in net profit

margin has been

ascertained that has

significant impact on

conducting audit.

Organization’s

profitability involves

high risk level.

Days in inventory Days in inventory has

increased to 166.53 in

year 2017 from 127.89

in year 2016.

Increase in days of

inventory needs to be

assessed by auditors.

Auditors need to make

the assessment about

the sales account and

inventories account.

Days in accounts

receivable

Days in account

receivable has

increased significantly

from 127.89 in year

2016 to 166.53 in year

2017.

Increase in days

receivable indicates

that organization is

collecting its

receivables frequently.

For this purpose, credit

policies of GPSA

should be examined.

Current ratio Current ratio has

witnessed an increasing

trend from 1.54 in year

2016 to 1.8 in year

2017 respectively.

Increase in current

ratio indicates that

liquidity position of

organization has

improved.

Auditors are required

to review the current

assets and its

utilization.

Quick asset ratio Quick asset ratio has

increased to 0.89 in

year 2017 compared to

0.78 in year 2016.

Changes in level of

inventories has impact

on audit plan of

organisation.

Auditors are required

to make the

examination of

inventories account

2016. This depicts that

gross margin has

increased.

to evaluate the

accounts.

Net profit margin % Net profit margin has

decline significantly to

10.38% in year 2017

from 20.27 in year

2016.

Fall in net profit

margin has been

ascertained that has

significant impact on

conducting audit.

Organization’s

profitability involves

high risk level.

Days in inventory Days in inventory has

increased to 166.53 in

year 2017 from 127.89

in year 2016.

Increase in days of

inventory needs to be

assessed by auditors.

Auditors need to make

the assessment about

the sales account and

inventories account.

Days in accounts

receivable

Days in account

receivable has

increased significantly

from 127.89 in year

2016 to 166.53 in year

2017.

Increase in days

receivable indicates

that organization is

collecting its

receivables frequently.

For this purpose, credit

policies of GPSA

should be examined.

Current ratio Current ratio has

witnessed an increasing

trend from 1.54 in year

2016 to 1.8 in year

2017 respectively.

Increase in current

ratio indicates that

liquidity position of

organization has

improved.

Auditors are required

to review the current

assets and its

utilization.

Quick asset ratio Quick asset ratio has

increased to 0.89 in

year 2017 compared to

0.78 in year 2016.

Changes in level of

inventories has impact

on audit plan of

organisation.

Auditors are required

to make the

examination of

inventories account

8AUDITING THEORY AND PRACTICE

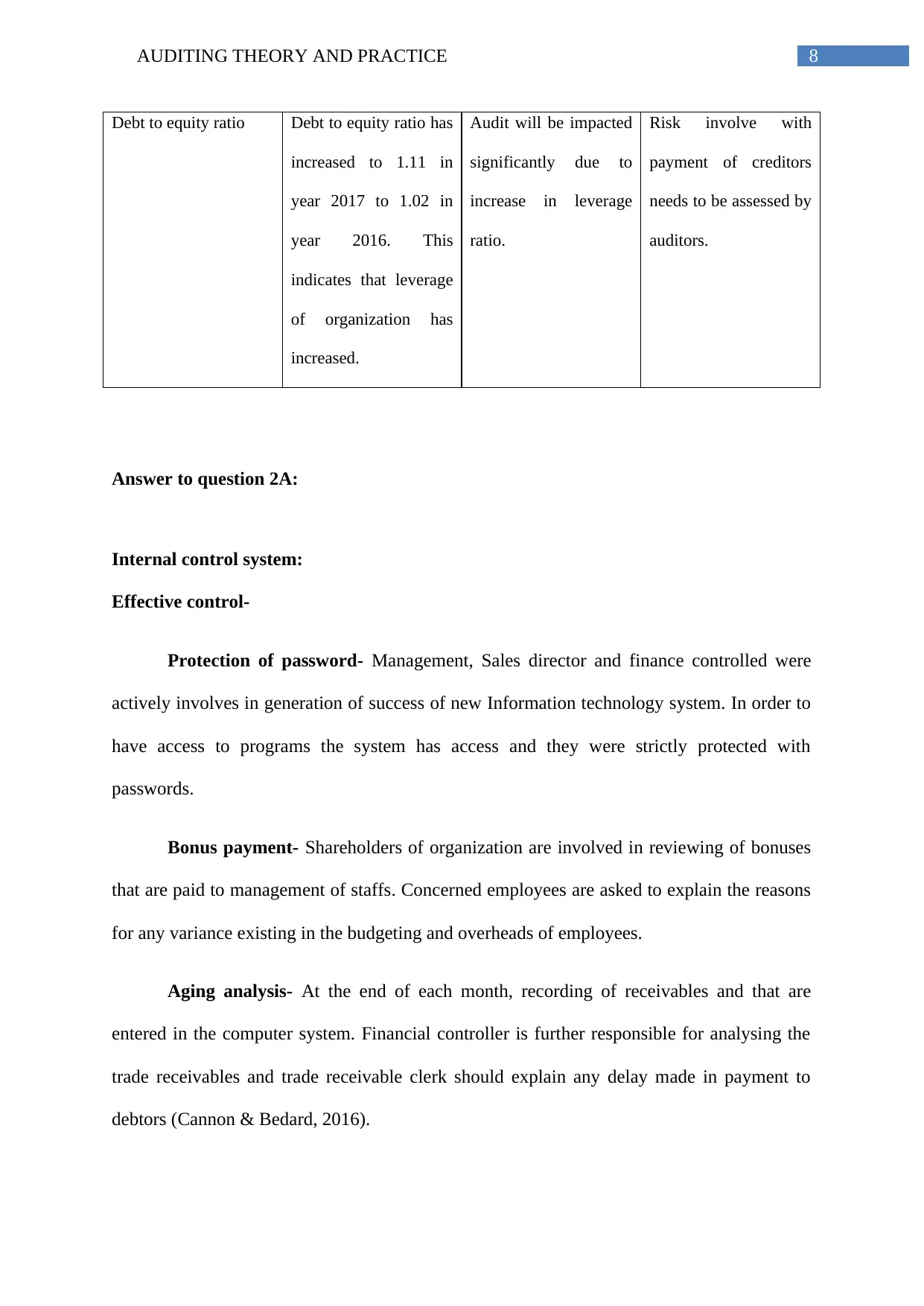

Debt to equity ratio Debt to equity ratio has

increased to 1.11 in

year 2017 to 1.02 in

year 2016. This

indicates that leverage

of organization has

increased.

Audit will be impacted

significantly due to

increase in leverage

ratio.

Risk involve with

payment of creditors

needs to be assessed by

auditors.

Answer to question 2A:

Internal control system:

Effective control-

Protection of password- Management, Sales director and finance controlled were

actively involves in generation of success of new Information technology system. In order to

have access to programs the system has access and they were strictly protected with

passwords.

Bonus payment- Shareholders of organization are involved in reviewing of bonuses

that are paid to management of staffs. Concerned employees are asked to explain the reasons

for any variance existing in the budgeting and overheads of employees.

Aging analysis- At the end of each month, recording of receivables and that are

entered in the computer system. Financial controller is further responsible for analysing the

trade receivables and trade receivable clerk should explain any delay made in payment to

debtors (Cannon & Bedard, 2016).

Debt to equity ratio Debt to equity ratio has

increased to 1.11 in

year 2017 to 1.02 in

year 2016. This

indicates that leverage

of organization has

increased.

Audit will be impacted

significantly due to

increase in leverage

ratio.

Risk involve with

payment of creditors

needs to be assessed by

auditors.

Answer to question 2A:

Internal control system:

Effective control-

Protection of password- Management, Sales director and finance controlled were

actively involves in generation of success of new Information technology system. In order to

have access to programs the system has access and they were strictly protected with

passwords.

Bonus payment- Shareholders of organization are involved in reviewing of bonuses

that are paid to management of staffs. Concerned employees are asked to explain the reasons

for any variance existing in the budgeting and overheads of employees.

Aging analysis- At the end of each month, recording of receivables and that are

entered in the computer system. Financial controller is further responsible for analysing the

trade receivables and trade receivable clerk should explain any delay made in payment to

debtors (Cannon & Bedard, 2016).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9AUDITING THEORY AND PRACTICE

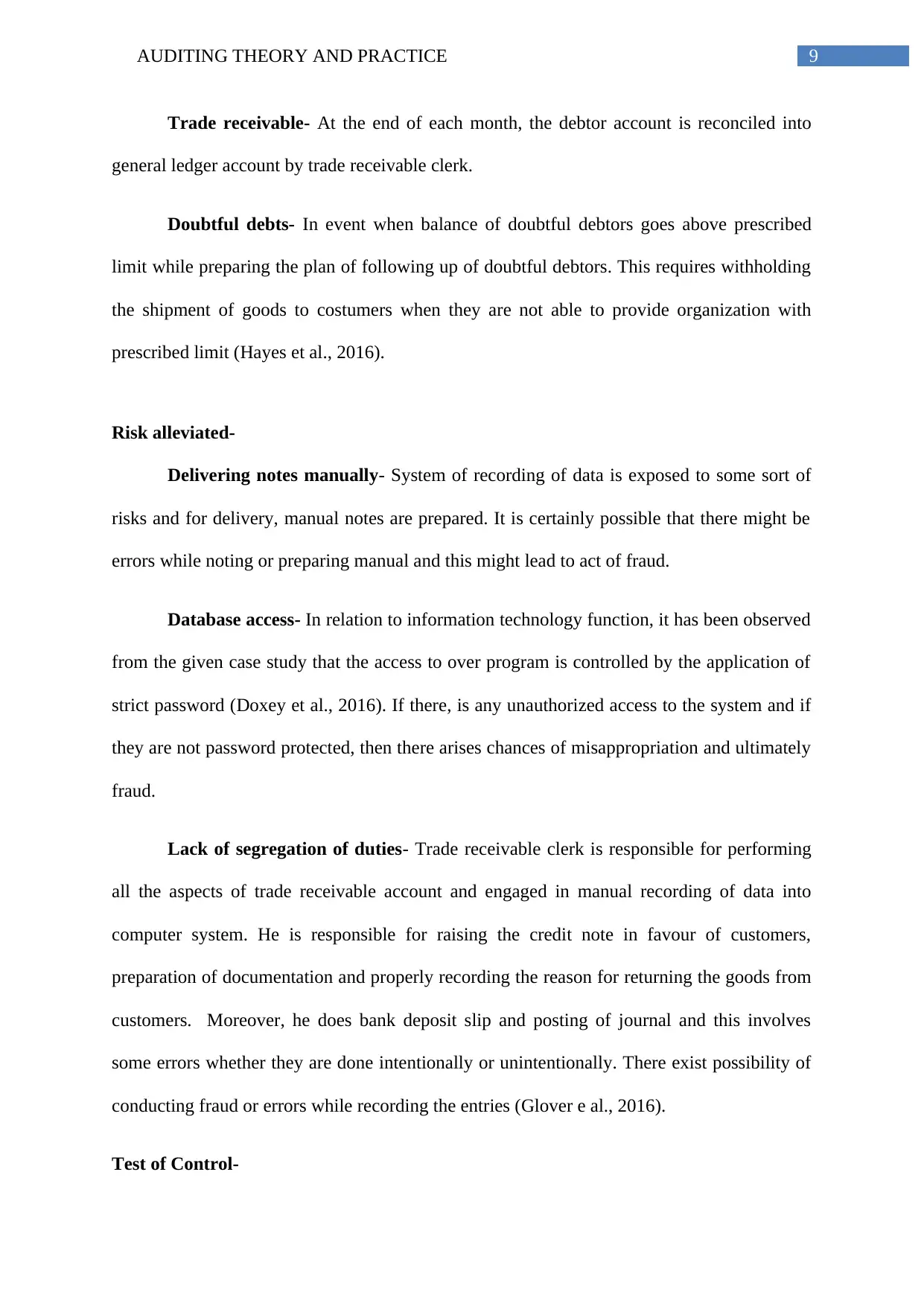

Trade receivable- At the end of each month, the debtor account is reconciled into

general ledger account by trade receivable clerk.

Doubtful debts- In event when balance of doubtful debtors goes above prescribed

limit while preparing the plan of following up of doubtful debtors. This requires withholding

the shipment of goods to costumers when they are not able to provide organization with

prescribed limit (Hayes et al., 2016).

Risk alleviated-

Delivering notes manually- System of recording of data is exposed to some sort of

risks and for delivery, manual notes are prepared. It is certainly possible that there might be

errors while noting or preparing manual and this might lead to act of fraud.

Database access- In relation to information technology function, it has been observed

from the given case study that the access to over program is controlled by the application of

strict password (Doxey et al., 2016). If there, is any unauthorized access to the system and if

they are not password protected, then there arises chances of misappropriation and ultimately

fraud.

Lack of segregation of duties- Trade receivable clerk is responsible for performing

all the aspects of trade receivable account and engaged in manual recording of data into

computer system. He is responsible for raising the credit note in favour of customers,

preparation of documentation and properly recording the reason for returning the goods from

customers. Moreover, he does bank deposit slip and posting of journal and this involves

some errors whether they are done intentionally or unintentionally. There exist possibility of

conducting fraud or errors while recording the entries (Glover e al., 2016).

Test of Control-

Trade receivable- At the end of each month, the debtor account is reconciled into

general ledger account by trade receivable clerk.

Doubtful debts- In event when balance of doubtful debtors goes above prescribed

limit while preparing the plan of following up of doubtful debtors. This requires withholding

the shipment of goods to costumers when they are not able to provide organization with

prescribed limit (Hayes et al., 2016).

Risk alleviated-

Delivering notes manually- System of recording of data is exposed to some sort of

risks and for delivery, manual notes are prepared. It is certainly possible that there might be

errors while noting or preparing manual and this might lead to act of fraud.

Database access- In relation to information technology function, it has been observed

from the given case study that the access to over program is controlled by the application of

strict password (Doxey et al., 2016). If there, is any unauthorized access to the system and if

they are not password protected, then there arises chances of misappropriation and ultimately

fraud.

Lack of segregation of duties- Trade receivable clerk is responsible for performing

all the aspects of trade receivable account and engaged in manual recording of data into

computer system. He is responsible for raising the credit note in favour of customers,

preparation of documentation and properly recording the reason for returning the goods from

customers. Moreover, he does bank deposit slip and posting of journal and this involves

some errors whether they are done intentionally or unintentionally. There exist possibility of

conducting fraud or errors while recording the entries (Glover e al., 2016).

Test of Control-

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10AUDITING THEORY AND PRACTICE

Test of control is used by auditors for analysing and evaluating the efficiency of

internal control system of organization. Level of reliance on internal control system of

organization is based on result and outcome of test conducted by auditors. The categorization

of test of control are discussed below:

Observation- Auditors under this category makes the analysis of efficiency of internal

control of organization and evaluating the business procedures that are in action.

Inspection- Under this, documents are examined with respect to internal control

authorization, stamps and signatures.

Performance- Internal control system of organization is checked in relation to any

new transactions involved in business.

In order to generate effective control in internal control system, some of test of

control are as follows-

Protection by passwords- in relation to protecting password, auditor will perform

inspection approach on control test.

Aging analysis- Auditor will perform inspection and observation approach.

Bonus payment- For this control test, auditor will perform observation approach

control test.

Trade receivable- Auditors will perform re performance approach control test

Doubtful debts- Auditors will perform re performance approach control test (Jia,

2016).

Test of control is used by auditors for analysing and evaluating the efficiency of

internal control system of organization. Level of reliance on internal control system of

organization is based on result and outcome of test conducted by auditors. The categorization

of test of control are discussed below:

Observation- Auditors under this category makes the analysis of efficiency of internal

control of organization and evaluating the business procedures that are in action.

Inspection- Under this, documents are examined with respect to internal control

authorization, stamps and signatures.

Performance- Internal control system of organization is checked in relation to any

new transactions involved in business.

In order to generate effective control in internal control system, some of test of

control are as follows-

Protection by passwords- in relation to protecting password, auditor will perform

inspection approach on control test.

Aging analysis- Auditor will perform inspection and observation approach.

Bonus payment- For this control test, auditor will perform observation approach

control test.

Trade receivable- Auditors will perform re performance approach control test

Doubtful debts- Auditors will perform re performance approach control test (Jia,

2016).

11AUDITING THEORY AND PRACTICE

Answer to question 2b:

Weakness in the internal control system of GPSA:

Internal control weakness Impact on audit Steps taken to reduce weakness

The recording of invoices are

done solely by trade receivable

clerk and he is responsible for

positing the journal and

reconciliation of accounts.

Risk might evolve while

maximization of sales revenue

and minimization of risks

(Knechel & Salterio, 2016).

Only trade receivable clerk

should not do the management

of all aspects of trade receivable

account and other should be two

or more person involved in

handling the accounts.

Management staff are receiving

bonuses based on targeted

volume of monthly sales,

departmental budget and

variation of sales overhead.

This type of weakness might led

to evolving of risks relating to

bonus payment to employees in

event when there is any non-

completed transactions.

Bonus amount should be

calculated irrespective of sales

made by sales department for

internal control check

facilitation.

Inefficiency in internal control

due to inappropriate recording

of data and journal entries by

trade receivable clerk

Several aspects of internal

control will significantly affect

audit, as there can be

misappropriation of data and

ultimately fraud.

System of internal control

should be made efficient by

segregating duties relating to all

aspects of trade receivable

account and sales system

(DeFond & Zhang, 2014).

Conclusion:

From the above analysis, it is depicted that the internal control system of GPSA

would be facilitated by creation of new internal control manual. This has made trade

receivable entitled to handling all data relating to such accounts. However, such system is

Answer to question 2b:

Weakness in the internal control system of GPSA:

Internal control weakness Impact on audit Steps taken to reduce weakness

The recording of invoices are

done solely by trade receivable

clerk and he is responsible for

positing the journal and

reconciliation of accounts.

Risk might evolve while

maximization of sales revenue

and minimization of risks

(Knechel & Salterio, 2016).

Only trade receivable clerk

should not do the management

of all aspects of trade receivable

account and other should be two

or more person involved in

handling the accounts.

Management staff are receiving

bonuses based on targeted

volume of monthly sales,

departmental budget and

variation of sales overhead.

This type of weakness might led

to evolving of risks relating to

bonus payment to employees in

event when there is any non-

completed transactions.

Bonus amount should be

calculated irrespective of sales

made by sales department for

internal control check

facilitation.

Inefficiency in internal control

due to inappropriate recording

of data and journal entries by

trade receivable clerk

Several aspects of internal

control will significantly affect

audit, as there can be

misappropriation of data and

ultimately fraud.

System of internal control

should be made efficient by

segregating duties relating to all

aspects of trade receivable

account and sales system

(DeFond & Zhang, 2014).

Conclusion:

From the above analysis, it is depicted that the internal control system of GPSA

would be facilitated by creation of new internal control manual. This has made trade

receivable entitled to handling all data relating to such accounts. However, such system is

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.