Trunkey Creek Wines Audit Program: An Audit Theory and Practice Report

VerifiedAdded on 2023/06/07

|20

|4625

|496

Report

AI Summary

This report details an audit program for Trunkey Creek Wines (TCW), a client of Miller Yates Howarth (MYH). It includes a business risk evaluation using liquidity, solvency, efficiency, and profitability ratios. Weaknesses in TCW's internal control systems for accounts payable and purchases are iden...

Running head: AUDITING THEORY AND PRACTICE

Auditing theory and practice

Name of the University

Name of the student

Authors note

Auditing theory and practice

Name of the University

Name of the student

Authors note

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1

AUDITING THEORY AND PRACTICE

Executive summary:

In the present study, the emphasis is placed on completing the audit program of one of the clients

of Miller Yates Howarth (MYH). Trunkey Creep Wines is the long standing clients of MYH that

has approached MYH for engaging in their audit plans by conducting the analysis of the

accounts. Business risks of TCW have been evaluated by analyzing the relevant ratios such as

liquidity, solvency, efficiency and profitability. Any weakness in the internal control systems of

account payable and purchase have been identified along with outlining one test of control. The

mitigation of audit risks faced by the accounts has been done by recommending the proper audit

steps.

AUDITING THEORY AND PRACTICE

Executive summary:

In the present study, the emphasis is placed on completing the audit program of one of the clients

of Miller Yates Howarth (MYH). Trunkey Creep Wines is the long standing clients of MYH that

has approached MYH for engaging in their audit plans by conducting the analysis of the

accounts. Business risks of TCW have been evaluated by analyzing the relevant ratios such as

liquidity, solvency, efficiency and profitability. Any weakness in the internal control systems of

account payable and purchase have been identified along with outlining one test of control. The

mitigation of audit risks faced by the accounts has been done by recommending the proper audit

steps.

2

AUDITING THEORY AND PRACTICE

Table of Contents

Introduction:....................................................................................................................................4

Discussion:.......................................................................................................................................4

Answer to question 1A:...................................................................................................................4

Answer to question 1B:...................................................................................................................4

Answer to question 2A:...................................................................................................................4

Answer to question 2B:...................................................................................................................4

Conclusion:......................................................................................................................................4

AUDITING THEORY AND PRACTICE

Table of Contents

Introduction:....................................................................................................................................4

Discussion:.......................................................................................................................................4

Answer to question 1A:...................................................................................................................4

Answer to question 1B:...................................................................................................................4

Answer to question 2A:...................................................................................................................4

Answer to question 2B:...................................................................................................................4

Conclusion:......................................................................................................................................4

You're viewing a preview

Unlock full access by subscribing today!

3

AUDITING THEORY AND PRACTICE

Introduction:

The report is prepared for demonstrating the audit plan of one of the long standing and

significant clients of Miller Yates Howarth that is the second largest accounting firm operating in

Australia. Trunkey Creep wines being one of the important audit clients have asked their

accounting firm to carry out the audit engagement. For this purpose, there are some areas of

concern that should be focused by the auditor and they are incorporated in completing the audit

program. These areas include several accounts of Trunkey Creep Wines such as investments,

accounts receivable, marketing expenses and property assets. The audit risks associate with these

accounts are analyzed and auditing steps to mitigate such risks have been presented in the report.

Moreover, the business risks faced by TCW have been evaluated by the implementation of ratio

analysis tool which is a quantitative analysis of the information contained in the financial report

of the company1. Several operating and financial aspects of company are evaluated with the help

of such tool which auditors find to be considerably relevant. The effectiveness of internal

control system has been evaluated along with identification of the respective test of control.

Discussion:

Answer to question 1A:

This section demonstrates the identification of potential audit risks associated with the

four accounts of Trunkey Creep Wines (TCW). Such analysis has been presented in the table

format with four columns with each column depicting accounts, their analysis, associated risk

1 Albring, Susan M., Randal J. Elder, and Xiaolu Xu. "Unexpected fees and the prediction of material weaknesses in

internal control over financial reporting." Journal of Accounting, Auditing & Finance (2016): 0148558X16662585.

AUDITING THEORY AND PRACTICE

Introduction:

The report is prepared for demonstrating the audit plan of one of the long standing and

significant clients of Miller Yates Howarth that is the second largest accounting firm operating in

Australia. Trunkey Creep wines being one of the important audit clients have asked their

accounting firm to carry out the audit engagement. For this purpose, there are some areas of

concern that should be focused by the auditor and they are incorporated in completing the audit

program. These areas include several accounts of Trunkey Creep Wines such as investments,

accounts receivable, marketing expenses and property assets. The audit risks associate with these

accounts are analyzed and auditing steps to mitigate such risks have been presented in the report.

Moreover, the business risks faced by TCW have been evaluated by the implementation of ratio

analysis tool which is a quantitative analysis of the information contained in the financial report

of the company1. Several operating and financial aspects of company are evaluated with the help

of such tool which auditors find to be considerably relevant. The effectiveness of internal

control system has been evaluated along with identification of the respective test of control.

Discussion:

Answer to question 1A:

This section demonstrates the identification of potential audit risks associated with the

four accounts of Trunkey Creep Wines (TCW). Such analysis has been presented in the table

format with four columns with each column depicting accounts, their analysis, associated risk

1 Albring, Susan M., Randal J. Elder, and Xiaolu Xu. "Unexpected fees and the prediction of material weaknesses in

internal control over financial reporting." Journal of Accounting, Auditing & Finance (2016): 0148558X16662585.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4

AUDITING THEORY AND PRACTICE

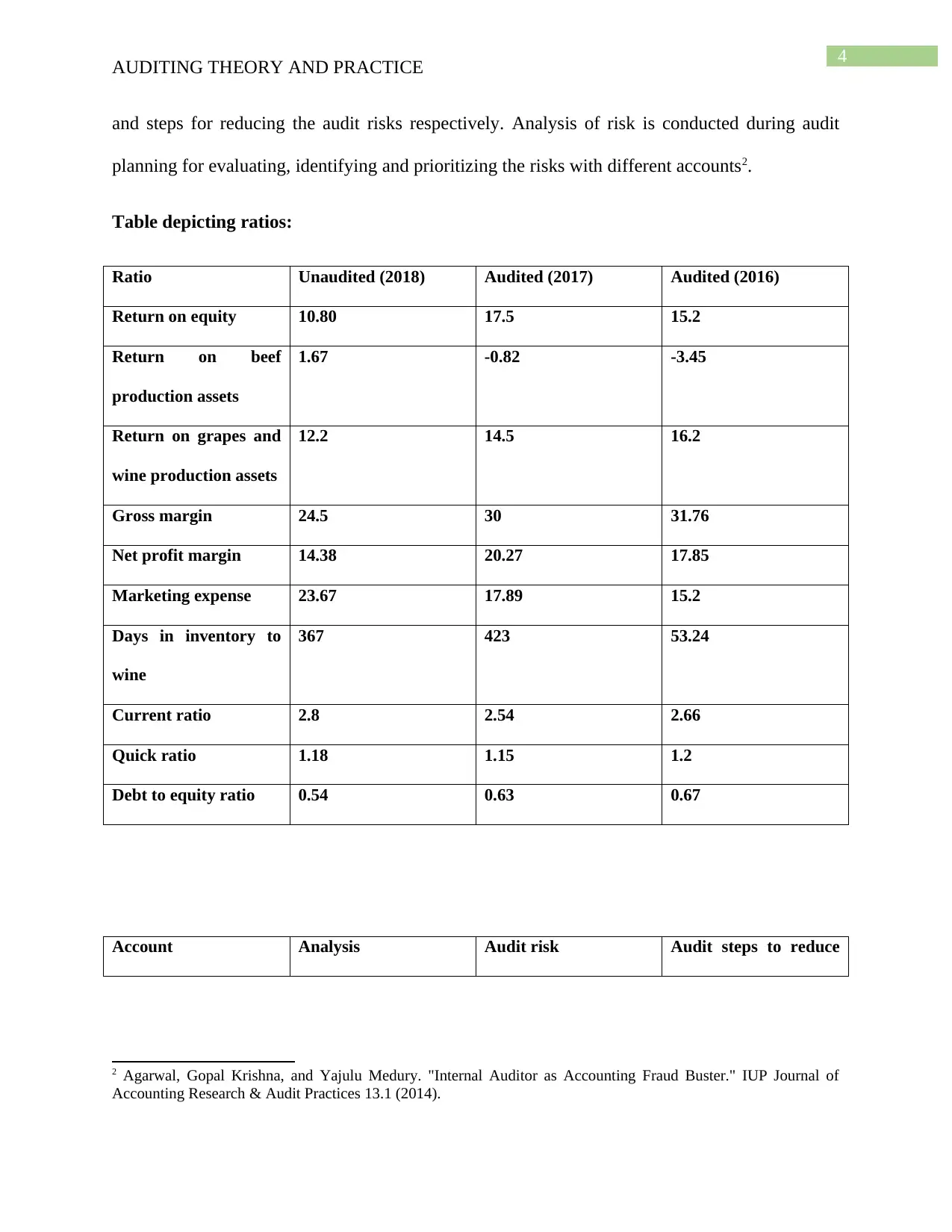

and steps for reducing the audit risks respectively. Analysis of risk is conducted during audit

planning for evaluating, identifying and prioritizing the risks with different accounts2.

Table depicting ratios:

Ratio Unaudited (2018) Audited (2017) Audited (2016)

Return on equity 10.80 17.5 15.2

Return on beef

production assets

1.67 -0.82 -3.45

Return on grapes and

wine production assets

12.2 14.5 16.2

Gross margin 24.5 30 31.76

Net profit margin 14.38 20.27 17.85

Marketing expense 23.67 17.89 15.2

Days in inventory to

wine

367 423 53.24

Current ratio 2.8 2.54 2.66

Quick ratio 1.18 1.15 1.2

Debt to equity ratio 0.54 0.63 0.67

Account Analysis Audit risk Audit steps to reduce

2 Agarwal, Gopal Krishna, and Yajulu Medury. "Internal Auditor as Accounting Fraud Buster." IUP Journal of

Accounting Research & Audit Practices 13.1 (2014).

AUDITING THEORY AND PRACTICE

and steps for reducing the audit risks respectively. Analysis of risk is conducted during audit

planning for evaluating, identifying and prioritizing the risks with different accounts2.

Table depicting ratios:

Ratio Unaudited (2018) Audited (2017) Audited (2016)

Return on equity 10.80 17.5 15.2

Return on beef

production assets

1.67 -0.82 -3.45

Return on grapes and

wine production assets

12.2 14.5 16.2

Gross margin 24.5 30 31.76

Net profit margin 14.38 20.27 17.85

Marketing expense 23.67 17.89 15.2

Days in inventory to

wine

367 423 53.24

Current ratio 2.8 2.54 2.66

Quick ratio 1.18 1.15 1.2

Debt to equity ratio 0.54 0.63 0.67

Account Analysis Audit risk Audit steps to reduce

2 Agarwal, Gopal Krishna, and Yajulu Medury. "Internal Auditor as Accounting Fraud Buster." IUP Journal of

Accounting Research & Audit Practices 13.1 (2014).

5

AUDITING THEORY AND PRACTICE

risk

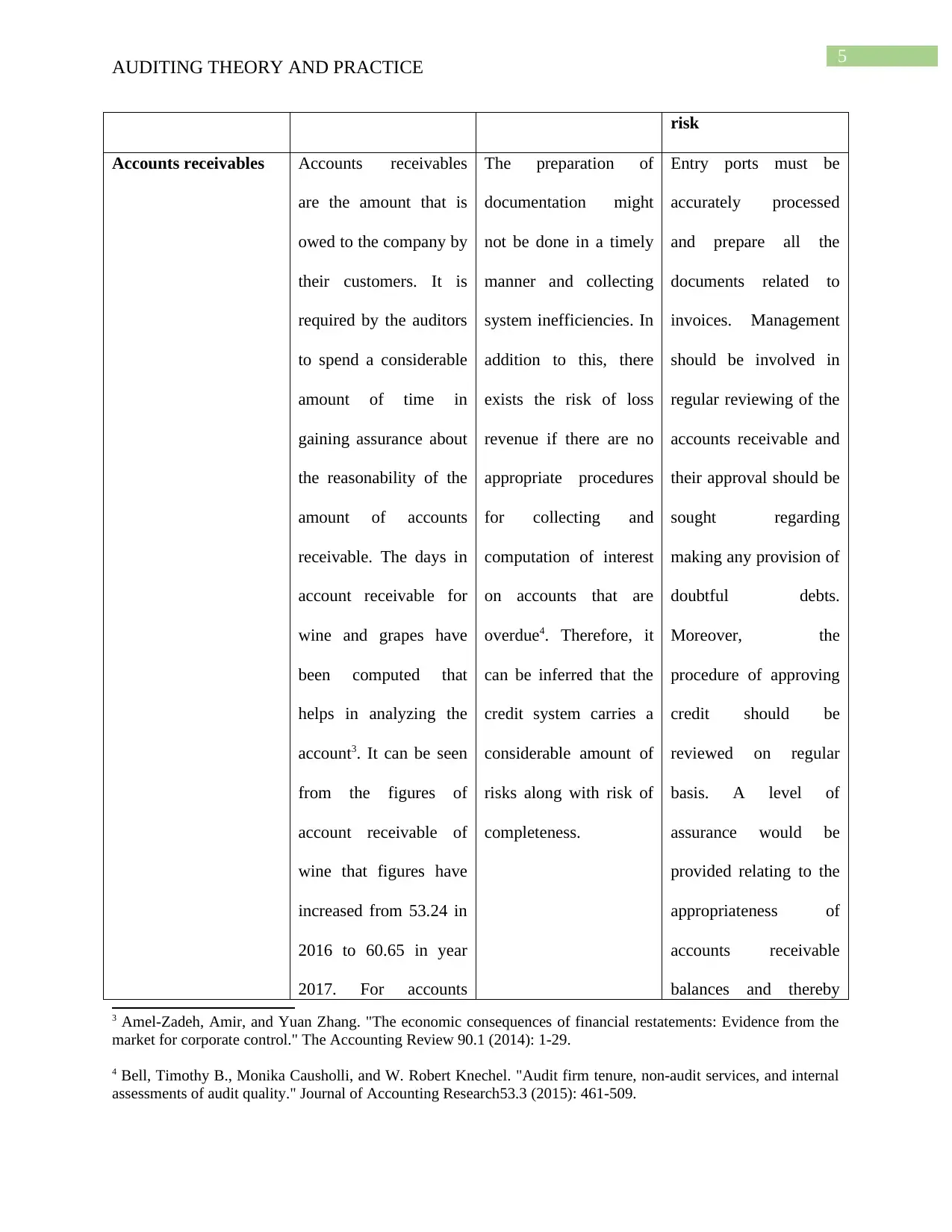

Accounts receivables Accounts receivables

are the amount that is

owed to the company by

their customers. It is

required by the auditors

to spend a considerable

amount of time in

gaining assurance about

the reasonability of the

amount of accounts

receivable. The days in

account receivable for

wine and grapes have

been computed that

helps in analyzing the

account3. It can be seen

from the figures of

account receivable of

wine that figures have

increased from 53.24 in

2016 to 60.65 in year

2017. For accounts

The preparation of

documentation might

not be done in a timely

manner and collecting

system inefficiencies. In

addition to this, there

exists the risk of loss

revenue if there are no

appropriate procedures

for collecting and

computation of interest

on accounts that are

overdue4. Therefore, it

can be inferred that the

credit system carries a

considerable amount of

risks along with risk of

completeness.

Entry ports must be

accurately processed

and prepare all the

documents related to

invoices. Management

should be involved in

regular reviewing of the

accounts receivable and

their approval should be

sought regarding

making any provision of

doubtful debts.

Moreover, the

procedure of approving

credit should be

reviewed on regular

basis. A level of

assurance would be

provided relating to the

appropriateness of

accounts receivable

balances and thereby

3 Amel-Zadeh, Amir, and Yuan Zhang. "The economic consequences of financial restatements: Evidence from the

market for corporate control." The Accounting Review 90.1 (2014): 1-29.

4 Bell, Timothy B., Monika Causholli, and W. Robert Knechel. "Audit firm tenure, non‐audit services, and internal

assessments of audit quality." Journal of Accounting Research53.3 (2015): 461-509.

AUDITING THEORY AND PRACTICE

risk

Accounts receivables Accounts receivables

are the amount that is

owed to the company by

their customers. It is

required by the auditors

to spend a considerable

amount of time in

gaining assurance about

the reasonability of the

amount of accounts

receivable. The days in

account receivable for

wine and grapes have

been computed that

helps in analyzing the

account3. It can be seen

from the figures of

account receivable of

wine that figures have

increased from 53.24 in

2016 to 60.65 in year

2017. For accounts

The preparation of

documentation might

not be done in a timely

manner and collecting

system inefficiencies. In

addition to this, there

exists the risk of loss

revenue if there are no

appropriate procedures

for collecting and

computation of interest

on accounts that are

overdue4. Therefore, it

can be inferred that the

credit system carries a

considerable amount of

risks along with risk of

completeness.

Entry ports must be

accurately processed

and prepare all the

documents related to

invoices. Management

should be involved in

regular reviewing of the

accounts receivable and

their approval should be

sought regarding

making any provision of

doubtful debts.

Moreover, the

procedure of approving

credit should be

reviewed on regular

basis. A level of

assurance would be

provided relating to the

appropriateness of

accounts receivable

balances and thereby

3 Amel-Zadeh, Amir, and Yuan Zhang. "The economic consequences of financial restatements: Evidence from the

market for corporate control." The Accounting Review 90.1 (2014): 1-29.

4 Bell, Timothy B., Monika Causholli, and W. Robert Knechel. "Audit firm tenure, non‐audit services, and internal

assessments of audit quality." Journal of Accounting Research53.3 (2015): 461-509.

You're viewing a preview

Unlock full access by subscribing today!

6

AUDITING THEORY AND PRACTICE

receivable of grapes,

figure have increased

from 24 to 36. This

increase in figures

depicts that the total

number of days to

collect receivables have

increased.

improving the accounts

receivable integrity.

Investments Analysis of audit risks

can be done by

evaluating the figures of

return on equity, return

on beef production asset

and return on wine and

grape production

assets5. There has been

increment in return

generated on equity

compared to return

generated on wine and

grapes production

assets.

The rate at which the

discounting of future

earnings has been done

might be a risk factor.

There can be reduced

working capital that

might impose practical

problem on liquidity

position of company.

Any amount of

investment that is

undertaken by TCW

should be evaluated in

terms of the total

amount invested and

comparison should be

made with the

availability of the liquid

money and cash

generated6. Management

of TCW should monitor

the investment account

on regular basis as part

of their operating

5 Brown-Liburd, Helen, Hussein Issa, and Danielle Lombardi. "Behavioral implications of Big Data's impact on

audit judgment and decision making and future research directions." Accounting Horizons 29.2 (2015): 451-468.

6 Cao, Min, Roman Chychyla, and Trevor Stewart. "Big Data analytics in financial statement audits." Accounting

Horizons29.2 (2015): 423-429.

AUDITING THEORY AND PRACTICE

receivable of grapes,

figure have increased

from 24 to 36. This

increase in figures

depicts that the total

number of days to

collect receivables have

increased.

improving the accounts

receivable integrity.

Investments Analysis of audit risks

can be done by

evaluating the figures of

return on equity, return

on beef production asset

and return on wine and

grape production

assets5. There has been

increment in return

generated on equity

compared to return

generated on wine and

grapes production

assets.

The rate at which the

discounting of future

earnings has been done

might be a risk factor.

There can be reduced

working capital that

might impose practical

problem on liquidity

position of company.

Any amount of

investment that is

undertaken by TCW

should be evaluated in

terms of the total

amount invested and

comparison should be

made with the

availability of the liquid

money and cash

generated6. Management

of TCW should monitor

the investment account

on regular basis as part

of their operating

5 Brown-Liburd, Helen, Hussein Issa, and Danielle Lombardi. "Behavioral implications of Big Data's impact on

audit judgment and decision making and future research directions." Accounting Horizons 29.2 (2015): 451-468.

6 Cao, Min, Roman Chychyla, and Trevor Stewart. "Big Data analytics in financial statement audits." Accounting

Horizons29.2 (2015): 423-429.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7

AUDITING THEORY AND PRACTICE

activities.

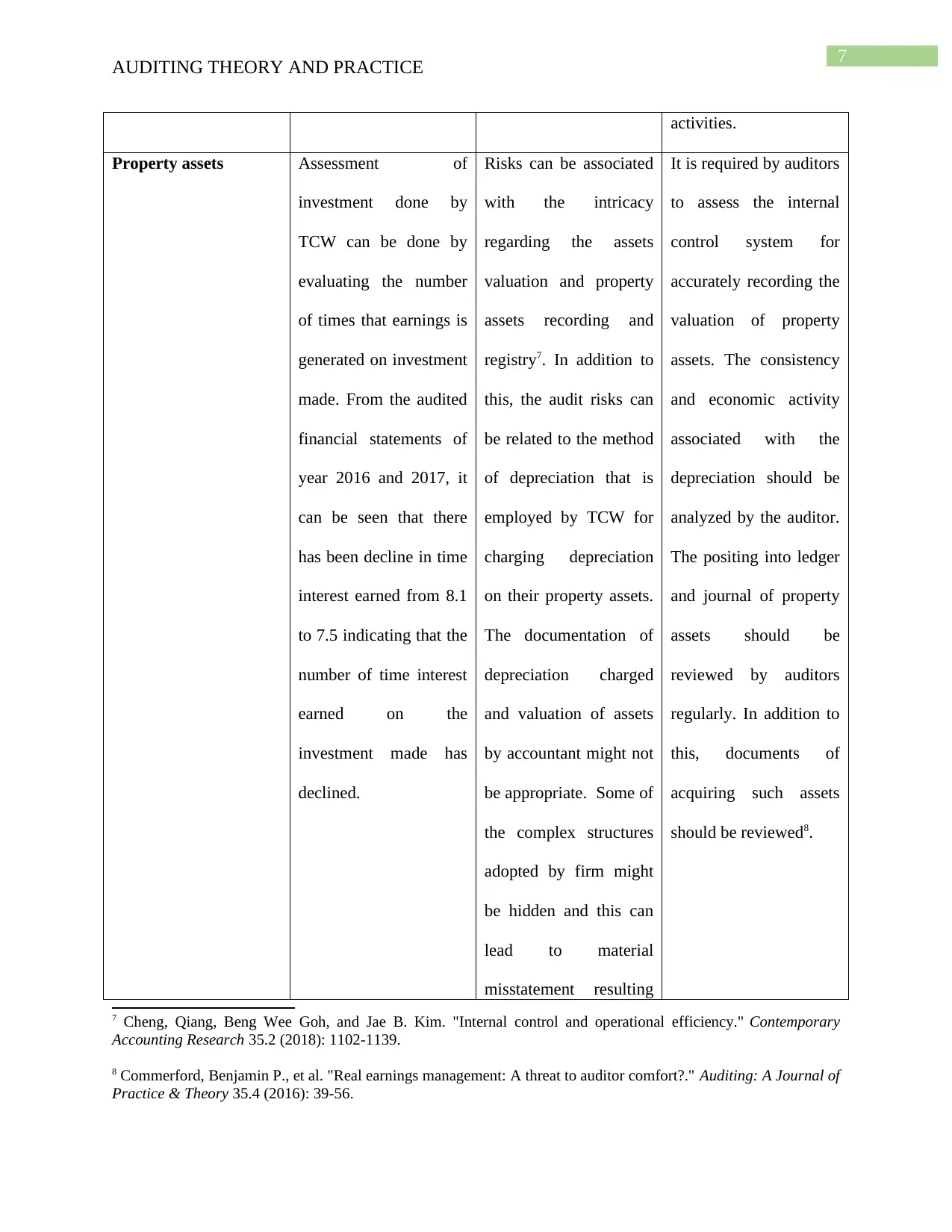

Property assets Assessment of

investment done by

TCW can be done by

evaluating the number

of times that earnings is

generated on investment

made. From the audited

financial statements of

year 2016 and 2017, it

can be seen that there

has been decline in time

interest earned from 8.1

to 7.5 indicating that the

number of time interest

earned on the

investment made has

declined.

Risks can be associated

with the intricacy

regarding the assets

valuation and property

assets recording and

registry7. In addition to

this, the audit risks can

be related to the method

of depreciation that is

employed by TCW for

charging depreciation

on their property assets.

The documentation of

depreciation charged

and valuation of assets

by accountant might not

be appropriate. Some of

the complex structures

adopted by firm might

be hidden and this can

lead to material

misstatement resulting

It is required by auditors

to assess the internal

control system for

accurately recording the

valuation of property

assets. The consistency

and economic activity

associated with the

depreciation should be

analyzed by the auditor.

The positing into ledger

and journal of property

assets should be

reviewed by auditors

regularly. In addition to

this, documents of

acquiring such assets

should be reviewed8.

7 Cheng, Qiang, Beng Wee Goh, and Jae B. Kim. "Internal control and operational efficiency." Contemporary

Accounting Research 35.2 (2018): 1102-1139.

8 Commerford, Benjamin P., et al. "Real earnings management: A threat to auditor comfort?." Auditing: A Journal of

Practice & Theory 35.4 (2016): 39-56.

AUDITING THEORY AND PRACTICE

activities.

Property assets Assessment of

investment done by

TCW can be done by

evaluating the number

of times that earnings is

generated on investment

made. From the audited

financial statements of

year 2016 and 2017, it

can be seen that there

has been decline in time

interest earned from 8.1

to 7.5 indicating that the

number of time interest

earned on the

investment made has

declined.

Risks can be associated

with the intricacy

regarding the assets

valuation and property

assets recording and

registry7. In addition to

this, the audit risks can

be related to the method

of depreciation that is

employed by TCW for

charging depreciation

on their property assets.

The documentation of

depreciation charged

and valuation of assets

by accountant might not

be appropriate. Some of

the complex structures

adopted by firm might

be hidden and this can

lead to material

misstatement resulting

It is required by auditors

to assess the internal

control system for

accurately recording the

valuation of property

assets. The consistency

and economic activity

associated with the

depreciation should be

analyzed by the auditor.

The positing into ledger

and journal of property

assets should be

reviewed by auditors

regularly. In addition to

this, documents of

acquiring such assets

should be reviewed8.

7 Cheng, Qiang, Beng Wee Goh, and Jae B. Kim. "Internal control and operational efficiency." Contemporary

Accounting Research 35.2 (2018): 1102-1139.

8 Commerford, Benjamin P., et al. "Real earnings management: A threat to auditor comfort?." Auditing: A Journal of

Practice & Theory 35.4 (2016): 39-56.

8

AUDITING THEORY AND PRACTICE

from overstatement of

exploration and

evaluation of assets.

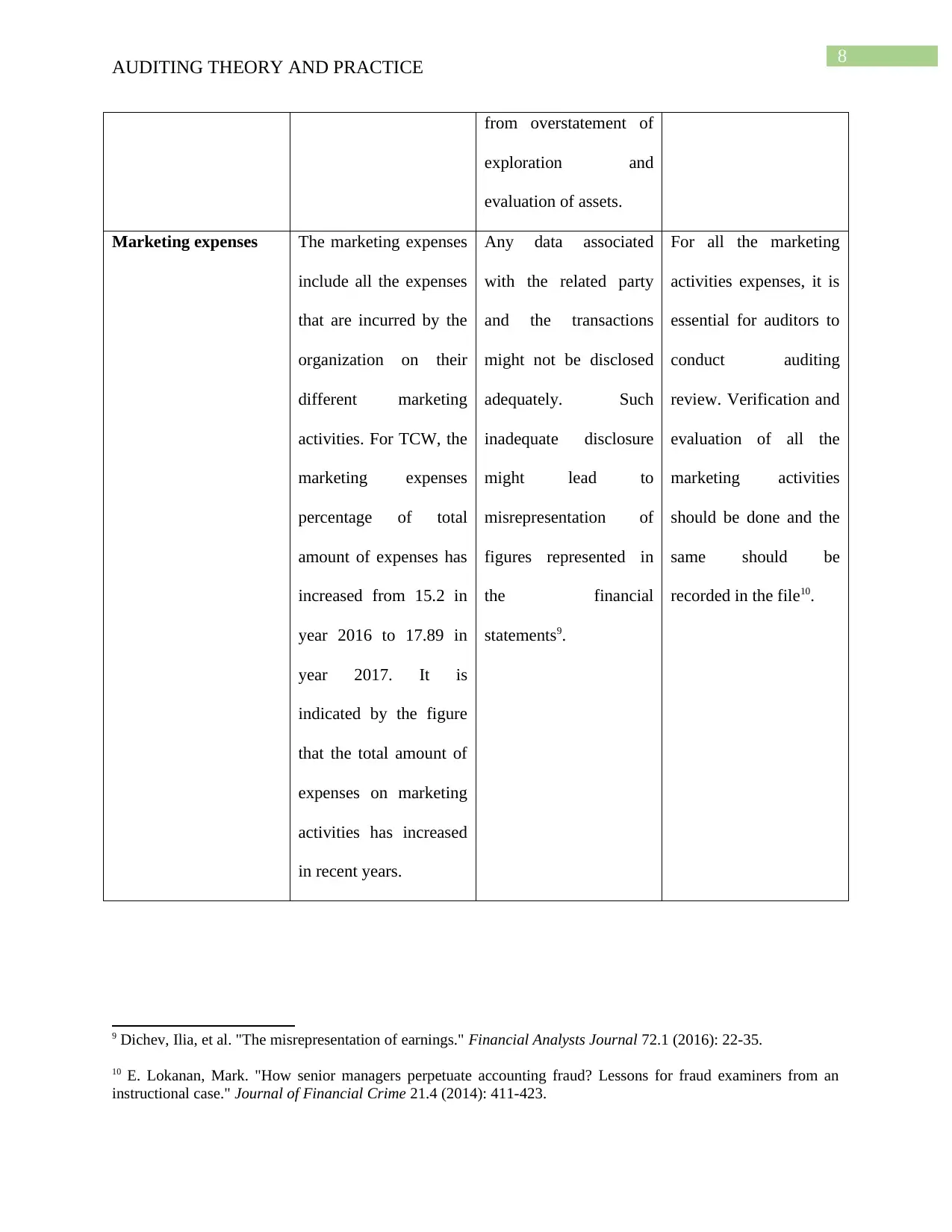

Marketing expenses The marketing expenses

include all the expenses

that are incurred by the

organization on their

different marketing

activities. For TCW, the

marketing expenses

percentage of total

amount of expenses has

increased from 15.2 in

year 2016 to 17.89 in

year 2017. It is

indicated by the figure

that the total amount of

expenses on marketing

activities has increased

in recent years.

Any data associated

with the related party

and the transactions

might not be disclosed

adequately. Such

inadequate disclosure

might lead to

misrepresentation of

figures represented in

the financial

statements9.

For all the marketing

activities expenses, it is

essential for auditors to

conduct auditing

review. Verification and

evaluation of all the

marketing activities

should be done and the

same should be

recorded in the file10.

9 Dichev, Ilia, et al. "The misrepresentation of earnings." Financial Analysts Journal 72.1 (2016): 22-35.

10 E. Lokanan, Mark. "How senior managers perpetuate accounting fraud? Lessons for fraud examiners from an

instructional case." Journal of Financial Crime 21.4 (2014): 411-423.

AUDITING THEORY AND PRACTICE

from overstatement of

exploration and

evaluation of assets.

Marketing expenses The marketing expenses

include all the expenses

that are incurred by the

organization on their

different marketing

activities. For TCW, the

marketing expenses

percentage of total

amount of expenses has

increased from 15.2 in

year 2016 to 17.89 in

year 2017. It is

indicated by the figure

that the total amount of

expenses on marketing

activities has increased

in recent years.

Any data associated

with the related party

and the transactions

might not be disclosed

adequately. Such

inadequate disclosure

might lead to

misrepresentation of

figures represented in

the financial

statements9.

For all the marketing

activities expenses, it is

essential for auditors to

conduct auditing

review. Verification and

evaluation of all the

marketing activities

should be done and the

same should be

recorded in the file10.

9 Dichev, Ilia, et al. "The misrepresentation of earnings." Financial Analysts Journal 72.1 (2016): 22-35.

10 E. Lokanan, Mark. "How senior managers perpetuate accounting fraud? Lessons for fraud examiners from an

instructional case." Journal of Financial Crime 21.4 (2014): 411-423.

You're viewing a preview

Unlock full access by subscribing today!

9

AUDITING THEORY AND PRACTICE

Answer to question 1B:

The business risks faced by TCW can be assessed by the analysis of different

ratios. Business risks faced by organization are driven by both internal and external factors.

Financial ratios play an important role in assessing the risks associated with the business.

Financial risks are generated from the nonpayment by clients or customers due to poor financial

projection and planning. Another risks faced by business can be due to the increasing proportion

of debt in their capital structure that would increase the financial leverage of business11.

Operating leverage risk- Risk related to the operating leverage faced by TCW can be

assessed by the evaluation of solvency ratios such as debt to equity ratio. For the audited

financial statements, it can be seen that the debt to equity ratio has decreased from 0.67 in year

2017 compared to 0.63 in year 2016 indicating that the proportion of borrowings in their capital

structure has reduced. If a company has reduced their dependence on borrowings, it a regarded as

positive sign and therefore the leverage risks of TCW has decreased.

Economic risk- Such risks arises from the external factors of economy such as change in

marketing conditions due to changing economic scenario. The negative changes in economic

conditions can lead to downturn of business in the form of reduced profit margin. The production

of sparkling wine has been affected by the climatic conditions of decreasing temperature.

Therefore, the reduced production of wine has affected the profits earned in domestic and

international markets. Therefore, the factors relating to economy and climatic conditions have

considerably impacted the profitability position of business and generated a risk of reduced

profit.

11 Glover, Steven M., Douglas F. Prawitt, and Michael S. Drake. "Between a rock and a hard place: A path forward

for using substantive analytical procedures in auditing large P&L accounts: Commentary and analysis." Auditing: A

Journal of Practice & Theory 34.3 (2014): 161-179.

AUDITING THEORY AND PRACTICE

Answer to question 1B:

The business risks faced by TCW can be assessed by the analysis of different

ratios. Business risks faced by organization are driven by both internal and external factors.

Financial ratios play an important role in assessing the risks associated with the business.

Financial risks are generated from the nonpayment by clients or customers due to poor financial

projection and planning. Another risks faced by business can be due to the increasing proportion

of debt in their capital structure that would increase the financial leverage of business11.

Operating leverage risk- Risk related to the operating leverage faced by TCW can be

assessed by the evaluation of solvency ratios such as debt to equity ratio. For the audited

financial statements, it can be seen that the debt to equity ratio has decreased from 0.67 in year

2017 compared to 0.63 in year 2016 indicating that the proportion of borrowings in their capital

structure has reduced. If a company has reduced their dependence on borrowings, it a regarded as

positive sign and therefore the leverage risks of TCW has decreased.

Economic risk- Such risks arises from the external factors of economy such as change in

marketing conditions due to changing economic scenario. The negative changes in economic

conditions can lead to downturn of business in the form of reduced profit margin. The production

of sparkling wine has been affected by the climatic conditions of decreasing temperature.

Therefore, the reduced production of wine has affected the profits earned in domestic and

international markets. Therefore, the factors relating to economy and climatic conditions have

considerably impacted the profitability position of business and generated a risk of reduced

profit.

11 Glover, Steven M., Douglas F. Prawitt, and Michael S. Drake. "Between a rock and a hard place: A path forward

for using substantive analytical procedures in auditing large P&L accounts: Commentary and analysis." Auditing: A

Journal of Practice & Theory 34.3 (2014): 161-179.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10

AUDITING THEORY AND PRACTICE

Reduced contribution margin- From the figures, it can be seen that there is decline in

both the gross and net profit margin. Gross profit margin has reduced from 31.76 in year 2017 to

30 in year 2016 and net profit margin has reduced from 17.85 in year 2016 to 14.38 in year 2018.

This fall in profitability margin of TCW can be attributable to the factors that are driven

externally such as economic downturn and this has led to reduced margin.

Risks associated with Credit control system- Business risk is also created by the

nonpayment made by clients resulting from the poor credit system. Such risk can results in

negative flow of cash and loss of income. The risks associated with the credit system of TCW

can be assessed by looking at the figures of days in accounts receivable for its product wine and

grapes. The days in accounts receivable for both wine and grapes has reduced considerably in

recent year. Such risks are of crucial importance to company because it helps in determining the

earnings and sales revenue made. For determining the seriousness of such risk, the credit status

of potential clients should be checked. The success generated should be monitored conducting

robust analytics and reporting systems and putting the process of credit control in place12.

Answer to question 2A:

In this section, the potential effectiveness of internal control system is evaluated along

with the identification of risks related to internal control system. For each of the identified

control, the test of control has been explained.

Effective control Risk alleviated Test of control

Preparation of supplier master All the information about The organization should exercise

12 Kim, Yeonkook J., Bok Baik, and Sungzoon Cho. "Detecting financial misstatements with fraud intention using

multi-class cost-sensitive learning." Expert systems with applications 62 (2016): 32-43.

AUDITING THEORY AND PRACTICE

Reduced contribution margin- From the figures, it can be seen that there is decline in

both the gross and net profit margin. Gross profit margin has reduced from 31.76 in year 2017 to

30 in year 2016 and net profit margin has reduced from 17.85 in year 2016 to 14.38 in year 2018.

This fall in profitability margin of TCW can be attributable to the factors that are driven

externally such as economic downturn and this has led to reduced margin.

Risks associated with Credit control system- Business risk is also created by the

nonpayment made by clients resulting from the poor credit system. Such risk can results in

negative flow of cash and loss of income. The risks associated with the credit system of TCW

can be assessed by looking at the figures of days in accounts receivable for its product wine and

grapes. The days in accounts receivable for both wine and grapes has reduced considerably in

recent year. Such risks are of crucial importance to company because it helps in determining the

earnings and sales revenue made. For determining the seriousness of such risk, the credit status

of potential clients should be checked. The success generated should be monitored conducting

robust analytics and reporting systems and putting the process of credit control in place12.

Answer to question 2A:

In this section, the potential effectiveness of internal control system is evaluated along

with the identification of risks related to internal control system. For each of the identified

control, the test of control has been explained.

Effective control Risk alleviated Test of control

Preparation of supplier master All the information about The organization should exercise

12 Kim, Yeonkook J., Bok Baik, and Sungzoon Cho. "Detecting financial misstatements with fraud intention using

multi-class cost-sensitive learning." Expert systems with applications 62 (2016): 32-43.

11

AUDITING THEORY AND PRACTICE

file suppliers are incorporated in the

master file and each supplier

carry a unique code. Rejection of

orders from an unapproved

suppliers are rejected which

lowers the risks of any wrong

sourcing of inputs. There would

be improvement in the accounts

payable process and thereby

improving its integrity. Any case

with discrepancies would be

detected with the help of creation

of such master file13.

security controls that are

stringent and some other

techniques such as record counts

and control totals should be done

by the auditors. Over the

amendment of any data, there

should be establishment of

adequate procedures. The

authority should be restricted to

the individual who are entrusted

to perform the activities and

performing duties accordingly14.

Computer ordering system The independent check

performed by the computer

ordering system helps in

reducing the errors probability.

There is a controlling on who

gets to read the information

which helps in ensuing the

confidentiality. Change in any

programs and information are

done in an authorized and

specific manner. Access to any

Opening of emails and deposit

preparation should be under

auditor’s observance. In order to

trace the deposits from the bank

and made to the bank should be

done by selecting a sample.

13 Knechel, W. Robert. "Audit quality and regulation." International Journal of Auditing 20.3 (2016): 215-223.

14 Kovács, Levente, and Sandor David. "Fraud risk in electronic payment transactions." Journal of Money

Laundering Control19.2 (2016): 148-157.

AUDITING THEORY AND PRACTICE

file suppliers are incorporated in the

master file and each supplier

carry a unique code. Rejection of

orders from an unapproved

suppliers are rejected which

lowers the risks of any wrong

sourcing of inputs. There would

be improvement in the accounts

payable process and thereby

improving its integrity. Any case

with discrepancies would be

detected with the help of creation

of such master file13.

security controls that are

stringent and some other

techniques such as record counts

and control totals should be done

by the auditors. Over the

amendment of any data, there

should be establishment of

adequate procedures. The

authority should be restricted to

the individual who are entrusted

to perform the activities and

performing duties accordingly14.

Computer ordering system The independent check

performed by the computer

ordering system helps in

reducing the errors probability.

There is a controlling on who

gets to read the information

which helps in ensuing the

confidentiality. Change in any

programs and information are

done in an authorized and

specific manner. Access to any

Opening of emails and deposit

preparation should be under

auditor’s observance. In order to

trace the deposits from the bank

and made to the bank should be

done by selecting a sample.

13 Knechel, W. Robert. "Audit quality and regulation." International Journal of Auditing 20.3 (2016): 215-223.

14 Kovács, Levente, and Sandor David. "Fraud risk in electronic payment transactions." Journal of Money

Laundering Control19.2 (2016): 148-157.

You're viewing a preview

Unlock full access by subscribing today!

12

AUDITING THEORY AND PRACTICE

programs is done by using

password which has lowered the

chance of conducting any fraud

activities by employees or any

other third party15.

Online approvals of payments

made

The completeness and accuracy

of accounting records is assured

by the implementation of such

system. In addition to this, the

effectiveness of control system is

ensured by the introduction of

online systems that would

contribute to the enhanced

internal control system by way of

elimination of theft and fraud

activities16.

In relation to any transactions

and standing data relating to the

online or computer system, there

should be controlling of

applications. Auditors should

evaluate record and ascertain

such applications so that any

misrepresentation of figures can

be detected easily17.

Appropriate and adequate

evaluation of invoices

Processing and receiving of

invoices in a timely fashion helps

in emphasizing the optimizing

the payable importance and

making the working capital free

that would help in fueling

growth. Automation of invoices

The testing of calculations and

assumptions should be done by

the auditors and the process of

control should be tested at

different stage. The latest

invoices record should be

obtained by the auditors at the

15 Albrecht, W. Steve, and Jeffrey L. Hoopes. "Why audits cannot detect all fraud." The CPA Journal 84.10 (2014):

16 Mazza, Tatiana, and Stefano Azzali. "Effects of internal audit quality on the severity and persistence of controls

deficiencies." International Journal of Auditing 19.3 (2015): 148-165.

17 Kassem, Rasha, and Andrew W. Higson. "External auditors and corporate corruption: Implications for external

audit regulators." Current Issues in Auditing 10.1 (2016): P1-P10.

AUDITING THEORY AND PRACTICE

programs is done by using

password which has lowered the

chance of conducting any fraud

activities by employees or any

other third party15.

Online approvals of payments

made

The completeness and accuracy

of accounting records is assured

by the implementation of such

system. In addition to this, the

effectiveness of control system is

ensured by the introduction of

online systems that would

contribute to the enhanced

internal control system by way of

elimination of theft and fraud

activities16.

In relation to any transactions

and standing data relating to the

online or computer system, there

should be controlling of

applications. Auditors should

evaluate record and ascertain

such applications so that any

misrepresentation of figures can

be detected easily17.

Appropriate and adequate

evaluation of invoices

Processing and receiving of

invoices in a timely fashion helps

in emphasizing the optimizing

the payable importance and

making the working capital free

that would help in fueling

growth. Automation of invoices

The testing of calculations and

assumptions should be done by

the auditors and the process of

control should be tested at

different stage. The latest

invoices record should be

obtained by the auditors at the

15 Albrecht, W. Steve, and Jeffrey L. Hoopes. "Why audits cannot detect all fraud." The CPA Journal 84.10 (2014):

16 Mazza, Tatiana, and Stefano Azzali. "Effects of internal audit quality on the severity and persistence of controls

deficiencies." International Journal of Auditing 19.3 (2015): 148-165.

17 Kassem, Rasha, and Andrew W. Higson. "External auditors and corporate corruption: Implications for external

audit regulators." Current Issues in Auditing 10.1 (2016): P1-P10.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

13

AUDITING THEORY AND PRACTICE

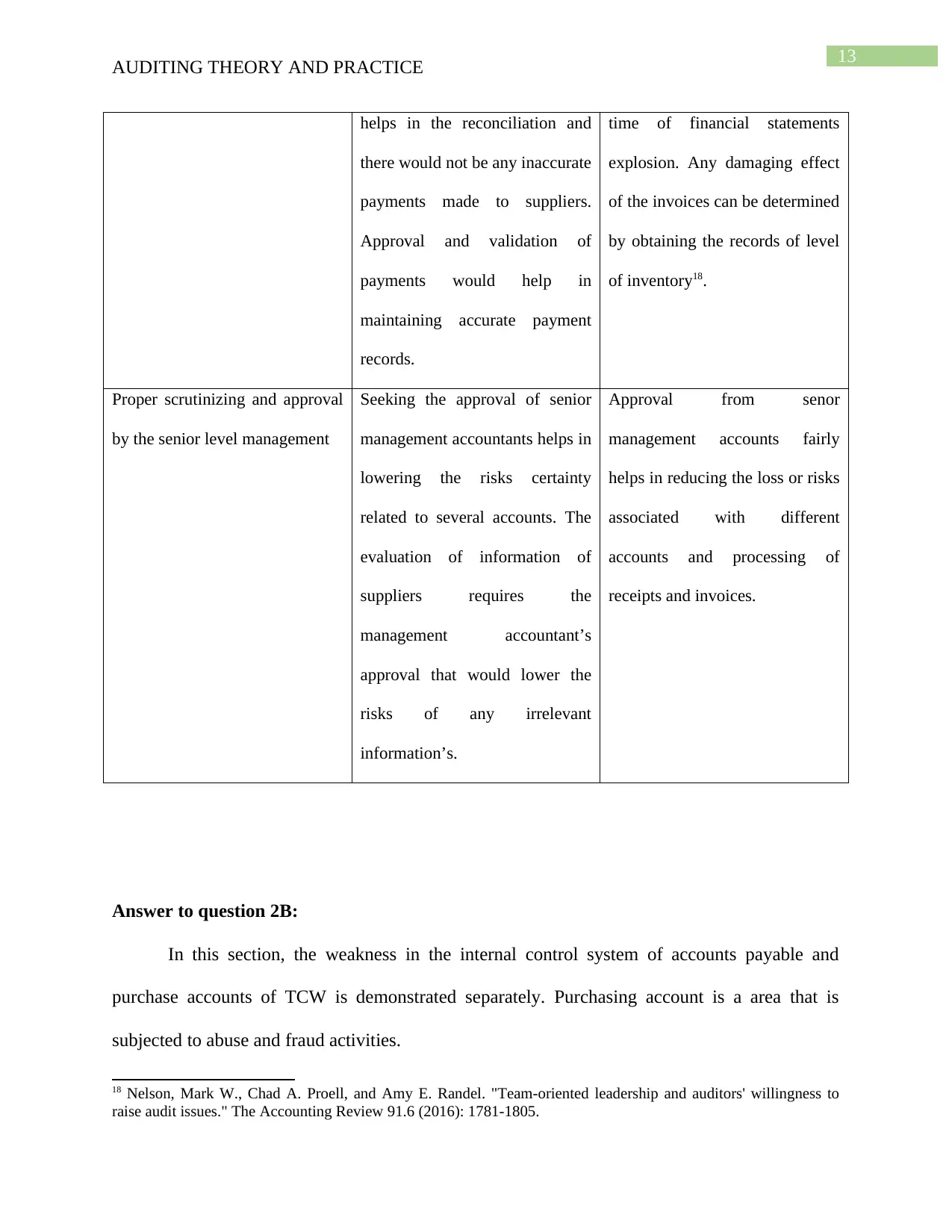

helps in the reconciliation and

there would not be any inaccurate

payments made to suppliers.

Approval and validation of

payments would help in

maintaining accurate payment

records.

time of financial statements

explosion. Any damaging effect

of the invoices can be determined

by obtaining the records of level

of inventory18.

Proper scrutinizing and approval

by the senior level management

Seeking the approval of senior

management accountants helps in

lowering the risks certainty

related to several accounts. The

evaluation of information of

suppliers requires the

management accountant’s

approval that would lower the

risks of any irrelevant

information’s.

Approval from senor

management accounts fairly

helps in reducing the loss or risks

associated with different

accounts and processing of

receipts and invoices.

Answer to question 2B:

In this section, the weakness in the internal control system of accounts payable and

purchase accounts of TCW is demonstrated separately. Purchasing account is a area that is

subjected to abuse and fraud activities.

18 Nelson, Mark W., Chad A. Proell, and Amy E. Randel. "Team-oriented leadership and auditors' willingness to

raise audit issues." The Accounting Review 91.6 (2016): 1781-1805.

AUDITING THEORY AND PRACTICE

helps in the reconciliation and

there would not be any inaccurate

payments made to suppliers.

Approval and validation of

payments would help in

maintaining accurate payment

records.

time of financial statements

explosion. Any damaging effect

of the invoices can be determined

by obtaining the records of level

of inventory18.

Proper scrutinizing and approval

by the senior level management

Seeking the approval of senior

management accountants helps in

lowering the risks certainty

related to several accounts. The

evaluation of information of

suppliers requires the

management accountant’s

approval that would lower the

risks of any irrelevant

information’s.

Approval from senor

management accounts fairly

helps in reducing the loss or risks

associated with different

accounts and processing of

receipts and invoices.

Answer to question 2B:

In this section, the weakness in the internal control system of accounts payable and

purchase accounts of TCW is demonstrated separately. Purchasing account is a area that is

subjected to abuse and fraud activities.

18 Nelson, Mark W., Chad A. Proell, and Amy E. Randel. "Team-oriented leadership and auditors' willingness to

raise audit issues." The Accounting Review 91.6 (2016): 1781-1805.

14

AUDITING THEORY AND PRACTICE

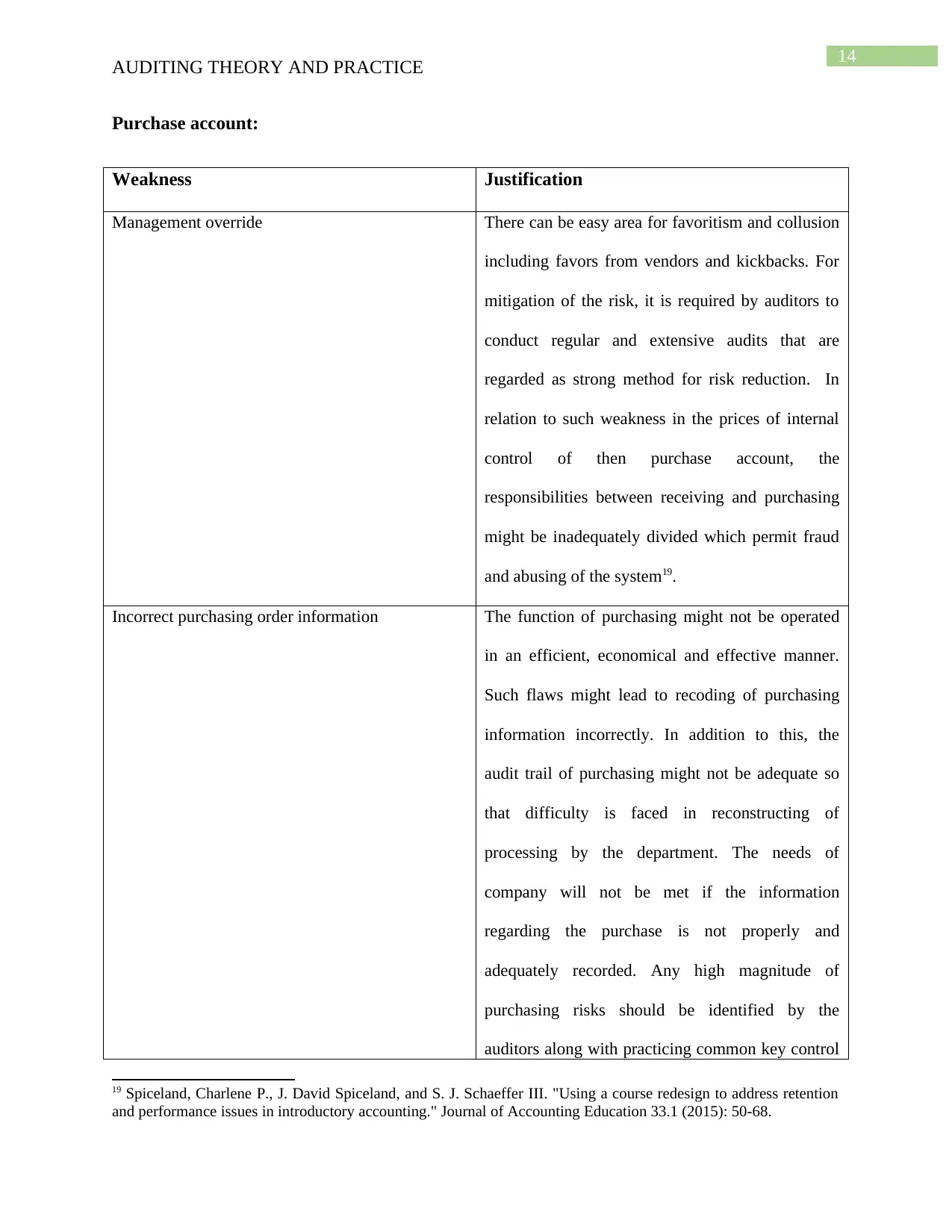

Purchase account:

Weakness Justification

Management override There can be easy area for favoritism and collusion

including favors from vendors and kickbacks. For

mitigation of the risk, it is required by auditors to

conduct regular and extensive audits that are

regarded as strong method for risk reduction. In

relation to such weakness in the prices of internal

control of then purchase account, the

responsibilities between receiving and purchasing

might be inadequately divided which permit fraud

and abusing of the system19.

Incorrect purchasing order information The function of purchasing might not be operated

in an efficient, economical and effective manner.

Such flaws might lead to recoding of purchasing

information incorrectly. In addition to this, the

audit trail of purchasing might not be adequate so

that difficulty is faced in reconstructing of

processing by the department. The needs of

company will not be met if the information

regarding the purchase is not properly and

adequately recorded. Any high magnitude of

purchasing risks should be identified by the

auditors along with practicing common key control

19 Spiceland, Charlene P., J. David Spiceland, and S. J. Schaeffer III. "Using a course redesign to address retention

and performance issues in introductory accounting." Journal of Accounting Education 33.1 (2015): 50-68.

AUDITING THEORY AND PRACTICE

Purchase account:

Weakness Justification

Management override There can be easy area for favoritism and collusion

including favors from vendors and kickbacks. For

mitigation of the risk, it is required by auditors to

conduct regular and extensive audits that are

regarded as strong method for risk reduction. In

relation to such weakness in the prices of internal

control of then purchase account, the

responsibilities between receiving and purchasing

might be inadequately divided which permit fraud

and abusing of the system19.

Incorrect purchasing order information The function of purchasing might not be operated

in an efficient, economical and effective manner.

Such flaws might lead to recoding of purchasing

information incorrectly. In addition to this, the

audit trail of purchasing might not be adequate so

that difficulty is faced in reconstructing of

processing by the department. The needs of

company will not be met if the information

regarding the purchase is not properly and

adequately recorded. Any high magnitude of

purchasing risks should be identified by the

auditors along with practicing common key control

19 Spiceland, Charlene P., J. David Spiceland, and S. J. Schaeffer III. "Using a course redesign to address retention

and performance issues in introductory accounting." Journal of Accounting Education 33.1 (2015): 50-68.

You're viewing a preview

Unlock full access by subscribing today!

15

AUDITING THEORY AND PRACTICE

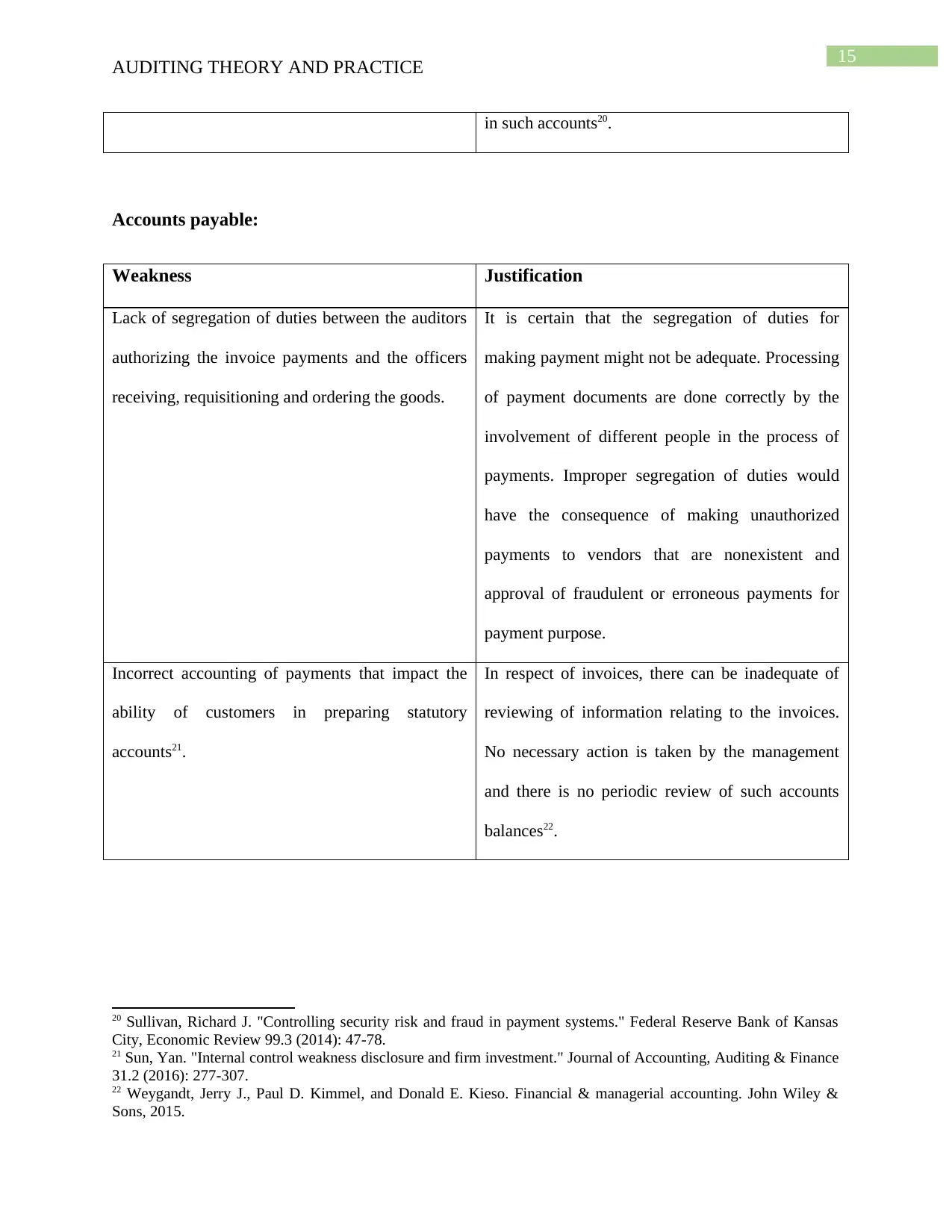

in such accounts20.

Accounts payable:

Weakness Justification

Lack of segregation of duties between the auditors

authorizing the invoice payments and the officers

receiving, requisitioning and ordering the goods.

It is certain that the segregation of duties for

making payment might not be adequate. Processing

of payment documents are done correctly by the

involvement of different people in the process of

payments. Improper segregation of duties would

have the consequence of making unauthorized

payments to vendors that are nonexistent and

approval of fraudulent or erroneous payments for

payment purpose.

Incorrect accounting of payments that impact the

ability of customers in preparing statutory

accounts21.

In respect of invoices, there can be inadequate of

reviewing of information relating to the invoices.

No necessary action is taken by the management

and there is no periodic review of such accounts

balances22.

20 Sullivan, Richard J. "Controlling security risk and fraud in payment systems." Federal Reserve Bank of Kansas

City, Economic Review 99.3 (2014): 47-78.

21 Sun, Yan. "Internal control weakness disclosure and firm investment." Journal of Accounting, Auditing & Finance

31.2 (2016): 277-307.

22 Weygandt, Jerry J., Paul D. Kimmel, and Donald E. Kieso. Financial & managerial accounting. John Wiley &

Sons, 2015.

AUDITING THEORY AND PRACTICE

in such accounts20.

Accounts payable:

Weakness Justification

Lack of segregation of duties between the auditors

authorizing the invoice payments and the officers

receiving, requisitioning and ordering the goods.

It is certain that the segregation of duties for

making payment might not be adequate. Processing

of payment documents are done correctly by the

involvement of different people in the process of

payments. Improper segregation of duties would

have the consequence of making unauthorized

payments to vendors that are nonexistent and

approval of fraudulent or erroneous payments for

payment purpose.

Incorrect accounting of payments that impact the

ability of customers in preparing statutory

accounts21.

In respect of invoices, there can be inadequate of

reviewing of information relating to the invoices.

No necessary action is taken by the management

and there is no periodic review of such accounts

balances22.

20 Sullivan, Richard J. "Controlling security risk and fraud in payment systems." Federal Reserve Bank of Kansas

City, Economic Review 99.3 (2014): 47-78.

21 Sun, Yan. "Internal control weakness disclosure and firm investment." Journal of Accounting, Auditing & Finance

31.2 (2016): 277-307.

22 Weygandt, Jerry J., Paul D. Kimmel, and Donald E. Kieso. Financial & managerial accounting. John Wiley &

Sons, 2015.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

16

AUDITING THEORY AND PRACTICE

Conclusion:

From the above discussion relating to the audit plan of TCW, there have been various

illustrations depicting the audit risks associated with several accounts. Assessment of the audit

risks by MYH has been done by the tool of ratios that have helped in identification of specific

risks related to accounts such as investment, marketing expenses, property assets and accounts

receivable. Evaluation of the accounts has led to the identification of the fact that the liquidity

position of company have declined. Furthermore, the implementation of the computerized

accounting system has found to be effective and efficient in recording in different accounts.

Nevertheless, they suffer from some of the weakness in their internal control system. The

accounts payable and purchase accounts suffer from several weaknesses relating to the

management, incorrect recording, management override and segregation of duties. Therefore, the

internal control systems need to be further enhanced by the employment of appropriate auditing

techniques.

Reference list:

Agarwal, Gopal Krishna, and Yajulu Medury. "Internal Auditor as Accounting Fraud

Buster." IUP Journal of Accounting Research & Audit Practices 13.1 (2014).

AUDITING THEORY AND PRACTICE

Conclusion:

From the above discussion relating to the audit plan of TCW, there have been various

illustrations depicting the audit risks associated with several accounts. Assessment of the audit

risks by MYH has been done by the tool of ratios that have helped in identification of specific

risks related to accounts such as investment, marketing expenses, property assets and accounts

receivable. Evaluation of the accounts has led to the identification of the fact that the liquidity

position of company have declined. Furthermore, the implementation of the computerized

accounting system has found to be effective and efficient in recording in different accounts.

Nevertheless, they suffer from some of the weakness in their internal control system. The

accounts payable and purchase accounts suffer from several weaknesses relating to the

management, incorrect recording, management override and segregation of duties. Therefore, the

internal control systems need to be further enhanced by the employment of appropriate auditing

techniques.

Reference list:

Agarwal, Gopal Krishna, and Yajulu Medury. "Internal Auditor as Accounting Fraud

Buster." IUP Journal of Accounting Research & Audit Practices 13.1 (2014).

17

AUDITING THEORY AND PRACTICE

Albrecht, W. Steve, and Jeffrey L. Hoopes. "Why audits cannot detect all fraud." The CPA

Journal 84.10 (2014): 12.

Albring, Susan M., Randal J. Elder, and Xiaolu Xu. "Unexpected fees and the prediction of

material weaknesses in internal control over financial reporting." Journal of Accounting,

Auditing & Finance (2016): 0148558X16662585.

Amel-Zadeh, Amir, and Yuan Zhang. "The economic consequences of financial restatements:

Evidence from the market for corporate control." The Accounting Review 90.1 (2014): 1-29.

Bell, Timothy B., Monika Causholli, and W. Robert Knechel. "Audit firm tenure, non‐audit

services, and internal assessments of audit quality." Journal of Accounting Research53.3 (2015):

461-509.

Brown-Liburd, Helen, Hussein Issa, and Danielle Lombardi. "Behavioral implications of Big

Data's impact on audit judgment and decision making and future research

directions." Accounting Horizons 29.2 (2015): 451-468.

Cao, Min, Roman Chychyla, and Trevor Stewart. "Big Data analytics in financial statement

audits." Accounting Horizons29.2 (2015): 423-429.

Cheng, Qiang, Beng Wee Goh, and Jae B. Kim. "Internal control and operational

efficiency." Contemporary Accounting Research 35.2 (2018): 1102-1139.

Commerford, Benjamin P., et al. "Real earnings management: A threat to auditor

comfort?." Auditing: A Journal of Practice & Theory 35.4 (2016): 39-56.

Dichev, Ilia, et al. "The misrepresentation of earnings." Financial Analysts Journal 72.1 (2016):

22-35.

AUDITING THEORY AND PRACTICE

Albrecht, W. Steve, and Jeffrey L. Hoopes. "Why audits cannot detect all fraud." The CPA

Journal 84.10 (2014): 12.

Albring, Susan M., Randal J. Elder, and Xiaolu Xu. "Unexpected fees and the prediction of

material weaknesses in internal control over financial reporting." Journal of Accounting,

Auditing & Finance (2016): 0148558X16662585.

Amel-Zadeh, Amir, and Yuan Zhang. "The economic consequences of financial restatements:

Evidence from the market for corporate control." The Accounting Review 90.1 (2014): 1-29.

Bell, Timothy B., Monika Causholli, and W. Robert Knechel. "Audit firm tenure, non‐audit

services, and internal assessments of audit quality." Journal of Accounting Research53.3 (2015):

461-509.

Brown-Liburd, Helen, Hussein Issa, and Danielle Lombardi. "Behavioral implications of Big

Data's impact on audit judgment and decision making and future research

directions." Accounting Horizons 29.2 (2015): 451-468.

Cao, Min, Roman Chychyla, and Trevor Stewart. "Big Data analytics in financial statement

audits." Accounting Horizons29.2 (2015): 423-429.

Cheng, Qiang, Beng Wee Goh, and Jae B. Kim. "Internal control and operational

efficiency." Contemporary Accounting Research 35.2 (2018): 1102-1139.

Commerford, Benjamin P., et al. "Real earnings management: A threat to auditor

comfort?." Auditing: A Journal of Practice & Theory 35.4 (2016): 39-56.

Dichev, Ilia, et al. "The misrepresentation of earnings." Financial Analysts Journal 72.1 (2016):

22-35.

You're viewing a preview

Unlock full access by subscribing today!

18

AUDITING THEORY AND PRACTICE

E. Lokanan, Mark. "How senior managers perpetuate accounting fraud? Lessons for fraud

examiners from an instructional case." Journal of Financial Crime 21.4 (2014): 411-423.

Glover, Steven M., Douglas F. Prawitt, and Michael S. Drake. "Between a rock and a hard place:

A path forward for using substantive analytical procedures in auditing large P&L accounts:

Commentary and analysis." Auditing: A Journal of Practice & Theory 34.3 (2014): 161-179.

Kassem, Rasha, and Andrew W. Higson. "External auditors and corporate corruption:

Implications for external audit regulators." Current Issues in Auditing 10.1 (2016): P1-P10.

Kim, Yeonkook J., Bok Baik, and Sungzoon Cho. "Detecting financial misstatements with fraud

intention using multi-class cost-sensitive learning." Expert systems with applications 62 (2016):

32-43.

Knechel, W. Robert. "Audit quality and regulation." International Journal of Auditing 20.3

(2016): 215-223.

Kovács, Levente, and Sandor David. "Fraud risk in electronic payment transactions." Journal of

Money Laundering Control19.2 (2016): 148-157.

Mazza, Tatiana, and Stefano Azzali. "Effects of internal audit quality on the severity and

persistence of controls deficiencies." International Journal of Auditing 19.3 (2015): 148-165.

Nelson, Mark W., Chad A. Proell, and Amy E. Randel. "Team-oriented leadership and auditors'

willingness to raise audit issues." The Accounting Review 91.6 (2016): 1781-1805.

Spiceland, Charlene P., J. David Spiceland, and S. J. Schaeffer III. "Using a course redesign to

address retention and performance issues in introductory accounting." Journal of Accounting

Education 33.1 (2015): 50-68.

AUDITING THEORY AND PRACTICE

E. Lokanan, Mark. "How senior managers perpetuate accounting fraud? Lessons for fraud

examiners from an instructional case." Journal of Financial Crime 21.4 (2014): 411-423.

Glover, Steven M., Douglas F. Prawitt, and Michael S. Drake. "Between a rock and a hard place:

A path forward for using substantive analytical procedures in auditing large P&L accounts:

Commentary and analysis." Auditing: A Journal of Practice & Theory 34.3 (2014): 161-179.

Kassem, Rasha, and Andrew W. Higson. "External auditors and corporate corruption:

Implications for external audit regulators." Current Issues in Auditing 10.1 (2016): P1-P10.

Kim, Yeonkook J., Bok Baik, and Sungzoon Cho. "Detecting financial misstatements with fraud

intention using multi-class cost-sensitive learning." Expert systems with applications 62 (2016):

32-43.

Knechel, W. Robert. "Audit quality and regulation." International Journal of Auditing 20.3

(2016): 215-223.

Kovács, Levente, and Sandor David. "Fraud risk in electronic payment transactions." Journal of

Money Laundering Control19.2 (2016): 148-157.

Mazza, Tatiana, and Stefano Azzali. "Effects of internal audit quality on the severity and

persistence of controls deficiencies." International Journal of Auditing 19.3 (2015): 148-165.

Nelson, Mark W., Chad A. Proell, and Amy E. Randel. "Team-oriented leadership and auditors'

willingness to raise audit issues." The Accounting Review 91.6 (2016): 1781-1805.

Spiceland, Charlene P., J. David Spiceland, and S. J. Schaeffer III. "Using a course redesign to

address retention and performance issues in introductory accounting." Journal of Accounting

Education 33.1 (2015): 50-68.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

19

AUDITING THEORY AND PRACTICE

Sullivan, Richard J. "Controlling security risk and fraud in payment systems." Federal Reserve

Bank of Kansas City, Economic Review 99.3 (2014): 47-78.

Sun, Yan. "Internal control weakness disclosure and firm investment." Journal of Accounting,

Auditing & Finance 31.2 (2016): 277-307.

Weygandt, Jerry J., Paul D. Kimmel, and Donald E. Kieso. Financial & managerial accounting.

John Wiley & Sons, 2015.

AUDITING THEORY AND PRACTICE

Sullivan, Richard J. "Controlling security risk and fraud in payment systems." Federal Reserve

Bank of Kansas City, Economic Review 99.3 (2014): 47-78.

Sun, Yan. "Internal control weakness disclosure and firm investment." Journal of Accounting,

Auditing & Finance 31.2 (2016): 277-307.

Weygandt, Jerry J., Paul D. Kimmel, and Donald E. Kieso. Financial & managerial accounting.

John Wiley & Sons, 2015.

1 out of 20

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.