Capital Budgeting Analysis of Auditizz Electronics Project - ACC211

VerifiedAdded on 2023/04/03

|8

|1382

|496

Report

AI Summary

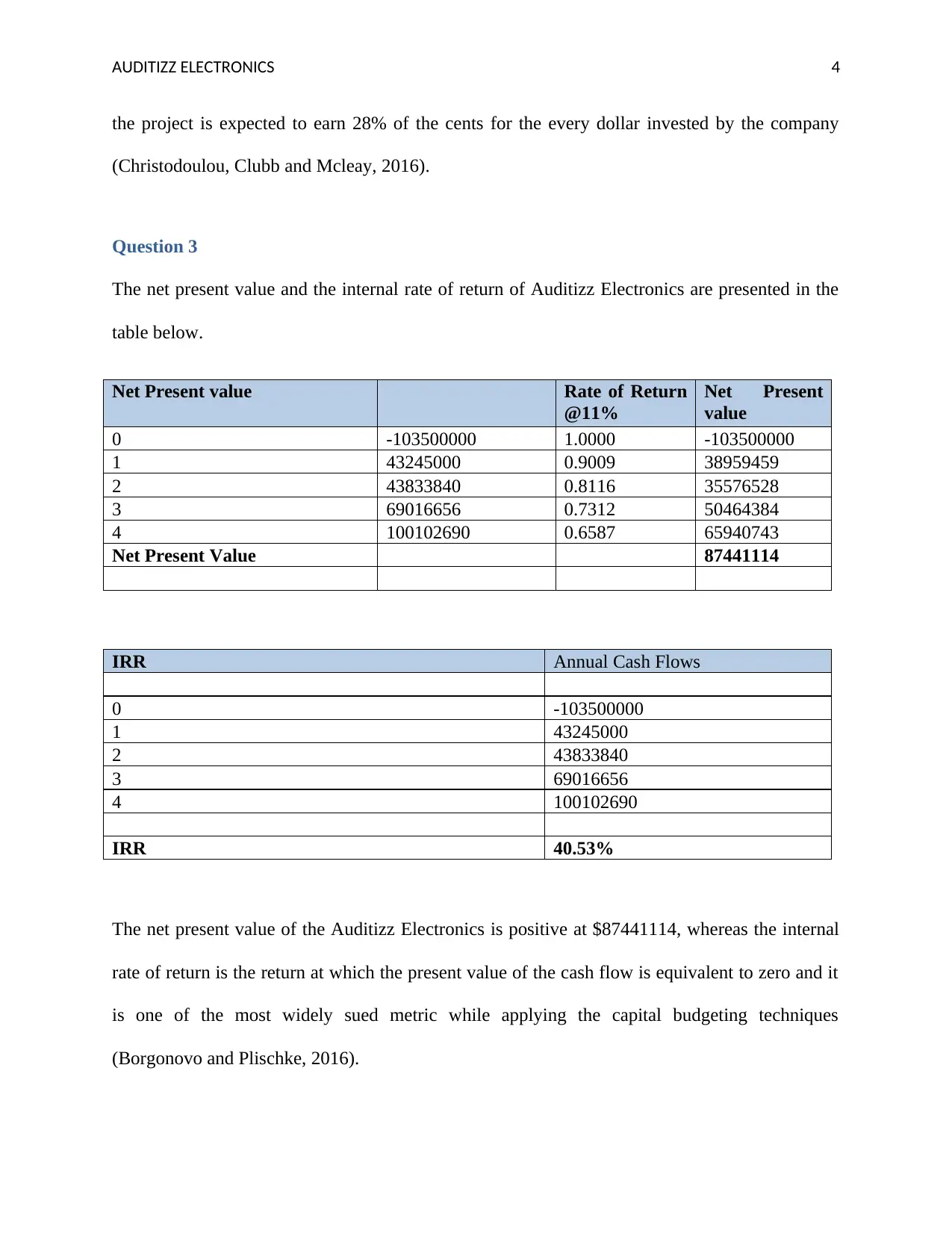

This report provides a comprehensive analysis of Auditizz Electronics' project using various capital budgeting techniques, including Net Present Value (NPV), Internal Rate of Return (IRR), Accounting Rate of Return (ARR), and sensitivity analysis. The analysis evaluates the project's feasibility, considering factors such as payback period, profitability, and the impact of changes in unit price and sales volume. The report concludes that the project is viable based on its positive NPV and acceptable IRR, while also highlighting the importance of monitoring unit price and sales volume to maintain profitability. The Efficient Market Hypothesis is also discussed in relation to the project's market value. Desklib offers this solved assignment and many other resources for students.

1 out of 8

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.