Investigating Auditor's Role in Fraud Detection: Data Analysis Report

VerifiedAdded on 2023/05/30

|14

|2066

|198

Report

AI Summary

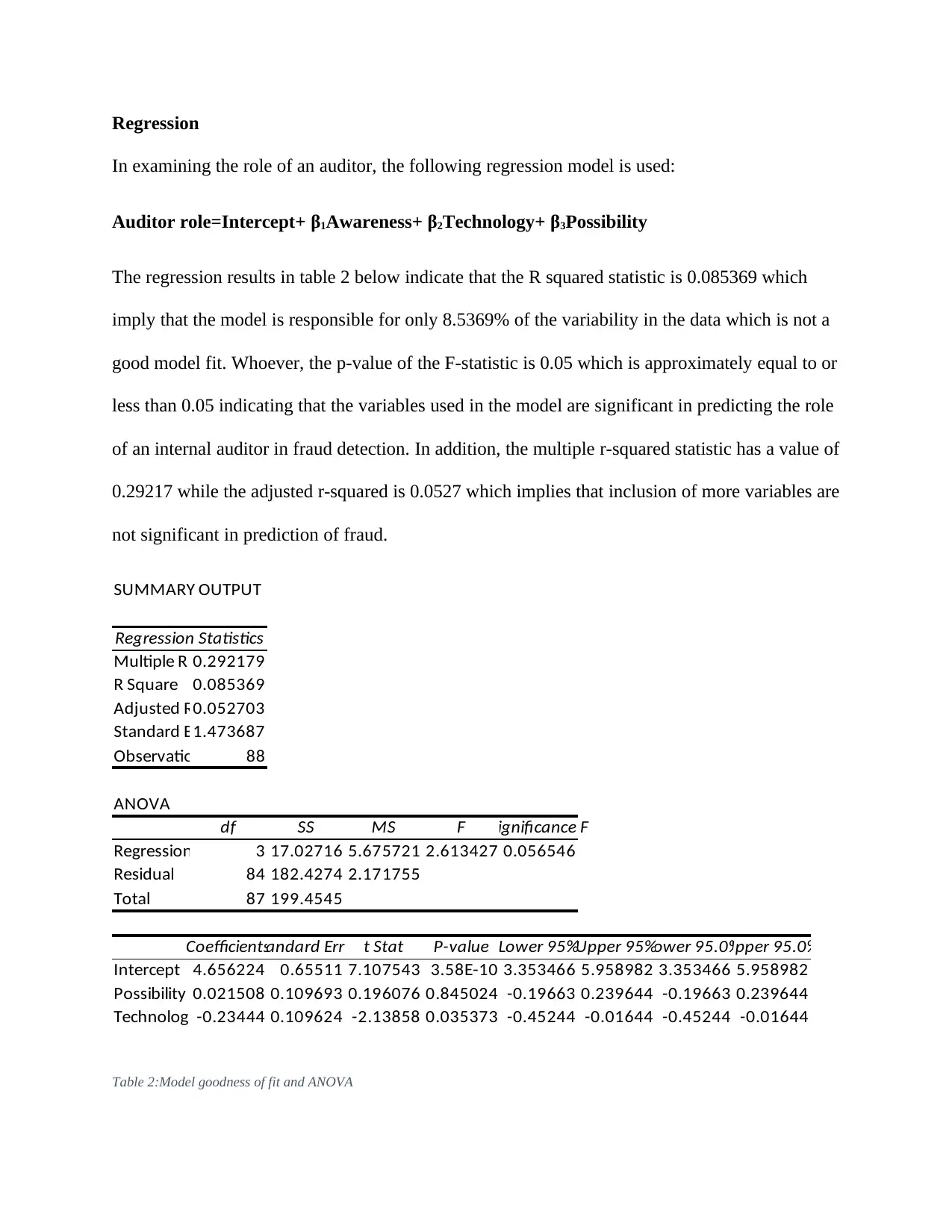

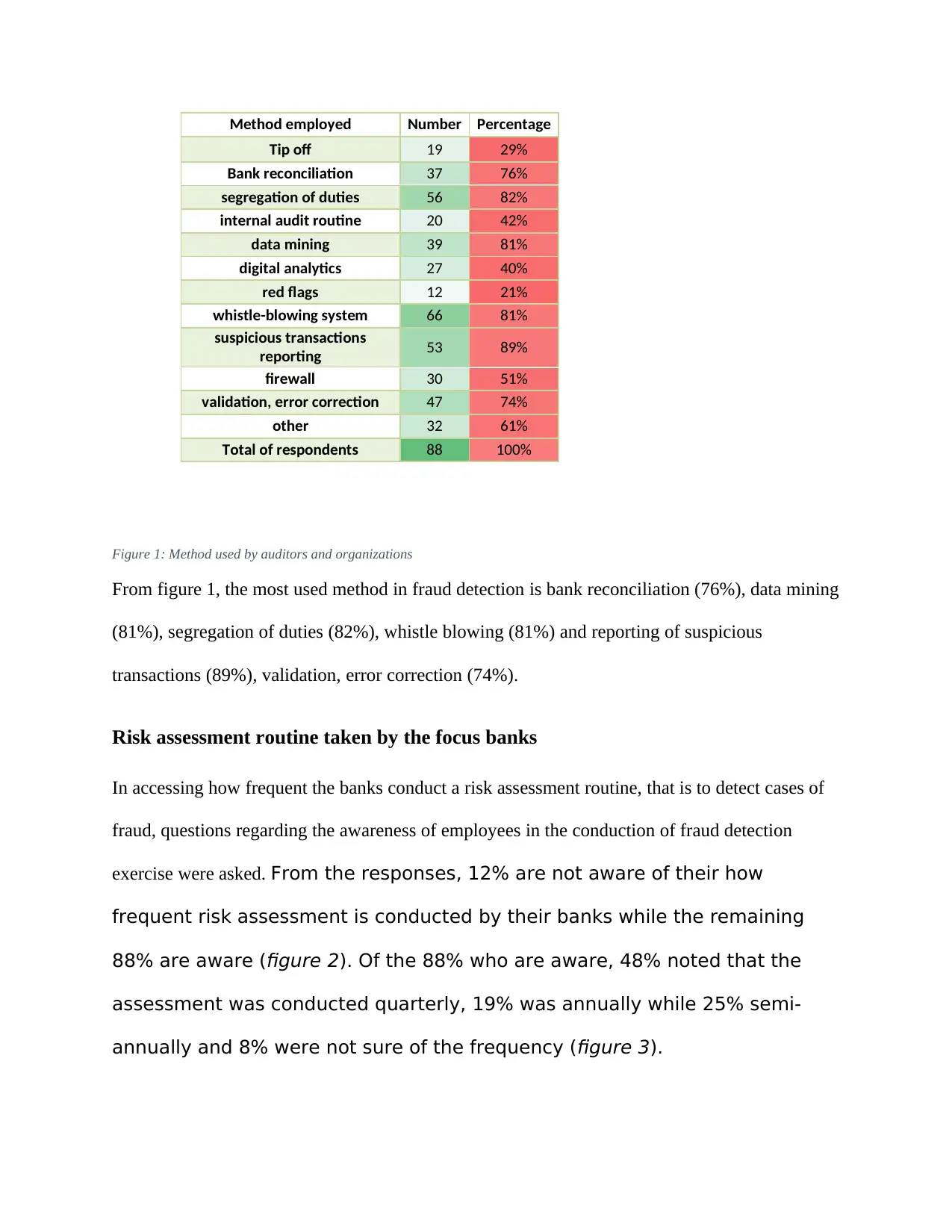

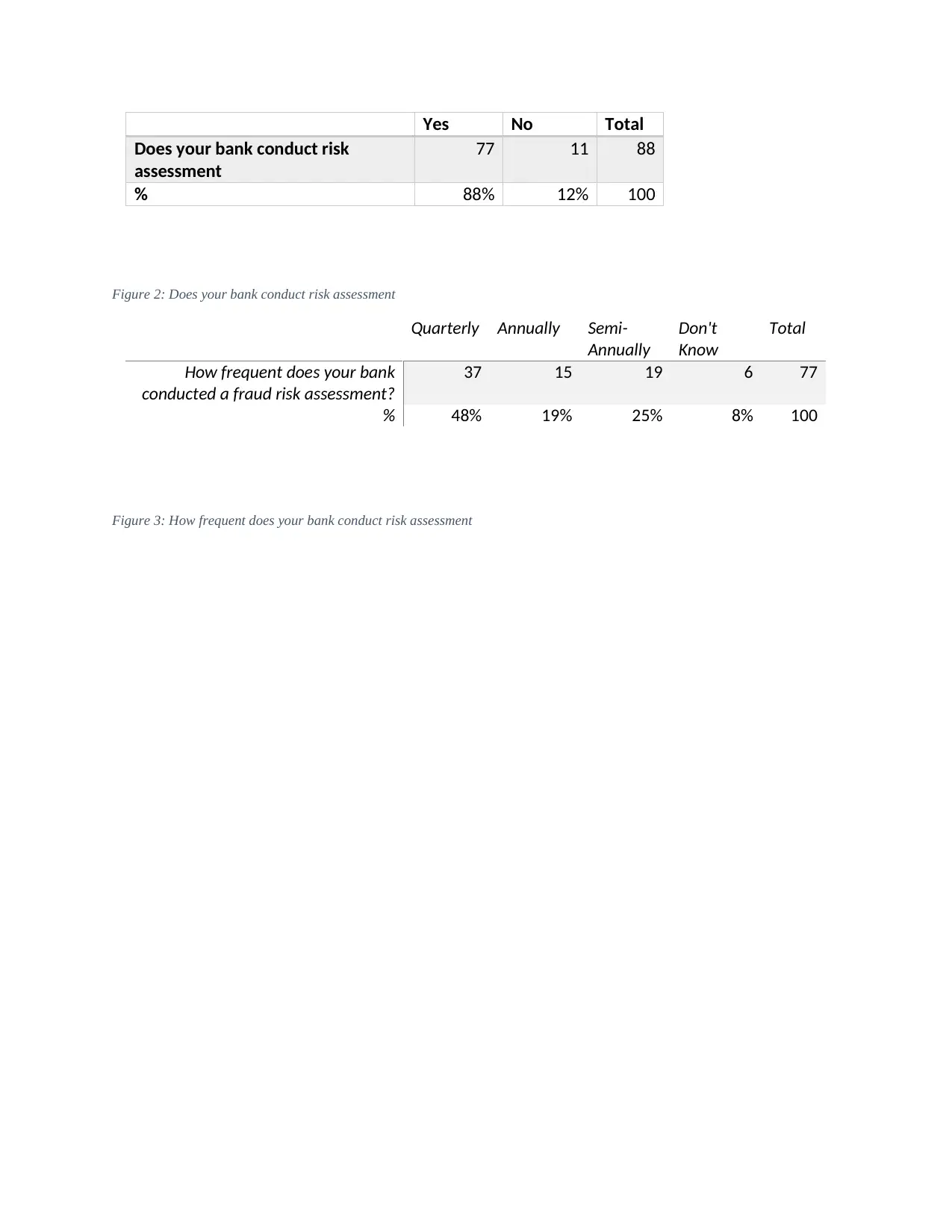

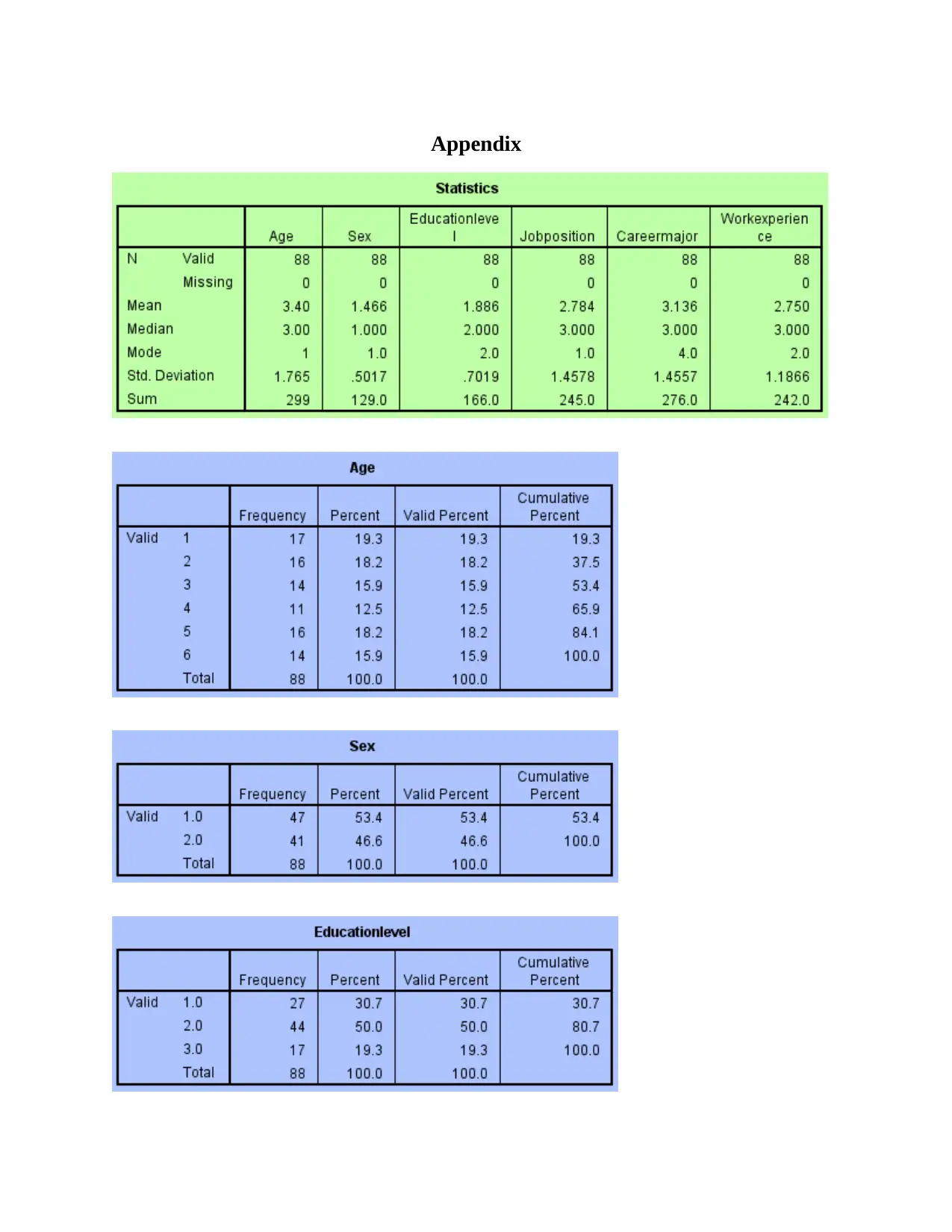

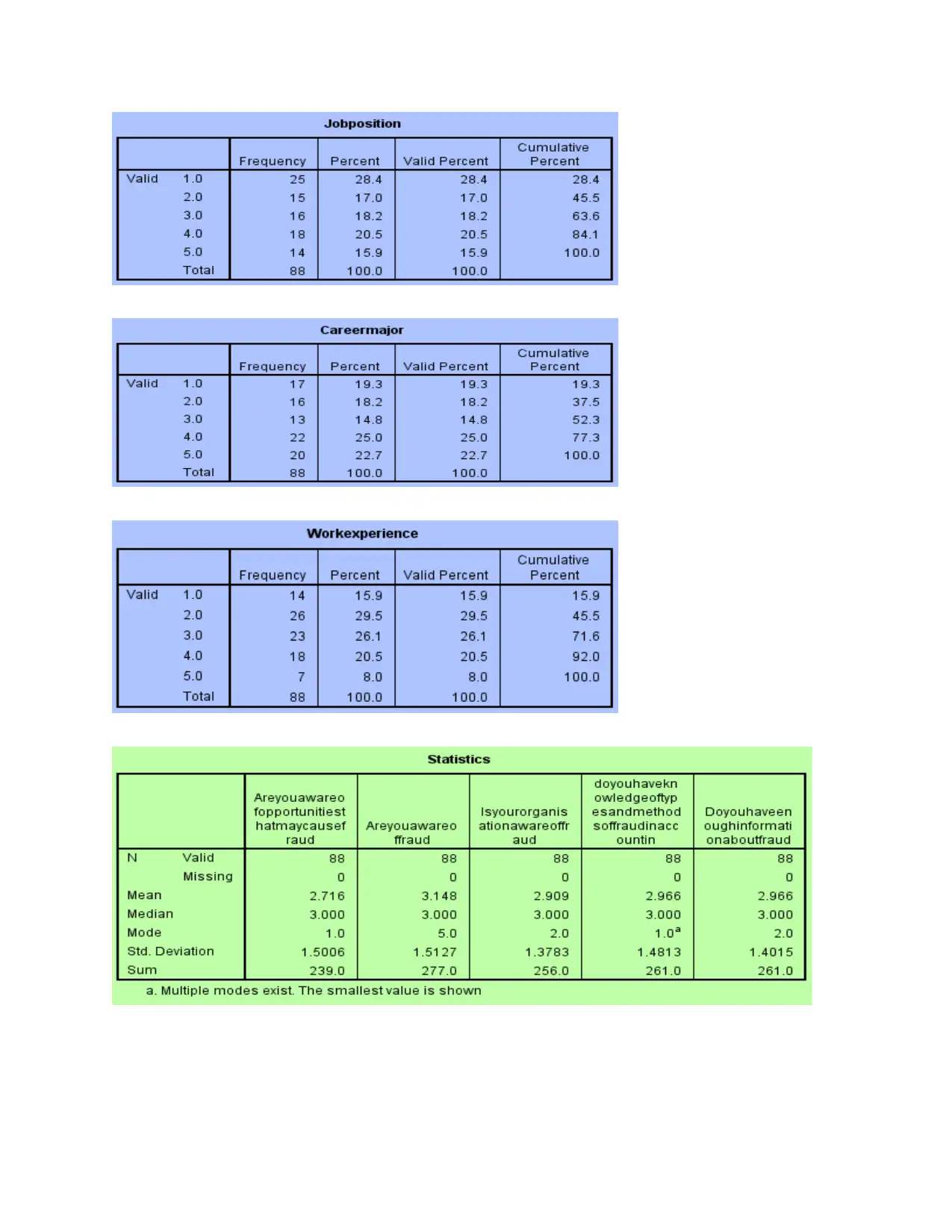

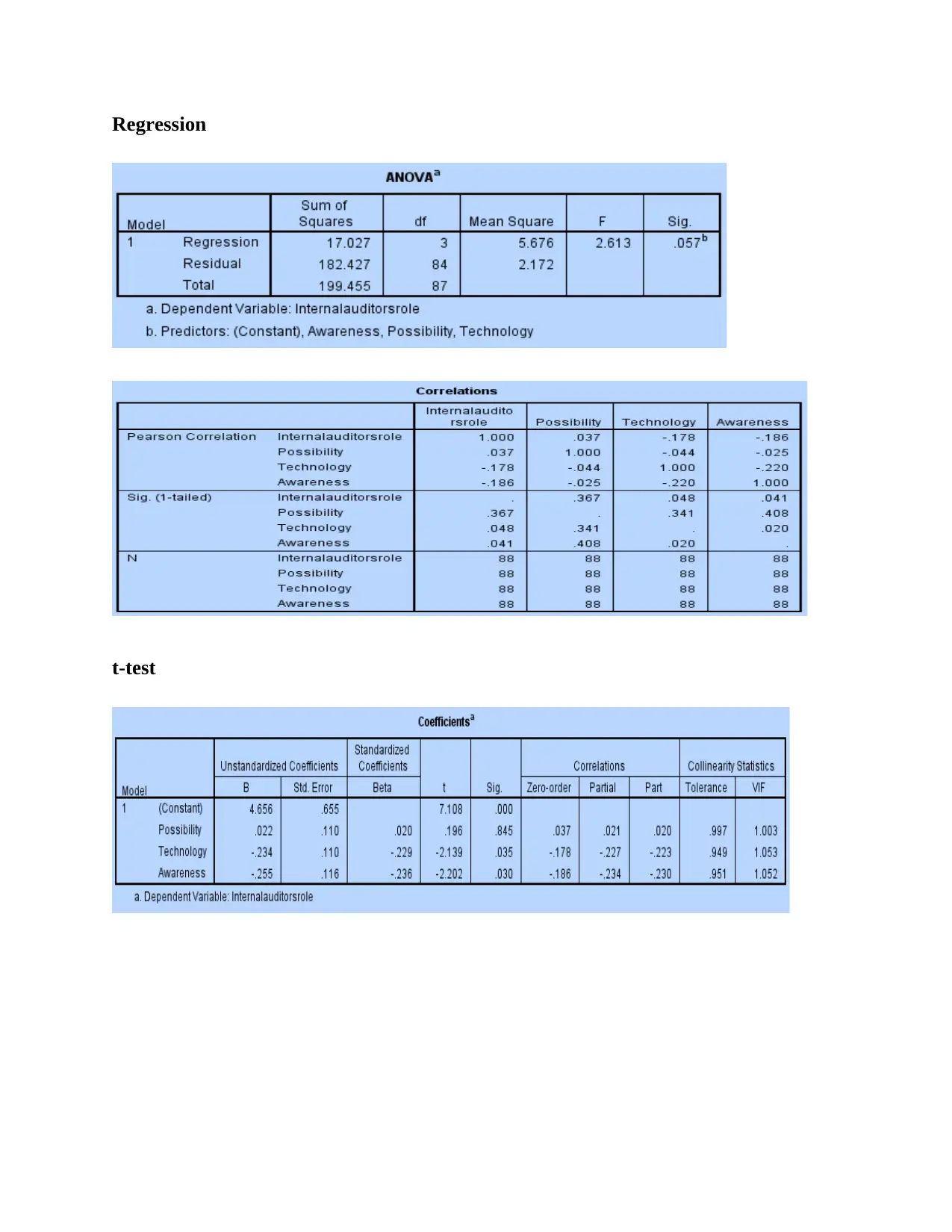

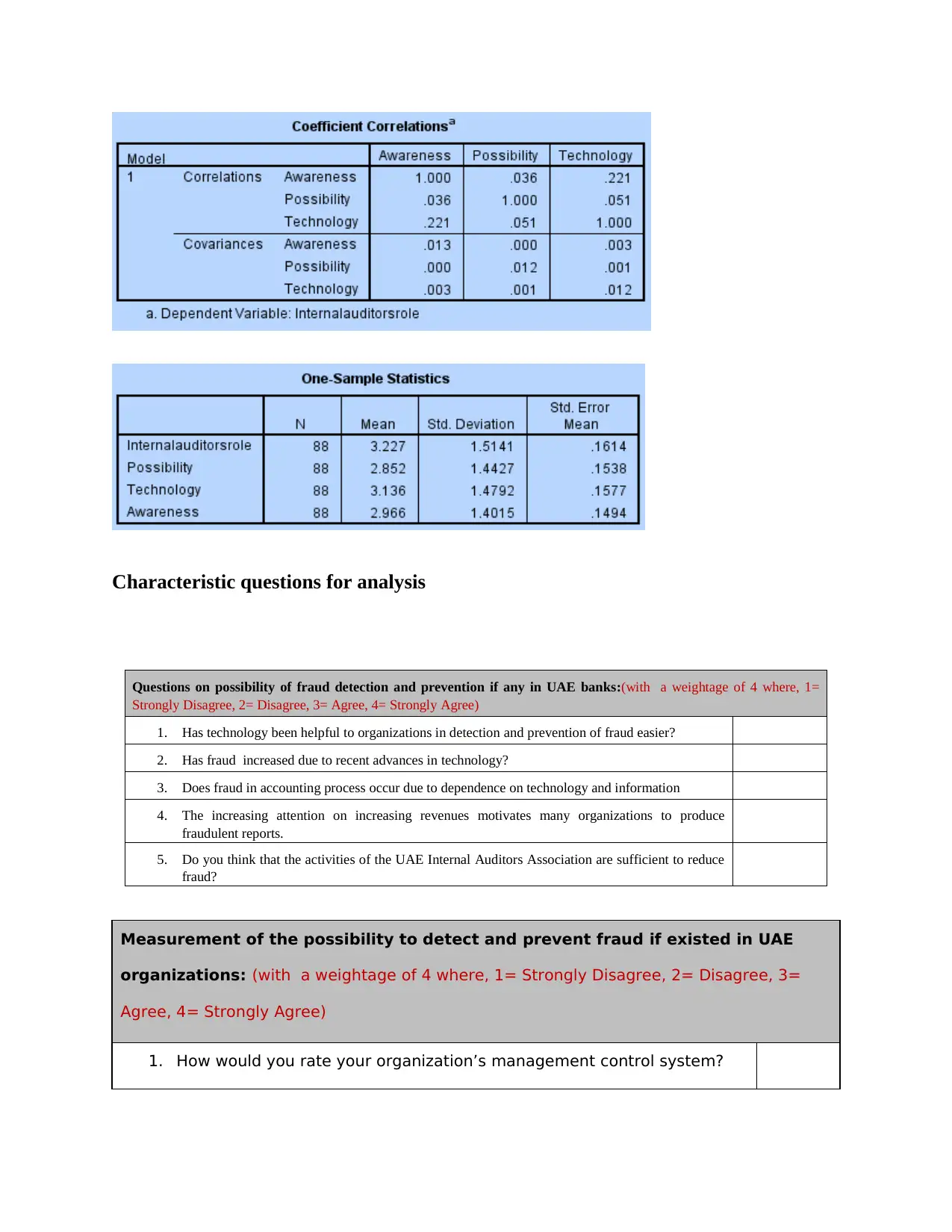

This report presents a data analysis of the role of auditors in fraud detection within UAE banks, based on a survey of 88 respondents from five different banks. The descriptive statistics cover demographic information such as gender, age, education level, job position, career major, and work experience. The analysis explores the respondents' awareness of fraud, the impact of technology in detecting fraud, and the perceived effectiveness of fraud detection and prevention in the UAE. Correlation and regression analyses are performed to examine the relationships between the role of internal auditors, the possibility of fraud detection, the role of technology, and awareness of fraud. The report also discusses the various techniques employed by banks for fraud detection, including bank reconciliation, data mining, segregation of duties, and whistleblowing systems, and assesses the frequency of risk assessment routines conducted by the banks. The findings indicate that while technology and fraud awareness are significant predictors of the role of internal auditors, the perceived possibility of fraud detection is not.

1 out of 14

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.