Data Analysis, Results and Discussion

Added on 2023-05-30

14 Pages2066 Words198 Views

Data analysis, results and discussion

Descriptive statistics

The descriptive statistics give a general structure of the sample dataset used in analysis of the

role of an auditor in fraud detection. It mainly covers the distribution of the variables, that is

frequency, percentages, and averages such as: median, mean, and mode. There are 88

respondents who are involved in the survey working in 5 banks. The banks include:

i. Bank of Sharjah

ii. Sharjah Islamic bank

iii. national bank of Abu Dhabi

iv. bank of Dubai

v. Noor bank

Demographical statistics

Gender

Out of the 88 respondents, 47 are male which represent 53.4% while there are 41 female

respondents who make up 46.6%. We can therefore infer that there are more male and female

respondents.

Age

The age variable is coded from 1 to 6, where:

Age Code

20-30 1

31-35 2

Descriptive statistics

The descriptive statistics give a general structure of the sample dataset used in analysis of the

role of an auditor in fraud detection. It mainly covers the distribution of the variables, that is

frequency, percentages, and averages such as: median, mean, and mode. There are 88

respondents who are involved in the survey working in 5 banks. The banks include:

i. Bank of Sharjah

ii. Sharjah Islamic bank

iii. national bank of Abu Dhabi

iv. bank of Dubai

v. Noor bank

Demographical statistics

Gender

Out of the 88 respondents, 47 are male which represent 53.4% while there are 41 female

respondents who make up 46.6%. We can therefore infer that there are more male and female

respondents.

Age

The age variable is coded from 1 to 6, where:

Age Code

20-30 1

31-35 2

36-40 3

41-45 4

46-50 5

50+ 6

From the analysis, most of the survey respondents are between the age of

20 and 25 i.e. they make up 19.3% of the total respondents. Respondents

between the age of 31 and 35 make up to 18.2% while those of the age

bracket 36 and 40 represent 15.9%. In addition, respondents between the

age of 41 and 45 make up 12.5% and those of the age 46-50 make up 18.2%

while those who are 50 years and above comprise 15.9%.

Educational level

Education variable is coded from 1 to 3 representing the highest attained educational level with 1

being bachelor’s degree, master’s degree and 3 being PhD.

Summary results indicate that most of the respondents involved in the survey attained a master’s

degree that is the mode making up to 50% while those with a bachelor’s degrees comprise 30.3%

of the whole respondent population and those with a PhD make up 19.3%. The educational mean

is 1.886 indicating that most respondents are either holders of a bachelor’s degree or a master’s

degree.

Job position

28.4% of the respondents are regular employees while 17% are junior supervisors, 18.2% are

senior managers and 20.5% are executive officers with 15.9% of the respondents being

members of the auditing committee. The mean job position is 2.784

indicating that most respondents are senior managers and are therefore

41-45 4

46-50 5

50+ 6

From the analysis, most of the survey respondents are between the age of

20 and 25 i.e. they make up 19.3% of the total respondents. Respondents

between the age of 31 and 35 make up to 18.2% while those of the age

bracket 36 and 40 represent 15.9%. In addition, respondents between the

age of 41 and 45 make up 12.5% and those of the age 46-50 make up 18.2%

while those who are 50 years and above comprise 15.9%.

Educational level

Education variable is coded from 1 to 3 representing the highest attained educational level with 1

being bachelor’s degree, master’s degree and 3 being PhD.

Summary results indicate that most of the respondents involved in the survey attained a master’s

degree that is the mode making up to 50% while those with a bachelor’s degrees comprise 30.3%

of the whole respondent population and those with a PhD make up 19.3%. The educational mean

is 1.886 indicating that most respondents are either holders of a bachelor’s degree or a master’s

degree.

Job position

28.4% of the respondents are regular employees while 17% are junior supervisors, 18.2% are

senior managers and 20.5% are executive officers with 15.9% of the respondents being

members of the auditing committee. The mean job position is 2.784

indicating that most respondents are senior managers and are therefore

suitable for the research purpose given that they have information on most

of the bank operations.

Career major

Career majoring is coded between 1 and 5 where, 1= accounting, 2= economics, 3=commerce

4=Financial management, 5=other majors.

Most of the respondents majored in financial management making up 25% while 19.3% majored

in accounting, 18.2% majored in economics and 14.8% majored in commerce while 22.7%

majored in other fields.

Work experience

Most of the respondents in the survey have a work experience of between 6 and 10 years making

up 29.5% while those who have a work experience of 1-5 years make up 15.9% and 11-15 years

of work experience comprise 26.1% of the total respondents. Additionally, 20.5% of the

respondents have a work experience of between 16-20 years while 8% have a work experience of

more than 20 years.

Data analysis and discussions

Awareness of fraud

Descriptive results from the data analysis indicate that up to 63.7% of the respondents are fully

aware of the opportunities that cause fraud with a mean value of 2.716. Moreover, with a mean

of 3.148, 53.4% of the respondents have got awareness regarding fraud which may include what

consists of fraud etcetera. In analysis of whether organizations are aware of fraud, 63.3% of the

respondents affirmed that the organizations which they work in have knowledge of fraud and that

56.8% of the respondents are also aware of accounting fraud and would detect one. Therefore, it

of the bank operations.

Career major

Career majoring is coded between 1 and 5 where, 1= accounting, 2= economics, 3=commerce

4=Financial management, 5=other majors.

Most of the respondents majored in financial management making up 25% while 19.3% majored

in accounting, 18.2% majored in economics and 14.8% majored in commerce while 22.7%

majored in other fields.

Work experience

Most of the respondents in the survey have a work experience of between 6 and 10 years making

up 29.5% while those who have a work experience of 1-5 years make up 15.9% and 11-15 years

of work experience comprise 26.1% of the total respondents. Additionally, 20.5% of the

respondents have a work experience of between 16-20 years while 8% have a work experience of

more than 20 years.

Data analysis and discussions

Awareness of fraud

Descriptive results from the data analysis indicate that up to 63.7% of the respondents are fully

aware of the opportunities that cause fraud with a mean value of 2.716. Moreover, with a mean

of 3.148, 53.4% of the respondents have got awareness regarding fraud which may include what

consists of fraud etcetera. In analysis of whether organizations are aware of fraud, 63.3% of the

respondents affirmed that the organizations which they work in have knowledge of fraud and that

56.8% of the respondents are also aware of accounting fraud and would detect one. Therefore, it

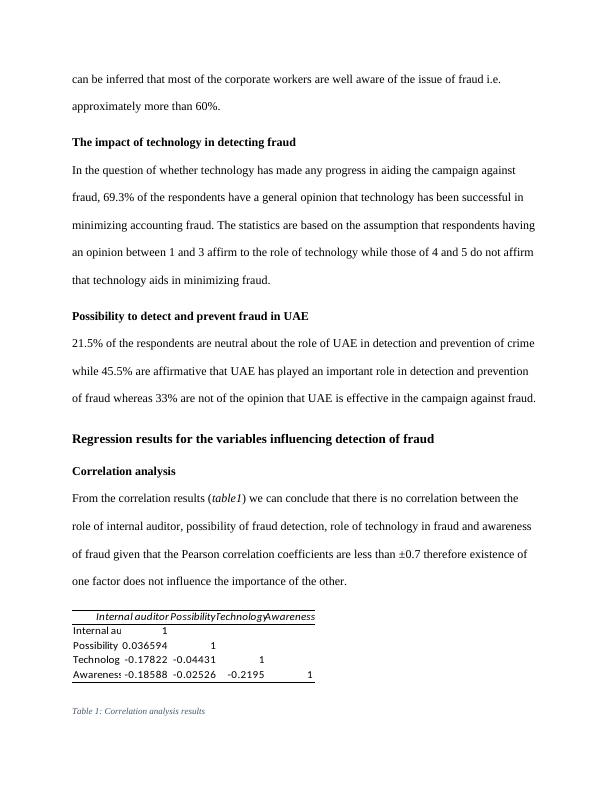

can be inferred that most of the corporate workers are well aware of the issue of fraud i.e.

approximately more than 60%.

The impact of technology in detecting fraud

In the question of whether technology has made any progress in aiding the campaign against

fraud, 69.3% of the respondents have a general opinion that technology has been successful in

minimizing accounting fraud. The statistics are based on the assumption that respondents having

an opinion between 1 and 3 affirm to the role of technology while those of 4 and 5 do not affirm

that technology aids in minimizing fraud.

Possibility to detect and prevent fraud in UAE

21.5% of the respondents are neutral about the role of UAE in detection and prevention of crime

while 45.5% are affirmative that UAE has played an important role in detection and prevention

of fraud whereas 33% are not of the opinion that UAE is effective in the campaign against fraud.

Regression results for the variables influencing detection of fraud

Correlation analysis

From the correlation results (table1) we can conclude that there is no correlation between the

role of internal auditor, possibility of fraud detection, role of technology in fraud and awareness

of fraud given that the Pearson correlation coefficients are less than ±0.7 therefore existence of

one factor does not influence the importance of the other.

Internal auditors rolePossibilityTechnologyAwareness

Internal au 1

Possibility 0.036594 1

Technolog -0.17822 -0.04431 1

Awareness -0.18588 -0.02526 -0.2195 1

Table 1: Correlation analysis results

approximately more than 60%.

The impact of technology in detecting fraud

In the question of whether technology has made any progress in aiding the campaign against

fraud, 69.3% of the respondents have a general opinion that technology has been successful in

minimizing accounting fraud. The statistics are based on the assumption that respondents having

an opinion between 1 and 3 affirm to the role of technology while those of 4 and 5 do not affirm

that technology aids in minimizing fraud.

Possibility to detect and prevent fraud in UAE

21.5% of the respondents are neutral about the role of UAE in detection and prevention of crime

while 45.5% are affirmative that UAE has played an important role in detection and prevention

of fraud whereas 33% are not of the opinion that UAE is effective in the campaign against fraud.

Regression results for the variables influencing detection of fraud

Correlation analysis

From the correlation results (table1) we can conclude that there is no correlation between the

role of internal auditor, possibility of fraud detection, role of technology in fraud and awareness

of fraud given that the Pearson correlation coefficients are less than ±0.7 therefore existence of

one factor does not influence the importance of the other.

Internal auditors rolePossibilityTechnologyAwareness

Internal au 1

Possibility 0.036594 1

Technolog -0.17822 -0.04431 1

Awareness -0.18588 -0.02526 -0.2195 1

Table 1: Correlation analysis results

End of preview

Want to access all the pages? Upload your documents or become a member.

Related Documents

Effect of Transactional and Transformational Leadership Styles on Staff Performancelg...

|24

|3827

|27

Gender Empowerment in Advertisinglg...

|5

|1060

|166