Evaluation of Auditors' Role in BHP Billiton's Annual Report

VerifiedAdded on 2023/06/08

|12

|3429

|55

AI Summary

This report evaluates the role of auditors in BHP Billiton's annual report, including their independence, significant audit matters, and audit committee. It also discusses material subsequent events and the efficiency of material information disclosed by auditors. The report highlights the importance of auditors in forming an opinion on the financials of an organization and their role in corporate governance. The report concludes that material information is either missing or remains under-reported in the annual report of BHP Billiton.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

BHP Billiton

Executive summary

The duty of auditors holds a significant position in the corporate world as it is interconnected

with the ethics and operations of an organization. Further, the organization’s corporate

governance depends upon an auditors’ functioning because they assist in forming an opinion

as to whether the financials are true and fair or not. Moreover, their report lays an effective

significance in relation to the stakeholders’ concept. For this report, the annual report of BHP

Billiton, a pioneer in the field of mining has been selected that is listed on the Australian

Stock Exchange and in view of this organization, the auditors’ role is evaluated deeply.

Further, the report starts with an introduction that is followed by the independence of

auditors, significant audit matters, and the committee of audit respectively. Lastly, a thorough

discussion is framed on the audit opinion and other matters for better understanding.

1

Executive summary

The duty of auditors holds a significant position in the corporate world as it is interconnected

with the ethics and operations of an organization. Further, the organization’s corporate

governance depends upon an auditors’ functioning because they assist in forming an opinion

as to whether the financials are true and fair or not. Moreover, their report lays an effective

significance in relation to the stakeholders’ concept. For this report, the annual report of BHP

Billiton, a pioneer in the field of mining has been selected that is listed on the Australian

Stock Exchange and in view of this organization, the auditors’ role is evaluated deeply.

Further, the report starts with an introduction that is followed by the independence of

auditors, significant audit matters, and the committee of audit respectively. Lastly, a thorough

discussion is framed on the audit opinion and other matters for better understanding.

1

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

BHP Billiton

Contents

Introduction...........................................................................................................................................3

BHP’s compliance with all independent requirements..........................................................................3

Non-audit services.................................................................................................................................3

Remuneration of auditors.....................................................................................................................4

Significant nature of the non-audit services of BHP..............................................................................4

Key audit matters..................................................................................................................................4

Audit Committee & Charter...................................................................................................................5

Differences in the responsibilities of management and directors from that of the auditors’................5

Material subsequent events..................................................................................................................6

Efficiency of the material information disclosed by auditors.................................................................7

Whether material information is missing or remains under-reported..................................................7

Conclusion.............................................................................................................................................9

Follow up questions.............................................................................................................................10

References...........................................................................................................................................11

Appendix.............................................................................................................................................12

2

Contents

Introduction...........................................................................................................................................3

BHP’s compliance with all independent requirements..........................................................................3

Non-audit services.................................................................................................................................3

Remuneration of auditors.....................................................................................................................4

Significant nature of the non-audit services of BHP..............................................................................4

Key audit matters..................................................................................................................................4

Audit Committee & Charter...................................................................................................................5

Differences in the responsibilities of management and directors from that of the auditors’................5

Material subsequent events..................................................................................................................6

Efficiency of the material information disclosed by auditors.................................................................7

Whether material information is missing or remains under-reported..................................................7

Conclusion.............................................................................................................................................9

Follow up questions.............................................................................................................................10

References...........................................................................................................................................11

Appendix.............................................................................................................................................12

2

BHP Billiton

Introduction

The requirements of auditors have become very crucial in the recent scenario because

organizations have become very vulnerable and risky in nature. Further, presence of effective

corporate governance also plays a role in mitigation of material risks that in turn assists in

enhancing the reputation or goodwill of the company. Therefore, this report has highlighted

the details of BHP Billiton Ltd and the auditors’ role has been reflected for better

understanding. Further, the company has been listed on the ASX (Australian Stock

Exchange) and this report has depicted proper information on the company’s key audit

matters and other relevant information on audit issues. Nevertheless, the information depicted

by BHP have assisted in depicting a true and fair view of the company’s performance.

BHP’s compliance with all independent requirements

Wesfarmers have properly reflected its audit requirements through its annual report and the

auditors have ensured a true and fair view of the company’s financial performance. Further, it

can be witnessed that the company has ensured that all necessary guidelines have been

fulfilled, thereby facilitating in addressing all requirements of the Australian Accounting

Standards. Further, other regulatory requirements that must be fulfilled by every company has

also been addressed by BHP Billiton in an effective way. Nevertheless, other requirements

like remuneration and audit control have also been represented by the company in an

appropriate way that can assist users in decision-making.

Non-audit services

Although the company’s external auditor has disclosed some of the non-audit services in the

annual report, their objectivity and independence are safeguarded by restrictions on the

provision of such services. For example, there are several types of non-audit services that the

external auditor of the company can adopt for better provision of services only with the prior

approval of the RAC. However, there can be various kinds of services that does not

necessitate the approval of RAC. In relation to this, the services consist of various kind of

activities that can be supervised or monitored by the company’s management. Furthermore,

advocacy role on behalf of the company can also be played by the external auditor in relation

to non-audit services (BHP Billiton, 2017). Lastly, even the RAC has framed a policy

wherein its entire group of policies and pre-approval procedures are prevalent and that can

play a role in maintaining the independence of external auditors.

3

Introduction

The requirements of auditors have become very crucial in the recent scenario because

organizations have become very vulnerable and risky in nature. Further, presence of effective

corporate governance also plays a role in mitigation of material risks that in turn assists in

enhancing the reputation or goodwill of the company. Therefore, this report has highlighted

the details of BHP Billiton Ltd and the auditors’ role has been reflected for better

understanding. Further, the company has been listed on the ASX (Australian Stock

Exchange) and this report has depicted proper information on the company’s key audit

matters and other relevant information on audit issues. Nevertheless, the information depicted

by BHP have assisted in depicting a true and fair view of the company’s performance.

BHP’s compliance with all independent requirements

Wesfarmers have properly reflected its audit requirements through its annual report and the

auditors have ensured a true and fair view of the company’s financial performance. Further, it

can be witnessed that the company has ensured that all necessary guidelines have been

fulfilled, thereby facilitating in addressing all requirements of the Australian Accounting

Standards. Further, other regulatory requirements that must be fulfilled by every company has

also been addressed by BHP Billiton in an effective way. Nevertheless, other requirements

like remuneration and audit control have also been represented by the company in an

appropriate way that can assist users in decision-making.

Non-audit services

Although the company’s external auditor has disclosed some of the non-audit services in the

annual report, their objectivity and independence are safeguarded by restrictions on the

provision of such services. For example, there are several types of non-audit services that the

external auditor of the company can adopt for better provision of services only with the prior

approval of the RAC. However, there can be various kinds of services that does not

necessitate the approval of RAC. In relation to this, the services consist of various kind of

activities that can be supervised or monitored by the company’s management. Furthermore,

advocacy role on behalf of the company can also be played by the external auditor in relation

to non-audit services (BHP Billiton, 2017). Lastly, even the RAC has framed a policy

wherein its entire group of policies and pre-approval procedures are prevalent and that can

play a role in maintaining the independence of external auditors.

3

BHP Billiton

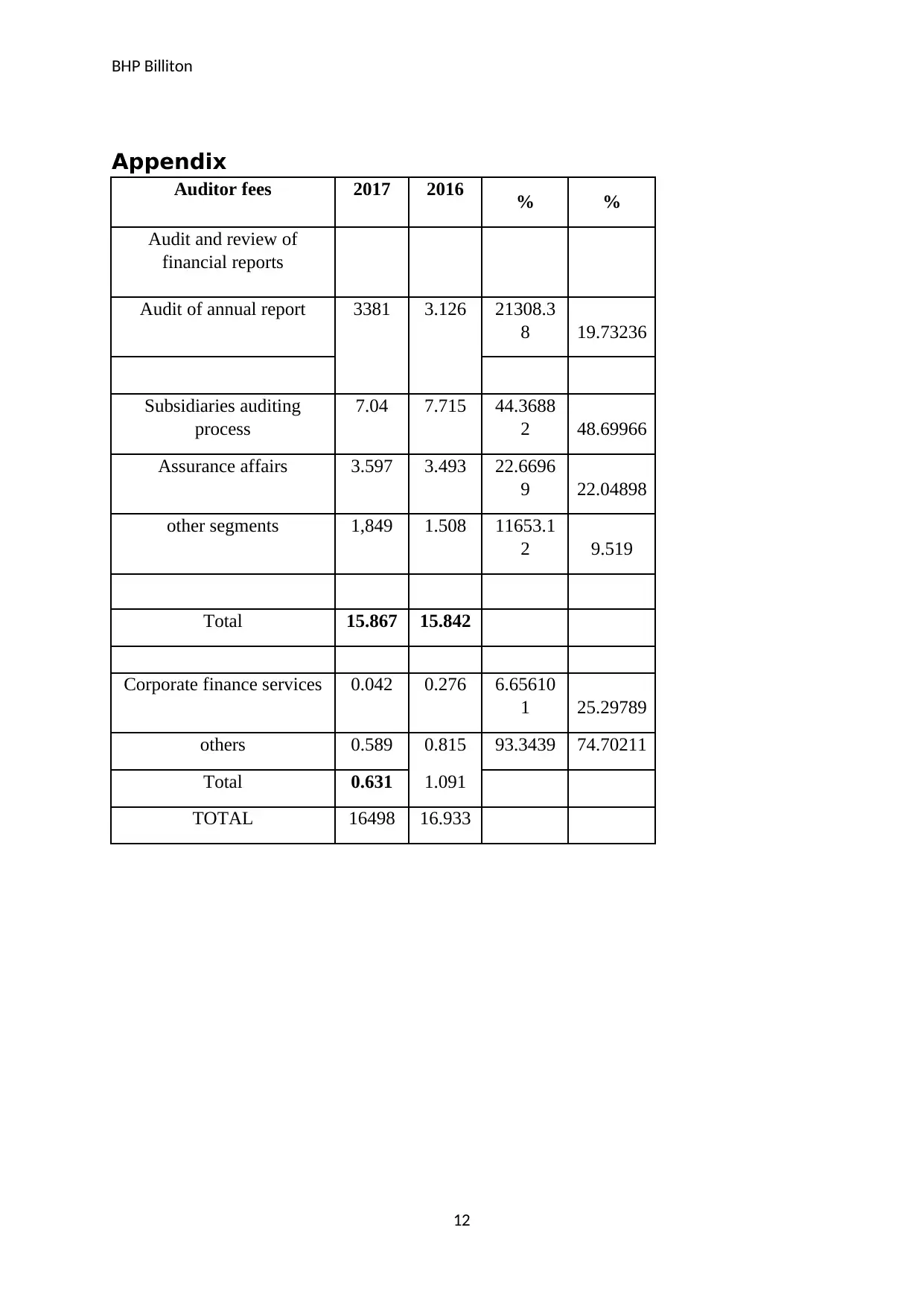

Remuneration of auditors

From the above table, it is evident that the major proportion of the auditor remuneration

derives from review of the financial report. Other segments include subsidiaries auditing,

assurance affairs, etc (Refer Appendix)

Significant nature of the non-audit services of BHP

It can be observed from the annual report of BHP that there were no non-audit services that

have been covered by it and was included in the policy of ‘Provision of audit and other

services.’

Key audit matters

In relation to any company, it is notable that key audit matters must be reflected to enhance

the quality of corporate reporting. Such matters are of prime importance and therefore, must

form part of a company’s annual report. Moreover, these matters cannot be disclosed by the

management because the judgement of auditors is mandatory in assessing the same. Besides,

disclosure of the same matters as key audit matter can allow users in understanding the

aspects that has made the auditor portray an unqualified opinion on the financials of the

company (Parker, Guthrie & Linacre, 2011). Moreover, the reason why auditors have

chosen various matters as key audit matters can be attributed to the fact that these can be

exposed to various types of fraud or errors and therefore, evaluation of the same is necessary.

When it comes to BHP, they have not changed their disclosure of key audit matters in 2017

because it was the same in previous year. The first key audit matter in relation to the

company is the assessment of future cash flows wherein judgement is compulsory for every

cash-generating units that can be used to assess the recoverable amount of Property, Plant,

and Equipment. This also includes the intangibles’ recoverable value in the company’s

financials. In addition, the recoverable value of investments is also included in the

subsidiaries of the company (BHP Billiton, 2017). The next key audit matter is the cash flows

of future in association with the forward-looking estimates and this also requires judgement

of auditors as the same cannot be determined accurately. BHP has also selected assets

valuation as a major matter due to sizes of balances that require judgement in evaluating the

efficacy of inputs used in analysing their recoverable value. Moreover, pursuing different

affairs in different companies also attract different types of taxes like corporation tax,

royalties, etc that are associated with international transfer pricing (BHP Billiton, 2017).

4

Remuneration of auditors

From the above table, it is evident that the major proportion of the auditor remuneration

derives from review of the financial report. Other segments include subsidiaries auditing,

assurance affairs, etc (Refer Appendix)

Significant nature of the non-audit services of BHP

It can be observed from the annual report of BHP that there were no non-audit services that

have been covered by it and was included in the policy of ‘Provision of audit and other

services.’

Key audit matters

In relation to any company, it is notable that key audit matters must be reflected to enhance

the quality of corporate reporting. Such matters are of prime importance and therefore, must

form part of a company’s annual report. Moreover, these matters cannot be disclosed by the

management because the judgement of auditors is mandatory in assessing the same. Besides,

disclosure of the same matters as key audit matter can allow users in understanding the

aspects that has made the auditor portray an unqualified opinion on the financials of the

company (Parker, Guthrie & Linacre, 2011). Moreover, the reason why auditors have

chosen various matters as key audit matters can be attributed to the fact that these can be

exposed to various types of fraud or errors and therefore, evaluation of the same is necessary.

When it comes to BHP, they have not changed their disclosure of key audit matters in 2017

because it was the same in previous year. The first key audit matter in relation to the

company is the assessment of future cash flows wherein judgement is compulsory for every

cash-generating units that can be used to assess the recoverable amount of Property, Plant,

and Equipment. This also includes the intangibles’ recoverable value in the company’s

financials. In addition, the recoverable value of investments is also included in the

subsidiaries of the company (BHP Billiton, 2017). The next key audit matter is the cash flows

of future in association with the forward-looking estimates and this also requires judgement

of auditors as the same cannot be determined accurately. BHP has also selected assets

valuation as a major matter due to sizes of balances that require judgement in evaluating the

efficacy of inputs used in analysing their recoverable value. Moreover, pursuing different

affairs in different companies also attract different types of taxes like corporation tax,

royalties, etc that are associated with international transfer pricing (BHP Billiton, 2017).

4

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

BHP Billiton

Therefore, such taxes are also considered as the key audit matters of the company owing to

its tax rules that necessitates judgement on the company’s part to analyse various contingent

liabilities, associated provisions, and expectation of tax resources. Another key audit matter is

the rehabilitation and closure policy wherein significant estimates over the mine and reserves’

life in evaluating the provision of rehabilitation that requires judgement because of issues in

expecting the quantum and time of future costs (Cappelleto, 2010). After this step,

determination of an efficient rate to discount such costs back to the present value is facilitated

and hence, requires judgement on the auditors’ part. Therefore, these matters are BHP’s key

audit matters.

Audit Committee & Charter

The company has an audit, risk management and compliance committee. Further, the charter

assists in framing the duties delegated by the management to the committee and its

objectives. The role of committee is to provide support to the management in association with

the company’s governance framework. This includes internal control and risk management

systems, accounting processes, both external and internal audit measures, etc.

The committee is primarily bound to perform various affairs within the boundaries of its roles

set in the charter and thereafter, provide significant recommendations to the management.

Further, the audit and risk committee also have unrestricted accessibility to the senior

management of the company and its financial records as and when required (Mock et. al,

2013). It is liable to set meetings with both the external and internal auditors without any

prime member of the board being prevalent, as and when the committee find it appropriate

(BHP Billiton, 2017). Nevertheless, the committee has been authorised to attain various

professional suggestions and independent counsels that it can regard as crucial to execute or

implement its operations.

Differences in the responsibilities of management and

directors from that of the auditors’

The fundamental to a company’s financial statement or report is the segregation betwixt the

responsibilities of an auditor and the directors or management. In relation to this, it is notable

that the management and directors of the company are responsible for the preparation of

financial report and the contents of such report are the assertions offered by them. In contrast

5

Therefore, such taxes are also considered as the key audit matters of the company owing to

its tax rules that necessitates judgement on the company’s part to analyse various contingent

liabilities, associated provisions, and expectation of tax resources. Another key audit matter is

the rehabilitation and closure policy wherein significant estimates over the mine and reserves’

life in evaluating the provision of rehabilitation that requires judgement because of issues in

expecting the quantum and time of future costs (Cappelleto, 2010). After this step,

determination of an efficient rate to discount such costs back to the present value is facilitated

and hence, requires judgement on the auditors’ part. Therefore, these matters are BHP’s key

audit matters.

Audit Committee & Charter

The company has an audit, risk management and compliance committee. Further, the charter

assists in framing the duties delegated by the management to the committee and its

objectives. The role of committee is to provide support to the management in association with

the company’s governance framework. This includes internal control and risk management

systems, accounting processes, both external and internal audit measures, etc.

The committee is primarily bound to perform various affairs within the boundaries of its roles

set in the charter and thereafter, provide significant recommendations to the management.

Further, the audit and risk committee also have unrestricted accessibility to the senior

management of the company and its financial records as and when required (Mock et. al,

2013). It is liable to set meetings with both the external and internal auditors without any

prime member of the board being prevalent, as and when the committee find it appropriate

(BHP Billiton, 2017). Nevertheless, the committee has been authorised to attain various

professional suggestions and independent counsels that it can regard as crucial to execute or

implement its operations.

Differences in the responsibilities of management and

directors from that of the auditors’

The fundamental to a company’s financial statement or report is the segregation betwixt the

responsibilities of an auditor and the directors or management. In relation to this, it is notable

that the management and directors of the company are responsible for the preparation of

financial report and the contents of such report are the assertions offered by them. In contrast

5

BHP Billiton

to this, the auditor is primarily responsible for the examination of such financial report

prepared by the directors and management to facilitate in the expression of an opinion on the

truthfulness and fairness (Cappelleto, 2010). Furthermore, the management’s duty for the

truthfulness and fairness of presentation in the report carries with it the privilege of

ascertaining which disclosures are mandatory. Even though the directors and management

have the responsibility in preparing financial report, yet the auditors can also assist in such

preparation. For instance, he can advise or counsel them as to the implementation or adoption

of a fresh accounting principle and during audit processes, he may also propose significant

adjustments to the financial report (Livne, 2015). However, acceptance of the auditors’

advice and the incorporation of such suggested adjustments in the financial report does not

alter the general separation of responsibility. Finally, the management is only liable for all the

decisions related to the content and form of the financial report (Arens et. al, 2013). Further,

if the auditor finds that the disclosure on the part of management and directors are not

acceptable, he may issue a qualified or adverse opinion or may also withdraw from himself

from the engagement. Overall, the responsibility of the auditors is restricted to the

performance of audit investigation and thereafter, reporting the outcomes based on the GAAP

(generally accepted auditing standards). In most of the cases, any significant omissions and

errors can be discovered if the audit has been performed in this way (Niemi & Sundgren,

2012).

Material subsequent events

BHP has encountered few material subsequent events after its date of reporting and this can

have a material impact on the financials in the upcoming tenure. Further, this can also result

in a material impact on the company’s financial performance if it was reported in the current

year. The first material subsequent event that incurred after the reporting date of BHP was

that it announced a scheme of investment amounting to $US2.5 billion so that its Spencer

Growth Option can be developed. Besides, this consisted of establishment of copper

constructors that can facilitate in wide spreading the life of mine by 50 years. Subsequently,

the company had also announced regarding the increment of global average capitalization up

to $US 2.9 billion (BHP Billiton, 2017). The next material subsequent event of the company

was that it evaluated its onshore US assets to be non-core in nature and thereafter, it also

paved a path for options that can enable in quitting these assets. This was done by the

directors and management of the company collectively. Nevertheless, such subsequent event

was a major part of the ongoing portfolio review. However, the company had also provided

6

to this, the auditor is primarily responsible for the examination of such financial report

prepared by the directors and management to facilitate in the expression of an opinion on the

truthfulness and fairness (Cappelleto, 2010). Furthermore, the management’s duty for the

truthfulness and fairness of presentation in the report carries with it the privilege of

ascertaining which disclosures are mandatory. Even though the directors and management

have the responsibility in preparing financial report, yet the auditors can also assist in such

preparation. For instance, he can advise or counsel them as to the implementation or adoption

of a fresh accounting principle and during audit processes, he may also propose significant

adjustments to the financial report (Livne, 2015). However, acceptance of the auditors’

advice and the incorporation of such suggested adjustments in the financial report does not

alter the general separation of responsibility. Finally, the management is only liable for all the

decisions related to the content and form of the financial report (Arens et. al, 2013). Further,

if the auditor finds that the disclosure on the part of management and directors are not

acceptable, he may issue a qualified or adverse opinion or may also withdraw from himself

from the engagement. Overall, the responsibility of the auditors is restricted to the

performance of audit investigation and thereafter, reporting the outcomes based on the GAAP

(generally accepted auditing standards). In most of the cases, any significant omissions and

errors can be discovered if the audit has been performed in this way (Niemi & Sundgren,

2012).

Material subsequent events

BHP has encountered few material subsequent events after its date of reporting and this can

have a material impact on the financials in the upcoming tenure. Further, this can also result

in a material impact on the company’s financial performance if it was reported in the current

year. The first material subsequent event that incurred after the reporting date of BHP was

that it announced a scheme of investment amounting to $US2.5 billion so that its Spencer

Growth Option can be developed. Besides, this consisted of establishment of copper

constructors that can facilitate in wide spreading the life of mine by 50 years. Subsequently,

the company had also announced regarding the increment of global average capitalization up

to $US 2.9 billion (BHP Billiton, 2017). The next material subsequent event of the company

was that it evaluated its onshore US assets to be non-core in nature and thereafter, it also

paved a path for options that can enable in quitting these assets. This was done by the

directors and management of the company collectively. Nevertheless, such subsequent event

was a major part of the ongoing portfolio review. However, the company had also provided

6

BHP Billiton

that implementation of such options can take some extra time. Hence, these were the material

subsequent events that occurred after the company’s reporting period and since these were

disclosed in the annual report, it signifies that these transactions of events could easily result

in a material impact on the financial performance.

Efficiency of the material information disclosed by

auditors

From the annual report of BHP, it cannot be observed that the material information disclosed

by auditors were not equipped with loopholes. Furthermore, the information was not

equipped with proper transparency that sheds light on the ineffectiveness of material

information. The primary reason behind such gaps can be due to the prime attention exerted

only on few matters and discarded the others that is not effective in nature. Moreover, the key

points chosen for disclosure was not portrayed well in the financial report and this clearly

highlights that the material information cannot even assist in proper decision-making on the

part of users (BHP Billiton, 2017). However, the auditors attempted in describing the reasons

behind the adoption of prime matters and explained the same to enable users in understanding

the same. This was a positive aspect on the part of auditors. In relation to this, when

investments are undertaken by any company, they must record enhanced and thorough details

about the liabilities and assets to gain better understanding related to the transaction. In

contrast to this, the auditors failed to offer a thorough understanding regarding the same and

that can pave a path of obstacle for the investors to make proper decisions. Therefore,

discarding various prime matters for disclosure and offering notes or footnotes cannot assist

in proper decision-making (Roach, 2010). Besides, this may mislead the users in their path

and cause hindrances in the future. Hence, it is the duty of auditors to present the reports in a

way that can assist every user in decision-making and every matter of significant importance

must be thoroughly disclosed.

Whether material information is missing or remains

under-reported

From the company’s annual report, it can be noted that it has disclosed material information

through footnotes and notes to financial statements but where the same was necessary, it has

failed to disclose the same. For instance, the company has not disclosed proper footnotes in

the financial statements segment that is not a positive indicator. In relation to this, it must be

taken into consideration that footnotes can play a key role in effective decision-making but

7

that implementation of such options can take some extra time. Hence, these were the material

subsequent events that occurred after the company’s reporting period and since these were

disclosed in the annual report, it signifies that these transactions of events could easily result

in a material impact on the financial performance.

Efficiency of the material information disclosed by

auditors

From the annual report of BHP, it cannot be observed that the material information disclosed

by auditors were not equipped with loopholes. Furthermore, the information was not

equipped with proper transparency that sheds light on the ineffectiveness of material

information. The primary reason behind such gaps can be due to the prime attention exerted

only on few matters and discarded the others that is not effective in nature. Moreover, the key

points chosen for disclosure was not portrayed well in the financial report and this clearly

highlights that the material information cannot even assist in proper decision-making on the

part of users (BHP Billiton, 2017). However, the auditors attempted in describing the reasons

behind the adoption of prime matters and explained the same to enable users in understanding

the same. This was a positive aspect on the part of auditors. In relation to this, when

investments are undertaken by any company, they must record enhanced and thorough details

about the liabilities and assets to gain better understanding related to the transaction. In

contrast to this, the auditors failed to offer a thorough understanding regarding the same and

that can pave a path of obstacle for the investors to make proper decisions. Therefore,

discarding various prime matters for disclosure and offering notes or footnotes cannot assist

in proper decision-making (Roach, 2010). Besides, this may mislead the users in their path

and cause hindrances in the future. Hence, it is the duty of auditors to present the reports in a

way that can assist every user in decision-making and every matter of significant importance

must be thoroughly disclosed.

Whether material information is missing or remains

under-reported

From the company’s annual report, it can be noted that it has disclosed material information

through footnotes and notes to financial statements but where the same was necessary, it has

failed to disclose the same. For instance, the company has not disclosed proper footnotes in

the financial statements segment that is not a positive indicator. In relation to this, it must be

taken into consideration that footnotes can play a key role in effective decision-making but

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

BHP Billiton

since the same is not prevalent in the financial statements, users may find it problematic to

extract usefulness from the financial statements like balance sheet, profit and loss account,

etc. In addition to this fact, the section of notes to financial statements has not been entirely

disclosed by the company that can create further complications for the users in their decision-

making processes. For instance, since the company has disclosed information regarding both

the statement of comprehensive income and statement of income, they are bound to disclose

non-material information separately and not in the financial statements (Wood, 2011).

Nevertheless, such financials must only accommodate material information that can assist in

enhancing the qualitative characteristics of conceptual framework like relevance, materiality,

reliability, etc.

Hence, disclosure of proper information on the part of the company is missing and if such

disclosure measures are not corrected in future, users may face complications in their

decision-making and the company’s reputation may be spoiled on a whole.

8

since the same is not prevalent in the financial statements, users may find it problematic to

extract usefulness from the financial statements like balance sheet, profit and loss account,

etc. In addition to this fact, the section of notes to financial statements has not been entirely

disclosed by the company that can create further complications for the users in their decision-

making processes. For instance, since the company has disclosed information regarding both

the statement of comprehensive income and statement of income, they are bound to disclose

non-material information separately and not in the financial statements (Wood, 2011).

Nevertheless, such financials must only accommodate material information that can assist in

enhancing the qualitative characteristics of conceptual framework like relevance, materiality,

reliability, etc.

Hence, disclosure of proper information on the part of the company is missing and if such

disclosure measures are not corrected in future, users may face complications in their

decision-making and the company’s reputation may be spoiled on a whole.

8

BHP Billiton

Conclusion

It can be seen from the annual report that the auditors have been effective in their disclosure

mechanisms and have not deviated themselves from ethical standards. This can be proved by

their disclosure of key audit matters and other relevant issues through the auditor’s report.

Moreover, even the directors and management have assured fulfilment of necessary rules and

regulations that has been catered to in an effective manner. The company has also disclosed

material information regarding the non-audit services that have been provided by the same

auditors who have undertaken the auditing services. This highlights the fact that internal

control mechanisms are in place that can safeguard the company from future risks. Besides,

there are some issues in the material information in the financials that is a slight complication

but must be addressed as soon as possible.

9

Conclusion

It can be seen from the annual report that the auditors have been effective in their disclosure

mechanisms and have not deviated themselves from ethical standards. This can be proved by

their disclosure of key audit matters and other relevant issues through the auditor’s report.

Moreover, even the directors and management have assured fulfilment of necessary rules and

regulations that has been catered to in an effective manner. The company has also disclosed

material information regarding the non-audit services that have been provided by the same

auditors who have undertaken the auditing services. This highlights the fact that internal

control mechanisms are in place that can safeguard the company from future risks. Besides,

there are some issues in the material information in the financials that is a slight complication

but must be addressed as soon as possible.

9

BHP Billiton

Follow up questions

There are questions that can be asked to the auditor at the general meeting of the company:

a. Can the audit chair understand complicated matters of accounting and other internal

control measures? What are some illustrations that support your conclusion?

b. Have you reported any significant deficiencies in the internal control measures to the

audit committee this year?

10

Follow up questions

There are questions that can be asked to the auditor at the general meeting of the company:

a. Can the audit chair understand complicated matters of accounting and other internal

control measures? What are some illustrations that support your conclusion?

b. Have you reported any significant deficiencies in the internal control measures to the

audit committee this year?

10

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

BHP Billiton

References

Arens, A. A, Best, P. J, Shailer, G. E. P & Loebbecke, J. K. (2013) Assurance Services and

Ethics in Australia, 9th ed, Australia: Pearson.

BHP Billiton. (2017) BHP 2017 Annual report and accounts. https://www.bhp.com/media-

and-insights/reports-and-presentations [Accessed 14 September 2018]

Cappelleto, G. (2010) Challenges Facing Accounting Education in Australia, AFAANZ,

Geoffrey D. B., Joleen K., K. K.S., and David A. W. (2016). Attracting Applicants for In-

House and Outsourced Internal Audit Positions: Views from External Auditors. Accounting

Horizons. [online]. 30(1), p.143-156. DOI: https://doi.org/10.2308/acch-51309

Livne, G. (2015) Threats to Auditor Independence and Possible Remedies [online].

Available from: http://www.financepractitioner.com/auditing-best-practice/threats-to-auditor-

independence-and-possible-remedies?full [Accessed 7 September 2018]

Mock, T. J., Bedard, J., Coram, P., Davis, S., Espahbodi, R. and Warne, R. (2013) The audit

reporting model: Current research synthesis and implications. Auditing: A Journal of

Practice and Theory. [online]. 32, pp. 323-351. DOI: https://doi.org/10.2308/ajpt-50294

Niemi, L. and Sundgren, S. (2012) Are modified audit opinions related to the availability of

credit? Evidence from Finnish SMEs. European Accounting Review. [online]. 21(4), p. 767-

796. Available from: https://doi.org/10.1080/09638180.2012.671465 [Accessed 14

September 2018]

Parker, L., Guthrie, J. and Linacre, S. (2011) The relationship between academic

accounting research and professional practice. Accounting , Auditing &

Accountability Journal. [online]. 24(1), pp. 5-14. Available from:

http://media.accountingeducation.com/1304/Parkeraaaj24(1).pdf [Accessed 14

September 2018]

Roach, L. (2010) Auditor Liability: Liability Limitation Agreements. Pearson.

Wood, D A. (2011) The Effect of Using the Internal Audit Function as a Management

Training Ground on the External Auditor's Reliance Decision. The Accounting Review.

[online] 86(6), 2131-2154. DOI: https://doi.org/10.2308/accr-10136

11

References

Arens, A. A, Best, P. J, Shailer, G. E. P & Loebbecke, J. K. (2013) Assurance Services and

Ethics in Australia, 9th ed, Australia: Pearson.

BHP Billiton. (2017) BHP 2017 Annual report and accounts. https://www.bhp.com/media-

and-insights/reports-and-presentations [Accessed 14 September 2018]

Cappelleto, G. (2010) Challenges Facing Accounting Education in Australia, AFAANZ,

Geoffrey D. B., Joleen K., K. K.S., and David A. W. (2016). Attracting Applicants for In-

House and Outsourced Internal Audit Positions: Views from External Auditors. Accounting

Horizons. [online]. 30(1), p.143-156. DOI: https://doi.org/10.2308/acch-51309

Livne, G. (2015) Threats to Auditor Independence and Possible Remedies [online].

Available from: http://www.financepractitioner.com/auditing-best-practice/threats-to-auditor-

independence-and-possible-remedies?full [Accessed 7 September 2018]

Mock, T. J., Bedard, J., Coram, P., Davis, S., Espahbodi, R. and Warne, R. (2013) The audit

reporting model: Current research synthesis and implications. Auditing: A Journal of

Practice and Theory. [online]. 32, pp. 323-351. DOI: https://doi.org/10.2308/ajpt-50294

Niemi, L. and Sundgren, S. (2012) Are modified audit opinions related to the availability of

credit? Evidence from Finnish SMEs. European Accounting Review. [online]. 21(4), p. 767-

796. Available from: https://doi.org/10.1080/09638180.2012.671465 [Accessed 14

September 2018]

Parker, L., Guthrie, J. and Linacre, S. (2011) The relationship between academic

accounting research and professional practice. Accounting , Auditing &

Accountability Journal. [online]. 24(1), pp. 5-14. Available from:

http://media.accountingeducation.com/1304/Parkeraaaj24(1).pdf [Accessed 14

September 2018]

Roach, L. (2010) Auditor Liability: Liability Limitation Agreements. Pearson.

Wood, D A. (2011) The Effect of Using the Internal Audit Function as a Management

Training Ground on the External Auditor's Reliance Decision. The Accounting Review.

[online] 86(6), 2131-2154. DOI: https://doi.org/10.2308/accr-10136

11

BHP Billiton

Appendix

Auditor fees 2017 2016 % %

Audit and review of

financial reports

Audit of annual report 3381 3.126 21308.3

8 19.73236

Subsidiaries auditing

process

7.04 7.715 44.3688

2 48.69966

Assurance affairs 3.597 3.493 22.6696

9 22.04898

other segments 1,849 1.508 11653.1

2 9.519

Total 15.867 15.842

Corporate finance services 0.042 0.276 6.65610

1 25.29789

others 0.589 0.815 93.3439 74.70211

Total 0.631 1.091

TOTAL 16498 16.933

12

Appendix

Auditor fees 2017 2016 % %

Audit and review of

financial reports

Audit of annual report 3381 3.126 21308.3

8 19.73236

Subsidiaries auditing

process

7.04 7.715 44.3688

2 48.69966

Assurance affairs 3.597 3.493 22.6696

9 22.04898

other segments 1,849 1.508 11653.1

2 9.519

Total 15.867 15.842

Corporate finance services 0.042 0.276 6.65610

1 25.29789

others 0.589 0.815 93.3439 74.70211

Total 0.631 1.091

TOTAL 16498 16.933

12

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.