Australia and New Zealand Bank- Deep Financial Analysis

VerifiedAdded on 2023/03/17

|12

|3529

|61

AI Summary

This document provides a deep financial analysis of Australia and New Zealand Bank (ANZ), including industry description, company description, financial instruments analysis, financial ratio analysis, competitor analysis, and financial market analysis.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

AUSTRALIA

AND

NEWZEALAND

BANK LIMITED

AND

NEWZEALAND

BANK LIMITED

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Contents

Industry description..................................................................................................................................3

Company description................................................................................................................................4

Financial Instruments Analysis.................................................................................................................5

Financial Ratio Analysis.............................................................................................................................6

Three Key financial ratios for the bank are:..........................................................................................6

Part B – Competitor Analysis................................................................................................................7

Financial Market Analysis.........................................................................................................................8

Findings, Conclusion and Recommendations...........................................................................................9

References..............................................................................................................................................10

Industry description..................................................................................................................................3

Company description................................................................................................................................4

Financial Instruments Analysis.................................................................................................................5

Financial Ratio Analysis.............................................................................................................................6

Three Key financial ratios for the bank are:..........................................................................................6

Part B – Competitor Analysis................................................................................................................7

Financial Market Analysis.........................................................................................................................8

Findings, Conclusion and Recommendations...........................................................................................9

References..............................................................................................................................................10

Australia and New Zealand Bank- Deep Financial Analysis

Industry description

Australia’s banking industry contributes a major share in the financial system.It also comprised of

147 authorised deposit-taking institutions which aggregate hold $4.6 trillion in assets, around two-

and-a-half times the size of Australia’s $1.8 trillion nominal economy. The major banks like

Australia and New Zealand Bank (ANZ), Bank of Queensland, Commonwealth Bank of Australia etc.

aggregate makes up 44% of the market capitalisation of the S&P/ASX20 and approximately 27% of

the market capitalisation of the S&P/ASX100.2 in terms of value. (S&P Dow Jones Indices LLC,

2019)

The main regulators of this high-profile industry are:

i)Australian Prudential Regulation Authority (APRA) – An integrated prudential regulator which

acts as watchdog for ADIs and some other insurance and superannuation. (Thomson Reuters. ,

2019)

ii) Australian Securities and Investments Commission (ASIC) – It develops policies, guidance,

enforcing legislative compliances and promotes honesty and fairness in company affairs.

(Thomson Reuters. , 2019)

iii) Reserve Bank of Australia (RBA) – Being the central bank of the country, it is responsible for

framing and implementation of monetary policy and maintenance of financial stability.

(Thomson Reuters. , 2019)

iv) Extent of Regulators Powers in the context of ensuring compliance:

APRA has strong statutory powers to ensure compliance to prudential standards framed by

it and even revoke an entity’s license for breach of these standards.

ASIC enforces the provisions of the Corporations Act, thus, controlling malpractices like

insider trading and market manipulation.

RBA functioning under the Reserve Bank Act 1959 (RBA Act) governs the ADIs in terms of

aligning their objectives with the goals of monetary policy, however interfering only in

matters of public concern.

It is critical for the industry to maintain its housing loan portfolios as it represents a substantial

portion of the market for all ADIs. Thus, it can be reasonably asserted that the construction

industry exercises significant influence over this industry as it supplies around 60% customer base

for the banks. (Reserve Bank Of Australia, 2019)

Industry description

Australia’s banking industry contributes a major share in the financial system.It also comprised of

147 authorised deposit-taking institutions which aggregate hold $4.6 trillion in assets, around two-

and-a-half times the size of Australia’s $1.8 trillion nominal economy. The major banks like

Australia and New Zealand Bank (ANZ), Bank of Queensland, Commonwealth Bank of Australia etc.

aggregate makes up 44% of the market capitalisation of the S&P/ASX20 and approximately 27% of

the market capitalisation of the S&P/ASX100.2 in terms of value. (S&P Dow Jones Indices LLC,

2019)

The main regulators of this high-profile industry are:

i)Australian Prudential Regulation Authority (APRA) – An integrated prudential regulator which

acts as watchdog for ADIs and some other insurance and superannuation. (Thomson Reuters. ,

2019)

ii) Australian Securities and Investments Commission (ASIC) – It develops policies, guidance,

enforcing legislative compliances and promotes honesty and fairness in company affairs.

(Thomson Reuters. , 2019)

iii) Reserve Bank of Australia (RBA) – Being the central bank of the country, it is responsible for

framing and implementation of monetary policy and maintenance of financial stability.

(Thomson Reuters. , 2019)

iv) Extent of Regulators Powers in the context of ensuring compliance:

APRA has strong statutory powers to ensure compliance to prudential standards framed by

it and even revoke an entity’s license for breach of these standards.

ASIC enforces the provisions of the Corporations Act, thus, controlling malpractices like

insider trading and market manipulation.

RBA functioning under the Reserve Bank Act 1959 (RBA Act) governs the ADIs in terms of

aligning their objectives with the goals of monetary policy, however interfering only in

matters of public concern.

It is critical for the industry to maintain its housing loan portfolios as it represents a substantial

portion of the market for all ADIs. Thus, it can be reasonably asserted that the construction

industry exercises significant influence over this industry as it supplies around 60% customer base

for the banks. (Reserve Bank Of Australia, 2019)

Company description1

a) The business has four divisions:

v) Australia – Offers full range of banking services at a retail level

vi) Institutional – Mainly serving global institutional and corporate customers in Australia, New

Zealand, Europe, America, Middle East etc. with three products, viz Transaction Banking,

Loans & Specialised Finance and Markets.

vii) Wealth Australia – Provides investment, superannuation, insurance and financial advice

services

viii) Asia Retail & Pacific – Basically, the collection of business units in the Asia-Pacific region

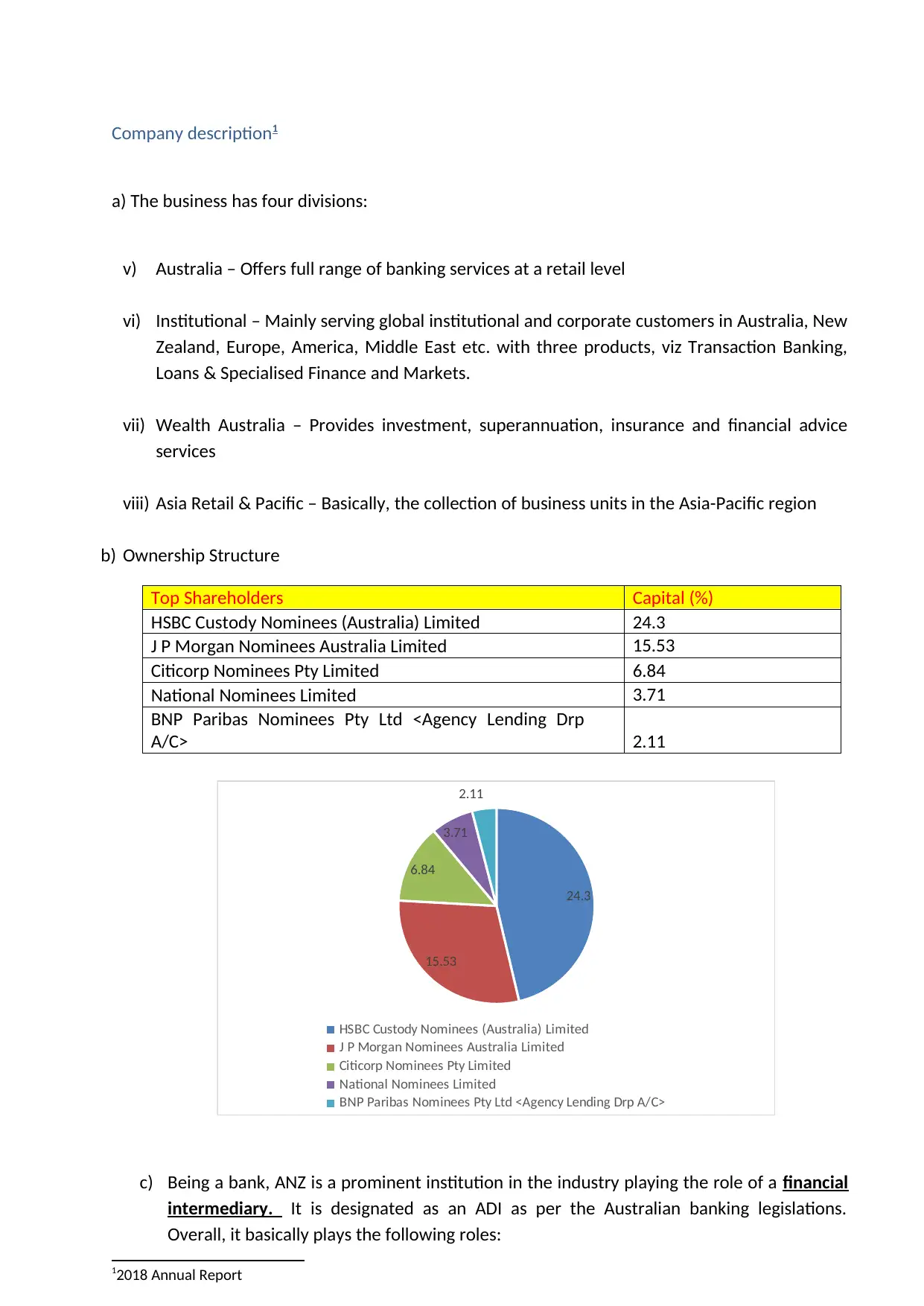

b) Ownership Structure

Top Shareholders Capital (%)

HSBC Custody Nominees (Australia) Limited 24.3

J P Morgan Nominees Australia Limited 15.53

Citicorp Nominees Pty Limited 6.84

National Nominees Limited 3.71

BNP Paribas Nominees Pty Ltd <Agency Lending Drp

A/C> 2.11

c) Being a bank, ANZ is a prominent institution in the industry playing the role of a financial

intermediary. It is designated as an ADI as per the Australian banking legislations.

Overall, it basically plays the following roles:

12018 Annual Report

24.3

15.53

6.84

3.71

2.11

HSBC Custody Nominees (Australia) Limited

J P Morgan Nominees Australia Limited

Citicorp Nominees Pty Limited

National Nominees Limited

BNP Paribas Nominees Pty Ltd <Agency Lending Drp A/C>

a) The business has four divisions:

v) Australia – Offers full range of banking services at a retail level

vi) Institutional – Mainly serving global institutional and corporate customers in Australia, New

Zealand, Europe, America, Middle East etc. with three products, viz Transaction Banking,

Loans & Specialised Finance and Markets.

vii) Wealth Australia – Provides investment, superannuation, insurance and financial advice

services

viii) Asia Retail & Pacific – Basically, the collection of business units in the Asia-Pacific region

b) Ownership Structure

Top Shareholders Capital (%)

HSBC Custody Nominees (Australia) Limited 24.3

J P Morgan Nominees Australia Limited 15.53

Citicorp Nominees Pty Limited 6.84

National Nominees Limited 3.71

BNP Paribas Nominees Pty Ltd <Agency Lending Drp

A/C> 2.11

c) Being a bank, ANZ is a prominent institution in the industry playing the role of a financial

intermediary. It is designated as an ADI as per the Australian banking legislations.

Overall, it basically plays the following roles:

12018 Annual Report

24.3

15.53

6.84

3.71

2.11

HSBC Custody Nominees (Australia) Limited

J P Morgan Nominees Australia Limited

Citicorp Nominees Pty Limited

National Nominees Limited

BNP Paribas Nominees Pty Ltd <Agency Lending Drp A/C>

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

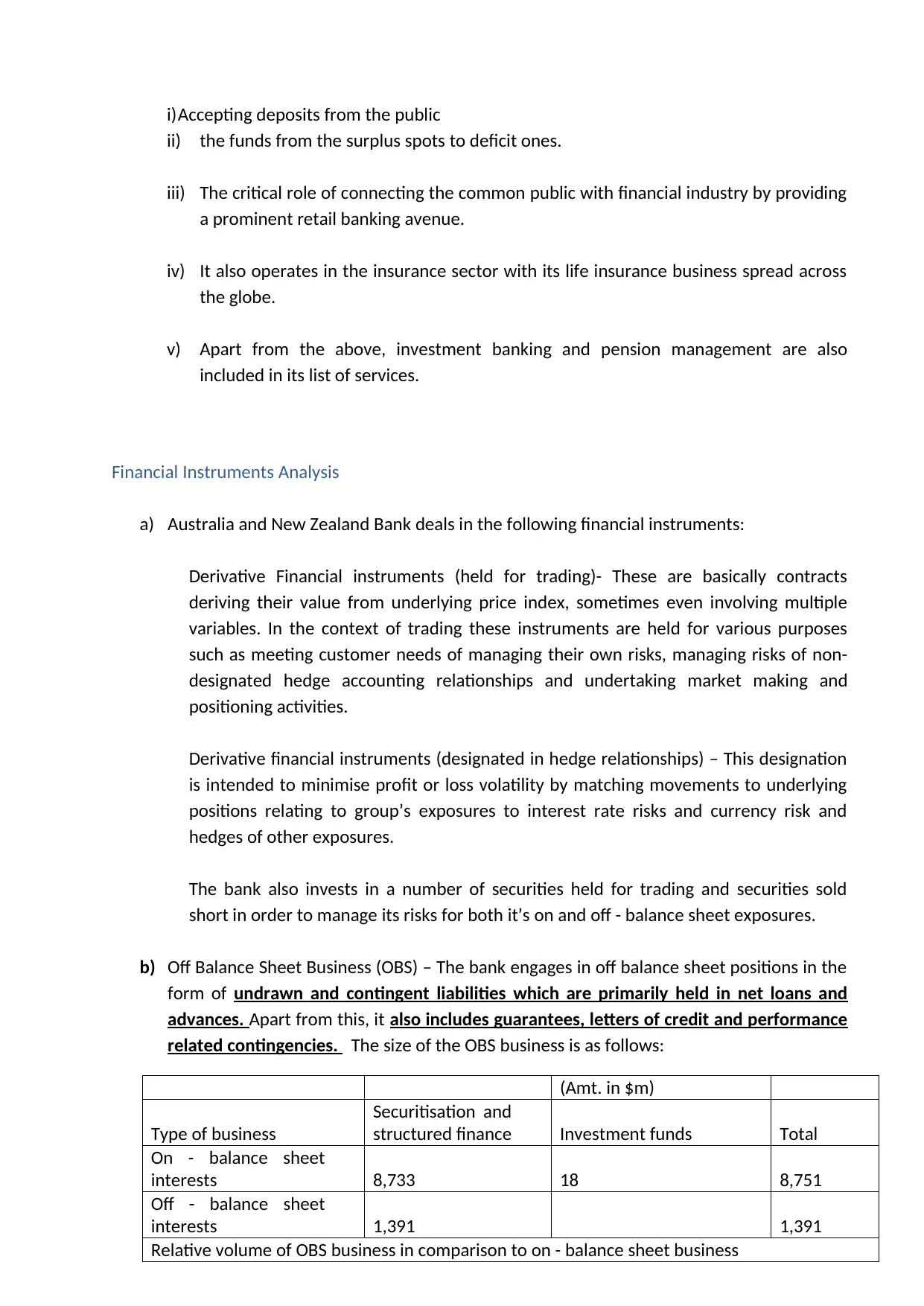

i)Accepting deposits from the public

ii) the funds from the surplus spots to deficit ones.

iii) The critical role of connecting the common public with financial industry by providing

a prominent retail banking avenue.

iv) It also operates in the insurance sector with its life insurance business spread across

the globe.

v) Apart from the above, investment banking and pension management are also

included in its list of services.

Financial Instruments Analysis

a) Australia and New Zealand Bank deals in the following financial instruments:

Derivative Financial instruments (held for trading)- These are basically contracts

deriving their value from underlying price index, sometimes even involving multiple

variables. In the context of trading these instruments are held for various purposes

such as meeting customer needs of managing their own risks, managing risks of non-

designated hedge accounting relationships and undertaking market making and

positioning activities.

Derivative financial instruments (designated in hedge relationships) – This designation

is intended to minimise profit or loss volatility by matching movements to underlying

positions relating to group’s exposures to interest rate risks and currency risk and

hedges of other exposures.

The bank also invests in a number of securities held for trading and securities sold

short in order to manage its risks for both it’s on and off - balance sheet exposures.

b) Off Balance Sheet Business (OBS) – The bank engages in off balance sheet positions in the

form of undrawn and contingent liabilities which are primarily held in net loans and

advances. Apart from this, it also includes guarantees, letters of credit and performance

related contingencies. The size of the OBS business is as follows:

(Amt. in $m)

Type of business

Securitisation and

structured finance Investment funds Total

On - balance sheet

interests 8,733 18 8,751

Off - balance sheet

interests 1,391 1,391

Relative volume of OBS business in comparison to on - balance sheet business

ii) the funds from the surplus spots to deficit ones.

iii) The critical role of connecting the common public with financial industry by providing

a prominent retail banking avenue.

iv) It also operates in the insurance sector with its life insurance business spread across

the globe.

v) Apart from the above, investment banking and pension management are also

included in its list of services.

Financial Instruments Analysis

a) Australia and New Zealand Bank deals in the following financial instruments:

Derivative Financial instruments (held for trading)- These are basically contracts

deriving their value from underlying price index, sometimes even involving multiple

variables. In the context of trading these instruments are held for various purposes

such as meeting customer needs of managing their own risks, managing risks of non-

designated hedge accounting relationships and undertaking market making and

positioning activities.

Derivative financial instruments (designated in hedge relationships) – This designation

is intended to minimise profit or loss volatility by matching movements to underlying

positions relating to group’s exposures to interest rate risks and currency risk and

hedges of other exposures.

The bank also invests in a number of securities held for trading and securities sold

short in order to manage its risks for both it’s on and off - balance sheet exposures.

b) Off Balance Sheet Business (OBS) – The bank engages in off balance sheet positions in the

form of undrawn and contingent liabilities which are primarily held in net loans and

advances. Apart from this, it also includes guarantees, letters of credit and performance

related contingencies. The size of the OBS business is as follows:

(Amt. in $m)

Type of business

Securitisation and

structured finance Investment funds Total

On - balance sheet

interests 8,733 18 8,751

Off - balance sheet

interests 1,391 1,391

Relative volume of OBS business in comparison to on - balance sheet business

15.90%

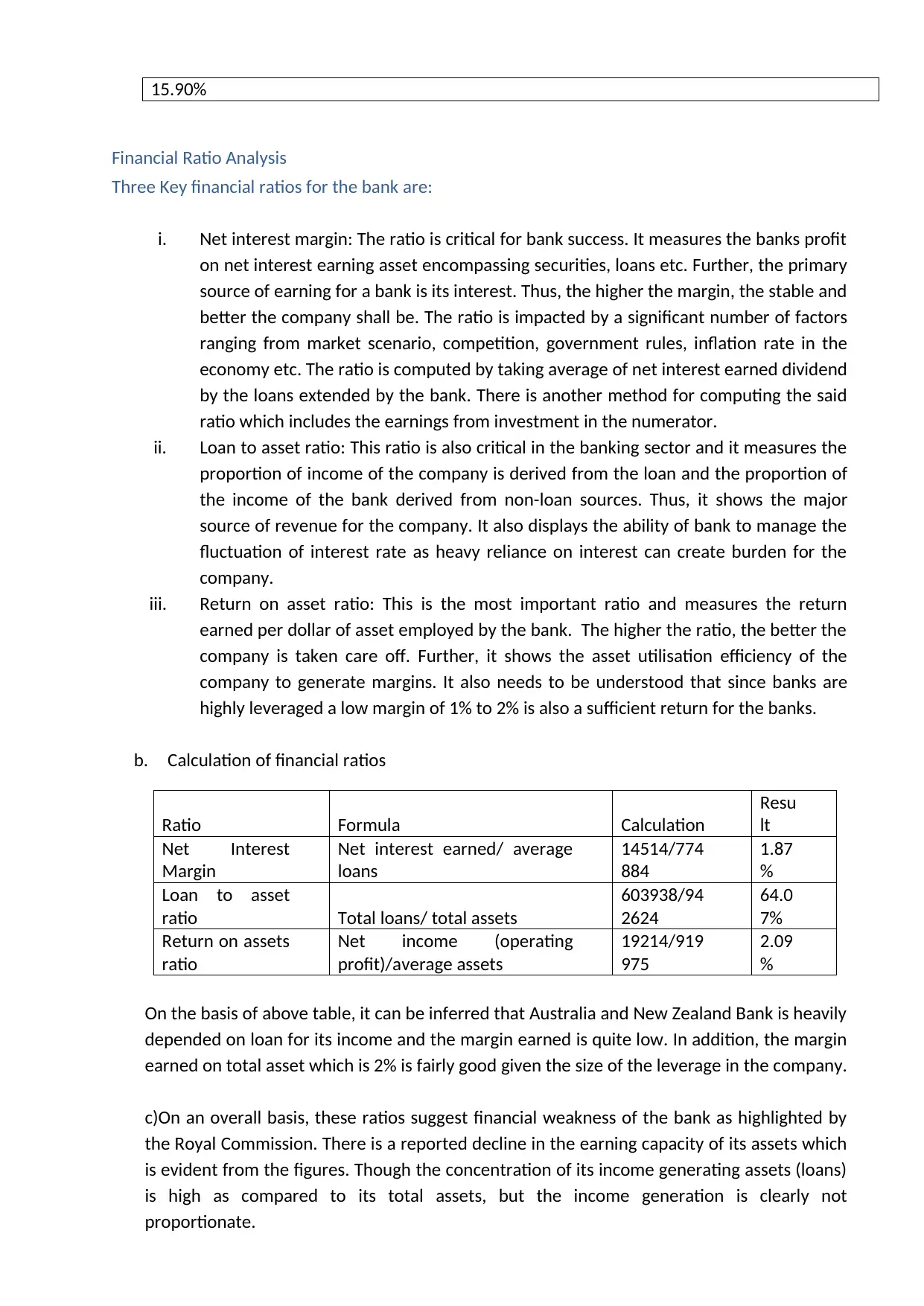

Financial Ratio Analysis

Three Key financial ratios for the bank are:

i. Net interest margin: The ratio is critical for bank success. It measures the banks profit

on net interest earning asset encompassing securities, loans etc. Further, the primary

source of earning for a bank is its interest. Thus, the higher the margin, the stable and

better the company shall be. The ratio is impacted by a significant number of factors

ranging from market scenario, competition, government rules, inflation rate in the

economy etc. The ratio is computed by taking average of net interest earned dividend

by the loans extended by the bank. There is another method for computing the said

ratio which includes the earnings from investment in the numerator.

ii. Loan to asset ratio: This ratio is also critical in the banking sector and it measures the

proportion of income of the company is derived from the loan and the proportion of

the income of the bank derived from non-loan sources. Thus, it shows the major

source of revenue for the company. It also displays the ability of bank to manage the

fluctuation of interest rate as heavy reliance on interest can create burden for the

company.

iii. Return on asset ratio: This is the most important ratio and measures the return

earned per dollar of asset employed by the bank. The higher the ratio, the better the

company is taken care off. Further, it shows the asset utilisation efficiency of the

company to generate margins. It also needs to be understood that since banks are

highly leveraged a low margin of 1% to 2% is also a sufficient return for the banks.

b. Calculation of financial ratios

Ratio Formula Calculation

Resu

lt

Net Interest

Margin

Net interest earned/ average

loans

14514/774

884

1.87

%

Loan to asset

ratio Total loans/ total assets

603938/94

2624

64.0

7%

Return on assets

ratio

Net income (operating

profit)/average assets

19214/919

975

2.09

%

On the basis of above table, it can be inferred that Australia and New Zealand Bank is heavily

depended on loan for its income and the margin earned is quite low. In addition, the margin

earned on total asset which is 2% is fairly good given the size of the leverage in the company.

c)On an overall basis, these ratios suggest financial weakness of the bank as highlighted by

the Royal Commission. There is a reported decline in the earning capacity of its assets which

is evident from the figures. Though the concentration of its income generating assets (loans)

is high as compared to its total assets, but the income generation is clearly not

proportionate.

Financial Ratio Analysis

Three Key financial ratios for the bank are:

i. Net interest margin: The ratio is critical for bank success. It measures the banks profit

on net interest earning asset encompassing securities, loans etc. Further, the primary

source of earning for a bank is its interest. Thus, the higher the margin, the stable and

better the company shall be. The ratio is impacted by a significant number of factors

ranging from market scenario, competition, government rules, inflation rate in the

economy etc. The ratio is computed by taking average of net interest earned dividend

by the loans extended by the bank. There is another method for computing the said

ratio which includes the earnings from investment in the numerator.

ii. Loan to asset ratio: This ratio is also critical in the banking sector and it measures the

proportion of income of the company is derived from the loan and the proportion of

the income of the bank derived from non-loan sources. Thus, it shows the major

source of revenue for the company. It also displays the ability of bank to manage the

fluctuation of interest rate as heavy reliance on interest can create burden for the

company.

iii. Return on asset ratio: This is the most important ratio and measures the return

earned per dollar of asset employed by the bank. The higher the ratio, the better the

company is taken care off. Further, it shows the asset utilisation efficiency of the

company to generate margins. It also needs to be understood that since banks are

highly leveraged a low margin of 1% to 2% is also a sufficient return for the banks.

b. Calculation of financial ratios

Ratio Formula Calculation

Resu

lt

Net Interest

Margin

Net interest earned/ average

loans

14514/774

884

1.87

%

Loan to asset

ratio Total loans/ total assets

603938/94

2624

64.0

7%

Return on assets

ratio

Net income (operating

profit)/average assets

19214/919

975

2.09

%

On the basis of above table, it can be inferred that Australia and New Zealand Bank is heavily

depended on loan for its income and the margin earned is quite low. In addition, the margin

earned on total asset which is 2% is fairly good given the size of the leverage in the company.

c)On an overall basis, these ratios suggest financial weakness of the bank as highlighted by

the Royal Commission. There is a reported decline in the earning capacity of its assets which

is evident from the figures. Though the concentration of its income generating assets (loans)

is high as compared to its total assets, but the income generation is clearly not

proportionate.

Part B – Competitor Analysis

a) Company’s Main Competitors are – Commonwealth Bank, West Pac and National Australia Bank

as provided below:

i. Commonwealth Bank – Founded in 1911, it is ANZ’s biggest rival. As evident, it generates

around $6B more than ANZ. Commonwealth Bank is the largest of all the bank in Australia

and it also provides a varied range of services to its customers. Today in the existing market

it provides services related to retail, business, institutional banking and services related to

wealth management to more than 16.6 million customers. This bank also has staff more than

51,800 in numbers and also operates more than 11,000 branches.

ii. Westpac – Founded in 1817, the company has its headquarters in Sydney, New South Wales.

It generates 276% of ANZ’s revenue. Westpac also provide varied range of services through

its five divisions namely Business Bank, Consumer Bank, BT Financial Group, Westpac

Institutional Bank and Westpac New Zealand. The bank also has staff more than 32,620 in

number.

iii. National Australia Bank –National Australia Bank has a headquarter in Docklands and this

bank is formed through the merger of National Bank of Australasia and the Commercial

Banking Company of Sydney in the year 1982.This bank has its operation in New Zealand, US,

Asia and Europe. The bank also has staff more than 35,063 in number.

b) Basis of Competition in the industry:

i) Price/ Interest Rate – Prices tend to be closely matched with prompt reactions by smaller

banks to the rate changes of even a single major bank. Many customers favour centralised

services like bundling, thus, making individual pricing difficult. The two-sided nature of

banking market also makes assessment of price-based competition.

ii) Product – It basically depends on the product differentiation through means such as bundling

which allows the bank to charge a premium price. This type of competition is also influenced

by two major factors- innovation and branding which constitute the most significant aspect of

the product mix. Many banks are seeking to these aspects like the introduction of Fast pay

and go Money by ANZ and targeted marketing through the use of data analytics.

iii) Varied Services: Different banks offer different unique services to client to attract them.

Further, may offer certain benefits to its client in order to attract more deposit and also may

provide incentives on taking loan clients.

c) These competitors pose a threat to ANZ because of the following factors:

a) Company’s Main Competitors are – Commonwealth Bank, West Pac and National Australia Bank

as provided below:

i. Commonwealth Bank – Founded in 1911, it is ANZ’s biggest rival. As evident, it generates

around $6B more than ANZ. Commonwealth Bank is the largest of all the bank in Australia

and it also provides a varied range of services to its customers. Today in the existing market

it provides services related to retail, business, institutional banking and services related to

wealth management to more than 16.6 million customers. This bank also has staff more than

51,800 in numbers and also operates more than 11,000 branches.

ii. Westpac – Founded in 1817, the company has its headquarters in Sydney, New South Wales.

It generates 276% of ANZ’s revenue. Westpac also provide varied range of services through

its five divisions namely Business Bank, Consumer Bank, BT Financial Group, Westpac

Institutional Bank and Westpac New Zealand. The bank also has staff more than 32,620 in

number.

iii. National Australia Bank –National Australia Bank has a headquarter in Docklands and this

bank is formed through the merger of National Bank of Australasia and the Commercial

Banking Company of Sydney in the year 1982.This bank has its operation in New Zealand, US,

Asia and Europe. The bank also has staff more than 35,063 in number.

b) Basis of Competition in the industry:

i) Price/ Interest Rate – Prices tend to be closely matched with prompt reactions by smaller

banks to the rate changes of even a single major bank. Many customers favour centralised

services like bundling, thus, making individual pricing difficult. The two-sided nature of

banking market also makes assessment of price-based competition.

ii) Product – It basically depends on the product differentiation through means such as bundling

which allows the bank to charge a premium price. This type of competition is also influenced

by two major factors- innovation and branding which constitute the most significant aspect of

the product mix. Many banks are seeking to these aspects like the introduction of Fast pay

and go Money by ANZ and targeted marketing through the use of data analytics.

iii) Varied Services: Different banks offer different unique services to client to attract them.

Further, may offer certain benefits to its client in order to attract more deposit and also may

provide incentives on taking loan clients.

c) These competitors pose a threat to ANZ because of the following factors:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

i. Relative employee base of ANZ is quite substantial as compared to other banks, however, still its

prospects suffer on funding and investment fronts. (Deloitte Access Economics Pty Ltd, 2014)

ii. The competition level is likely to be intensified by the increased regulations and the increased

risk exposures in the industry which can pose serious concerns in the light of the weak financials

of the bank.

iii. Grave concerns are marked for the bank as the securitisation funding has declined to a

comparatively insignificant level coupled with increased dependence on deposits which

ultimately increases the cost of capital.

iv. Increasing competition from foreign banks in Australia and Asia Pacific Regions is also a threat for

ANZ in the upcoming future.

v. Shrinking non other sources of income for the company and heavy dependence on loan earnings.

vi. Better asset management among the other TOP 5 Banks.

Financial Market Analysis

A. In every country there is a financial system which allows the movement of funds between

lenders, investors and borrowers. The system rums at national and global level. The all

services provided consist of close relation between the borrower and investors of the

company. Banks are the main financial intermediary which acts as a middleman between

the lenders and depositor. They are the major player of the market as they move fund

from one party who have excess capital funding to another party who have shortages of

fund This process creates an efficient business and lowers the cost of business. Banking is

the channel through which the borrowers, investors, financial intermediaries and

regulators connect with each other through the mediator bankThe banking channel also

connects the borrower and lender of money by providing them the required capital from

other financial institutions and the federal reserve of the bank.

All the players in the banking sector are in mutually beneficial relationship as whether it is

an investor, borrowers, financial intermediaries, regulators. As the financial players are

satisfied with the return and urgent need derived through the bank sector. Investors and

financial intermediaries derive the return from their deposit and borrowers derive the

fund required.

B. The Australian banking system plays a very vital role in the financial system of the

country. Apart from the traditional service which is provided by the bank, the bank also

provides many services which include business banking, trading in financial market,

stockbroking, insurance and fund management services. There are mainly 53 Australian

Banks out of which 14 are owned by the Australian government. (CFI Education Inc.,

2019)

prospects suffer on funding and investment fronts. (Deloitte Access Economics Pty Ltd, 2014)

ii. The competition level is likely to be intensified by the increased regulations and the increased

risk exposures in the industry which can pose serious concerns in the light of the weak financials

of the bank.

iii. Grave concerns are marked for the bank as the securitisation funding has declined to a

comparatively insignificant level coupled with increased dependence on deposits which

ultimately increases the cost of capital.

iv. Increasing competition from foreign banks in Australia and Asia Pacific Regions is also a threat for

ANZ in the upcoming future.

v. Shrinking non other sources of income for the company and heavy dependence on loan earnings.

vi. Better asset management among the other TOP 5 Banks.

Financial Market Analysis

A. In every country there is a financial system which allows the movement of funds between

lenders, investors and borrowers. The system rums at national and global level. The all

services provided consist of close relation between the borrower and investors of the

company. Banks are the main financial intermediary which acts as a middleman between

the lenders and depositor. They are the major player of the market as they move fund

from one party who have excess capital funding to another party who have shortages of

fund This process creates an efficient business and lowers the cost of business. Banking is

the channel through which the borrowers, investors, financial intermediaries and

regulators connect with each other through the mediator bankThe banking channel also

connects the borrower and lender of money by providing them the required capital from

other financial institutions and the federal reserve of the bank.

All the players in the banking sector are in mutually beneficial relationship as whether it is

an investor, borrowers, financial intermediaries, regulators. As the financial players are

satisfied with the return and urgent need derived through the bank sector. Investors and

financial intermediaries derive the return from their deposit and borrowers derive the

fund required.

B. The Australian banking system plays a very vital role in the financial system of the

country. Apart from the traditional service which is provided by the bank, the bank also

provides many services which include business banking, trading in financial market,

stockbroking, insurance and fund management services. There are mainly 53 Australian

Banks out of which 14 are owned by the Australian government. (CFI Education Inc.,

2019)

The need for the government regulations is because of the few reasons like if there is no

stability in the financial system than it can have major effects in the domestic and

international sectors. Protection of consumer which is very much important as the

government had the main obligation to protect the need of consumer, as various laws

and rules came in force which protect the customer right and give fair and equal access to

credit. The bank conducts the banking transactions with customers either directly or in

directly .The regulators of the bank enforce consumer protection by overviewing the

banking operations conducted and customer complaint on a daily basis. (Stackhouse,

2017)

C. The Australia and New Zealand Bank head of the lending service department admitted

that the bank had been continuously involved in “unethical and unfair” in all its dealing

with the rural families. He (Steinberg head of the Australia New Zealand Bank) also

admitted that the bank did not comply with the banking code of practice which is

required to be complied in terms of the financial assistance to their client.

Steinberg also quoted that "I think the dealings were consistent but I think they weren’t

fair and they weren’t reasonable, “Steinberg also added that the bank was not ethical at

all in dealings with clients.

One case which was also heard about the bank about the 87-year-old Charlie phillott,

who was forced by the bank to leave his property in which he was residing despite of any

failure to meet the mortgage repayment. Charlie also added that the ANZ bank had

devalued his station because the said region was affected by drought. But when this news

came to light in media and Charlie updated to the media about the case, the ANZ bank

returned back the property to Charlie and apologised for the mistake. (Tacadena, 2018)

One case also heard about the ANZ bank about the chessman family who used to run a

farm in western Victoria and due to financial pro problem when chessman decided to sell

the farm, the ANZ denied the request of keeping their homes and farm. .When the

commission asked about the case of chessman’s he admitted that whatever has been

done was bad ,he also added “If this was done today it would be dealt with in different

way” (Tacadena, 2018)

Findings, Conclusion and Recommendations

The four major banks in Australia comprised of Westpac Banking Corporation,

Commonwealth Bank of Australia, Australia and New Zealand Banking Group (ANZ) and

National Australia Bank (NAB). But the major concern about the bank is about the

liquidity as it is there in the rest of the world. The banking system in country Australia is

reliable and transparent, but there are huge structural and operational differences

between the management of Australian and American bank. The banking structure of

Australia have not been operating under any restrictions that US bank operations

between 1933 and the repeal of the Glass Steagall Act. The Australian Bank is such in a

position that the distinction between the retail and investment bank cannot be seen. (The

International Trade Administration (ITA), 2018)

stability in the financial system than it can have major effects in the domestic and

international sectors. Protection of consumer which is very much important as the

government had the main obligation to protect the need of consumer, as various laws

and rules came in force which protect the customer right and give fair and equal access to

credit. The bank conducts the banking transactions with customers either directly or in

directly .The regulators of the bank enforce consumer protection by overviewing the

banking operations conducted and customer complaint on a daily basis. (Stackhouse,

2017)

C. The Australia and New Zealand Bank head of the lending service department admitted

that the bank had been continuously involved in “unethical and unfair” in all its dealing

with the rural families. He (Steinberg head of the Australia New Zealand Bank) also

admitted that the bank did not comply with the banking code of practice which is

required to be complied in terms of the financial assistance to their client.

Steinberg also quoted that "I think the dealings were consistent but I think they weren’t

fair and they weren’t reasonable, “Steinberg also added that the bank was not ethical at

all in dealings with clients.

One case which was also heard about the bank about the 87-year-old Charlie phillott,

who was forced by the bank to leave his property in which he was residing despite of any

failure to meet the mortgage repayment. Charlie also added that the ANZ bank had

devalued his station because the said region was affected by drought. But when this news

came to light in media and Charlie updated to the media about the case, the ANZ bank

returned back the property to Charlie and apologised for the mistake. (Tacadena, 2018)

One case also heard about the ANZ bank about the chessman family who used to run a

farm in western Victoria and due to financial pro problem when chessman decided to sell

the farm, the ANZ denied the request of keeping their homes and farm. .When the

commission asked about the case of chessman’s he admitted that whatever has been

done was bad ,he also added “If this was done today it would be dealt with in different

way” (Tacadena, 2018)

Findings, Conclusion and Recommendations

The four major banks in Australia comprised of Westpac Banking Corporation,

Commonwealth Bank of Australia, Australia and New Zealand Banking Group (ANZ) and

National Australia Bank (NAB). But the major concern about the bank is about the

liquidity as it is there in the rest of the world. The banking system in country Australia is

reliable and transparent, but there are huge structural and operational differences

between the management of Australian and American bank. The banking structure of

Australia have not been operating under any restrictions that US bank operations

between 1933 and the repeal of the Glass Steagall Act. The Australian Bank is such in a

position that the distinction between the retail and investment bank cannot be seen. (The

International Trade Administration (ITA), 2018)

The condition is such that the Australian banking system is undergoing continuously

deregulation and privatization. The foreign banks also can easily enter the market. The

retail banks also can provide nowadays wide variety of services like life insurance, general

insurance brokering services. And underwriting of stock for few customers. In addition to

all the above providing consumer and corporate loan to the consumer. This also helps

them to do competition with other brokerage firm and industry houses. (The

International Trade Administration (ITA), 2018)

The Australian Government also allows non -Australian banks to operate their branches

to serve the wholesale market. According to the banking regulation act only retail banking

is allowed to operate through a locally -incorporated subsidiary. (The International Trade

Administration (ITA), 2018)

Further recommendations which can be provided from the industry experts and

regulators in order to sustain is that there should be strict banking code and regulations

in order to protect the interest of customer ,there should be stringent rules and

regulation to assure that the foreign bank does not enter the domestic market without

complying with proper rules and policy Reserve Bank Of Australia.

References

CFI Education Inc., 2019. Overview of Australian Banks. [Online]

Available at: https://corporatefinanceinstitute.com/resources/careers/companies/top-australian-

banks/

[Accessed 17 May 2019].

deregulation and privatization. The foreign banks also can easily enter the market. The

retail banks also can provide nowadays wide variety of services like life insurance, general

insurance brokering services. And underwriting of stock for few customers. In addition to

all the above providing consumer and corporate loan to the consumer. This also helps

them to do competition with other brokerage firm and industry houses. (The

International Trade Administration (ITA), 2018)

The Australian Government also allows non -Australian banks to operate their branches

to serve the wholesale market. According to the banking regulation act only retail banking

is allowed to operate through a locally -incorporated subsidiary. (The International Trade

Administration (ITA), 2018)

Further recommendations which can be provided from the industry experts and

regulators in order to sustain is that there should be strict banking code and regulations

in order to protect the interest of customer ,there should be stringent rules and

regulation to assure that the foreign bank does not enter the domestic market without

complying with proper rules and policy Reserve Bank Of Australia.

References

CFI Education Inc., 2019. Overview of Australian Banks. [Online]

Available at: https://corporatefinanceinstitute.com/resources/careers/companies/top-australian-

banks/

[Accessed 17 May 2019].

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Commonwealth Of Australia, 2018. Some Features of the Australian Banking Industry. [Online]

Available at: https://financialservices.royalcommission.gov.au/publications/Documents/some-

features-of-the-australian-banking-industry-background-paper-1.pdf

[Accessed 16 May 2019].

Deloitte Access Economics Pty Ltd, 2014. Competition in retail Banking. [Online]

Available at: https://www2.deloitte.com/content/dam/Deloitte/au/Documents/Economics/deloitte-

au-economics-retail-banking-competition-010314.pdf

[Accessed 16 May 2019].

Reserve Bank Of Australia, 2019. The Australian Financial System. [Online]

Available at: https://www.rba.gov.au/publications/fsr/2015/oct/aus-fin-sys.html

[Accessed 16 May 2019].

S&P Dow Jones Indices LLC, 2019. S&P/ASX 300 (AUD). [Online]

Available at: https://us.spindices.com/indices/equity/sp-asx-300

[Accessed 16 May 2019].

Stackhouse, J., 2017. Why Are Banks Regulated?. [Online]

Available at: https://www.stlouisfed.org/on-the-economy/2017/january/why-federal-reserve-

regulate-banks

[Accessed 17 May 2019].

Tacadena, G., 2018. ANZ owns up to unethical and unfair practices. [Online]

Available at: https://www.yourmortgage.com.au/mortgage-news/anz-owns-up-to-unethical-and-

unfair-practices/251676/

[Accessed 17 May 2019].

The International Trade Administration (ITA), 2018. Australia - Banking Systems. [Online]

Available at: https://www.export.gov/article?id=Australia-banking-systems

[Accessed 17 May 2019].

Thomson Reuters. , 2019. Banking regulation in Australia: overview. [Online]

Available at: https://uk.practicallaw.thomsonreuters.com/w-006-9098?

transitionType=Default&contextData=(sc.Default)&firstPage=true&comp=pluk&bhcp=1

[Accessed 16 May 2019].

Available at: https://financialservices.royalcommission.gov.au/publications/Documents/some-

features-of-the-australian-banking-industry-background-paper-1.pdf

[Accessed 16 May 2019].

Deloitte Access Economics Pty Ltd, 2014. Competition in retail Banking. [Online]

Available at: https://www2.deloitte.com/content/dam/Deloitte/au/Documents/Economics/deloitte-

au-economics-retail-banking-competition-010314.pdf

[Accessed 16 May 2019].

Reserve Bank Of Australia, 2019. The Australian Financial System. [Online]

Available at: https://www.rba.gov.au/publications/fsr/2015/oct/aus-fin-sys.html

[Accessed 16 May 2019].

S&P Dow Jones Indices LLC, 2019. S&P/ASX 300 (AUD). [Online]

Available at: https://us.spindices.com/indices/equity/sp-asx-300

[Accessed 16 May 2019].

Stackhouse, J., 2017. Why Are Banks Regulated?. [Online]

Available at: https://www.stlouisfed.org/on-the-economy/2017/january/why-federal-reserve-

regulate-banks

[Accessed 17 May 2019].

Tacadena, G., 2018. ANZ owns up to unethical and unfair practices. [Online]

Available at: https://www.yourmortgage.com.au/mortgage-news/anz-owns-up-to-unethical-and-

unfair-practices/251676/

[Accessed 17 May 2019].

The International Trade Administration (ITA), 2018. Australia - Banking Systems. [Online]

Available at: https://www.export.gov/article?id=Australia-banking-systems

[Accessed 17 May 2019].

Thomson Reuters. , 2019. Banking regulation in Australia: overview. [Online]

Available at: https://uk.practicallaw.thomsonreuters.com/w-006-9098?

transitionType=Default&contextData=(sc.Default)&firstPage=true&comp=pluk&bhcp=1

[Accessed 16 May 2019].

APPENDIX:

Attached report of ANZ bank limited

Attached report of ANZ bank limited

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.