Risk and Regulations in AML/CTF Program for Australian Banks

VerifiedAdded on 2022/11/16

|20

|4267

|304

AI Summary

This document discusses the risk assessment programs undertaken by Australian banks to evaluate the severity and likelihood of AML/CTF risks. It also covers the identification and segregation of risks, calculating the likelihood and impact of risk occurrence, strategy formulation, and customer, product, delivery, and jurisdiction risks.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Running head: AUSTRALIA

RISK AND REGULATIONS

CON-000523338

Name of the student

Name of the university

Author note

RISK AND REGULATIONS

CON-000523338

Name of the student

Name of the university

Author note

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

1AUSTRALIA

Part a

Risk assessment programs are undertaken by the organizations with the objective of

evaluating the severity and the likelihood of the risk to occur. On the contrary, the different

modifications that are planned by the organizations are enabled through the evolution of

different strategies based on the prioritization of risks. It has been noted that the different

changes that are commenced by the organizations might face a significant amount of risks that

should be assessed and addressed with the objective of continuing the progressiveness. In this

relation, the assessment of the AML/CTF risks is assessed by banks with the objective of

minimizing the chances of fraudulent activities relating to money laundering and misstatement1.

Again, the purpose of undertaking the risk assessment is to identify the sources of terrorist

financing (ML/TF) for grasping the even distribution of control mechanisms.

The risk assessment programs that are commenced by the organizations are mainly

divided into two parts- Part A and Part B. The AML program requires the enrollment of the

Australian bank with AUSTRAC after which the operational criterions are developed in

orientation with the needs of the venture. The creation of the operational framework after the

assessment and prioritization of the risks would enable the organization in improving the success

factors of the program. The major steps of the risks assessment and strategy formulating

operations are undertaken by the organizations in part a of the AML program2. In this relation,

1 Choo, Kim-Kwang Raymond. "Designated non-financial businesses and professionals: A

review and analysis of recent financial action task force on money laundering mutual evaluation

reports." Security Journal 27, no. 1 (2014): 1-26.

2 De Koker, Louis, and Mark Turkington. "Anti-money laundering measures and the

effectiveness question." In Research Handbook on International Financial Crime. Edward Elgar

Part a

Risk assessment programs are undertaken by the organizations with the objective of

evaluating the severity and the likelihood of the risk to occur. On the contrary, the different

modifications that are planned by the organizations are enabled through the evolution of

different strategies based on the prioritization of risks. It has been noted that the different

changes that are commenced by the organizations might face a significant amount of risks that

should be assessed and addressed with the objective of continuing the progressiveness. In this

relation, the assessment of the AML/CTF risks is assessed by banks with the objective of

minimizing the chances of fraudulent activities relating to money laundering and misstatement1.

Again, the purpose of undertaking the risk assessment is to identify the sources of terrorist

financing (ML/TF) for grasping the even distribution of control mechanisms.

The risk assessment programs that are commenced by the organizations are mainly

divided into two parts- Part A and Part B. The AML program requires the enrollment of the

Australian bank with AUSTRAC after which the operational criterions are developed in

orientation with the needs of the venture. The creation of the operational framework after the

assessment and prioritization of the risks would enable the organization in improving the success

factors of the program. The major steps of the risks assessment and strategy formulating

operations are undertaken by the organizations in part a of the AML program2. In this relation,

1 Choo, Kim-Kwang Raymond. "Designated non-financial businesses and professionals: A

review and analysis of recent financial action task force on money laundering mutual evaluation

reports." Security Journal 27, no. 1 (2014): 1-26.

2 De Koker, Louis, and Mark Turkington. "Anti-money laundering measures and the

effectiveness question." In Research Handbook on International Financial Crime. Edward Elgar

2AUSTRALIA

the AML/CTF program is divided into two parts, namely Part A and Part B, would enable the

organization in improving the rate of operations3.

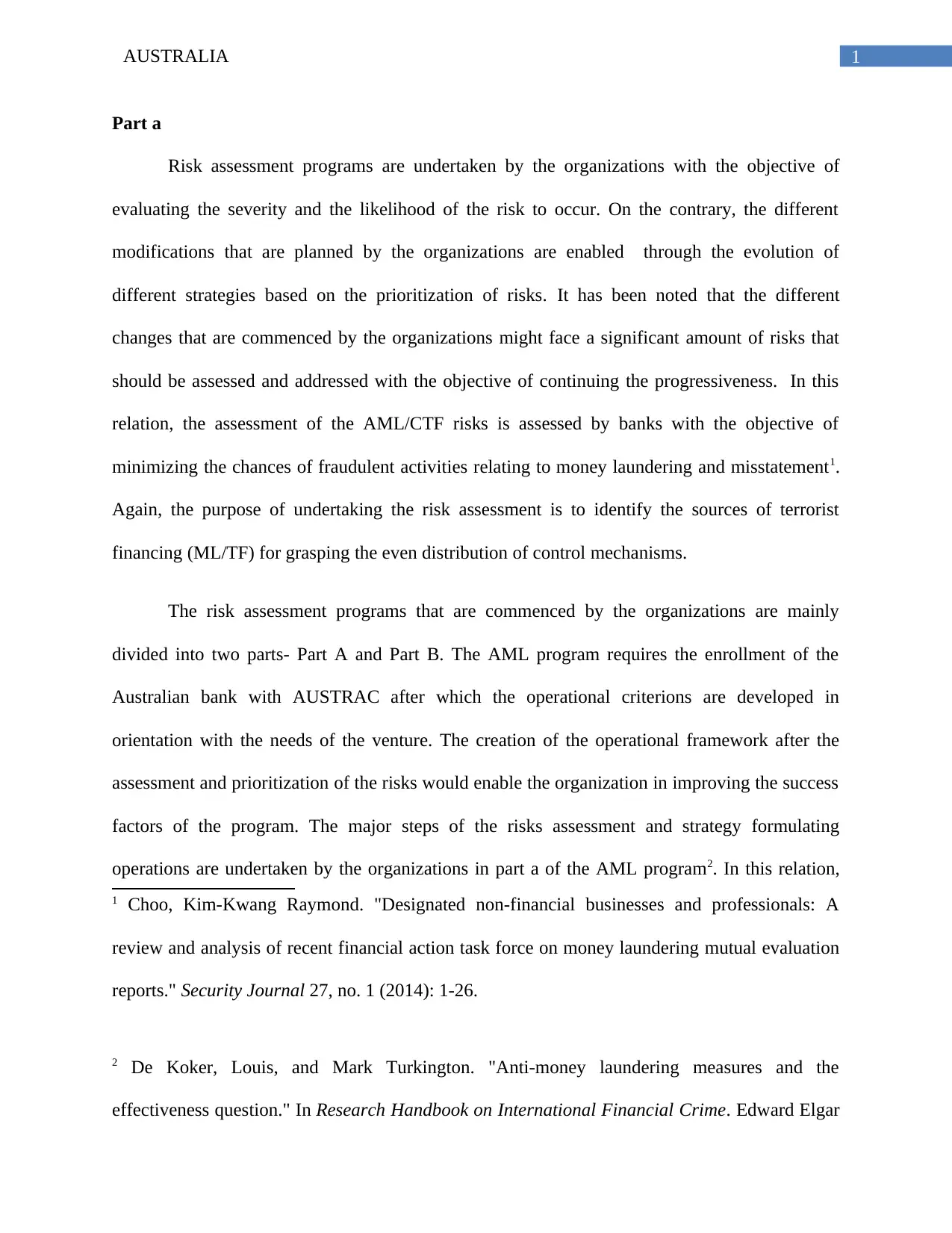

Figure: AML/CTF Risk Factors (Source: 4)

Part A of AML/CTF risk program

Identification and segregation of risks

Publishing, 2015.

3 Fratangelo, Pierpaolo. "Prevention and countering of money laundering and terrorism

financing." In Italian Banking and Financial Law, pp. 105-130. Palgrave Macmillan, London,

2015.

4 De Koker, Louis. "Money laundering compliance—the challenges of technology." In Financial

Crimes: Psychological, Technological, and Ethical Issues, pp. 329-347. Springer, Cham, 2016.

the AML/CTF program is divided into two parts, namely Part A and Part B, would enable the

organization in improving the rate of operations3.

Figure: AML/CTF Risk Factors (Source: 4)

Part A of AML/CTF risk program

Identification and segregation of risks

Publishing, 2015.

3 Fratangelo, Pierpaolo. "Prevention and countering of money laundering and terrorism

financing." In Italian Banking and Financial Law, pp. 105-130. Palgrave Macmillan, London,

2015.

4 De Koker, Louis. "Money laundering compliance—the challenges of technology." In Financial

Crimes: Psychological, Technological, and Ethical Issues, pp. 329-347. Springer, Cham, 2016.

3AUSTRALIA

The large Australian bank might take steps to enhance communication with the

stakeholders with the objective of continuing the transparency and gaining knowledge of the

procedures followed by the different departments. On the contrary, the bank might also take

steps to consult with the AUSTRAC with the objective reviewing the policies and evaluating the

loopholes that might influence the scope of ML/TF occurrence5. The inherent risks are

specifically the uncertainties that arise out of the operations that are undertaken by the

organizations while operating in the diverse global economies. In this relation, the banks

encounter different risks relating to the internal operations of the employees and the external

aspects like customer insolvency and the like which might affect the interests of the ventures.

Therefore, the banks form different strategies with the objective of minimizing the level of risk

that are encountered by the organizations. The key changes in the organizational operations are

influenced bythe identification of the ML/TF risks and mitigate the same with the objective of

improving the rate of operations. The AML/CTF program enables an organization in addressing

the money laundering and terrorism financing risks that might be faced by the bank. The Risk

program enables an organization in evaluating the customers, the services that are being

provided, the nature of delivery of the services and the jurisdictions that might be taken into

account.

On the other hand, the residual risks that are being faced by the banks are grounded on

the remaining risks that are often encountered by the banks while making fund transfers and

managing wholesome assets of the customers. The residual risks, like the inherent risks are often

5 Gelb, Alan. "Balancing Financial Integrity with Financial Inclusion: The Risk-Based Approach

to «Know Your Customer»." CGD Policy Paper 74 (2016): 1-24.

The large Australian bank might take steps to enhance communication with the

stakeholders with the objective of continuing the transparency and gaining knowledge of the

procedures followed by the different departments. On the contrary, the bank might also take

steps to consult with the AUSTRAC with the objective reviewing the policies and evaluating the

loopholes that might influence the scope of ML/TF occurrence5. The inherent risks are

specifically the uncertainties that arise out of the operations that are undertaken by the

organizations while operating in the diverse global economies. In this relation, the banks

encounter different risks relating to the internal operations of the employees and the external

aspects like customer insolvency and the like which might affect the interests of the ventures.

Therefore, the banks form different strategies with the objective of minimizing the level of risk

that are encountered by the organizations. The key changes in the organizational operations are

influenced bythe identification of the ML/TF risks and mitigate the same with the objective of

improving the rate of operations. The AML/CTF program enables an organization in addressing

the money laundering and terrorism financing risks that might be faced by the bank. The Risk

program enables an organization in evaluating the customers, the services that are being

provided, the nature of delivery of the services and the jurisdictions that might be taken into

account.

On the other hand, the residual risks that are being faced by the banks are grounded on

the remaining risks that are often encountered by the banks while making fund transfers and

managing wholesome assets of the customers. The residual risks, like the inherent risks are often

5 Gelb, Alan. "Balancing Financial Integrity with Financial Inclusion: The Risk-Based Approach

to «Know Your Customer»." CGD Policy Paper 74 (2016): 1-24.

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

4AUSTRALIA

identified and analyzed by the different banks with the objective of reducing the atrocities and

major likelihood of occurring. The major necessities of the AML program are to set out the

policies in writing and reviewing the same from time to time. The delineation of the policies and

the application of the regulatory operations would enable the ventures in discriminating between

the risks and planning compliances. Again, the enhanced operations of the venture is influenced

bythe identification of the issues and the mitigation of the same. The delineation of the issues

and the method that is applied for they might be resolved is one of the major part of the AML

program.

The program is required to be reviewed and reported continuously with the objective of

continuing the efficiency of the operations in orientation with the standards. The reporting of the

risks to the compliance officer and the Board of senior management enables in influencing the

uninterrupted functioning of the program as per the defined parameters6. The segregation of the

risks would allow the organization in evaluating the compliance mechanisms that might be

positioned for the vulnerable situations. Segregation of the risks would enable the organizations

in deriving knowledge of the different situations and likelihood of the risk occurrence7. The

assessment of the likelihood and impact would allow the organization in grading and prioritizing

6 Gurule, Jimmy. "Jimmy Gurule delivered the keynote address at the Korea Banking Risk

Dialogue 2014 in Seoul, South Korea on July 2." (2014).

7 Henning, Johan, and Mignon Hauman. "Fortifying a risk-based approach in the South African

AML/CFT process." Journal of Financial Crime 24, no. 4 (2017): 520-528.

identified and analyzed by the different banks with the objective of reducing the atrocities and

major likelihood of occurring. The major necessities of the AML program are to set out the

policies in writing and reviewing the same from time to time. The delineation of the policies and

the application of the regulatory operations would enable the ventures in discriminating between

the risks and planning compliances. Again, the enhanced operations of the venture is influenced

bythe identification of the issues and the mitigation of the same. The delineation of the issues

and the method that is applied for they might be resolved is one of the major part of the AML

program.

The program is required to be reviewed and reported continuously with the objective of

continuing the efficiency of the operations in orientation with the standards. The reporting of the

risks to the compliance officer and the Board of senior management enables in influencing the

uninterrupted functioning of the program as per the defined parameters6. The segregation of the

risks would allow the organization in evaluating the compliance mechanisms that might be

positioned for the vulnerable situations. Segregation of the risks would enable the organizations

in deriving knowledge of the different situations and likelihood of the risk occurrence7. The

assessment of the likelihood and impact would allow the organization in grading and prioritizing

6 Gurule, Jimmy. "Jimmy Gurule delivered the keynote address at the Korea Banking Risk

Dialogue 2014 in Seoul, South Korea on July 2." (2014).

7 Henning, Johan, and Mignon Hauman. "Fortifying a risk-based approach in the South African

AML/CFT process." Journal of Financial Crime 24, no. 4 (2017): 520-528.

5AUSTRALIA

the risk. Therefore, the process would enable the organizations in evaluating, assessing and

implementing relative compliances for the ML/TF risks.

Calculating the likelihood and the impact of risk occurrence

The organizations might take steps to analyze the risks and thereby calculate the

likelihood and the impact that might be infested by the same on the organizational operations.

The utilization of the risk probability matrix, in this relation, would enable the organizations in

evaluating the prospect of the risks and the compliance framework that might be enabled for

mitigation8. The employee due diligence program would enable the organization in evaluating

the employees which might create vulnerable positions for the organization. On the contrary, the

delineation of the different aspects of change in the organizational operations are influenced

bythe suitable assessment of the risk register. The calculation of the risk score through

multiplying the likelihood with the impact of the risks enables an organization in prioritizing the

different uncertainties that are being faced by the same. In this relation, the different changes in

the organizational operations would be enabled through the effectiveness of the reporting while

adhering to the regulations that are being forwarded by AUSTRAC9. The different aspects of

change that are undertaken by the organizations are influenced bythe efficiency of reporting the

risks that might be encountered by the banks. In this relation, the banks might take steps to

8 Henning, Johan, and Mignon Hauman. "Fortifying a risk-based approach in the South African

AML/CFT process." Journal of Financial Crime 24, no. 4 (2017): 520-528.

9 Mills, Clinton. "Predictive analytics in fraud and AML." Journal of Financial Compliance 1,

no. 1 (2017): 17-26.

the risk. Therefore, the process would enable the organizations in evaluating, assessing and

implementing relative compliances for the ML/TF risks.

Calculating the likelihood and the impact of risk occurrence

The organizations might take steps to analyze the risks and thereby calculate the

likelihood and the impact that might be infested by the same on the organizational operations.

The utilization of the risk probability matrix, in this relation, would enable the organizations in

evaluating the prospect of the risks and the compliance framework that might be enabled for

mitigation8. The employee due diligence program would enable the organization in evaluating

the employees which might create vulnerable positions for the organization. On the contrary, the

delineation of the different aspects of change in the organizational operations are influenced

bythe suitable assessment of the risk register. The calculation of the risk score through

multiplying the likelihood with the impact of the risks enables an organization in prioritizing the

different uncertainties that are being faced by the same. In this relation, the different changes in

the organizational operations would be enabled through the effectiveness of the reporting while

adhering to the regulations that are being forwarded by AUSTRAC9. The different aspects of

change that are undertaken by the organizations are influenced bythe efficiency of reporting the

risks that might be encountered by the banks. In this relation, the banks might take steps to

8 Henning, Johan, and Mignon Hauman. "Fortifying a risk-based approach in the South African

AML/CFT process." Journal of Financial Crime 24, no. 4 (2017): 520-528.

9 Mills, Clinton. "Predictive analytics in fraud and AML." Journal of Financial Compliance 1,

no. 1 (2017): 17-26.

6AUSTRALIA

segregate the products and services that are vulnerable to the ML/TF risks. The segregation of

the products and services enables the banks in easing the reporting based operations.

Strategy formulation

The appropriate identification of the risks would be succeeded by strategy formulation.

The development of different strategies would enable the organizations in continuing the

efficiency of the operations in orientation with the needs of the venture. In this relation, the

strategies that are framed by the organizations are dependent on the extensive operational

framework through which the organization operates. The development of the strategies would be

influenced byconsultation and adherence to the regulations that are imposed by AUSTRAC in

Australia. Therefore, the strategies will be developed through consideration of the operational

framework that would be considered by the organizations. Apart from the strategies the

organization might also take steps to provide adequate training to the employees based on the

AML/CTF requirements with the objective of reducing the likelihood of vulnerable situations10.

The strategies that are formulated by the organizations are influenced bythe effective

understanding of the different risks and the mitigation based strategies that would be considered

by the same with the objective of avoiding the risks related to AML/CTF11.

10 Levi, Michael, Peter Reuter, and Terence Halliday. "Can the AML system be evaluated

without better data?." Crime, Law and Social Change 69, no. 2 (2018): 307-328.

11 Sadiq, Shazia, and Guido Governatori. "Managing regulatory compliance in business

processes." In Handbook on Business Process Management 2, pp. 159-175. Springer, Berlin,

Heidelberg, 2010.

segregate the products and services that are vulnerable to the ML/TF risks. The segregation of

the products and services enables the banks in easing the reporting based operations.

Strategy formulation

The appropriate identification of the risks would be succeeded by strategy formulation.

The development of different strategies would enable the organizations in continuing the

efficiency of the operations in orientation with the needs of the venture. In this relation, the

strategies that are framed by the organizations are dependent on the extensive operational

framework through which the organization operates. The development of the strategies would be

influenced byconsultation and adherence to the regulations that are imposed by AUSTRAC in

Australia. Therefore, the strategies will be developed through consideration of the operational

framework that would be considered by the organizations. Apart from the strategies the

organization might also take steps to provide adequate training to the employees based on the

AML/CTF requirements with the objective of reducing the likelihood of vulnerable situations10.

The strategies that are formulated by the organizations are influenced bythe effective

understanding of the different risks and the mitigation based strategies that would be considered

by the same with the objective of avoiding the risks related to AML/CTF11.

10 Levi, Michael, Peter Reuter, and Terence Halliday. "Can the AML system be evaluated

without better data?." Crime, Law and Social Change 69, no. 2 (2018): 307-328.

11 Sadiq, Shazia, and Guido Governatori. "Managing regulatory compliance in business

processes." In Handbook on Business Process Management 2, pp. 159-175. Springer, Berlin,

Heidelberg, 2010.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7AUSTRALIA

Part B of AML/CTF risk program

The Part B of the AML/CTF plan would address the needs of the organization in

evaluating the background of the customers and reviewing the same before providing with the

services. In this part of the risks assessment plan, the banks must take steps to develop a

complete understanding of the background of the customers through reviewing the KYC

applications. The banking organizations must take steps to segregate the customers into different

groups and determine whether they are associated with politics. The AML/CTF risk assessment

program enables an organization in evaluating the politically exposed person (PEP) with the

objective of reducing the rate of Risks relating to money laundering and terrorist functions. In

this relation, the banks would be reviewing the policies and procedures that are imposed by

AUSTRAC with the objective of planning the time and place of collecting the information of the

customers. The assessment of the customer background would enable the organization in

evaluating the prospective customers for making the transactions while avoiding the risks

relating to AML/CTF12.

Part b

The organizations undertake the AML/CTF risk assessments with the objective of

evaluating the gaps in the policies and procedures which might result to money laundering and

financial thefts or scams. The assessment of the gaps in the policies and procedures would enable

12 Stanley, Rebecca L., and Ross P. Buckley. "Protecting the west, excluding the rest: The impact

of the AML/CTF regime on financial inclusion in the pacific and potential responses." Melb. J.

Int'l L. 17 (2016): 83.

Part B of AML/CTF risk program

The Part B of the AML/CTF plan would address the needs of the organization in

evaluating the background of the customers and reviewing the same before providing with the

services. In this part of the risks assessment plan, the banks must take steps to develop a

complete understanding of the background of the customers through reviewing the KYC

applications. The banking organizations must take steps to segregate the customers into different

groups and determine whether they are associated with politics. The AML/CTF risk assessment

program enables an organization in evaluating the politically exposed person (PEP) with the

objective of reducing the rate of Risks relating to money laundering and terrorist functions. In

this relation, the banks would be reviewing the policies and procedures that are imposed by

AUSTRAC with the objective of planning the time and place of collecting the information of the

customers. The assessment of the customer background would enable the organization in

evaluating the prospective customers for making the transactions while avoiding the risks

relating to AML/CTF12.

Part b

The organizations undertake the AML/CTF risk assessments with the objective of

evaluating the gaps in the policies and procedures which might result to money laundering and

financial thefts or scams. The assessment of the gaps in the policies and procedures would enable

12 Stanley, Rebecca L., and Ross P. Buckley. "Protecting the west, excluding the rest: The impact

of the AML/CTF regime on financial inclusion in the pacific and potential responses." Melb. J.

Int'l L. 17 (2016): 83.

8AUSTRALIA

the organizations in enabling informed decisions while implementing control efforts, allocation

of the resources and technological infusions. The assessment of the nature of the ML/TF risks

and the method that is applied for the same might contribute to the organizational operations will

be influenced bythe effective functioning of the systems in orientation with the needs of the

venture.

While evaluating the literature it has been noted that most of the companies monitor and

implement strategies related to compliance as per the guidelines of the AML program. The

strategies of the organizations does not only enable the same in ensuring the internal controls but

also enables an organization in examining the rate of residual risks with the objective of avoiding

ML/TF13. On the contrary, the AML program would enable the organizations in making the

higher management aware of the different risks that might be encountered by the organization

and the method that is applied for control gaps and remediation efforts might be placed. It has

been noted that the AML program would enable the banking organizations in evaluating the

background of the customers while making business.

The loan providing department of the banks often face risks related to the insolvencies,

claimed by the business owners whom the bank provides loans, resulting to huge financial losses.

On the other hand, the different aspects of money laundering through inefficient wealth

management systems affected the rate of operations of the bank while operating in the diverse

global economies. Therefore, the different business units of the bank must initiate steps to

13 Spicer, Jane. "AUSTRAC and the financial sector-partners in crime prevention: A look into

AUSTRAC's money laundering/terrorism financing risk assessments." Journal of the Australian

Institute of Professional Intelligence Officers 26, no. 3 (2018): 3.

the organizations in enabling informed decisions while implementing control efforts, allocation

of the resources and technological infusions. The assessment of the nature of the ML/TF risks

and the method that is applied for the same might contribute to the organizational operations will

be influenced bythe effective functioning of the systems in orientation with the needs of the

venture.

While evaluating the literature it has been noted that most of the companies monitor and

implement strategies related to compliance as per the guidelines of the AML program. The

strategies of the organizations does not only enable the same in ensuring the internal controls but

also enables an organization in examining the rate of residual risks with the objective of avoiding

ML/TF13. On the contrary, the AML program would enable the organizations in making the

higher management aware of the different risks that might be encountered by the organization

and the method that is applied for control gaps and remediation efforts might be placed. It has

been noted that the AML program would enable the banking organizations in evaluating the

background of the customers while making business.

The loan providing department of the banks often face risks related to the insolvencies,

claimed by the business owners whom the bank provides loans, resulting to huge financial losses.

On the other hand, the different aspects of money laundering through inefficient wealth

management systems affected the rate of operations of the bank while operating in the diverse

global economies. Therefore, the different business units of the bank must initiate steps to

13 Spicer, Jane. "AUSTRAC and the financial sector-partners in crime prevention: A look into

AUSTRAC's money laundering/terrorism financing risk assessments." Journal of the Australian

Institute of Professional Intelligence Officers 26, no. 3 (2018): 3.

9AUSTRALIA

minimize the rate of uncertainties through suitable evaluation processes. The customer enable

department must ensure the trustworthiness of the customers while dealing with the same as per

the objective of reducing the ML risks. On the other hand, the loan providing and sanctioning

department must evaluate the rate of redemption from the business owners through auditing the

overall transactions that are undertaken by the same with the bank. In this relation, the AML

programs also enables the senior management in taking decisions for mitigating the issues

relating to the development of the operations and the method that is applied for the same might

be avoided.

The risk assessment and control mechanisms that are enumerated through the utilization

of AML programs would enable the organizations in improving the status reporting resulting to

minimization of fraudulent activities relating to money laundering. Again, it has been noticed

that the organizations undertaking the AML program efficiently reports to the compliance officer

with the objective of developing the operations of the same while operating in the diverse global

economies. It has been noted that the different risk management related operations that are

commenced by the organizations are influenced bythe effective understanding of the nature and

likelihood of the ML/TF risks14. The calculations of the risk occurrence and the impact of the

uncertainties on the organizational operations would enable the banking institution in improving

the rate of reporting with the objective of upholding the efficiency of the operations.

14 Mugarura, Norman. "Customer due diligence (CDD) mandate and the propensity of its

application as a global AML paradigm." Journal of Money Laundering Control 17, no. 1 (2014):

76-95.

minimize the rate of uncertainties through suitable evaluation processes. The customer enable

department must ensure the trustworthiness of the customers while dealing with the same as per

the objective of reducing the ML risks. On the other hand, the loan providing and sanctioning

department must evaluate the rate of redemption from the business owners through auditing the

overall transactions that are undertaken by the same with the bank. In this relation, the AML

programs also enables the senior management in taking decisions for mitigating the issues

relating to the development of the operations and the method that is applied for the same might

be avoided.

The risk assessment and control mechanisms that are enumerated through the utilization

of AML programs would enable the organizations in improving the status reporting resulting to

minimization of fraudulent activities relating to money laundering. Again, it has been noticed

that the organizations undertaking the AML program efficiently reports to the compliance officer

with the objective of developing the operations of the same while operating in the diverse global

economies. It has been noted that the different risk management related operations that are

commenced by the organizations are influenced bythe effective understanding of the nature and

likelihood of the ML/TF risks14. The calculations of the risk occurrence and the impact of the

uncertainties on the organizational operations would enable the banking institution in improving

the rate of reporting with the objective of upholding the efficiency of the operations.

14 Mugarura, Norman. "Customer due diligence (CDD) mandate and the propensity of its

application as a global AML paradigm." Journal of Money Laundering Control 17, no. 1 (2014):

76-95.

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

10AUSTRALIA

Part c

The different risks that are encountered by the banks has affected the rate of return and the

loyalty of the customers. On the contrary, the occurrence of the AML/CTF risks might taint the

brand image of the banking organization. The assessment of the business risks is the initial step

that might be commenced by a bank, which would assist in evaluating uncertainties relating to

customer, product, delivery and jurisdiction.

Part c

The different risks that are encountered by the banks has affected the rate of return and the

loyalty of the customers. On the contrary, the occurrence of the AML/CTF risks might taint the

brand image of the banking organization. The assessment of the business risks is the initial step

that might be commenced by a bank, which would assist in evaluating uncertainties relating to

customer, product, delivery and jurisdiction.

11AUSTRALIA

Customer risk

Identification of the type of the customers and examining the rate of risk that might be

encountered through the same assist organizations in strengthening the compliance mechanisms.

In this relation, the banking organization might take steps to segregate the customers into low,

medium and high risk bucket with the objective of evaluating the uncertainty that is posed by the

same15. On the contrary, the KYC verification of the customers would also enable the bank in

segregating the customers to the different buckets. The segregation of the customers would

enable the banking organization in evaluating the customers individually and marking them on

the level of uncertainty they might pose to the venture. On the contrary, reviewing the KYC that

are submitted by the customers would enable an organization in gaining knowledge on the

background of the customers, assisting the venture in their segregation process. Therefore, the

identification of the customers and segregating the same in orientation with the impact posed by

the same would enable the bank in preventing ML/TF related risks.

Product risk

As for the risks related to the product offerings of the banks, like exchange, organizations

must take steps to compile the product offering and report to AUSTRAC for checking the

vulnerability towards ML/TF threats. The examination of the compliance actions and the

regulatory bindings that are imposed by the AUSTRAC, the concerned bank would identify the

products that are more vulnerable to the ML/TF. On the contrary, the organization might also

15 Valkanov, N., 2019. Smart Compliance or How New Technologies Change Customer

Identification Mechanisms in Banking. Economics and computer science, (2), pp.12-19.

Customer risk

Identification of the type of the customers and examining the rate of risk that might be

encountered through the same assist organizations in strengthening the compliance mechanisms.

In this relation, the banking organization might take steps to segregate the customers into low,

medium and high risk bucket with the objective of evaluating the uncertainty that is posed by the

same15. On the contrary, the KYC verification of the customers would also enable the bank in

segregating the customers to the different buckets. The segregation of the customers would

enable the banking organization in evaluating the customers individually and marking them on

the level of uncertainty they might pose to the venture. On the contrary, reviewing the KYC that

are submitted by the customers would enable an organization in gaining knowledge on the

background of the customers, assisting the venture in their segregation process. Therefore, the

identification of the customers and segregating the same in orientation with the impact posed by

the same would enable the bank in preventing ML/TF related risks.

Product risk

As for the risks related to the product offerings of the banks, like exchange, organizations

must take steps to compile the product offering and report to AUSTRAC for checking the

vulnerability towards ML/TF threats. The examination of the compliance actions and the

regulatory bindings that are imposed by the AUSTRAC, the concerned bank would identify the

products that are more vulnerable to the ML/TF. On the contrary, the organization might also

15 Valkanov, N., 2019. Smart Compliance or How New Technologies Change Customer

Identification Mechanisms in Banking. Economics and computer science, (2), pp.12-19.

12AUSTRALIA

undertake steps to initiate PEP and Sanctions for the customers with the objective of regulating

the flow of vulnerable products16.

Delivery risk

The delivery risk is associated with the delivery of the products or services that are

prepared by the banks. In this relation, the OTC (Over the Counter) transactions are safer than

through the digital platforms. Therefore, in this relation, the bank must take steps to enhance the

rate of security of the digital software through which the transactions are processed with the

objective of minimizing the chances of ML/TF risks. Therefore, the identification and

compliance formation strategies would enable the organization in preventing and resolving the

risk factors due to ML/TF.

Jurisdiction risk

The jurisdiction risk is characterized by the lack of transparency in the operations and the

shortfalls in the AML/CTF framework. Therefore, the organization must take steps to enhance

the rate of reporting with the objective of monitoring and controlling the activities. On the

contrary, the bank might take steps to encourage the regulatory bodies to review the policies and

procedures that are undertaken by the banks and thereby identify the vulnerable aspects that

might compromise on the safety concerns17.

16 Stanley, Rebecca L., and Ross P. Buckley. "Protecting the west, excluding the rest: The impact

of the AML/CTF regime on financial inclusion in the pacific and potential responses." Melb. J.

Int'l L. 17 (2016): 83.

17 Sadiq, Shazia, and Guido Governatori. "Managing regulatory compliance in business

processes." In Handbook on Business Process Management 2, pp. 159-175. Springer, Berlin,

undertake steps to initiate PEP and Sanctions for the customers with the objective of regulating

the flow of vulnerable products16.

Delivery risk

The delivery risk is associated with the delivery of the products or services that are

prepared by the banks. In this relation, the OTC (Over the Counter) transactions are safer than

through the digital platforms. Therefore, in this relation, the bank must take steps to enhance the

rate of security of the digital software through which the transactions are processed with the

objective of minimizing the chances of ML/TF risks. Therefore, the identification and

compliance formation strategies would enable the organization in preventing and resolving the

risk factors due to ML/TF.

Jurisdiction risk

The jurisdiction risk is characterized by the lack of transparency in the operations and the

shortfalls in the AML/CTF framework. Therefore, the organization must take steps to enhance

the rate of reporting with the objective of monitoring and controlling the activities. On the

contrary, the bank might take steps to encourage the regulatory bodies to review the policies and

procedures that are undertaken by the banks and thereby identify the vulnerable aspects that

might compromise on the safety concerns17.

16 Stanley, Rebecca L., and Ross P. Buckley. "Protecting the west, excluding the rest: The impact

of the AML/CTF regime on financial inclusion in the pacific and potential responses." Melb. J.

Int'l L. 17 (2016): 83.

17 Sadiq, Shazia, and Guido Governatori. "Managing regulatory compliance in business

processes." In Handbook on Business Process Management 2, pp. 159-175. Springer, Berlin,

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

13AUSTRALIA

Part d

Risk: Defaulted payments of the borrowers

The different risks that are encountered by the organizations are relating on the lack of

effective status reporting and control mechanisms. In this relation, a large Australian retail bank

might face a risk relating to the defaulted payments of the borrowers. The risk is categorized

under credit risks with the objective of segregating the same from the other uncertainties. The

segregation of the risk would enable the venture in keeping a close eye on the likelihood and the

impact of the risk on the organizational operations. In most of the cases, it is noted that the

customers fail to pay the interests or the loan amount that was borrowed by the same. The

owners of the multinational organizations and the general customers take credits with the

objective of making suitable investments. However, many of the creditors fail to pay back the

principle amount along with the interests and proclaim themselves as insolvents, which affect the

capital based operations of the bank. Therefore, it might be stated that the ML categorized risk

might affect the internal processes as well as external accountabilities while operating in the

diverse global economies. In this relation, the organization must take steps to check the

background of the customers through the utilization of KYC and thereby refer to the regulations

and requirements of AUSTRAC.

The development of the organizational operations while relying on the regulations by the

AUSTRAC would enable the organization in evaluating the relevant policies that might be

Heidelberg, 2010.

Part d

Risk: Defaulted payments of the borrowers

The different risks that are encountered by the organizations are relating on the lack of

effective status reporting and control mechanisms. In this relation, a large Australian retail bank

might face a risk relating to the defaulted payments of the borrowers. The risk is categorized

under credit risks with the objective of segregating the same from the other uncertainties. The

segregation of the risk would enable the venture in keeping a close eye on the likelihood and the

impact of the risk on the organizational operations. In most of the cases, it is noted that the

customers fail to pay the interests or the loan amount that was borrowed by the same. The

owners of the multinational organizations and the general customers take credits with the

objective of making suitable investments. However, many of the creditors fail to pay back the

principle amount along with the interests and proclaim themselves as insolvents, which affect the

capital based operations of the bank. Therefore, it might be stated that the ML categorized risk

might affect the internal processes as well as external accountabilities while operating in the

diverse global economies. In this relation, the organization must take steps to check the

background of the customers through the utilization of KYC and thereby refer to the regulations

and requirements of AUSTRAC.

The development of the organizational operations while relying on the regulations by the

AUSTRAC would enable the organization in evaluating the relevant policies that might be

Heidelberg, 2010.

14AUSTRALIA

considered by the same while providing loans to the customers18. On the contrary, the banks

might also review the AML program Part B which aims at evaluating and evaluating the

background of the customers before providing the same with the products and the services. In

this relation, the organization might take steps to identify the potential customers along with the

PEPs (Politically Engaged Persons) with the objective of assessing the net value of the assets and

the method that is applied for the loan amount might be procured after a default.

On the contrary, the organization might take steps to initiate continued reporting of the

status to the senior management with the objective of making the same aware of the situation for

empowering their activities and strategies. The organization might also take steps to train the

employees with the objective of making the same aware of the method that is applied for the

customers are to be evaluated and provided for loans19. The major aspects of changes in the

organizational operations are influenced bythe effective design of the AML compliances. The

different changes in the organizational operations will be influenced bythe effectiveness of the

status reporting. In this relation, KYC reporting and analysis of the due diligence of the

consumers would enable the venture in evaluating the likelihood of the credit risks. On the

contrary, reviewing the regulations and requirements of AUSTRAC would enable the

18 Mugarura, Norman. "Customer due diligence (CDD) mandate and the propensity of its

application as a global AML paradigm." Journal of Money Laundering Control 17, no. 1 (2014):

76-95.

19 Henning, Johan, and Mignon Hauman. "Fortifying a risk-based approach in the South African

AML/CFT process." Journal of Financial Crime 24, no. 4 (2017): 520-528.

considered by the same while providing loans to the customers18. On the contrary, the banks

might also review the AML program Part B which aims at evaluating and evaluating the

background of the customers before providing the same with the products and the services. In

this relation, the organization might take steps to identify the potential customers along with the

PEPs (Politically Engaged Persons) with the objective of assessing the net value of the assets and

the method that is applied for the loan amount might be procured after a default.

On the contrary, the organization might take steps to initiate continued reporting of the

status to the senior management with the objective of making the same aware of the situation for

empowering their activities and strategies. The organization might also take steps to train the

employees with the objective of making the same aware of the method that is applied for the

customers are to be evaluated and provided for loans19. The major aspects of changes in the

organizational operations are influenced bythe effective design of the AML compliances. The

different changes in the organizational operations will be influenced bythe effectiveness of the

status reporting. In this relation, KYC reporting and analysis of the due diligence of the

consumers would enable the venture in evaluating the likelihood of the credit risks. On the

contrary, reviewing the regulations and requirements of AUSTRAC would enable the

18 Mugarura, Norman. "Customer due diligence (CDD) mandate and the propensity of its

application as a global AML paradigm." Journal of Money Laundering Control 17, no. 1 (2014):

76-95.

19 Henning, Johan, and Mignon Hauman. "Fortifying a risk-based approach in the South African

AML/CFT process." Journal of Financial Crime 24, no. 4 (2017): 520-528.

15AUSTRALIA

organization in framing the compliance processes more effectively through the inclusion of a

compliance officer20. The assessment of the risks and the strategies that would be considered by

the banks would enable the same in minimizing the likelihood by offering products based on the

capacity of the customers. The evaluation of the KYC would also enable the organization in

evaluating the background of the customers while providing credit to the same.

Risk- Bribery and corruption among the employees

Bribery and corruption might affect the brand image of the banks while minimizing the

rate of satisfaction of the customers. In most of the cases, it has been noted that the bank

employees seek bribery for processing loans or superannuation which might affect the interests

of the customers. On the contrary, the bribes and corrupted practices might also result to

misstatement which might again affect the profitability of the bank along with the brand image.

Therefore, in this relation, the banks might take steps to follow the AML program Part A for

reviewing the operations of the employees and thereby analyzing the employee due diligence

with the objective of evaluating their motifs and intents21. On the contrary, the bank might also

follow the Anti-Bribery and Corruption Guidance along with the recommended policies of

20 Gelb, Alan. "Balancing Financial Integrity with Financial Inclusion: The Risk-Based Approach

to «Know Your Customer»." CGD Policy Paper 74 (2016): 1-24.

21 De Koker, Louis, and Mark Turkington. "Anti-money laundering measures and the

effectiveness question." In Research Handbook on International Financial Crime. Edward Elgar

Publishing, 2015.

organization in framing the compliance processes more effectively through the inclusion of a

compliance officer20. The assessment of the risks and the strategies that would be considered by

the banks would enable the same in minimizing the likelihood by offering products based on the

capacity of the customers. The evaluation of the KYC would also enable the organization in

evaluating the background of the customers while providing credit to the same.

Risk- Bribery and corruption among the employees

Bribery and corruption might affect the brand image of the banks while minimizing the

rate of satisfaction of the customers. In most of the cases, it has been noted that the bank

employees seek bribery for processing loans or superannuation which might affect the interests

of the customers. On the contrary, the bribes and corrupted practices might also result to

misstatement which might again affect the profitability of the bank along with the brand image.

Therefore, in this relation, the banks might take steps to follow the AML program Part A for

reviewing the operations of the employees and thereby analyzing the employee due diligence

with the objective of evaluating their motifs and intents21. On the contrary, the bank might also

follow the Anti-Bribery and Corruption Guidance along with the recommended policies of

20 Gelb, Alan. "Balancing Financial Integrity with Financial Inclusion: The Risk-Based Approach

to «Know Your Customer»." CGD Policy Paper 74 (2016): 1-24.

21 De Koker, Louis, and Mark Turkington. "Anti-money laundering measures and the

effectiveness question." In Research Handbook on International Financial Crime. Edward Elgar

Publishing, 2015.

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

16AUSTRALIA

AUSTRAC with the objective of ensuring the minimization of criminal activities related to

bribery and corruption among the employees.

The anticipation of the different activities that might be monitored and controlled while

developing the due diligence programs for evaluating the loyalty and dignity of the employees

towards the processes of the banks would enable in minimizing the rate of ML/TF risks. The

development of different monitoring and controlling operations would be enableing the ventures

in minimizing the rate of money laundering and bribery activities among the bank employees22.

The different changes that might be enforced by the organizations are significantly based on the

nature and criteria of risks. In this relation, the application of the AML/CTF contexts enabled the

organizations in improving the rate of operations while ensuring the minimization of risks related

to bribery.

The organization might take steps to develop a positive environment along with enhanced

reporting which would enable the banks in monitoring over the operations that are being

undertaken by the employees. On the contrary, the inclusion of penalty in case of convicts might

also enable the banks in minimizing the rate of corrupted practices among the workforce. The

bribery and corruption related activities of the banks might affect the rate of operations of the

same while operating in the diverse global economies. On the contrary, the application of

favorable policies sanctioned by the AUSTRAC would enable the bank in improving the rate of

22 Choo, Kim-Kwang Raymond. "Designated non-financial businesses and professionals: A

review and analysis of recent financial action task force on money laundering mutual evaluation

reports." Security Journal 27, no. 1 (2014): 1-26.

AUSTRAC with the objective of ensuring the minimization of criminal activities related to

bribery and corruption among the employees.

The anticipation of the different activities that might be monitored and controlled while

developing the due diligence programs for evaluating the loyalty and dignity of the employees

towards the processes of the banks would enable in minimizing the rate of ML/TF risks. The

development of different monitoring and controlling operations would be enableing the ventures

in minimizing the rate of money laundering and bribery activities among the bank employees22.

The different changes that might be enforced by the organizations are significantly based on the

nature and criteria of risks. In this relation, the application of the AML/CTF contexts enabled the

organizations in improving the rate of operations while ensuring the minimization of risks related

to bribery.

The organization might take steps to develop a positive environment along with enhanced

reporting which would enable the banks in monitoring over the operations that are being

undertaken by the employees. On the contrary, the inclusion of penalty in case of convicts might

also enable the banks in minimizing the rate of corrupted practices among the workforce. The

bribery and corruption related activities of the banks might affect the rate of operations of the

same while operating in the diverse global economies. On the contrary, the application of

favorable policies sanctioned by the AUSTRAC would enable the bank in improving the rate of

22 Choo, Kim-Kwang Raymond. "Designated non-financial businesses and professionals: A

review and analysis of recent financial action task force on money laundering mutual evaluation

reports." Security Journal 27, no. 1 (2014): 1-26.

17AUSTRALIA

operations while improving the process flow23. The development of different monitoring units

and the emergence of sustainable reporting standards would be enableing the organization in

improving the rate of operations in orientation with the needs of the customers24. References to

the policies imposed by AUSTRAC and the AML program Part A would enable the venture in

improving the rate of operations of the same while minimizing the rate of corruption among the

employees of the organization. Therefore, the improvements in the policies and procedures of the

banking organization through the inclusion of appropriate legislations would enable the same in

minimizing the rate of corrupted practices and money laundering.

References

Choo, Kim-Kwang Raymond. "Designated non-financial businesses and professionals: A review

and analysis of recent financial action task force on money laundering mutual evaluation

reports." Security Journal 27, no. 1 (2014): 1-26.

Choo, Kim-Kwang Raymond. "Cryptocurrency and virtual currency: Corruption and money

laundering/terrorism financing risks?." In Handbook of digital currency, pp. 283-307. Academic

Press, 2015.

23 Mills, Clinton. "Predictive analytics in fraud and AML." Journal of Financial Compliance 1,

no. 1 (2017): 17-26.

24 Fratangelo, Pierpaolo. "Prevention and countering of money laundering and terrorism

financing." In Italian Banking and Financial Law, pp. 105-130. Palgrave Macmillan, London,

2015.

operations while improving the process flow23. The development of different monitoring units

and the emergence of sustainable reporting standards would be enableing the organization in

improving the rate of operations in orientation with the needs of the customers24. References to

the policies imposed by AUSTRAC and the AML program Part A would enable the venture in

improving the rate of operations of the same while minimizing the rate of corruption among the

employees of the organization. Therefore, the improvements in the policies and procedures of the

banking organization through the inclusion of appropriate legislations would enable the same in

minimizing the rate of corrupted practices and money laundering.

References

Choo, Kim-Kwang Raymond. "Designated non-financial businesses and professionals: A review

and analysis of recent financial action task force on money laundering mutual evaluation

reports." Security Journal 27, no. 1 (2014): 1-26.

Choo, Kim-Kwang Raymond. "Cryptocurrency and virtual currency: Corruption and money

laundering/terrorism financing risks?." In Handbook of digital currency, pp. 283-307. Academic

Press, 2015.

23 Mills, Clinton. "Predictive analytics in fraud and AML." Journal of Financial Compliance 1,

no. 1 (2017): 17-26.

24 Fratangelo, Pierpaolo. "Prevention and countering of money laundering and terrorism

financing." In Italian Banking and Financial Law, pp. 105-130. Palgrave Macmillan, London,

2015.

18AUSTRALIA

De Koker, Louis, and Mark Turkington. "Anti-money laundering measures and the effectiveness

question." In Research Handbook on International Financial Crime. Edward Elgar Publishing,

2015.

De Koker, Louis. "Money laundering compliance—the challenges of technology." In Financial

Crimes: Psychological, Technological, and Ethical Issues, pp. 329-347. Springer, Cham, 2016.

Fratangelo, Pierpaolo. "Prevention and countering of money laundering and terrorism financing."

In Italian Banking and Financial Law, pp. 105-130. Palgrave Macmillan, London, 2015.

Gelb, Alan. "Balancing Financial Integrity with Financial Inclusion: The Risk-Based Approach

to «Know Your Customer»." CGD Policy Paper 74 (2016): 1-24.

Gurule, Jimmy. "Jimmy Gurule delivered the keynote address at the Korea Banking Risk

Dialogue 2014 in Seoul, South Korea on July 2." (2014).

Henning, Johan, and Mignon Hauman. "Fortifying a risk-based approach in the South African

AML/CFT process." Journal of Financial Crime 24, no. 4 (2017): 520-528.

Levi, Michael, Peter Reuter, and Terence Halliday. "Can the AML system be evaluated without

better data?." Crime, Law and Social Change 69, no. 2 (2018): 307-328.

Mills, Clinton. "Predictive analytics in fraud and AML." Journal of Financial Compliance 1, no.

1 (2017): 17-26.

Mugarura, Norman. "Customer due diligence (CDD) mandate and the propensity of its

application as a global AML paradigm." Journal of Money Laundering Control 17, no. 1 (2014):

76-95.

De Koker, Louis, and Mark Turkington. "Anti-money laundering measures and the effectiveness

question." In Research Handbook on International Financial Crime. Edward Elgar Publishing,

2015.

De Koker, Louis. "Money laundering compliance—the challenges of technology." In Financial

Crimes: Psychological, Technological, and Ethical Issues, pp. 329-347. Springer, Cham, 2016.

Fratangelo, Pierpaolo. "Prevention and countering of money laundering and terrorism financing."

In Italian Banking and Financial Law, pp. 105-130. Palgrave Macmillan, London, 2015.

Gelb, Alan. "Balancing Financial Integrity with Financial Inclusion: The Risk-Based Approach

to «Know Your Customer»." CGD Policy Paper 74 (2016): 1-24.

Gurule, Jimmy. "Jimmy Gurule delivered the keynote address at the Korea Banking Risk

Dialogue 2014 in Seoul, South Korea on July 2." (2014).

Henning, Johan, and Mignon Hauman. "Fortifying a risk-based approach in the South African

AML/CFT process." Journal of Financial Crime 24, no. 4 (2017): 520-528.

Levi, Michael, Peter Reuter, and Terence Halliday. "Can the AML system be evaluated without

better data?." Crime, Law and Social Change 69, no. 2 (2018): 307-328.

Mills, Clinton. "Predictive analytics in fraud and AML." Journal of Financial Compliance 1, no.

1 (2017): 17-26.

Mugarura, Norman. "Customer due diligence (CDD) mandate and the propensity of its

application as a global AML paradigm." Journal of Money Laundering Control 17, no. 1 (2014):

76-95.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

19AUSTRALIA

Sadiq, Shazia, and Guido Governatori. "Managing regulatory compliance in business processes."

In Handbook on Business Process Management 2, pp. 159-175. Springer, Berlin, Heidelberg,

2010.

Spicer, Jane. "AUSTRAC and the financial sector-partners in crime prevention: A look into

AUSTRAC's money laundering/terrorism financing risk assessments." Journal of the Australian

Institute of Professional Intelligence Officers 26, no. 3 (2018): 3.

Stanley, Rebecca L., and Ross P. Buckley. "Protecting the west, excluding the rest: The impact

of the AML/CTF regime on financial inclusion in the pacific and potential responses." Melb. J.

Int'l L. 17 (2016): 83.

Valkanov, N., 2019. Smart Compliance or How New Technologies Change Customer

Identification Mechanisms in Banking. Economics and computer science, (2), pp.12-19.

Sadiq, Shazia, and Guido Governatori. "Managing regulatory compliance in business processes."

In Handbook on Business Process Management 2, pp. 159-175. Springer, Berlin, Heidelberg,

2010.

Spicer, Jane. "AUSTRAC and the financial sector-partners in crime prevention: A look into

AUSTRAC's money laundering/terrorism financing risk assessments." Journal of the Australian

Institute of Professional Intelligence Officers 26, no. 3 (2018): 3.

Stanley, Rebecca L., and Ross P. Buckley. "Protecting the west, excluding the rest: The impact

of the AML/CTF regime on financial inclusion in the pacific and potential responses." Melb. J.

Int'l L. 17 (2016): 83.

Valkanov, N., 2019. Smart Compliance or How New Technologies Change Customer

Identification Mechanisms in Banking. Economics and computer science, (2), pp.12-19.

1 out of 20

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.