Tax Law Case Study Analysis

VerifiedAdded on 2020/04/01

|7

|1908

|417

AI Summary

This assignment delves into various tax law case studies, requiring students to analyze the legal principles at play in each scenario. It covers topics like capital gains tax, loss offsetting, tax evasion strategies, and the evolution of tax law interpretations. Students are expected to demonstrate their understanding of these concepts by applying them to specific cases and providing well-supported arguments.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Running Head: AUSTRALIA TAXATION LAW 1

Australia Taxation Law

<Student ID>

<Student Name>

<University Name>

Australia Taxation Law

<Student ID>

<Student Name>

<University Name>

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

AUSTRALIA TAXATION LAW 2

Contents

Question 1..................................................................................................................................3

Introduction............................................................................................................................3

Critical analysis......................................................................................................................3

Supporting evidence...............................................................................................................3

Conclusion..............................................................................................................................4

Question 2..................................................................................................................................4

Introduction............................................................................................................................4

Critical analysis......................................................................................................................4

Supporting evidence...............................................................................................................5

Conclusion..............................................................................................................................5

Question 3..................................................................................................................................5

Introduction:...........................................................................................................................5

Critical analysis:.....................................................................................................................6

Supporting evidence...............................................................................................................6

Conclusion..............................................................................................................................6

Question 4..................................................................................................................................6

Question 5..................................................................................................................................7

References..................................................................................................................................7

Contents

Question 1..................................................................................................................................3

Introduction............................................................................................................................3

Critical analysis......................................................................................................................3

Supporting evidence...............................................................................................................3

Conclusion..............................................................................................................................4

Question 2..................................................................................................................................4

Introduction............................................................................................................................4

Critical analysis......................................................................................................................4

Supporting evidence...............................................................................................................5

Conclusion..............................................................................................................................5

Question 3..................................................................................................................................5

Introduction:...........................................................................................................................5

Critical analysis:.....................................................................................................................6

Supporting evidence...............................................................................................................6

Conclusion..............................................................................................................................6

Question 4..................................................................................................................................6

Question 5..................................................................................................................................7

References..................................................................................................................................7

AUSTRALIA TAXATION LAW 3

Question 1

Introduction

The observation of the case of Eric depicts that he has acquired certain resources in the

course of the recent year. The concerns of taxability on capital gains can be applied in this

case on the basis of the offering cost of the asset being greater than the procurement cost. The

critical condition that can be apprehended in the case of Eric is that he is not liable to obtain

indexation benefits owing to the duration of holding the assets for less than a year.

Critical analysis

The resources purchased for individual utilization could be implicative of fulfilling the

personal objectives or recreation. The resources acquired for personal utilization do not

comprise of collectibles. It is mandatory to note that the assets which were procured at costs

under$10000 could be exempted from the capital gains tax (Boyle, 2015). In the case of Eric,

the resources procured for personal utilization refer to the incorporation of offers of a listed

company which are procured at $5000 and a home sound system which has a procurement

cost of $12000 (Wilson-Rogers, Morgan & Pinto, 2014).

Collectibles or individual resources are procured by individuals for accomplishing additional

targets including realization of self-efficacies. The concerns of applying capital gains tax to

the profits on sale of collectibles have to be addressed in case of Eric. Collectibles which are

purchased at costs lesser than or equivalent to $500 are exempted from the precedents of

capital gains tax. The collectibles which are acquired by Eric refer to an antique vase, a

painting and an antique chair at the procurement costs of $2000, $9000 and $3000

respectively (Wilson-Rogers, Morgan & Pinto, 2014).

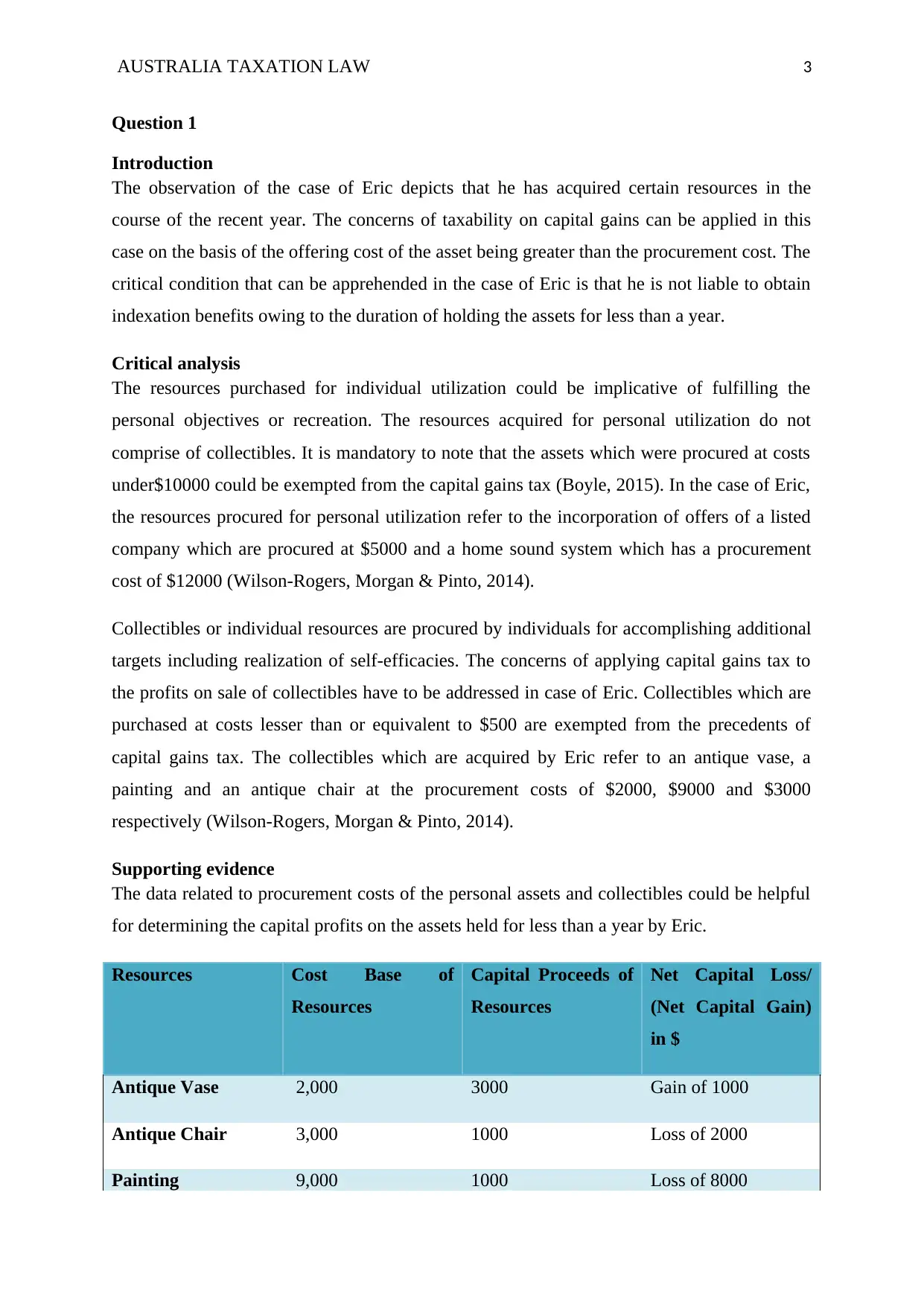

Supporting evidence

The data related to procurement costs of the personal assets and collectibles could be helpful

for determining the capital profits on the assets held for less than a year by Eric.

Resources Cost Base of

Resources

Capital Proceeds of

Resources

Net Capital Loss/

(Net Capital Gain)

in $

Antique Vase 2,000 3000 Gain of 1000

Antique Chair 3,000 1000 Loss of 2000

Painting 9,000 1000 Loss of 8000

Question 1

Introduction

The observation of the case of Eric depicts that he has acquired certain resources in the

course of the recent year. The concerns of taxability on capital gains can be applied in this

case on the basis of the offering cost of the asset being greater than the procurement cost. The

critical condition that can be apprehended in the case of Eric is that he is not liable to obtain

indexation benefits owing to the duration of holding the assets for less than a year.

Critical analysis

The resources purchased for individual utilization could be implicative of fulfilling the

personal objectives or recreation. The resources acquired for personal utilization do not

comprise of collectibles. It is mandatory to note that the assets which were procured at costs

under$10000 could be exempted from the capital gains tax (Boyle, 2015). In the case of Eric,

the resources procured for personal utilization refer to the incorporation of offers of a listed

company which are procured at $5000 and a home sound system which has a procurement

cost of $12000 (Wilson-Rogers, Morgan & Pinto, 2014).

Collectibles or individual resources are procured by individuals for accomplishing additional

targets including realization of self-efficacies. The concerns of applying capital gains tax to

the profits on sale of collectibles have to be addressed in case of Eric. Collectibles which are

purchased at costs lesser than or equivalent to $500 are exempted from the precedents of

capital gains tax. The collectibles which are acquired by Eric refer to an antique vase, a

painting and an antique chair at the procurement costs of $2000, $9000 and $3000

respectively (Wilson-Rogers, Morgan & Pinto, 2014).

Supporting evidence

The data related to procurement costs of the personal assets and collectibles could be helpful

for determining the capital profits on the assets held for less than a year by Eric.

Resources Cost Base of

Resources

Capital Proceeds of

Resources

Net Capital Loss/

(Net Capital Gain)

in $

Antique Vase 2,000 3000 Gain of 1000

Antique Chair 3,000 1000 Loss of 2000

Painting 9,000 1000 Loss of 8000

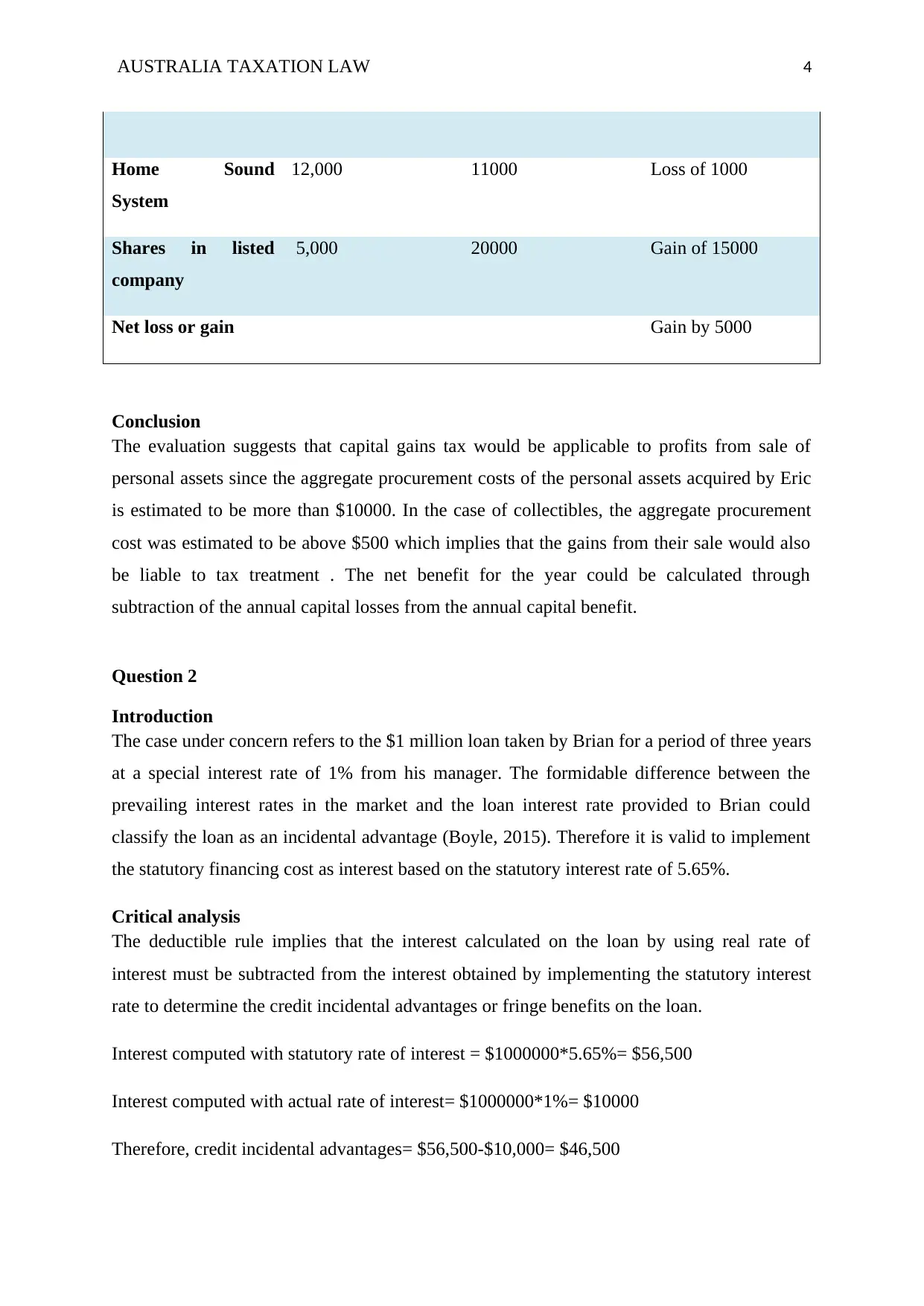

AUSTRALIA TAXATION LAW 4

Home Sound

System

12,000 11000 Loss of 1000

Shares in listed

company

5,000 20000 Gain of 15000

Net loss or gain Gain by 5000

Conclusion

The evaluation suggests that capital gains tax would be applicable to profits from sale of

personal assets since the aggregate procurement costs of the personal assets acquired by Eric

is estimated to be more than $10000. In the case of collectibles, the aggregate procurement

cost was estimated to be above $500 which implies that the gains from their sale would also

be liable to tax treatment . The net benefit for the year could be calculated through

subtraction of the annual capital losses from the annual capital benefit.

Question 2

Introduction

The case under concern refers to the $1 million loan taken by Brian for a period of three years

at a special interest rate of 1% from his manager. The formidable difference between the

prevailing interest rates in the market and the loan interest rate provided to Brian could

classify the loan as an incidental advantage (Boyle, 2015). Therefore it is valid to implement

the statutory financing cost as interest based on the statutory interest rate of 5.65%.

Critical analysis

The deductible rule implies that the interest calculated on the loan by using real rate of

interest must be subtracted from the interest obtained by implementing the statutory interest

rate to determine the credit incidental advantages or fringe benefits on the loan.

Interest computed with statutory rate of interest = $1000000*5.65%= $56,500

Interest computed with actual rate of interest= $1000000*1%= $10000

Therefore, credit incidental advantages= $56,500-$10,000= $46,500

Home Sound

System

12,000 11000 Loss of 1000

Shares in listed

company

5,000 20000 Gain of 15000

Net loss or gain Gain by 5000

Conclusion

The evaluation suggests that capital gains tax would be applicable to profits from sale of

personal assets since the aggregate procurement costs of the personal assets acquired by Eric

is estimated to be more than $10000. In the case of collectibles, the aggregate procurement

cost was estimated to be above $500 which implies that the gains from their sale would also

be liable to tax treatment . The net benefit for the year could be calculated through

subtraction of the annual capital losses from the annual capital benefit.

Question 2

Introduction

The case under concern refers to the $1 million loan taken by Brian for a period of three years

at a special interest rate of 1% from his manager. The formidable difference between the

prevailing interest rates in the market and the loan interest rate provided to Brian could

classify the loan as an incidental advantage (Boyle, 2015). Therefore it is valid to implement

the statutory financing cost as interest based on the statutory interest rate of 5.65%.

Critical analysis

The deductible rule implies that the interest calculated on the loan by using real rate of

interest must be subtracted from the interest obtained by implementing the statutory interest

rate to determine the credit incidental advantages or fringe benefits on the loan.

Interest computed with statutory rate of interest = $1000000*5.65%= $56,500

Interest computed with actual rate of interest= $1000000*1%= $10000

Therefore, credit incidental advantages= $56,500-$10,000= $46,500

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

AUSTRALIA TAXATION LAW 5

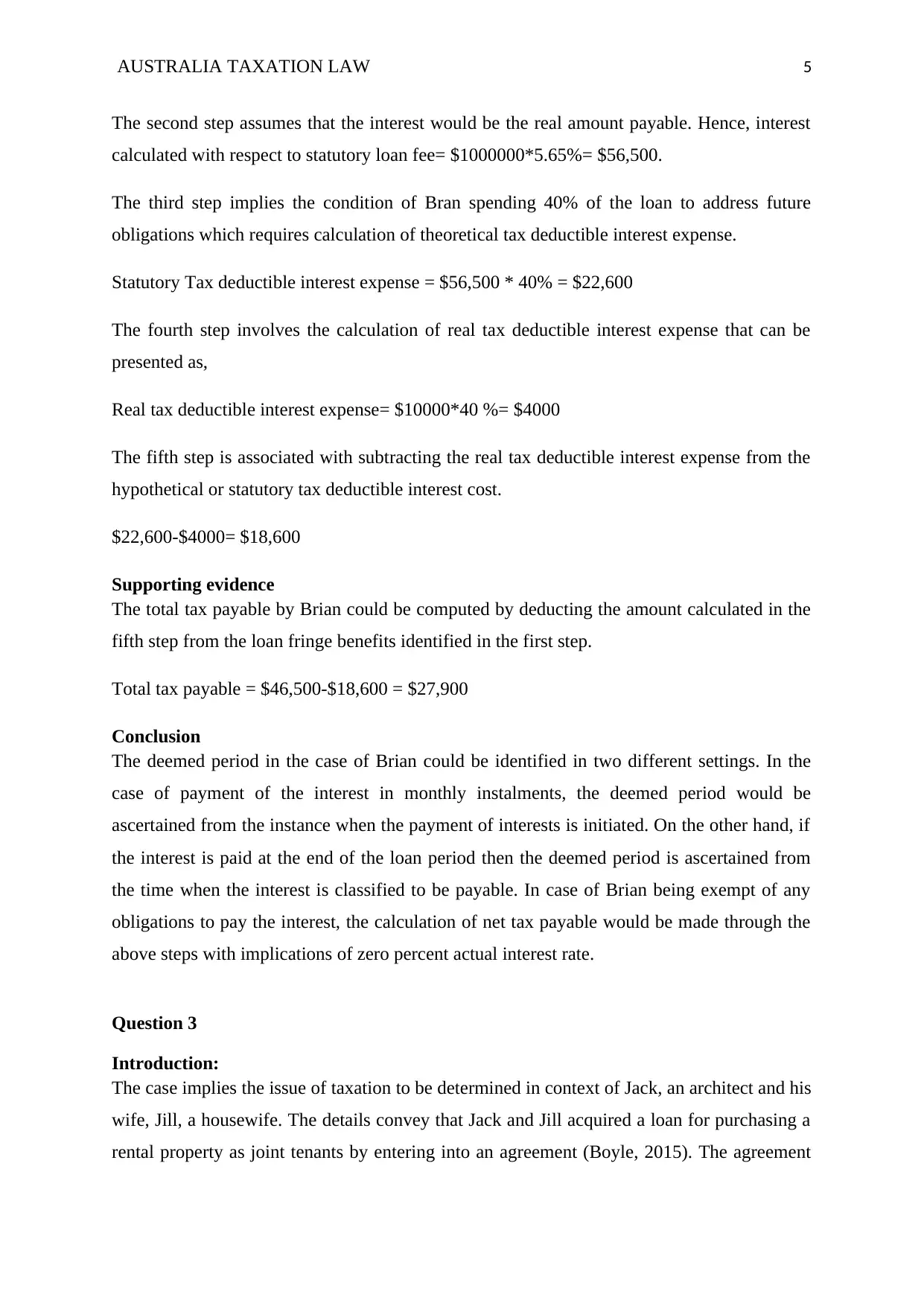

The second step assumes that the interest would be the real amount payable. Hence, interest

calculated with respect to statutory loan fee= $1000000*5.65%= $56,500.

The third step implies the condition of Bran spending 40% of the loan to address future

obligations which requires calculation of theoretical tax deductible interest expense.

Statutory Tax deductible interest expense = $56,500 * 40% = $22,600

The fourth step involves the calculation of real tax deductible interest expense that can be

presented as,

Real tax deductible interest expense= $10000*40 %= $4000

The fifth step is associated with subtracting the real tax deductible interest expense from the

hypothetical or statutory tax deductible interest cost.

$22,600-$4000= $18,600

Supporting evidence

The total tax payable by Brian could be computed by deducting the amount calculated in the

fifth step from the loan fringe benefits identified in the first step.

Total tax payable = $46,500-$18,600 = $27,900

Conclusion

The deemed period in the case of Brian could be identified in two different settings. In the

case of payment of the interest in monthly instalments, the deemed period would be

ascertained from the instance when the payment of interests is initiated. On the other hand, if

the interest is paid at the end of the loan period then the deemed period is ascertained from

the time when the interest is classified to be payable. In case of Brian being exempt of any

obligations to pay the interest, the calculation of net tax payable would be made through the

above steps with implications of zero percent actual interest rate.

Question 3

Introduction:

The case implies the issue of taxation to be determined in context of Jack, an architect and his

wife, Jill, a housewife. The details convey that Jack and Jill acquired a loan for purchasing a

rental property as joint tenants by entering into an agreement (Boyle, 2015). The agreement

The second step assumes that the interest would be the real amount payable. Hence, interest

calculated with respect to statutory loan fee= $1000000*5.65%= $56,500.

The third step implies the condition of Bran spending 40% of the loan to address future

obligations which requires calculation of theoretical tax deductible interest expense.

Statutory Tax deductible interest expense = $56,500 * 40% = $22,600

The fourth step involves the calculation of real tax deductible interest expense that can be

presented as,

Real tax deductible interest expense= $10000*40 %= $4000

The fifth step is associated with subtracting the real tax deductible interest expense from the

hypothetical or statutory tax deductible interest cost.

$22,600-$4000= $18,600

Supporting evidence

The total tax payable by Brian could be computed by deducting the amount calculated in the

fifth step from the loan fringe benefits identified in the first step.

Total tax payable = $46,500-$18,600 = $27,900

Conclusion

The deemed period in the case of Brian could be identified in two different settings. In the

case of payment of the interest in monthly instalments, the deemed period would be

ascertained from the instance when the payment of interests is initiated. On the other hand, if

the interest is paid at the end of the loan period then the deemed period is ascertained from

the time when the interest is classified to be payable. In case of Brian being exempt of any

obligations to pay the interest, the calculation of net tax payable would be made through the

above steps with implications of zero percent actual interest rate.

Question 3

Introduction:

The case implies the issue of taxation to be determined in context of Jack, an architect and his

wife, Jill, a housewife. The details convey that Jack and Jill acquired a loan for purchasing a

rental property as joint tenants by entering into an agreement (Boyle, 2015). The agreement

AUSTRALIA TAXATION LAW 6

absolved Jill of any responsibilities for losses incurred due to the property while allocating all

responsibilities on Jack. The precedents for distribution of profits could be observed in the

share of 10% for Jack and 90% of the profits for Jill. The property has incurred a loss of

$10000 last year and therefore it must be reviewed for the purpose of tax treatment with the

implications for the couple’s decision to sell the property.

Critical analysis:

The case reflects on the agreement of Jack and Jill in context of the purchase of the rental

property. The loss incurred by the property last year i.e. $10000 has to be attributed solely to

Jack who can choose to address this loss through inputs from his other sources of income or

selecting to carry forward the loss in his account statements to the next year (Wilson-Rogers,

Morgan & Pinto, 2014). On the other hand, if the property is able to generate profits then the

distribution won’t be affected due to the losses and would be divided among Jack and Jill in

the shares of 10% and 90%.

Supporting evidence

The opportunities for the sale of the property and the profits acquired from it could also help

Jack in addressing the loss of $10000. Therefore, Jill could not be accounted for any form of

tax treatment in context of this loss.

Conclusion

The above discussion related to the case conveys that Jack could be able to offset the losses

of last year with the profits acquired this year or through his other sources of income. In case

Jack could not be able to obtain profits in the present year, he has to bear the responsibility

for losses and ensure that they are reflected in accounts for tax treatment.

Question 4

The case of IRC v Duke of Westminster [1936] AC 1 is primarily related to the references to

tax evasion and the tax avoidance standoff (Boyle, 2015). This principle otherwise known as

the Westminster principle could be characterized by the provision of opportunities to

individuals and businesses for reducing tax liabilities. The major highlights that can be

inferred from the case include:

An individual could not be legally questioned regarding strategic measures for

reducing aggregate income.

The use of moral means provides exemption for questioning by authorities

absolved Jill of any responsibilities for losses incurred due to the property while allocating all

responsibilities on Jack. The precedents for distribution of profits could be observed in the

share of 10% for Jack and 90% of the profits for Jill. The property has incurred a loss of

$10000 last year and therefore it must be reviewed for the purpose of tax treatment with the

implications for the couple’s decision to sell the property.

Critical analysis:

The case reflects on the agreement of Jack and Jill in context of the purchase of the rental

property. The loss incurred by the property last year i.e. $10000 has to be attributed solely to

Jack who can choose to address this loss through inputs from his other sources of income or

selecting to carry forward the loss in his account statements to the next year (Wilson-Rogers,

Morgan & Pinto, 2014). On the other hand, if the property is able to generate profits then the

distribution won’t be affected due to the losses and would be divided among Jack and Jill in

the shares of 10% and 90%.

Supporting evidence

The opportunities for the sale of the property and the profits acquired from it could also help

Jack in addressing the loss of $10000. Therefore, Jill could not be accounted for any form of

tax treatment in context of this loss.

Conclusion

The above discussion related to the case conveys that Jack could be able to offset the losses

of last year with the profits acquired this year or through his other sources of income. In case

Jack could not be able to obtain profits in the present year, he has to bear the responsibility

for losses and ensure that they are reflected in accounts for tax treatment.

Question 4

The case of IRC v Duke of Westminster [1936] AC 1 is primarily related to the references to

tax evasion and the tax avoidance standoff (Boyle, 2015). This principle otherwise known as

the Westminster principle could be characterized by the provision of opportunities to

individuals and businesses for reducing tax liabilities. The major highlights that can be

inferred from the case include:

An individual could not be legally questioned regarding strategic measures for

reducing aggregate income.

The use of moral means provides exemption for questioning by authorities

AUSTRALIA TAXATION LAW 7

Legal means and strategies are necessary in the process of modifying aggregate

income to prevent action by authorities such as Commissioner of Inland Revenue.

However, the application of these precedents has been expanded with the introduction of new

laws according to contemporary case scenarios. The new case laws refer to the opportunities

for companies incurring losses to alter their financial records as well as discount their fixed

assets according to desired rates. It can also be observed that the laws exempt cases where the

means are applied for operational improvement in the organization.

Question 5

The case of Bill has to be reviewed in context of capital gains tax on the income obtained by

him from a logging company. Bill hired the services of the logging company to clear off his

large piece of land filled with pine trees (Boyle, 2015). The concerns for applying capital

gains tax on the income obtained from the logging company could be reviewed from the

different nature of receipts. In the case of capital receipts, the logging company provides a

one-time payment of $50000 for clearing off the entire piece of land. This income or capital

receipt is characterized by providing rights to another party, time required for regrowth of the

trees and the lump sum nature of the payment (Wilson-Rogers, Morgan & Pinto, 2014).

Therefore the income could be subject to capital gains tax in this scenario. On the other hand,

if Brian receives payment from the logging company in instalments of $1000 for every 100

meters of land cleared then it would be categorized as recurring deposits thereby implying

exemption from capital gains tax. However, Bill would be liable to pay taxes on the income

in recurring receipts based in the actual tax rates.

References

Boyle, L. (2015). An Australian August Corpus: Why There is Only One Common Law in

Australia. Bond Law Review, 27(1), 3.

Wilson-Rogers, N., Morgan, A., & Pinto, D. (2014). The primacy of client privilege:

designing a statutory tax advice privilege for accredited non-lawyer tax advisors.

Legal means and strategies are necessary in the process of modifying aggregate

income to prevent action by authorities such as Commissioner of Inland Revenue.

However, the application of these precedents has been expanded with the introduction of new

laws according to contemporary case scenarios. The new case laws refer to the opportunities

for companies incurring losses to alter their financial records as well as discount their fixed

assets according to desired rates. It can also be observed that the laws exempt cases where the

means are applied for operational improvement in the organization.

Question 5

The case of Bill has to be reviewed in context of capital gains tax on the income obtained by

him from a logging company. Bill hired the services of the logging company to clear off his

large piece of land filled with pine trees (Boyle, 2015). The concerns for applying capital

gains tax on the income obtained from the logging company could be reviewed from the

different nature of receipts. In the case of capital receipts, the logging company provides a

one-time payment of $50000 for clearing off the entire piece of land. This income or capital

receipt is characterized by providing rights to another party, time required for regrowth of the

trees and the lump sum nature of the payment (Wilson-Rogers, Morgan & Pinto, 2014).

Therefore the income could be subject to capital gains tax in this scenario. On the other hand,

if Brian receives payment from the logging company in instalments of $1000 for every 100

meters of land cleared then it would be categorized as recurring deposits thereby implying

exemption from capital gains tax. However, Bill would be liable to pay taxes on the income

in recurring receipts based in the actual tax rates.

References

Boyle, L. (2015). An Australian August Corpus: Why There is Only One Common Law in

Australia. Bond Law Review, 27(1), 3.

Wilson-Rogers, N., Morgan, A., & Pinto, D. (2014). The primacy of client privilege:

designing a statutory tax advice privilege for accredited non-lawyer tax advisors.

1 out of 7

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.