ARBE2307 Economics of Construction Industry: Performance Analysis

VerifiedAdded on 2023/06/08

|19

|4484

|260

Report

AI Summary

This report provides a comprehensive analysis of the performance of Australia's construction industry. It begins with an overview of key economic indicators, including real GDP, GDP growth rate, and inflation, examining their trends over a five-year period. The report then delves into the fiscal and monetary policies that have shaped the industry's performance, highlighting their impact on economic stability and growth. A significant portion of the report is dedicated to a detailed examination of the construction industry itself, breaking it down into its major sectors: engineering construction, non-residential buildings, and residential buildings. Each sector's performance, growth drivers, and future prospects are analyzed, supported by data and forecasts. The report concludes with a summary of the key findings and insights into the current state and future outlook of the Australian construction industry, offering a valuable resource for students studying economics and related fields.

Running head: PERFORMANCE OF AUSTRALIA’S CONSTRUCTION INDUSTRY

Performance of Australia’s Construction Industry

Name of the Student

Name of the University

Author Note

Performance of Australia’s Construction Industry

Name of the Student

Name of the University

Author Note

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1PERFORMANCE OF AUSTRALIA’S CONSTRUCTION INDUSTRY

Table of Contents

Table of Contents.............................................................................................................................1

Introduction..................................................................................................................................2

Discussion....................................................................................................................................2

Production Analysis.................................................................................................................2

Price Level Analysis................................................................................................................4

Fiscal Policy.............................................................................................................................6

Monetary Policy.......................................................................................................................6

Construction Industry Analysis...............................................................................................6

Conclusion.................................................................................................................................11

Part 2..............................................................................................................................................12

Introduction................................................................................................................................12

Analysis of the Engineering Construction Sector......................................................................12

Government Measures...............................................................................................................14

Conclusion.................................................................................................................................14

Table of Contents

Table of Contents.............................................................................................................................1

Introduction..................................................................................................................................2

Discussion....................................................................................................................................2

Production Analysis.................................................................................................................2

Price Level Analysis................................................................................................................4

Fiscal Policy.............................................................................................................................6

Monetary Policy.......................................................................................................................6

Construction Industry Analysis...............................................................................................6

Conclusion.................................................................................................................................11

Part 2..............................................................................................................................................12

Introduction................................................................................................................................12

Analysis of the Engineering Construction Sector......................................................................12

Government Measures...............................................................................................................14

Conclusion.................................................................................................................................14

2PERFORMANCE OF AUSTRALIA’S CONSTRUCTION INDUSTRY

Part 1

Introduction

The economy of Australia has been growing over the years and has been performing well

consistently in comparison to the other OECD countries. In 2017, as per the IMF (International

Monetary Fund) data, the rate of inflation in Australia had been around 1.9% in 2017. The

unemployment rate as on 2017 was low at 5.6% and is expected to further fall as predicted by the

ABS or Australian Bureau of Statistics. This part of the report analyses a few of the economic

indicators of Australia and checks its economic performance for the last five years and the

performance of the different sectors of the construction industry. The indicators selected are the

real GDP, the growth rate of real GDP and the inflation rate. Further analysis of the construction

industry and its different sectors is carried out in details. The monetary and fiscal policies

undertaken over the past five years have also been studied in the following sections of this

report.

Discussion

Production Analysis

Real GDP

Real GDP or real gross domestic product takes into account the final value of goods and

services that is produced by a given country, in a given year, within its geographical territory of

that country. Real GDP is an inflation-adjusted measure, which is expressed with respect to a

given year which is kept constant and is called a base year. By keeping the base year constant,

the changes that take place in the price level of the economy can be traced and this will help in

providing a more accurate reflection of a country’s economic growth. To analyze the purchasing

power and level of growth of an economy governments often use this measure. The graph shows

Part 1

Introduction

The economy of Australia has been growing over the years and has been performing well

consistently in comparison to the other OECD countries. In 2017, as per the IMF (International

Monetary Fund) data, the rate of inflation in Australia had been around 1.9% in 2017. The

unemployment rate as on 2017 was low at 5.6% and is expected to further fall as predicted by the

ABS or Australian Bureau of Statistics. This part of the report analyses a few of the economic

indicators of Australia and checks its economic performance for the last five years and the

performance of the different sectors of the construction industry. The indicators selected are the

real GDP, the growth rate of real GDP and the inflation rate. Further analysis of the construction

industry and its different sectors is carried out in details. The monetary and fiscal policies

undertaken over the past five years have also been studied in the following sections of this

report.

Discussion

Production Analysis

Real GDP

Real GDP or real gross domestic product takes into account the final value of goods and

services that is produced by a given country, in a given year, within its geographical territory of

that country. Real GDP is an inflation-adjusted measure, which is expressed with respect to a

given year which is kept constant and is called a base year. By keeping the base year constant,

the changes that take place in the price level of the economy can be traced and this will help in

providing a more accurate reflection of a country’s economic growth. To analyze the purchasing

power and level of growth of an economy governments often use this measure. The graph shows

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3PERFORMANCE OF AUSTRALIA’S CONSTRUCTION INDUSTRY

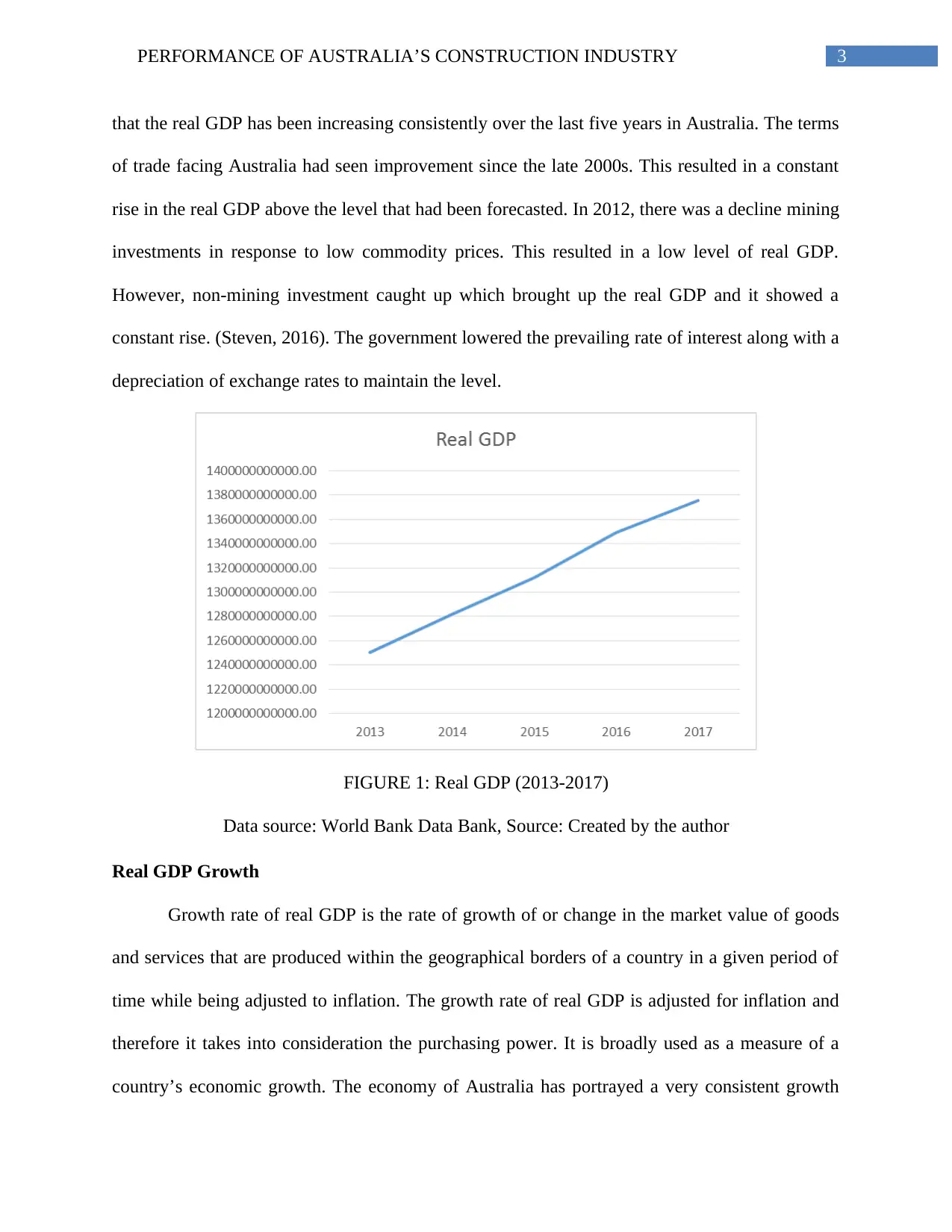

that the real GDP has been increasing consistently over the last five years in Australia. The terms

of trade facing Australia had seen improvement since the late 2000s. This resulted in a constant

rise in the real GDP above the level that had been forecasted. In 2012, there was a decline mining

investments in response to low commodity prices. This resulted in a low level of real GDP.

However, non-mining investment caught up which brought up the real GDP and it showed a

constant rise. (Steven, 2016). The government lowered the prevailing rate of interest along with a

depreciation of exchange rates to maintain the level.

FIGURE 1: Real GDP (2013-2017)

Data source: World Bank Data Bank, Source: Created by the author

Real GDP Growth

Growth rate of real GDP is the rate of growth of or change in the market value of goods

and services that are produced within the geographical borders of a country in a given period of

time while being adjusted to inflation. The growth rate of real GDP is adjusted for inflation and

therefore it takes into consideration the purchasing power. It is broadly used as a measure of a

country’s economic growth. The economy of Australia has portrayed a very consistent growth

that the real GDP has been increasing consistently over the last five years in Australia. The terms

of trade facing Australia had seen improvement since the late 2000s. This resulted in a constant

rise in the real GDP above the level that had been forecasted. In 2012, there was a decline mining

investments in response to low commodity prices. This resulted in a low level of real GDP.

However, non-mining investment caught up which brought up the real GDP and it showed a

constant rise. (Steven, 2016). The government lowered the prevailing rate of interest along with a

depreciation of exchange rates to maintain the level.

FIGURE 1: Real GDP (2013-2017)

Data source: World Bank Data Bank, Source: Created by the author

Real GDP Growth

Growth rate of real GDP is the rate of growth of or change in the market value of goods

and services that are produced within the geographical borders of a country in a given period of

time while being adjusted to inflation. The growth rate of real GDP is adjusted for inflation and

therefore it takes into consideration the purchasing power. It is broadly used as a measure of a

country’s economic growth. The economy of Australia has portrayed a very consistent growth

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4PERFORMANCE OF AUSTRALIA’S CONSTRUCTION INDUSTRY

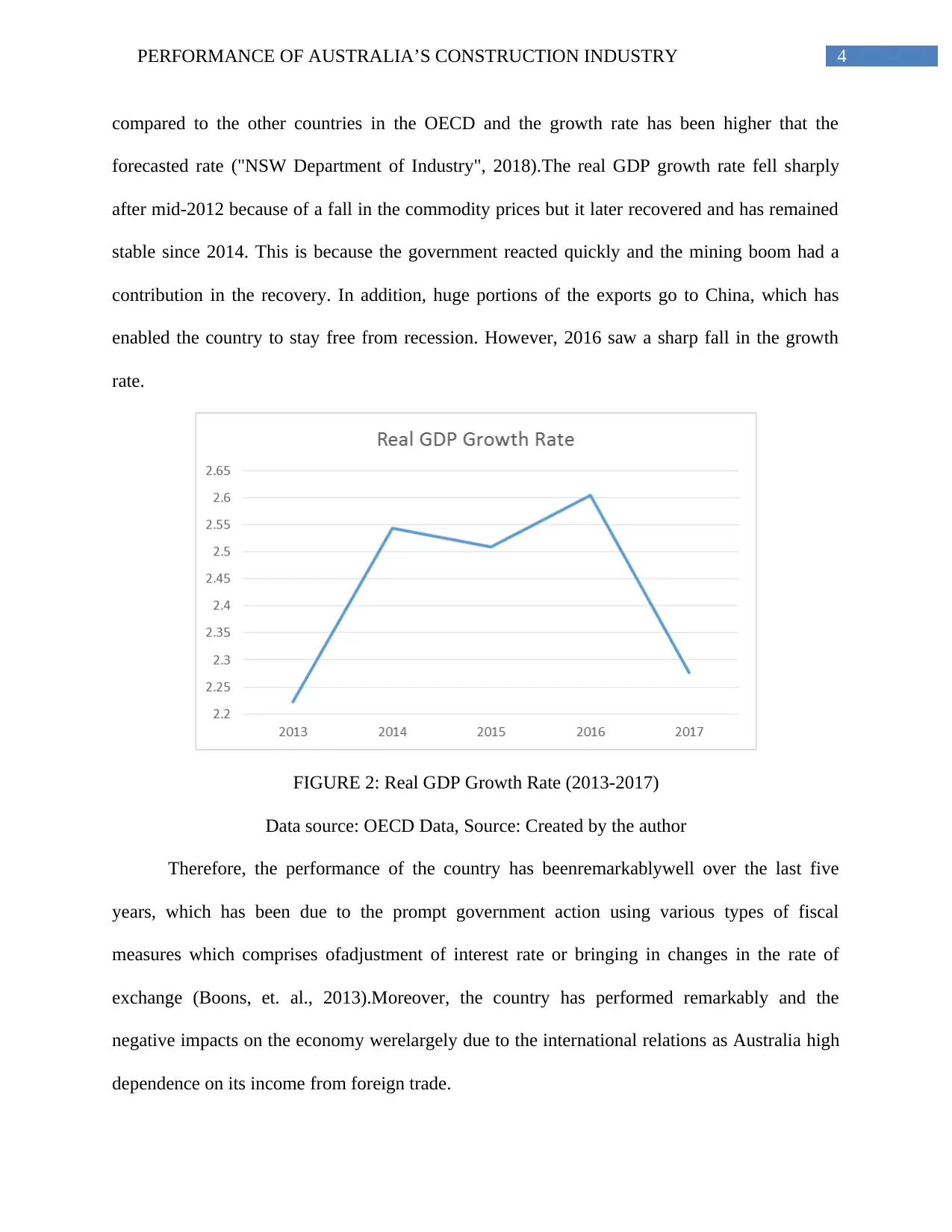

compared to the other countries in the OECD and the growth rate has been higher that the

forecasted rate ("NSW Department of Industry", 2018).The real GDP growth rate fell sharply

after mid-2012 because of a fall in the commodity prices but it later recovered and has remained

stable since 2014. This is because the government reacted quickly and the mining boom had a

contribution in the recovery. In addition, huge portions of the exports go to China, which has

enabled the country to stay free from recession. However, 2016 saw a sharp fall in the growth

rate.

FIGURE 2: Real GDP Growth Rate (2013-2017)

Data source: OECD Data, Source: Created by the author

Therefore, the performance of the country has beenremarkablywell over the last five

years, which has been due to the prompt government action using various types of fiscal

measures which comprises ofadjustment of interest rate or bringing in changes in the rate of

exchange (Boons, et. al., 2013).Moreover, the country has performed remarkably and the

negative impacts on the economy werelargely due to the international relations as Australia high

dependence on its income from foreign trade.

compared to the other countries in the OECD and the growth rate has been higher that the

forecasted rate ("NSW Department of Industry", 2018).The real GDP growth rate fell sharply

after mid-2012 because of a fall in the commodity prices but it later recovered and has remained

stable since 2014. This is because the government reacted quickly and the mining boom had a

contribution in the recovery. In addition, huge portions of the exports go to China, which has

enabled the country to stay free from recession. However, 2016 saw a sharp fall in the growth

rate.

FIGURE 2: Real GDP Growth Rate (2013-2017)

Data source: OECD Data, Source: Created by the author

Therefore, the performance of the country has beenremarkablywell over the last five

years, which has been due to the prompt government action using various types of fiscal

measures which comprises ofadjustment of interest rate or bringing in changes in the rate of

exchange (Boons, et. al., 2013).Moreover, the country has performed remarkably and the

negative impacts on the economy werelargely due to the international relations as Australia high

dependence on its income from foreign trade.

5PERFORMANCE OF AUSTRALIA’S CONSTRUCTION INDUSTRY

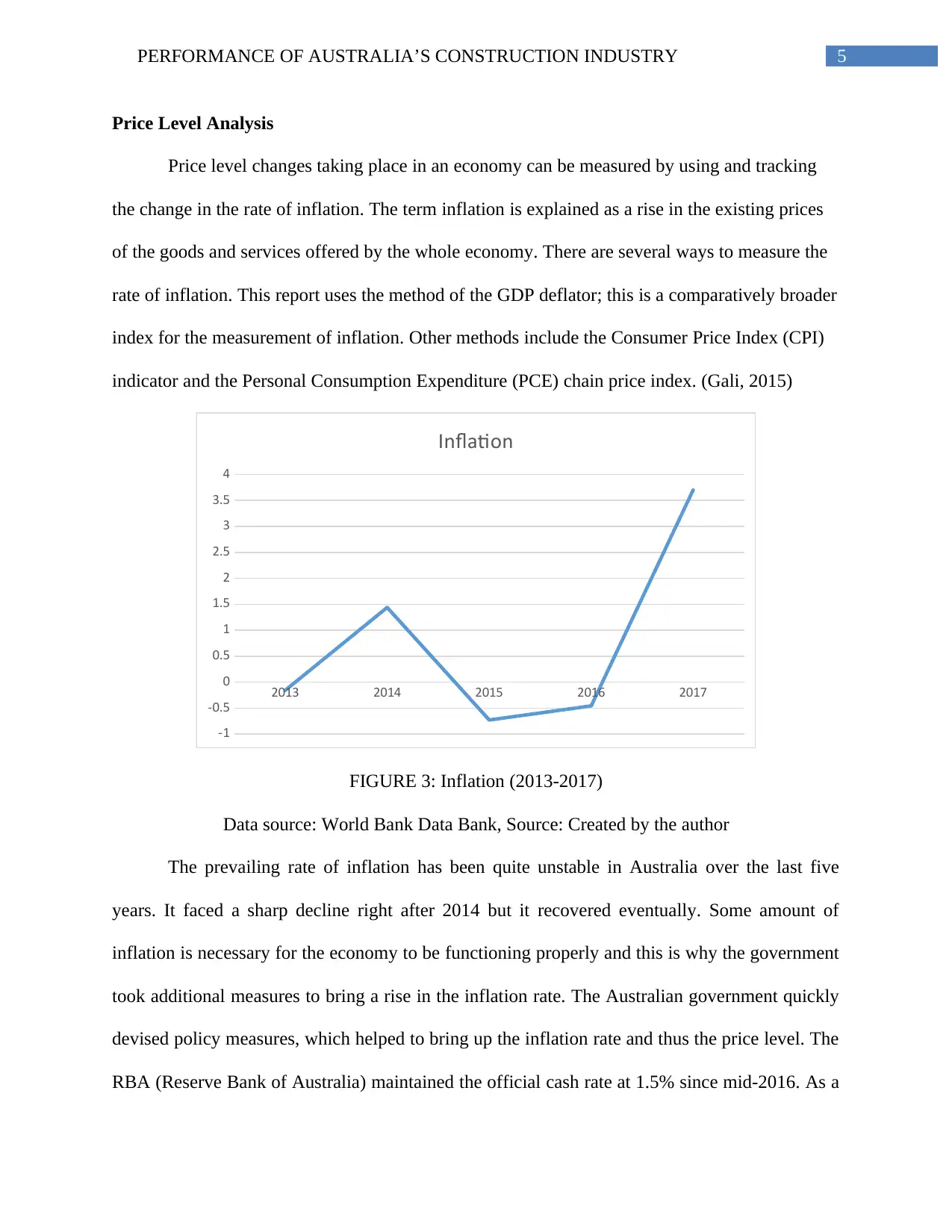

Price Level Analysis

Price level changes taking place in an economy can be measured by using and tracking

the change in the rate of inflation. The term inflation is explained as a rise in the existing prices

of the goods and services offered by the whole economy. There are several ways to measure the

rate of inflation. This report uses the method of the GDP deflator; this is a comparatively broader

index for the measurement of inflation. Other methods include the Consumer Price Index (CPI)

indicator and the Personal Consumption Expenditure (PCE) chain price index. (Gali, 2015)

2013 2014 2015 2016 2017

-1

-0.5

0

0.5

1

1.5

2

2.5

3

3.5

4

Inflation

FIGURE 3: Inflation (2013-2017)

Data source: World Bank Data Bank, Source: Created by the author

The prevailing rate of inflation has been quite unstable in Australia over the last five

years. It faced a sharp decline right after 2014 but it recovered eventually. Some amount of

inflation is necessary for the economy to be functioning properly and this is why the government

took additional measures to bring a rise in the inflation rate. The Australian government quickly

devised policy measures, which helped to bring up the inflation rate and thus the price level. The

RBA (Reserve Bank of Australia) maintained the official cash rate at 1.5% since mid-2016. As a

Price Level Analysis

Price level changes taking place in an economy can be measured by using and tracking

the change in the rate of inflation. The term inflation is explained as a rise in the existing prices

of the goods and services offered by the whole economy. There are several ways to measure the

rate of inflation. This report uses the method of the GDP deflator; this is a comparatively broader

index for the measurement of inflation. Other methods include the Consumer Price Index (CPI)

indicator and the Personal Consumption Expenditure (PCE) chain price index. (Gali, 2015)

2013 2014 2015 2016 2017

-1

-0.5

0

0.5

1

1.5

2

2.5

3

3.5

4

Inflation

FIGURE 3: Inflation (2013-2017)

Data source: World Bank Data Bank, Source: Created by the author

The prevailing rate of inflation has been quite unstable in Australia over the last five

years. It faced a sharp decline right after 2014 but it recovered eventually. Some amount of

inflation is necessary for the economy to be functioning properly and this is why the government

took additional measures to bring a rise in the inflation rate. The Australian government quickly

devised policy measures, which helped to bring up the inflation rate and thus the price level. The

RBA (Reserve Bank of Australia) maintained the official cash rate at 1.5% since mid-2016. As a

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6PERFORMANCE OF AUSTRALIA’S CONSTRUCTION INDUSTRY

result, the CPI was as low as to 1.9%. The RBA cautioned that low inflation might exceed the

period that was previously forecast.

Fiscal Policy

Over the last five years, taxes in the Australian government was made to grow faster than

the growth in their GDP and this lead high increases in the revenue. The fiscal strategy of the

Australian government relies greatly on the optimism projections. Medium term fiscal objectives

will be undertaken to achieve balanced budget in different economic cycles (McCallum, et al.,

2015).

Monetary Policy

Over the past five years, the monetary policy decisions are made and expressed in terms

of the targeted cash rates. A cash rate is the overnight money market interest rate for overnight

loans. Over the past five years, the cash rate has been falling and this cash rate is decided upon

keeping the inflation rate in perspective the target rate of which has been 2-3 percent (Wilkins, &

Wooden, 2014). The determination of the monetary policy is done by the bank while making

sure that full employment, price stability, welfare and economic prosperity is maintained.

Construction Industry Analysis

According to economists from the American Institute of Architects (AIA), Associated

Builders and Contractors (ABC), and National Association of Home Builders (NAHB), the

future of the construction industry looks very promising where the engineering construction

sector has dominated the industry and accounts for over 10% of the GDP. The total value of the

industry was over $200 billion in 2012-2013 (Lehmann, et al., 2015). This industry has three

sectors:

result, the CPI was as low as to 1.9%. The RBA cautioned that low inflation might exceed the

period that was previously forecast.

Fiscal Policy

Over the last five years, taxes in the Australian government was made to grow faster than

the growth in their GDP and this lead high increases in the revenue. The fiscal strategy of the

Australian government relies greatly on the optimism projections. Medium term fiscal objectives

will be undertaken to achieve balanced budget in different economic cycles (McCallum, et al.,

2015).

Monetary Policy

Over the past five years, the monetary policy decisions are made and expressed in terms

of the targeted cash rates. A cash rate is the overnight money market interest rate for overnight

loans. Over the past five years, the cash rate has been falling and this cash rate is decided upon

keeping the inflation rate in perspective the target rate of which has been 2-3 percent (Wilkins, &

Wooden, 2014). The determination of the monetary policy is done by the bank while making

sure that full employment, price stability, welfare and economic prosperity is maintained.

Construction Industry Analysis

According to economists from the American Institute of Architects (AIA), Associated

Builders and Contractors (ABC), and National Association of Home Builders (NAHB), the

future of the construction industry looks very promising where the engineering construction

sector has dominated the industry and accounts for over 10% of the GDP. The total value of the

industry was over $200 billion in 2012-2013 (Lehmann, et al., 2015). This industry has three

sectors:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7PERFORMANCE OF AUSTRALIA’S CONSTRUCTION INDUSTRY

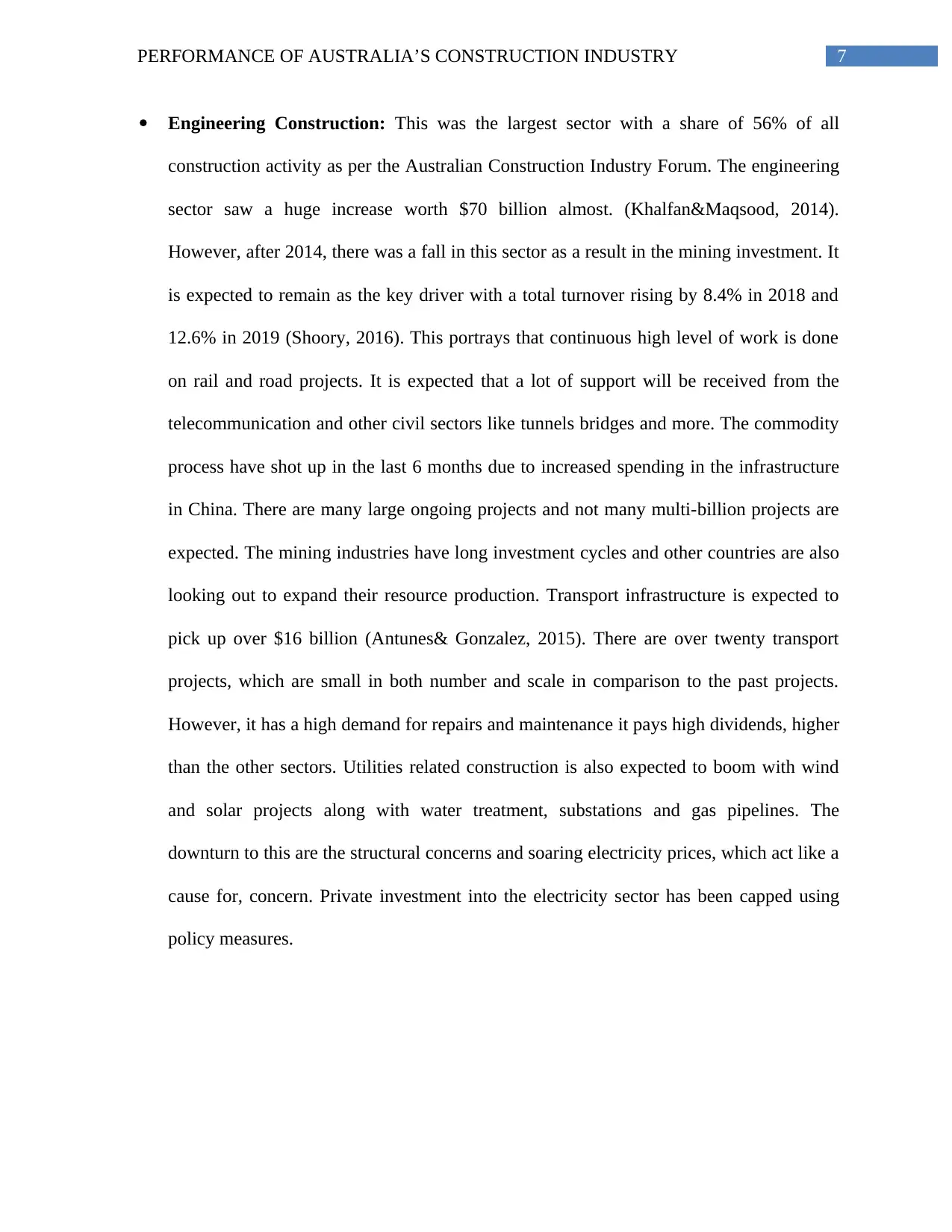

Engineering Construction: This was the largest sector with a share of 56% of all

construction activity as per the Australian Construction Industry Forum. The engineering

sector saw a huge increase worth $70 billion almost. (Khalfan&Maqsood, 2014).

However, after 2014, there was a fall in this sector as a result in the mining investment. It

is expected to remain as the key driver with a total turnover rising by 8.4% in 2018 and

12.6% in 2019 (Shoory, 2016). This portrays that continuous high level of work is done

on rail and road projects. It is expected that a lot of support will be received from the

telecommunication and other civil sectors like tunnels bridges and more. The commodity

process have shot up in the last 6 months due to increased spending in the infrastructure

in China. There are many large ongoing projects and not many multi-billion projects are

expected. The mining industries have long investment cycles and other countries are also

looking out to expand their resource production. Transport infrastructure is expected to

pick up over $16 billion (Antunes& Gonzalez, 2015). There are over twenty transport

projects, which are small in both number and scale in comparison to the past projects.

However, it has a high demand for repairs and maintenance it pays high dividends, higher

than the other sectors. Utilities related construction is also expected to boom with wind

and solar projects along with water treatment, substations and gas pipelines. The

downturn to this are the structural concerns and soaring electricity prices, which act like a

cause for, concern. Private investment into the electricity sector has been capped using

policy measures.

Engineering Construction: This was the largest sector with a share of 56% of all

construction activity as per the Australian Construction Industry Forum. The engineering

sector saw a huge increase worth $70 billion almost. (Khalfan&Maqsood, 2014).

However, after 2014, there was a fall in this sector as a result in the mining investment. It

is expected to remain as the key driver with a total turnover rising by 8.4% in 2018 and

12.6% in 2019 (Shoory, 2016). This portrays that continuous high level of work is done

on rail and road projects. It is expected that a lot of support will be received from the

telecommunication and other civil sectors like tunnels bridges and more. The commodity

process have shot up in the last 6 months due to increased spending in the infrastructure

in China. There are many large ongoing projects and not many multi-billion projects are

expected. The mining industries have long investment cycles and other countries are also

looking out to expand their resource production. Transport infrastructure is expected to

pick up over $16 billion (Antunes& Gonzalez, 2015). There are over twenty transport

projects, which are small in both number and scale in comparison to the past projects.

However, it has a high demand for repairs and maintenance it pays high dividends, higher

than the other sectors. Utilities related construction is also expected to boom with wind

and solar projects along with water treatment, substations and gas pipelines. The

downturn to this are the structural concerns and soaring electricity prices, which act like a

cause for, concern. Private investment into the electricity sector has been capped using

policy measures.

8PERFORMANCE OF AUSTRALIA’S CONSTRUCTION INDUSTRY

FIGURE 4: Transport Sector, (2010 – 2022)

Source: Australian Bureau of Statistics

Non-Residential Buildings: This sector expanded by around $2 billion mainly due to

large ongoing projects but the overall level of work has remained subdued in the recent

years combined with low investor sentiment and high degree of risk aversion weighing

down the sector. The mining boom has also played a role in the fall in the growth of the

sector. However, there are growth approval data from the ABS, which predict that the

non-residential sector will play a more prominent role. The value of work done is

forecasted is expected to grow by 14.6% to a value of approximately $42 billion out of

this $6.9 billion comes from construction related activities due to an influx of

international retailers into Australia (Zou, et al., 2013). Offices fall second in line with

$6.8 billion value and this increase is a function of increase in white-collar employment.

The tourism sector has also increased despite the strong Australian dollar rate and Asian

FIGURE 4: Transport Sector, (2010 – 2022)

Source: Australian Bureau of Statistics

Non-Residential Buildings: This sector expanded by around $2 billion mainly due to

large ongoing projects but the overall level of work has remained subdued in the recent

years combined with low investor sentiment and high degree of risk aversion weighing

down the sector. The mining boom has also played a role in the fall in the growth of the

sector. However, there are growth approval data from the ABS, which predict that the

non-residential sector will play a more prominent role. The value of work done is

forecasted is expected to grow by 14.6% to a value of approximately $42 billion out of

this $6.9 billion comes from construction related activities due to an influx of

international retailers into Australia (Zou, et al., 2013). Offices fall second in line with

$6.8 billion value and this increase is a function of increase in white-collar employment.

The tourism sector has also increased despite the strong Australian dollar rate and Asian

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9PERFORMANCE OF AUSTRALIA’S CONSTRUCTION INDUSTRY

tourists are the highest contributor. Asian investment is also high with over $4 billion

projects under construction. Out of the $11.7 billion, $9 billion has been allocated to

resort projects. In the education related construction, sector forecasts show 27.5% growth

with a value of $6.2 billion while the health sector has shown healthy growth whose

forecast shows a 17.9% growth (Loosemore, 2014).

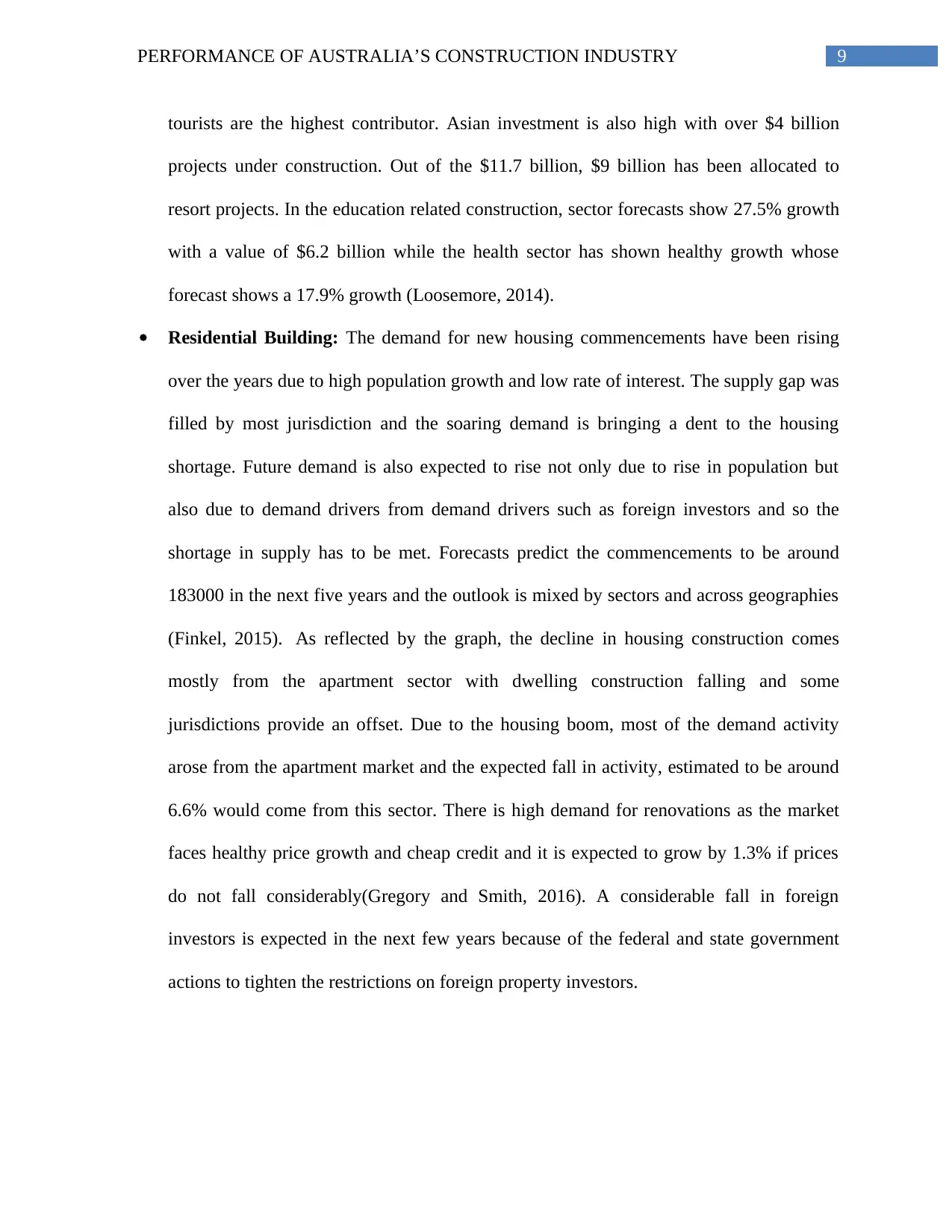

Residential Building: The demand for new housing commencements have been rising

over the years due to high population growth and low rate of interest. The supply gap was

filled by most jurisdiction and the soaring demand is bringing a dent to the housing

shortage. Future demand is also expected to rise not only due to rise in population but

also due to demand drivers from demand drivers such as foreign investors and so the

shortage in supply has to be met. Forecasts predict the commencements to be around

183000 in the next five years and the outlook is mixed by sectors and across geographies

(Finkel, 2015). As reflected by the graph, the decline in housing construction comes

mostly from the apartment sector with dwelling construction falling and some

jurisdictions provide an offset. Due to the housing boom, most of the demand activity

arose from the apartment market and the expected fall in activity, estimated to be around

6.6% would come from this sector. There is high demand for renovations as the market

faces healthy price growth and cheap credit and it is expected to grow by 1.3% if prices

do not fall considerably(Gregory and Smith, 2016). A considerable fall in foreign

investors is expected in the next few years because of the federal and state government

actions to tighten the restrictions on foreign property investors.

tourists are the highest contributor. Asian investment is also high with over $4 billion

projects under construction. Out of the $11.7 billion, $9 billion has been allocated to

resort projects. In the education related construction, sector forecasts show 27.5% growth

with a value of $6.2 billion while the health sector has shown healthy growth whose

forecast shows a 17.9% growth (Loosemore, 2014).

Residential Building: The demand for new housing commencements have been rising

over the years due to high population growth and low rate of interest. The supply gap was

filled by most jurisdiction and the soaring demand is bringing a dent to the housing

shortage. Future demand is also expected to rise not only due to rise in population but

also due to demand drivers from demand drivers such as foreign investors and so the

shortage in supply has to be met. Forecasts predict the commencements to be around

183000 in the next five years and the outlook is mixed by sectors and across geographies

(Finkel, 2015). As reflected by the graph, the decline in housing construction comes

mostly from the apartment sector with dwelling construction falling and some

jurisdictions provide an offset. Due to the housing boom, most of the demand activity

arose from the apartment market and the expected fall in activity, estimated to be around

6.6% would come from this sector. There is high demand for renovations as the market

faces healthy price growth and cheap credit and it is expected to grow by 1.3% if prices

do not fall considerably(Gregory and Smith, 2016). A considerable fall in foreign

investors is expected in the next few years because of the federal and state government

actions to tighten the restrictions on foreign property investors.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10PERFORMANCE OF AUSTRALIA’S CONSTRUCTION INDUSTRY

FIGURE 5: Housing in Australia, (2010 -2022)

Source: Australian Bureau of Statistics

In Australia, the construction industry has a value of around $112 billion annually and

contributes to the GDP growth by 9%. According to the Australian Constructors Association,

there had been a 10% fall in 2015 and recovered by 5.2% in 2017. The forecast for 2018 is a

9.3% rise and an 8% rise in 2019 (Ball, 2014). This rise will come from the road, rail, civil and

telecommunication infrastructure. Commercial construction activities, which had contracted in

2017, is expected to rise in 2018 to 7.8% (Australian Constructors Association, 2018). A

decrease is expected in the residential sector in 2019 but with the mining investment, the decline

rate will be easing out. The overall increase in the sector will lead to higher workload and

investment demand and therefore the workforce will expand. This expansion is expected to result

in a rise in the total employment by 2.9% in 2018 and 2.7% in 2019 as per the recent Australian

Bureau of Statistics Labour Force Survey data.

FIGURE 5: Housing in Australia, (2010 -2022)

Source: Australian Bureau of Statistics

In Australia, the construction industry has a value of around $112 billion annually and

contributes to the GDP growth by 9%. According to the Australian Constructors Association,

there had been a 10% fall in 2015 and recovered by 5.2% in 2017. The forecast for 2018 is a

9.3% rise and an 8% rise in 2019 (Ball, 2014). This rise will come from the road, rail, civil and

telecommunication infrastructure. Commercial construction activities, which had contracted in

2017, is expected to rise in 2018 to 7.8% (Australian Constructors Association, 2018). A

decrease is expected in the residential sector in 2019 but with the mining investment, the decline

rate will be easing out. The overall increase in the sector will lead to higher workload and

investment demand and therefore the workforce will expand. This expansion is expected to result

in a rise in the total employment by 2.9% in 2018 and 2.7% in 2019 as per the recent Australian

Bureau of Statistics Labour Force Survey data.

11PERFORMANCE OF AUSTRALIA’S CONSTRUCTION INDUSTRY

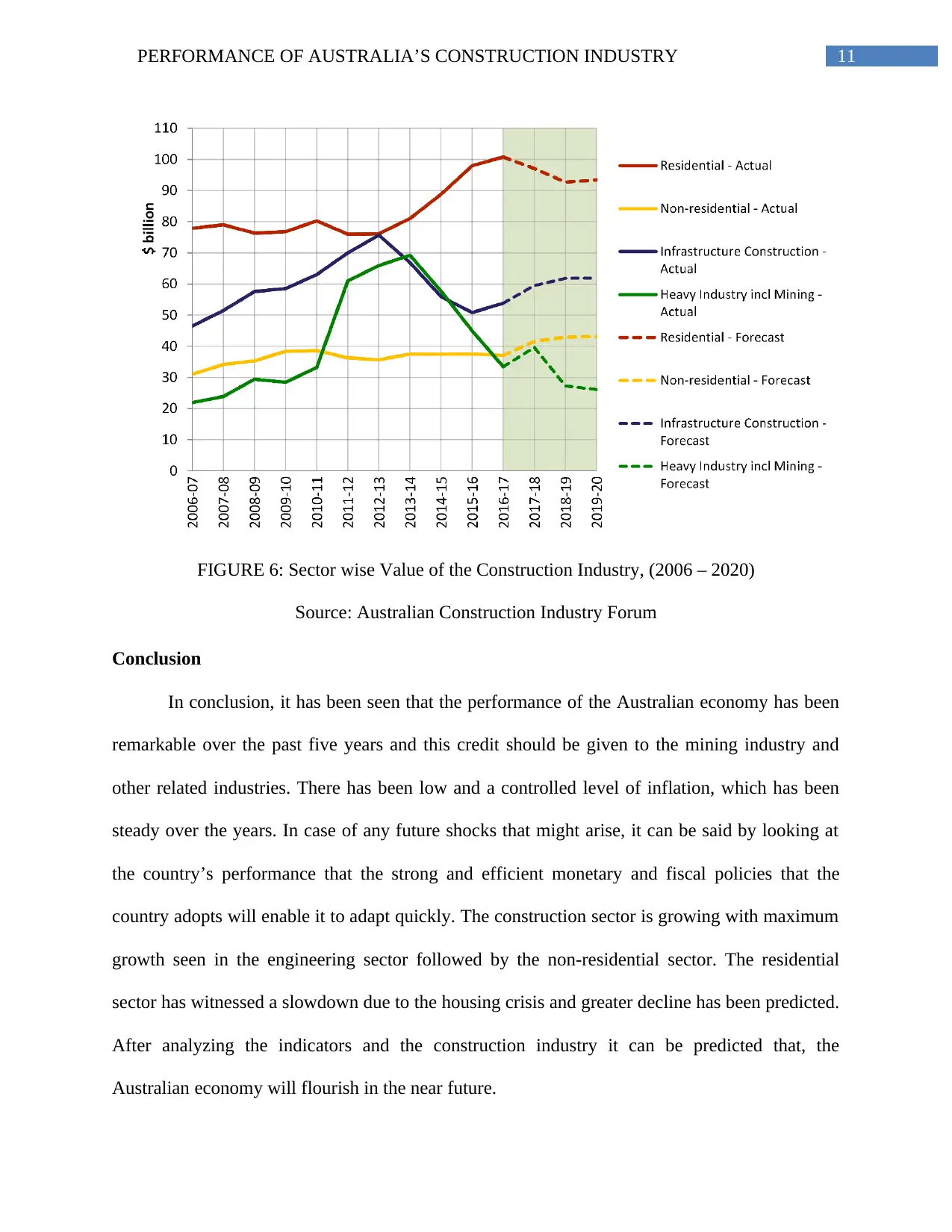

FIGURE 6: Sector wise Value of the Construction Industry, (2006 – 2020)

Source: Australian Construction Industry Forum

Conclusion

In conclusion, it has been seen that the performance of the Australian economy has been

remarkable over the past five years and this credit should be given to the mining industry and

other related industries. There has been low and a controlled level of inflation, which has been

steady over the years. In case of any future shocks that might arise, it can be said by looking at

the country’s performance that the strong and efficient monetary and fiscal policies that the

country adopts will enable it to adapt quickly. The construction sector is growing with maximum

growth seen in the engineering sector followed by the non-residential sector. The residential

sector has witnessed a slowdown due to the housing crisis and greater decline has been predicted.

After analyzing the indicators and the construction industry it can be predicted that, the

Australian economy will flourish in the near future.

FIGURE 6: Sector wise Value of the Construction Industry, (2006 – 2020)

Source: Australian Construction Industry Forum

Conclusion

In conclusion, it has been seen that the performance of the Australian economy has been

remarkable over the past five years and this credit should be given to the mining industry and

other related industries. There has been low and a controlled level of inflation, which has been

steady over the years. In case of any future shocks that might arise, it can be said by looking at

the country’s performance that the strong and efficient monetary and fiscal policies that the

country adopts will enable it to adapt quickly. The construction sector is growing with maximum

growth seen in the engineering sector followed by the non-residential sector. The residential

sector has witnessed a slowdown due to the housing crisis and greater decline has been predicted.

After analyzing the indicators and the construction industry it can be predicted that, the

Australian economy will flourish in the near future.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 19