BUS700 Economics: Macroeconomic Performance of Australia & USA

VerifiedAdded on 2023/06/12

|11

|3532

|157

Report

AI Summary

This report provides a comprehensive analysis of Australia's macroeconomic performance from 1990 to 2016, examining key indicators such as GDP growth, unemployment, inflation, interest rates, exchange rates, and net exports. It explores the relationships between real GDP growth and inflation, as well as GDP growth and unemployment, identifying evidence of the business cycle. The analysis includes pairwise graphs and summary statistics to illustrate these relationships. The report also discusses the impact of exchange rates on net exports and compares cash rates and fund rates between Australia and the USA, highlighting the influence of monetary policy in one nation on the other. The conclusion offers an outlook on the Australian economy, suggesting a potential return to economic growth following a period of recovery.

Running Head: ECONOMIC ASSIGNMENT

Economic Assignment

Name of the Student

Name of the University

Course ID

Economic Assignment

Name of the Student

Name of the University

Course ID

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1ECONOMIC ASSIGNMENT

Executive Summary

USA and Australia are two of the most powerful developed nations in the world. The paper has

scrutinized the Australia’s economic performance. In this context, the relation between USA and Australia

has been explored in light of relation between exchange rate and net export and movement and bank rate

in the two nation. The trend analysis of GDP growth and unemployment shows unemployment moves in

opposite direction of growth. GDP growth though initially influences price level the relation however

weakens following inflation targeting policy of unemployment. A weak Australian dollar helps to maintain a

trade surplus while a strong Australian dollar does the reverse. Bank rate in both the nation has declined

overtime following a monetary easing. The quick recovery of Australian economy indicates that the

economy will soon enter in a new era of economic growth.

Executive Summary

USA and Australia are two of the most powerful developed nations in the world. The paper has

scrutinized the Australia’s economic performance. In this context, the relation between USA and Australia

has been explored in light of relation between exchange rate and net export and movement and bank rate

in the two nation. The trend analysis of GDP growth and unemployment shows unemployment moves in

opposite direction of growth. GDP growth though initially influences price level the relation however

weakens following inflation targeting policy of unemployment. A weak Australian dollar helps to maintain a

trade surplus while a strong Australian dollar does the reverse. Bank rate in both the nation has declined

overtime following a monetary easing. The quick recovery of Australian economy indicates that the

economy will soon enter in a new era of economic growth.

2ECONOMIC ASSIGNMENT

Table of Contents

Introduction.................................................................................................................................................. 3

Relationship between real GDP and inflation and unemployment...............................................................3

Growth in real GDP and trend in unemployment......................................................................................3

Growth in real GDP and trend in inflation................................................................................................. 4

Business cycle and economic growth...................................................................................................... 4

Net export and exchange rate.................................................................................................................. 5

Cash rate and fund rate............................................................................................................................... 6

Outlook of Australian economy.................................................................................................................... 7

Conclusion................................................................................................................................................... 7

List of References........................................................................................................................................ 9

Table of Contents

Introduction.................................................................................................................................................. 3

Relationship between real GDP and inflation and unemployment...............................................................3

Growth in real GDP and trend in unemployment......................................................................................3

Growth in real GDP and trend in inflation................................................................................................. 4

Business cycle and economic growth...................................................................................................... 4

Net export and exchange rate.................................................................................................................. 5

Cash rate and fund rate............................................................................................................................... 6

Outlook of Australian economy.................................................................................................................... 7

Conclusion................................................................................................................................................... 7

List of References........................................................................................................................................ 9

You're viewing a preview

Unlock full access by subscribing today!

3ECONOMIC ASSIGNMENT

Introduction

Different indicative measures of economic performance of a nation are GDP growth, inflation,

unemployment, interest rate, export and import. Evaluation of economic performance thus requires

analysis of economic performance in each of this indicator (Fontana and Setterfield, 2016). Australia is a

small-developed nation with high dependency on service sector especially financial services. Like several

other developed nation Australia also has experienced dynamic fluctuation in the economy. The interest

factor about austral is that, it has quickly absorbed the economic shocks and successfully balanced the

stable growth path. The paper tries to find insights about macroeconomic performance of Australia for the

last few years specifically from 1990 to 2016. The analysis also includes the economic relation between

Australia and USA.

Relationship between real GDP and inflation and unemployment

Among different interconnected macro variables, relation between GDP growth, inflation and

unemployment is widely discussed. Unemployment and price level in a nation move along with the growth

in real GDP. A rising GDP growth implies a favorable condition for employment growth pushing

unemployment to a low level (Terra, 2015). Growth in real GDP by boosting economic activity pushes up

the price level. Very high price level however has an adverse effect on growth by a lower output resulted

from increasing cost of production.

Growth in real GDP and trend in unemployment

1990

1992

1994

1996

1998

2000

2002

2004

2006

2008

2010

2012

2014

2016

-2.00

0.00

2.00

4.00

6.00

8.00

10.00

12.00

Real GDP growth and unemployment

Real GDP growth rate Unemployment

Year

Unemployment and GDP growth rate

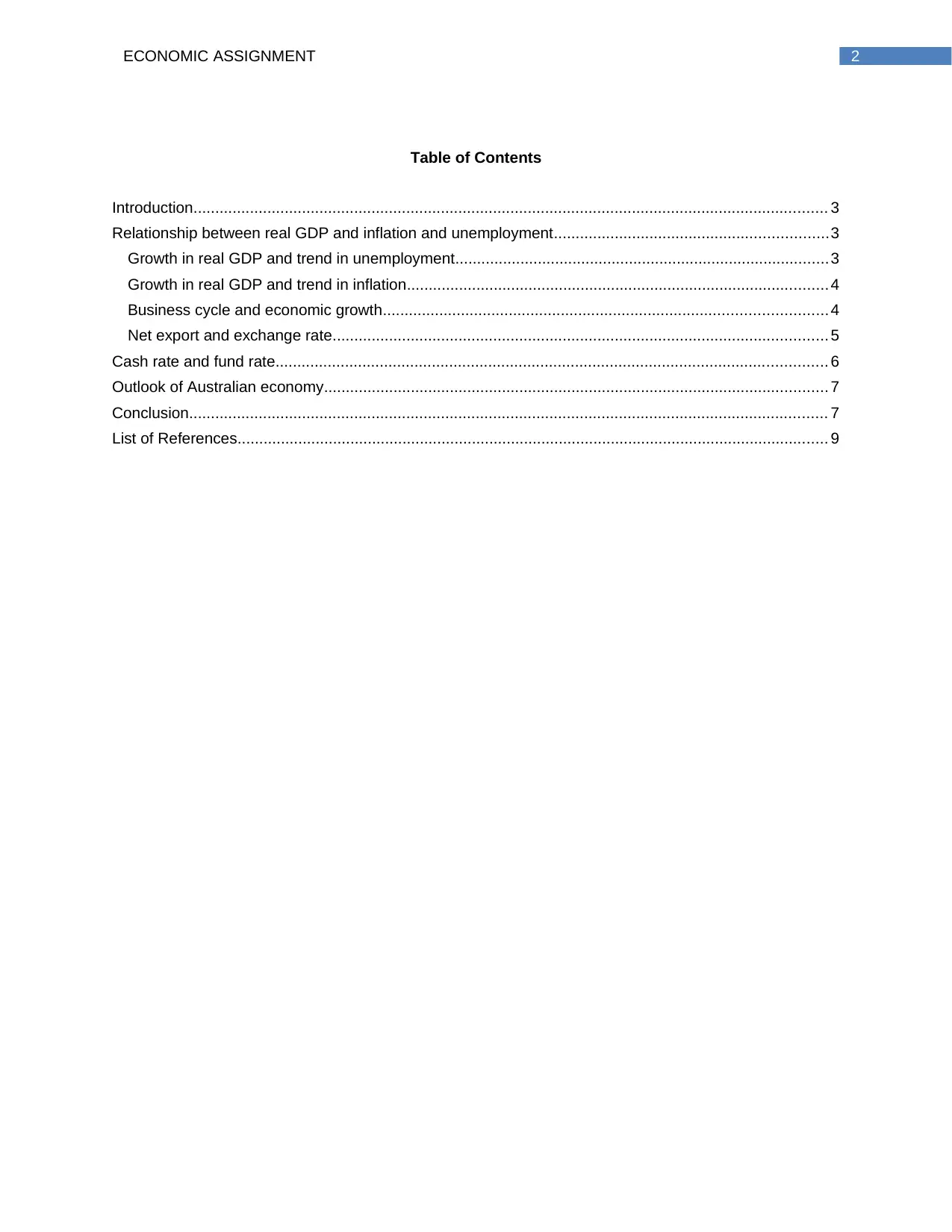

Figure 1: Unemployment and GDP growth

Figure 1 represents the unemployment trend in Australia along with trend in GDP growth rate. The

unemployment rate except in the last few years has a more or less declining trend. GDP growth on the

other hand has only a moderate growth rate with a sudden fall in growth during years of recession. The

decline in unemployment along with a growth in GDP reduces the gap between rate of growth and that of

unemployment. This shows a positive influence of economic growth on labor market performance. The

economic growth in Australia thus expands opportunities for laborers (Hartwell, 2017). One major driver of

Australian economic growth for several years is the mining sector. The sector being highly labor intensive,

during mining boom of Australian many people get opportunities to get employed. With a decline in

growth rate unemployment increases as reflected from widening gap between unemployment and growth

rate since 2013.

Introduction

Different indicative measures of economic performance of a nation are GDP growth, inflation,

unemployment, interest rate, export and import. Evaluation of economic performance thus requires

analysis of economic performance in each of this indicator (Fontana and Setterfield, 2016). Australia is a

small-developed nation with high dependency on service sector especially financial services. Like several

other developed nation Australia also has experienced dynamic fluctuation in the economy. The interest

factor about austral is that, it has quickly absorbed the economic shocks and successfully balanced the

stable growth path. The paper tries to find insights about macroeconomic performance of Australia for the

last few years specifically from 1990 to 2016. The analysis also includes the economic relation between

Australia and USA.

Relationship between real GDP and inflation and unemployment

Among different interconnected macro variables, relation between GDP growth, inflation and

unemployment is widely discussed. Unemployment and price level in a nation move along with the growth

in real GDP. A rising GDP growth implies a favorable condition for employment growth pushing

unemployment to a low level (Terra, 2015). Growth in real GDP by boosting economic activity pushes up

the price level. Very high price level however has an adverse effect on growth by a lower output resulted

from increasing cost of production.

Growth in real GDP and trend in unemployment

1990

1992

1994

1996

1998

2000

2002

2004

2006

2008

2010

2012

2014

2016

-2.00

0.00

2.00

4.00

6.00

8.00

10.00

12.00

Real GDP growth and unemployment

Real GDP growth rate Unemployment

Year

Unemployment and GDP growth rate

Figure 1: Unemployment and GDP growth

Figure 1 represents the unemployment trend in Australia along with trend in GDP growth rate. The

unemployment rate except in the last few years has a more or less declining trend. GDP growth on the

other hand has only a moderate growth rate with a sudden fall in growth during years of recession. The

decline in unemployment along with a growth in GDP reduces the gap between rate of growth and that of

unemployment. This shows a positive influence of economic growth on labor market performance. The

economic growth in Australia thus expands opportunities for laborers (Hartwell, 2017). One major driver of

Australian economic growth for several years is the mining sector. The sector being highly labor intensive,

during mining boom of Australian many people get opportunities to get employed. With a decline in

growth rate unemployment increases as reflected from widening gap between unemployment and growth

rate since 2013.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4ECONOMIC ASSIGNMENT

Growth in real GDP and trend in inflation

1990

1992

1994

1996

1998

2000

2002

2004

2006

2008

2010

2012

2014

2016

-1.00

0.00

1.00

2.00

3.00

4.00

5.00

6.00

7.00

8.00

Real GDP growth and inflation

Real GDP growth rate Inflation

Year

GDP growth and inflation

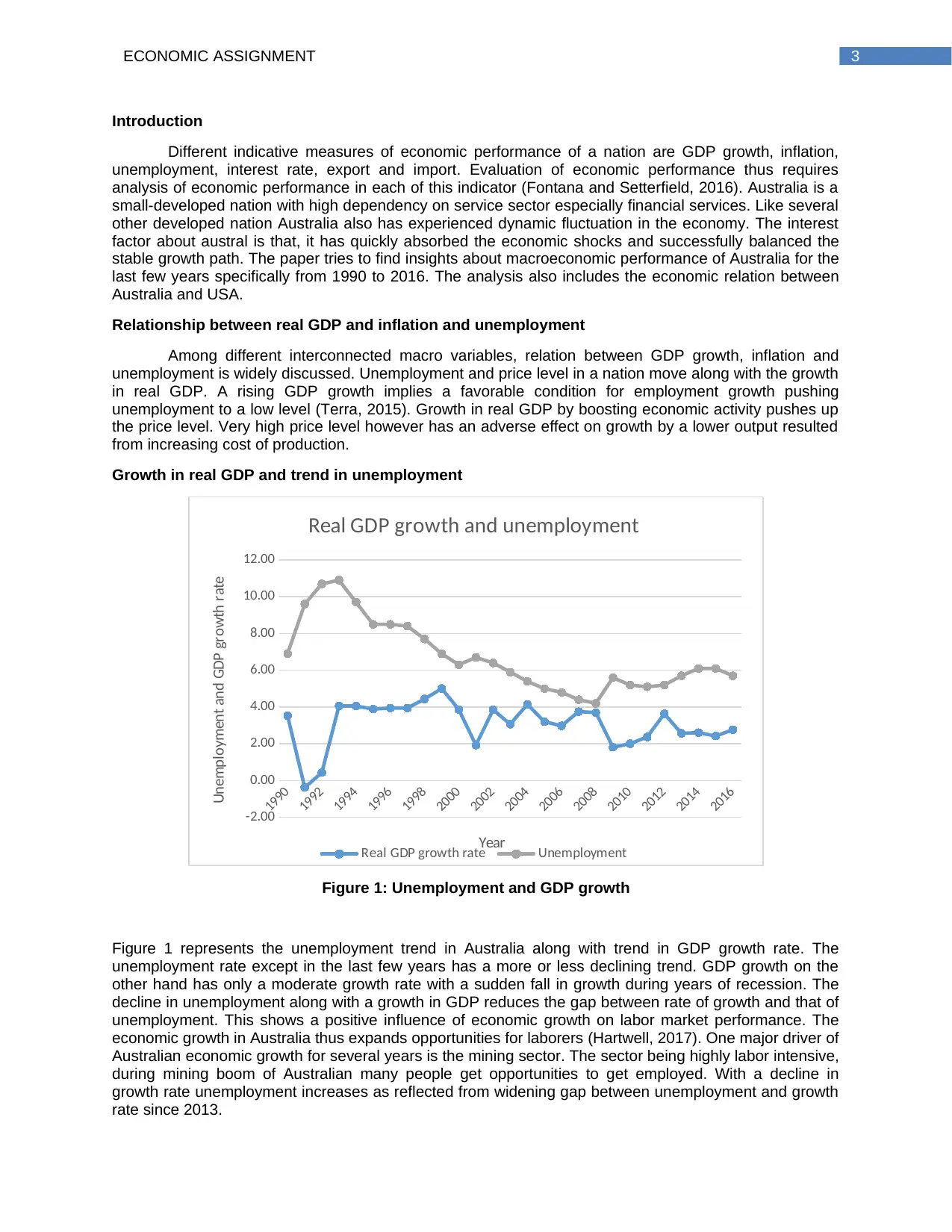

Figure 2: GDP growth and trend in inflation

Unlike unemployment, no steady relation is observed between economic growth and that of inflation. The

price level fluctuates more than GDP growth indicating there are factors other than GDP growth having

significant influence on price level (Thorpe and Leitão, 2014). The price level in recent years is much

stable as compared to that in early 1990s. For some years, both growth rate and inflation increases

simultaneously showing signs of economic expansion. While in others the growth rates are associated

with a low level price indicating an inverse relation. One factor explaining existence of economic growth

along with a slow or stable movement of price level is inflation targeting policy of Reserve Bank of

Australia, targets to maintain a price level of 2 percent (Svensson, 2015).

Business cycle and economic growth

1 9 9 0

1 9 9 2

1 9 9 4

1 9 9 6

1 9 9 8

2 0 0 0

2 0 0 2

2 0 0 4

2 0 0 6

2 0 0 8

2 0 1 0

2 0 1 2

2 0 1 4

2 0 1 6

-1.00

0.00

1.00

2.00

3.00

4.00

5.00

6.00

Real GDP growth rate

Year

Growth rate

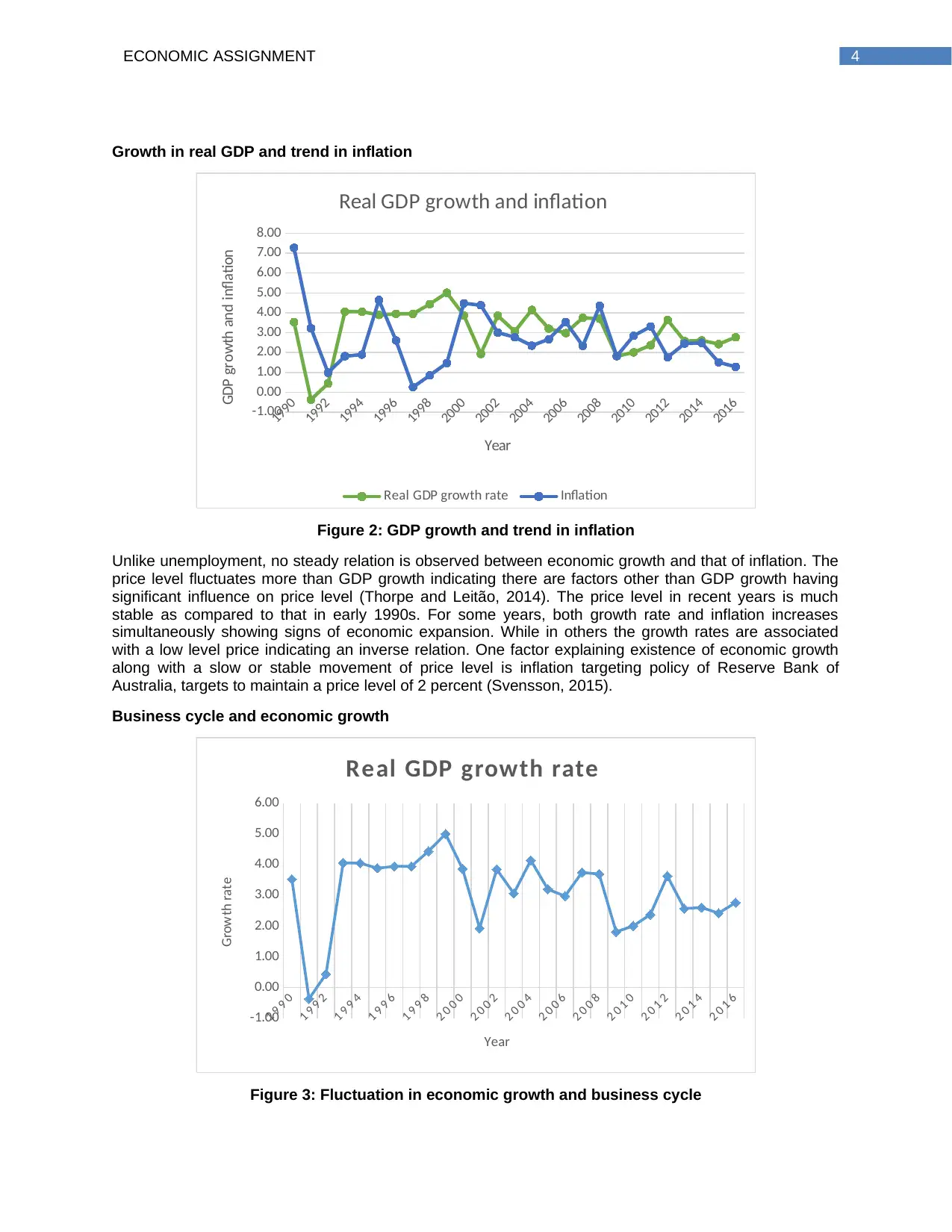

Figure 3: Fluctuation in economic growth and business cycle

Growth in real GDP and trend in inflation

1990

1992

1994

1996

1998

2000

2002

2004

2006

2008

2010

2012

2014

2016

-1.00

0.00

1.00

2.00

3.00

4.00

5.00

6.00

7.00

8.00

Real GDP growth and inflation

Real GDP growth rate Inflation

Year

GDP growth and inflation

Figure 2: GDP growth and trend in inflation

Unlike unemployment, no steady relation is observed between economic growth and that of inflation. The

price level fluctuates more than GDP growth indicating there are factors other than GDP growth having

significant influence on price level (Thorpe and Leitão, 2014). The price level in recent years is much

stable as compared to that in early 1990s. For some years, both growth rate and inflation increases

simultaneously showing signs of economic expansion. While in others the growth rates are associated

with a low level price indicating an inverse relation. One factor explaining existence of economic growth

along with a slow or stable movement of price level is inflation targeting policy of Reserve Bank of

Australia, targets to maintain a price level of 2 percent (Svensson, 2015).

Business cycle and economic growth

1 9 9 0

1 9 9 2

1 9 9 4

1 9 9 6

1 9 9 8

2 0 0 0

2 0 0 2

2 0 0 4

2 0 0 6

2 0 0 8

2 0 1 0

2 0 1 2

2 0 1 4

2 0 1 6

-1.00

0.00

1.00

2.00

3.00

4.00

5.00

6.00

Real GDP growth rate

Year

Growth rate

Figure 3: Fluctuation in economic growth and business cycle

5ECONOMIC ASSIGNMENT

The economic growth of a nation is subject to fluctuation resulted from shock in domestic and

external economy. The business cycle theory captures the fluctuation in economy growth rate. an

economy generally undergoes through four phases of business cycle – expansion, economic boom,

recession and finally trough. Among these economic boom and trough are the two extreme phase when

the economy records highest and lowest growth point respectively. Expansion implies expansion of

output, employment and other economic activity (Belongia and Ireland, 2016.). During recession there is a

general downward trend in economic activity. Every economy passes through these four phases of

business cycle. No exception is observed for Australia. The time length of business cycle phases however

varies across different economies depending on the internal structure of the economy.

The period of early 1990s showed a clear evidence of economic recession. Growth rate in the

early 1991 was negative. Economic expansion began since 1992 with growth rate gradually started

increasing. Growth rate peaked to 5.01 percent in 1999 (Kent, 2014). Growth gradually, In between these

years, there was a moderate recession in 1995 with growth rate fell to 3.89. Growth rate expanded from

1196 onwards and finally reached to the peak level in 1999. In the beginning if twenty first century growth

rate began to decline with a sign of recovery in 2004, the economy grew at a rate of 4.15 percent. Growth

slightly slowed down in the three years and backed to a rate of 3.75 in 2007. Economic trough gain

evidenced in 2009 with a growth rate of only 1.81 percent (Word Bank, 2018). Expansion began in 2010

and in 2012 growth recovered to 3.63 percent. From 2013 onwards, economy began to grew at a

relatively slow rate with an average growth rate of 2.5%.

Net export and exchange rate

Among four primary components of GDP, net export is one major component. It is an estimate of

net gain from trade and obtained as total export less total import. In context of Australian economy, the

external sector plays an important role in determining GDP (DFAT, 2018). Until the decade of 1960s,

trade relation of Australia was mostly limited to United State and Britain. With passes of time and

development of different industries and service sectors Australia has gained a competitive edge in the

global market leading to expansion of trade relation with several nations across the world. Australia

enjoys a comparative advantage over wide variety of goods and services (Argy and Nevile, 2016). The

competitive advantage of Australia varied from high quality technology intensive product to high quality

wine and in food processing. Service trade of Australia include services like education and tourism,

financial and professional services.

Iron ores and concentrates, coal, natural gas, education related travel service and personal travel

service excluding education are the top five exports of Australia. The goods and services are exported to

different markets of China, Japan, United State, Republic of Korea and India. Australia’s importable

include personal travel service, which excludes education, passengers’ vehicles; refine petroleum, freight

service and telecom equipment and part (Gilpin, 2016). The importable are obtained from China, United

State, Japan, Republic of Korea and Thailand.

The demand for export, import, and hence, balance in trade depends on the relative value of

currency termed as the exchange rate. It measures how much home currency needs to be exchanged for

one unit of foreign currency. High value of home currency is though favorable for import but hurts trade

balance by lowering is export demand. In contrast, low value of currency indicates a weak position of the

nation but is favorable for export and trade balance (Pagan and Wilcox, 2015). The value of Australian

dollar especially against US dollar has a considerable impact on Australia’s balance of trade. Devaluation

of Australian dollar implies a relatively a lower price for exported goods from Australia. This increases

export demand of Australian export. The cheaper export and relatively expensive import improves trade

balance. Currency appreciation has an opposite effect on net export.

The figure below shows pairwise movement of real exchange rate between United State and

Australia and that of the net export of Australia.

The economic growth of a nation is subject to fluctuation resulted from shock in domestic and

external economy. The business cycle theory captures the fluctuation in economy growth rate. an

economy generally undergoes through four phases of business cycle – expansion, economic boom,

recession and finally trough. Among these economic boom and trough are the two extreme phase when

the economy records highest and lowest growth point respectively. Expansion implies expansion of

output, employment and other economic activity (Belongia and Ireland, 2016.). During recession there is a

general downward trend in economic activity. Every economy passes through these four phases of

business cycle. No exception is observed for Australia. The time length of business cycle phases however

varies across different economies depending on the internal structure of the economy.

The period of early 1990s showed a clear evidence of economic recession. Growth rate in the

early 1991 was negative. Economic expansion began since 1992 with growth rate gradually started

increasing. Growth rate peaked to 5.01 percent in 1999 (Kent, 2014). Growth gradually, In between these

years, there was a moderate recession in 1995 with growth rate fell to 3.89. Growth rate expanded from

1196 onwards and finally reached to the peak level in 1999. In the beginning if twenty first century growth

rate began to decline with a sign of recovery in 2004, the economy grew at a rate of 4.15 percent. Growth

slightly slowed down in the three years and backed to a rate of 3.75 in 2007. Economic trough gain

evidenced in 2009 with a growth rate of only 1.81 percent (Word Bank, 2018). Expansion began in 2010

and in 2012 growth recovered to 3.63 percent. From 2013 onwards, economy began to grew at a

relatively slow rate with an average growth rate of 2.5%.

Net export and exchange rate

Among four primary components of GDP, net export is one major component. It is an estimate of

net gain from trade and obtained as total export less total import. In context of Australian economy, the

external sector plays an important role in determining GDP (DFAT, 2018). Until the decade of 1960s,

trade relation of Australia was mostly limited to United State and Britain. With passes of time and

development of different industries and service sectors Australia has gained a competitive edge in the

global market leading to expansion of trade relation with several nations across the world. Australia

enjoys a comparative advantage over wide variety of goods and services (Argy and Nevile, 2016). The

competitive advantage of Australia varied from high quality technology intensive product to high quality

wine and in food processing. Service trade of Australia include services like education and tourism,

financial and professional services.

Iron ores and concentrates, coal, natural gas, education related travel service and personal travel

service excluding education are the top five exports of Australia. The goods and services are exported to

different markets of China, Japan, United State, Republic of Korea and India. Australia’s importable

include personal travel service, which excludes education, passengers’ vehicles; refine petroleum, freight

service and telecom equipment and part (Gilpin, 2016). The importable are obtained from China, United

State, Japan, Republic of Korea and Thailand.

The demand for export, import, and hence, balance in trade depends on the relative value of

currency termed as the exchange rate. It measures how much home currency needs to be exchanged for

one unit of foreign currency. High value of home currency is though favorable for import but hurts trade

balance by lowering is export demand. In contrast, low value of currency indicates a weak position of the

nation but is favorable for export and trade balance (Pagan and Wilcox, 2015). The value of Australian

dollar especially against US dollar has a considerable impact on Australia’s balance of trade. Devaluation

of Australian dollar implies a relatively a lower price for exported goods from Australia. This increases

export demand of Australian export. The cheaper export and relatively expensive import improves trade

balance. Currency appreciation has an opposite effect on net export.

The figure below shows pairwise movement of real exchange rate between United State and

Australia and that of the net export of Australia.

You're viewing a preview

Unlock full access by subscribing today!

6ECONOMIC ASSIGNMENT

1990

1992

1994

1996

1998

2000

2002

2004

2006

2008

2010

2012

2014

2016

-60000000000

-40000000000

-20000000000

0

20000000000

40000000000

60000000000

80000000000

0.00

0.50

1.00

1.50

2.00

2.50

Net export and Real exchange rate

Net Export Exchange rate

Year

Net Export

AUD/US

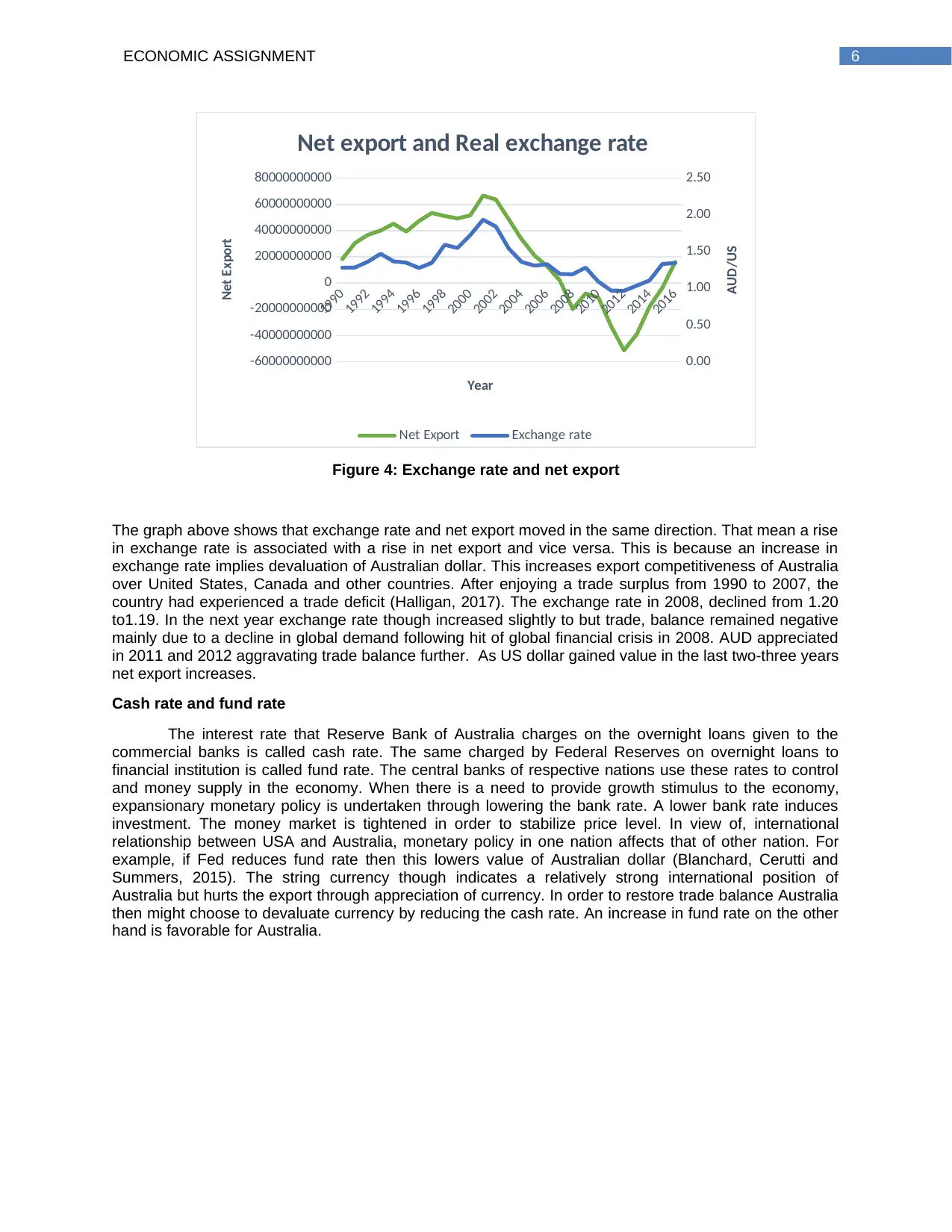

Figure 4: Exchange rate and net export

The graph above shows that exchange rate and net export moved in the same direction. That mean a rise

in exchange rate is associated with a rise in net export and vice versa. This is because an increase in

exchange rate implies devaluation of Australian dollar. This increases export competitiveness of Australia

over United States, Canada and other countries. After enjoying a trade surplus from 1990 to 2007, the

country had experienced a trade deficit (Halligan, 2017). The exchange rate in 2008, declined from 1.20

to1.19. In the next year exchange rate though increased slightly to but trade, balance remained negative

mainly due to a decline in global demand following hit of global financial crisis in 2008. AUD appreciated

in 2011 and 2012 aggravating trade balance further. As US dollar gained value in the last two-three years

net export increases.

Cash rate and fund rate

The interest rate that Reserve Bank of Australia charges on the overnight loans given to the

commercial banks is called cash rate. The same charged by Federal Reserves on overnight loans to

financial institution is called fund rate. The central banks of respective nations use these rates to control

and money supply in the economy. When there is a need to provide growth stimulus to the economy,

expansionary monetary policy is undertaken through lowering the bank rate. A lower bank rate induces

investment. The money market is tightened in order to stabilize price level. In view of, international

relationship between USA and Australia, monetary policy in one nation affects that of other nation. For

example, if Fed reduces fund rate then this lowers value of Australian dollar (Blanchard, Cerutti and

Summers, 2015). The string currency though indicates a relatively strong international position of

Australia but hurts the export through appreciation of currency. In order to restore trade balance Australia

then might choose to devaluate currency by reducing the cash rate. An increase in fund rate on the other

hand is favorable for Australia.

1990

1992

1994

1996

1998

2000

2002

2004

2006

2008

2010

2012

2014

2016

-60000000000

-40000000000

-20000000000

0

20000000000

40000000000

60000000000

80000000000

0.00

0.50

1.00

1.50

2.00

2.50

Net export and Real exchange rate

Net Export Exchange rate

Year

Net Export

AUD/US

Figure 4: Exchange rate and net export

The graph above shows that exchange rate and net export moved in the same direction. That mean a rise

in exchange rate is associated with a rise in net export and vice versa. This is because an increase in

exchange rate implies devaluation of Australian dollar. This increases export competitiveness of Australia

over United States, Canada and other countries. After enjoying a trade surplus from 1990 to 2007, the

country had experienced a trade deficit (Halligan, 2017). The exchange rate in 2008, declined from 1.20

to1.19. In the next year exchange rate though increased slightly to but trade, balance remained negative

mainly due to a decline in global demand following hit of global financial crisis in 2008. AUD appreciated

in 2011 and 2012 aggravating trade balance further. As US dollar gained value in the last two-three years

net export increases.

Cash rate and fund rate

The interest rate that Reserve Bank of Australia charges on the overnight loans given to the

commercial banks is called cash rate. The same charged by Federal Reserves on overnight loans to

financial institution is called fund rate. The central banks of respective nations use these rates to control

and money supply in the economy. When there is a need to provide growth stimulus to the economy,

expansionary monetary policy is undertaken through lowering the bank rate. A lower bank rate induces

investment. The money market is tightened in order to stabilize price level. In view of, international

relationship between USA and Australia, monetary policy in one nation affects that of other nation. For

example, if Fed reduces fund rate then this lowers value of Australian dollar (Blanchard, Cerutti and

Summers, 2015). The string currency though indicates a relatively strong international position of

Australia but hurts the export through appreciation of currency. In order to restore trade balance Australia

then might choose to devaluate currency by reducing the cash rate. An increase in fund rate on the other

hand is favorable for Australia.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7ECONOMIC ASSIGNMENT

1990

1992

1994

1996

1998

2000

2002

2004

2006

2008

2010

2012

2014

2016

0.00

2.00

4.00

6.00

8.00

10.00

12.00

14.00

16.00

Cash rate and Fed fund rate

cash rate Fund rate

Year

Cash rate and fund rate

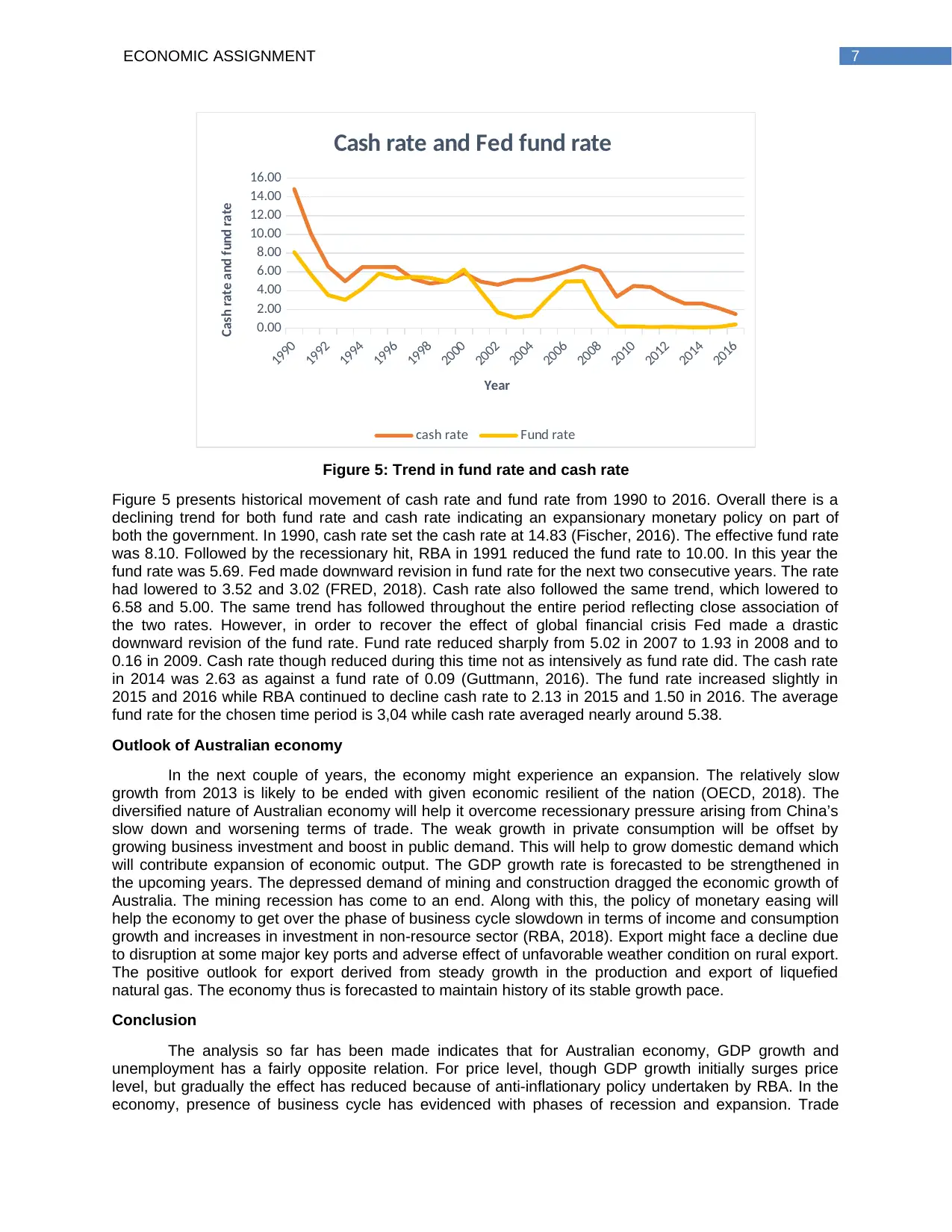

Figure 5: Trend in fund rate and cash rate

Figure 5 presents historical movement of cash rate and fund rate from 1990 to 2016. Overall there is a

declining trend for both fund rate and cash rate indicating an expansionary monetary policy on part of

both the government. In 1990, cash rate set the cash rate at 14.83 (Fischer, 2016). The effective fund rate

was 8.10. Followed by the recessionary hit, RBA in 1991 reduced the fund rate to 10.00. In this year the

fund rate was 5.69. Fed made downward revision in fund rate for the next two consecutive years. The rate

had lowered to 3.52 and 3.02 (FRED, 2018). Cash rate also followed the same trend, which lowered to

6.58 and 5.00. The same trend has followed throughout the entire period reflecting close association of

the two rates. However, in order to recover the effect of global financial crisis Fed made a drastic

downward revision of the fund rate. Fund rate reduced sharply from 5.02 in 2007 to 1.93 in 2008 and to

0.16 in 2009. Cash rate though reduced during this time not as intensively as fund rate did. The cash rate

in 2014 was 2.63 as against a fund rate of 0.09 (Guttmann, 2016). The fund rate increased slightly in

2015 and 2016 while RBA continued to decline cash rate to 2.13 in 2015 and 1.50 in 2016. The average

fund rate for the chosen time period is 3,04 while cash rate averaged nearly around 5.38.

Outlook of Australian economy

In the next couple of years, the economy might experience an expansion. The relatively slow

growth from 2013 is likely to be ended with given economic resilient of the nation (OECD, 2018). The

diversified nature of Australian economy will help it overcome recessionary pressure arising from China’s

slow down and worsening terms of trade. The weak growth in private consumption will be offset by

growing business investment and boost in public demand. This will help to grow domestic demand which

will contribute expansion of economic output. The GDP growth rate is forecasted to be strengthened in

the upcoming years. The depressed demand of mining and construction dragged the economic growth of

Australia. The mining recession has come to an end. Along with this, the policy of monetary easing will

help the economy to get over the phase of business cycle slowdown in terms of income and consumption

growth and increases in investment in non-resource sector (RBA, 2018). Export might face a decline due

to disruption at some major key ports and adverse effect of unfavorable weather condition on rural export.

The positive outlook for export derived from steady growth in the production and export of liquefied

natural gas. The economy thus is forecasted to maintain history of its stable growth pace.

Conclusion

The analysis so far has been made indicates that for Australian economy, GDP growth and

unemployment has a fairly opposite relation. For price level, though GDP growth initially surges price

level, but gradually the effect has reduced because of anti-inflationary policy undertaken by RBA. In the

economy, presence of business cycle has evidenced with phases of recession and expansion. Trade

1990

1992

1994

1996

1998

2000

2002

2004

2006

2008

2010

2012

2014

2016

0.00

2.00

4.00

6.00

8.00

10.00

12.00

14.00

16.00

Cash rate and Fed fund rate

cash rate Fund rate

Year

Cash rate and fund rate

Figure 5: Trend in fund rate and cash rate

Figure 5 presents historical movement of cash rate and fund rate from 1990 to 2016. Overall there is a

declining trend for both fund rate and cash rate indicating an expansionary monetary policy on part of

both the government. In 1990, cash rate set the cash rate at 14.83 (Fischer, 2016). The effective fund rate

was 8.10. Followed by the recessionary hit, RBA in 1991 reduced the fund rate to 10.00. In this year the

fund rate was 5.69. Fed made downward revision in fund rate for the next two consecutive years. The rate

had lowered to 3.52 and 3.02 (FRED, 2018). Cash rate also followed the same trend, which lowered to

6.58 and 5.00. The same trend has followed throughout the entire period reflecting close association of

the two rates. However, in order to recover the effect of global financial crisis Fed made a drastic

downward revision of the fund rate. Fund rate reduced sharply from 5.02 in 2007 to 1.93 in 2008 and to

0.16 in 2009. Cash rate though reduced during this time not as intensively as fund rate did. The cash rate

in 2014 was 2.63 as against a fund rate of 0.09 (Guttmann, 2016). The fund rate increased slightly in

2015 and 2016 while RBA continued to decline cash rate to 2.13 in 2015 and 1.50 in 2016. The average

fund rate for the chosen time period is 3,04 while cash rate averaged nearly around 5.38.

Outlook of Australian economy

In the next couple of years, the economy might experience an expansion. The relatively slow

growth from 2013 is likely to be ended with given economic resilient of the nation (OECD, 2018). The

diversified nature of Australian economy will help it overcome recessionary pressure arising from China’s

slow down and worsening terms of trade. The weak growth in private consumption will be offset by

growing business investment and boost in public demand. This will help to grow domestic demand which

will contribute expansion of economic output. The GDP growth rate is forecasted to be strengthened in

the upcoming years. The depressed demand of mining and construction dragged the economic growth of

Australia. The mining recession has come to an end. Along with this, the policy of monetary easing will

help the economy to get over the phase of business cycle slowdown in terms of income and consumption

growth and increases in investment in non-resource sector (RBA, 2018). Export might face a decline due

to disruption at some major key ports and adverse effect of unfavorable weather condition on rural export.

The positive outlook for export derived from steady growth in the production and export of liquefied

natural gas. The economy thus is forecasted to maintain history of its stable growth pace.

Conclusion

The analysis so far has been made indicates that for Australian economy, GDP growth and

unemployment has a fairly opposite relation. For price level, though GDP growth initially surges price

level, but gradually the effect has reduced because of anti-inflationary policy undertaken by RBA. In the

economy, presence of business cycle has evidenced with phases of recession and expansion. Trade

8ECONOMIC ASSIGNMENT

balance of Australia is subject to variation in the exchange rate between Australia and USA. So far as

monetary policy is concerned, USA and Australia both has provided monetary policy stimulus as a

strategy of economy growth. Economic slowdown of Australia is likely to be recovered within a next few

years moving it again to the path of economic expansion.

balance of Australia is subject to variation in the exchange rate between Australia and USA. So far as

monetary policy is concerned, USA and Australia both has provided monetary policy stimulus as a

strategy of economy growth. Economic slowdown of Australia is likely to be recovered within a next few

years moving it again to the path of economic expansion.

You're viewing a preview

Unlock full access by subscribing today!

9ECONOMIC ASSIGNMENT

List of References

Data.worldbank.org. (2018). Official exchange rate (LCU per US$, period average) | Data. [online]

Available at: <https://data.worldbank.org/indicator/PA.NUS.FCRF?locations=AU> [Accessed 19 May

2018].

Reserve Bank of Australia. (2018). Cash Rate | RBA. [online] Available at:

<https://www.rba.gov.au/statistics/cash-rate/ > [Accessed 19 May 2018].

Fred.stlouisfed.org. 2018. Effective Federal Funds Rate. [online] Available at:

<https://fred.stlouisfed.org/series/FEDFUNDS> [Accessed 21 May 2018].

Department of Foreign Affairs and Trade. 2018. Trade. [online] Available at: <http://dfat.gov.au/about-

australia/australia-world/Pages/trade.aspx> [Accessed 23 May 2018].

Oecd.org. 2018. Australia - Economic Forecast Summary (November 2017) - OECD. [online] Available at:

<http://www.oecd.org/eco/outlook/australia-economic-forecast-summary.htm> [Accessed 23 May 2018].

Reserve Bank of Australia. 2018. Economic Outlook | Statement On Monetary Policy – February 2018 |

RBA. [online] Available at: <https://www.rba.gov.au/publications/smp/2018/feb/economic-outlook.html>

[Accessed 23 May 2018].

Fontana, G. and Setterfield, M. eds., 2016. Macroeconomic Theory and Macroeconomic Pedagogy.

Springer.

Terra, C., 2015. Principles of International Finance and Open Economy Macroeconomics: Theories,

Applications, and Policies. Academic Press.

Belongia, M.T. and Ireland, P.N., 2016. A Classical View of the Business Cycle (No. 921). Boston College

Department of Economics.

Kent, C., 2014. The Business Cycle in Australia. Address to the Australian Business Economists,

Sydney, 13.

Pagan, A. and Wilcox, D., 2015. External Review–Reserve Bank of Australia Economic Group Forecasts

and Analysis. report to the Reserve Bank of Australia.

Halligan, J., 2017. Reform design and performance in Australia and New Zealand. In Transcending New

Public Management (pp. 55-76). Routledge.

Hartwell, R.M., 2017. The industrial revolution and economic growth (Vol. 4). Taylor & Francis.

Thorpe, M. and Leitão, N.C., 2014. Economic growth in Australia: Globalisation, trade and foreign direct

investment. Global Business and Economics Review, 16(1), pp.75-86.

Argy, V.E. and Nevile, J. eds., 2016. Inflation and Unemployment: Theory, Experience and Policy Making.

Routledge.

Blanchard, O., Cerutti, E. and Summers, L., 2015. Inflation and activity–Two explorations and their

monetary policy implications (No. w21726). National Bureau of Economic Research.

Svensson, L.E., 2015. The possible unemployment cost of average inflation below a credible

target. American Economic Journal: Macroeconomics, 7(1), pp.258-96.

Gilpin, R., 2016. The political economy of international relations. Princeton University Press.

Fischer, S., 2016. Monetary policy, financial stability, and the zero lower bound. American Economic

Review, 106(5), pp.39-42.

Guttmann, R., 2016. How Credit-money Shapes the Economy: The United States in a Global System:

The United States in a Global System. Routledge.

List of References

Data.worldbank.org. (2018). Official exchange rate (LCU per US$, period average) | Data. [online]

Available at: <https://data.worldbank.org/indicator/PA.NUS.FCRF?locations=AU> [Accessed 19 May

2018].

Reserve Bank of Australia. (2018). Cash Rate | RBA. [online] Available at:

<https://www.rba.gov.au/statistics/cash-rate/ > [Accessed 19 May 2018].

Fred.stlouisfed.org. 2018. Effective Federal Funds Rate. [online] Available at:

<https://fred.stlouisfed.org/series/FEDFUNDS> [Accessed 21 May 2018].

Department of Foreign Affairs and Trade. 2018. Trade. [online] Available at: <http://dfat.gov.au/about-

australia/australia-world/Pages/trade.aspx> [Accessed 23 May 2018].

Oecd.org. 2018. Australia - Economic Forecast Summary (November 2017) - OECD. [online] Available at:

<http://www.oecd.org/eco/outlook/australia-economic-forecast-summary.htm> [Accessed 23 May 2018].

Reserve Bank of Australia. 2018. Economic Outlook | Statement On Monetary Policy – February 2018 |

RBA. [online] Available at: <https://www.rba.gov.au/publications/smp/2018/feb/economic-outlook.html>

[Accessed 23 May 2018].

Fontana, G. and Setterfield, M. eds., 2016. Macroeconomic Theory and Macroeconomic Pedagogy.

Springer.

Terra, C., 2015. Principles of International Finance and Open Economy Macroeconomics: Theories,

Applications, and Policies. Academic Press.

Belongia, M.T. and Ireland, P.N., 2016. A Classical View of the Business Cycle (No. 921). Boston College

Department of Economics.

Kent, C., 2014. The Business Cycle in Australia. Address to the Australian Business Economists,

Sydney, 13.

Pagan, A. and Wilcox, D., 2015. External Review–Reserve Bank of Australia Economic Group Forecasts

and Analysis. report to the Reserve Bank of Australia.

Halligan, J., 2017. Reform design and performance in Australia and New Zealand. In Transcending New

Public Management (pp. 55-76). Routledge.

Hartwell, R.M., 2017. The industrial revolution and economic growth (Vol. 4). Taylor & Francis.

Thorpe, M. and Leitão, N.C., 2014. Economic growth in Australia: Globalisation, trade and foreign direct

investment. Global Business and Economics Review, 16(1), pp.75-86.

Argy, V.E. and Nevile, J. eds., 2016. Inflation and Unemployment: Theory, Experience and Policy Making.

Routledge.

Blanchard, O., Cerutti, E. and Summers, L., 2015. Inflation and activity–Two explorations and their

monetary policy implications (No. w21726). National Bureau of Economic Research.

Svensson, L.E., 2015. The possible unemployment cost of average inflation below a credible

target. American Economic Journal: Macroeconomics, 7(1), pp.258-96.

Gilpin, R., 2016. The political economy of international relations. Princeton University Press.

Fischer, S., 2016. Monetary policy, financial stability, and the zero lower bound. American Economic

Review, 106(5), pp.39-42.

Guttmann, R., 2016. How Credit-money Shapes the Economy: The United States in a Global System:

The United States in a Global System. Routledge.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10ECONOMIC ASSIGNMENT

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.